Mad Hedge Technology Letter

January 22, 2024

Fiat Lux

Featured Trade:

(TAKE A DEEP BREATH WITH AI)

(NVDA), (QRVO), (GOOGL), (AMZN), (AMD), (AVGO), (AAPL), (AI)

Mad Hedge Technology Letter

January 22, 2024

Fiat Lux

Featured Trade:

(TAKE A DEEP BREATH WITH AI)

(NVDA), (QRVO), (GOOGL), (AMZN), (AMD), (AVGO), (AAPL), (AI)

Stocks and firms tethered to artificial intelligence won’t always have a one-way joyride to profits.

The honest truth is that the road will be met with drawbacks some years and the sector will need time to digest the new developments.

Mainstream tech has made most people believe that AI can do no wrong in the short-term future.

There is a consensus that it’s the panacea for everything and anything.

The Magnificent 7 tech firms are priced for an AI boom and the hype is there, but it will take some time for AI to really filter into meaningful balance sheet development.

We are still in the beginning stages.

It’s not surprising that the Massachusetts Institute of Technology published a study that sought to address fears about AI replacing humans in a swath of industries and found that artificial intelligence can’t ACTUALLY replace the majority of jobs right now in cost-effective ways.

It’s important to note this report because much of AI has been celebrated with no mention of cost control or benefit versus the price or expenses incurred.

Any corporate tech will need to evaluate whether it’s worth gutting whole divisions to replace it with AI.

In many cases in early 2024, this type of strategy to a workforce could turn into an unmitigated disaster.

For instance, a new AI study found only 23% of workers, measured in terms of dollar wages, could be effectively supplanted. In other cases, because AI-assisted visual recognition is expensive to install and operate, humans did the job more economically.

The adoption of AI across industries accelerated last year after OpenAI’s ChatGPT and other generative tools showed the technology’s potential. Tech firms from Microsoft and Alphabet in the US to Baidu and Alibaba in China rolled out new AI services and ramped up development plans which could serve as a canary in the coal mine for things to come. Fears about AI’s impact on jobs have long been a central concern.

Computer vision is a field of AI that enables machines to derive meaningful information from digital images and other visual inputs, with its most ubiquitous applications showing up in object detection systems for autonomous driving or in helping categorize photos on smartphones.

The cost-benefit ratio of computer vision is most favorable in segments like retail, transportation, and warehousing.

The study was funded by the MIT-IBM Watson AI Lab and used online surveys to collect data on about 1,000 visually assisted tasks across 800 occupations. Only 3% of such tasks can be automated cost-effectively today, but that could rise to 40% by 2033 if data costs fall and accuracy improves.

When getting academic about the subject, many projections feel way too ambitious.

AI won’t take over the workforce in the next few years and will struggle to make inroads before 2030.

That doesn’t mean firms like Nvidia, AMD, Qorvo, and Broadcom will not sell AI-based chips promising better AI.

That doesn’t mean firms like Google, Apple, Microsoft, Amazon, and Meta won’t feel a small AI bump in revenue.

There certainly will be some changes, but wholesale transformation is a ways off.

I believe the AI hype has gotten too far over its skis.

Tech needs to slow down and make sure it’s properly implemented and the real effects will be seen after 2030.

Mad Hedge Technology Letter

January 19, 2024

Fiat Lux

Featured Trade:

(ANOTHER CHIP NAME BESIDES NVIDIA)

(AVGO), (AAPL), (AI)

Broadcom (AVGO) has gone through several major transformations since its founding in 1991, and a chart of the stock looks like a hockey stick.

AVGO is now worth close to $600 billion and the show isn’t over yet folks, there is more yet to come.

AVGO has a history of buying growth using debt.

Prior to buying Broadcom, Avago had already acquired a long list of smaller companies to expand its portfolio of wireless, optical, and data storage chips.

By paying $37 billion for Broadcom, it gained even more mobile, networking, wireless, and industrial chips. That inorganic growth strategy made it one of the world's largest chipmakers.

Broadcom subsequently expanded into the infrastructure software market by buying CA Technologies in 2018, Symantec's enterprise security division in 2019, and the cloud software giant Vmware in 2023.

Those acquisitions should diversify its business away from the cyclical semiconductor market and curb its dependence on Apple, which still accounted for 20% of its revenue over the last two fiscal years.

Growth in the 20% range should be driven by three long-term catalysts.

First, the expansion of the generative artificial intelligence (AI) market should trigger stronger sales of its data center and infrastructure chips over the next few years.

