Mad Hedge Technology Letter

February 12, 2019

Fiat Lux

Featured Trade:

(MEET YOUR HOME OF THE FUTURE),

(KASITA),

(PLEASE SIGN UP NOW FOR MY FREE TEXT ALERT SERVICE NOW)

Mad Hedge Technology Letter

February 12, 2019

Fiat Lux

Featured Trade:

(MEET YOUR HOME OF THE FUTURE),

(KASITA),

(PLEASE SIGN UP NOW FOR MY FREE TEXT ALERT SERVICE NOW)

Mad Hedge Technology Letter

February 11, 2019

Fiat Lux

Featured Trade:

(HOW FORTNITE IS TAKING OVER THE GAMING WORLD),

(TTWO), (EA), (ATVI), (NFLX), (FORTNITE)

One idyllic content company reshaping the content landscape as we know it is Epic Games who is the producer of the video game phenomenon Fortnite.

Not only is Epic Games rapidly altering the video game industry by itself, it is also starting to take a bite out of Netflix’s subscriber growth momentum.

The company was established by Tim Sweeney as Potomac Computer Systems in 1991, originally founded in his parents' house in Potomac, Maryland.

The most fascinating nugget of information that came out of Netflix’s most recent earnings call was not that Netflix has already corralled 10% of television screen time in America, but the reason why this percentage is lower abroad is because of Fortnite taking away Netflix’s mojo.

Netflix (NFLX) has lately been asked to measure their content lead to the likes of Hulu, HBO, and the potential Disney streaming product about to hit the market.

But they explicitly confessed they were more worried about Fortnite and the revolution it is spawning.

The key takeaway is that Netflix is not only competing with fellow online content streamers, but video games are more of a threat to them than ever as they compete for the cord cutters and the elusive “cord nevers”.

Cord nevers are consumers who are digital natives who bypassed traditional media channels altogether.

Echoing the stickiness that Netflix has with its younger demographics, the company has targeted mobile screen time as a core driver usurping around 8% of American mobile phone screen time.

And if you thought Netflix was trying to sort out its own Fortnite problem, then how do you think the traditional American video game cohort felt about their own Fortnite problem?

The traditional trio of EA Sports (EA), Activision (ATVI), and Take Two Interactive (TTWO) have been shredded to bits by Fortnite.

Late last year, I gave readers a steer clear synopsis of this company and the latest dead cat bounce in EA and Take Two Interactive should be chances to cut your losses instead of putting more money to work in these names.

Yes, the momentum in Fortnite is that palpable that you stay away from any name that this phenomenon affects.

Activision had no dead cat bounce being the weakest of the three and the stock has gone awry almost halving from $83 to $43 today.

EA’s earnings report was a disaster with their lead title, Battlefield V, doing 1 million fewer sales than the 7.3 million management expected.

During the same holiday season, Take Two Interactive issued a follow-up to a classic that was better than EA’s holiday flagship game called Red Dead Redemption 2 and Activision rolled out another iteration of Call of Duty: Black Ops 4.

Even between the three, the competition was fierce, then throw Fortnite into the mix and comps are getting killed with huge earnings misses penalizing the share prices of this once-vaunted trio.

With the explosion of content in the past several years, consumers are absorbing more content than ever.

Most of this avalanche of content is consumed on mobile phones or televisions, but the behavior varies when you look closer at the different demographics.

Cord cutters total in the low 20 million and are growing 30% annually.

Cord nevers amount to about 30 million growing at 66%.

This all amounts to Americans spending about 12 hours accessing content every day running up to the barrier of natural limits.

That might give consumers some allocated time to sleep, eat, and work, but not much else. We are robotically reliant on content providers to deliver us our fill of daily content.

When automotive technology comes online, it could potentially eke out an incremental 1-2 hours that Americans can stare at their content while being chauffeured around.

How is Fortnite doing financially?

Fortnite earned $2.5 billion in 2018 from a mix of in-game items and passes.

A seasonal Battle Pass is $10, and over 30% of American gamers have purchased this product.

