Global Market Comments

March 29, 2019

Fiat Lux

SPECIAL FANG ISSUE

Featured Trade:

(FINDING A NEW FANG),

(FB), (AAPL), (NFLX), (GOOGL),

(TSLA), (BABA)

Global Market Comments

March 29, 2019

Fiat Lux

SPECIAL FANG ISSUE

Featured Trade:

(FINDING A NEW FANG),

(FB), (AAPL), (NFLX), (GOOGL),

(TSLA), (BABA)

Mad Hedge Technology Letter

February 7, 2019

Fiat Lux

Featured Trade:

(THE DEATH OF THE COLLEGE DEGREE),

(GOOGL), (IBM), (AAPL), (BABA), (BIDU)

If you’re an educator not at a top 25 American university, you might want to stop reading right now.

Disruption.

You’re either on the right or wrong side of it.

I’ve detailed numerous subsets of the economy and society that have been transformed by sharp shifts in technological innovation.

But the one industry that has stealthily moved into the heart and center of technological disruption is education.

For centuries, universities and higher learning institutions had a stranglehold on critical information required to successfully perform in the cutting-edge knowledge economy of those times.

Then on September 15, 1997, a mere 21 years ago, Google search launched its free services to the world and grabbed the monopoly of information away from the college system.

This website effectively caused the cost of information to crater to zero and its free website is ranked #1 as of February 2019 with over 4.5 billion monthly active users.

The ensuing 21 years has been a renaissance in the ability to distribute information propelled by this one platform, and the result is that billions have the ability to study and read up on what they want and when they want.

The ability to learn for free combined with a tight labor market is a promising landscape for job seekers, with analysts forecasting more opportunities for professionals without a degree.

Job-search site Glassdoor amassed a list of various employers no longer bound by requiring applicants to possess a 4-year bachelor’s degree.

These firms aren’t your second-rate companies either made up of gold standard workplaces such as Google, Apple, and IBM.

In 2017, IBM's vice president of talent Joanna Daley confided that about 15% of IBM’s new hires don't have a four-year bachelor qualification.

She emphasizes hands-on experience through coding boot camp or industry-related vocational classes as explicit criteria to get hired.

This development bodes poorly for the future of universities and boosts the prospects of alternative education.

Online college offers working adults ample flexibility in furthering their education.

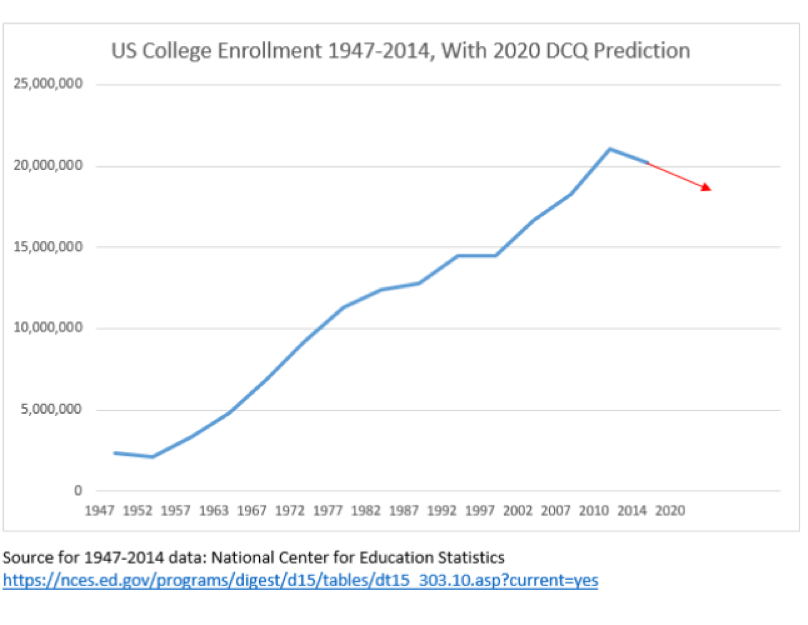

According to the most recent federal statistics from 2016, roughly one out of every three, or 6.3 million college students learned online.

