Going through Warren Buffet’s letter to the shareholders of Berkshire Hathaway (BRK/A) you can’t help but notice that his performance nosedived from a breathtaking 21.9% in 2017 to a much more sedentary 2.8% last year. That is with an S&P 500 down -4.4%, including dividends.

That compares to my own 23.67% profit for 2018. But Warren has a much higher bar to reach. He does this with a staggering market capitalization that was pegged at $496 billion as of today. At best, the combined buying power of my Trade Alerts is only about a billion dollars.

And here is the stunning piece of information that should have been the headline. Warren has $112 billion in cash and equivalents, some 22.58% of the total, and an all-time high. That means buying stocks at these levels is the least attractive in the fund’s 57-year history.

Buffet would much rather buy back his own stock. He is willing to pay a premium to book value but only when it trades at a discount to intrinsic value, as he did in size during the fourth quarter of 2018.

Which raises one screaming great question. If Warren Buffet isn’t buying stocks, why should you?

Buffet isn’t even buying Apple, which he only started soaking up in 2017. It now is his second largest holding, with an average cost of $140. I’m amazed that the stock didn’t get crushed on this news, but then we live in a constantly amazing world these days.

The big change in Berkshire Hathaway over the years is that it is becoming more of an operating company and less of an investing one. That is because Buffet is increasingly buying entire companies, rather than exchange-traded stocks. One of the reasons for his cash hoard that an effort to buy a company for high double-digit billions of dollars fell through last year.

Still, Warren bought $43 billion worth of public stocks in 2018 and only sold $19 billion worth. These are his five largest public shareholdings and his percentage of outstanding shares:

American Express (AXP) – 17.9%

Apple (AAPL) – 5.4%

Bank of America (BAC) – 9.5%

Coca-Cola (KO) – 9.4%

Wells Fargo (WFC) – 9.8%

Warren likes to break up his entire holdings into five “groves”, as there are too many companies to follow individually.

1) Wholly owned companies where Berkshire has 80%-100% stakes, such as the BNSF railroad and Berkshire Hathaway Energy.

2) Publicly listed equities like those listed above

3) Companies controlled with third parties, like Kraft Heinz (KHT)

4) US Treasury bills

5) Property/Casualty Insurance operations like GEICO that generate an enormous free cash float

Buffet described the enormous tax benefits his company received from the 2017 tax bill. It amounted to the government’s indirect ownership of Berkshire shares falling, which he humorously calls “AA” shares, from 35% to 21% at no cost whatsoever. That greatly increased the value of the remaining shares.

Warren spent the rest of his letter talking about the Great American Tailwind. Since he started investing on March 11, 1942, one dollar invested in the S&P 500 has grown to an eye-popping $5,288! That works out to an average annualized compound return of 11.8% a year.

The end result has been the greatest creation of wealth and rise in standards of living in human history.

That is a tough record to beat.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/warren-buffet.png412618Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-01 11:03:212019-03-01 13:05:40Oh, How the Mighty Have Fallen

Yu'e Bao or "leftover treasure" in English has caught the attention of more than 400 million Chinese investors.

This money market fund has exponentially grown into a $250 billion fund by the end of 2017, and is now the largest money market fund in the world!

This product isn't offered by Bank of China or another giant state-owned bank or financial enterprise, but Alibaba's (BABA) Ant Financial (gotta love those Chinese names).

Assets under management are up 100% YOY and it now accounts for a quarter of China's money-market mutual fund industry in just one fund.

These inflows coincide with the sudden migration into mobile payments. Common folks are comfortable with investing their life savings in these short-term instruments with a too-big-to-fail, larger-than-life firm such as Alibaba.

Yu'e Bao derives its funds from Alipay users, Alibaba's digital third-party platform, that allows consumers to pay for everything in life from theater tickets to utility bills.

Service is unified on a holistic graphic interface. Users can easily divert cash into this fund with a few screen taps on their app. Yu'e Bao's ROI offers a seven-day annualized yield of 4.02%, down from the introductory annualized rate of 6.9% around the launch in 2013.

