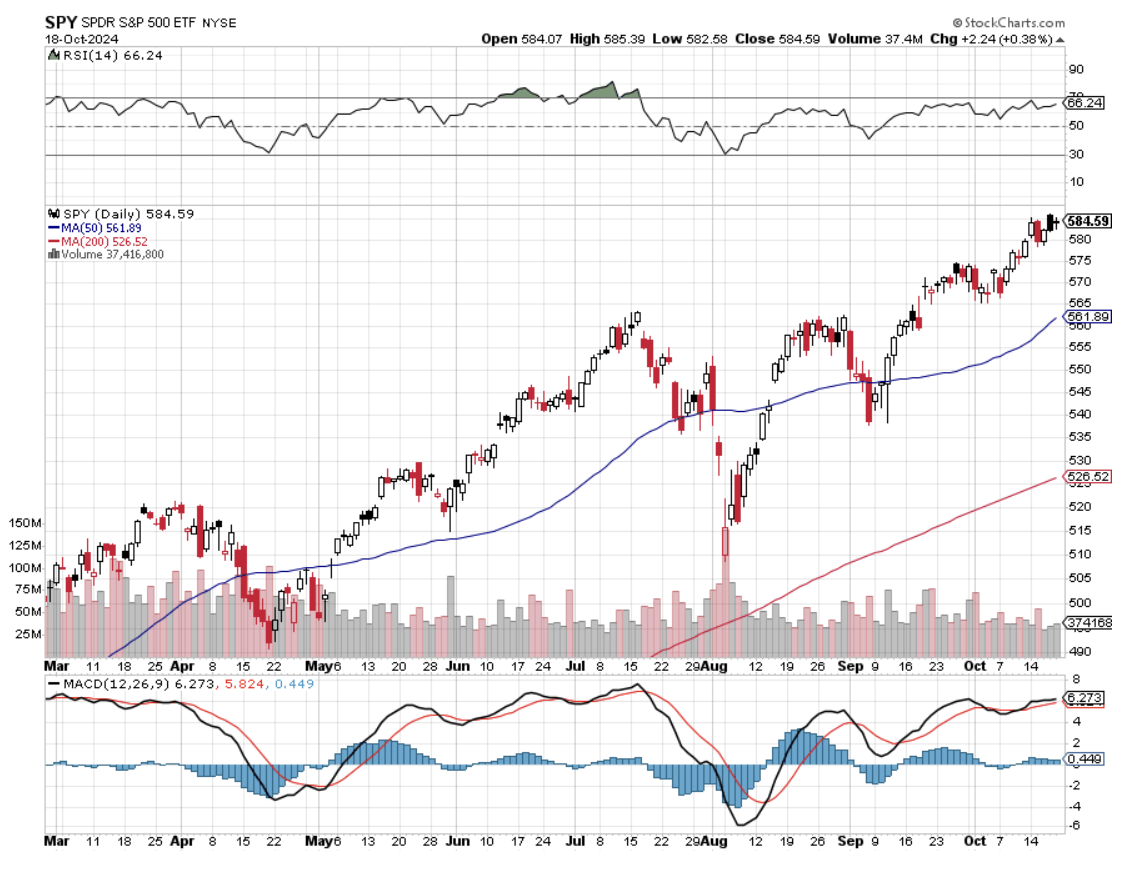

We are now nearly three months into an almost straight-up move in the stock market, and money managers everywhere are scratching their heads. We are now only 136 points or 2.32% from my yearend (SPX) target of 6,000, which is starting to look pretty conservative. The price-earnings multiple for the S&P 500 is now 21X, the Magnificent Seven 28X, and NVIDIA 65X.

I’ve seen all this before.