Even though online courses are becoming more widespread, the best and brightest aren’t attending these schools.

However, it did hijack the marginal student that was on the fence for a 4-year university and brought them into the orbit of for-profit online courses and the revenues that came with it.

That was the first stage of online forces imposing financial pressure on the education marketplace.

Now analysts are discovering the second major trend with higher rated students opting out of the university system altogether.

In many cases, a 4-year university degree is a bad value proposition.

Why is that?

Costs.

In a capitalistic economy that lives and dies by the mantra of buy low and sell high – universities seem to be getting sold short lately.

The exorbitant costs to obtain a 4-year degree has led to an outsized student debt bubble and removed the mystique of this once treasured qualification.

A growing chorus of bipartisan voices has pigeonholed student debt as a major problem across the country.

In the previous presidential election, Democratic candidate Bernie Sanders called this situation “outrageous” as national student debt has spiraled out of control to the amount of $1.5 trillion.

This has been a terrible commercial for the younger generations to follow in the footsteps of the indebted Millennial generation.

And with Generation Z tech savvy at building stand-alone firms buttressed by Instagram and YouTube platforms, why go to college anymore?

Or to nail one of those jobs developing iPhones in Cupertino, why not take a few coder boot camps and self-develop a portfolio impressive enough to score an Apple interview?

The bottom line is that there are workarounds for a fraction of the price.

And because tech firms have outpaced analog companies in salaries and hiring for the past two decades, there is an outsized bias on compiling technical skills that will lead a candidate down a path to a salary of over $100,000 quicker than a 4-year degree can.

Not many other industries can claim the same.

The cracks are beginning to reveal themselves in the overall university apparatus.

Universities had years of record revenue that they reinvested into the system to enhance programs, staff, buildings, stadiums, and infrastructure.

The financial catalyst was the rise of the Chinese college student.

The latest statistics nailed the number of Chinese nationals in America studying for 4-year degrees at over half a million.

Many of those were trained up with engineering-related degrees and bolted back home to find jobs at Baidu (BIDU), Tencent, or Alibaba (BABA) powering Chinese Inc.

However, the drop off in demographics from young Chinese and Americans are forcing universities to fight for a shallower pool of candidates with less attractive degrees relative to the value of degrees of past generations.

The second-tier universities are hardest hit with examples galore.

Alcorn State University in Mississippi saw a dramatic 69.45% decrease in applications in 2018 and its rural location didn’t help either.

Alabama State University is feeling the pinch with a 33.06% drop in application in recent years.

If you thought the University of New Orleans was clawing its way back to relevancy after Hurricane Katrina, you are mistaken with its 38.23% drop in applications.

Military schools haven’t been spared either with applications to The United States Air Force Academy crashing 28.12% over the past ten years.

A confluence of deadly trends is about to beset the university system and schools will likely go bust.

Technology is giving a reason for students to bypass the system while also speeding up the financial timebombs many universities are about to confront.

Then we must ask ourselves, will universities even exist in the future?

Probably, but perhaps just the top 25 elite schools that are still worth the high costs.

Mad Hedge Technology Letter

January 15, 2019

Fiat Lux

Featured Trade:

(THE BALKANIZATION OF THE INTERNET),

(AAPL), (FB), (CTRP), (PDD), (BABA), (JD), (TME)

The Mad Hedge Technology Letter has a front-line seat to the carnage wrought by the balkanization of technology that is swiftly descending across all corners of the tech universe.

In technology terms, this is frequently referred to as “splinternet.”

A quick explanation for the novices can be summed up by saying splinternet is the fragmenting of the Internet causing it to divide due to powerful forces such as technology, commerce, politics, nationalism, religion, and interests.

The rapid rise of global splinternet news stories will have an immediate ramification on your tech portfolio and it’s my job to untangle the knots.

What investors are seeing is the bifurcation of the global tech game into a binary world of Chinese and American tech.