Yu'e Bao's short-term yield outmuscles the 1.5% interest rate on one-year Chinese bank deposits and the 3.6% yield on 10-year Chinese government debt.

Weak banking regulation has spawned a mammoth FinTech (financial technology) industry in the Middle Kingdom. Only one yuan (16 cents) is enough to create an account and considerable retail flow has rushed in.

China has catapulted ahead of the rest of the world emerging as the leader of global FinTech innovation. The pace, sophistication, and scale of development of China's FinTech have surpassed the level in any other of the developed countries.

The country's digital metamorphosis has enhanced e-commerce, payment systems, and connected logistical services. The Chinese discretionary spender for the past decade has been the deepest and most reliable lever of global growth.

Mobile third-party payments in China, 90% cornered by Tencent's WeChat and Alibaba's Alipay, are estimated to reach a lofty $6 trillion in revenue by 2019, more than 50 times that of the U.S.

These omnipresent payment systems are now deeply embedded into the fabric of Chinese society. It's common to witness homeless people on Shanghai subways waving around a scannable image for WeChat or Alipay money transfers instead of asking for physical cash.

Even in rural farmlands, shabby convenience stores prioritize digital currency and sometimes don't accept paper currency at all. Yes, China is beating the U.S. to a cashless society.

Digitization is changing the competitive balance, and global banks must embrace large-scale disruption caused by big tech platforms.

Banks in China regard these companies as potential collaborators resulting in a net positive long-term infusion of enhanced products and services.

Agreements have been forged between the Bank of China and Tencent, and the China Construction Bank has linked up with Alibaba.

China has incorporated the technical power of A.I. (artificial intelligence) and machine learning into its FinTech platforms at every opportunity. Robo-advisors are also making inroads creating a bespoke financial program for the individual.

This trend has so far failed to go viral in America where individuals still prefer plastic cards or even paper cash. E-commerce clocked in a paltry 9.1% of total U.S. retail sales in the third quarter of 2017.

Even though most of us have our heads buried deep in our smartphone virtual world, Americans are still programmed to whip out debit or credit cards at every opportunity.

Chinese who visit America carp endlessly about America's archaic payment system.

Ultimately, American payment systems are ripe for digital disruption.

The American consumer will ultimately cause severe damage to MasterCard (MA), Visa (V), and American Express (AXP) which are happy with the current status quo.

The lack of innovation in the US FinTech sector is a failure in the otherwise fabulous technological leadership of the US. American smartphones should already be a fertile digital wallet, not just a niche market.

Savvy Jack Dorsey even invented a firm based on this inefficiency exploiting the lack of proficiency in domestic FinTech with Square (SQ).

And a vital reason the stock has gone parabolic this year is because of the brisk execution and the long runway ahead in this industry.

American big tech will gradually utilize China's FinTech model and extrapolate it with "American personality." It is much more of a two-way street now than before with cutting-edge ideas flowing both ways.

The next leg up after digital wallet penetration of FinTech is money market funds on tech platforms. In effect, the Chinese innovation of this industry has allowed more variations of potential financing for the ambitious Chinese, and the same trends will gradually appear on Yankee shores.

Ironically enough, Amazon's (AMZN) land grab strategy is more prevalent in China as artificially low financing and juicier scale justify this strategy.

The scaling premium also explains why corporate China's early adopter advantage is so effective because not many countries boast a 1.3-billion-person consumer market.

Soon, Americans will wake up to the reality that American FinTech must advance or foreign firms will rush in.

Mediocrity is not good enough.

iPhones and Android consumers could direct savings into tech money market funds with compounding yield all on a single digital platform.

Tech companies could deploy some of the repatriated cash to invest in some fledgling FinTech expertise to smoothly execute this new endeavor.

