Mad Hedge Biotech and Healthcare Letter

January 17, 2023

Fiat Lux

Featured Trade:

(COMPROMISE IS THE BEST STRATEGY)

(JNJ), (AMGN), (TAK), (VRTX), (CRSP), (EDIT), (PFE), (CRBU), (SGMO), (LLY), (AXSM)

Mad Hedge Biotech and Healthcare Letter

January 17, 2023

Fiat Lux

Featured Trade:

(COMPROMISE IS THE BEST STRATEGY)

(JNJ), (AMGN), (TAK), (VRTX), (CRSP), (EDIT), (PFE), (CRBU), (SGMO), (LLY), (AXSM)

An optimist looks at bubbles and visualizes champagne, while a pessimist’s mind goes to Alka-Seltzer. The same thing happens with investors.

Some believe that the steep losses suffered by stocks and bonds in 2022 are a much-needed “cleansing,” which would set the stage for renewed partnerships and collaborations along with high returns. Others simply view it as the first chapter in a protracted bear market.

Meanwhile, a handful believes that it’s a combination of both perspectives—especially for the biotechnology industry.

Roughly two years following the decline of biotechnology stocks, several executives from small and midsize organizations finally concede that their share prices might no longer be able to bounce back anytime soon. In fact, some have been fielding panicked calls from execs of fledgling biotech firms, offering to sell their companies at a discount.

The alteration in the medical device and biotechnology landscape only started a few months before the previous year ended.

This is because, before the change in perspective, when the SPDR S&P Biotech exchange-traded fund (XBI) had slid by about 40% from its 2021 peak, many leaders in the biotech sector still believed that their companies could regain momentum.

The primary concern for smaller biotech and medical devices companies, which allocate years to developing and testing products without any commercially approved treatment, is that the continuous decline in their valuations has made it practically impossible to generate new money to fund any of their projects.

Given this scenario, many small and midsize biotechs would go under soon, particularly those with no data strong enough to provide near-term growth catalysts.

This is where Big Pharma names are expected to come in. After all, these large-cap companies offer an alternative option with their non-dilutive sources of funding and ever-growing war chests.

Big companies, though, have been more cautious in cutting big checks for acquisitions. Despite the high expectations last year, we only saw a few massive deals, including Abiomed’s sale to Johnson & Johnson’s (JNJ) for $19 billion and Amgen’s (AMGN) $30 billion agreement with Horizon Therapeutics.

Instead, these Big Pharma companies appear to prefer partnerships and collaborations. In these deals, they give out smaller payments to biotechnology firms to work with them on specific early-stage programs.

This type of investment seems to be a safer bet for big companies because it allows them to make several deals without spending too much. They can even collaborate with competing biotechs to determine which could develop the most effective and cost-efficient solution.

Smaller biotechs benefit from this type of deal as well.

In the pre-pandemic era, the valuations of these companies quickly soared based on the potential of their pipeline candidates. Some share prices would skyrocket with just a hint of positive data. This is no longer the case these days, not only because investors have become more discerning but also more anxious over experimental programs.

So instead of getting acquired, smaller biotechs can choose to strike partnerships with large-cap companies. This is an excellent way to inject some funding into their programs and, hopefully, provide them with revenue streams, especially since Big Pharma companies know how to market new products.

It sounds challenging, but a genuinely promising program could fetch a large sum.

Perhaps the most significant indicator that not all hope is lost comes from Takeda (TAK) when it purchased an experimental treatment undergoing tests as a potential psoriasis medication.

This candidate, developed by a privately held biotechnology firm called Nimbus Therapeutics, was sold for a whopping $4 billion upfront, plus roughly $2 billion more for future milestone payments. And here’s the clincher: Takeda got the experimental drug by a razor-thin margin.

In terms of acquisitions, some larger companies have been open to that route. For instance, AstraZeneca (AZN) shelled out $1.3 billion for CiniCor Pharma, while Ipsen (IPSEY) purchased Albireo Pharma (ALBO) for $1 billion.

While the future for smaller biotechs remains uncertain, several names continue to be in conversations whenever acquisitions are discussed.

There’s Vertex Pharmaceuticals (VRTX), which has long been reported to take interest in acquiring CRISPR Therapeutics (CRSP) and Editas Medicine (EDIT), with the latter looking more attractive thanks to its cheaper price tag.

Meanwhile, Pfizer (PFE) has been shopping around for a biotech to bolster its gene-editing programs, and so far, Caribou Biosciences (CRBU) and Sangamo Therapeutics (SGMO) are under serious consideration.

