Mad Hedge Technology Letter

July 8, 2024

Fiat Lux

Featured Trade:

(ARM SHINES BRIGHT)

(ARM), (NVDA), (AMD)

Mad Hedge Technology Letter

July 8, 2024

Fiat Lux

Featured Trade:

(ARM SHINES BRIGHT)

(ARM), (NVDA), (AMD)

With the US Central Bank’s policy being quite accommodative, this advantageous backdrop has really set the platform for certain strategic tech companies to shine on the public markets.

In particular, chip stocks have been the darlings of the AI revolution and will continue to be in the limelight.

Part of this is about investors not knowing in particular what software firms will benefit from AI.

It is really a crapshoot to know how the software will look like in the future, but investors do know that software will be powered by the backend infrastructure which is why AI chips are fetching a premium at market in today’s stock market.

Once the software part of it starts to reveal itself, then it is highly likely the software winners will start to experience the same sort of price appreciation in shares that AI chip companies are experiencing right now.

That trend reversal is still years off so it is better to spend our energy on chip stocks.

The no-brainers are the likes of Nvidia and AMD, but the lineup is dee.

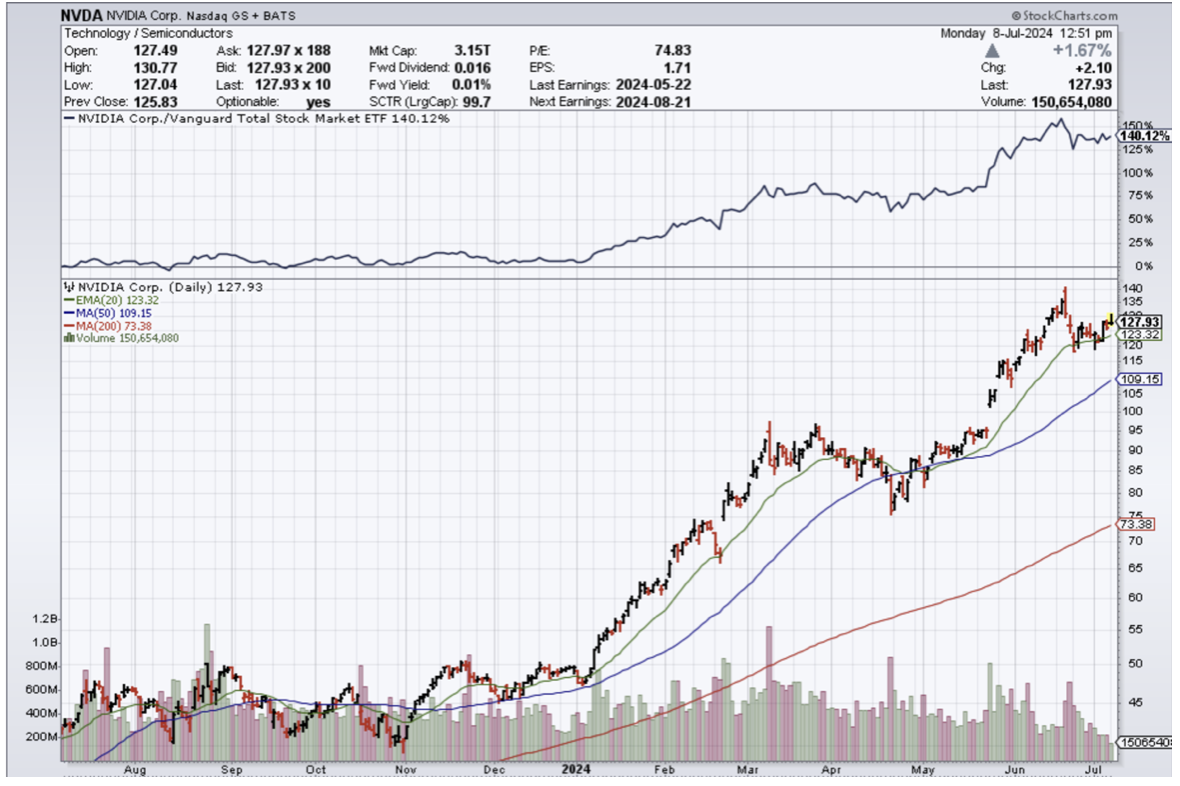

Look at the 2nd and 3rd tier of chip stocks like British chip company ARM (ARM).

Arm is also right in the mix of the AI boom. The positive market sentiment toward AI advancements continues to propel Arm's stock upwards. Furthermore, the company's former focus on low-power embedded and mobile chips is changing before your eyes. These days, you'll find Arm-based chips all over modern data centers and PC systems.

The broader market dynamics also played a role in Arm's rise. A softer-than-expected jobs report in May fueled hopes for potential interest rate cuts by the Federal Reserve, which would benefit growth stocks. The semiconductor sector is full of growth stories, including Arm.

Industry news also contributed to Arm's strong performance. Reports that Taiwan Semiconductor Manufacturing was investing in extreme ultraviolet lithography suggested a robust demand for next-generation chip technologies. As TSMC is a leading manufacturer of Arm-based chips, this investment indicated a positive outlook for Arm's future growth.

Arm's strategic positioning in the AI ecosystem highlights its potential for sustained growth. The company's advanced v9 architecture and its power-efficient processor platforms are increasingly interesting to major industry players, strengthening Arm's competitive edge in the semiconductor market.

ARM and its ticker symbol were added to the Nasdaq-100 Index on June 24.

