CEO of Ark Invest and infamous creator of the ARK Innovation ETF (ARKK) Cathie Wood defiantly said that “innovation solves problems, and the world is facing many more problems today than two years ago. Innovation is key to real growth!”

She likes to keep on banging on about innovation being the panacea to the tech industry when the big tech titans are doing absolutely zilch regarding innovation.

Offering new personalized lock screen designs doesn’t move the needle, but that doesn’t mean that tech stocks ($COMPQ) will go down and shareholders will lose money.

Quite the opposite for the tech cash cow business models.

She later goes on to complain that “The Fed seems to be responding to COVID-related supply shocks spanning 15 months the same way that Volcker battled inflation that had been brewing and building for 15 years. I would not be surprised to see a significant policy pivot in the next three to six months.”

First, Fed Central Bank governor Jerome Powell is nowhere close to the Volker era which saw short-term U.S. interest rates raised to 20% in 1981.

Powell is the antithesis of former Fed chair Paul Volcker and that’s why these bear market rallies are strong and lasting.

Powell wants a “soft landing” – that’s his goal.

The Fed has continuously said they aren’t ready to pivot and by pivot, I mean going from raising rates to lowering rates.

Wood believes that raising rates does nothing to help supply side shocks and that the Fed should start to condition itself to soon lower rates.

The Fed deals solely participates in demand-side policies.

The Fed is on record saying they plan to raise Fed Funds rates to 4% by the end of 2023 and keep rates there for an extended period.

That timeline seems to clash with Wood’s idea of dropping rates in 3 months.

The reason Wood has little credibility is because she has been saying the economy is experiencing deflation every 2 weeks for the past 3 years.

She has the most to lose because her portfolio possesses speculative tech stocks that mostly execute unprofitable business models and need low rates to refinance their large debts just to survive.

She continued to say that the Fed should be looking at metrics like “gold and copper” which “are flagging the risk of deflation.”

It’s quite bizarre that gold would be selected as the leading indicator for monetary policy.

Last time I checked, people can’t eat or drink gold and gold doesn’t heat your shower or apartment, even if you can install golden toilets like Russian President Vladimir Putin. Consumers can’t drive gold either. Higher or lower gold prices don’t indicate that our discretionary budgets are crashing or bulging either.

She also says to completely ignore employment because it’s a “lagging indicator.” This last sentence is false as well as it seems she is confusing this with the unemployment rate being a lagging indicator.

Unfortunately for Wood, the Fed slowly raising rates means it will be longer until they lower them because rates are still highly accommodative.

The silver lining for Wood is that the Fed is more worried about breaking the stock market which could evaporate trillions of dollars in stock market wealth.

Bear market rallies are essential for a soft landing, and we are seeing them in full force.

The last thing investors need is a crashing stock market and impotent tech companies. Remember that Silicon Valley and the tech industry are still the drivers of the US economy.

The Fed will do what they need to do to engineer the result of a soft landing regardless of Cathie Wood.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-12 15:02:022022-10-03 02:56:49Cathie Wood Urges Action

After a half-century in the markets, I have noticed that it is the investors with the correct long-term views who make the biggest money. My favorite example is my friend, Warren Buffet, who doesn’t care if an investment turns good in five minutes or five years.

Buffet’s Berkshire Hathaway (BRKB) is the largest outside investor in Apple (AAPL). And guess what his cost has been? By the time you add up the compounded dividends he has collected since he started buying the stock in 2011, it's zero. The value today? $15.5 billion.

Buffet didn’t buy Apple for its hardware, iPhone, or iTunes. He bought it for the brand, which has improved astronomically. Look at Berkshire’s portfolio and it is packed with brands, like American Express (AXP), Coca-Cola (KO), and Exxon (XOM).

When did Buffet last buy Apple? In May when it hit $130.

That’s why Warren Buffet is Warren Buffet and you are you.

While the inflation news last week has been great and it is likely to get better, I believe that investors are missing the bigger, more important long-term picture.

The fact is that markets are now discounting an earlier than expected end to the Ukraine War, much earlier.