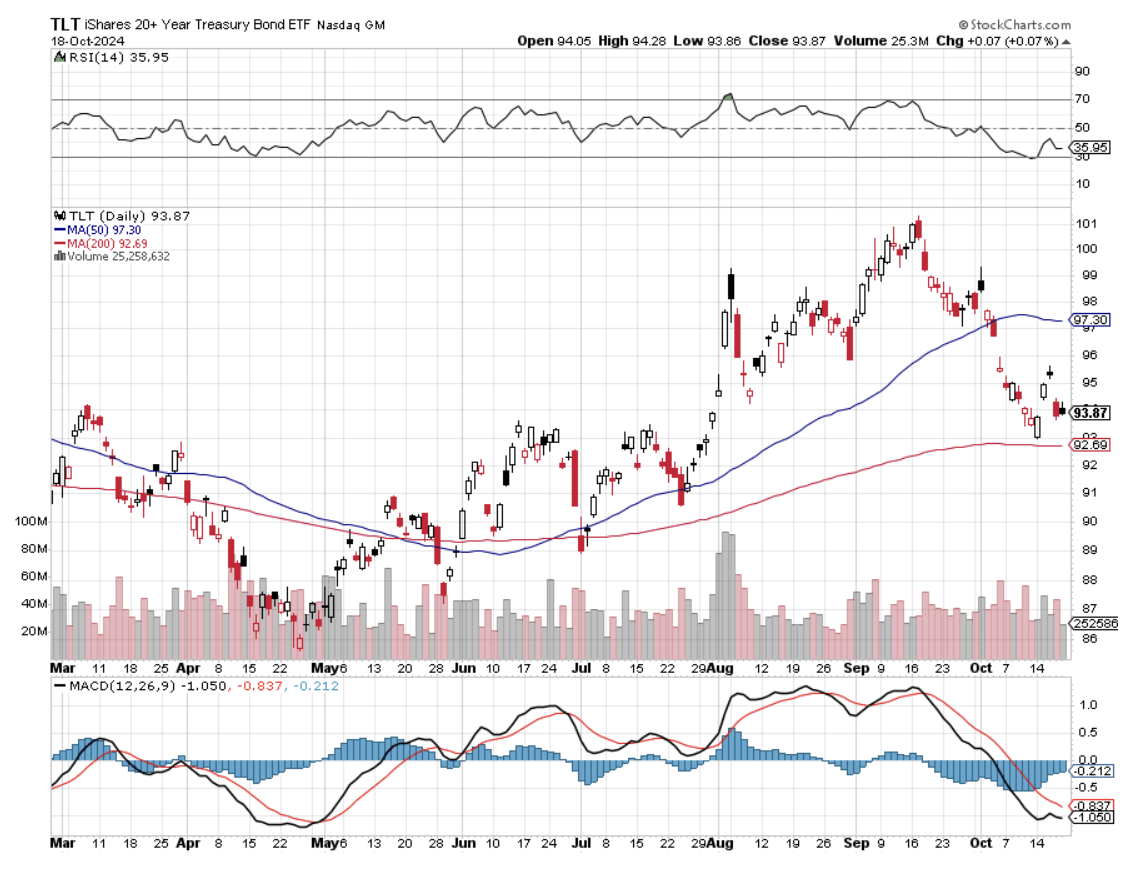

We are about as close to a perfect Goldilocks scenario as we can get. Interest rates and inflation are falling. A 3% GDP growth rate means the US has the strongest major economy and is the envy of the world. We have entered the euphoria stage of the current market move in almost all asset glasses. Gold (GLD) has gone up almost every day. Some big tech remains on fire. Energy prices are in free fall. Even bonds (TLT) are trying to put in a bottom.

Complacence is running rampant.

So, how the heck do we trade a market like this? You play the laggard trade.

The biggest risk to the gold trade is that it has gone up 40% in a year. So, what do you do? The response by traders has been to move into lagging silver (SLV) (AGQ), which has been on a tear since September.

Had enough with the Mag Seven? Then, rotate in the sub $1 trillion part of the market with Broadcom (AVGO), ASML Holdings NV (ASML), Micron Technology (MU), and Lam Research (LRCX).

Tired of watching your DH Horton (DHI) go up every day? Then, flip into smaller homebuilders like Pulte Homes (PHM) and Lennar (LEN).

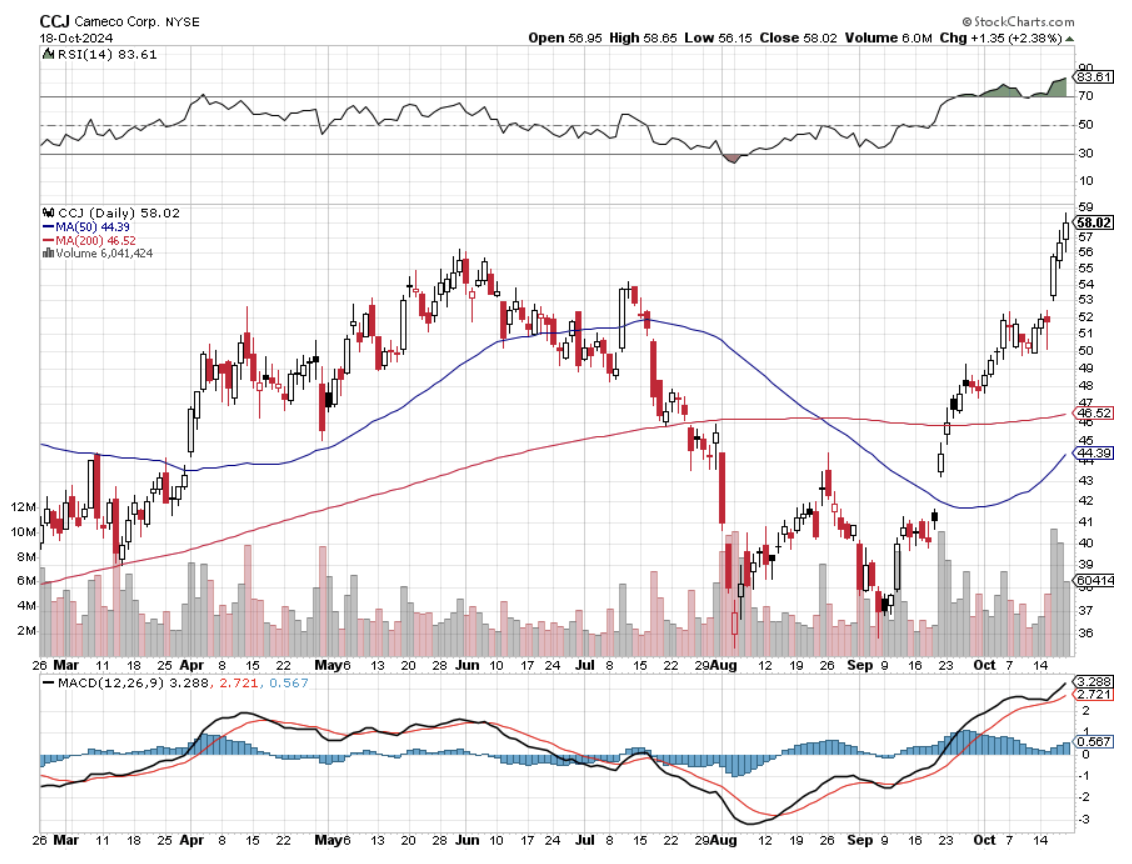

And then there is the biggest laggard of all, the nuclear trade, which is just crawling out of a 40-year penalty box. With news that Amazon (AMZN) was planning to order up to eight Small Modular Reactors to power its AI efforts, all uranium plays continue to go ballistic. The proliferation of power-hungry data centers is driving the greatest growth of power needs since WWII and the Manhattan Project.

