Mad Hedge Technology Letter

February 3, 2021

Fiat Lux

Featured Trade:

($4,000 A DONE DEAL FOR AMAZON IN 2021)

(AMZN)

Mad Hedge Technology Letter

February 3, 2021

Fiat Lux

Featured Trade:

($4,000 A DONE DEAL FOR AMAZON IN 2021)

(AMZN)

Amazon is highly likely to surge past $4,000 this year.

Like many other tech stocks, last March was a kick in the teeth that served up a quick correction.

But unlike a handful of sectors, investors saw their faith in Amazon rewarded when the stock reversed and roared to $3,500.

After a sharp spiral down off the March lows, as investors saw Amazon as a beneficiary of lockdown measures, the stock had been consolidating within a narrowing range over the past several months.

Traders have solid support levels at $3,100 and any trader should be buying AMZN at anything close to that.

The price action suggests that AMZN has a favorable chance to break up to the upside some point after what was a blowout fourth quarter results of net income of decisively more than the predicted $6.3 billion and revenue approaching $120 billion.

They outdid themselves and reported earnings of $14.09 per share on record revenue of $125.56 billion.

The e-commerce and technology titan went into its important holiday quarter report on a strong note and 2021 will be no different as features if the pandemic persists.

Just a quick rewind to the third quarter, revenue and earnings also easily beat consensus estimates, and Amazon perennially guides up. This is becoming a constant pattern with the stock boding well for the future stock price.

Investors like companies who constantly over-deliver on earnings metrics.

The biggest bombshell of yesterday’s report was clearly that Jeff Bezos, the company’s founder and CEO, would leave from his role in the third quarter of 2021.

I thought it was interesting that after-hour trading was largely indifferent as investors were digesting the founder leaving his creation.

Next on deck is Andy Jassy, who currently leads Amazon Web Services (AWS), and will take over Bezos’ job.

Bezos will stick around in an “executive chairman” role and I envision this as Bezos not really leaving and still handling all the “big vision” stuff.

Inside the company, Jassy is the highest profile candidate and part of the most profitable part of the company giving him major clout.

This is out of the same mold of Microsoft’s CEO Satya Nadella who was also promoted to the top via the cloud division.

Bezos will now have more time to spend on Day 1 Fund which is a non-profit organization that will launch and operate a network of high-quality, full-scholarship Montessori-inspired preschools in underserved communities.

Along with that, he will spend time with the Bezos Earth Fund, Blue Origin, The Washington Post while Jassy handles the daily grind of the operation.

Don’t forget that Bezos is the largest shareholder, but because Amazon has become quite heralded for grooming top-level management, the company won’t miss a beat with Jassy.

Just look at what Jassy did in the fourth quarter.

Amazon Web Service (AWS) grew revenue 28% to $12.74 billion. That year-over-year growth rate held roughly steady compared to the third quarter and is the U.S. market share leader in cloud web hosting.

AWS operating income grew even more strongly, jumping 37% to nearly $3.6 billion.

Awarding the best performing manager at a company is something good companies do.

The pandemic, in itself, was a major catalyst to take revenue growth higher and sales got a boost from the company's annual Prime Day event, which was pushed back to the fourth quarter this year from its usual place in the third quarter due to the global crisis.

This year could be a similar repeat of 2020 with consumers crazy for e-commerce services and Amazon, best of breed service.

This should be a buy on every small dip stock and simply the best company in the world right now whether examining tech or anything else.

Global Market Comments

February 2, 2021

Fiat Lux

Featured Trade:

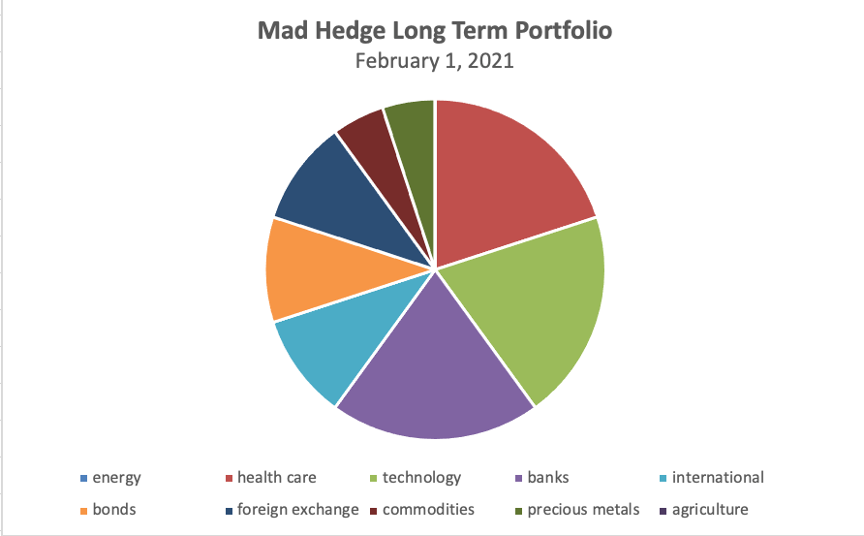

(MY NEWLY UPDATED LONG-TERM PORTFOLIO),

(PFE), (BMY), (AMGN), (CELG), (CRSP), (FB), (PYPL), (GOOGL), (AAPL), (AMZN), (SQ), (JPM), (BAC), (MS), (GS), (BABA), (EEM), (FXA), (FCX), (GLD), (SLV), (TLT)

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on July 21, 2020. In fact, not only did we nail the best sectors to go heavily overweight, we also completely dodged the bullets in the worst-performing ones.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing, these are the investments you can make, and then not touch until you start drawing down your retirement funds at age 72.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted below.

To download the entire new portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go “My Account”, then “Global Trading Dispatch”, then click on the “Long Term Portfolio” button.

Changes

I am cutting back my weighting in biotech from 25% to 20% because Celgene (CELG) was taken over by Bristol Myers (BMY) at a 110% profit compared to our original cost. We also earned a spectacular 145% gain on Crisper Therapeutics (CRSP). I’m keeping it because I believe it has more to run.

My 30% weighting in technology also gets pared back to 20% because virtually all of my names have doubled or more. These have been in a sideways correction for the past six months but are still an important part of any barbell portfolio. So, take out Facebook (FB) and PayPal (PYPL) and keep the rest.

I am increasing my weighting in banks from 10% to 20%. Interest rates are finally starting to rise, setting up a perfect storm in favor of bank earnings. Loan default rates are falling. Banks are overcapitalized, thanks to Dodd-Frank. And because of the trillions in government stimulus loans they are disbursing, they are now the most subsidized sector of the economy. So, add in Morgan Stanley (MS) and Goldman Sachs (GS), which will profit enormously from a continuing bull market in stocks.

Along the same vein, I am committing 10% of my portfolio to a short position in the United States Treasury Bond Fund (TLT) as I think bonds are about to go to hell in a handbasket. I rant on this sector on an almost daily basis, so go read Global Trading Dispatch.

I am keeping my 10% international exposure in Chinese Internet giant Alibaba (BABA) and the iShares MSCI Emerging Market ETF (EEM). The Biden administration will most likely dial back the recent vociferous anti-Chinese stance, setting these names on fire.

I am also keeping my foreign currency exposure unchanged, maintaining a double long in the Australian dollar (FXA). The Aussie has been the best performing currency against the US dollar and that should continue.

Australia will be a leveraged beneficiary of the synchronized global economic recovery, both through strong commodity prices and gold which has already started to rise, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

As for precious metals, I’m baling on my 10% holding in gold (GLD), which delivered a nice 20% gain in 2020. From here, it is having trouble keeping up with other alternative assets, like Bitcoin, and there are better fish to fry.

Yes, in this liquidity-driven global bull market, a 20% return is just not enough to keep my interest. Instead, I add a 5% weighting in the higher beta and more volatile iShares Silver Trust (SLV), which has far wider industrial uses in solar panels and electric vehicles.

As for energy, I will keep my weighting at zero. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free. You are looking at the next buggy whip industry.

My ten-year assumption for the US and the global economy remains the same. I’m looking at 3%-5% a year growth for the next decade.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient, productive, and profitable than the old.

You won’t believe what’s coming your way!

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

January 27, 2021

Fiat Lux

Featured Trade:

(DINOSAURS OF TECH REINVENTING THEMSELVES)

(BB), (AMZN), (BIDU), (GME)

Tech companies change so quickly that sometimes companies have no choice but to reinvent themselves and that is exactly what BlackBerry (BB) has done as their stock has already delivered gains of 190% in 2021.