Unlike traditional video gamers who are tied to certain consoles, Fortnite is available on seven platforms: PlayStation 4, Nintendo Switch, Xbox One, PC, Mac, iOS, and Android.

In a time of $60 video games, this new freemium model must shake the foundations of the video gaming establishment.

The rise of freemium games could eradicate the console completely.

A $200-300 console seems expensive if games are free on your $100 Android phone.

The worst side-effect of Fortnite for the traditional video game producers is not Fortnite itself.

It’s the fact that this new model has opened up a new can of worms proving this freemium model with no consoles is the key to unlocking gaming audiences with a 24-hour battle royale, free to play, on-demand, in-game currency, season pass model that was thought to be a hopeful wish by industry analysts.

Then the next question is when will the next Fortnite-esque freemium go viral and can these legacy gaming companies alter their model to accommodate this new business model?

Indeed, management must be freaking out. They thought they had a monopoly on the gaming industry but the nimbler and forward-thinking firm has won-out.

Even the most subscribed YouTuber PewDiePie from Sweden is using Fortnite to keep him in the lead for most YouTube subscribers as Indian music YouTube channel T-Series has caught up with his subscriber count that currently totals 84.3 million.

PewDiePie’s lead was cut down to 20,000 and decided to leverage playing Fortnite squad matches to boost his subs.

The upload got over seven million views in a day backing up my thesis that Fortnite has become the hottest media content asset for cord cutters and cord nevers around the world.

As for the video game stocks, don’t touch them until Fortnite trails off.

And if another freemium game comes to the fore that they aren’t on, run for the hills.

Mad Hedge Technology Letter

December 12, 2018

Fiat Lux

Featured Trade:

(WHY GAMERS ARE TAKING OVER THE WORLD)

(EA), (TTWO), (ATVI), (GME), (MSFT)

I nailed it.

The video game migration has been nothing short of bonkers for the average onlooker who has no interest in gaming.

Personally, I can’t really fathom spending every waking moment in front of a screen playing a game, but I was born in a different generation.

But for the younger generations, this is completely normal and a standard way to use extracurricular time.

This behavior is the origin hewing together a broader thesis of investing in behemoth video game companies boasting premium gameplay and high-quality content.

As the year inches closer to the finish line, I would have been proved correct if it wasn’t for one surprise that nobody could have ever predicted.

Enter Fortnite.

Fortnite has reigned supreme in 2018 and single-handedly tarnished the performance of the powerful trio of Electronic Arts (EA), Activision Blizzard (ATVI), and Take-Two Interactive (TTWO).

The multiplayer battle royale game is produced by Epic Games, an American video game developer based in Cary, North Carolina and this small town in Chatham County owns the video game world right now.

Funnily enough, the company was created by Tim Sweeney in 1991 in his parents' basement in Potomac, Maryland.

Epic Games blindsided the video game industry who believed barriers of entry were too high, and an outsider would have no chance to steal legitimate market share from the incumbents.

They thought wrong because Epic Games has done exactly that and more.

Instead of splurging on a pricey console and game titles, Fortnite has followed the cloud industry’s blueprint with a freemium model as an introductory way to lure in new users.

This must have Sony and Microsoft tearing their hair out because it could potentially rule the Xbox One and PS4 consoles obsolete.

How easy is it to play Fortnite?

Simply download and install the game for free on your Xbox One, Nintendo Switch, PlayStation 4, iPhone, Android, or Mac by opening the respective app store and selecting “Fortnite.”

That’s right, you can play this game on almost any platform appealing to the masses of fans.

Does this freemium model mean that Epic Games misses out on revenue?

Absolutely not.

The freemium model is just the conversional entry point to lure in new gamers.

Epic Games profits by selling in-game currency named V-Bucks or Vinderbucks used for purchasing items from the in-game Vindertech Store in Save the World, or to pocket cosmetic items from the Item Shop and the Battle Pass in Battle Royale.

V-Bucks revenue has been piling up with global gamers spending an average of $1.23 million per day in the iOS version for the month of November.