With its continuing interest in central nervous system diseases, such as Alzheimer’s and Parkinson’s, Eli Lilly (LLY) has been aggressive in its search for a company to acquire. Among the strongest candidates is Axsome Therapeutics (AXSM).

With this daunting reality setting in, one thing has become absolutely sure: the biotechnology sector has become a buyer’s market for big companies with cash to spare for acquisitions and collaborations.

Mad Hedge Biotech and Healthcare Letter

August 25, 2022

Fiat Lux

Featured Trade:

(A RISK WORTH TAKING)

(AXSM), (SAGE), (RLMD), (PFE), (LLY), (BMY), (BIIB)

When a drugmaker does not deliver a new product within the promised timeframe, its shares generally drop.

When this happens, investors should take a closer look at regulatory headwinds as potential buying opportunities, especially in the biotechnology world.

However, it’s important to determine whether the business in question can satisfactorily address the issues raised by the regulators and eventually get the green light for the held-up product.

Several companies find themselves in this scenario, but a particular one looks promising: Axsome Therapeutics (AXSM).

While Axsome isn’t one of the most renowned biotechs and its shares may look somewhat risky, it’s worth considering initiating positions in this growing company.

One reason is Axsome’s recent victory over a hurdle, finally gaining the long-awaited FDA approval for its depression drug that can take effect within just 1 week because it uses a unique mechanism instead of the traditional elements.

The drug, previously known as AXS-05, will be marketed as Auvelity and slated for sale in the fourth quarter of 2022.

For months, investors have been closely monitoring the progress and approval of this drug with some concern.

Doubts over Axsome’s capacity to deliver started to hound the company, especially after FDA’s self-imposed approval deadline for AXS-05 passed in 2021.

However, the company attributed the delay to the pandemic and shrugged off concerns over the actual drug.

Auvelity is the first of a class of drugs, which are classified as NMDA receptor antagonists, to be marketed in pill form created as a treatment for depression.

It is the only approved pill working as a fast-acting drug targeting major depressive disorder. This will also be Axsome’s first-ever marketed product.

Other than Axsome, there are several biotechs working on antidepressant treatments.

Among them, the closest potential competitors are Sage Therapeutics (SAGE) and Relmada Therapeutics (RLMD).

Sage recently started rolling out its own candidate, Zuranalone, for approval as a treatment for major depressive disorder.

Relmada is also working on a similar candidate, REL-1017, but seems to be at an earlier stage.

Psychiatric treatments like Auvelity are widely sought after and highly coveted assets in the biopharma world for a myriad of reasons.

The sheer potential of Auvelity puts Axsome on buyout watch for several Big Pharma and even expanding biotechnology and healthcare companies today.

Moreover, Axsome’s major depressive disorder drug would dovetail conveniently with the lineups of a lot of leading pharmaceutical names in the industry including Pfizer (PFE), Eli Lilly (LLY), Bristol-Myers Squibb (BMY), and even Biogen (BIIB).

With that in mind, Axsome’s brain trust would most likely demand an astronomical premium based on or relative to its current valuation if it ever enters any buyout discussion with interested suitors.

Auvelity sales are projected to hit $209.1 million in 2023, growing impressively to blockbuster status by 2027 at $1.5 billion.

By 2030, sales of this major depressive disorder drug are estimated to reach $2 billion every year.

Auvelity is made up of two drugs that physicians already readily prescribe and are comfortable with for years; one of which is bupropion.

Bupropion, marketed under the brand name Zyban, actually raked in blockbuster sales marketed as a smoking cessation treatment.

Hence, Axsome plans to leverage the success of Auvelity to begin a pivotal study that could utilize this major depressive disorder as a smoking cessation treatment as well.

On top of these, Axsome is anticipating another FDA approval in the next months.

The company submitted its new migraine treatment, AXS-07, for review in 2021. Like Auvelity, it encountered delays due to the pandemic. However, things seem to be moving along as the regulatory committees catch up.

By 2023, Axsome plans to submit another candidate for FDA approval. Clinical trial results for its fibromyalgia treatment, AXS-14, recently released positive data.

So, what now?

When investing in biotech, it’s always good to keep in mind that extreme volatility is an ever-present risk. This makes the sector unfit for those looking for short-term investments.

For Axsome, the biggest challenge today is showing that Auvelity sales can support the development of AXS-07 and AXS-14 and fund operations into 2024 without the need to ask shareholders for more capital.