Historically known as a hardware business, BlackBerry decided to opt out of its legacy operations and elect for a push into enterprise software, internet of things (IoT), and cybersecurity, pivoting away from handsets as that business flagged.

That is where all the serious tech money is these days.

A torrent of positive announcement has rallied investors to this stock with the company announcing an expanded partnership with Baidu (BIDU) that will see it continue working on automated high-definition mapping software that Baidu uses in its autonomous driving technology.

Baidu is a Chinese tech company that is also hoping to reinvent themselves away from their legacy business of internet search.

Data and connectivity are opening new avenues for innovation in the automotive industry, and BlackBerry and auto companies share a common vision to provide automakers and developers with optimal data so that they can deliver new services to consumers.

The tie-up with Baidu caused the stock to shoot higher by 17.3% at $21.15 in premarket trading.

This move broadens the company's use of BlackBerry’s operating system in its "Apollo" autonomous driving open platform.

Under the expanded partnership, Baidu’s high-definition map will be integrated with BlackBerry’s QNX Neutrino real-time operating system.

The integrated system will be mass-produced and available on Guangzhou Automobile Group electric vehicle arm’s upcoming GAC New Energy Aion models.

The BlackBerry QNX software scores high in functional safety, network security, and reliability, while Baidu has achieved long-term development in artificial intelligence and deep learning.

GAC is one of China’s largest automakers. It also manufactures the Hycan 007 cars under a joint venture with EV startup NIO.

This is just an example of how BB is running to the part of the end zone where the ball is going to be thrown unlike other dinosaur tech like IBM.

The company’s stock has recently been included in strong dialogue on online message boards such as Reddit, which like GameStop (GME) has felt a sharp appreciation in price or probably better describes as rocket boosters.

GME is up 100% just today which can only be described as an epic short squeeze.

At a strategic level, the success of BlackBerry’s stock can be attributed in part to the strategic shift to cybersecurity and the Internet of Things.

The shift away from handheld devices is long due, and so what's really happening is the market is putting its stamp of approval on this new shift of BlackBerry away from its old business model and what it’s doing now.

BB holds more patents than any other company in Canada.

BlackBerry shares spiked as much as 20% after settling a patent infringement suit with Facebook.

BlackBerry first targeted Facebook with a lawsuit back in 2018, filing a 117-page complaint accusing the social network of infringing on Blackberry's innovative messaging technology.

The settlement removed any litigious uncertainty offering another clear pathway for the stock to rise.

The biggest strategic overhaul has been its recent partnerships with Amazon (AMZN) Web Services in December to use its cloud services.

They signed an agreement with Amazon for BB to develop a software platform that allows automakers to read vehicle sensor data, improving cloud-connected vehicles' performance.

Blackberry announced it sold 90 patents to China's largest phone manufacturer, Huawei.

Automakers can use this information to create responsive in-vehicle services that enhance driver and passenger experiences.

BlackBerry IVY addresses a critical data access, collection, and management problem in the automotive industry.

Cars and trucks use many different parts, with each vehicle model comprising a unique set of proprietary hardware and software components.

These components, which include an increasing variety of vehicle sensors, produce data in unique and specialized formats.

The highly specific skills required to interact with this data, as well as the challenges of accessing it from within contained vehicle subsystems, limit developers’ abilities to innovate quickly and bring new solutions to market.

BlackBerry IVY will solve these challenges by applying machine learning to that data to generate predictive insights and inferences, making it possible for automakers to offer in-vehicle experiences that are highly personalized and able to take action based on those insights.

Although many legacy tech companies get caught in the weeds, never to grow again. BB has sorted out its vision and is well on its way to delivering shareholder value back to the end investor.

Even though I would say the short-term price action in BB is at this point euphoric, it would serve any tech investor well to dip their toe into this stock long term when there is a pullback.

Global Market Comments

January 22, 2021

Fiat Lux

Featured Trade:

(JANUARY 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (IWM), (SPY), (ROM), (BRK/A), (AMZN), NVDA), (MU), (AMD), (UNG), (USO), (SLV), (GLD), ($SOX), CHIX), (BIDU), (BABA), (NFLX), (CHIX), ($INDU), (SPY), (TLT)

Below please find subscribers’ Q&A for the January 20 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, NV.