The number of total gamers recently eclipsed the 200 million mark and the previous recorded number was in June when Fortnite users totaled 125 million.

The 60% surge in five months has been the main catalyst for large video game makers to experience violent sell-offs because there is a direct correlation between growing Fortnite users and cratering usership from the traditional players.

Then throw in the mix of the secret recipe to Fortnite’s success - the mind-numbing speed and impact of the online updates enhancing the game; adding and adjusting weapons, providing new cosmetic items for players to buy and altering the game map.

Not only did Epic draw in new players in waves, it retained them just as well.

Putting the cherry on top, Fortnite made major cultural inroads into mainstream society legitimizing this title as the game of 2018.

This was evident during the Russia FIFA World Cup where star soccer players were doing Fortnite dances after scoring critical goals.

Put it this way, the game hasn’t even been allowed in China and is expected to earn over $2 billion in 2018.

As we speak, millions more plan to migrate from their former games enticed by the free battle royal platform.

The game is nothing short of a cultural phenomenon and none of the major video game developers can keep up.

Take-Two Interactive even had a smash hit come online with Red Dead Redemption 2, a Western-themed action-adventure game developed and published by Rockstar Games, lighting up screens all over the world.

Not even that could taper off the enthusiasm for Fortnite.

Activision cannot keep its gamers from jumping ship.

The mainstay game developer announced a major contraction of users from 345 million monthly active users for top games in its Candy Crush, World of Warcraft and Call of Duty franchises in the third quarter sharply down from 352 million users in the second quarter and 384 million users a year ago.

GameStop (GME) who recently slashed its full-year 2019 earnings outlook faces a grim 2019 as shares are down about 25% this year.

I perfectly predicted this and in almost every scenario, GameStop’s future looks ugly unless they do some major surgery to the business model.

There is no room for video game brokers anymore in this cloud-based world.

This is because new game studios will follow the Epic Games blueprint and bypass consoles all together and offer games for free.

The cloud will be the new go-to device for playing video games, and gamers will download games straight from the cloud via wireless broadband.

This trend is set to mushroom when 5G comes online in 2019 and 2020, connection speeds are expected to be 100 times faster than current 4G speeds.

In fact, the new consoles currently being developed by Nintendo, Microsoft, and Sony could be the last game consoles ever developed before they go extinct.

The digital revolution promises that hardware becomes incrementally slimmed down with every iteration until at some point there will be no hardware at all.

We have seen this trend in consumer devices with the smartphone, television, and desktop computer amongst other products.

This is why Microsoft (MSFT) has been busy buying up video game content producers, and confident in this sense that gold standard content truly is king.

It makes sense to put in more irons in the fire to potentially score a culture-shifting game like Fortnite. Not every video game will be a blockbuster hit, but the more video game developer Microsoft buys, there will be a higher chance of dominating the video game market.

Fortnite’s disruption of Activision, EA, and Take-Two Interactive signals a new beginning of the end for the traditional video game developers.

Darkhorse game developer could sprout up out of nowhere even more in 2019 offering console-less free games and leaner, nimbler models.

How are console manufacturers and game developers expected to keep up with the surge in gaming expectation?

The answer is they will not and look for these big three developers to attempt to stem the bleeding as Fortnite is expected to become even more thrilling next year tearing away more gamers from other systems in a dog-eat-dog world.

And then there is the possibility of the FANGs crossing over to gaming, searching for new growth drivers which would really flatten these shares like a pancake.

Microsoft is already deep into this industry, why wouldn’t their cousins follow them to profits too?

Ultimately, I am bearish on Activision, Electronic Arts, and Take-Two Interactive going into 2019 unless there is an upside catalyst that magically appears.

At our weekly Monday staff meeting, coworkers were griping and grimacing about their failed internet connections and annoying glitches to their favorite e-commerce sites during the mad rush to find the best deal during Black Friday and Cyber Monday.

Internet traffic was that torrential when sites were driven offline for minutes and some, hours by a bombardment of gleeful shoppers hoping to splash their credit card numbers all over the web on sweet discounts.

