Mad Hedge Technology Letter

July 26, 2023

Fiat Lux

Featured Trade:

(GOOD SIGNS FOR TECH)

(GOOGL), (APPL), (CHATGPT)

Mad Hedge Technology Letter

July 26, 2023

Fiat Lux

Featured Trade:

(GOOD SIGNS FOR TECH)

(GOOGL), (APPL), (CHATGPT)

It’s incredible that a 7% increase year-over-year in revenue means an extra $5 billion in just one quarter.

That’s what happens when a company is a behemoth, and the company I am talking about is Alphabet, or better known as Google (GOOGL).

Some of these tech companies are so large that growth rates don’t mean much unless they are negative.

Whether it is 3% or 6%, the nominal amount of revenue increase is gargantuan.

The law of large numbers is certainly valid in these situations so don’t expect multi-trillion dollar tech firms to grow 30% or 40% like they used to.

As I correctly predicted, Google and similar companies are doing just fine this earnings season, and I believe they could have gotten away with even 3% growth.

The 7% growth translated into a 7% bump in GOOGL shares this morning showing that investors care more about the additional $5 billion in revenue rather than the low growth rate.

For the fourth straight quarter, Google reported growth in the single digits as it reckons with a pullback in digital ad spending that reflects concerns about the economy.

Across the industry, investors will be looking for updates on cost-cutting measures implemented earlier in the year and the impact of artificial intelligence investments on profitability.

Revenue in Google’s cloud unit, which includes infrastructure and productivity apps, increased 28%.

Google’s ad revenue rose 3.3% to $58.14 billion, up from $56.29 billion last year. YouTube ads came in above analyst expectations at $7.67 billion marginally up from $7.34 billion the year before.

Google’s “search and other” revenue rose to $42.63 billion, up slightly from last year.

The only “growth” part of the business has been the cloud and even that is starting to taper off.

Up until recently, they were expanding that business around 35% year-over-year and now they are down to 28%. In a few years, they will be down to the teens.

Google is slowing down but that doesn’t mean they aren’t profitable.

The cash cow of the ad business keeps churning out the revenue and Microsoft hasn’t turned out to be the threat to Google search that investors first thought when ChatGPT came out.

Investors reacting to 7% growth by pouring money into the stock are a good omen for the rest of big tech.

It means that these other companies, like Apple, only need to marginally outperform to get rocket fuel in their stock and I will take that for all its worth.

Any worst-case scenario will not come to fruition.

Any tech analyst who is bearish this year can be described in one way – unemployed.

The fake narrative of an “earnings recession” and higher interest rates hasn’t even put a dent in the strength of tech.

It’s like throwing pebbles at the Titanic.

Even scarier for the bears, this was supposed to finally be the entry point when a dip could present itself so the bears could get into tech to try and salvage a terrible year.

Well, now, they need to chase another 7% because Google’s ship has sailed and I have conviction that Apple will jump over the low bar for its shares to have a similar effect.

As for GOOGL, I am a buyer on the next mini-dip.

Mad Hedge Technology Letter

July 21, 2023

Fiat Lux

Featured Trade:

(WHAT TO DO ABOUT NETFLIX SHARES?)

(NFLX), (APPL), (MSFT)

It’s quite the irony that Netflix’s earnings report came smack dab in the middle of Hollywood’s meltdown as the contract standoff between writers and studios threaten to implode a Southern Californian industry that has been on life support for quite some time.

One’s famine is another’s fortune.

NFLX had a mixed earnings report so it’s not like it has been gangbusters for streaming platforms either.

They used to be a perennial tech growth company and now they are down to just 3% revenue growth which won’t cut it.

NFLX has been saved by the macro picture as traders scurried into tech stocks from early 2023 while investors bet on a Fed pivot and a reversion to the mean after a horrible 2022.

The business itself isn’t doing anything special like it used to, and they are also way too woke, but when they don’t have to be spectacular, it’s easier for the stock to elevate.

The brightest number of all was the addition of 5.9 million subs.

Netflix, which now boasts 238 million global subscribers, will keep benefiting from this password-sharing clampdown.

Some expected it to backfire, but viewers have flashed their wallets and signed up for the service.

The streamer boasted that “sign-ups are already exceeding cancellations” and that it is implementing the password policy across the world now.

Profitability is starting to become an issue for NFLX as they missed on revenue.

Streaming has become a worse business lately because the world is too saturated with content.

Another positive is that NFLX upped its free cash flow from $1.5 billion to approximately $5 billion for the year.

This is what mature tech companies are supposed to do.

