Mad Hedge Technology Letter

May 9, 2018

Fiat Lux

Featured Trade:

(HERE'S THE TOP STOCK IN THE MARKET TO BUY TODAY),

(MSFT), (AMZN), (AAPL), (APTV), (QCOM), (FB)

Mad Hedge Technology Letter

May 9, 2018

Fiat Lux

Featured Trade:

(HERE'S THE TOP STOCK IN THE MARKET TO BUY TODAY),

(MSFT), (AMZN), (AAPL), (APTV), (QCOM), (FB)

When the CEO of Microsoft, Satya Nadella, sits down for a candid interview, I move mountains then cross heaven and hell to listen to him, and you should, too.

Microsoft is at the top of my list as a conviction buy.

Nadella is one of the great CEOs of our time and was able to complete Microsoft's makeover after Steve Ballmer's insipid tenure at the helm.

Microsoft's Build conference is the perfect platform for Nadella to share his wisdom about the company, industry, and changes going forward.

In an age where tech CEOs thrive off of smoke and mirrors, Nadella was succinct conveying the concept of trust as the secret sauce that will help tech's digital footprint expand into new territories.

Trust infused products through the cloud and A.I. will be the perfect archetype of future tech that will encourage accelerated adoption rates.

A.I. was the message of the day at the Build conference. Nadella used the term A.I. 14 times and the word cloud four times when interviewed.

It was fitting that Microsoft wowed the audience with a sparkly, new-fangled demo.

The demo put on by Microsoft in conjunction with Amazon's (AMZN) Alexa showed smart-assistants working in collaboration.

Microsoft showed how it is possible to use a PC Windows desktop to order an Uber car through Amazon's Alexa.

This technology is very powerful and is a work-around for the "walled garden" problem where big companies are closing off their systems only to proprietary software and products limiting upside potential.

The ability to collaborate with multiple A.I. smart systems will generate a whole new layer of business catering toward the communication and business developments among A.I. systems.

Nadella also offered extended examples of A.I. applications, for instance, the capability of detecting cracks in an oil pipeline and running recognition software through a drone using a Qualcomm (QCOM) manufactured camera to monitor the state of containers.

Trusting A.I. will expedite the usage of A.I. business applications, and the companies diverting capital into A.I. enhancement will reap from what they sow.

The knock-on effect is that university A.I. staff members are being poached faster than a breakfast egg. There is a bidding war going on as we speak from both sides of the Pacific.

Facebook is opening new A.I. research centers in Seattle and Pittsburgh.

Previously, A.I. was a buzzword and companies would trot out a visually stimulating display with pizzazz. But that is all changing with A.I. swiftly moving into the backbone of all business operations.

Ottomatika, a company that develops software for autonomous cars acquired by Aptiv (APTV), was entirely a Carnegie Mellon University (CMU) in-house project that was picked up by Aptiv for commercial applications.

In one fell swoop, (CMU) lost a whole team of leading A.I. researchers.

Microsoft is a premium stock because it straddles both sides of the fence.

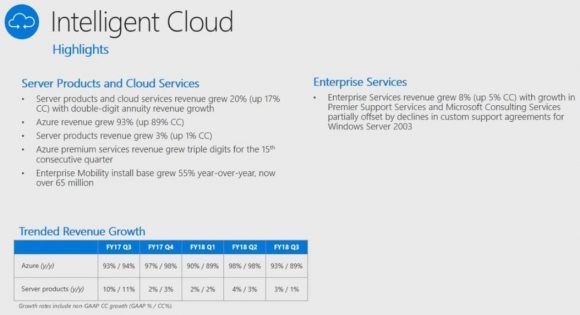

On one side, it's an uber growth company with Microsoft Azure growing 93% YOY satisfying investors requirement for insatiable growth.

On the other hand, Microsoft is robustly lucrative profiting $21.20 billion in 2017, and would be a Warren Buffett-type of cash flow reliant stock even though he has smothered any inkling of buying Microsoft shares because of his close relationship with co-founder Bill Gates.