The crashing of system servers epitomizes the robust transition to online commerce that has most of us pinned to our devices surfing our go-to platforms all day long.

According to data from Adobe (ADBE) analytics, Black Friday sales jumped 23.6% YOY to $6.22 billion, and it was the first time in history that mobile sales broke the $2 billion threshold.

It is a clear victory for e-commerce and, in particular, mobile shopping that has become more integrated into modern tech DNA.

Mobile sales comprised 33.5% of total sales and were up from 29.1% last year, signaling that more is yet to come from this transcending movement that is shoving everything from content, digital ads, entertainment, banking and pretty much everything you can think of to your handheld smartphone.

CEO of Kohl’s (KSS) Michelle Gass confirmed the e-commerce strength by saying, “80 percent of traffic online came from mobile devices.”

The beauty of this movement is that it’s not an “Amazon (AMZN) takes all” scenario with other players allowed to feast on a growing size of the e-commerce pie.

“Click and collect” has been a strategy that has paid off handsomely with sales up 73% YOY during the shopping holidays.

This all supports my prior claim that e-commerce is one of the most innovative and dynamic parts of technology especially the grocery space, and the buckets full of capital attempting to reconfigure the e-commerce spectrum is creating an enhanced customer experience for the final buyer resulting in better products, superior delivery methods, and cheaper prices.

Some other retailers spicing up their e-commerce strategy are dinosaur big-box retailer’s intent to defend their business from the Amazon death star.

If you can’t innovate in-house, then “borrow” the innovation from somewhere else.

That is exactly what Target (TGT) has chosen to do announcing last week that it would grant free 2-day shipping with no minimum sale threshold.

The tactic is bent on undercutting Walmart (WMT) who currently operate a 2-day free shipping policy with a minimum order of $35.

Most shoppers will buy in bulk easily eclipsing the $35 per order mark minimizing the rot of small orders.

And if they aren’t eclipsing the $35 per order mark, it demonstrates the firm’s offerings lack the diversity and quality to compete with Amazon.

Capturing the incremental sale squarely rests on the e-tailers ability to coax out the buyers’ impulses to move on the can’t-miss items.

The lesser known retailers fail miserably at matching the lineup of products that Amazon can roll out.

The bountiful product selection at Amazon leads customers to pay for 3, 4, 5, 6 or more items on Amazon.com.

That said, I am bullish on Walmart’s e-commerce strategy. The “click and collect” strategy has shown to be an outsized winner increasing industry sales of this type 120% YOY.

Walmart is at the center of this strategy and they are refurbishing their supercenters to accommodate this growth in collecting from the curb.

Effectively, this gives customers the option to skip the queue instead of bracing the hoards and navigating the crowds of shoppers in the supercenter.

Other changes are minor but will help, such as offering online product location maps to customers beforehand and allowing customers to pay for large items like big-screen televisions on the spot.

The biggest windfall is derived from the cataclysmic demise of Toy “R” Us, giving Walmart a new foothold into the toy business.

Walmart is beefing up toy items by 40% in the stores and layering that addition with another 30% increase in their e-commerce division.

Adobe’s upper management recently said in an interview that interactive toys have been a wildly popular theme this year amid a backdrop of the best holiday shopping season ever recorded.

Another attractive gift selling like hotcakes are video games, titles boding well for sales at Activision (ATVI), EA Sport (EA), and Take-Two Interactive (TTWO).

Reliant IT infrastructure will be a key component to executing these holiday sales bonanzas.

Clothing retailer J. Crew and home improvement chain Lowe's (LOW) were grappling with sudden disruptions to their IT systems before they managed to get back online.

More than 75 million shoppers parade the internet to shop during Black Friday and Cyber Monday, and the opportunity cost swallowed to a tech glitch is a CEO’s worst nightmare.

Ultimately, what does this all mean?

Focusing on the positive side of the surging holiday sales is the right thing to do because the avalanche of momentum will have a knock-on effect on the rest of the economy.