This move guarantees more capital flow into ARM as it becomes part of a bigger ETF meaning pension and institutional money will own a piece of ARM and help the stock rise.

Arm's rapid inclusion in the index after an initial public offering last September reminds investors of its growing importance in the global technology ecosystem. As CEO Rene Haas highlighted in that announcement, this achievement validates Arm's business strategy and its critical role in providing foundational compute solutions for AI workloads.

Don’t forget that ARM agreed to be purchased by Nvidia which speaks volumes of what Nvidia believes about ARM.

Unfortunately for both, the deal was shut down due to regulatory issues, and imagines the future trajectory of ARM if that deal went through.

In the past 365 days, the stock is up over 200% and just looking at a 2024 chart, readers can understand how investors have complete belief in the future of ARM.

ARM will continue to maintain an important position in the future of AI and they are a juicy takeover target.

I do believe that AI stocks like ARM will continue to grind up, but we are inching closer to a point where investors will take profits before the next leg up.

Global Market Comments

June 14, 2024

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(JUNE 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(NVDA), (AVGO), (ARM), (GM), (TSLA), (SQM), (FMC), (ALB), (AAPL), ($VIX), (AMZN), (MO), (NFLX), (ABNB)

Below please find subscribers’ Q&A for the June 12 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: How will Nvidia (NVDA) trade post-split?

A: Well, it’ll probably keep going up, because I think the year-end target—the old $1400, which is now $140—is still good. And I have a whole bunch of LEAPS, which are post-split $40, $50, $60 in-the-money, and I’m just keeping those. It’s a good cash management tool to have. So, even $500 points in the money, you’re still looking at about 20% returns by the end of the year on a January LEAPS. If you can buy the January 2025 $70-$71 LEAPS for 83 cents that’s a 20.48% profit at expiration in six months. So if you want a safe, very high return, that is the best way to do it in the financial markets, is to go way in the money. LEAPS will still pay you a lot of money amazingly. This trade will disappear someday but it’s there now and I’m taking it. Screw 90-day T-bills—I’m going into $500 in-the-money LEAPs on Nvidia, which pays four times as much.

Q: Is Broadcom Inc (AVGO) the next Nvidia?

A: There is no next Nvidia—the next Nvidia is Nvidia. Buy Nvidia on a 20% decline, which I think we may get sometime this summer. That’s a dip you want to buy for a year-end run to $140. Also, Broadcom isn’t exactly undiscovered at this point. It has doubled since October, while Nvidia is up 4 times. So if the bargain in the market for you is double in six months, I’m not sure you should be in the market. That said, I put out a report on split candidates last week and (AVGO) is very high on the list.

Q: What’s the best way to trade split candidates?

A: I actually just wrote a newsletter about this last week. There are in fact 36 high-priced, good money-earning split candidates, and I listed them all. You can buy really any of those if you’re looking for a high-priced stock that is growing. And management has a huge incentive to do splits because it makes the stock go up faster, and they’re all paid in stock options. So that is another reason you go into these. The best way to trade splits is buying the candidates because the biggest move is on the announcement of the split—you usually get 10%, 15%, or even 20% returns on the announcement.

Q: How do you envision AI in 10 years?

A: Well, it’s unimaginable. I can tell you from experiencing a lot of these big technology changes—it’s always tremendously underestimated by the markets, and you can safely bet on that. It’ll go up a lot more than you realize. That’s what happened when we jumped from six track tapes to cassettes, Betamax to VHS, teletypes to faxes, and faxes to emails. I thought Steve Jobs was crazy when he introduced the iPhone. Nobody makes money in handsets. But he proved me wrong. That makes my $240,000 DOW by 2030 projection completely reasonable.

Q: What will inflation do for the rest of the year, and how will it affect stocks?

A: Inflation will go flat to down for the rest of the year. And that is being driven by artificial intelligence—the greatest deflationary product ever created in the history of the economy. It’s unbelievable the rate at which AI is replacing real people in jobs. If you want a good example of that, I had to call Verizon yesterday to buy an international plan, and I never even talked to a human. They listed out three international plans in a calm, even male voice, and I picked one. Or go to McDonald's where $500 machines are replacing $40,000 a year workers. This is going on everywhere at the same time at the fastest speed I have ever seen any new technology adopted. So buy stocks, that’s all I can say.

Q: What’s your opinion on Arm Holdings (ARM)?

A: I love it. There are very few serious companies in the chip area, and this is one of them.

Q: Do you expect gold mining stocks to continue upward?

A: Yes, but the better play here is the metal. Gold and silver aren't being held back by inflation while the miners are. Plus, the main buyers in the market now are the Chinese, and they don’t buy gold miners—they buy gold, silver, copper, platinum, and uranium outright.

Q: What about Tesla (TSLA) long-term? Kathy Woods's target is $2000 long-term.

A: I think Kathy Woods is right. But we have to get through the nuclear winter in the EV space first, where suddenly the market got saturated. I think Tesla is the only one who could come out of this alive by cutting costs and advancing technology, as they have always done. When I bought my first Tesla Model S1 in 2010, the battery cost $32,000. Now it’s $6,000, and you get a lot more range. Did (GM) offer an equivalent cost improvement with internal combustion engines? So, yes, never bet against Elon Musk—that’s a good 25-year lesson on my part, and should be for you too.

Q: Can you elaborate on the lithium trades?