Fortunately, I got in early. This is a trend that could become the next NVIDIA, as the public stocks involved are coming off such a low base. I have personally interviewed the founders and examined Nuscale’s plans with a fine tooth come and consider them genius. The company is, far and away, the overwhelming leader in the sector. The puzzle for the pros who understand the technology is why it took so long. Buy (CCJ), (VST), (CEG), (BWXT), and (OKLO) on dips.

It's like everything is racing towards a key, even with an unknown outcome. There happens to be a big one coming up: the US presidential elections on November 6.

Speaking of elections, I took the time to participate in the first day of voting in Nevada on Saturday, October 19, at the Incline Village Public Library. I waited in line for two hours in a brisk and breezy 40 degrees. I wore my Marine Corps cap and Ukraine Army ID just to confuse people. Some got so tired of waiting in the cold that they went home, retrieved their mail-in ballots, and returned to the polls to drop them off.

I looked back on the line, and women outnumbered the men by three to one. Where did all these women come from? There used to be such a shortage of women at Lake Tahoe that it was impossible to get a date. Hunting, fishing, long-distance backpacking, and skiing weren’t used to attract such large numbers of the female gender. Maybe now they do? But now they’re driving up in Mercedes AMG’s and Range Rovers.

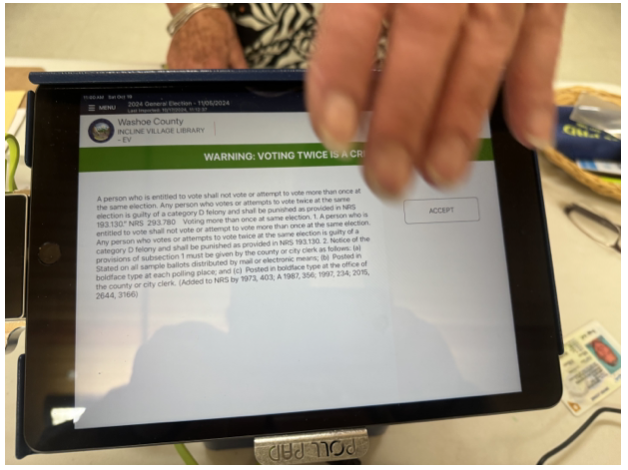

When I finally arrived at the front of the line, I was asked to sign an agreement with my finger, acknowledging that I knew it was illegal to vote twice. The poll worker noticed my ID. When I explained what it was in the Cyrillic alphabet, she burst into tears, apologized, and said she had goosebumps all over.

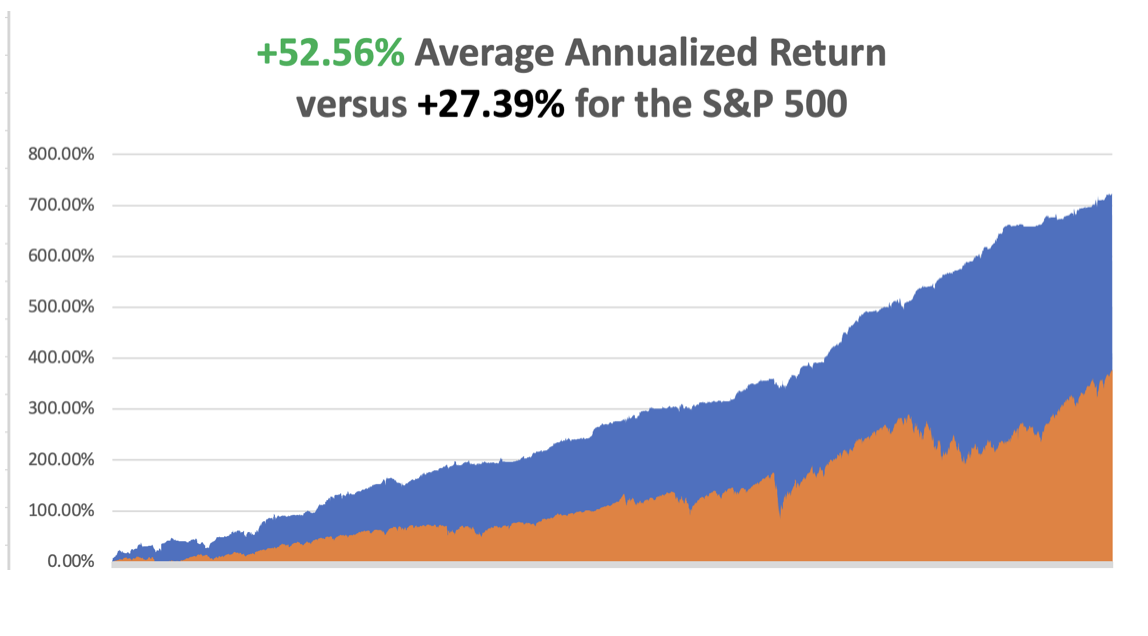

It was another blockbuster week, up over 6%. So far in October, we have gained +4.89%.My 2024 year-to-date performance is at +50.13%.The S&P 500 (SPY) is up +22.43%so far in 2024. My trailing one-year return reached a nosebleed +65.90. That brings my 16-year total return to +726.76%.My average annualized return has recovered to +52.56%.