Consequently, a successfully created money market fund on a tech platform would enlarge the already substantial cash hoard these firms possess. Not only will the large tech companies flourish, but the big will get absolutely massive.

The determining factor is financial regulation. Capitol Hill has drawn a large swath of mighty Silicon Valley tech titans to testify because they are stepping on too many toes lately.

A scheme to hijack the digital payments market and dominate the mutual fund industry will cause unyielding push back in Washington especially when the Amazon death star continues pillaging select industries of their choosing and eliminating brick-and-mortar jobs by the millions.

J.P. Morgan (JPM) which has the largest institutional money market fund in the country and retail stalwarts such as BlackRock and Vanguard will be sweating profusely too if mega tech starts probing around its turf.

Alibaba is also coming for its bacon with the failed purchase of payment transfer service MoneyGram International (MGI) temporarily shutting out Jack Ma from a foothold in the American payment system industry.

And if the Chinese aren't let in, there will be others sniffing around for the bacon, too.

The momentum for these financial instruments is robust as FinTech integrates deeper into consumer life. The global cash glut from a decade of cheap financing is causing profit-hungry investors to starve for high-yield vehicles.

The stability and clean balance sheets of tech giants give them ample chance to successfully execute. So, why can't they also become banks? Would you buy an Apple, Amazon, or Google money market fund if they offered a 4% to 7% annualized yield?

I believe most Americans would.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-01-02 02:06:322019-07-09 05:00:39The FANGs' Path to Online Banking

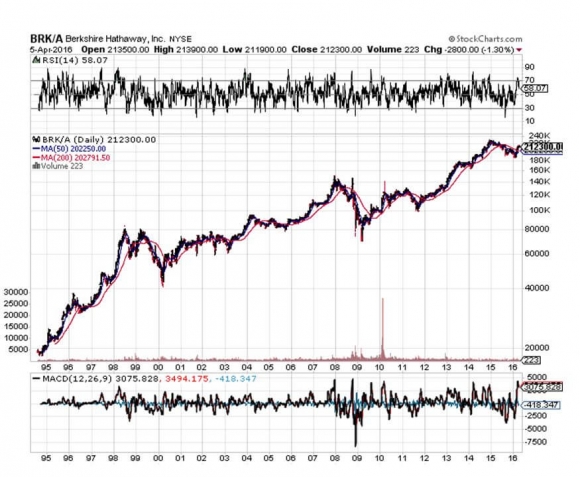

Sometime in the early 1970?s, a friend of mine said I should take a look at a stock named Berkshire Hathaway (BRKA) run by a young stud named Warren Buffett.

I thought, ?Why the hell should I invest in a company that makes sheets??

After all, the American textile industry was in the middle of a long trek toward extinction that began in the 1920?s, and was only briefly interrupted by the hyper prosperity of WWII. The industry?s travails were simply an outcome of ever rising US standards of living, which pushed wages, and therefore costs, up.

It turns out that Warren Buffett made a lot more than sheets. However, he is not a young stud anymore, just an old one, like me.

Since then, Warren?s annual letter to investors has been an absolute ?must read? for me when it is published every spring.

It has been edited for the past half century by my friend, Carol Loomis, who just retired after a 60-year career with Fortune magazine. (I never wrote for them because their freelance rates were lousy).

Witty, insightful, and downright funny, I view it as a cross between a Harvard Business School seminar and a Berkeley anti establishment demonstration. You will find me lifting from it my ?Quotes of the Day? for the daily newsletter over the next several issues. There are some real zingers.

And what a year it has been!

Berkshire?s gain in net worth was $18.3 billion, which increased the share value by 8.3%, and today, the market capitalization stands at an impressive $343.4 billion. (Sorry Warren, but I clocked 30% last year, eat your heart out).

The shares are not for small timers, as one now costs $214,801, and no, they don?t sell half shares. This compares to a 1965 per share market value of $23.80, and is why the media are always going gaga over Warren Buffett.