Most recently, Central European country Poland, who was thought to be siding with the Chinese because of the growing presence by large-cap Chinese tech in Warsaw, announced government security had arrested a Huawei employee, Chinese national Wang Weijing, for allegedly spying on behalf of the Chinese state.

For all the naysayers that believe the administration’s hope of curtailing the theft of western technology was a bogus endeavor, this recent event buttresses the notion that Chinese state-funded tech companies are truly running nefariously throughout the world.

In fact, Poland has little to gain from this maneuver if you take the current status quo as your guidebook, and I would argue it is a net negative for Poland because Chinese tech is deeply embedded inside of the Poland tech structure bestowing profits and internet capabilities on multiple parties.

Making the case stronger against China, Poland has no flagship tech communications company that would serve as competition to the Chinese or could directly gain from this breach of trust.

The fringe of the Eurozone Central European nations and Eastern European countries bordering Russia running developing economies rely on Huawei and other low-cost Chinese tech suppliers like ZTE to offer value for money for a populace who cannot afford $1000 Apple (AAPL) iPhones and exorbitant western European telecommunications infrastructure equipment.

The Chinese beelining to this burgeoning area in Europe has given these less developed countries high-speed broadband internet for $10-$15 per month and 4G mobile service for $7 per month, a smidgeon of what westerners fork out for the same monthly service.

Poland rebuffing Huawei is an ominous sign for Chinese tech doing business in the Czech Republic and Hungary as European countries are moving towards denying Huawei in unison.

The last few years saw China create the same recipe of success for fueling economic expansion mimicking the American economy.

The tech sector led the way with outsized gains boosting productivity while analog companies transformed into digital companies to take advantage of the efficiencies high-tech provides.

At the same time, Beijing has initiated a muscular response to the accelerated growth of local tech companies.

The foul play of American tech in Europe has given impetus to Beijing to launch a power grab on local tech structures such as Baidu, Alibaba, and Tencent.

This couldn’t be more evident at Tencent who has failed to secure any new gaming licenses for their best gaming titles.

PlayerUnknown’s Battlegrounds (PUBG), a battle royale multiplayer, has been deprived of massive revenue because of Tencent’s inability to win a proper gaming license from the Chinese authorities to sell in-game add-ons.

In total, lost revenue has already cost Chinese video game companies over $2 billion in revenue since May 2017.

Beijing wants to temper the growing clout of private tech companies who were the recipient of the Chinese consumer’s gorge on technology in the last 20 years.

These companies have never been more infiltrated by the communist party and this can be mainly attributed to the acknowledgment by Beijing that Chinese tech companies are too powerful for their own good now and are a legitimate threat to the powers above.

That is what the sudden retirement of Founder of Alibaba Jack Ma told us who infuriated Chairman Xi because Ma was the first Chinese of note to meet American President Donald Trump at Trump Towers pledging to create a million jobs in America.

Ma later rescinded that statement and was put out to pasture by Beijing.

What does this all mean?

As the broad-based balkanization spreads like wildfire, Chinese and American tech companies’ addressable markets will shrink hamstringing the drive to accelerate revenue.

The potential loss of Europe for the Chinese could give way to Nokia, Siemens, and other western telecommunication companies to move in hijacking a bright spot for Huawei.

If Apple isn’t punching above their weight in China, well that almost certainly means that local tech companies aren’t having a cake walk in the park as well.

The winter sell-off turned the screws on tech first and then the rest of equities obediently, Chinese tech could have a similar domino effect to the Chinese economy boding badly for Chinese ADRs listed on the New York Stock Exchange (NYSE).

Last year, the Shanghai index was one of the worst performing stock markets in the world.

And if the trade wars are really ravaging a few key limbs from local Chinese tech firms, then companies exposed to the Chinese consumer such as Alibaba (BABA), JD.com (JD), Pinduoduo (PDD), Ctrip.com International (CTRP) and Tencent Music Entertainment (TME) could fall off a cliff.