A: I listed three names in my letter last week, (SQM), (FMC), (ALB), and the only thing you know for sure is that they’re cheap now. They could stay cheap for another six or 12 months. But when you get a turnaround in the global EV market and the manufacturers start screaming for more lithium, and all of the lithium stocks will double, or triple and they’ll do it fairly quickly. You can’t beat a market bottom for getting involved. Just look at my above (NVDA) trade. Not only would they be good stocks buy, but it would be a good LEAPS buy down here because then you could get 4 or 5 times your money on a small move.

Q: Can you suggest Amazon (AMZN) LEAPS?

A: January 2025 $195-200 just out of the money, should give you a return of about 120% over the next 6 months. That gets you the annual yearend run-up. And that’s my conservative position. My aggressive ones are all in Nvidia.

Q: Do you think zero-day options have permanently forced the Volatility Index ($VIX) to the $12 handle?

A: Yes, I do; it’s killed that market. Something like 40% of all the option traders on the CBOE were trading the ($VIX) from the short side. Shorting the ($VIX) now would be madness. That has to bring tough times for that whole industry. Trading call spreads at a $12 volatility, you’re better off buying the LEAPS because the LEAPS give you much bigger returns with much less risk. And a $12 ($VIX) means you’re getting your LEAPS at half the historic price. I’m just waiting for a new market low to start pumping out the LEAPS recommendations. All the more reason to sign up for the Mad Hedge Concierge Service to get an early read into the LEAPS recommendations. For more information on that, contact support at support@madhedgefundtrader.com

Q: What will happen to Apple (AAPL) after the 11% surge?

A: It goes to $250 by the end of the year. Now that it has the kiss of AI on it, people will pour into it.

Q: Why is value lagging?

A: Because AI is entirely a growth story, and you look at all the domestic value stocks, they’re going absolutely nowhere. Value has been in the dog house for years and I’m in no hurry to get in there.

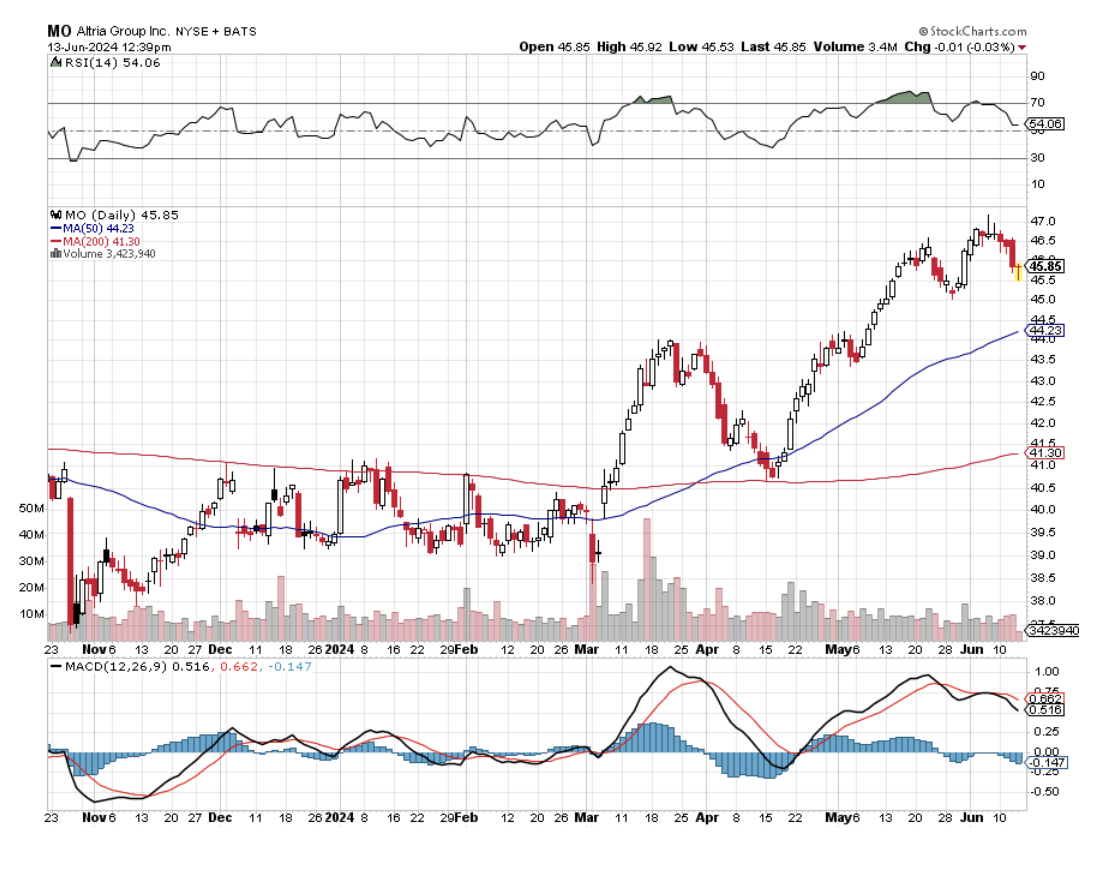

Q: What is the best dividend stock I can invest in right now?

A: That’s an easy one. Altria (MO) has a 9% dividend—you can’t beat that. But you have to hold your nose when you buy this stock because they are in the cigarette business. However, their big growth now is in Asia ex-Japan where the government has a monopoly on tobacco, particularly China. Note that this is not an undiscovered idea; lots of people like a 9% dividend stock and (MO) has already gone up 20% this year, but I think there is still some money to be made here.

Q: How can we subscribe to get early LEAPS recommendations?

A: That would be the Concierge Service. Contact Filomena at customer support, and they will get you taken care of right away.

Q: What about the small nuclear plays?

