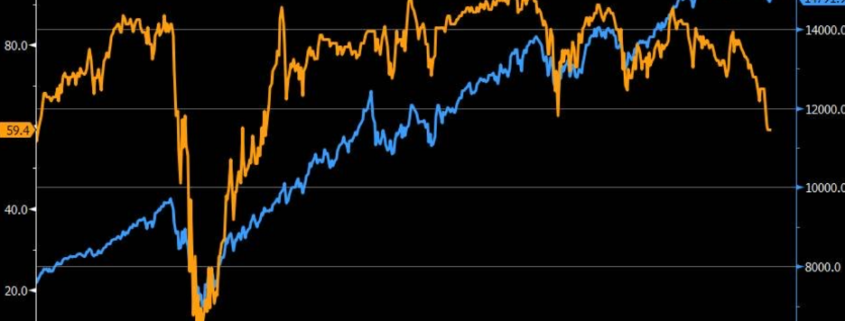

The “Buy the Dip” strategy in tech stocks hasn’t failed — it will just take longer than it used to.

Much of this Nasdaq rally has been represented by the resiliency of large cap tech stocks — every mini dip was bought with a vengeance.

This go-to playbook drove tech shares higher after the March 2020 meltdown.

These past 30 days have really tested that thesis and signals that we, as market participants, have arrived at a crossroads because if the dip isn’t bought soon, we could either fall off a ledge and barrel into a harrowing correction or we could initiate a sideways correction and trade in a fixed range.

It’s hard to ignore the near-term weakness in many of the household names like Apple (AAPL), Amazon (AMZN), and Facebook (FB).

The upper echelon of tech leadership is signaling imminent decelerating growth and tightening financial conditions.

I do believe much of it is in the price, yet it’s cognizant to know there could be meaningful spillover from the Evergrande debt implosion in China into other asset classes.

External events are shaping the narrative around the Nasdaq dip buyers.

It also doesn’t help that a Facebook whistleblower came forward to tell the press about its malpractices and less than ideal tendencies to put profit over safety, but everyone already knew that about Facebook.

What I am surprised about is that investors usually look through the bad Facebook press and prioritize the metrics which hasn’t been happening the past month.

Facebook shares are still waiting to be bought after the dip.

The lack of Facebook shoppers on the pullback is definitely one area of concern because the U.S. government still has done very little to stop Facebook in its stubborn practices.

The U.S. government will not crack down through legislation on social media companies in the short term.

Much of the negative Nasdaq price action in the short term can be attributed to the worries about China taking a machete to its susceptible tech sector and crushing it even more.

Many don’t think the cudgeling is over.

In this scenario, a flight to safety could be in the cards, which would suppress interest rates offering an olive branch for the dip-buyers.

Ultimately, I do believe it’s a matter of time before we get some recovery price action in the leadership tech stocks; but yes, it could take 1-3 weeks.

Much of this second half of the year was consolidating tech shares that overshot themselves last year.

That’s why tech firms like Tesla (TSLA) had almost a zero percent chance of repeating last year’s performance.

Take ad tech stock Roku (ROKU) for instance, shares are down 23% YTD and that doesn’t mean it’s a bad stock.

Hardly so.

When one considers that Roku shares ended 2020 up 300%, then giving back 23% or 50% in 2021 is worth the annoyances.

These stocks can’t go up in a straight line even if they almost feel like they can sometimes.

This all sets up for a brilliant 2022, as many of these high-quality names will finally have gotten through the consolidation phase and will be buttered up to initiate their next leg up in early 2022.

In the broad scheme of things, tech won the pandemic over any other sector, and 2021 is turning into a rest year.

Sometimes one needs to go backwards one step to take the next three forward.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/10/techoct4.png508936Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-10-04 15:02:472021-10-08 19:54:05It Will Just Take Longer

One of the most underappreciated names in the biotechnology sector might just be the biggest winner in a winner-take-most market today: Invitae (NVTA).

Despite being at the receiving end of a seemingly endless flogging since the year started, Invitae remains an attractive stock for the likes of Cathie Woods.