I get constant updates on the war from the Joint Chiefs of Staff, Britain’s Defense Committee, and NATO headquarters and I can tell you that the war has taken a dramatic turn in Ukraine’s favor just in the last two weeks.

Russian casualties have topped 80,000, nearly half the standing army. They have lost 2,200 of their 2,800 operational tanks. Some 120 front line aircraft have been destroyed. This week, Ukraine attacked the principal Russian air base in Crimea, leaving the smoking ruins of seven more aircraft there.

Russia is in effect fighting a modern digitized war with 50-year-old Cold War weapons and it isn’t working. Its generals have no experience fighting wars against determined opposition. Putin would do better listening to the retired generals on CNN for military advice.

America’s High HIMARS (the M142 High Mobility Artillery Rocket System) has become the Stinger missile of this war. The Lockheed Martin (LMT) factory in Camden, Arkansas that makes these missiles is running 24/7 on doubled orders.

The sanctions against Russia have been wildly successful. The Russian economy is utterly collapsing. What oil they are selling now is at half price. Aircraft are being cannibalized for parts to keep others flying. Much of the educated middle class has fled the country. Draft dodging is rampant.

What does all this mean for you and me?

The commodity price spike the war prompted has ended and most are now in steep downtrends. Gold (GLD), where the Russians were major buyers, has been flat as a pancake. This has put our inflation numbers into freefall. Interest rate fears peaked in June and are now in the rear-view mirror.

As is always the case, markets have seen these developments and correctly ascertained their consequences far before we humans did (except for maybe me). It has been no surprise that they have been tracking the Russian defeat day by day and have been on an absolute tear since June 15.

Even small techs suffering 18-month bear markets have now begun major recoveries, with companies like Snowflake (SNOW), up 50%, Netflix (NFLX), up 39%, and Cathie Wood’s Innovation Fund (ARKK) up 57%. Even crypto has returned from the grave, with Ethereum (ETHE) up an eye-popping 105%.

But don’t go gaga over stocks just yet.

The Fed ramps up quantitative tightening in September to $95 billion a month and will deliver another interest rate hike. That's why I am running a double short in the bond market (TLT), (TBT) once again.

We also have the midterms to worry about which, with recent developments, promise to be more contentious than ever. Look for another round of tiring new election fraud claims.

That’s great because these events will give us good entry points lower down for trade alerts, not the short-term top we are looking at right now.

It helps that with ten-year US Treasury yields at 2.80%, it has an effective price earning multiple of 37, while stocks growing earnings at 10% a year boast a price earnings multiple of only 16. That sets up a massive, long stock/short bond trade which Mad Hedge will be pushing well on into 2023.

And you know what?

The smart guys I know in the hedge fund community are starting to model for the next Fed interest rate CUT. Markets will love it and discount this far in advance.

If you want to get on the train with me before it leaves the station, just keep reading this newsletter.

Yes, markets are now being driven by rate cuts and peace prospects, not rate rises and war!

Your retirement fund will love it.

I just thought you’d like to know.

CPI Dives to 8.5%, down 0.6% in July. The peak is in, and stocks rallied 500. Look for another drop in August, with gasoline prices falling daily. The 800-pound gorilla in the room has exited.

The Producer Price Index Dives 0.5%, confirming last week’s weak CPI number. And many core prices are indicating that we will get another drop when the August numbers are reported in September. It was worth another 300-point rally in the Dow Average, which is getting seriously overbought.

Consumer Inflation Expectations dive to 6.2% for the coming year and only 3.2% for three years. according to a New York Fed Survey. Expectations for food costs saw the largest decline. The CPI is out on Wednesday. No doubt a media onslaught over a coming recession has a lot to do with it.

Elon Musk Sells $6.9 billion worth of Tesla (TSLA) Stock, explaining the $100 drop in the shares last week. Ostensibly, this is to pay for Twitter if he loses his court case. Musk clearing took advantage of a 60% rise in (TSLA) to head off distress sales in the future. Musk also opened the door to share buy backs in the future. Buy (TSLA) on dips.