If you?re lazy and don?t want to do the math, that works out to a compound annualized return of an eye popping 21.6%. This is why guessing what Warren is going to do next has become a major cottage industry (Progressive Insurance anyone?).

Warren brought in these numbers despite the fact that its largest non-insurance subsidiary, the old Burlington Northern Santa Fe Railroad (BNSF) suffered an awful year.

Extensive upgrades under construction and terrible winter weather disrupted service, causing the railroad to lose market share to rival Union Pacific (UNP).

I was kind of pissed when Warren bought BNSF in 2009 for a blockbuster $44 billion, as it was long my favorite trading vehicles for the sector. Since then, its book value has doubled. Typical Warren.

Buffett plans to fix the railroad?s current problems with $6 billion in new capital investment this year, one of the largest single capital investments in American history. Warren isn?t doing anything small these days.

Buffett also got a hickey from his investment in UK supermarket chain Tesco, which ran up a $444 million loss for Berkshire in 2014. Warren admits he was too slow in getting out of the shares, a rare move for the Oracle of Omaha, who rarely sells anything (which avoids capital gains taxes).

Warren increased his investment in all of his ?Big Four? holdings, American Express (AXP), Coca-Cola (KO), IBM (IBM), and Wells Fargo (WFC).

In addition, Berkshire owns options on Bank of America (BAC) stock, which have a current exercise value of $12.5 billion (purchased the day after the Mad Hedge Fund Trader issued a Trade Alert on said stock for an instant 300% gain on the options).

The secret to understanding Buffett picks over the years is that cash flow is king.

This means that he has never participated in the many technology booms over the decades, or fads of any other description, for that matter.

He says this is because he will never buy a business he doesn?t intrinsically understand, and they didn?t offer computer programming as an elective in high school during the Great Depression.

No doubt this has lowered his potential returns, but with the benefit of much lower volatility.

That makes his position in (IBM) a bit of a mystery, the worst performing Dow stock of the past two years. I would much rather own Apple (AAPL) myself, which also boasts great cash flow, and even a dividend these days (with a 1.50% yield).

Warren will be the first to admit that even he makes mistakes, sometimes, disastrous ones. He cites his worst one ever as a perfect example, his purchase of Dexter Shoes for $433 million in 1993. This was right before China entered the shoe business as a major competitor.

Not only did the company quickly go under, he exponentially compounded the error through buying the firm with an exchange of Berkshire Hathaway stock, which is now worth a staggering $5.7 billion.

Ouch, and ouch again!

Warren has also been mostly missing in action on the international front, believing that the mother load of investment opportunities runs through the US, and that its best days lie ahead. I believe the same.

Still, he has dipped his toe in foreign waters from time to time, and I was sometimes quick to jump on his coattails. A favorite of mine was his purchase of 10% of Chinese electric car factory BYD (BYDDF) in 2009, where I have captured a few doubles over the years.

Buffett expounds at great length the attractions of the insurance industry, which today remains the core of his business. For payment of a premium up front, the buyers of insurance policies receive a mere promise to perform in the future, sometimes as much as a half century off.

In the meantime, Warren can invest the money any way he wants. The model has been a real printing press for Buffett since he took over his first insurer in 1951, GEICO.

Much of the letter promotes the upcoming shareholders annual meeting, known as the ?Woodstock of Capitalism?.

There, the conglomerate?s many products will be for sale, including, Justin Boots (I have a pair), the gecko from GEICO (which insures my Tesla S-1), and See?s Candies (a Christmas addiction, love the peanut brittle!).

There, visitors can try their hand at Ping-Pong against Ariel Hsing, a 2012 American Olympic Team member, after Bill Gates and Buffett wear her down first.

They can try their hand against a national bridge champion (don?t play for money). And then there is the newspaper-throwing contest (Buffett?s first gainful employment).

Some 40,000 descend on remote Omaha for the firm?s annual event. All flights to the city are booked well in advance, with fares up to triple normal rates.