In fact, this San Francisco-based company is one of the Top 20 holdings of ARK Innovation (ARKK) and ARK Genomic Revolution (ARKG).

Described by Woods as "probably one of the most important companies in the genomic revolution," Invitae is the sixth-largest holding of the ARK Investment portfolio with more than $1 billion worth of exposure.

Aside from ARK, Invitae also recently attracted the attention of Japanese tech conglomerate SoftBank (SFTBY), which came in the form of $1.2 billion worth of convertible bond investment.

First, it’s essential to understand that biotech companies opt to target particular niches where they aim to maintain high prices and maximize profitability for as long as possible.

That way, they can maintain and continue to boost their profits.

This results in highly prohibitive costs in the healthcare innovation section, which in turn cause rationing of cases because only a select group of patients can actually afford the exorbitant fees for the innovative drug or therapy.

While rationing care and maximizing profits are obviously great for investors, this makes the innovations inaccessible to people who could not shell out the cash to take the tests or treatments.

This is where Invitae comes in.

Basically, Invitae is taking a completely different approach compared to its peers in the biotechnology world.

According to the company, its mission is "to bring comprehensive genetic information into mainstream medicine to improve healthcare for billions of people."

How will Invitae achieve this?

Instead of choosing a single genetic variant to test, which costs over $1,000 each, the company is developing a testing platform that can identify thousands of genetic variants.

The clincher? This will only cost less than $250 for the entire test panel.

This nonconforming approach to biotechnological innovations is what has primarily led to Invitae’s under-appreciation.

However, Invitae’s mission holds incredible potential.

What it means in medical terms is that the company can help about 1 in 6 people suffering from a medical condition with an inherent genetic factor.

What it means in financial terms is that the company holds the possibility of generating several hundred dollars per year from over 2 billion people—a jaw-dropping market opportunity worth $4 trillion.

One of Invitae’s key ideas is to grant people access to their genetic information and then interpret it for them.

To me, this indicates the company’s goal of doing for genetics what Amazon (AMZN) has done for book buyers.

The next question is this: Can Invitae truly accomplish this?

Let’s consider the company’s growth trajectory along with the catalysts ahead.

So far, three catalysts can push the company towards its goals.

First is the steady growth in testing volume. As with most medical procedures, the volume of genetic testing went down during the COVID-19 pandemic. However, this is now rebounding gradually.

In the first quarter of 2021, the billable volume went up by 72% year over year, with roughly 259,000 tests in that quarter alone.

Traditionally, genetic testing is generally driven by orders from doctors and the cooperation of health plans to cover the tests.

Moving forward, we expect pharmaceutical firms to play more significant roles in promoting and even paying for these tests.

Approximately 90% of the pharma pipelines these days are based on genetic conditions.

As these new and innovative genetic treatments gain FDA approval, the pharma companies would have additional vested interest in ensuring eligible patients receive testing. That way, they can drive demand for the therapies they developed.

The second catalyst comprises the oncology sector.

Genetic testing has become the trend, particularly for cancer—an undoubtedly massive and financially lucrative market.

To leverage this growth, Invitae acquired ArcherDX in 2020 in an effort to expand its offerings.

With this purchase, the company can help major cancer centers implement their testing systems while also offering support to healthcare providers who opt not to do their own testing.

The availability of these comprehensive services will serve as critical drivers of income and profitability considering the historically proven high reimbursement rates in the oncology testing segment.

Apart from this, Invitae recently announced its decision to acquire Ciitizen, a consumer health tech firm, for $325 million.

This move will allow Invitae to expand its patient database through the genomic and clinical information gathered from Ciitizen’s platform.

Thus far, Invitae has announced 13 acquisitions over the past 5 years.

The third catalyst is the continuous global growth of Invitae.

Evidently, the mission of reaching 2 billion people requires worldwide expansion—something that the company has been working on.

In fact, roughly 18% of the total billable volume of Invitae in the first quarter came from international transactions, which have the potential to grow faster than their business in the US.

To date, Invitae has been expanding its operations in Japan, Israel, Europe, and Australia.