Second, its sales of chips to mobile and IT infrastructure customers should heat up again as the macro environment improves.

Apple also signed a new blockbuster deal to buy Broadcom's 5G radio frequency components and other wireless connectivity components for several more years last May, so it won't lose its top semiconductor customer anytime soon.

Broadcom's aggressive expansion strategies have been lucrative, but the sprawl could weaken the company. If that happens, investors will be a lot less forgiving of its rising debt and dilution.

I fully expect strong double-digit revenue growth in the company's AI-related businesses.

I anticipate a proliferation of Gen AI across a broad set of data center workloads to drive strength in Broadcom's custom compute offload and next-generation Networking businesses both in the near- and medium term.

There is also a strong chance of a cyclical recovery in the company's non-AI business.

In addition, I expect synergy capture following the acquisition of VMware, to drive operating margin expansion and earnings growth well in excess of the industry average.

The last lever that will affect stock appreciation will come in the form of shareholder returns.

I do believe that AVGO will ramp up the dividends as revenue accelerates.

Profits went from around $11.5 billion 2 years ago to $14 billion last year.

It’s easy to see the chip company blow by $16 billion this year as well.

It is well on its way to becoming a trillion-dollar company.

I do believe they will reach that goal around 2030.

The stock has more or less gone parabolic and now sitting around $1,200 per share.

It’s been like that for a while now.

Any dip to around $1,100 or $1,000 would be classified as a buying opportunity.

Mad Hedge Technology Letter

November 13, 2020

Fiat Lux

Featured Trade:

(HOW TO STOP THE E-CRIMINALS)

(CRWD), (AVGO)

Cybersecurity is not a discretionary purchase for corporates.

This must-have product soothes the minds of every cybersecurity executive in the world.

I’ll explain how this point of strength is capitalized on by major growth security tech company CrowdStrike (CRWD).

Let me put my stamp on this indispensable service keeping cloud services afloat.

I can say with conviction that this is the beginning of a multi-year trend being driven by the industry consolidation that took place last year along with the seismic shift to cloud technologies.

Fortune 500 companies are increasingly choosing CrowdStrike as their security cloud platform.

CrowdStrike customers have never been larger and have never bought more modules and the same type of optimism appears in the stickiness of the number of new customers that surpass annual recurring revenue (ARR) of over $1 million.

Cybersecurity is mission-critical to both the public and private sectors.

Endpoint or workload security is also essential to protecting a remote workforce and as many of you know, the global remote workforce has never been bigger because of the pandemic.

While the damage to the macroeconomy from the coronavirus is gyrating at an accelerated pace, it is forcing companies to conduct business differently and rapidly shift to a remote workforce.

With CrowdStrikes’ cloud-native platform, this lightweight agent is easily deployed at scale and its frictionless go-to-market engine, CrowdStrike is uniquely positioned to meet any type of cybersecurity requirement.

The financial performance of the company is as healthy as ever as the company added a record $99 million in net new ARR and year-over-year, they increased the number of net new subscription customers by 116%, achieving 90% subscription revenue growth and 89% total revenue growth.

There were three outsized achievements this year: CrowdStrike delivered exceptional growth at scale, significantly improved margins, and achieved positive free cash flow for the fiscal year.

The seismic shift to cloud-native technologies and cloud workloads including containers has created an environment with massive greenfield opportunities.

Many competitors are dragged down by the complexities of integrating acquired technologies, rationalizing their workforce, or retooling their on-prem offerings.

Another positive tailwind is when Broadcom (AVGO) began integrating Symantec, there was a nice increase in inquiries among both customers and partners because they simply didn’t like Broadcom’s new products and vacated them to move towards CrowdStrike’s offerings.

This dynamic will contribute to an expansion in CrowdStrike’s pipeline, an acceleration in the overall customer adoption and increased engagement with partners.

Several partners in the United States and abroad have launched Symantec replacement campaigns as well but I believe CrowdStrike offers some of the most robust products.

One company submitted a list of several thousand of their customers that will be migrating away from Symantec in the next year and there was very little overlap between these prospects and CrowdStrike’s existing customer base.

The customer base has more than doubled and now protects the safety of 5,431 customers.

870 net new customers in Q4 joined CrowdStrike, which is up 136% year-over-year.

Chief Information Officers (CIOs) and Chief Information Security Officers (CISOs) are looking for a strategic partner to help them bridge this skills gap and simplify their operations, while at the same time, reducing cost.

They are also looking for ways to leverage enhanced automation in their security operations to increase efficacy and free up resources.