A: I actually happen to know quite a lot about nuclear plant design, having worked for the Atomic Energy Commission in my youth, and the new designs address every major issue that held back nuclear power with the old 1950s designs. For example, building them underground and eliminated the need for these giant billion-dollar four-foot-thick reinforced concrete containment structures that dot the horizon. Not using pure Uranium alloys that can’t go supercritical is another great idea. So I like them. Are they good stock plays? Not right now. It takes a long time to introduce a new energy technology. Bill Gates is financing a new plant built by Terrapower in Wyoming, and it looks like a fantastic plant, but only Bill Gates could invest at this stage and expect to make money on it. He has very long-term money and you don’t. I would wait until you get a working model plant in the United States before going into these things, but potentially you’re looking at a 10 to 100 times return on your money if it works.

Q: Should I invest in Airbnb (ABNB) because of increased international travel?

A: Yes, we like Airbnb. Especially since they will get a push with the Paris Olympics next month. Not only does that get people to Paris, but it gets people to all of Europe because they usually add on additional trips to a visit to the Olympics.

Q: What would you do in Netflix (NFLX), and what strikes would you use?

A: I would do a LEAPS. Wait for a correction, at least 10%, preferably 20%, and then I would go at the money one year out and that would get you about 100% return. So, that’s the way to do that. This is not LEAPS territory right here —all-time highs are not LEAPS territory. You want to put on LEAPS when everyone else is throwing up on their shoes; the last time they did that was October 26.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

You Only Need One Big Hit to Make a Great Year

Global Market Comments

February 12, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or RAISING MY YEAREND TARGET TO (SPX) $6,000)

(AAPL), (GOOGL), (META) (MSFT), (AMZN), (V), (PANW), (CCJ), (ARM), (USO), (XOM), (OXY), (INDA), (INDY), (FXI), (BABA), (NVDA), (TSA), (RCL)

When I announced my year-end target for the S&P 500 on the first of January, I knew it was cautious. That provided for only a 15% gain for 2024. Yet here we are a mere six weeks into the New Year, and we only have 10.4% to go.

That is with the six lead stocks, which account for 30% of the entire stock market capitalization, seeing earnings grow up to 300% annually. With that kind of growth, even $6,000 is looking overly conservative, even allowing for no multiple expansion whatsoever.

The top six stocks are over 11% YTD, while half of all S&P 500 stocks are down. A few friends of mine who are still alive and have been in the market for as long as I have never seen a market this concentrated. They are amazed, befuddled, and aghast, as am I.

And if you do want to buy big tech, you’re going to have to compete with the big tech companies themselves to do so. The buyback machine continues full speed ahead, with Apple (AAPL) Hoovering up $20.5 billion of its own shares, Alphabet (GOOGL) $16.1 billion, Meta (META) 6.3 billion, and Microsoft (MSFT) $4 billion.

I am a firm believer that markets will do whatever they have to do to screw the most people. So far this year it has done an admirable job doing just that, going up in a straight line with everyone underinvested and with $8 trillion on the sideline.

This is how markets will continue screwing most people. It keeps going up a little bit more. The NVIDIA earnings announcement due out on February 21 could be the ideal turning point.

Then the market suffers a ferocious correction, maybe 10% in a short period. Traders panic and dump all their positions. Then the (SPX) turns around at about $4,800 on a dime and then rockets all the way up to $6,000, frustrating investors once again.

I just thought you’d like to know.

I am usually cautious about ultra bears, but I picked up an interesting view last week about how long it may take the Chinese economy to recover.

During the US house bust from 2007 to 2012, the United States had 3 million excess unwanted homes weighing on the market like a dead weight, or about a seven-month oversupply. That was enough excess to cause the Great Recession, a 52% crash in the S&P 500, and the demise of thousands of American companies, including Lehman Brothers and Bear Stearns.

Today, China has a staggering 50 million excess homes in a population only four times larger than ours. That is a 15-year oversupply for the market. That means China could suffer a decade and a half of subpar growth and lagging stock markets. Don’t touch Chinese stocks even though they offer attractive single-digit multiples.

Why do you care? Because China is the world’s largest consumer and importer of most commodities, food, and energy. The stocks that specialize in these areas could be facing a long-term drag from the Middle Kingdom unless it is offset somewhere else.

The Chinese are only now discovering that the principal driver of their economic growth for the past 30 years has been US investment. President Xi has managed to scare that away with a hostile attitude towards America and saber-rattling over Taiwan. Last year for the first time the US imported more from Mexico than from China, where many companies have re-shored.

Wonder why crude oil (USO), (XOM), (OXY) is at $68 a barrel when the US economy is growing at a 3.1% rate? This is the reason. It is also a strong argument in favor of investing in India, which I discussed last week. Buy the (INDA) and the (INDY), not the (FXI) or (BABA).

In the meantime, you’ve got to love ARM Holdings PLC, whose earnings announcement triggered a heroic 56% one-day move up in the stock. They execute sub-designs for almost every AI chip out there. That’s what a 3% float in the stock gets you. Anyone who has any doubts about the durability of the AI story should take a look at what happened to (ARM) last week.