Meanwhile, Invitae’s incredible potential has attracted other companies as well. Exact Sciences (EXAS) has been linked to the company for a potential merger among the firms interested.

Admittedly, Invitae’s mission to offer affordable and accessible genetic testing to 2 billion people will require many more years before it comes to fruition.

When that day comes, the company will join Apple (APPL), Amazon, and Microsoft (MSFT) as part of an elite group with $1 trillion and over market cap.

The long wait for Invitae to achieve this ambitious goal would be worth it for patient buy-and-hold investors.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-14 16:00:572021-09-16 02:27:21Is This the Biggest Winner in a Winner-Take-Most Market?

People have no idea what the Metaverse is, so I will be the one to fill you in.

What is the Metaverse? Simply put, the Metaverse is the next mega-phase of the internet, a merging of the physical world with XR, AR, and VR that is just beginning to revolutionize.

It is an extensive online world transcending individual tech platforms, where people exist in immersive, shared virtual spaces. Through avatars, people would be able to try on items available in stores or attend concerts with friends, just as they would offline.

On a recent earnings call, Facebook (FB) CEO Mark Zuckerberg detailed the Metaverse: “It's a virtual environment where you can be present with people in digital spaces,” he said. “You can kind of think about this as an embodied internet that you're inside of rather than just looking at. We believe that this is going to be the successor to the mobile internet.”

Does the Metaverse exist anywhere yet? The answer is yes, early versions of it. The closest approximations of it right now include the likes of digital game platforms Roblox (RBLX) and Fortnite.

The internet era was defined by the computer being in the living room and the connection to the internet being occasional.

The shift to mobile computing is defined by moving the computer from the living room to the office and into your pocket and changing access to the internet from occasional to continuous and persistent.

Metaverse is the idea of computing everywhere, ubiquitous, ambient. In a simplified sense, think about the Metaverse as a series of interconnected and persistent simulations.

One could almost describe it as the next internet, web 3.0.

And crypto, or some sort of crypto offspring or cousin of it, will be the coin of this new realm which is why crypto in its form now is so important.

Consider the internet and mobile internet. Over time it disrupted nearly every industry in nearly every geography.

It changed how consumers patronized, business models, products, behaviors. This produces an extraordinary economic opportunity overall.

The same will happen via the Metaverse.

In the future, instead of just doing calls over a phone call, you’ll be able to sit as a hologram on a couch, or I’ll be able to sit as a hologram on your couch, and it’ll actually feel like we’re in the same place even though it is remote.

Sharing space is what humans perceive as closer to something real.

There’s spatial audio in which distance can change the meaning of a sentence.

This has been in the works for years, ever since Zuckerberg bought Oculus in 2014 and Oculus is effectively the gateway to the Metaverse that Zuckerberg wants to spawn.

Other power Silicon Valley elite are also moving forward into the Metaverse for their own objectives. Microsoft (MSFT) CEO Satya Nadella commented at his earnings call, “As the digital and physical worlds converge, we are leading in a new layer of the infrastructure stack, the enterprise Metaverse."

Many Metaverse believers say the economy of the Metaverse will be larger than that of the physical world.

Personally, I believe it will be 100X larger than the physical world’s economies and much more dynamic.

One of the biggest winners of this Metaverse race will be Epic Games —owner of Fortnite —founded by CEO Tim Sweeney.

Epic released "Fortnite" just five years ago. The game now has 350 million registered players, with anywhere from six to 12 million people playing at any given time.

The Metaverse is a great example of a technology that will likely bring huge benefits to people but there will be unintended, unanticipated costs and harms.

Right now, the Metaverse operates with zero regulations, while its previous iteration, the internet, operates with the least number of regulations out of any major industry in 2021.

The bottom line is that every power Silicon Valley has skin in the game such as Facebook, Apple, Amazon, Microsoft, and Netflix after Epic Games, and they will receive another supercharger to accelerating revenue growth.

The revenue growth in the Metaverse for these companies will make what they earn in the physical world look like a pittance.