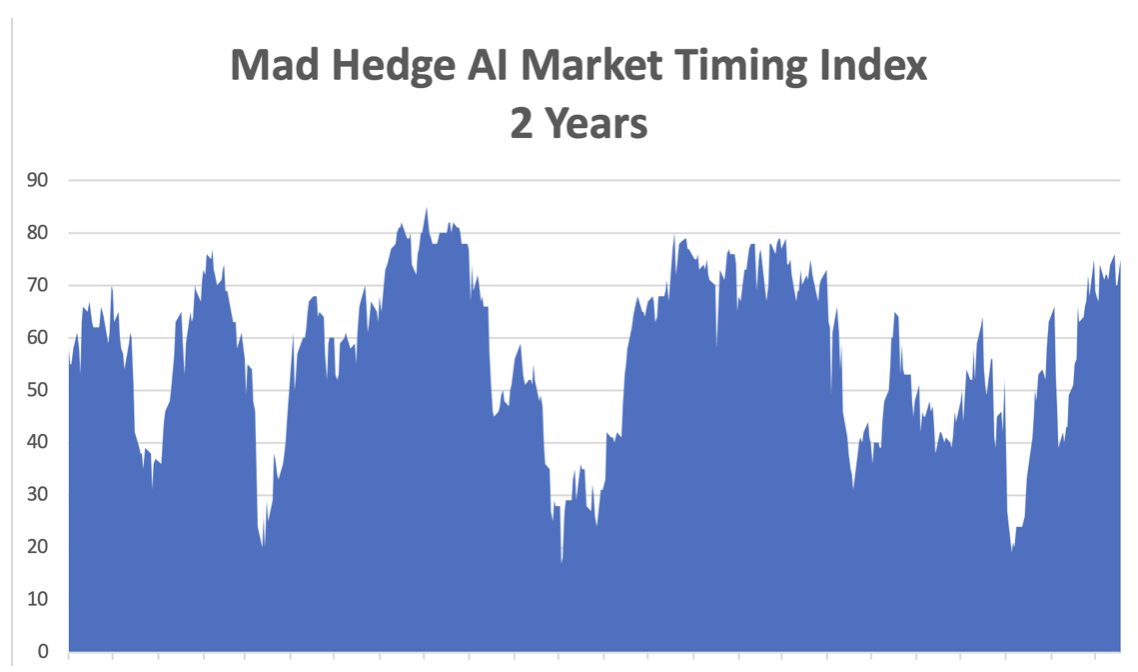

With my Mad Hedge Market Timing Index at the 70 handles for the first time in five months, I am remaining cautious with a 70% cash and 30% long. I look for a small profit in (TSLA) to reduce risk. Two of my positions expired at their maximum profit point for (NEM) and (DHI) on Friday, October 18 options expiration.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 60 of 80 trades have been profitable so far in 2024, and several of those losses were really break-even. Some 16 out of the last 19 trade alerts were profitable. That is a success rate of +75.00%.

Try beating that anywhere.

Risk Adjusted Basis

Current Capital at Risk

Risk On

(TSLA) 11/$165-$175 call spread 10.00%

(JPM) 11/$195-$205 call spread10.00%

(GLD) 11/230-$235 call spread 10.00%

Risk Off

NO POSITIONS 0.00%

Total Net Position 30.00%

Total Aggregate Position 30.00%

Netflix Soars on Blockbuster Earnings, up 11% at the opening on a 5 million gain in subscribers. The company posted earnings per share of $5.40 for the period ended Sept. 30, higher than the $5.12 LSEG consensus estimate.

Crucially, Netflix saw momentum in its ad-supported membership tier, which surged 35% quarter over quarter. The streaming wars are over, and (NFLX) won. Buy (NFLX) on dips.

Silver is Ready to Break Out to the Upside after a year-long-range trade. The white metal is a predictor of a healthy recovery and a solar rebound. It’s a long overdue catch-up with (GLD). Buy (AGQ) on dips.

Apple China Sales Jump 20% on the new iPhone 16 launch. Both Apple and Huawei's (HWT.UL) latest smartphones went on sale in China on Sept. 20, underscoring intensifying competition in the world's biggest smartphone market, where the U.S. firm has been losing market share in recent quarters to domestic rivals. Buy (AAPL) on dips.

Taiwan Semiconductor Soars on Spectacular Earnings, dragging up the rest of the chip sector with it. The world's largest contract chipmaker raised its expectation for annual revenue growth and said sales from AI chips would account for mid-teen percentage of its full-year revenue. U.S.-listed TSMC shares rose nearly 9%, and if gains hold, the company's market capitalization would cross $1 trillion. Buy (NVDA) on dips.

Weekly Jobless Claims Fall. Initial claims for state unemployment benefits dropped 19,000 last week to a seasonally adjusted 241,000 for the week ended Oct. 12, the Labor Department said on Thursday. Economists polled by Reuters had forecast 260,000 claims for the latest week. Claims jumped to more than a one-year high in the prior week, attributed to Helene, which devastated Florida and large swathes of the U.S. Southeast in late September.