85,000 IRS Agents are Headed Your Way, but only if the government can hire them and only if you are a billionaire or a profitable large oil company. The rest of us will be ignored by this unpublicized portion of the Biden inflation bill.

US Dollar (UUP) Takes a Hit on CPI Report, which effectively showed that the US saw deflation in July. The greenback is pulling back the 20-year highs which gave you the cheapest European vacation in your lives. The prospect of interest rates rising at a slower pace is dollar negative. Buy (FXA) and (FXC) on dips.

Boeing (BA) Delivered its First 787 Dreamliner in a year, after long-awaited regulatory approval. The monster 30% rise in the shares off the June low predicted as much. A global aircraft shortage helps. Airbus is going to have to start earnings its money again. Keep buying (BA) on dips.

Weekly Jobless Claims Pop 12,000 to 262,000, a new high for the year. It’s not at concerning levels yet but is definitely headed in the wrong direction. Maybe it’s just a summer slowdown? Maybe not.

Shipping Container Charges are Plunging Everywhere, except in the US, which currently has the world’s strongest economy. It’s a sign that global supply chain problems are easing. But the US leads the world in demurrage, or delays, with New York the worst, followed by Long Beach. Import Prices are Plunging, thanks to a super strong dollar, taking more pressure off of inflation. They fell 1.4% in July according to the Department of Labor. Easing supply chain problems are helping. Biden has had the run of the table for months now

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil prices now rapidly declining, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

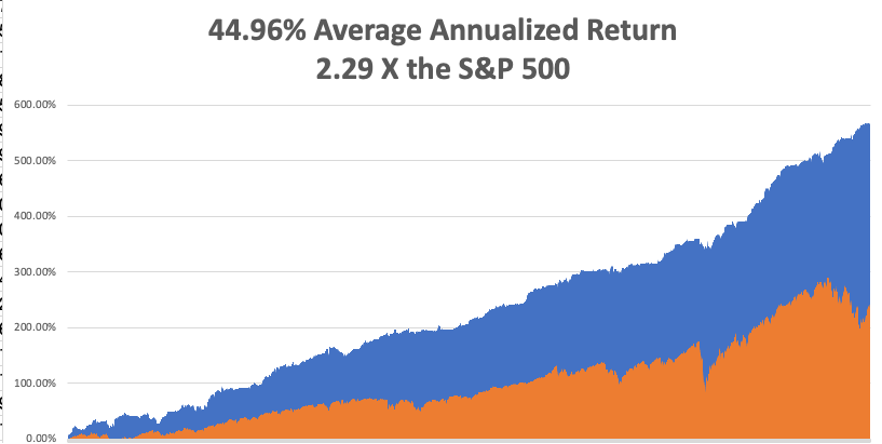

My August performance climbed to +2.14%. My 2022 year-to-date performance ballooned to +56.97%, a new high. The Dow Average is down -7.0% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 74.76%.

That brings my 14-year total return to 569.53%, some 2.56 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.96%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 93 million, up 300,000 in a week and deaths topping 1,037,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, August 15 at 8:30 AM EDT, the New York Empire State Manufacturing Index for August is released.

On Tuesday, August 16 at 8:30 AM, the Housing Starts for July are out.

On Wednesday, August 17 at 8:30 AM, Retail Sales for July are published. At 11:00 AM the Fed Minutes from the last meeting are printed.

On Thursday, August 18 at 8:30 AM, Weekly Jobless Claims are announced. Existing Home Sales for July are announced. On Friday, August 19 at 2:00 the Baker Hughes Oil Rig Count is out.

As for me, while we’re all waiting for the dog days of August to end, it is time to reminisce about my old friend George Schultz who passed away last year at the age of 101.

My friend was having a hard time finding someone to attend a reception who was knowledgeable about financial markets, White House intrigue, international politics, and nuclear weapons.

I asked who was coming. She said Reagan’s Treasury Secretary George Shultz. I said I’d be there wearing my darkest suit, cleanest shirt, and would be on my best behavior, to boot.

It was a rare opportunity to grill a high-level official on a range of top-secret issues that I would have killed for during my days as a journalist for The Economist magazine. I guess arms control is not exactly a hot button issue these days.