We are driving to that point in tech development through hell or high water, and like how every company became a tech company to survive, when the Metaverse and an operable iteration of it become good enough for people to transact smoothly, every company will have to become a Metaverse company or die.

This is the future and it’s creeping closer by the day.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/metaverse.png342862Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-10 13:02:182021-09-16 00:31:59Your Guide to the Metaverse

I know many readers gripe about certain tech stocks being too expensive like Google (GOOGL), Facebook (FB), or even Amazon (AMZN), but that’s not the case for all high-quality tech names out there.

There are still deals to be had.

An undervalued tech name in the same industry, albeit more diminutive than the three I just mentioned, is ad revenue platform Snap Inc. (SNAP).

Their story is a good one and their revenue model appears to be maturing at an optimal time while still exhibiting many elements of explosive growth.

To see what I mean — Snap grew both revenue and daily active users at the highest rates they have achieved in the last four years.

Daily active users grew 23% year-over-year to 293 million — expanding revenue by 116% year-over-year to $982 million.

This outperformance reflects the momentum in SNAP's core advertising business and the positive results of their team serving ad partners helping them to generate a return on investment.

SNAP benefited from a favorable operating environment and continued success with both direct response and large brand advertisers — continue to leverage performant ad products to grow an advertiser base globally.

Adjusted EBITDA improved by $213 million compared to last year, marking the third adjusted EBITDA profitable quarter in the last 12 months as SNAP continues to demonstrate the leverage in their business as they scale.

They are also fully absorbed in making progress against revenue and Average Revenue Per User (ARPU) opportunities, which I believe will be driven by three key priorities.

First, driving ROI through measurement, ranking, and optimization.

Second, investing in aggressive sales and marketing functions by continuing to train, hire, and build for scale.

And third, building innovative ad experiences around video and augmented reality, with a focus on shopping and commerce.

The commitment to these three priorities, along with a unique reach and large, engaged community, allows SNAP to drive performance at scale for businesses around the world.

They have proven through results in North America that with a robust team, surrounding resources, and a local focus, they can accelerate revenue.

They are now taking that model and replicating it in several markets that they have identified as having a large digital advertising market and significant levels of existing Snapchat adoption.

It’s true to say they still have a lot of room to grow in some of the world's most established ad markets outside of North America, especially in Europe.

For example, in the UK, France, and the Netherlands, SNAP reaches over 90% of 13- to 24-year-olds — 75% of 13- to 34-year-olds.

SNAP continues to invest heavily in video advertising, with the goal of driving results for advertising partners and connecting them to the Snapchat Generation.

For example, SNAP worked with Nielsen to help U.S. advertisers understand how to more efficiently reach their target audiences via Snap Ads.

The Total Ad Ratings study analyzed how over 30 cross-platform advertising campaigns reached people on both Snapchat and television.

The analysis showed that Snapchat campaigns contributed an average of 16% incremental reach to advertisers' target audiences, and over 70% of the Gen Z audience that was reached by Snapchat was not reached by TV-only campaigns.

This is especially important as people are increasingly cutting the cord, and mobile content consumption continues to grow, presenting SNAP with a large opportunity to help advertisers reach the Snapchat Generation at scale.

Augmented reality advertising is delivering a return on investment that is measurable and repeatable, which is encouraging the incremental businesses to invest in AR.

For example, Smile Direct Club (SDC) leveraged a Goal-Based Bidding Click optimization for Augmented Reality (AR), which drove 49% of Snap customer leads in Q2 and was the most effective ad unit at driving traffic for their business compared to other social channels.

The success of the Lens ultimately encouraged Smile Direct Club to include AR Lenses as part of their long-term business strategy.

SNAP is betting the ranch on efforts to help advertisers improve conversions and ROI, and recently launched optimization for AR, which allows advertisers to optimize their AR campaigns for down-funnel purchases and fits well into the broader shopping strategy.

SNAPs bread and butter region of North America is hitting on all cylinders with revenue growing 129% year-over-year in Q2, while ARPU grew 116% year-over-year as they continue to benefit from significant investments made in sales teams and sales support in the prior year.