Morgan Stanley Announces Blowout Earnings, fueling a 32% profit jump for the third quarter. Revenue from the trading business rose 13%. That followed gains recorded by its biggest rivals as the market business lifted fortunes across the industry, and a steady rebound in investment banking fees increased dealmaking. The wealth unit generated revenue of $7.27 billion, higher than analysts’ expectations, with $64 billion in net new assets. The unit boosted its pretax margin to 28%, driven by growth in fee-based assets. Buy (MS) on dips.

Global EV Sales Up 30% in September, with the largest gains in China. Gains in the U.S. market have been lagging in anticipation of the Nov. 5 election. Chinese carmakers are seeking to grow their sales in the EU despite import duties of up to 45% and amid cooling global demand for electric cars. Chinese and European automakers were going head-to-head at the Paris Car Show on Monday. Buy (TSLA) on dips.

Dollar Hits Two Month High on rising US interest rates. Ten-year US Treasuries have risen from 3.55% to 4.12% since the September Nonfarm Payroll Report. A string of U.S. data has shown the economy to be resilient and slowing only modestly, while inflation in September rose slightly more than expected, leading traders to trim bets on large rate cuts from the Fed. Buy all foreign currencies on dips (FXA), (FXE), (FXB), (FXY).

S&P 500 Value Gain Hits $50 Trillion, since the 1982 bottom, which I remember well and is up 50X. The index hit a record high Wednesday and is trading Thursday at around 5770, up 21% so far in 2024. The index’s value is up sixfold since it stood at $8 trillion at year-end 2008, near the depth of the bear market during the financial crisis.

JP Morgan Delivers Blowout Earnings. Its stock, trading around $223, was on course for its biggest daily percentage gain in 1-1/2 years.

(JPM)'s investment-banking fees surged 31%, doubling guidance of 15% last month. Equities propelled trading revenue up 8%, exceeding an earlier 2% forecast. These earnings are consistent with the soft-landing narrative of modest U.S. economic growth. Buy (JPM) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy is decarbonizing, and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000, here we come!

On Monday, October 21 at 8:30 AM EST, nothing of note takes placeis out. On Tuesday, October 22 at 6:00 AM, the Richmond Fed Manufacturing Index is out.

On Wednesday, October 23 at 11:00 AM, the Existing Home Sales is printed.

On Thursday, October 24 at 8:30 AM, the Weekly Jobless Claims are announced. We also get New Homes Sales.

On Friday, October 25 at 8:30 AM, the US Durable Goods Orders are announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I am headed out for early voting in Nevada this morning. It’s been a year since I came back from Ukraine badly wounded, so I thought I would recall my recollections from that time.

You know you’re headed into a war zone the moment you board the train in Krakow, Poland. There are only women and children headed for Kiev, plus a few old men like me. Men of military age have been barred from leaving the country since the Russians Invaded. That leaves about 8 million to travel to Ukraine from Western Europe to visit spouses and loved ones.

After a 15-hour train ride, I arrived at Kiev’s magnificent Art Deco station. I was met by my translator and guide, Alicia, who escorted me to the city’s finest hotel, the Premier Palace on T. Shevchenka Blvd. The hotel, built in 1909, is an important historic site as it was where the Czarist general surrendered Kiev to the Bolsheviks in 1919. No one in the hotel could tell me what happened to the general afterward.

Staying in the best hotel in a city run by Oligarchs does have its distractions. Thanks to the war, occupancy was about 10%. That didn’t keep away four heavily armed bodyguards from the lobby 24/7. Breakfast was well populated by foreign arms merchants. And for some reason, there are always a lot of beautiful women hanging around with nothing to do.

The population is definitely getting war-weary. Nightly air raids across the country and constant bombings take their emotional toll. Kiev’s Metro system is the world’s deepest and, at two cents a ride, the cheapest. It’s where the government hid out during the early days of the war. They perform a dual function as bomb shelters when the missile attacks become particularly heavy.

My Look Out Ukraine has duly announced every incoming Russian missile and its targeted neighborhood. The buzzing app kept me awake at night, so I turned it off. Let the missiles land where they may. For this reason, I reserved a south-facing suite and kept the curtains drawn to protect against flying glass.

The sound of the attacks was unmistakable. The anti-aircraft drones started with a pop, pop, pop until they hit a big 1,000-pound incoming Russian cruise missile, then you heard a big kaboom! Disarmed missiles that were duds are placed all over the city and are amply decorated with colorful comments about Putin.

The extent of the Russian scourge has been breathtaking, with an epic resource grab. The most important resource is people to make up for a Russian population growth that has been plunging for the last century. The Russians depopulated their occupied territory, sending adults to Siberia and children to orphanages to turn them into Russians. If this all sounds medieval, it is. Some 19,000 Ukrainian children have gone missing since the war started.

Everyone has their own atrocity story, almost too gruesome to repeat here. Suffice it to say that every Ukrainian knows these stories and will fight to the death to avoid the unthinkable happening to them. There will be no surrender.

It will be a long war.

Touring the children’s hospital in Kiev is one of the toughest jobs I ever undertook. Kids are there shredded by shrapnel, crushed by falling walls, and newly orphaned. I did what I could to deliver advanced technology and $10,000 in cash, but their medical system is so backward, maybe 30 years behind our own, that it couldn’t be employed. Still, the few smiles I was able to inspire made the trip worth it. This is the children’s hospital that was bombed a few months ago.