Eventually, they will increase deliverables back to the shareholder in the form of buybacks and dividends like Apple (AAPL) and Microsoft (MSFT).

The company cited “lower cash content spend” amid the writers’ and actors’ strikes that have brought content production to an absolute standstill.

No more $9.99 ad-free plan.

Netflix axed its cheapest ad-free option in the US and the UK. The plan, offered at $9.99, is no longer available to new customers.

The decision to cut the skeleton plan appears aimed at pushing subscribers in that price tier toward the ad-supported model, which is priced at $6.99. The company has previously said the ad-supported model performed better on the “economics” than the $9.99 ad-free model.

NFLX shares have had a great year so far with shares up 44%.

The 44% upswing is also after an 8% drop yesterday on this earnings report.

Clearly, traders used this opportunity to take profits.

NFLX’s performance is part of my wider thesis that earnings won’t be anything special, but good enough to deliver a better entry point into these stocks.

Buy the dip strategy will perpetuate for most brand-name tech companies.

It’s not exactly simple to get into a stock that has gone up 44% in 7 months because most of the time the stock needs to be chased.

Chasing tech stocks is an underlying theme of 2023 with fear of missing out (FOMO) engulfing most fund manager’s plans of attack.

So yes, I do believe many investors will use these tepid earnings reports to take profits and these dips are incredibly healthy for the tech sector.

Thus, traders should reload because tech stocks like NFLX will be on discount before the next leg higher.

Mad Hedge Technology Letter

June 23, 2023

Fiat Lux

Featured Trade:

(POACHING FOREIGN TECH)

(OCDO.L), (AMZN), (TSLA), (APPL)

Europe is reeling and now it is becoming Silicon Valley’s playground.

The evidence is all over Europe and quite clear-cut at this point.

The royal 7 from the likes of Tesla (TSLA) and Apple (APPL), who have been responsible for most of the stock market gains this year, are leading the charge to cherry-pick the best tech companies in Europe.

The Ukraine military conflict was a godsend for American big tech, as many European companies are now waving the red flag amid commercial electricity costs spiking 100% in many Western European countries.

The unrelenting electricity increase has caused a mad rush to relocate the best European talent to the United States.

Or, if they don’t relocate out of their own will, many are buy-out targets just like yesterday’s news of British online grocer Ocado.

They are on the verge of tasting the sweet hand of acquisitive cash from Amazon (AMZN).

Poached or not poached – Silicon Valley is dominating.

Ocado Group shares jumped as much as 47% - the most in more than five years.

Even with today’s gains, shares in Ocado have still lost about two-thirds of their value since the end of 2021 amid a selloff in growth stocks.

The stock soared in 2018 on a landmark deal to build warehouses and license software to US supermarket chain Kroger Co., boosting the grocer’s credentials as a technology company. Ocado has partnerships with several grocers, but investor focus has shifted to profitability as demand for automated warehouses slows.

I’m not surprised to hear about Amazon’s interest in Ocado.

Ocado has developed, leading automated warehouse technology that could be of great use to Amazon if it tried to take over the supermarket industry in Europe, which it might.

Many American tourists might experience how outdated and obsolete many European supermarkets are these days.

On the corporate side, when I talk to many European workers on the ground in Milan and Brussels, the consensus is that finding a job at an American big tech firm is considered the proverbial golden paycheck.

European counterparts are mired in inefficiency, unproductivity, and the politicians who exist as 27 European Joe Bidens are ruthlessly driving the industry into the ground by taxing and regulating the hell out of them.

European workers also take 2 months of vacation every year along with 15 to 20 federal holidays per year.

When I read the tea leaves, the next expansion of Silicon Valley is to gobble up anything of perceived value in Europe and anything in any European Union country is fair game.

This buying spree could trigger another leg up to big tech and expand margins.

American tech possesses the powerful balance sheets to wield around the world and dominating the European supermarket industry would add to the top line.

Amazon has already forayed into the food industry with Whole Foods in America so this should be viewed as something similar to that.

Look for big tech to enter strategic European industries and eventually buy something like Manchester United or any other high-quality asset.

Mad Hedge Technology Letter

May 26, 2023

Fiat Lux

Featured Trade:

(RIDE THE ELEVATOR UP WITH GENERATIVE AI)

(NVIDA), (FOMO), (APPL), (MSFT), (META), (GOOGL), (AMZN)

Part of these artificial intelligence executives going on record to sound out the problems with AI is mostly to protect themselves if this weird digital experiment goes disastrously wrong.

They have mostly said that AI going rogue is a real possibility and could end mankind.

Obviously, we hope that doesn’t happen.

