Mad Hedge Biotech & Healthcare Letter

May 28, 2020

Fiat Lux

Featured Trade:

(ASTRAZENECA’S WASHINGTON FREEBIE)

(AZN), (MRK), (PFE), (JNJ)

Mad Hedge Biotech & Healthcare Letter

May 28, 2020

Fiat Lux

Featured Trade:

(ASTRAZENECA’S WASHINGTON FREEBIE)

(AZN), (MRK), (PFE), (JNJ)

The coronavirus disease (COVID-19) has pushed people to gamble on unproven and untested products for as long as these can offer even just a shred of hope.

Call it the grasping for straws strategy.

The latest biotechnology company granted this kind of confidence is AstraZeneca (AZN).

The U.S. Department of Health and Human Services (HHS) recently announced its decision to provide the cardiovascular heavyweight up to $1.2 billion in funding to speed up the company’s progress on AZD1222. The problem is that the vaccine has not been proven to work.

You would think that if the US government was going to blow $1.2 billion on an unproven vaccine at least it would be on an American company. That is not the case. Pre pandemic, a drug at this stage of development would not have earned the time of day.

The experimental vaccine is a gene therapy that AstraZeneca has been working on alongside Oxford University. Aside from the funding, HHS also committed to supporting the clinical trial for this vaccine which would involve 30,000 participants.

In return, the biopharmaceutical company has agreed to send up to 300 million doses of the vaccine to the US, with the first shipment expected to be sent before 2020 ends. AstraZeneca will also provide 100 million doses to Great Britain.

Before getting too excited on this news though, it’s critical to note that AZD1222 is not yet proven effective against COVID-19.

This proposed vaccine from Oxford is created from a weakened version of a common cold virus. It was then genetically altered to disable it from growing in humans. So far, over 1,000 individuals already received this vaccine during an early stage test that started in April.

The plan is for the two companies to use the same technique that the Oxford University researchers applied to fight the Middle East Respiratory Syndrome (MERS).

Based on the results of a small clinical trial, this approach managed to prevent the transmission of MER-CoV among the patients. The goal is to replicate this success and halt the spread of COVID-19.

With AstraZeneca securing a manufacturing capacity of 1 billion doses, the first deliveries of the vaccine are estimated to start by September.

Apart from the US and the UK, AstraZeneca is also tapping the Serum Institute of India along with other potential collaborators to boost the production of the COVID-19 vaccine.

While all these updates sound promising, it’s undeniable that choosing which stock to invest in this chaotic market is not for the faint of heart.

The pandemic has clouded the earnings landscape of practically all companies across the board for at least the rest of 2020, with the uncertainty possibly spilling into 2021.

So far, several vital members of various industries have already sought unprecedented levels of aid from the state. A glaring example of this is the ailing airline industry, which has been receiving the most help from governments across the globe.

Meanwhile, AstraZeneca’s shares are up nearly double from the March bottom.

Looking at its financial history, it can be said that AstraZeneca’s ability to swim against the current is due in large part to its top-quality clinical pipeline.

In 2018 alone, the company received a whopping 23 regulatory approvals in various fields including oncology, cardiovascular, and kidney disorders.

The latest product to boost AstraZeneca’s already potent pipeline is its collaboration drug with Merck (MRK) called Lynparza.

Previously approved as a treatment for ovarian and breast cancer, Lynparza is now approved as medication for prostate cancer as well.

This label expansion allows AstraZeneca and Merck to go head to head against Johnson & Johnson’s (JNJ) Zytiga and even Pfizer (PFE) and Astellas Pharma’s Xtandi.

In 2019, Lynparza’s annual sales increased by 85% primarily because of label expansions. The drug is anticipated to show a surge in its 2020 sales as well thanks to this recent approval.

However, the best is yet to come for AstraZeneca.

While the company has put on hold a couple of its clinical trials, reports show that it has many late-stage data readouts up its sleeve. Hence, investors should be on the lookout for these announcements in the next 24 months.