Hotels sell out too, and many now charge three-day minimums (after Warren, what is there to do in Omaha for two more days other than to visit PayPal?s technical support?). Buffett recommends Airbnb as a low budget option (for the single shareholders?).

I was amazed to learn that Berkshire files a wrist breaking 24,100-page Federal tax return (and I thought mine was bad!). Add to this a mind numbing 3,400 separate state tax returns.

Overall, Berkshire holdings account for more than 3% of the total US gross domestic product, but a far lesser share of the government?s total tax revenues, thanks to careful planning.

Buffett ends his letter by advertising for new acquisitions and listing his criteria. They include:

(1) ?Large purchases (at least $75 million of pre-tax earnings unless the business will fit into one of our existing units),

(2) ?Demonstrated consistent earning power (future projections are of no interest to us, nor are ?turnaround? situations),

(3) ?Businesses earning good returns on equity while employing little or no debt,

(4) Managemen

t in place (we can?t supply it),

(5) Simple businesses (if there?s lots of technology, we won?t understand it),

(6) An offering price (we don?t want to waste our time or that of the seller by talking, even preliminarily, about a transaction when price is unknown).

https://www.madhedgefundtrader.com/wp-content/uploads/2015/04/Warren-Buffett-e1429740484967.jpg249400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-04-19 01:06:052016-04-19 01:06:05A Chat With Berkshire Hathaway?s Warren Buffett

I remember that the highlight of my 1968 trip to Europe was always my visit to the nearest American Express (AXP) office to pick up my mail.

In those pre Internet and email days, it was the only way that a fresh faced 16 year old could stay in touch with a hand wringing family while traveling around the world.

They just wrote ?John Thomas, c/o American Express, Paris, France,? and the letters never failed to get through to me.

It was also a great place to meet other vagabonding Americans my age--of the female persuasion. At least they spoke English. Almost.

That was a very long time ago.

So I got to know well the American Express locations off the Spanish Steps in Rome, Saint Mark?s Square in Venice, Berlin?s Kurfurstendamm, and the Champs-Elysees in Paris.

I have a feeling that American Express is about to give me a warm and fuzzy feeling once again.

After being taken out to the woodshed and getting beaten senseless in the wake of getting fired by Costco, one of the biggest customers, the shares appear poised for a comeback.

We have a rare occasion where the highest quality stock in a sector with the best business model is selling cheaper than its cohorts for a series of temporary reasons.

Take a look at the charts for (AXP) and Visa (V) below, and one of the greatest pairs trades of all time may be setting up, whereby you want to buy for the former and sell short the latter against it.

At the very least, you should be taking your monster profits on Visa and rolling the money into American Express.

Since its inception in 1958, that flashy green (or platinum) piece of plastic has long been a status symbol, and owned the premium end of the credit card market.

As a result, it earns more fees and extends fewer loans than its competitors. The loans it does have enjoy a far lower default rate. There are now 107 million Amex cards in circulation, compared to only 55 million in 2001. Thank you 1%!

American Express cardholders run balances three times larger than the average Master Card holder. That?s what happens when you buy a Ferrari on your Amex card, as I once did (to get the frequent flier points).

Merchants pay very high fees, usually 5% of the purchase. That?s why many shun the card. (AXP) is currently running a credit card balance of $940 billion, versus $3.1 trillion for Visa (V).

Fees accounted for an impressive 57% of the company?s revenues, a far higher ratio than other credit card companies. Better yet, (AXP)?s fees are rising, while those of others are falling. Interest on balances brings in 15% and cardholder fees 8%.

(AXP) is expected to earn $5.8 billion in net income on $33.9 billion in revenues this year, up 9.4%. With the US economy recovering, growing by 2.6% this year and 3.0% plus in 2015, the company is in the sweet spot for capturing more profits.

Morgan Stanley estimates that cardholder spending grows at 4.5 times the US GDP growth rate. That should cause (AXP)?s earnings to double, and the stock as well. An extra tailwind will be the company?s new strategy of moving down market to expand market share.