Much of the tech market gains this year have been because of the technology surrounding AI.

Strip that out and the gains will look paltry.

A good example is Nvidia (NVDA) offering legendary guidance to the demand of their chips because of the need to install them in AI-based technology.

The AI narrative truly has legs – it will be the theme that defines 2023 in technology stocks.

The Big 7 tech stocks will possess explosive qualities to their stock precisely because of this thesis.

Then there is the fear of missing out (FOMO).

Every financial advisor is pitching AI as an investment of a lifetime – something that cannot be missed by their clients.

Therefore, I do expect meteoric legs up in shares of Nvidia, Apple, Microsoft, Tesla, Amazon, Facebook, and Google in 2023.

These 7 stocks dominate the tech market and the generative AI gains will mostly manifest themselves in these 7 tech firms.

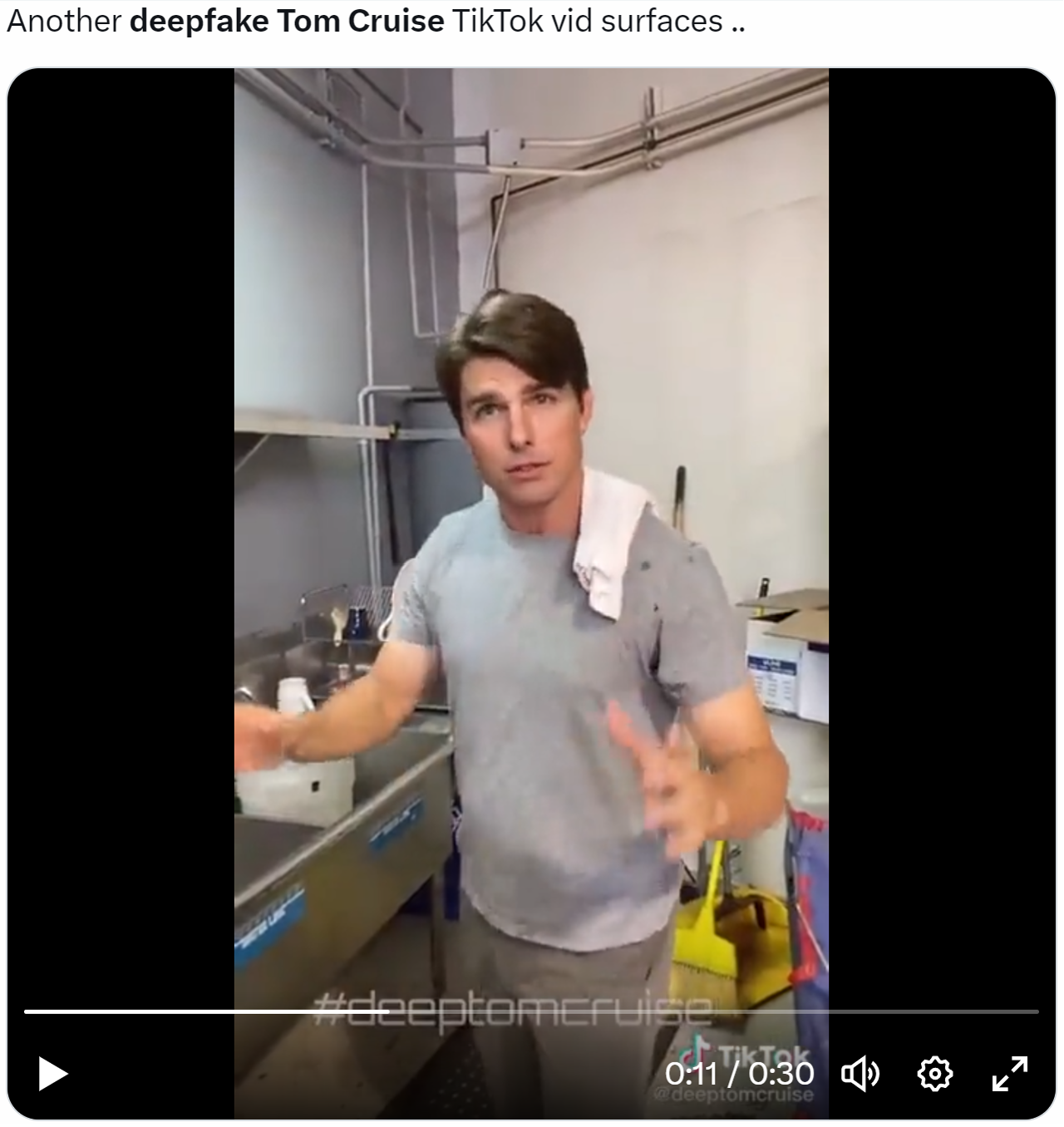

Yet there are dangerous concerns that AI could also destroy these companies and the internet which we interface with, because the changes could erode the trust in platforms by populating fake photos like deep fakes.