Due to all the new growth products and label expansions, AstraZeneca’s top line is projected to jump by 13.7% in 2021, making it one of the fastest forecasted growth rates in the industry at this point.

For even more good news, this biopharmaceutical powerhouse disclosed that it has no intention of revising its annual guidance despite the pandemic. This announcement is tangible proof of the economic staying power of AstraZeneca’s portfolio.

AstraZeneca stock is not exactly cheap though. With its recent developments and track record, the company has definitely gained a following in the biotechnology and healthcare sector. Nonetheless, AstraZeneca has proven that it deserves its top-shelf valuation.

![]()

Global Market Comments

May 19, 2020

Fiat Lux

Featured Trade:

(THE 2020 DARK HORSES OF BIOTECH)

(AMRN), (THOR), (SAN), (NBSE), (OHRP),

(MRNA), (MRK), (AZN), (VRTX), (RGLS), (ARWR)

One of our dark horses came in a big winner this morning.

No, I did not go to the Golden Gate Fields race track on San Francisco Bay and win big on a horse with 5:1 odds, although I might as well have.

Moderna (MRNA) soared to $85 this morning on news of a successful trial of a new Covid-19 vaccine. We recommended it on January 19 at $17.78 for precisely this reason.

Never mind that the trial only involved a mere eight patients, involved RNA, and won’t be available in bulk for two years. That’s all the market wants to hear today.

So, if you are interested in playing the long shot game, I am re-running my January 9 research piece, which was sent out to paid subscribers of the Mad Hedge Biotech & Healthcare Letter. If you want to subscribe to the letter, which has been pulling in long shots on a weekly bases recently, please click here.

For all the flak the healthcare sector has received for the exorbitant prices of its products and services, there’s no denying the fact that this industry had an incredibly remarkable decade -- and biotechnology proved to be one of the most lucrative markets when it comes to stocks that actually double or triple in value, sometimes even overnight.

The primary reason for this is that no one could predict the success or failure of clinical trials with any degree of accuracy, forcing investors to take into account elements of surprise in the valuation process in biotech.

Companies that analysts believe to be prime candidates for acquisition early on in their life cycle would end up repeatedly failing to lure viable tender offers for years. Meanwhile, dark horses emerge from the leftfield and snap up the best deals.

A good case in point would be how experts and investors alike missed the mark on Amarin Pharmaceutical’s (AMRN) cardiovascular treatment Vascepa. On the outset, analysts pegged the new prescription omega-3 treatment as a failure and a money sinkhole.

Instead, Vascepa surpassed all expectations and is now hailed as the fish oil supplement to demonstrate clear-cut cardiovascular benefits to high-risk heart attack patients.

In 2019 alone, Vascepa grew by 85% compared to its 2018 report, coming in between $410 million and $425 million in sales -- and 2020 is expected to be an even better year for this drug as sales are estimated to reach between $650 million and $700 million.

Another example is synthetic protein maker Synthorx (THOR), which was initially tagged as an ominous stock.

The company proved detractors wrong when it went on to fetch huge offers from giant biotech firms, with Sanofi SA (SAN) winning the bidding war over Synthorx to the tune of $2.5 billion.

This new year, though, promises to offer more predictability, especially on the merger and acquisition front.

Several blue-chip biotechs are on the verge of key patent expirations in the next decade. On top of that, these companies are facing tremendous pressure from US politicians to cut down on the prices of their brand name drugs. Today, the State of California announced that it was going into the generic drug industry to undercut the majors.

These dual headwinds are expected to fuel an uptick in the demand for bolt-on acquisitions, which can provide the giant biotechs with healthy levels of profit via large sales volumes as they attempt to slash their slashes to acceptable levels.

With this in mind, big biopharmas will be willing to shell out top dollar to acquire promising companies this 2020.

Which biotechs have the goods to take full advantage of this acquisition demand?

One up and coming company tagged as a red-hot acquisition candidate is NeuBase Therapeutics (NBSE).