At a 30-thousand-foot level, the global internet services market was valued at over $450 billion in 2020, the year in which the pandemic fundamentally altered how society functions, accelerating a push towards digital offerings.

The internet market is expected to grow at a compound annual growth rate of 5% through 2027 and reach a value of $652 billion. US-based equities presently control close to 30% of the total global market share in the industry.

My takeaway from this is that even though there is GOOGL and FB in this space, the pie is growing so fast that there is easily room for others like SNAP.

One must believe that if SNAP keeps operating anywhere close to its pandemic performance relative to other companies, they are surely guaranteed to be a buy-the-dip company.

In terms of price action, that’s exactly what we have witnessed as the price has zig-zagged up by 300% — the stock price goes two levels up and retraces back one — rinse and repeat.

Just view the big down days as optimal entry points into a burgeoning social media platform and deploy capital.

In the short term, on the monetization side, I have to note that the fiscal comparisons will be more challenging in the second half as SNAP begins to lap the acceleration in top-line growth that they experienced in the prior year.

Once that sell-off gets baked into the equation via a 3-5% sell-off, readers should jump back into SNAP.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-30 12:02:192021-09-05 17:12:54A Great Alternative in the Ad Tech Space

Below please find subscribers’ Q&A for the August 25 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from The Atlantis Casino Hotel in Reno, NV.

Q: How does a 2X ProShares Ultra Technology ETF (ROM) February 2022 vertical bull call spread on the ROM look? Would you do $110-$115 or $115-$120?

A: I would do nothing here at $112.50 because we’ve just gone up 10 points in a week. I’d wait for some kind of pullback, even just $5 or $10 points, and then I would do the $110-$115. I’m leaning towards more conservative LEAPS these days—bets that the market goes sideways to up small rather than going ballistic, which it has done for the last 18 months. Think at-the-money strikes, not deep out-of-the-money on your LEAPS from here on for the rest of this economic cycle. The potential profits are still enormous. The only problem with (ROM) is that the longest maturities on the options are only six months.

Q: How do you recommend entering your long-term portfolio?

A: I would use the one-third rule: you put on ⅓ now, ⅓ higher or lower later on, and ⅓ higher or lower again. That way you get a good average price. Long term, everything goes up until we hit the next recession, which is probably several years off.

Q: I keep reading that the Delta variant is a market risk, but I don’t think that investors will look through this. Is Delta already priced into the shares?

A: Yes, what is not priced into the shares is the end of Delta, the end of the pandemic—and that will lead to my “everything” rally that I’ve been talking about for a month now. And we have already seen the beginning of that, especially with the price action this week. So yes, Delta in: dead market; Delta out: roaring market.

Q: Do you think there will eventually be a rotation into emerging markets (EEM), or has the virus battered these markets too much to even consider it?

A: Sometime in our future—not yet—the emerging markets will be our core holding. And the trigger for that will be the collapse of the dollar, which is hitting an interim high right now. When the greenback rolls over and dies, you can expect emerging markets, especially China, to take off like a rocket. That’s going to be our next big trade. I don't know if it will be this year or next year but it’s coming, so start doing your emerging market research now, and keep reading my newsletter.

Q: Is the coming tax hike a problem for the stock market?

A: No, I don’t think so. First off, I don’t think they’re going to do a tax bill this year; they don’t want anything to interfere with the 2022 election, so it may be next year’s business. Also, any new taxes are going to be overwhelmingly focused on billionaires, carried interest, offshoring, and large corporations. The middle class, people who make less than $400,000 a year, will not see any tax hike at all, possibly even getting some tax cuts via restored SALT deductions. So, I don't really see it affecting the stock market at all.

Q: What do you think about Chinese stocks (FXI)?

A: Long-term they’re okay, short term possibly more downside. Interestingly, the bigger risk may not be China itself and how the government is beating up its own tech companies, but the SEC. It has indicated they don’t really like these offshore vehicles that have been listed on the New York Stock Exchange, and they may move to ban them. I’m not rushing into China right now, only because there are just so many better opportunities in the US stock market for the time being. I may go back in the future—it’s a case where I’d rather buy them on the way up than trying to catch a falling knife on China right now.