This has already been in the works.

These companies are a good barometer of the health of the Chinese consumer and have had an abysmal last six months of price action.

The vicious cycle will repeat itself with worsening Chinese data drying up the demand for Chinese tech services and the Chinese consumer tightening their purse strings as they try to save money from a cratering economy.

It could become a self-fulfilling prophecy and that is what other indicators such as negative automobile sales and a rapidly failing real estate market are telling us.

The 65 million ghost apartments dotted around China don't help.

This could be the perfect opportunity to instigate wide-ranging reforms to open up the financial, insurance, a tech market to the west, something many analysts thought China would do after joining the World Trade Organization (WTO).

However, Beijing’s retrenchment preferring to pedal mercantilism and cold-blooded power grabs could offer Chairman Xi the prospect of further consolidating his authority by sticking his fingers deeper into the local tech structures giving the state even more control.

I would guess this is a false dawn.

American tech will confront balkanization headwinds of its own evidence in Vietnam as the government blamed Zuckerberg’s Facebook (FB) for failing to root out anti-government rhetoric which is illegal in the communist-based country.

If you haven’t figured it out yet – there is an underlying suitability issue with western tech services that tie up with authoritarian governments.

It many times leads the western tech companies to be a pawn in a political game that later turns into a bloody mess.

The weak rule of law has spawned a convenient practice of blaming western tech to distract from internal disputes strengthening the nationalist case of a purported western tech firm gone rogue.

This could lead Facebook to be removed in Vietnam, and the $238 million in ad revenue that will vanish.

Headaches are sprouting up across Europe with Facebook clashing with more stringent data privacy rules through General Data Protection Regulation (GDPR).

German’s largest national Sunday newspaper Bild am Sonntag claimed from sources that the Federal Cartel Office will summon Facebook to halt collecting some user data.

This could take a machete to ad revenue in a critical lucrative market for Facebook, and this experience is being echoed by other American tech companies who are running full speed into complicated regulatory quagmires outside of America.

Adding benzine to the flames, Deputy Attorney General Rod Rosenstein speaking at a cybercrime symposium at Georgetown University’s Law Center in Washington added to the tech misery explaining that to “secure devices requires additional testing and validation—which slows production times — and costs more money.”

This is not bullish to the overall tech picture at all.

Hamstringing tech is not ideal to promoting economic growth, but the decades of unchecked growth is finally reverting back to the mean with regulation rearing its unpretty head and the balkanization of tech forcing countries to pick between China or America.

The silver lining is that the American economy remains resilient taking the body blows of a government shutdown, interest rate drama, and trade war uncertainty in full stride.

The net-net is that American and Chinese tech firms could experience decelerating revenue growth far dire than any worst-case scenario forecasted by industry analysts.

Therefore, I forecast that American tech shares have limited upside for the next 6-10 weeks and Chinese tech is dead money in that same time span.

Any rally is ripe for another sell-off if there are no meaningful breakthroughs in the trade war and if China’s economic data continues to falter.

The global growth scare could actually come home to roost.

The supposed narrowing of trade differences has been nothing more than tactical, and procuring any fundamental victories is a hard ask in the short term.

In an ideal world, China would open the floodgates and allow the world to join them in an economic détente, however, based on Chairman Xi’s record of purging his mainland enemies and the military, slamming the gates shut and padlocking them seems more likely at this point.

Seizing the rights to an untimed Chairmanship term has its perks – this is one of them and he is using the entire assortment of options available to him.

Traders should look at deep in-the-money vertical bear put spreads on any sharp rally to specific out-of-fashion tech names saddled with regulatory and data balkanization headwinds, or tech firms with a large footprint in mainland China.

Mad Hedge Technology Letter

January 3, 2019

Fiat Lux

Featured Trade:

(HOW TO TAKE OVER THE WORLD),

(SFTBY), (BABA), (NVDA)

The wild west of the data wars is spawning into an all-out, gunslinging shoot-out with a winner-takes-all mentality.