Founded in 2018, this Pittsburgh company has raked in $9 million in funding so far to develop treatments that target rare, genetic neurological disorders. Neubase’s platform called peptide-nucleic acid antisense oligonucleotide or PATrOL technology was developed at Carnegie Melon University.

Basically, this technology offers gene-silencing therapies for its patients suffering from rare genetic disorders.

In July 2019, NeuBase engaged in a reverse merger with fellow biotech innovator Ohr Pharmaceuticals (OHRP). This partnership is expected to rake in massive rewards since both companies greatly complement each other’s work.

NeuBase’s work zeroes in on curing rare genetic diseases via gene-silencing treatments while Ohr’s research is geared towards helping patients suffering from cancer cachexia and macular degeneration.

The combined efforts of these two should result in a wider reach as they offer cutting edge treatments to highly lucrative and specialized markets.

As of December 2019, NeuBase has a recorded market cap of $114.38 million. Considering all its assets and the way its pipeline is shaping up, NeuBase could easily be your best sleeper stock in 2020.

Another biotech company to watch out for this year is Moderna Inc (MRNA), which has raised a whopping $1.8 billion in funding over 10 rounds.

So far, this company has attracted blue-chip companies in the form of Merck and Co (MRK), which invested $125 million, and AstraZeneca (AZN) with $474 million so far.

In terms of stability, Moderna has been doing quite well for itself with $68.2 million in estimated annual revenue.

In 2019, Moderna shared that it has at least 11 programs set for clinical trials along with 20 development candidates. Its research leans towards producing cancer vaccines and localized regenerative therapeutics.

Its strategic alliances not only with AstraZeneca and Merck but also with Vertex Pharmaceuticals (VRTX), Biomedical Advanced Research and Development Authority, and even the Bill & Melinda Gates Foundation equip Moderna with a remarkable competitive edge against rivals Regulus Therapeutics (RGLS), Arrowhead Pharmaceuticals (ARWR), and CureVac.

I’m expecting huge movements in the biotech market in 2020 as the curtain rises on all these promising technologies and the rise of this industry becomes impossible to ignore.

Mad Hedge Biotech & Healthcare Letter

May 12, 2020

Fiat Lux

Featured Trade:

(GLAXOSMITHKLINE’S ENTRY INTO THE COVID-19 VACCINE RACE)

(GSK), (VIR), (AZN)

It’s all-hands-on-deck for the biotech sector as the world battles the deadly coronavirus disease COVID-19.

As the US coronavirus-related deaths mount to over 80,000 and reported cases hitting over 1.3 million, the need to find a cure and vaccines increases in urgency every passing minute.

Joining the biotech companies throwing their hats into the ring is GlaxoSmithKline (GSK), which recently announced its decision to work hand in hand with Vir Biotechnology (VIR) in the search for a coronavirus cure.

On top of the collaboration efforts, the partnership will also involve GSK investing $250 million in Vir. According to these terms, each Vir share will be worth $37.73.

The collaboration announcement also pushed Vir shares to rise by as much as 34% and trading more than doubled. Meanwhile, (GSK) went up by roughly 2%.

The partnership will explore several platforms to come up with a treatment for COVID-19.

So far, the most promising candidates involve two antibodies presently dubbed as VIR-7831 and VIR-7832. Both were developed by Vir as treatments for SARS, which is also caused by a coronavirus.

Actually, these antibodies were developed using samples from a patient who recovered from SARS. However, these could also be produced artificially.

(GSK) and Vir estimate that Phase 2 clinical trials will commence in three to five months.

Apart from these antibody treatments, the two companies are also looking into utilizing CRISPR screening technology to figure out which proteins are used by the coronavirus to infect the healthy cells.

Once they identify these, (GSK) and Vir could come up with drugs that block viral infection. That is, they can use the information to create a vaccine to be used not only for COVID-19 but also for other types of coronaviruses.

According to (GSK), the Vir proteins had been identified as “highly potent” when targeted at the coronavirus in the laboratory.

If all goes well, a coronavirus vaccine could be on its way in 12 to 18 months.

Aside from (GSK), Vir also has an ongoing collaboration with another bigwig biotech, Biogen (BIIB).