Q: Do you expect any market impact from the Jackson Hole meeting?

A: Yes, whatever J Powell says, even if he says nothing, will have a market impact. And it will have a bigger impact on the bond market than it will on the stock market, which is down a full point this morning. So yes, but not yet. I imagine we’ll hear something very soon.

Q: September and October tend to be volatile; do you see us having a 5% or 10% pullback in those months?

A: I don’t see any more than 5%, with the hyper liquidity that we have in the system now. There just aren’t any events out there that could trigger a pullback of 10%—no geopolitical events, and the economy will be getting stronger, not worse. So yes, an “everything rally” doesn’t give you many long side entry points, so I just don’t see 10% happening.

Q: What about a Walt Disney (DIS) January 2022 $180-$220 LEAPS?

A: I would do the $180-$200. I think you can afford to be tighter on your spread there, take some more risk because I think it’s just going to go nuts to the upside once we get a drop in COVID cases. By the way, Disney parks are only operating at 70% capacity, so if you go back up to 100% that's a near 50% increase in profits for the company. And it’s not just Disney, but Netflix (NFLX), Amazon (AMZN), and everybody else that’s about to have the greatest number of blockbuster movies released of all time. They’re holding back their big-ticket movies for the end of the pandemic when people can go back into theaters. We’ll start seeing those movies come out in the last quarter of this year, and I’m particularly looking forward to the next James Bond movie, a man after my own heart.

Q: Are EV car charging companies like ChargePoint Holdings (CHPT) going to do as well as the car companies?

A: No. They’re low margin business, so it’s not a business model for me. I like high-profit margins, huge barriers to entry, and very wide moats, which pretty much characterizes everything I own. The big profits in EVs are going to be in the cars themselves. Charging the cars is a very capital-intensive, highly regulated, and low-margin business.

Q: Would a Fed taper cause a 10% pullback?

A: Absolutely not; in fact, I think a taper would make the market go up because Jay Powell has been talking it into the market all year. And that’s his goal, is to minimize the impact of a taper so when they finally do it, they say ho-hum and “okay you can take that risk out of the market.” That’s the way these things work.

Q: What is your yearend target for United States Treasury Bond Fund (TLT)?

A: $132. Call it bold, but I'm all about bold. I think the first stop will be at $144, then $138, then bombs away!

Q: What will it take for (TLT) to dip below $130?

A: Another year of hot economic growth, which Congress seems hell-bent on delivering us.

Q: What are your ProShares Ultra Short 20+ Year Treasury ETF (TBT) targets?

A: When we were at 1.76% on the 10-year bond, the (TBT) made it all the way back to 22 ½. Next year we go higher, probably to $25, maybe even $30.

Q: What’s your 10-year view on the (TBT)?

A: $200. That’s when you get interest rates back to 10% in 10 years on the 10-year bond. So yes, that’s a great long-term play.

Q: How long can we hold (TBT)?

A: As long as you want. Ten years would be a good time frame if you want to catch that $17 to $200 move. The (TBT) is an ETF, not an option, therefore it doesn’t expire.

Q: Are you working on an electrification stock list?

A: I am not, because it’s such a fragmented sector. It’s tough to really nail down specific stocks. I think it’s safe to say that the electric power grid is going to change beyond all recognition, but they won’t necessarily be in high margin companies, and I tend to prefer high-profit-margin, large-moat companies which nobody else can get into, like Apple (AAPL) or Google (GOOG).

Q: What about gas pipelines with high yields?

A: They have a high yield for a reason; because they’re very high risk. If you're going to a carbon-free economy, you don’t necessarily want to own pipelines whose main job is moving carbon; it’s another buggy whip-type industry I would avoid. I’ve seen people get wiped out by these things more times than I could count. If you remember Master Limited Partnerships, quite a few of them went bankrupt last year with the oil crash, so I would avoid that area. These tend to be very highly leveraged and poorly managed instruments.