However, even if Auvelity fails to deliver strong revenues in 2023, the rest of the company’s late-stage pipeline still looks pretty exciting.

Taken together, Axsome looks like a promising stock to invest in as a relatively small portion of a diversified biotech portfolio.

Mad Hedge Biotech and Healthcare Letter

February 1, 2022

Fiat Lux

Featured Trade:

(A SHIFT IN NEUROSCIENCE BIOTECH)

(BIIB), (AXSM), (PFE), (BMY), (MRK), (NVS), (ABBV), (GSK), (JNJ), (LLY), (RHHBY), (TAK)

Industry experts typically describe mergers and acquisitions as the life force that propels the biotechnology and healthcare sector forward.

Based on that description, it’s safe to say that the segment’s health has plummeted, considering the sluggishness observed last year.

In 2021, the M&A of this industry had fallen to one of its lowest recorded levels in history.

During this period, the deals only amounted to $108 billion for the entire year. This number was approximately 40% of the total recorded in 2019.

Despite the sluggishness in 2021 and the relatively slow start in 2022, this year is still projected to push the would-be buyers into more aggressive action.

After all, several key products are facing patent expiration before this decade ends.

The list includes Big Pharma players like Pfizer (PFE), Bristol Myers Squibb (BMY), Merck (MRK), and Novartis (NVS).

This means that a massive deal might be on the horizon, pretty much when AbbVie (ABBV) executed its jaw-dropping $63 bill acquisition of Allergan in 2019 following its problems with generics competing against its blockbuster drug Humira.

Aside from patent protection concerns, another factor in play is the intense competition in lucrative research sectors such as immunology, neurology, rare diseases, and oncology.

Add to this the constant pressure of Congress to pull down drug prices, and it becomes apparent why companies—big or small—turn to mergers and acquisitions for survival.

Simply put, biotech and healthcare companies have no other choice but to be aggressive in looking for external innovation to secure the continuous transformation of their businesses.

On that note, I think there could be major acquisitions to be announced in 2022.

One deal I’m looking forward to is Biogen’s (BIIB) potential acquisition of Axsome Therapeutics (AXSM).

To remain competitive in the neuro stage, Biogen must keep up with the times—and a deal with Axsome might just be the solution.

Axsome’s size and price, with a market capitalization of $992 million, appear to be just the right fit for Biogen to gobble up.

More importantly, its portfolio is an excellent fit for Biogen. Both focus on neurological diseases, making their pipelines complementary to each other.

So far, Axsome has several leading candidates in the clinical stages.

One is AXS-05, which is a treatment for major depressive disorder (MDD).

Apart from MDD, this candidate is under late-stage review to target Alzheimer’s disease agitation.

In addition, Axsome is looking to advance AXS-05 in late-stage trials for smoking cessation therapy.

Needless to say, AXS-05 would go hand in hand with Biogen’s own approved, albeit controversial, Alzheimer’s drug Aduhelm.

Another promising candidate is AXS-07, a potential competitor of Pfizer and Novartis’ migraine medication. This drug has been submitted for FDA approval and might be launched by the second quarter of 2022.

There’s also AXS-12, which is a narcolepsy treatment candidate, and AXS-14, which is geared towards fibromyalgia. Both candidates are slated for FDA review by the third or fourth quarter of 2022.

For over 20 years, even the biggest and most powerful drug companies have stayed away from working on treatments specifically for the brain and central nervous system (CNS).

That’s not surprising considering the sheer number of failed programs in neuroscience, pushing drugmakers to believe that we still don’t have sufficient data on the subject, so the money might be better spent elsewhere.

Nowadays, though, the CNS landscape is starting to shift.

GlaxoSmithKline (GSK) recently embarked on reviving its CNS program by striking a $700 million deal with a smaller biotechnology company called Alector.

Meanwhile, Pfizer and Novartis reached an agreement with Biohaven Pharmaceuticals for the latter’s migraine treatment and Parkinson’s drug.

Aside from these, Johnson & Johnson (JNJ), Eli Lilly (LLY), Roche (RHHBY), and Takeda (TAK) are anticipated to secure CNS-centered deals soon.

Despite the lower number of M&A deals last year, the volume of strategic collaborations in the neuroscience sector climbed by about 50% in 2021 compared to its 2020 performance.

By 2022, this space is projected to become even more investable, considering the number of biotechnology companies focusing on CNS. Watch out for blockbuster deals in this sector.