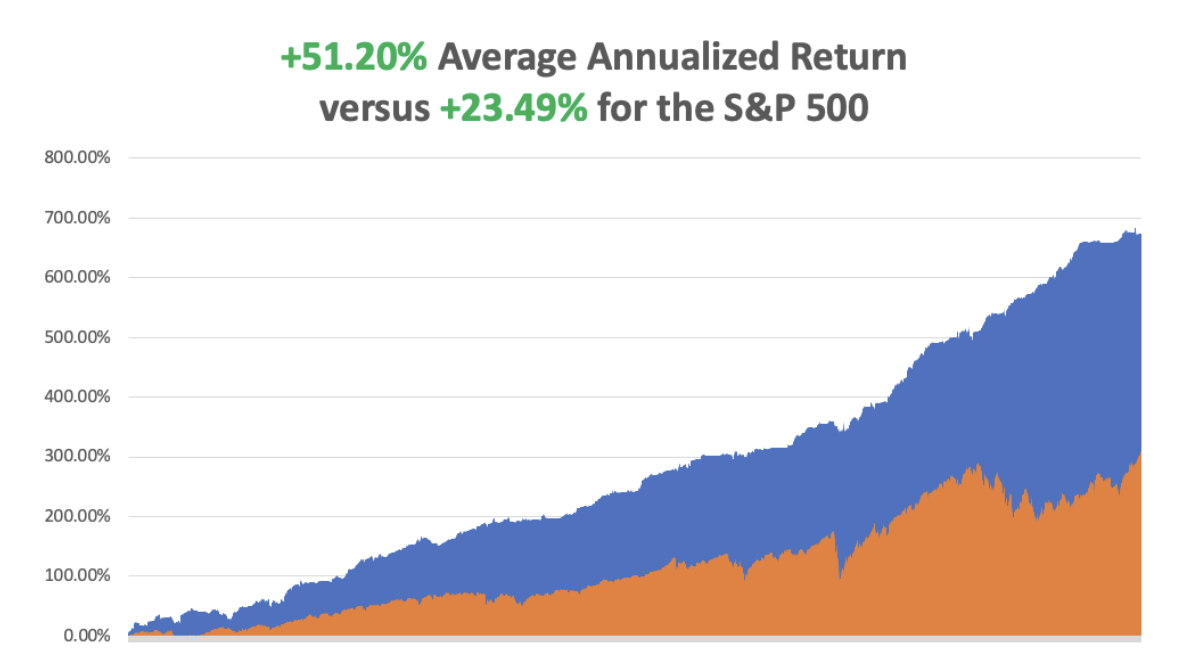

So far in February, we are up +1.78%. My 2024 year-to-date performance is also at -2.50%. The S&P 500 (SPY) is up +5.03% so far in 2024. My trailing one-year return reached +60.44% versus +33.13% for the S&P 500.

That brings my 16-year total return to +674.13%. My average annualized return has retreated to +51.20%.

Some 63 of my 70 trades last year were profitable in 2023.

I am maintaining longs in (MSFT), (AMZN), (V), (PANW), and (CCJ).

Reheating is Becoming an Issue, with a strong US economy and record-low unemployment rate possibly prompting the Fed to delay interest rate cuts. The stock market has been running on steroids on the expectation of imminent cuts. This is a new market risk and could unleash a thunderstorm on our parade.

CPI Revised Down, in December, from 0.3% to 0.2%. The deflationary economy is back! Stocks loved it, with the S&P 500 catapulting to $5,000. That’s why I revised my yearend target up to $6,000.

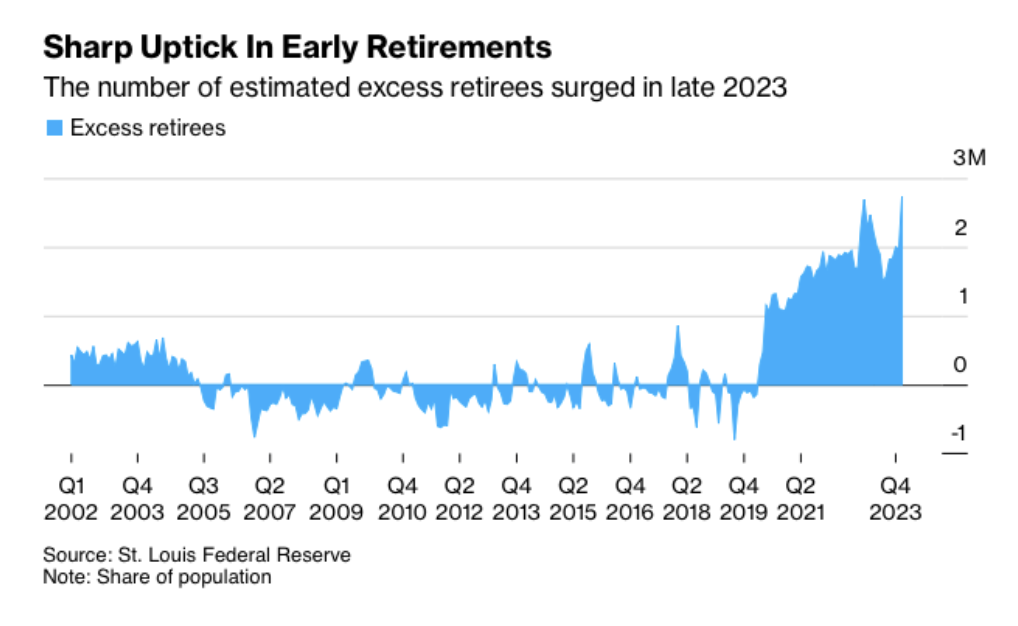

Early Retirements are Soaring, thanks to a stock market at new all-time highs. Baby boomers can now afford to “take this job and shove it.”

NVIDIA Enters New Custom Chip Market, potentially adding another $30 billion in revenues. The dominant global designer and supplier of AI chips aim to capture a portion of an exploding market for custom AI chips and to protect itself from the growing number of companies interested in finding alternatives to its products. Buy (NVDA) on dips.