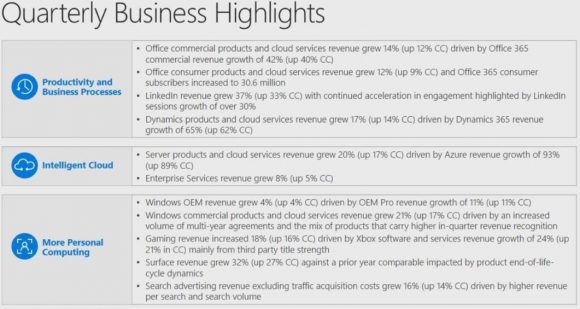

Even Microsoft's legacy product Microsoft Office 365 is a gangbuster segment swelling 42% YOY.

This contrasts with other legacy companies that are attempting to wean themselves from their own outdated products.

Office 365 products are still embedded in daily life, and I am using it now to type this story.

On the technical side of it, Microsoft is beefing up its developer tools.

Microsoft will integrate Kubernetes, an open-source system for automating deployment, into the Azure as well as upping its Azure Bot Service adding 100 new features.

There are more than 300,000 developers who operate the Azure Bot Service alone.

The slew of upgrades for developers will enhance the power of Microsoft's software and ecosystem.

The overarching theme to the Build conference is the integration of A.I. into real life business applications and the importance of the cloud.

Now the Cloud.

Nadella reaffirmed Microsoft's position in the cloud wars characterizing the current environment as a duo of Amazon and Microsoft with Google trailing behind.

Microsoft has the potential to nick Amazon's position as the industry's cloud leader because of the unique set of products it can combine with the cloud.

Most of the world utilizes a mix of PC-based hardware, using Microsoft's software and operating system, supplemented by an Android-based smartphone.

As expected, Microsoft, Alphabet (GOOGL), and Amazon are spending a pretty penny advancing their cloud business.

Microsoft spends more than $1 billion per month on Azure cloud data centers.

This number now surpasses the entire annual Microsoft R&D budget.

In the interview, Nadella cited that Microsoft now has 50 domestic data centers.

Amazon habitually holds between 50,000 to 80,000 servers at each data center. Extrapolate the lower range of the number with 50 data centers and Microsoft could have at least 2.5 million servers working for its data needs.

The barriers of entry have never been higher in the cloud industry because the costs are spiraling out of control.

Few people have billions upon billions to make this business work at the appropriate scale.

Tom Keane, head of Global Infrastructure at Microsoft Azure, recently said that Azure meets 58 compliance requirements set forth by the federal government, industry, and local players.

Azure is the first cloud that satisfies the Defense Federal Acquisition Regulation Supplement criteria for contractors to handle Department of Defense work.

Regulation has emerged as one of the controversial issues of 2018, and this did not get lost in the shuffle.

The trust comment was clearly a thinly veiled swipe against Facebook's (FB) much frowned upon business model, making it commonplace these days for prominent CEOs to distance themselves from Mark Zuckerberg's creation.

Protecting a company's image and reputation is paramount in the new rigid era of big data.

Nadella's anti-Facebook rhetoric continued by noting the auction-based pricing standards are "funky," explaining the model is counterintuitive. His reason was that as demand increases, the price should drop and not rise.

Apple (AAPL) CEO Tim Cook has largely been negative about Facebook's tactics. The fury is justified when you consider Apple and Microsoft hustle industriously to develop software and hardware products while Facebook manipulates user data to profit from collected data. A nice shortcut if there ever was one.

It's clear that Apple and Microsoft have no interest in giving third parties access to personal data because the leadership understands it is a slippery slope to go down and unsustainable.

Nadella's emphasis on tech ethics is a breath of fresh air and the data Microsoft accumulates is used to improve the cloud and software products rather than pedal to mercenaries.

The companies that have staying power create proprietary products that cannot be replicated.

Microsoft's assortment of software products acts as the perfect gateway into the cloud and is a moat widening tool.

A.I. and the cloud are all you need to know, and Microsoft is at the heart of this revolutionary movement.

Any weakness of Microsoft's shares into the low-90s is a screaming buy.