Q: What will a significant rise in long term bond yields (TLT) do to PE ratios in general, and high tech specifically?

A: Well, the key question here is: what is “significant”. Is “significant” a move in a 10-year from 120 to 150, which may be only months off? I don’t think that will have any impact whatsoever on the stock market. I think to really give us a good scare on interest rates, you need to get the 10-year up to 3.0%, and that might be two years off. We’re also going to be testing some new ground here: how high can bond interest rates go while the Fed keeps overnight rates at 25 basis points? They can go up more, but not enough to hurt the stock market. So, I think we essentially have a free run on stocks for two more years.

Q: What about the Shiller price earnings ratio?

A: Currently, it’s 34.5X and you want to completely ignore anything from Shiller on stock prices. He’s been bearish on stocks for 6 years now and ignoring him is the best thing you can do for your portfolio. If you had listed to him, you would have missed the last 15,000 Dow ($INDU) points. Someday, he’ll be right, but it may be when the market goes from 50,000 to 40,000, so again, I haven't found the Shiller price earnings ratio to be useful. It’s one of those academic things that looks great on paper but is terrible in practice.

Q: Do you see any opportunity in China financials with the change of administration, like the (CHIX)?

A: I always avoid financials in China because everyone knows they have massive, defaulted loans on their books that the government refuses to force them to recognize like we do here. So, it’s one of those things where they look good on paper, but you dig deeper and find out why they’re really so cheap. Better to go with the big online companies like Baidu (BIDU) and Alibaba (BABA).

Q: Is it too late to enter copper?

A: No, the high in the last cycle for Freeport McMoRan (FCX) was $50 dollars and I think we’re only in the mid $ ’20s now, so you could get another double. Remember, these commodity stocks have discounted recovery that hasn’t even started yet. Once you do get an actual recovery, you could get another enormous move and that's what could take the Dow to 120,000.

Q: Do you see the FANGs coming back to life with the earnings results?

A: I think it'll take more than just Netflix to do that. By the way, Netflix (NFLX) is starting to look like the Tesla of the media industry, so I’d get into Netflix on the next dip. You could get a surprise, out-of-nowhere double out of that anytime. But yes, FANGs will come to life. They've been in a correction for five months now, and we’ll see—it may be the end of the pandemic that causes these stocks to really take off. So that's why I'm running the barbell portfolio and buying the FANGs on weakness.

Q: Are you recommending LEAPS on gold (GLD) and silver (SLV)?

A: Absolutely yes, go out two years with your maturity, you might buy 120% out of the money. That's where you get your leverage on the LEAPS. Something like a (GLD) January 2023 $210-$220 in-the-money vertical bull call spread and generate a 500% profit by expiration.

Q: Do you foresee a cool off for semiconductors ($SOX) even though there's been recent news of shortages?

A: No, not really. There are so many people trying to get into these it’s incredible. And again, we may get a time correction where we sideline at the top and then break out again to the upside. This is classic in liquidity-driven markets, which is what we have in spades right now. Thanks to 5G, the number of chips in your everyday devices is about to increase tenfold, and it takes at least two years to build a new chip factory. So, keep buying (NVDA), (MU), and (AMD) on dips.

Q: Where are the best LEAPS prospects (Long Term Equity Participation Securities)?

A: That would have to be in technology—that's where the earnings growth is. If you go 20% out of the money on just about any big tech LEAPs two years out, to 2023 those will be worth 500% more at expiration.

Q: What about SPACs (Special Purpose Acquisition Company) now, as we’re getting up to five new SPACs a day?

A: My belief is that a SPAC is a vehicle that allows a manager to take out a 20% a year management fee instead of only 1%. And it's another aspect of the current mania we’re in that a lot of these SPACs are doubling on the first day—especially the electric vehicle-related SPACs. Also, a lot of these SPACs will never invest in anything, but just take the money and give it back to you in two years with no return when they can't find any good investments…. If you’re lucky. There's not a lot of bargains to be found out there by anyone, including SPAC managers.

Q: Does natural gas (UNG) fall into the same “avoid energy” narrative as oil?