This isn’t the first venture of (GSK) in looking for a COVID-19 cure though.

The British biotech giant is also working with China’s Xiamen Innovex on another potential coronavirus vaccine.

In addition, (GSK) is looking into forming a joint laboratory with AstraZeneca (AZN) to assist the UK government in stretching and expanding its supplies for COVID-19 diagnostic tests.

Although diagnostics are not part of their primary efforts, the goal is for the two big biotechs to determine the best ways to help in detecting the spread of COVID-19.

While these efforts to help find a solution to the pandemic are at the forefront of the biotech world today, GSK has a lot more to offer.

(GSK) manufactures products that people need to take on a regular basis.

The need is so great that the company actually allocates 80% of its research efforts focused on drug development for various issues like oncology, immuno-inflammation, and HIV. These treatments are vital to the daily existence of so many patients across the globe.

Meanwhile, (GSK) also aims to streamline its business and focus on the research and development of products and services. Hence, it decided to split its businesses into two.

One will be geared towards pharmaceutical efforts. The second will be focused on consumer health.

This is an excellent move in ensuring that (GSK) maximizes its potential to dominate its chosen markets.

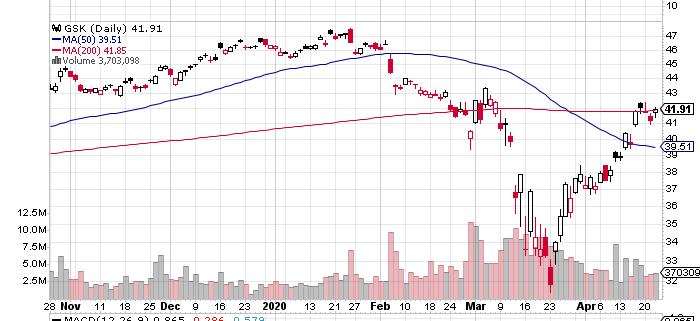

Throughout the years, (GSK) has demonstrated its capacity to grow while delivering a strong bottom line. From 2015 until 2019, the biotech giant’s sales increased by over 40% with its operating margin rising as well.

While it’s undeniable that this global biotech stock has gotten itself caught up in the COVID-19 whirlwind that managed to hurt virtually every sector, its downside alternative makes absolutely no sense.

No one has the ability to predict and control when they get sick or what type of illness they get afflicted with, which makes the biotech sector and specifically drug developers particularly safe bet whatever the financial climate is.

So, investors looking for a stable stock can now afford to buy (GSK) shares at approximately 10 times worth of next year’s per-share profit potential. As if that’s not enough, the company also offers a mouthwatering 7.5% dividend yield.

Keep in mind that a wise way to insulate your portfolio amid the fears of a market crash is through investing in stable businesses that offer products and services needed on a daily basis.

If the companies provide essential items in both good and bad times, it’s a good sign the stocks will be able to survive any market crash.

(GSK), which is currently at an 11-year low due to the pandemic and economic crisis, is worth considering.

![]()

Mad Hedge Biotech & Healthcare Letter

January 9, 2020

Fiat Lux

Featured Trade:

(THE 2020 DARK HORSES OF BIOTECH)

(AMRN), (THOR), (SAN), (NBSE), (OHRP),

(MRNA), (MRK), (AZN), (VRTX), (RGLS), (ARWR)

For all the flak the healthcare sector has received for the exorbitant prices of its products and services, there’s no denying the fact that this industry had an incredibly remarkable decade -- and biotechnology proved to be one of the most lucrative markets when it comes to stocks that actually double or triple in value, sometimes even overnight.

The primary reason for this is that no one could predict the success or failure of clinical trials with any degree of accuracy, forcing investors to take into account elements of surprise in the valuation process in biotech.

Companies that analysts believe to be prime candidates for acquisition early on in their life cycle would end up repeatedly failing to lure viable tender offers for years. Meanwhile, dark horses emerge from the leftfield and snap up the best deals.