I moved in for the kill.

I have known George Shultz for decades, back when he was the CEO of the San Francisco-based heavy engineering company, Bechtel Corp in the 1970s.

I saluted him as “Captain Schultz”, his WWII Marine Corp rank, which has been our inside joke for years. Now that I am a major, I guess I outrank him.

Since the Marine Corps didn’t know what to do with a PhD in economics from MIT, they put him in charge of an anti-aircraft unit in the South Pacific, as he was already familiar with ballistics, trajectories, and apogees.

I asked him why Reagan was so obsessed with Nicaragua, and if he really believed that if we didn’t fight them there, would we be fighting them in the streets of Los Angeles as the then-president claimed.

He replied that the socialist regime had granted the Soviets bases for listening posts that would be used to monitor US West Coast military movements in exchange for free arms supplies. Closing those bases was the true motivation for the entire Nicaragua policy.

To his credit, George was the only senior official to threaten resignation when he learned of the Iran-contra scandal.

I asked his reaction when he met Soviet premier Mikhail Gorbachev in Reykjavik in 1986 when he proposed total nuclear disarmament.

Shultz said he knew the breakthrough was coming because the KGB analyzed a Reagan speech in which he had made just such a proposal.

Reagan had in fact pursued this as a lifetime goal, wanting to return the world to the pre nuclear age he knew in the 1930s, although he never mentioned this in any election campaign. Reagan didn’t mention a lot of things.

As a result of the Reykjavik Treaty, the number of nuclear warheads in the world has dropped from 70,000 to under 10,000. The Soviets then sold their excess plutonium to the US, which has generated 20% of the total US electric power generation for two decades.

Shultz argued that nuclear weapons were not all they were cracked up to be. Despite the US being armed to the teeth, they did nothing to stop the invasions of Korea, Hungary, Vietnam, Afghanistan, and Kuwait.

Schultz told me that the world has been far closer to an accidental Armageddon than people realize.

Twice during his term as Secretary of State, he was awoken in the middle of the night by officers at the NORAD early warning system in Colorado to be told that there were 200 nuclear missiles inbound from the Soviet Union.

He was given five minutes to recommend to the president to launch a counterstrike. Four minutes later, they called back to tell him that there were no missiles, that it was just a computer glitch projecting ghost images on a screen.

When the US bombed Belgrade in 1989, Russian president Boris Yeltsin, in a drunken rage, ordered a full-scale nuclear alert, which would have triggered an immediate American counter-response. Fortunately, his generals ignored him.

I told Schultz that I doubted Iran had the depth of engineering talent needed to run a full-scale nuclear program of any substance.

He said that aid from North Korea and past contributions from the AQ Khan network in Pakistan had helped them address this shortfall.

Ever in search of the profitable trade, I asked Schultz if there was an opportunity in nuclear plays, like the Market Vectors Uranium and Nuclear Energy ETF (NLR) and Cameco Corp. (CCR), that have been severely beaten down by the Fukushima nuclear disaster.

He said there definitely was. In fact, he was personally going to lead efforts to restart the moribund US nuclear industry. The key here is to promote 5th generation technology that uses small, modular designs, and alternative low-risk fuels like thorium.

Schultz believed that the most likely nuclear war will occur between India and Pakistan. Islamic terrorists are planning another attack on Mumbai. This time, India will retaliate by invading Pakistan. The Pakistanis plan on wiping out this army by dropping an atomic bomb on their own territory, not expecting retaliation in kind.

But India will escalate and go nuclear too. Over 100 million would die from the initial exchange. But when you add in unforeseen factors, like the broader environmental effects and crop failures (CORN), (WEAT), (SOYB), (DBA), that number could rise to 1-2 billion. This could happen as early as 2023.

Schultz argued that further arms control talks with the Russians could be tough. They value these weapons more than we do because that’s all they have left.

Schultz delivered a stunner in telling me that Warren Buffet had contributed $50 million of his own money to enhance security at nuclear power plants in emerging markets.

I hadn’t heard that.