This slugfest is reminiscent of the unregulated 19th-century American oil barons whose clout and complete control of the supply of oil fueled the industrial revolution that drove America's economy to the top of the global food chain.

Yes, data has become the oil of the 21st century. It is the oxygen of the next leg of the Internet revolution.

And there is one man moving early to stake out the premium real estate of our futures: SoftBank's Masayoshi Son.

His $100 billion SoftBank Vision Fund is not only creating waves in Silicon Valley but tidal waves.

Many countries, such as Iran, Saudi Arabia, and Russia, still rely on petroleum for the lion's share of government revenues. Saudi Arabia is attempting to wean themselves from the reliance on oil, but teething pains are sprouting up everywhere.

The choreographed killing of former Saudi Arabian dissident Jamal Khashoggi at a Saudi Arabian Embassy in Turkey will have many unintended consequences to the future economy further delaying the supposed pivot to a legitimate knowledge economy.

Oil prices crashing offers less financial support to make this pivot even possible.

Even though oil is still integral to the growth of the global economy, there is a new sheriff in town: big data.

Cut it up any way you want, data is simply information, the "zeros" and "ones" that make up the digital world. The information that commands mouthwatering premiums these days can be unraveled by computers.

Computer-deciphered data can show behavioral and consumer trends in stark daylight, helping companies ferret out business strategies that are proving immensely powerful.

There is an exponential hockey stick effect going on here. As the quantity of data accumulates, the more valuable it becomes.

The types of data being collected are personal data, transactional data, web data, and sensor data used for IoT (Internet of Things) products.

Who is the major player vacuuming up this data?

Masayoshi Son, the CEO of SoftBank (SFTBY), is an ethnic Korean who grew up in a small village in Japan. He transferred to Serramonte High School on the San Francisco Peninsula as a bustling youth and graduated in three weeks.

He was and still is that brilliant.

Son ventured on to UC Berkeley majoring in economics and computer science. He is one of the most dynamic people in the world and has amassed personal wealth of around $25 billion.

A few of his brilliant preemptive strikes were seed-investing in Yahoo, creating Yahoo Japan, and a $20 million for a stake in Alibaba (BABA) in 1999. These investments increased more than 100-fold in value.

Son is on a mission to own or control assets that are the linchpin to global growth nourished by Artificial Intelligence in selective industries such as transportation, food, work, medicine, and finance.

The solid anchor that ties all these firms together is the massive hordes of harvested data which are central to directing how future automated robots and machines perform.

His goal envisions the construction of responsive robots that will emerge as the cash cow in 2045. The construction, utilization, and high performance of these machines will be the key to his vision.

Instead of splurging for premium human data, investors will be competing for the best performing robots and the data derived from them. Accurate human data will provide the springboard to the machine data these robots will generate.

After the first generation of robots endows us with their first batch of data, all human data will be irrelevant. Human information is the test case on which robots are founded.

Once the first cohort of robot data comes to market, the second generation of robots will be derived off the first generation of robots.

Humans and the data generated from us will become irrelevant.

Once you marry the treasure trove of data with A.I., the results will enter the realm of today's science fiction. Imagine being the first CEO to bring functional robots to mass market and how valuable that first tranche of robot data would represent.

Priceless.

Son is positioning himself to organically engineer the highest-grade robots catalyzing the next gap up in global competition.

This year, Son is on a global treasure hunt to meld together the most precise "big data" he requires to build his robot squadron that will take over the world.

The fight these days is acquiring the oxygen to power these non-human contraptions. Without pure oxygen, i.e. massive amounts of data, engineers will create faulty, error-prone robots that underperform and are less valuable.

Looking at the amalgam of companies in which Son has bet on, it is difficult to decipher any rhyme or reason. That is until you find the commonality of big data.

Son invested $200 million in "Plenty" in July 2017, a company developing indoor farms. If indoor farm data is not diverse enough, then how about the $300 million he showered on the San Francisco dog-walking app called "Wag."