Despite all this good news, (AXP) shares are selling at a 13.4X multiple, a discount to its industry (21X), and the main market (18X). An ambitious share buy back program should put a floor under the stock.

Part of the discount can be explained by a Justice Department suit claiming that the company overcharges merchants. Amex correctly argues that, as the smallest of the major credit card companies, it has nowhere near monopoly pricing power.

It will be interesting to see how aggressively the government pursues its action, now that attorney general Eric Holder, has moved on to retirement.

You all know by now that I think financials are the place to be for years going forward because of imminently rising interest rates. But I?ll hold back on pulling the trigger on single name long side stocks plays until the carnage in the markets abate.

When I?m ready to shoot out a Trade Alert, you?ll be the first to know.

When I do, don't even think about putting it on your credit card.

Just Stopping By to Pick Up the Mail

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/John-Thomas-16-yrs-old.jpg349348Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-11-05 01:06:302015-11-05 01:06:30Keep American Express on Your Short List

Regular readers of this letter are probably weary of me harping away about the financials as a great place to put your money for the rest of 2014.

Never mind that these names have all jumped 10% in the past month. But this is not an ?I told you so? story. This is more of a ?But wait, there?s more,? story.

The basis for my call is quite simple. I believe that bond prices are peaking, and yields bottoming. As mining the yield curve is a major source of bank profits, borrowing short term and lending long term, a rise in interest rates falls straight to the bottom line. Thus, buying banks is an indirect way of selling short the bond market.

However, there are many more reasons to overweight this long neglected sector. In a market that has gone virtually straight up for the past three years, many large institutions are going to be forced to roll money out of leaders, like my favored technology, energy and health care, into laggards, such as the financials.

Expect this trend to accelerate as we head into yearend institutional book closing, which start as early as October 30.

Look at other important drivers of bank profits, and you?ll find them at multi decade lows.

Trading and investment banking volumes are off 30%-40% from mean historic levels. We options traders already know this all too well, as turnover has cratered and spreads widened due to investor lack of interest.

This is especially true of put options, which are now being given away virtually for free. Volatility that seems to permanently live at the $12 handle is another such indicator of this disinterest.

This will not last. If my ?Golden Age? scenario plays out in the 2020?s (click here for ?Get Ready for the Coming Golden Age?), trading and investment banking volumes will not only double to return to the norms, they will skyrocket tenfold from today?s tedious, moribund levels.

Indeed, I have recently discovered an entire subculture of financial oriented private equity firms currently amassing portfolios that are betting on precisely such an outcome. Think of big, smart, long-term money. The big bets on the coming decade are being made now.

There is another ripple in the case for banks. After passage of the Financial Stability Act of 2010, otherwise known as ?Dodd Frank?, banks became target numero uno of the federal government. The public?s demand for accountability for the 2008-09 crash knew no bounds.

As a result, the fines and settlements with the big banks, most of which were rescued from bankruptcy by the government, now well exceed $100 billion. Four years into the enforcement onslaught, the Feds are running out of scandals to prosecute. There is nothing left for the banks to plead guilty to.

This means that a major portion of the banks? costs are about to disappear, not only new massive fines, but hundreds of millions of dollars in legal fees and diverted management time as well. More money drops to the bottom line.

Dramatically rising income? Substantially falling costs? Sounds like ?Ka-ching? to me, and a ?BUY? for the bank stocks.

The bottom line is that bank stock could double from here in coming years. It is not hard to pick names. Bank of America (BAC) took the big hit on fines and settlements, and therefore should enjoy the largest bounce.

So should Citigroup (C), which came the closest to vaporizing. And for good measure, I?ll throw in American Express (AXP) as a play on the burgeoning credit card spending by the growing class of well to do.

Barney Frank Had a Few Things to Say

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/John-Thomas-and-Barney-Frank.jpg357577Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-09-03 09:29:542014-09-03 09:29:54The Case for Buying Financials

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.