These organizations are increasingly rotating capital to CrowdStrike’s Falcon platform to protect an array of workloads, stop breaches, and restore system performance.

All new customers increased average number of modules in every quarter this past fiscal year.

The percentage of all subscription customers with four or more modules once again increased and those that adopted five or more cloud modules grew to one-third of their customer base.

As customers adopt more modules that span a wide array of workloads, it strengthens the customer relationship and increases CrowdStrike’s strategic position with the customer.

Companies who pay for other security alternatives keep running into the same roadblock of patchwork vendors who are largely ineffective and bureaucratic.

The burden is then directly placed on their resource-constrained IT security team eroding performance and souring team morale.

Another big problem is that a large percentage of the corporate platforms are not on the latest build of Windows, they could not update to newer versions exposing them to malware and security malfunctions.

This result is a cumbersome, manual remediation process and often requires the security team to reach out to users directly dragging out any possible IT solution.

CrowdStrike simply has this covered and can replace all three endpoint security solutions with the Falcon platform and offer seven modules providing firms with comprehensive protection and visibility in their environment and freeing up internal resources.

Existing legacy vendor failing is a common problem, and they fall victim to malicious activity shutting down production at major international facilities.

The ability to deploy the solution quickly can save the customer millions in manufacturing line productivity losses.

Beyond the immediate value provided by remediating a breach, there is significant value realized by streamlining a security stack. With the Falcon platform, firms can eliminate more than ten legacy tools and considerably improve their visibility and security posture.

CrowdStrike is collecting customers across diverse industries, geographies, and size because of proven efficacy and stopping breaches, and its cloud-native platform and lightweight single agent that is easily deployed at scale.

The predictive power of AI-driven threat graph that gets smarter the more data it consumes means the products get better with age.

The coronavirus has done nothing to dent the insatiable trend of companies searching for better security solutions.

While the coronavirus is having an impact on the global economy, it will not stop cyber adversaries. Cybersecurity provides business resiliency and meets compliance requirements.

In times of crisis, adversaries will try to exploit the situation, prey on the public's fear, and escalate new attacks.

I know it's difficult to fathom, but we've already seen nation-state adversaries from rogue regimes and e-criminals launch phishing campaigns using coronavirus marketing as clickbait entrance mechanism.

The world of global business is certainly not naïve in 2020 and tech investors shouldn’t be too.

CrowdStrike is still a small company but its growth trajectory is a sight to behold and every dip should be bought on the back of their solid business model.

Mad Hedge Technology Letter

September 23, 2019

Fiat Lux

Featured Trade:

(THE COMING REVOLUTION IN 5G)

(MSFT), (TSM), (AVGO)

5G is overhyped but that doesn’t mean everyone will be a loser.

The shift to fifth-generation wireless technology, or 5G, will offer investors numerous compelling investment opportunities.

It has been predicted that 5G phone shipments will rise from 17 million this year to 130 million in 2020 and 327 million in 2021.

However, on the flip side of it, 5G, especially for the technically astute consumer and at current prices, is oversold.

At least for 2020.

Some percentage of teens and students will want to watch movies and play high-bandwidth games on their phones but when they discover the data costs, they will retreat from such purchases.

Also, many who hype 5G aren't aware of the technical limitations especially for those outside of certain metro areas.

It could turn out to be a vanity buy for some or most.

It will benefit businesses, of course, but not the majority of the cell phone market. Certainly not in the US.

Even for me, everything I use on my smartphone wouldn’t need 5G.

If there is no noticeable effect, then do consumers really need this technology?

I would say not until something more comes out that requires us to need 5G and I do not see that on the horizon.

Back in the world of the stock market, many analysts understand that RF (radio frequency chip) supply chain companies are compelling in their new growth opportunities for 5G phones.

Even if many consumers do not need 5G, many device makers will splurge on their supply chain to get there, meaning chip companies who sell 5G components will gain.

The marketing of 5G entails the standard hyping-up of the shift to 5G.

And industry participants would say it is substantially important to the semiconductor and telecom industries, but it will take time to absorb on the consumer side.

Analysts expect 5G to deliver speeds 10 to 40 times faster than current 4G LTE networks. Its lower latency promises to enable new applications from augmented reality and automated factories to self-driving and cloud gaming.

But as I referenced above, there are only a handful of consumers that need cloud gaming and augmented reality.

Automated factories work with the current speed of technology and in a global slowdown, corporates will want to wait for a healthier environment to initiate a new CAPEX cycle.