_________________________________________________________________________________________________

Quote of the Day

"Innovation has nothing to do with how many R&D dollars you have. When Apple came up with the Mac, IBM was spending at least 100 times more on R&D. It's not about money. It's about the people you have, how you're led, and how much you get it." - said Apple cofounder Steve Jobs.

Mad Hedge Technology Letter

April 12, 2018

Fiat Lux

Featured Trade:

(THE BIG PLAY IN AUTONOMOUS DRIVING WITH APTIV),

(APTV), (Waymo), (TSLA)

The conventional wisdom on Electric Vehicles (EVs) is that they are here to stay.

The secular trends of harsher government environmental policy, a healthy global economic backdrop, rapid-fire technological development, and broad-based mainstream acceptance are the catalysts that will place EVs at the apex of the digital transportation movement for the rest of this century.

EVs are set to eventually capture more than 60% of market share, forcing legacy automotive and niche start-ups to reinvest into their operations in a fiercely competitive industry.

The EV industry still has a mountain to climb as it only represented less than 1% of total global auto unit sales in 2016. That percentage has gradually risen to 1.25% at the end of 2017.

The transition to 60% EV share of total units will organically occur in a slow and steady manner giving automakers ample time to shed legacy technology.

Cost is a major obstacle for widespread EV adoption. Many consumers cannot afford one, but price efficiencies are slowly dropping the cost of owning an EV, appealing to the masses with sleeker models possessing price tags similar to normal cookie-cutter sedans such as the Tesla Model 3.

EV makers have coped with the arduous task of constructing a car within truncated cost limitations. They make up the difference by offering a proliferation of premium add-ons such as souped-up engines and glitzy interiors that extract additional marginal revenue from well-off individuals.

EV technology advancement paired together with higher emission standards will narrow the gap between electric vehicles and the legacy internal combustion engine within the next decade.

Modern EVs new to market such as the Tesla Model 3 could serve as a springboard for able consumers to dive head in to EV revolution.

The disruption time horizon will take around 15 years and affect 80% of the market.

EV mania is destined to integrate with the traditional concept of a car to give transportation breakthrough A.I. functionality, user-friendly connectivity, and self-driving capabilities.

Let's face it, it's easier to install computer systems and software in an electrified platform, and the technologies complement each other.

About 60% of autonomous, light vehicle retrofits are constructed over an electric powertrain, and an additional 21% go with a hybrid powertrain.

Thus, owning the best autonomous vehicle (AV) technology stocks positions investors for the next leg of hyper-accelerating tech.

Waymo's leadership in the AV space is frightening for Tesla, which trails the Alphabet subsidiary that smoothly rolled out its for-profit service in Arizona in early 2018.

Aptiv PLC made a massive splash in the deep-end by acquiring the second best AV technology company NuTonomy. The Cambridge, MA-based tech firm spun off from MIT in 2013, for $450 million late last year and was spun out again in 2017.

Delphi Technologies spun out its legacy and tech business into two separate companies. The legacy part of the company is now the ticker symbol (DLPH), and the AV company became Aptiv PLC (APTV).

Spin-offs give organizations the opportunity to streamline operations and allow the market to value the company on an independent basis instead of the sum of the parts. This can lead to uncorking additional shareholder value.

Aptiv is the closest thing on the market you will find for an unfettered play on self-driving technology.

Management declined against merging its legacy and AV technology, which is a smart move considering legacy technology gets the wrong rub of the green by investors.

NuTonomy lags Alphabet's Waymo but has been operating robo-taxis in Singapore since 2016. Delphi has gifted additional engineers, reinforcing its fantastic technical talent.

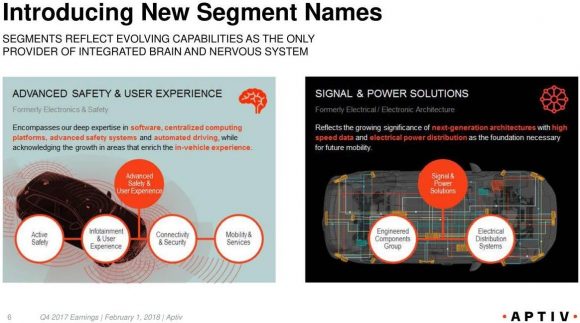

Aptiv has split its business into two new different segments in the new company.