As the event ended, I returned to Secretary Shultz to grill him some more about the details of the Reykjavik conference held some 36 years ago.

He responded with incredible detail about names, numbers, and negotiating postures. I then asked him how old he was. He said he was 100.

I responded, “I want to be like you when I grow up”.

He answered that I was “a promising young man.” I took that as encouragement in the extreme.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

We’re Getting Pretty High

https://www.madhedgefundtrader.com/wp-content/uploads/2022/08/wristwatch.jpg331441Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-08-15 09:02:082022-08-15 13:26:22The Market Outlook for the Week Ahead, or What the Market is Really Discounting Now

Below please find subscribers’ Q&A for the August 10 Mad HedgeFund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: What are your yearend targets for Nvidia (NVDA), Tesla (TSLA), and Google (GOOGL)?

A: Higher for all but I can’t give you the exact date and time. Google has a special situation in that they might be hit with an anti-trust suit in September, so that could cap things. For Tesla, we have the Twitter overhang, and Elon Musk sold $6.9 billion worth of stock last week to fund that. And then Nvidia could have another dive, depending on how much of a glut in chips there is, but I'd be buying any chips from here on. By the way, if Tesla breaks the old high of $1,200, which I expect by the end of the year, we could get to $2,000 very rapidly on yet another massive short squeeze against the permanent Tesla haters, who’ve already been completely decimated by the last 60% move.

Q: How would I play Amazon (AMZN) going forward?

A: Buy the dips. I think they’re going to be the world's dominant retailer going forward and they’re doing the right things and going crazy.

Q: Which sectors?

A: Well, for ETFs, you can look at the ProShares Ultra Technology ETF (ROM). That’s 2x leveraged long tech. But only do that on dips because the volatility of the ROM is enormous since it’s 2x in the most volatile sector. Also, I think we can start taking a look at banks again, what with interest rates rising and a recovery on the horizon, banks could come back into play after sitting at the bottom for the last 3 or 4 months.

Q: I’m doing a LEAP on Freeport-McMoRan Inc. (FCX); should I go for January 2025 or 2024?

A: I’d go longer dated—that way you can get a bigger move and will almost certainly be on a full-on economic recovery, and massive electrification of the auto fleet by 2025, thanks to the climate bill that will be passed Friday. That means the demand for copper is about to go absolutely through the roof—I'm looking for (FCX) to go from $30 to $100 in the next 3 years.

Q: Thoughts on Disney (DIS)?

A: No one can believe how cheap Disney has gotten, it’s been a disaster. Obviously (DIS) took it on the nose with the recession and some of the parks still have limitations on the number of visitors. It should do better and I'm amazed it got this cheap. I would expect a move to the $200 level by the end of next year.

Q: What LEAPS do you recommend for January 2023?

A: Well it’s not really a LEAPS if you’re only going out 6 months; that’s just a long-dated call spread. LEAPS are usually a year or longer. I’d say pretty much anything in any sector will be higher except maybe energy by 2023. We’re not at LEAPS territory yet, but we’re getting close. The next major selloff I might start putting LEAPS out there.

Q: Is the Consumer Price Index (CPI) dropping from 9.1% YOY down to 8.5% meaning the top is in and deflation’s over?

A: I think so, because there are a lot of price declines that were not reflected in this July number that have yet to come. I'm talking about wheat, lumber, and energy. So yes, we could get another big move down in August, and if that’s the case, the Fed may only raise by 50 basis points in September. That's the hope. The things that aren’t going to go down are rental costs and labor costs. We may never get back to the inflation rate that we had 2 years ago of 2%. The long-term average for the last 100 years is 3% and certainly a move down to 4% is possible this year (and would be very welcome by the stock market as part of my long-term bull case).

Q: What are your thoughts on Elon Musk selling $6.9 billion worth of Tesla shares?

A: It’s amazing he sold that amount of stock last week and only went down $100. It does remove a big overhang on the stock and paves the way on a much bigger move up later in the year. By selling the $9 in January and $7 now, that’s $16 billion he sold this year. He could almost pay for Twitter with a little outside bank financing.

Q: How far above current prices should I place a LEAPS?