The hospital is also taking the overflow of patients from the military hospitals. One foreign volunteer from Sweden was severely banged up, a mortar shell landing yards behind him. He had enough shrapnel in him, some 250 pieces, to light up an ultrasound and had already been undergoing operations for months. It was amazing he was still alive.

To get to the heavy fighting, I had to take another train ride a further 15 hours east. You really get a sense of how far Hitler overreached in Russia in WWII. After traveling by train for 30 hours to get to Kherson, Stalingrad, where the German tide was turned, is another 700 miles east!

I shared a cabin with Oleg, a man of about 50 who ran a car rental business in Kiev with 200 vehicles. When the invasion started, he abandoned the business and fled the country with his family because they had three military-aged sons. He now works at a minimum-wage job in Norway and never expects to do better.

What the West doesn’t understand is that Ukraine is not only fighting the Russians but a Great Depression as well. Some tens of thousands of businesses have gone under because people save during war and also because 20% of their customer base has fled.

I visited several villages where the inhabitants had been completely wiped out. Only their pet dogs remained alive, which roved in feral starving packs. For this reason, my major issued me my own AK47. Seeing me heavily armed also gave the peasants a greater sense of security.

It’s been a long time since I’ve held an AK, which is a marvelous weapon. It’s it’s like riding a bicycle. Once you learned, you never forget.

I’ve covered a lot of wars in my lifetime, but this is the first fought by Millennials. They post their kills on their Facebook pages. Every army unit has a GoFundMe account where doners can buy them drones, mine sweepers, and other equipment.

Everyone is on their smartphones all day long, killing time, and units receive orders this way. But go too close to the front, and the Russians will track your signal and call in an artillery strike. The army had to ban new Facebook postings from the front for exactly this reason.

Ukraine has been rightly criticized for rampant corruption, which dates back to the Soviet era. Several ministers were rightly fired for skimming off government arms contracts to deal with this. When I tried to give $10,000 to the Children’s Hospital, they refused to take it. They insisted I send a wire transfer to a dedicated account to create a paper trail and avoid sticky fingers.

I will recall more memories from my war in Ukraine in future letters, but only if I have the heart to do so. They will also be permanently posted on the home page at www.madhedfefundtrader.com under the tab “War Diary”.

Donating $10,000 to the Children’s Hospital

On the Front at Crimea with a Dud Russian Missile

A Gift or Piroshkis from Local Peasants

One of 2,000 Destroyed Russian Tanks

The Battle of Kherson with my Unit

This Blown Bridge Blocked the Russians from Entering Kiev

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-10-21 09:02:412024-10-21 12:00:25The Market Outlook for the Week Ahead, or Complacence is Running Rampant

Computer chip equipment maker ASML said they will cut 2025 financial guidance, citing weakness in markets other than AI and delayed orders.

This triggered a steep sell-off in many chip names, and I view this as a healthy event.

We are bombarded with so much robust news from the chip sector that it is hard for investors to catch their breath before the next spike higher in underlying shares.

Once in a while, it is highly positive to recalibrate momentum and allow the stock to settle.

Chips are definitely boom-and-bust stocks, and we are right in the middle of the boom. and I wouldn’t be too worried for other chip companies as we head into earnings.

This is a great chance to buy the dip in many of the best of class.

Europe's most valuable technology company, ASML, as an essential supplier to chipmakers, is not in question. But doubts have emerged over short-term sales and, for the longer term, whether it can continue to outgrow the overall market.

ASML's dominance of the market for lithography tools needed to create circuitry triggered the stock to all-time highs before this recent weakness.

After the health crisis of the early 2020’s, customers stopped overbuying, which reduced demand.

Now, ASML said some customers had announced delays of new plants and upgrades, including makers of the logic chips used in smartphones, PCs, and other devices.

Manufacturers that make the memory chips that go into them also plan fewer expansions, meaning they can rely on existing equipment for longer.

That's especially the case for an upstream equipment supplier highly reliant on the spending plans of its manufacturing customers.

It’s highly likely that Taiwan Semiconductor was the company who decided to cut back on business with ASML.

TSMC has been spending rather low capex numbers so far this year, and they may do so again next year because their overall (plant) utilization is not as good as their sales numbers suggest.

Among ASML customers that make logic chips, Intel said in August it would cut capital spending by $10 billion in 2025, while Samsung has said it faces challenges at the factory it is building in Texas.

Roughly a quarter of chipmakers' spending on tools goes to ASML, though some analysts say changes in chip-making techniques could lead that to be lower.

Management also said that customer delays are also a negotiating tactic that may force pricing concessions from ASML, squeezing margins.

Ultimately, this is a temporary demand adjustment after years of outperformance, and I would allow the seasonality to work itself through the system.

I see no threat to the overall business model of ASML, and if bad news on ASML triggers hits to other great chip stocks, I would look at some short-term bull call spreads on strong chip stocks in the US.

At the very least, if you don’t buy the dip, don’t take the other side of the trade because, more often than not, this type of price action sets up a “rip your face off” rally to the upside.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-10-16 14:02:152024-10-16 14:52:44The Chip Trade Is Still In-Tact

I hit the nail on the head – I’ll take another victory lap and you’re welcome.

I’ve been telling all my subscribers.

Apple backing off production of the new iPhone 14s signals that the US consumer is tapped out.