Morgan Stanley Upgrades NVIDIA to an $800 Target. An exceptional supply-demand imbalance in the artificial intelligence-chip sector, as well as a massive shift in spending toward emerging technology, is likely to persist over the near term. Buy (NVDA) on dips.

ARM Holdings (ARM) Soars by 41%, off a spectacular forecast-based demand for designed-up AI chips. UK-based Arm makes money through royalties, when companies pay for access to build Arm-compatible chips, usually amounting to a small percentage of the final chip price. Arm said its customers shipped 7.7 billion Arm chips during the September quarter.

Tesla (TSLA) Looking to Cut Jobs, and reduce costs, as is the rest of Silicon Valley. The move could mark the bottom of the stock. Elon Musk is the master job cutter, axing 80% of the Twitter staff on takeover.

Meta (META) Gains $196 Billion in Market Cap in One Day, off the back of record sales, tripled earnings, and reduced costs.

Construction Spending Gains, up 0.9% in December, the best since October. Watch the industry reaccelerate as interest rates fall.

Royal Caribbean Beats, with record bookings in an industry I have recently become intensely interested in. (RCL) is grabbing market share from land-based vacations, as Millennials are finally discovering cheap cruise vacations, where it is often cheaper than to stay in a motel with all you can eat. Only a few cruises were lost to the Red Sea War. (RCL) just launched Icon of the Seas, the world’s largest cruise ship.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, February 12, the US Consumer Inflation Expectations are announced.

On Tuesday, February 13 at 8:30 AM EST, the Core Inflation Rate will be released.

On Wednesday, February 14 at 2:00 PM, the Producer Price Index is published. The Federal Reserve announces its interest rate decision.

On Thursday, February 15 at 8:30 AM, the Weekly Jobless Claims are announced. We also get Retail Sales.

On Friday, February 16 at 2:30 PM, the January Building Permits are published, along with the University of Michigan Consumer Sentiment. At 2:00 PM the Baker Hughes Rig Count is printed.

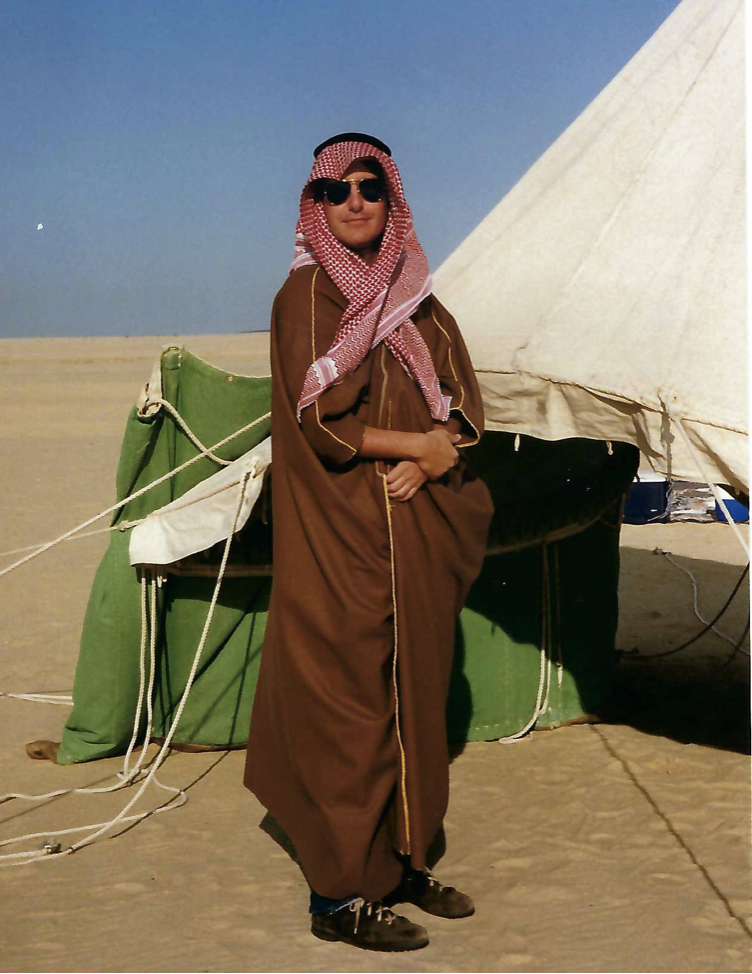

As for me, it was in 1986 when the call went out at the London office of Morgan Stanley for someone to undertake an unusual task. They needed someone who knew the Middle East well, spoke some Arabic, was comfortable in the desert, and was a good rider.

The higher-ups had obtained an impossible-to-get invitation from the Kuwaiti Royal family to take part in a camel caravan into the Dibdibah Desert. It was the social event of the year.

More importantly, the event was to be attended by the head of the Kuwait Investment Authority, who ran over $100 billion in assets. Kuwait had immense oil revenues, but almost no people, so the bulk of their oil revenues were invested in western stock markets. An investment of goodwill here could pay off big time down the road.

The problem was that the US had just launched air strikes against Libya, destroying the dictator, Muammar Gaddafi’s royal palace, our response to the bombing of a disco in West Berlin frequented by US soldiers. Terrorist attacks were imminently expected throughout Europe.

Of course, I was the only one who volunteered.

My managing director didn’t want me to go, as they couldn’t afford to lose me. I explained that in reviewing the range of risks I had taken in my life, this one didn’t even register. The following week found myself in a first-class seat on Kuwait Airways headed for a Middle East in turmoil.