A: It depends on where the market is; if we’re having a cataclysmic selloff down 1,000-point days, then you can have the luxury of going 10%, 20%, or even 30% out-of-the-money; and that of course gets you a 100%, 200% and 300% returns. If we have a higher low, then you may want to go lower risk and go at the money, that might get you a 50% return. On LEAPS that are only slightly in-the-money, even those generate 25% returns one year out with the most conservative possible position.

Q: Would you load the boat on dips?

A: I would but remember: a dip is not one hour or on down days, it’s like half of the recent gain, which would be down 1,500 Dow points, or all of the recent gain, which would be down 3,000 points. So be careful that you don’t get too aggressive just because you’ve gotten bullish.

Q: Do you think the semiconductor chips will lead the tech recovery in the second half of the year?

A: I do, but we do have an inventory problem to digest first, and we have to figure out the implications of the CHIPS act that was signed this week which makes available a couple hundred billion dollars to build new chip factories in the US. Chip companies are particularly challenged right now because they have to provision for a recession which is going to cut chip demand, and they also have to provision for a potential oversupply created by the CHIPS Act. Remember that for the industry, creating safe supplies of chips means more lots of chips at lower prices for consumers. Great for us, great for the auto industry, not so great for chip companies. You have to be careful. On the other hand, on the bullish side, chips are being designed into more products faster and in larger numbers than ever before. This is the main reason why most investors underestimated the chip industry for the last 10 years. That also is a factor that’s accelerating. The average car now has 100 chips. 20 years ago they had maybe 10 chips, and 30 years ago they had none.

Q: Will the eventual big win of Ukraine against Russia result in inflation going back to 2%?

A: No, but it will result in it going back to 3% or 4%, which we could hit next year. You get oil back down below $50, gasoline down to $2/gallon, and the world's food supply opened up once again, and inflation will disappear in a heartbeat.

Q: What’s the deal with the 1% buyback tax in the inflation reduction package?

A: Well they had to get revenue somewhere, and 1% is so small it won’t inhibit anyone from buying back stock, especially if it makes the CEO a billionaire. That is a great incentive—even if you had a 50% tax, they would still be doing buybacks for things like Apple (AAPL), Microsoft (MSFT), and the other buyback players.

Q: What will high energy prices do to crypto?

A: It might actually make it go up because the cost of electricity feeds straight into the manufacturing/programming cost of crypto. And if you notice, Bitcoin bottomed at $17,000 per bitcoin. But that's exactly where the new mining cost is. Just like all of the commodities, when you hit cost of production, the supply suddenly dries up because nobody can make any money at it.

Q: Will US homebuyers buy the dip since mortgage rates have come down?

A: Yes, and we’re already seeing that in the statistics. The fact is we still have a huge housing shortage in the United States. You don’t get big price falls when you have a shortage of supply, and you have 10 million millennials who still need to trade up from their one and two-bedroom apartments all over the country. So, things may stall a bit in home buying, but I don’t think you get very big price drops.

Q: Do you think the US consumer is strong?

A: They never stopped being strong, even throughout recession fears. Never, ever bet against the propensity of Americans to spend money, both individuals and governments.

Q: What are the chances the US goes to war with China over Taiwan?

A: Zero. # 1 China doesn't have ships, #2 we have the 7th Fleet there, and #3 they have been threatening to invade Taiwan for 70 years and done nothing. The Taiwanese are used to this. Though there is the other side issue that most of the other private companies in Taiwan are already owned by the Chinese and have Chinese capital, so it’s unlikely they want to blow up their own facilities. So, the answer is no.

Q: What is the Long term outlook for gold and silver?

A: It’s been dead for so long that I’m not inclined to rush into gold. But you have to expect that when you get a recovery in the commodity boom, it’s going drag gold and silver along with it. I see upsides for both of these, especially silver.

Q: Should student loans be paid off by the federal government?

A: I think yes, because as long as these people have massive debts, they cannot borrow and they cannot enter the US economy as consumers. If you forgive all student debt, you unleash 10 million new customers onto the market who can now borrow, get credit cards, and take out home mortgages. As long as they have massive debts, they can’t do that.