Mad Hedge Biotech & Healthcare Letter

July 6, 2021

Fiat Lux

FEATURED TRADE:

(A PROMISING BIOTECH FOR RISK-TAKERS)

(AXSM), (AMGN), (MRK)

Biotechnology companies are known as the riskiest investments in the stock market. More often than not, they are small, cash-strapped, and with futures so closely tied up to the success or failure of a single clinical study.

For each Amgen (AMGN), which exploded from a market capitalization of less than $1 billion roughly 30 years ago to a whopping $137.15 billion today, there are thousands that fail and fall into obscurity.

However, when a biotech makes it big, the rewards can be transformative—and this speckle of hope is what makes this industry incredibly exciting and interesting.

Let’s take Axsome Therapeutics (AXSM) as an example.

This stock has been beaten down, but its pipeline programs still hold the potential to inflate the portfolios of its shareholders if their science proves to be successful.

Actually, things appear to be turning around for Axsome these days.

Focused on developing novel and innovative treatments for central nervous system disorders, Axsome’s stock price recently enjoyed a 13% climb thanks to the latest development on one of its pipeline candidates: AXS-14.

AXS-14, which is a fibromyalgia treatment, should be ready for submission by the fourth quarter of 2022.

Looking at the potential target market for this drug, its estimated peak sales are somewhere in the range between $500 million to $1 billion.

Another promising treatment in Axsome’s pipeline is its novel migraine medication, AXS-07, which showed great efficacy results in its Phase 3 trial.

In addition, 74% of patients who took AXS-07 experienced no pain progression from two to 24 hours since taking the medication, with almost 50% of them no longer needing rescue medication.

Given the remarkable results for AXS-07, Axsome plans to submit it for a new drug application in the first half of 2021. In fact, this candidate has shown better results than the current gold standard, Merck’s (MRK) Maxalt.

If approved, this migraine treatment can reach peak sales from half a billion to over $1 billion in the United States alone.

However, the most promising candidate in Axsome’s pipeline is its treatment for major depressive disorder (MDD), AXS-05, which recently received priority review from the US FDA.

If things go as planned, the company plans to submit it for review by August 22 this year.

This drug is also a frontrunner medication for Alzheimer’s Disease (AD) Agitation.

On top of these, its Phase 3 clinical trial of AXS-05 showed that it significantly improved the symptoms of people suffering from depression.

Beyond these conditions, Axsome is also looking into using AXS-05 as treatment for migraines, smoking cessation, and even migraines.

AXS-05 has a massive addressable market, with roughly one-third of the 17 million adults in the US suffering from MDD. This could mean peak sales for this indication alone at $4 billion.

While Axsome still has other promising treatments in its pipeline, these three late-stage candidates clearly indicate a very high ceiling.

All of them have the capacity to reach blockbuster status once approved.

At this point and looking at its recent earnings report, Axsome recorded a cash balance of $164 million. It also still has some money left from its $225 million loan, which means the company can still sufficiently fund its operations and continue with its research into at least 2024.

Considering the timeline it has for the three candidates in its pipeline, it’s reasonable to assume that it can generate sales before that date.

All in all, they could rake in a total of at least $8 billion in sales annually for Axsome—a lucrative leap considering that the company currently only has $2.62 billion in market capitalization.

Given its vast pipeline, host of successful trials thus far, and near-term catalysts, I say this clinical-stage biotech’s lowered prices offer a cautious buying opportunity for investors with a penchant for risks.

Mad Hedge Biotech & Healthcare Letter

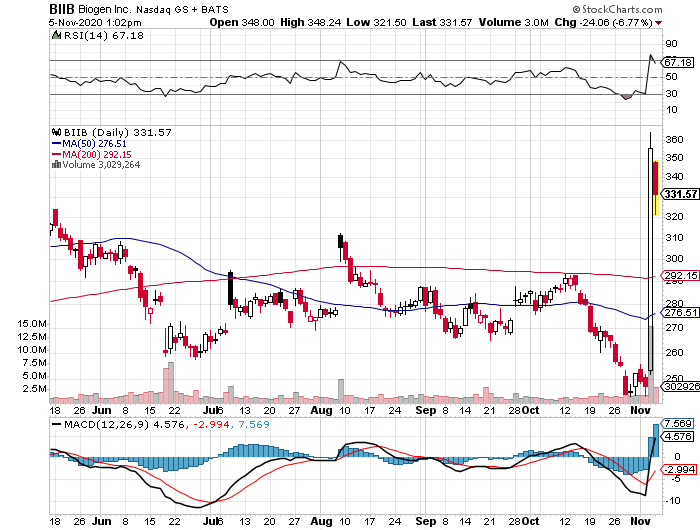

November 5, 2020

Fiat Lux

FEATURED TRADE:

(IT’S GO TIME FOR BIOGEN’S ALZHEIMER’S DRUG)

(BIIB), (LLY), (AXSM), (MYL)

Investing in beaten-up stocks in this period of uncertainty demands nerves of steel.