Throw in the towel!

What does that mean?

At the low-end, US consumers don’t have the extra funds to pay for all the streaming services or the extra hardware, gizmos, and gadgets they are used to.

That means the iPhone 14 Pro is next to get squeezed from the budget after an eye-watering $1,500 pretax price tag. At least at that price point, it includes 1 TB of data storage, but no charger.

Personally, I acknowledge that Apple makes a pretty darn good smartphone, but it’s way too overpriced in 2022 and there aren’t enough improvements to justify the lofty prices.

But the killing of new iPhone production goes well beyond just the issue of global sales of smartphones, this is a harbinger of things to come as global economic growth goes from bad to worse.

This is also legit confirmation that inflation is not only transitory, but it’s terrorizing US consumers’ budgets.

Interestingly enough, the most expensive models did still see high demand, confirming what I already have been saying is that high income US consumers are navigating elevated inflation more than superb even if conditions aren’t ideal.

Because they are in good shape – great personal financial balance sheets – hope it stays that way.

Thus, Apple supplier is shifting production capacity from lower-priced iPhones to premium models.

High income households are passing on their costs to the end consumers in the companies they run, and they are jacking up rents in the condos they let out.

They are even hitting up Walmart more than usual and abstaining from pricier options like Whole Foods or Whole paycheck.

Fantastically, high income Americans are ready to spend, spend, spend and that’s great news for employers and employees, but bad news for the bond market.

Apple is cutting the iPhone 14 product family by as many as 6 million units in the second half of this year.

Instead, the company will aim to produce 90 million handsets for the period, roughly the same level as the prior year and in line with Apple’s original forecast this summer.

In Taipei, key chipmaker Taiwan Semiconductor Manufacturing Co. (TSM) fell 2.2% and Apple’s biggest iPhone assembler Hon Hai Precision Industry Co. (HNHPF) was down 2.9%, amid a wide selloff of electronics suppliers.

ASML Holding NV (ASML), maker of advanced chipmaking gear, dropped as much as 3.2% in Amsterdam.

Purchases of the iPhone 14 series over its first three days of availability in China were 11% down on its predecessor the previous year.

Readers must be aware of Apple being the biggest component of the S&P. When Apple goes, so does the market.

Then there is the issue of, maybe the phones just suck now, since each iteration is the trigger for higher expectations which aren’t really met anymore.

Either way, CEO Tim Cook needs to roll up his sleeves, and this report ostensibly means that Apple won’t return to 2022 highs anytime soon.

It also vindicates and confirms that we are still in a sell the rallies mode or buy the dip after deep selloffs mode. This is a short-term traders' world right now and the data backs me up.

Happy trading!

https://www.madhedgefundtrader.com/wp-content/uploads/2022/09/apple-phone.png6901220Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-28 16:02:112022-09-29 03:09:36Chickens Come Home to Roost

As the bear market rally picked up steam Tuesday with even Cathy Wood’s growth ETF (ARKK) gaining 9%, it’s clearly a reaction to the Nasdaq repricing its biggest underlying risk.

The market is now pricing in a global recession and that has replaced inflation as the number one worry for investors.

This new development has led to the Nasdaq sniffing out the return to the bad news is good news effect.

That is why the U.S. 10-year treasury yield cratered from 3.5% to 2.8% which reflects the future expectation of a pulled-forward global recession.

This would trigger a fresh interest rate lowering cycle by global central banks.

Lowering rates is good for Nasdaq stocks and tech stocks will be a big beneficiary of lowered rates as they have overshot to the downside on this rate rise cycle.

That doesn’t mean it’s all rosy in the land of the Nasdaq, hardly so.

We are still in the fog of war and amid improving technical data like lower oil prices, worsening economic relations between the large nuclear-equipped countries are not only moving the world towards a soft technological decoupling but a hard fracturing of general relations.

My first thought was will China finally strike back against the United States in the form of destroying Tesla’s (TSLA) Gigafactory in Shanghai or blacklist Apple (AAPL) iPhones in China.

These two events would be the point of no return for the two countries’ economic cooperation and anything beyond that, relations could spiral out of control rapidly and even be the impetus for a Taiwan takeover.

Clearly, Silicon Valley does much better when the world is getting along, and everyone is paying for their stuff.

That can’t happen as smoothly with the world rapidly balkanizing which is a big reason for massive selloffs in Netflix whose international audience has soured.

On the production side of things, Chinese-produced stuff won’t be able to get sold back to Americans using Guangdong factory production as semiconductor chips and equipment have become the focal point of national security efforts.

The US has placed export controls against Chinese technology firms from purchasing chips and equipment.

Now Biden is blackmailing the Netherlands to ban one of its top chipmakers from selling semiconductor equipment to Chinese companies.

The Biden administration is pushing hard for Dutch chip equipment maker ASML Holding NV (ASML) to halt selling some of its older deep ultraviolet lithography, or DUV, systems.

Even though these machines are one generation behind cutting-edge, they offer high-tech chips for automobiles and consumer electronics.

Washington has also pressured Japan to stop shipping semiconductor machines to China.

Since the Trump tariffs, China has been the biggest buyer of chipmaking gear for the last two years.

On the European front, regulation is hitting home hard as the U.K. has initiated investigations on Amazon’s selling practice by in-house brands and is looking into Microsoft’s anti-competitive acquisition of Activision.

If American tech companies have nowhere to produce, nobody to acquire for instant growth, and nobody to sell to then it becomes a massive issue for shareholders.