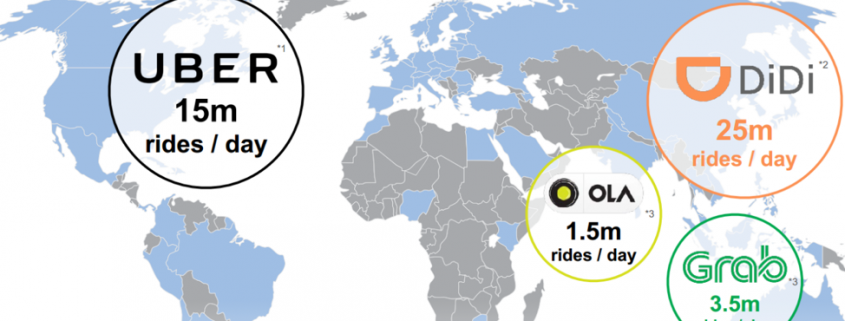

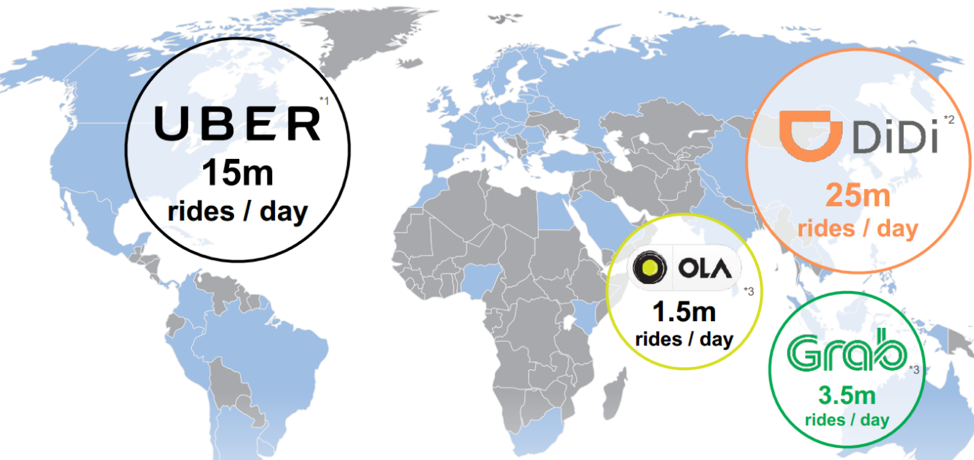

The biggest holding in the SoftBank Vision Fund is Uber. For those without an Internet connection, Uber is ubiquitously known as a ride-sharing company that shuttles passengers from spot A to spot B.

Sweetening the deal was a substantial discount the Vision Fund received on a private placement of Uber shares. Uber is now worth about $70 billion and may someday become a FANG in its own right.

Supplementing this transaction is the custom online map app Mapbox, founded as a competitor to Google Maps. Some of Mapbox's partners include Snapchat, Lonely Planet, and The Weather Channel.

Vision Fund's second largest position is ARM Holdings which is an English semiconductor chip company that has carved out a large segment of the Android and laptop market.

It produces simple CPUs (central processing units) and much more advanced GPUs (graphics processing units) that are placed in smartphones, TVs, tablets, and computers.

Son has shelled out $8.2 billion through the SoftBank Vision Fund already, and the remaining 75% stake is owned by parent company SoftBank Group. ARM is one of the shining beacons of European tech and SoftBank has pegged its future to its success.

There are even whispers of a second $100 billion vision fund lurking around the corner.

Unsurprisingly, Nvidia (NVDA) is the third-largest weighting, and the $5 billion SoftBank investment into Nvidia (NVDA) represents a 4.9% stake in the company. The Nvidia commitment is logical considering ARM licenses its chip designs to Nvidia.

As autonomous vehicles will be one of the first benefactors from the cross-pollination between big data and automation, these investments completely justify Son's long-term vision.