In Washington speech, Brad Smith calls for steps to ensure people know when a photo or video is generated by AI.

Brad Smith, the president of Microsoft, has said that his biggest concern around artificial intelligence was deep fakes, realistic-looking but false content.

Smith called for steps to ensure that people know when a photo or video is real and when it is generated by AI, potentially for harmful purposes.

For weeks, lawmakers in Washington have struggled with what laws to pass to control AI even as companies large and small have raced to bring increasingly versatile AI to market.

Last week, Sam Altman, CEO of OpenAI, the startup behind ChatGPT, told a Senate panel in his first appearance before Congress that the use of AI interferes with election integrity is a “significant area of concern,” adding that it needs regulation.

Lawmakers need to ensure that safety brakes be put on AI used to control the electric grid, water supply and other critical infrastructure so that humans remain in control.

It’s hard to know what is fake and real these days. Fake photos of politicians getting attacked or fake videos of tigers roaming around freely in Times Square New York look weirdly authentic.

AI is getting so good that nobody knows what is real anymore.

I’m sure some of you saw the recent Tom Cruise deep fake where the fake Tom Cruise is telling the audience that he does a lot of “industrial clean up” along with his own stunts. Honestly, I could not tell it was fake, and most people wouldn’t. It caught me – hook, line, and sinker.

As it stands, ride this generative AI to riches in the short-term, but be aware that this technology could blow up the internet or make the internet unusable because of security and trust reasons.

DEEPFAKES LOOK AND SOUND TOTALLY REAL IN 2023

Mad Hedge Technology Letter

April 12, 2023

Fiat Lux

Featured Trade:

(TECH EARNINGS BECOME BIGGEST RISK TO TECH)

(COMPQ), (APPL), (ABNB)

In prior iterations of the CPI report, a set of data reflecting the current inflation trends in the US, a positive report would have sent the tech index, known as the Nasdaq (COMPQ), soaring.

Today, we got none of that.

Volatility has taken a nap for the time being – even to the downside.

Why is that?

This time around the tech market is already looking around the corner to earnings that are assumed to be terrible.

Most of the profit margin gains were accrued last year and in the first quarter of this year. The rest of the year, tech companies won’t be able to raise the price of services.

Last year, Apple pushed that extra level pricing of iPhone, and Airbnb charged that extra level for that vacation rental. Now – no more.

Tech consumers are at the extreme upper limit of what they can afford and in fact, have been going deeper into debt to pay for software, hardware, and streaming.

The credit card debt levels have been soaring, showing that consumers are paying more for each item but getting less for every tech product.

What does this mean?

Management will offer bleak tech forecasts.

Silicon Valley might use this underwhelming period as a great platform to throw out the kitchen sink with the bath water.

That’s what today’s price action is telling us.

The easy gains in tech share appreciation were secured in January and March.

Conditions for the same melt up have soured quickly, and not bouncing hard off a great inflation report is an ominous sign in the short term for tech shares.

Now is a time when the easiest path of movement is south in shares as many investors could be taking profits heading into the earnings season.

There are no catalysts for a short-term bounce.

One bright note is that the US dollar has continued its awful performance this year which is highly positive for global growth which tech companies more than participate in.

Hollowing out the tech consumers isn’t the greatest strategy, but until now, it has worked. However, at what point will they stop taking on debt to fund their latest purchase? We could be coming to an inflection point, and that is not good for tech stocks.

As it stands, U.S. inflation is at its lowest level in nearly two years, but underlying price pressures will be sticky for a while.

Inflation rose 5% last month from a year earlier, down from February’s 6% increase and the smallest gain since May 2021, the Labor Department said Wednesday.

The labor market cooled some in March, with hiring gains moderating and wage growth easing. Weekly jobless claims, a proxy for layoffs, are up from historic lows. Also, job openings have dropped—a signal that demand for workers is softening.

Even if the job market has cooled, it hasn’t cooled enough for inflation to crash.

Yes, many tech jobs have been cut, and I see that as a much needed solution to the excesses of Silicon Valley, but today is more of a story of the number one risk to the market shifting from inflation to bad individual performance.

Get ready for many tech companies to tell us why they won’t be doing great later this year.

Remember the market always looks forward, and at the end of last month I predicted a slow April; that forecast has been nothing short of perfect so far.