A good case in point would be how experts and investors alike missed the mark on Amarin Pharmaceutical’s (AMRN) cardiovascular treatment Vascepa. On the outset, analysts pegged the new prescription omega-3 treatment as a failure and a money sinkhole.

Instead, Vascepa surpassed all expectations and is now hailed as the fish oil supplement to demonstrate clear-cut cardiovascular benefits to high-risk heart attack patients.

In 2019 alone, Vascepa grew by 85% compared to its 2018 report, coming in between $410 million and $425 million in sales -- and 2020 is expected to be an even better year for this drug as sales are estimated to reach between $650 million and $700 million.

Another example is synthetic protein maker Synthorx (THOR), which was initially tagged as an ominous stock.

The company proved detractors wrong when it went on to fetch huge offers from giant biotech firms, with Sanofi SA (SAN) winning the bidding war over Synthorx to the tune of $2.5 billion.

This new year, though, promises to offer more predictability, especially on the merger and acquisition front.

Several blue-chip biotech’s are on the verge of key patent expirations in the next decade. On top of that, these companies are facing tremendous pressure from US politicians to cut down on the prices of their brand name drugs. Today, the State of California announced that it was going into the generic drug industry to undercut the majors.

These dual headwinds are expected to fuel an uptick in the demand for bolt-on acquisitions, which can provide the giant biotech’s with healthy levels of profit via large sales volumes as they attempt to slash their slashes to acceptable levels.

With this in mind, big biopharma’s will be willing to shell out top dollar to acquire promising companies this 2020.

Which biotech’s have the goods to take full advantage of this acquisition demand?

One up-and-coming company tagged as a red-hot acquisition candidate is NeuBase Therapeutics (NBSE).

Founded in 2018, this Pittsburgh company has raked in $9 million in funding so far to develop treatments that target rare, genetic neurological disorders. Neubase’s platform, called peptide-nucleic acid antisense oligonucleotide or PATrOL technology, was developed at Carnegie Melon University.

Basically, this technology offers gene-silencing therapies for its patients suffering from rare genetic disorders.

In July 2019, NeuBase engaged in a reverse merger with fellow biotech innovator Ohr Pharmaceuticals (OHRP). This partnership is expected to rake in massive rewards since both companies greatly complement each other’s work.

NeuBase’s work zeroes in on curing rare genetic diseases via gene-silencing treatments while Ohr’s research is geared towards helping patients suffering from cancer cachexia and macular degeneration.

The combined efforts of these two should result in a wider reach as they offer cutting-edge treatments to highly lucrative and specialized markets.

As of December 2019, NeuBase has a recorded market cap of $114.38 million. Considering all its assets and the way its pipeline is shaping up, NeuBase could easily be your best sleeper stock in 2020.

Another biotech company to watch out for this year is Moderna Inc (MRNA), which has raised a whopping $1.8 billion in funding over 10 rounds.

So far, this company has attracted blue-chip companies in the form of Merck and Co (MRK), which invested $125 million, and AstraZeneca (AZN) with $474 million so far.

In terms of stability, Moderna has been doing quite well for itself with $68.2 million in estimated annual revenue.

In 2019, Moderna shared that it has at least 11 programs set for clinical trials along with 20 development candidates. Its research leans towards producing cancer vaccines and localized regenerative therapeutics.

Its strategic alliances not only with AstraZeneca and Merck but also with Vertex Pharmaceuticals (VRTX), Biomedical Advanced Research and Development Authority, and even the Bill & Melinda Gates Foundation equip Moderna with a remarkable competitive edge against rivals Regulus Therapeutics (RGLS), Arrowhead Pharmaceuticals (ARWR), and CureVac.

I’m expecting huge movements in the biotech market in 2020 as the curtain rises on all these promising technologies and the rise of this industry becomes impossible to ignore.

Mad Hedge Biotech & Healthcare Letter

November 14, 2019

Fiat Lux

Featured Trade:

JUMP ON THE ASTRAZENECA BANDWAGON

(AZN)

AstraZeneca plc (AZN) has shown a dramatic turnaround over the past three years, crushing its close competitors in the big biopharma landscape. Posting growth for the fifth straight quarter for both profit and sales, the stock has gained more than 10% in the run-up to its latest earnings report.