A: Absolutely, yes. The only benefit of natural gas is it produces 50% less carbon dioxide than oil. However, you can't get gas without also getting oil (USO), as the two come out of the pipe at the same time; so I would avoid natural gas also. Gas and oil are also about to lose a large chunk, if not all, of their tax incentives, like the oil depletion allowance, which has basically allowed the entire oil industry to operate tax-free since the 1930s.

Q: What about hydrogen cars?

A: I don't really believe in the technology myself, and when you burn hydrogen, that also produces CO2. The problem with hydrogen is that it’s not a scalable technology. It’s like gasoline—you have to build stations all over the US to fuel the cars. Of course, it produces far less carbon than gas or natural gas, but it is hard to compete against electric power, which is scalable and there's already a massive electric grid in place.

Q: If you inherited $4 million today, would you cost average into (QQQ), (IWM), or (SPY)?

A: I would go into the ProShares Ultra Technology ETF (ROM), which is double the (QQQ); and if you really want to be conservative, put half your money into (QQQ) or (ROM), and then half into Berkshire Hathaway (BRK/A), which is basically a call option on the industrial and recovery economy. I know plenty of smart people who are doing exactly that.

Q: Is it weird to see oil, as well as green energy stocks, moving up?

A: No, that's actually how it works. The higher oil and gas prices go, the more economical it is to switch over to green energy. So, they always move in sync with each other.

Q: I heard rumors that Amazon (AMZN) is likely to raise Prime’s annual fee by $10-20 a year in 2021. Will that be a catalyst for the stock to go higher?

A: Yes. For every $10 dollars per person in Prime revenue, Amazon makes $2 billion more in net profit. I would say that's a very strong argument for the stock going up and maybe what breaks it out of its current 6-month range. By the way, Amazon is wildly undervalued, and my long-term target is $5,000.

Q: Do you think that the spike in Apple (AAPL) MacBook purchases means that computers will overtake iPhones as the revenue driver for Apple in 2021, or is the phone business too big?

A: The phone business is too big, and 5G will cause iPhone sales to grow exponentially. Remember, the iPhones themselves are getting better. I just bought the 12G Pro, and the performance over the old phone is incredible. So yeah, iPhones get bigger and better, while laptops only grow to the extent that people need an actual laptop to work on in a fixed office. Is that a supercomputer in your pocket, or are you just glad to see me?

Q: Share buybacks dried up because of revenue headwinds; do you think they will come back in a massive wave, giving more life to equities?

A: Absolutely, yes. Banks, which have been banned from buybacks for the past year, are about to go back into the share buyback business. Netflix has also announced that they will go buy their shares for the first time in 10 years, and of course, Apple is still plodding away with about $100 or $200 million a year in share buybacks, so all of that accelerates. The only ones you won't see doing buybacks are airlines and Boeing (BA) because they have such a mountain of debt to crawl out from before they can get back into aggressive buybacks.

Q: Interest rates are at historic lows; the smartest thing we can do is act big.

A: That’s absolutely right; you want to go big now when we’re all suffering so we can go small later and run a balanced budget or even pay down national debt if the economy grows strong enough. The last person to do that was Bill Clinton, who paid down national debt in small quantities in ‘98 and ‘99.

Q: What do you think about General Motors (GM)?

A: They really seem to be making a big effort to get into electric cars. They said they're going to bring out 25 new electric car models by 2025, and the problem is that GM is your classic “hour late, dollar short” company; always behind the curve because they have this immense bureaucracy which operates as if it is stuck in a barrel of molasses. I don’t see them ever competing against Tesla (TSLA) because the whole business model there seems like it’s stuck in molasses, whereas Tesla is moving forward with new technology at warp speed. I think when Tesla brings out the solid-state battery, which could be in two years, they essentially wipe out the entire global car industry, and everybody will have to either make Tesla cars under license from Tesla—which they said they are happy to do—or go out of business. Having said that, you could get another double in (GM) before everyone figures out what the game is.

Q: Will you update the long-term portfolio?

A: Yes, I promise to update it next week, as long as you promise me that there won’t be another insurrection next week. It’s strictly a time issue. After last year being the most exhausting year in history, this year is proving to be even more exhausting!

Q: Do you see a February pullback?

A: Either a small pullback or a time correction sideways.

Q: Do you think the Zoom (ZM) selloff will continue, or is it done now that the pandemic is hopefully ending?