A limo picked me up at the Kuwait Hilton, just across the street from the US embassy, where I occupied the presidential suite. We headed west into the desert.

In an hour, I came across the most amazing sight - a collection of large tents accompanied by about 100 camels. Everyone was wearing traditional Arab dress with a ceremonial dagger. I had been riding horses all my life, camels not so much. So, I asked for the gentlest camel they had.

The camel wranglers gave me a tall female, which was more docile and obedient than the males. Imagine that! Getting on a camel is weird, as you mount them while they are sitting down. My camel had no problem lifting my 180 pounds.

They were beautiful animals, highly groomed, and in the pink of health. Some were worth millions of dollars. A handler asked me if I had ever drunk fresh camel milk, and I answered no. They didn’t offer it at Safeway. He picked up a metal bowl, cleaned it out with his hand, and milked a nearby camel.

He then handed me the bowl with a big smile across his face. There were definitely green flecks of manure floating on the top, but I drank it anyway. I had to, lest my host would lose face. At least it was white. It was body temperature warm and much richer than cow’s milk.

The motion of a camel is completely different from a horse. You ride back and forth in a rocking motion. I hoped the trip was short, as this ride had repetitive motion injuries written all over it. I was using muscles I had never used before. Hit your camel with a stick and they take off at 40 miles per hour.

I learned that a camel is a super animal ideally suited for the desert. It can ride 100 miles a day, and 150 miles in emergencies, according to TE Lawrence, who made the epic 600-mile trek to Aquaba in only four weeks in the height of summer. It can live 15 days without water, converting the fat in its hump.

In ten miles, we reached our destination. The tents went up, clouds of dust rose, the camels were corralled, and the cooking began for an epic feast that night.

It was a sight to behold. Elaborately decorated huge three-by-five wide bronze platers were brought overflowing with rice and vegetables, and every part of a sheep you can imagine, none of which was wasted. In the center was a cooked sheep’s head with the top of the skull removed so the brains were easily accessible. We all ate with our right hands.

I learned that I was the first foreigner ever invited to such an event, and the Arabs delighted in feeding me every part of the sheep, the eyes, the brains, the intestines, and the gristle. I pretended to love everything and laid back and thought of England. When they asked how it tasted I said it was great. I lied.

As the evening progressed, the Johnny Walker Red came out of hiding. Alcohol is illegal in Kuwait, and formal events are marked by copious amounts of elaborate fruit juices. I was told that someone with a royal connection had smuggled in an entire container of whiskey and I could drink all I wanted.

The next morning I was awoken by a bellowing camel and the worst headache in the world. I threw a rock at him to get him to shut up and he sauntered over and peed all over me.

The things I did for Morgan Stanley!

Four years later, Iraq invaded Kuwait. Some of my friends were kidnapped and held for ransom, while others were never heard from again.

The Kuwaiti government said they would pay for the war if we provided the troops, tanks, and planes. So they sold their entire $100 million investment portfolio and gave the money to the US.

Morgan Stanley got the mandate to handle the liquidation, earning the biggest commission in the firm’s history. No doubt, the salesman who got the order was considered a genius, earned a promotion, and was paid a huge bonus.

I spent the year as a Marine Corps captain, flying around assorted American generals and doing the odd special opp. I got shot down and still set off airport metal detectors. No bonus here. But at least I gained an insight and an experience into a medieval Bedouin lifestyle that is long gone.

They say success has many fathers. This is a classic example.

You can’t just ride out into the Kuwait desert anymore. It is still filled with mines planted by the Iraqis. There are almost no camels left in the Middle East, long ago replaced by trucks. When I was in Egypt in 2019, I rode a few mangy, pitiful animals held over for the tourists.

When I passed through my London Club last summer, the Naval and Military Club on St. James Square, whose portrait was right at the front entrance? None other than that of Lawrence of Arabia.

It turns out we were members of the same club in more ways than one.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

John Thomas of Arabia

Checking Out the Local Camel Milk

This One Will Do

Traffic in Arabia

Mad Hedge Technology Letter

September 18, 2023

Fiat Lux

Featured Trade:

(WILL THE TECH IPO MARKET THAW?)

(ARM), (AAPL), (NVDA)

I wouldn’t say that the IPO market is back - hardly not.

There is still a long way to go before the floodgates open, but the ARM IPO is a good start and its successful debut is a good example for others that are sitting off the fence.

British chipmaker Arm (ARM) debuted on the public markets jumping 25% in trading.

The chipmaker's go-public is the most high-profile IPO that the Nasdaq has seen since 2021's IPO boom, which cycled into a bust in 2022.

However, just because these IPOs are moving doesn't mean their valuations are not a sticking point. In Arm's case, the company reportedly sought a valuation of between $60 billion and $70 billion.

Likewise, Instacart — valued at $39 billion at the close of its 2021 funding round — is reportedly now seeking a $9.3 billion valuation.

Arm is a unique company, especially among tech companies. As a chip designer, Arm's customers include some of the biggest names in tech, including Apple (AAPL).

The company has been through a number of transitions over the last several years. In 2016, SoftBank acquired Arm, taking it private for around $30 billion. In 2021, Nvidia (NVDA) attempted to acquire Arm in a deal that failed after regulatory tussling for almost a year and a half.

Recently, Arm has sought to shift its revenue model, altering pricing and rolling out a changed customer licensing strategy.

In short, Arm's return to the public markets was a pivotal moment.