Son has also snapped up other ride-sharing entities such as Didi Chuxing in China, Ola in India, Grab in Southeast Asia, and 99 in Brazil.

Some 31% of the global population is without Internet connectivity. Thus, Son bought OneWeb which pioneers low-cost, high-quality satellites striving to grant Internet access for the people still without access. This maneuver will surely see his net data load increase.

In many of the Mad Hedge Technology Letters, we often offer readers the creme de la creme of public stock symbols, but this time it is different.

First, the major holdings in the SoftBank vision fund, aside from Nvidia, are privately held companies that do not trade on any stock market.

However, it is very important to watch what he buys as it gives insights into the best-performing, fastest-growing sub-sectors of technology and a comprehensive barometer or tech risk appetite from higher echelon VCs.

Or you could just buy SoftBank itself whose shares have doubled over the past two years.

Giving further color to the backstory, not all is doom and gloom for Saudi Arabia as they have invested heavily into the Vision Fund giving Son a key source of financing.

Son’s relationship with the Saudis is important to spearheading a 2nd Vision Fund which he hopes to deploy shortly.

Readers must not forget that 40% of the $100 billion constitutes debt and must be serviced forcing Son to supercharge the growth of the companies he purchases to maintenance his monthly debt bills.

Son won't just flip these companies for a 30% or 50% profit. Tenfold, or hundred-fold gains are the order of the day and that is exactly what he has been successful at.

In reality, Son's ultimate goal is to leach out the future aggregate data spewing from his underlying portfolio and cross-pollinate it with A.I. and automation to revolutionize the world while becoming the richest man in the world.

As 5G is literally on our doorstep, Son, large tech firms, China, and the rest of the VC universe are jockeying with each other and staunchly positioning themselves accordingly for the next 30, 40 and 50 years.

Welcome to the future and good luck.

Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(THE HIGH COST OF DRIVING OUT

OUR FOREIGN TECHNOLOGISTS),

(EA), (ADBE), (BABA), (BIDU), (FB), (GOOGL), (TWTR)

Mad Hedge Technology Letter

November 28, 2018

Fiat Lux

Featured Trade:

(TRUMP'S TARIFF THREAT FOR APPLE))

(AAPL), (BABA), (EBAY), (WMT), (FB), (MSFT), (AMZN)

The administration’s threat of levying 10% on iPhones is a great sign for the technology sector as a whole.

The short-term media sensationalism has flipped this story the other way around crying about this as if it is a major penalty to Apple (AAPL).

Don’t get me wrong, these potential stiff tariffs have the possibility of triggering a $1 billion loss on Apple’s revenue, but this is all about protecting American technology long term.

This is not like taking a sledgehammer and ruining their business model, and it will not strip away this brilliant wealth creation vehicle.

Apple remains a cheap stock to buy for patient long-term holders and is one of the best run companies in the world with an operating maestro executing the roll-out of premium products named Tim Cook, the CEO of Apple.

The administration might not like some of technology firms’ tactics, but in reality, they are a pivotal reason why the economy has been humming along in the longest bull-market ever.

Effectively, the administration has put Apple and its peers up on a pedestal and is defending them from Chinese competition.

What industry wouldn’t want this?

Most of 2018, the current administration presided over a stock market that was going up in a straight line and the bulk of those gains were harvested by the major tech companies, mainly the FANGs.

The administration was quick to take credit for a strengthening stock market and would like to see rates suppressed to engineer more upside.

The FANGs are going through a reversion to the mean after 100% gains and giving back 20% or 30% of profits offer opportune entry point for long-term investors.

The only FANG that needs a structural change is Facebook (FB) and has the funds to do it. The other three plus Microsoft (MSFT) will lead the tech charge when the short-term weakness subsides.

If you think Chinese consumers would bail on Apple products because of the trade war, then you are wrong.

Apple has been grandfathered into Chinese society and it is one of the few iconic American products that can boast this achievement.

Apple is a luxury brand produced by an epochal superpower.