Q: With all the major companies in the world moving to EVs, where are we going to get these commodities?

A: We’re not. Tesla (TSLA) has already locked up major supplies of commodities over the next 10 years, and everyone else will have to pay more money. Some of the weaker producers like Ford (F) and General Motors (GM), are being restrained on shortages of not just chips but also basic commodities like chromium for stainless steel. They’re going to have a real problem competing with Tesla, which is why you own Tesla.

Q: What do you think about the unprofitable tech companies like those in the ARK ETFs (ARKK)?

A: I would avoid those for now. Why take on additional risk buying a non-earning company when the highest quality companies are selling at the cheapest valuations in ten years? Maybe when the big companies like Apple get overvalued—go up another 100% — then you might look at the smaller companies if they’re still cheap. But the risk/reward on the nonearners right now is no good, while it’s fantastic in the large tech companies. That is my opinion and I’m sticking to it.

Q: It seems Russia’s strategy has mirrored those of the Czars.

A: Actually, what they’re doing is repeating their WWII strategy, which worked in 1945— not so much in 2022; and that was massive artillery barrages against retreating Germans. Except this time Ukrainians are not retreating and have far more modern weapons than the Russians.

Q: Would you buy Micron Technology (MU) on bigger dips?

A: Absolutely yes; but again, wait for the down days. You have plenty of volatility in chip stocks, no need to pay up or chase higher prices.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/07/john-thomas-parachute.jpg580432Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-08-12 11:02:382022-08-13 21:52:27August 10 Biweekly Strategy Webinar Q&A

As the bear market rally picked up steam Tuesday with even Cathy Wood’s growth ETF (ARKK) gaining 9%, it’s clearly a reaction to the Nasdaq repricing its biggest underlying risk.

The market is now pricing in a global recession and that has replaced inflation as the number one worry for investors.

This new development has led to the Nasdaq sniffing out the return to the bad news is good news effect.

That is why the U.S. 10-year treasury yield cratered from 3.5% to 2.8% which reflects the future expectation of a pulled-forward global recession.

This would trigger a fresh interest rate lowering cycle by global central banks.

Lowering rates is good for Nasdaq stocks and tech stocks will be a big beneficiary of lowered rates as they have overshot to the downside on this rate rise cycle.

That doesn’t mean it’s all rosy in the land of the Nasdaq, hardly so.

We are still in the fog of war and amid improving technical data like lower oil prices, worsening economic relations between the large nuclear-equipped countries are not only moving the world towards a soft technological decoupling but a hard fracturing of general relations.

My first thought was will China finally strike back against the United States in the form of destroying Tesla’s (TSLA) Gigafactory in Shanghai or blacklist Apple (AAPL) iPhones in China.

These two events would be the point of no return for the two countries’ economic cooperation and anything beyond that, relations could spiral out of control rapidly and even be the impetus for a Taiwan takeover.

Clearly, Silicon Valley does much better when the world is getting along, and everyone is paying for their stuff.

That can’t happen as smoothly with the world rapidly balkanizing which is a big reason for massive selloffs in Netflix whose international audience has soured.

On the production side of things, Chinese-produced stuff won’t be able to get sold back to Americans using Guangdong factory production as semiconductor chips and equipment have become the focal point of national security efforts.

The US has placed export controls against Chinese technology firms from purchasing chips and equipment.

Now Biden is blackmailing the Netherlands to ban one of its top chipmakers from selling semiconductor equipment to Chinese companies.

The Biden administration is pushing hard for Dutch chip equipment maker ASML Holding NV (ASML) to halt selling some of its older deep ultraviolet lithography, or DUV, systems.

Even though these machines are one generation behind cutting-edge, they offer high-tech chips for automobiles and consumer electronics.

Washington has also pressured Japan to stop shipping semiconductor machines to China.

Since the Trump tariffs, China has been the biggest buyer of chipmaking gear for the last two years.

On the European front, regulation is hitting home hard as the U.K. has initiated investigations on Amazon’s selling practice by in-house brands and is looking into Microsoft’s anti-competitive acquisition of Activision.