Q: Best play on silver (SLV)?

A: Wheaton Precious Metals (WPM) is the highest leveraged silver play out there, and a great LEAPS candidate. Go out 2 years and triple your money.

Q: Geopolitical oil (USO) risks?

A: No, nobody cares about oil anymore—that’s why we’re giving up on Afghanistan. China is buying 80% of the Persian Gulf oil right now. We don’t really need it at all, so why have our military over there to protect China’s oil supply?

Q: What about Freeport McMoRan (FCX)?

A: I absolutely love it. Any big economic recovery can’t happen without copper, and you have a huge tailwind there from electric cars which need 200 pounds of copper each, as opposed to 20 pounds in conventional cars.

Q: I see AMC Entertainment Holdings (AMC) is up 20% today; should everyone be chasing this stock?

A: No, absolutely not. (AMC) and all the meme stocks aren’t investments, they’re gambling, and there are better ways to gamble.

Q: Should I buy the lumber dip?

A: Yes. I think the slowdown on housing is temporary because it will take 10 years for supply and demand in the housing market to come back into balance because of all the millennials entering the housing market for the first time. So, that would be a yes on lumber and all the other commodities out there that go into housing like copper, steel, and aluminum.

Q: Should I put money into Canadian Junior Gold Miners (GDX)?

A: No, I would rather go out and take a long nap first. These are just so high risk, and they often go bankrupt. The liquidity is terrible, and the dealing spreads are wide. I would stick with the bigger precious metal plays like Newmont Mining (NEM), Barrick Gold (GOLD), and Wheaton Precious Metals (WPM).

Q: Is Boeing (BA) a buy here?

A: Yes, we’re back at the bottom end of the trading range for the stock. It’s just a matter of time before they get things right, and the 737 Max orders are rolling in like crazy now that there’s an airplane shortage.

Q: What do you think about Robinhood (HOOD)?

A: I like it quite a lot; I got flushed out of my long position on Friday with a 10% down move. Of course, 90% of my stop losses end up expiring at their maximum profit points, but I have to do it to keep the volatility of the portfolio down. So yes, I’ll try to buy it again on the next dip. The trouble is it’s kind of a quasi-meme stock in its own right, hence the volatility; so I would say on the next 10% down day, you go into Robinhood, and I probably will too.

Q: How are the wildfires around Tahoe?

A: They’re terrible and there are three of them. I did a hike two days ago there, and out of a parking lot with 100 spaces, I was the only one there. It’s the only time I’d ever seen Tahoe deserted in August. With visibility of 500 yards, it's just terrible. Fortunately, I was able to hike without coughing my guts out—it’s not so thick that you can’t breathe.

Q: What do you think of US Steel (X)?

A: I like it, I think the whole industrial commodity complex rallies like crazy going into the end of the year.

Q: As a new member, where is the best place to start? It’s just kind of like drinking from a fire hose.

A: Wait for the trade alerts; they only happen at sweet spots and you may have to wait a few days or weeks to get one since we only like to enter them at good points. That’s the best place to enter new positions for the first time. In the meantime, keep reading all the research, because when these trade alerts do come out, they’re not surprises because I’m pumping out research on them every day, across multiple fronts. Be patient— we are running a 93% success rate, but only because we take our time on entering good trades. The services that guarantee a trade alert every day lose money hand over fist.

Q: If they do delist Chinese stocks, will US investors be left holding the bag?

A: Yes, and that will be the only reason they don’t delist them, that they don’t want to wipe out all current US investors.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER (whichever applies to you), then select WEBINARS and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-wine-1.png812562Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-27 10:02:412021-08-27 11:03:48August 25 Biweekly Strategy Webinar Q&A

Mad Hedge Technology Letter August 25, 2021 Fiat Lux

Featured Trade:

(THE BEST WAY TO ALPHA YOUR TECH PORTFOLIO) (MU), (PLTR), (AMD), (AMZN), (SQ), (PYPL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-25 15:04:232021-08-25 15:39:28August 25, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.