Here are some chip stocks that supply chain could benefit from.

Taiwan Semiconductor Manufacturing (TSM) is a stock with thematic drivers that can potentially benefit from the upcoming 5G renaissance and global supply chain shifts.

TSM has a large foundry and advanced chip-making technology leadership.

Broadcom (AVGO) will also become a vital winner of 5G smartphone adoption while supplying specialized processors for 5G front and back haul.

Broadcom will supply chips to both Apple and Samsung for their 5G smartphones.

The rapid run of chip shares could have more to go for the end of the year as investors have front-run chip stocks for the past few months.

However, I do believe that the downdraft in smartphone demand and connected devices will hurt the end product sales.

Consumers will hold off on buying 5G-supported Huawei, Samsung, and Apple products, meaning chip stocks could stall out after this nice run.

Global Market Comments

September 10, 2019

Fiat Lux

SPECIAL ARTIFICIAL INTELLIGENCE ISSUE

Featured Trade:

(NEW PLAYS IN ARTIFICIAL INTELLIGENCE),

(NVDA), (AMD), (ADI), (AMAT), (AVGO), (CRUS),

(CY), (INTC), (LRCX), (MU), (TSM)

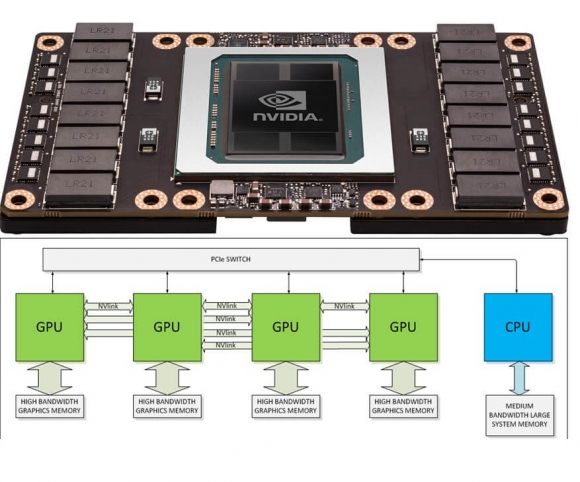

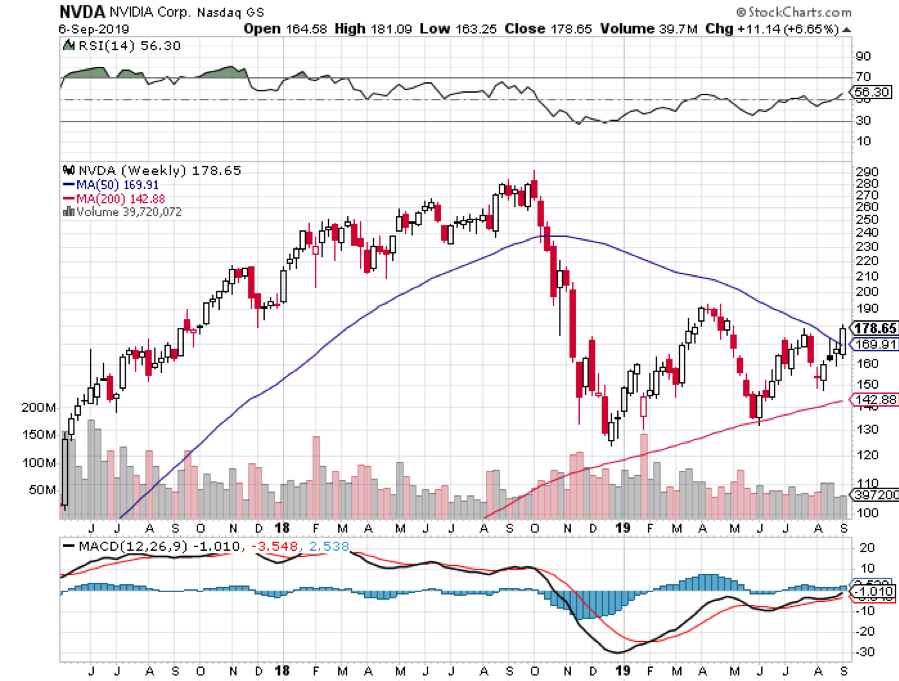

It’s been three years since I published my first Special Report on artificial intelligence and urged readers to buy the processor maker NVIDIA (NVDA) at $68.80.

The stock quadrupled, readers are understandably asking me for my next act in the sector.

The good news is that I have one.

For a start, you could go out and buy NVIDIA again.