If American tech companies have nowhere to produce, nobody to acquire for instant growth, and nobody to sell to then it becomes a massive issue for shareholders.

Even though the equity mojo boost of good news is bad news is a nice reprieve, a global recession where many companies fire staff and can’t sell their product because lack of parts is worse.

Therefore, we are still issuing a sell the rallies in tech type of recommendation to our readers while acknowledging there has been a small wave of dip buyers entering back into the game.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-07-06 16:02:362022-07-06 16:30:07Good News Is Bad News

“We could have a couple of negative quarters” – uttered Federal Reserve Bank of Philadelphia President Patrick Harker.

We badly needed to hear that, because the jargon we’ve been offered so far from federal representatives has not been honest enough.

Ironically enough, saying the truth could offer relief to the Nasdaq index as pricing in a recession moves us along, but that doesn’t mean we are out of the woods yet.

Harker also said it is possible the U.S. economy might see a modest contraction in growth, but he expects the job market to remain strong.

Let me translate that for you.

Harker expects a soft recession, and he feels that it is increasingly priced into stocks.

However, the Nasdaq isn’t priced for a hard recession today, which could be the potential driving force for another dip in the index.

Adding some validation to a possible leg lower is that one of the biggest dip buyers out there, Blackrock (BLK), has said that it is not buying the dip in stocks, as valuations haven’t really improved.

Maybe they are targeting more single-family homes!

To get a real reversal of momentum, we will need not only big stocks like Apple to participate, but also the big buyers.

Don’t look at the Saudi’s either, they are busy earnings $2 billion a day selling oil.

From behind the scenes talks, there is still the hush hush feeling that positioning indicates that we are in for a sharp V-shaped rebound.

How do I know this?

Tech earnings still have a highly optimistic tinge to them, and lower inflation is built into earnings’ calculations.

Don’t forget that many garden-variety tech CFOs built low inflation into their 2nd half of the year revenue models.

Inflation, according to them, is supposed to subside triggering earnings’ beats around the pantheon of great tech companies.

This is what is supposed to happen if consensus plays out.

It rarely does.

Adding fuel to the fire is a proposed federal gas tax holiday by the current administration which is extraordinarily inflationary even if it does help marginal tech companies like Uber (UBER) and Lyft (LYFT) in the short run.

A tax holiday will destroy oil capacity by disincentivizing oil companies in capital investments.

Supply will also crash by encouraging gas hoarding by clever consumers and CEOs hellbent on taking advantage of this brief tax holiday.

The 800-pound gorilla in the room is clearly China.

Imagine if the Communists finally start to peel back their dystopian arbitrary lockdowns and what that will do for rampant inflation.

Pork prices will rise 25% and more importantly oil prices will revisit the peak we had from the on set of the military event East of Poland.

All of this matters for tech companies that consummate contracts for chips, parts, pay salaries to inflationary traumatized coders and build computers.

The conundrum here is that CFOs and CEOs might be guilty of being too positive in regard to the economic cycle.

Consensus estimates (IBES data by Refinitiv) still show very healthy levels of earnings growth. S&P 500 earnings per share for 2022 remain at +10.8%, but the expectations for 2023 continue to reflect a probably optimistic +8.1% growth, with revenues up 4%.

This is ridiculously overly optimistic and isn’t in tune to the realities on the ground.

It is highly plausible we will experience another bear market rally in tech only to be reminded by upcoming earnings’ revisions that there’s still multiple contractions that needs to be rammed down our throat.

Tech stocks will be the most volatile during this period and traders looking for the best bang for a buck should look at smaller positions but in higher beta names like Tuttle Capital Short Innovation ETF (SARK) for the post-bear market rally and ARK Innovation ETF (ARKK) for the current bear market rally.

It’ll be interesting to see if stocks like Apple (AAPL) can eclipse their previous bear market rally peak of $151.

Apple stands at $138, and I presume with these lower gas prices, it should eke out at least $145 before another acid test.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-22 16:02:182022-06-26 00:11:30Earnings Revision in the Pipeline

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.