Even though the equity mojo boost of good news is bad news is a nice reprieve, a global recession where many companies fire staff and can’t sell their product because lack of parts is worse.

Therefore, we are still issuing a sell the rallies in tech type of recommendation to our readers while acknowledging there has been a small wave of dip buyers entering back into the game.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-07-06 16:02:362022-07-06 16:30:07Good News Is Bad News

If you thought you missed profiting off of Amazon then you’re in luck; you still have another chance with the South American iteration of Amazon – MercadoLibre (MELI).

This e-commerce and payments platform in Latin America boasts presence in 18 countries within South and Central America but derives the bulk of its revenue from three countries: Brazil, Argentina, and Mexico.

MELI is the entrenched e-commerce player in the region and has multiple retailer solutions such as MercadoLibre Marketplace (an online platform for the buying and selling of merchandise), Mercado Pago (an online payments solution), and Mercado Envios (a logistics solution).

The company's market-leading position revolves around a strong network effect that has allowed it to expand its exploding user base as well as its gross merchandise volume (GMV).

In 2015, MELI had around 145 million registered users, and that number has more than tripled by 2020.

The tectonic shift toward digital transactions network caused by the pandemic means the number of items sold jumped 66% year over year to 284 million, and the number of unique active users climbed 27% year over year.

It’s undeniable that the company has strong tailwinds backing its overarching story.

MELI was already primed for a strong growth trajectory before the pandemic crushed the global economy.

The company was savvy in introducing new and useful services over the years to solve digital bottlenecks, and its suite of services made customers stickier toward its platform.

Hosting an integrated e-commerce and payments platform meant an unrelenting buildup of new vendors and users coming on board over time.

MELI looks set to take the next step in e-commerce penetration.

Although its growth has been phenomenal over the last decade, I believe the company may be on the cusp of doubling its growth rate because of the rapid digitalization by businesses.

A share repurchase program has been set in motion and I do believe they will dip into this financial tool once the global economy stabilizes.

Getting into the weeds, MELI expanded its category-take rates to Chile and Mexico in Q2 2020, with Brazil and Argentina set for last half of 2020.

For online marketplaces like what Amazon and eBay offer, the take rate refers to the fees and commissions that the companies collect on sales by third-party sellers which is critical to overall revenue.

The successful take rate rationalization could drive sellers to list more of their inventory and reduce prices.

With this increased supply, MELI should be seeing the cascading benefits of an improving shopping experience and rising conversion rates.

Scaling this beautifully translates to lower per-unit logistic costs such as sequential 23% decrease in unit shipping costs.

Ala Amazon, its drive to step up the buildout of its own logistics network to take down the dependency on Correios in Brazil is yielding meaningful results and also places the company to potentially buttress a greater amount of free shipping subsidies as the unit cost of deliveries continues to swan dive.

Logistics transforming into a higher reliability, faster shipping times, and greater cost savings offering can be passed along to the consumer upgrading the quality of service.

Soon, MELI is expected to invest in Consumer Electronics and price competitiveness could see the company grab market share taking down yet another adjacent industry.

At some point, like Amazon, MELI will target the grocery market and will have the logistic infrastructure in place to do the same type of 1-day “free” shipping that Amazon guarantees.

On the digital payments side of the business, MELI has sold over 1 million mobile point-of-sale (mPOS) devices, versus 900,000 during Q1 2020, driven primarily by smaller merchants.

The individual bull case for MELI is rock-solid but feeling out the global state of affairs is a must in a quickly changing environment.

With an onslaught of stimulus in Europe and the U.S. to deal with the pandemic, China’s economy beginning to recover, and a weaker dollar, foreign markets are becoming more attractive to U.S. investors.

Emerging markets could turn from stock market pariah to darling in a nanosecond and if investors are comfortable with targeting companies in higher growth markets, then MELI should be an option.

Emerging markets broadly have lagged behind developed market peers over the past decade, even as some fund managers have found investing in domestically-oriented companies in India, China, or Brazil hugely rewarding—just look at the outperformance by foreign brand names like Alibaba Group (BABA), Meituan Dianping and HDFC Bank (HDFC) in India just to name a few.

It’s true that more developed markets have the advantages of greater trading liquidity, minimal systemic risk, better corporate governance, and greater access to dollar-denominated debt that emerging markets’ companies don’t benefit from.

Therefore, investors seeking a conservatively biased portfolio should only focus on U.S. tech brand names that have moats around their business model.

Another second derivate play would be to find U.S. tech companies that siphon a big chunk of sales in emerging markets and are U.S. companies like Apple (AAPL), Nvidia (NVDA), and Mastercard (M).

Each secures between one-third and two-thirds of sales from emerging markets. But with those companies vulnerable to the geopolitical trip wire between the U.S. and China, proportioning a small amount of the portfolio to a Latin American tech growth firm could produce alpha.

Another quick recommendation is ASML, a semiconductor chip company from the Netherlands.

It’s an option generating outsized sales coming from emerging markets but is headquartered in an economically responsible country.

This Dutch tech firm boasts positive free cash flow yields, a sign the company is generating ample cash to operate and also reinvest in itself.

Investors who can stomach greater risk levels and desire growth should take a serious look at MELI, plus the myriad of other tech recommendations I offered if MELI doesn’t suit your appetite.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-10-05 11:02:572020-10-06 15:08:10The Amazon of Latin America

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.