A: It’s natural for a tech stock to give up one third after a 10X move. It might sell off a little bit more, but like it or not, Zoom is here to stay; it’s now a permanent part of our lives. They’re trying to grow their business as fast as they can, they’re hiring like crazy, so they’re going to be a big factor in our lives. The stock will eventually reflect that.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 13, 2021

Fiat LuxFeatured Trade:

(MY RADICAL VIEW OF THE MARKETS),

(INDU), (SPY), (AAPL), (FB), (AMZN), (ROKU)

What if the consensus is wrong?

What if instead of being in the 12th year of a bull market, we are actually in the first year, which has another decade to run? It’s not only possible but also probable. Personally, I give it a greater than 90% chance.

There is a possibility that the bear market that everyone and his brother have been long predicting and that the talking heads assure you is imminent has already happened.

It took place during the first quarter of 2020 when the Dow Average plunged a heart-rending 40%. How could this be a bear market when historical ursine moves down lasted anywhere from six months to two years, not six weeks?

Blame it all on hyperactive algorithms, risk parity traders, Robin Hood traders, and hedge funds, which adjust portfolios with the speed of light. If this WAS a bear market and you blinked, then you missed it.

It certainly felt like a bear market at the time. Lead stocks like Amazon (AMZN), Apple (AAPL), Facebook (FB), and Alphabet (GOOGL) were all down close to 40% during the period. High beta stocks like Roku (ROKU), one of our favorites, were down 60% at the low. It has since risen by 600%.

It got so bad that I had to disconnect my phone at night to prevent nervous fellows from calling me all night.

In my experience, if it walks like a duck and quacks like a duck, then it is a bear. If true, then the implications for all of us are enormous.

If I’m right, then my 2030 target of a Dow Average of $120,000, an increase of 300% no longer looks like the mutterings of a mad man, nor the pie in the sky dreams of a permabull. It is in fact eminently doable, calling for a 15% annual gain until then, with dividends.

What have we done over the last 11 years? How about 13.08% annually with dividends reinvested for a total 313% gain.

For a start, from here on, we should be looking to buy every dip, not sell every rally. Institutional cash levels are way too high. Markets have gone up so fast, up 12,000 Dow points in eight months, that many slower investors were left on the sideline. Most waited for dips that never came.

It all brings into play my Golden Age scenario of the 2020s, a repeat of the Roaring Twenties, which I have been predicting for the last ten years. This calls for a generation of 85 million big spending Millennials to supercharge the economy. Anything you touch will turn to gold, as they did during the 1980s, the 1950s, and well, the 1920s. Making money will be like falling off a log.

If this is the case, you should be loading the boat with technology stocks, domestic recovery stocks, and biotech stocks at every opportunity. Although stocks look expensive now, they are still only at one fifth peak valuations of the 2000 market summit.

Let me put out another radical, out of consensus idea. It has become fashionable to take the current red-hot stock market as proof of a Trump handling of the economy.

I believe the opposite is true. I think stocks have traded at a 10%-20% discount to their true earnings potential for the past four years. Anti-business policies were announced and then reversed the next day. Companies were urged to reopen money-losing factories in the US. Capital investment plans were shelved.

Yes, the cut in corporate earnings was nice, but that only had value to the 50% of S&P 500 companies that actually pay taxes.

Now that Trump is gone, that burden and that discount are lifted from the shoulders of corporate America.

It makes economic sense. We will see an immediate end to our trade war with the world, which is currently costing us 1% a year in GDP growth. Take Trump out of the picture and our economy gets that 1% back immediately, leaping from 2% to 3% growth a year and more.

The last Roaring Twenties started with doubts and hand wringing similar to what we are seeing now. Everyone then was expecting a depression in the aftermath of WWI because big-time military spending was ending.

After a year of hesitation, massive reconstruction spending in Europe and a shift from military to consumer spending won out, leading to the beginning of the Jazz Age, flappers, and bathtub gin.

I know all this because my grandmother regaled me with these tales, an inveterate flapper herself, which she often demonstrated. This is the same grandmother who bought the land under the Bellagio Hotel in Las Vegas for $500 in 1945 and then sold it for $10 million in 1978.

And you wonder where I got my seed capital.

It all sets up another “Roaring Twenties” very nicely. You will all look like geniuses.

I just thought you’d like to know.