Certain companies are positioned to harvest the benefits more than others.

Amazon guided its 4th quarter estimates conservatively and is in-line to beat top and bottom line forecasts.

Other pockets of strength are Walmart’s tech pivot, albeit from a low base. Walmart still has more room to maneuver and they are in the 2nd inning of their tech transformation snatching the low-hanging fruit for now.

Another interesting e-commerce company swinging its elbows around is Etsy (ETSY).

They sell vintage and handmade craft adding the personalized touch that Amazon can’t destroy.

Margins will be higher than the typical low-cost, value e-commerce platform, but scaling this type of business will be more difficult.

Sales grew 41% sequentially and just in time for a winter holiday blowout.

Etsy became profitable in 2017 after three straight loss-making years, and 2018 is poised to become its best year ever.

The profitability bug is hitting Etsy at the perfect time with its EPS growth rate up 36% sequentially.

They report at the end of February and I expect them to smash all estimates.

There are some deep ramifications for the long term of e-commerce that is beginning to suss itself out.

For one, shipping times will continue to be slashed with a machete. If you are enjoying the 2-day free shipping from Amazon and Target now, then wait until 2-day becomes 1-day free shipping.

Then after 1-day free shipping, customers will get 10-hour shipping, and this won’t stop until goods are shipped to the customer’s door in less than 1-hour or less.

This is what the massive $50 billion in logistical investments over the next five years by the likes of Uber and Amazon are telling us.

It will take years for the efficiencies to come to fruition, but it is certainly in the works.

In the next five years, America’s logistics infrastructure will have to accommodate the doubling of e-commerce packages from 2 billion to 4 billion per year.

Another trend is that omnichannel offerings are sticking and won’t go away anytime soon.

It was once premised that online sales would destroy brick and mortar, yet moving forward, a mix of different sales channels will be the most efficient way of moving goods in the future.

Pop-up stores have been an intriguing phenomenon of late, and surprisingly, 60% of consumers still require interaction with the product to be convinced it's worthy of buying.

Certain products such as fashionable dresses and designer shoes must be given a whirl before a decision can be made. This won’t change anytime soon.

The timing of the sales and marketing push has been moved forward as competitors are eager to get a jump on one another.

Management is agnostic to the timing of the sale.

Thus, discounted sales will show up a week before Thanksgiving as pre-Thanksgiving sales in the future elongating the holiday shopping season cycle by starting it early and delaying the finish of it.

Lastly, the record numbers prove that the e-commerce renaissance and the pivot to mobile is not just a flash in the plan.

What does this mean for tech equities?

The temporal tech sell-off of late is largely a result of outside macro forces and is not indicative of the overall health of the tech sector that has experienced record earnings.

If the markets can keep its head above the February lows, it sets up an intriguing December fueled by Americans flashing their digital wallets on online platforms.

Mad Hedge Technology Letter

November 21, 2018

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO SELL SHORT ON THE NEXT RALLY)

(WDC), (SNAP), (STX), (APRN), (AMZN), (KR), (WMT), (MSFT), (ATVI), (GME), (TTWO), (EA), (INTC), (AMD), (FB), (BBY), (COST), (MU)