With an explosive 50% annual earnings growth, a near-monopoly in super fast processors, and a huge lead over the competition, I think there is another double in the shares that could take the price up to a stratospheric $300. Its newest super-fast graphics card, the Turing, promises to be a real barn burner and dominate the industry yet again.

But I can do better than that.

The good news if you are new to this sector is that the entire AI space has started to broaden out to offer a host of investment opportunities beyond the tiny handful I first mentioned in 2016.

These include legacy chipmakers, survivors of the great Dotcom bust, whose shares have barely moved in years.

Yes, there is such a thing as a cheap AI stock. To find out who they are, read on.

The reason for the expansion of the AI sector is that practically overnight these ultra-sophisticated algorithms have become essential to any company that wants to survive in online commerce or stay in business….period.

Those of us who have been in this business for more than 15 minutes have seen this pattern before, and the resulting impact on share prices: the Boeing 707, the personal computer, Windows, the Internet, and the smart cell phone.

AI is everywhere.

In the old days, visiting a website and window-shopping their products was easy. You just clicked around a few times and then moved on to the next site.

Now if you click on a product once, that site will follow you around relentlessly for months, appearing in the margins of your emails, offering you endless discounts and special deals.

I bought a Dell computer six months ago, and it is still pounding away at me with better offers. I feel like such a dummy buying a machine at the first price asked.

That is all AI.

The auto industry is now a major growth industry for AI. Even a simple garden-variety vehicle needs 100 chips just to operate.

The gull-wing doors on my new Tesla Model X each has its own learning program. They never open the same way twice.

In fact, when I first picked up the car last year, the salesman warned by saying it would be “stupid” for the first 3,000 miles.

It had to “learn” how to drive before I let it attempt any sophisticated self-driving maneuvers, like backing into a parking space on a crowded street.

I let it park itself in my garage now. I have only had a heart attack once.

With US annual auto production at 16.7 million units annualized, and global car and commercial vehicle production at a record 94.64 million, that is a lot of processors.

I have been covering Silicon Valley since it was a verdant, sun-kissed peach orchard in Northern California.

I have to say that in the half-century that I have followed the technology industry, I have never seen the principals, gurus, and visionaries so excited about a major new trend like AI.

Asking if AI is relevant now is like pondering the future of Thomas Edison’s new electricity invention in 1890.

If you think that AI still belongs in the realm of science fiction, you obviously didn’t get the memo. It is all around us all the time, 24/7. You just don’t know it yet.

And here’s the rub.

It is impossible to invest purely in AI.

All-new AI startups comprise small teams of experts from private labs and universities financed by big venture capital firms like Sequoia Capital, Kleiner Perkins, and Andreeson Horowitz.

After developing software for a year or two, they are sold on to major technology firms at huge premiums. They never see the light of day in the form of a public listing.

Alphabet (GOOGL) acquired Britain-based Deep Mind in 2014. Later that year, Google’s AlphaGo program defeated the world’s top-ranked Go player.

In 2016, Microsoft (MSFT) purchased Equivio, a small firm that applies AI to advanced document searches on the Internet.

Amazon (AMZN) recently bought out Orbeus, a startup known for machine learning tools for image recognition.

Amazon’s Jeff Bezos now says that his Amazon Fresh home food delivery service is using AI to grade strawberries.

Really!

We’re not talking small potatoes here.

The global artificial intelligence market is expected to grow at an annual rate of 44.3% a year to $23.5 billion by 2025.

Nearly half of all applications now use some form of AI that by 2020 will earn businesses an extra $60 billion a year in profits.

And from what I have learned from speaking to the major players over the last few weeks, I am convinced that these are low numbers by an order of magnitude.

I have been following developments in artificial intelligence since the 1960s.

There were those feeble computer dating attempts in the early seventies where we all had to prepare IBM punch cards.

I was matched with an annoyingly aggressive bleach blonde real estate agent. (Really?). Her only real qualification was that she was female.

It took decades and tens of thousands of programming man-hours before IBM’s Deep Blue could become a chess grandmaster in 1996, defeating Gary Kasparov.

Big Blue’s latest effort came to us with Watson in 2007, an 85,000-watt behemoth with 90 servers and 15 terabytes of data, or three quarters of the content of the entire Library of Congress.

The machine can read a staggering 1 million books a second. IBM has so far poured $15 billion into the project.

In 2011, Watson defeated the top-rated Jeopardy game show contestant by answering the question “What city’s national museum lost the “Lion of Nimrod.” The answer was “What is Baghdad” (I knew that!).