The Advanced Safety and User experience segment will act as the brain in the vehicle, emphasizing software know-how to guarantee user security while a centralized system maintains connectivity.

The new Signal and Power Solutions segment will act as the nervous system in the vehicle by enabling high-speed data fluidity within the next-gen architecture. This segment includes the cable management and connector products that contribute a further $1 billion of revenue to the top line.

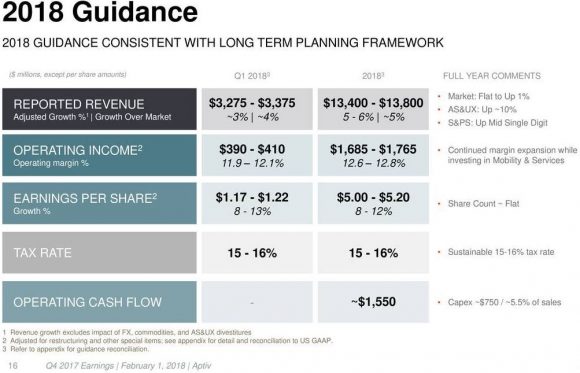

In total, Aptiv procured $12.9 billion in annual revenue in 2017, which was a boost of 4.9% from 2016. Earnings per share growth was up 10.5% YOY.

Investors cannot reasonably expect AV companies to annually grow top line by 20% to 30% as cloud companies, and the margins are unfortunately less savory. The dynamics of the business are different, and the revenue guidance of $13.4 to $13.8 billion should keep investors happy.

The pipeline is in fine fettle with $19.3 billion in bookings, which represent the lifetime gross revenue for consummated contracts.

Some of the outsized awards came in the form of an active safety contract with an OEM alliance, a high-voltage mobile charger contract from a leading North American EV producer, and an architectural contract for BYD's SUV platform in China.

It's no wonder both of the newly crafted segments expect a 10% boost in revenue for 2018.

NuTonomy is such a gem of a company that it is shocking that a large-cap tech firm declined to swoop in.

Half a billion is peanuts for such valuable and innovative technology.

Level 4 and Level 5 grade technologies are already starting to mature.

Other minor acquisitions of analytics firms Control-Tec and Movimento will initiate data monetization opportunities that effectively analyze their aggregated data then translate data into actionable profit-making opportunities.

Big data analytics are needed to decipher the path forward after compiling millions of miles of auto-robo data. And algorithms needing refinement are starving for the data, too.

A fully connected user experience will become standard in these robo-cars, and an integrated, optimized architecture is the secret sauce to commercialization of Level 4 and Level 5 automated vehicles.

Aptiv and Waymo are the only end-to-end system providers of the integrated brain and nervous system in a vehicle.

By late 2018, NuTonomy will have more than 150 Level 4 vehicles in live action.

Aptiv forecasts about $300 million in revenue from Level 4 or Level 5 AV systems by 2025.

Level 4 is practically autonomous - ready with a driver waiting to take control if need be.

Level 1, 2 and 3 revenues will mushroom to $1.8 billion per year, more than tripling from $500 million today.

Ottomatika, a Carnegie Mellon University spin-off founded in 2013, which provides software for self-driving cars, and NuTonomy are the in-house duo entirely focused on complex Level 4 and Level 5 solutions.

The shared access to the system has been set up to allow multiple teams access to the algorithms and technology that feeds through to other parts of the business.

Aptiv PLC is the perfect company to place in a buy and forget portfolio because AV monetization is still in its incubation phase.

Just as investors of pure cloud plays recently have been rewarded in spades, pure AV technology companies will be rewarded as mass rollouts of for-profit services become commonplace.

__________________________________________________________________________________________________

Quote of the Day

"The only constant in the technology industry is change." - said CEO of Salesforce Marc Benioff