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

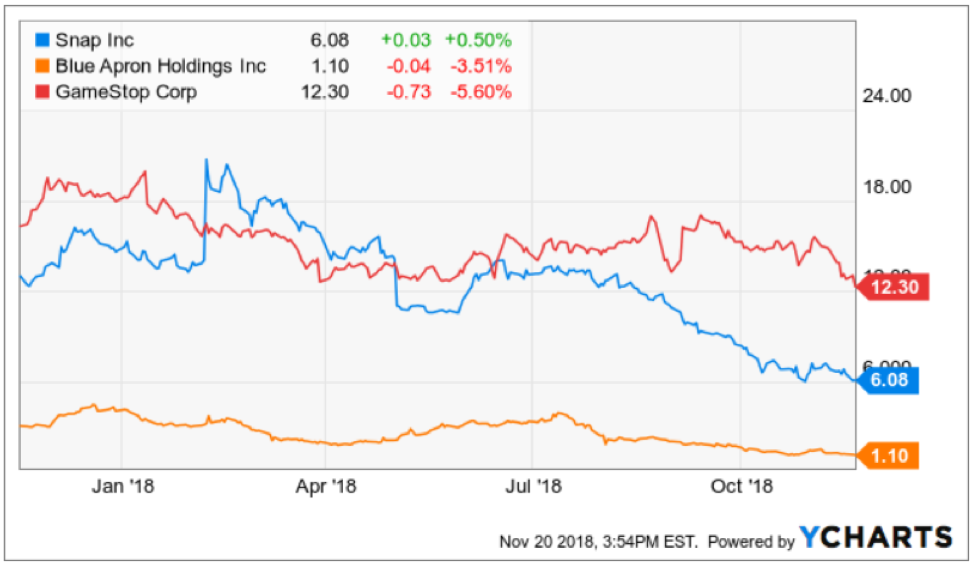

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.

Mad Hedge Technology Letter

September 4, 2018

Fiat Lux

Featured Trade:

(READY PLAYER ONE’S INSIGHT INTO THE FUTURE OF TECHNOLOGY),

(MSFT), (SQ), (TTWO), (AMD), (NVDA), (EA), (ATVI), (PYPL), (GOOGL), (FB)

The technology-laced film Ready Player One gives viewers a snapshot into the future where technology, income inequality, and society have run their course, and the year 2045 looks vastly different from the world of 2018.

Set in a semi-dystopian backdrop, the movie offers us a deeper insight into how certain technology trends will permeate into everyday life.

The first and most obvious future trend is the copious use of avatars.

Avatars will become the new normal. The first place that humans will find them is through the use of social media and entertainment, as children eventually becoming a part of us like our social media profiles today.

The Mad Hedge Technology Letter has incessantly hammered home about the phenomenon of gaming, and this will incorporate virtual reality allowing gamers access to a new digital world.

This was the on show in the film where the likes of protagonist Wade Watts, played by Tye Sheridan spent most of his life playing in the virtual world of Oasis using his character Parzival.

This could be your child in the future.

Wade Watts character is the new cool for Generation Z, as they are largely unconcerned about underage drinking and partying like the generations before them.

Gaming and hanging out on their preferred social media platforms are the new cool.

The companies dictating the current video game industry will have the first crack at it to realize profits and develop new businesses such as Microsoft (MSFT), Nvidia (NVDA), Advanced Micro Devices (AMD), Electronic Arts Inc. (EA), Take-Two Interactive Software, Inc. (TTWO), and Activision Blizzard, Inc. (ATVI).

Children just aren’t going outside like they used to and per most studies, they are addicted to the smartphone you bought them at age 10.

Most studies have found that once a child becomes hooked on technology, it is hard to reverse the habit, as once they enter into adult life and start their career, they become even more reliant on the technologies that got them to that point in the first place.

If your kid is already staring at tech devices three to four hours per day now for activities other than school work, expect that to grow to a minimum of six to seven hours per day once he hits puberty and smartphone time limits begin to fade away.

This all means that VR and gaming could be the handsome winner in all this, and the use of social media platforms will reap the benefits as well.

Generation Z just surpassed Millennials in terms of population comprising 25% of the American populace.

Neither of these generations have grown up with VR in their daily lives because the technology wasn’t advanced enough to really make a dent in their lives.

More than 75% of Generation Z has access to a smartphone, and they can truly be called the first generation of digital natives.

Avatars will push deeper into everyday life because the facial tracking technology has advanced by leaps and bounds.

Instead of cartoon-like avatars, lifelike avatars have replaced the less refined versions. It will be a tough time going forward distinguishing what is real and what is fake.

If you think fake news is a problem now, imagine how fake it will become in the future.

This could devastate the news industry as news organizations run the risk of melting down at any point, or just being completely taken over by tech companies and their algorithms, which is already happening now with Alphabet (GOOGL).