Today, Watson is on loan to the University of North Carolina at Chapel Hill where it has been deployed to cure cancer.

It took scientists a week to teach Watson how to read medical literature. In the second week, it read every paper published on cancer, some 25 million.

By the third week, it was proposing customized cures for advanced cancer patients, which achieved a 33% success rate.

After all, it can read all of the 8,000 cancer papers that are published every day from around the world IN SECONDS!

Scientists say that Watson has so far reached only 1% of its true potential.

It gets better than that.

A clinic can now biopsy your tumor, sequence its DNA, design a custom protein that will target and destroy your personal tumor, mass-produce it, inject it in your tumor, and cure you of cancer in a month.

This is being done with human volunteers in clinical trials NOW.

Expect this procedure to go retail and be made available to you in about five years. And by that, I mean cheap, locally available, and covered by your health insurance policy.

I believe that Watson and its future offspring will cure the major human maladies within a decade. My generation will probably be the last to suffer serious disease.

It isn’t just Watson that will take us the great leap forward in computing. By 2020, you will be able to buy a low-end laptop for $500 that can hold ALL KNOWLEDGE ACCUMULATED IN HUMAN HISTORY!

They better hurry. That body of knowledge is doubling every 18 months!

It is a key part of my argument that the US will enjoy a Golden Age and see a return of the “Roaring Twenties” during the 2020s.

If you have in any way been involved in the stock market for the past five years, AI has invaded your life.

High frequency trading and hedge funds now account for 70% of the daily trading volume on the major stock exchanges, and almost all of this is AI-driven.

Having spent my entire life trading stocks, I can confirm that in recent years the market’s character has dramatically changed, and not for the better. Call it trading untouched by human hands.

Algorithms are trading against algorithms, and whoever wins the nuclear arms race brings home the big bucks.

You used to need degrees in Finance and Economics, or perhaps an MBA, to become a professional fund manager. Now it’s a Ph.D. in Computer Science.

Remember the May 2010 flash crash when the Dow Average plunged 1,100 points in minutes wiping out $4.1 billion in equity value? AI’s fingerprints were all over that.

In 2016, the British pound lost 6% of its value in a mere two minutes, a move unprecedented in the history of foreign exchange markets. The culprit was AI.

Don’t expect the path forward to AI to be an easy one.

Indeed, the machines already have the power of life and death over all of us.

No less figures than Nobel Prize winner Dr. Stephen Hawking and Tesla’s Elon Musk have warned that computers and the Internet may have the power to pose a threat to human existence within a decade.

They are especially concerned about the militarization of powerful robots, something I know the US Defense Department is hell-bent on developing.

As I write this, the only thing preventing a drone attacking a village in Afghanistan is an Army corporal hitting a red button on a console in Nevada.

In the future, antivirus software won’t be needed to protect your computer. It will be essential to protect you FROM your computer.

You know that massive denial of service attack that hit the United States on October 21, 2016?

I asked one of my friends at security giant Palo Alto Networks (PANW) if it was the Russians again. He replied, “You better hope it’s the Russians.”

The implication is that the Internet may have launched the attack itself.

Now, about that stock recommendation.

Since we aren’t venture capitalists, we can’t buy into pure AI firms in their early stages. And I’m too old to get a Ph.D. in computer science.

We, therefore, have to be sneaky and get in through the back door via an indirect play which still has plenty of upside leverage.

My current favorite among the AI alternative stocks is Advanced Micro Devices (AMD).

If Intel only piques your appetite for AI stocks and you feel you need another serving, I have listed below ten names that will benefit mightily from this once-a-century opportunity.

AI Stock to BUY

Advanced Micro Devices (AMD)

Analogue Devices Communication (ADI)

Applied Materials (AMAT)

Broadcom (AVGO)

Cirrus Logic (CRUS)

Cypress Semiconductor (CY)

Intel (INTC)

Lam Research (LRCX)

Micron Technology (MU)

Taiwan Semiconductor (TSM)

If you’re really lazy, you can just buy a basket of semiconductor stocks through an industry-specific ETF.

The largest is the VanEck Vectors Semiconductor ETF (SMH), with $1.3 billion in assets under management. For a prospectus on the fund, please click here.

Or you could just stick with NVIDIA.

No matter how you want to slice and dice it, AI should be a dominant factor in your IRA, 401k, or benefit plan.

And you are a trader by nature, this will be a great sector to trade around.

As for your computer, you better start leaving it unplugged at night.

You never know.

![]()