The positive response to this IPO won’t thaw the IPO market completely but will set the stage for 2024 such as payment processor Stripe and computer software provider Databricks.

I will say that the bar has risen significantly for tech firms who want to go public.

Before, many could go public with just hope and dreams with promises of a pot of gold at the end of the rainbow.

This usually meant paltry revenue and massive cash burn at the time of IPO.

Moving forward, it’s obvious that tech companies will need to be more mature to go public and there will be more emphasis on quality management than any time before.

This is because interest rates are still highly elevated and management teams won’t be able to tap the debt markets so easily for a bailout.

Artificial intelligence-related IPOs will also be in an advantageous position to do well post-IPO because that is where the hot money is targeting.

Instead of a slew of capital chasing the new IPOs, I do believe we default back into a rotation of big tech being the safety trade.

Higher bond yield and accelerating tech stocks is an odd couple that appears to be working like clockwork in 2023.

The next spike up in yield could happen soon with the catalyst being the price of a barrel of oil hitting that $100 per barrel mark.

As for ARM, it’s sitting at $56 per share which is down from the $65 per share.

Once the euphoria subsides, wait for a dip in the $40s to buy into ARM, at that price, ARM would be valued at around $50 billion and I would call that a steal for the long-term buy-and-hold readers.

Mad Hedge Technology Letter

October 30, 2020

Fiat Lux

Featured Trade:

(THE TWO CAN'T-MISS CHIP COMPANIES)

(NVDA), (AMD), (XLNX), (ARM)

I want to talk about two companies that are the “no-brainers” of the semiconductor space that would give you a call option on the data center space.

Let’s take a quick look back at some of their latest moves and what it would mean for your tech portfolio.

A few months ago, Nvidia said it would buy British chip company Arm from SoftBank for $40 billion in a stock and cash deal.

CEO Jensen Huang admitted that while the company's acquisition of the rival British chipmaker was a little on the expensive side, it would make sense in the long-term.

“I had to pay you an arm and a leg for it,” the Nvidia CEO said, and “I told you I was going to be the last and highest bidder.”

Overpaying for high quality companies is something that is only possible from a position of strength.

Huang justified Arm’s price tag saying that the chipmaker’s network of customers made it worthwhile and that he wants to expose those customers to Nvidia’s artificial intelligence technology.

Cross-selling the products and services is where the synergies between the companies can be exploited.

AMD is the other player that is really crushing it along with Nvidia and they recently made a deal to acquire Xilinx.

The deal is a direct response to Nvidia’s attempts to become the leader in high performance computing.

Obviously, the acquisitions are made possible because of years of refining their balance sheets and buying into more growth is a time-honored strategy that tech companies focus on.

AMD will give Nvidia a run for their company with a combined additional 13,000 talented engineers and over $2.7 billion in annual R&D investments.

This is very much a talent grab as well as a revenue grab.

Xilinx offers AMD access to adaptive platforms in critical areas such as 5G and automotive.

The tie-up is a transformational opportunity to tap into a total addressable market of $110 billion, up from previous AMD standalone estimates of $79 billion for 2022.

Xilinx adds about $31 billion to the total addressable market and on the operational side, AMD will see gross margins spike from 45% to 51%.

Even more impressive, operating income margins will surge to 21%, up from 16%.

It’s not like AMD needed much help, as they smashed expectations by growing 55.6% and beating estimates by $240 million in the latest earnings report.

EPS beat analyst estimates by $0.06 providing the highest level of earnings in years at $0.41 per share.

The Computing and Graphics division beats estimates with revenues of $1.67 billion.

The ramp-up of new consoles and data center sales led to a mindboggling 101% sequential revenue increase.

The company’s server processor revenue almost doubled compared with the year earlier, and AMD is on track to begin shipping its next-generation server processors later this year.

The current and future status of gaming is very much tied to the fortunes of Nvidia and AMD and the pandemic has fueled massive migration to time spent playing video games.

Who would have thought if people can’t go outside, more video games would be played?

The new generation of consoles is set to launch in November from Microsoft (MSFT) and Sony (SNE) which has helped boost AMD’s gaming chip business.

Typically, this gaming chip segment drops in the fourth quarter, but this year it will mushroom because of the new console launches and ramp-up in production and sales.

Ultimately, in terms of the Xilinx (XNLX) deal, it is complimentary to AMD’s business – an appetizer to the main dish.

It will help improve the company’s ability to support data center customers and adds exposure to sectors such as automotive, aerospace, defense, and industrials.

Through Xilinx’s field-programmable gate array (FPGA) chips—or semiconductors that can be reprogrammed after production, unlike most semiconductors—AMD could benefit from the tail end of the 5G upgrade cycle, too.

That’s because with many emerging technologies, it’s too expensive to experiment with chips with instructions that are set in stone, and build emerging infrastructure such as 5G.

Xilinx’s businesses also tend to retain customers for longer because its strong designs can lead to longer product cycles.

Together, Xilinx and AMD will also operate at a significantly larger scale, which should improve margins and cash flow.

These deals will create a leading supplier of chips for edge-network base stations.

Unlike in the data center market where general-purpose chips win, edge networks require chips that are good at specific things: low-latency, custom-built, specific units.

Those are all things AMD and Xilinx are good at making. Edge computing is a concept that refers to moving processing power and data storage closer to where it’s needed, thus improving performance on local machines.

In short, Nvidia and AMD are the leading lights of the semi-chip industry involved in all the growth industries from artificial intelligence, data centers, video gaming, and self-driving technologies.

I am highly bullish both.