This pushed the company’s total stock market gains for 2019 to a stellar 33.4%. From a forward-looking price-to-earnings perspective though, investors must remain cautious as the stock also now sports a high valuation.

One of the reasons for the stock’s soaring performance this year is the promising cancer drug lineup, which is the result of AstraZeneca’s risky move to splurge on the development of these products way back in 2014.

Now, although no hard data has been disclosed to the public to date, AstraZeneca’s oncology lineup has been pegged to give Merck & Co.’s (MRK) Keytruda and Bristol-Myers Squibb Co.’s (BMY) Opdivo a run for their money in the lucrative lung cancer drug market.

AstraZeneca is anticipated to release survival data by 2020, with its acquired company Pearl Therapeutics taking charge of testing the effectiveness of Imfinzi to treat non-small cell lung cancer. The robust competition presented by both Bristol’s Opdivo and AstraZeneca’s Imfinzi is projected to carve out $2.5 billion from the sales of Merck’s cash cow Keytruda from 2021 to 2028.

Aside from Imfinzi, AstraZeneca has also raked in increasing revenue from another NSLC drug Tagrisso and ovarian cancer medication Lynparza.

Sales of AstraZeneca’s cancer drugs jumped 48% to hit $2.3 billion in the third quarter of 2019. In the first half of the year, total revenue from the company’s oncology lineup alone soared 52% year over year.

AstraZeneca’s largest moneymaker at the moment, Tagrisso, contributed more than $1.4 billion in the first six months of the year, jumping by 86% compared to the same period in 2018. The surge brought about by this strong cancer drug lineup resulted in a 16% rise in the company’s earnings in the third quarter, hitting $6.1 billion.

While these results are impressive, AstraZeneca’s cancer drug sales have yet to reach their peak. As impressive as Tagrisso has been in the first half of 2019, the other two cancer drugs of the company are actually outperforming this product.

One is Imfinzi, which saw its sales skyrocket by 248% during the same period, raking in $633 million. Meanwhile, Lynparza sales practically doubled to reach $520 million.

While its US sales remain competitive with the company achieving 17% revenue growth, AstraZeneca’s initiatives to expand to the Chinese market have also started to pay off. In fact, earnings from this East Asian country account for almost a fifth of the company’s revenue.

Sales in China continued its positive streak, rising 40% to reach $1.28 billion. To sustain this momentum and strengthen its stronghold in the market, the company recently announced its move to invest $1 billion to develop healthcare startups in the Middle Kingdom. This makes AstraZeneca the latest biopharma behemoth to place a bet on the second-biggest pharmaceuticals market in the world.

With all these in mind, it’s almost impossible to handicap the long-term outlook for AstraZeneca. The company currently has an impressive nine-drug lineup all set to turn into blockbusters this year.

Although the loss of patent exclusivity for cardiovascular disease moneymaker Crestor definitely affected the company, its move to transform its cancer drugs into core growth drivers has been quite successful thus far.

Bolstering its pillars of growth is AstraZeneca’s focus on building on its high-value lung cancer lineup particularly on Imfinzi and Tagrisso. Its emerging cardiovascular drug line has also been garnering attention, making heart medication Brilinta and diabetes treatment Farxiga the next blockbusters for the company.

On top of these, AstraZeneca has been actively developing potent combinations involving mantle cell lymphoma treatment Calquence and Lynparza. Needless to say, the company’s clinical pipeline has presented itself as one of the most promising in the biotech world today.

From where things stand at the moment, AstraZeneca appears to be vindicated in fighting for its standalone strategy and pushing back from the $118 billion hostile takeover attempt of Pfizer in 2014.

In increasing its footprint in emerging markets, AstraZeneca has transformed itself into a biotech company with the potential to dominate the industry in the years to come.

Buy AstraZeneca with both hands on the next dip.