The future looks bleak for all newspaper assets, and the ones with the most advanced digital strategies will survive.

Newspapers only have so much time they can hang on with digital ad revenue, the reason they are still in business.

Viewers don’t want to see ads – period. And at some point, they will be disrupted as well.

Swashbuckling youth already have downloaded ad-blockers to completely remove ads from their lives, and refuse to open any website that forces them to white list a website.

There are children in Generation Z who might never have seen an ad before because their digital native capability allows them to navigate around ads with adept skill.

Or the easy solution for many Millennials is just watch Netflix because the platform is ad-less. The aversion to ads is so strong that traditional media giants such as Fox are experimenting with six-second ads because that is all a viewer can tolerate these days.

The traditional media giants were forced to adopt this new format after Alphabet’s YouTube rolled out micro-ads.

Popular browser Mozilla announced it will block all tracking scripts by default beginning in 2019, thwarting unregulated data collection and relentless ad pop-ups.

The reason why digital ads will have an existential crisis is because companies will be able to monetize the pure data, forcing companies with huge digital ad businesses such as Facebook (FB) to battle with the new competition that only wants your data and not hawk ads.

This is already happening in the e-brokerage space with disruptors such as Robinhood, which charges no commission and is more interested in collecting data and getting by with interest payment revenue.

Let’s face it, digital ads are not a high-quality business even though they are a high-margin business. As tech moves forward, the quality of tech will rise eliminating all low-grade tech that is still profiting in 2018.

On the business side of things, automation is replacing humans faster than humans realize, and the replacement will be an avatar representing the face of a company.

For lower-end services, an avatar chosen by the customer will populate to often give better service than a human can provide.

If this type of service is scaled, it would offer a massive cut in costs for American corporations saving on employee costs.

It will have the same effect that self-checkout kiosks have at supermarkets, wiping out another position at the low-end.

The front-end avatar that will service you is all possible because of the rapid advancement of artificial intelligence.

Every possible situation will be programmed in the software and executed briskly.

If customers desire the human touch, they will have to pay up.

Human interaction will command a premium price because human interaction cannot be automated.

The financial industry has a huge target on its back, and swaths of financial advisors could be sacked in favor of avatars with the functional software behind it to produce profits.

In fact, many financial advisors are instructed to refrain from recommendations now and urged to collect input to enter into a proprietary algorithm that will decide the customers’ portfolio.

Big banks have enjoyed their time in the sun, but technology will disrupt them in the near future. This is why you have seen huge run-ups in innovative fintech companies such as Square (SQ) and PayPal (PYPL).

Many forms of outside entertainment are on the chopping block, as well as indoor entertainment such as Hollywood.

Hollywood A-list actors command hefty premiums to contract their services, and that could all crumble if younger audiences prefer avatar-based films with the human roles performed by unknowns.

Johnny Depp earns more than $50 million for one movie, and these insane amounts could deflate rapidly if human participation in films becomes marginalized.

Ready Player One was a test case for how much technology could be infused into a movie, and the audience easily absorbed it.

I could argue that audiences could argue even more in this VR format.

The movie had a budget of $175 million, and returned $582 million at the box office.

The resounding success will encourage more directors to inject technology into their movies, and they will have to, if they hope to tempt younger audiences to the movie theater.

Going to the movie theater is another activity that has struggled to cope against the rise of Netflix and technology.

Theaters have been forced to improve the overall experience of watching a film with prime seating, comfortable seats, and other extras that never existed.

Every industry is going through the same headache of competing with technological disruption.

Stagnation is akin to surrendering in 2018.

And it wasn’t just a fringe director creating Ready Player One, it was visionary director Steven Spielberg, one of the most famous movie directors to ever exist.

This will pave the way for other lesser-known movie directors relying on technology to pump out the profits.

They wouldn’t be the first people or the first industry to go down this road either.

________________________________________________________________________________________________

Quote of the Day

“The worst thing a kid can say about homework is that it is too hard. The worst thing a kid can say about a game is it's too easy,” – said American media scholar Henry Jenkins III.