In fact, some biotechnology and healthcare stocks have been left for dead in recent months. Meanwhile, there are others that continue to deliver amidst the ongoing pandemic.

One of them is Biogen (BIIB).

Biogen has been consistently tagged as a high-risk-high-reward stock even before the COVID-19 pandemic started.

However, people seem to miss the fact that the company has relatively low debt and a surprisingly positive free cash flow in the past years.

Since 2019, the banner headline for Biogen has been its experimental Alzheimer’s disease treatment Aducanumab.

Recently, Biogen released promising progress following its decision to submit the Alzheimer’s candidate for a priority review to the FDA. It has also been accepted for review by European health regulators.

Although this move appears risky, the goal is to accelerate FDA’s timeline for Aducanumab.

That is, Biogen’s decision to submit the drug for approval earlier than expected also pushes the decision to an earlier date, which is March 7, 2021.

If approved, then Aducanumab will be the first-ever approved drug for Alzheimer’s disease.

The road to this point was not easy though. Biogen went through a series of failed trials and even a brief period of giving up on the project before the company gave the effort another chance.

Looking at the market opportunity for this sector, Biogen’s about-face no longer comes as a surprise.

For decades now, companies have been looking into ways to at least slow the progress of the condition, treat the symptoms, and offer faster ways to diagnose it.

There is currently no cure for this disease, which is ranked as the sixth leading cause of death in the country and accounts for approximately 2 million deaths globally.

Given that this disease takes years to progress, it means tens of millions of patients live with the condition on a daily basis -- and this sector comprise the target niche for Aducanumab.

In the United States alone, over 5 million people are diagnosed with Alzheimer’s disease annually and this number is projected to increase to nearly triple by 2050.

With all the treatments geared towards Alzheimer’s disease, sales for these products were estimated at $3.5 billion in 2018. This cost is expected to hit a 7.2% compound growth rate yearly until 2030.

If successful, Aducanumab can reach peak sales somewhere between $10 billion and $20 billion.

For context, the annual sales of Biogen today is only under $15 billion.

This underscores the significance of Aducanumab for the company as the drug can more than double its total earnings and even its market capitalization. It can also offer a 3x to 4x jump in Biogen’s share price.

Apart from Biogen, other big names working on an Alzheimer’s treatment are Eli Lilly (LLY) and Axsome Therapeutics (AXSM).

Outside Biogen’s work on Aducanumab, the company also has an impressive asset portfolio.

Its second quarter earnings results for 2020 showed that revenues from its multiple sclerosis drug segment contributed significantly to the company’s profits, with Ocrevus raking in $2.3 billion for the period.

The newly acquired rare spinal muscular atrophy disease drug Spinraza also performed well, reporting approximately $2 billion in annual sales.

Even its embattled multiple sclerosis treatment Tecfidera, which has been facing patent exclusivity issues with generic companies like Mylan (MYL), reported an increase from its notable $1 billion in revenue for the first quarter of the year to $1.2 billion in the second quarter.

Finally, Biogen has been working on expanding its biosimilar segment to increase its competitive advantage particularly for its drugs that are nearing the end of their patent exclusivity.

Amid the pandemic, Biogen’s revenue was up by 1% to hit $3.5 billion in the first quarter of 2020 and increased by 2% to reach $3.7 billion in the second quarter.

The company’s financial results also rose by approximately $100 million in the first three months of this challenging year.

However, a widely known caveat not only for Biogen but also for a number of biotechnology companies is the volatility of the stocks.

There is no one-size-fits-all formula for investing in beaten-up stocks. It comes with zero guarantees that their past performances would make a repeat either.

The strategy for these things though is quite basic. Make sure to look at businesses that offer sufficient bandwidth to bounce back once things normalize and the effects of the pandemic start to ease.

Looking at its overall performance, Biogen has achieved an impressively strong financial position despite the setbacks along the way. The company even offers room for growth regardless of the performance of its much-awaited Aducanumab.