The presence of Apple products reverberates around China’s economic landscape, and even if Chinese people do not like America, they respect its economic prowess and wish to learn from its capitalistic ways.

This is the main reason they send their kids to American universities.

Historically, China was once entirely dependent on Russia to fill in its economic and social vision with the communist party sending its best and brightest to Moscow to study the Soviet Union’s secret sauce.

If you go to Beijing now, most of the second ring road of flats conspicuously remind me of Khrushchyovkas, the unofficial name of a type of low-cost, concrete-paneled or brick three- to five-storied apartment building which was developed in the Soviet Union during the early 1960s.

During this time, its namesake Nikita Khrushchev directed the Soviet government.

Pre-Deng Xiaoping Soviet influences can still be found everywhere in central Beijing.

Once the Chinese communist government realized that the Soviet model impoverished large swaths of society, they went on the open market to find a more optimal method to run their economy that could take advantage of their monstrous man power.

The model they decided on was a fusion of communism and capitalism, and for 30 years, this system fueled Chinese peasants out of poverty and to the promenades of Saint-Tropez.

Because of Chinese laser-like obsession on social status, material possessions are the most important way for them to differentiate against each other.

For Chinese women, the x-factor is skin tone, but for Chinese men, it is the brand, quality, and volume of possessions.

Even if rich Chinese hate Apple and their iPhones, they are permanently married to this product because owning a Chinese smartphone would be a monumental faux pas on the same level as American First Lady Melania Trump shopping for her new clothes at Walmart (WMT).

This is the same reason why every political who’s who in China drives an Audi A6, and every successful Chinese business executive drives a BMW.

Luxury brands are closely associated to the person’s social status in China and these unwritten rules have even more weight than the official rules in China partly because most Chinese over 40 are uneducated, plus China’s lack of public trust.

Apple’s tentacles reaching deep into Chinese society have in fact led to a situation where Apple-related jobs for Chinese citizens add up to over 5 million jobs which is over double the number of jobs Apple supports in America.

The result of Apple morphing into a pseudo-Chinese company is that pain for Apple means a loss of Chinese jobs on a large scale at a time when the Chinese economy is becoming more precarious by the day.

The Chinese economy is softening under a massive burden of crippling public and private debt that is putting the cap on growth.

As a result of the trade skirmish, China has temporarily halted its deleveraging effort that was intended to remedy the health of the economy and has reverted back to the China of old, low-quality infrastructure projects and heavily polluted coal production.

China’s rapid ascent to prosperity could also mean the Chinese consumer and economy could go through a reversion to the mean scenario with private and public companies loaded to their eyeballs with debt going bust and a looming economic stimulus in the cards if this plays out.

All this means is that Apple is too big to fail in China and CEO of Apple Tim Cook absolutely knows this.

Theoretically, Chinese consumers absolutely have access to local smartphone substitutes for $200 that would do the same job as a $1,000 iPhone.

I have tested out Huawei and Xiaomi premium smartphones costing $400, and they have more than enough firepower to be a reliable everyday smartphone and some.

The fact is that Chinese consumers intentionally choose not to substitute Apple products.

And I would go deeper than that by saying Steve Jobs is revered in China like a demigod and his passing turned him into a sort of tech martyr with a level of status that not even Alibaba (BABA) originator Jack Ma can touch.

Jack Ma performed miracles by copying eBay’s (EBAY) blueprint of e-commerce from a shabby Hangzhou flat ditching his former job as an English teacher then copying Amazon (AMZN) to juice up growth.

But Jack Ma never created the iPhone, iPod, tablet, or Apple app store from thin air. That he never did.

Making matters even more ironic is that most Chinese communist members actually use an Apple iPhone for the same reasons I mentioned earlier.

Not only that, the children of Chinese communist politicians take lavish vacations to Silicon Valley to take selfie’s in front of Apple’s spaceship headquarters in Cupertino and upload them onto social media.

They then proceed to visit the nearest Apple store right next door at the Apple Park visitor center which is essentially an Apple store on steroids to make bulk purchases of Apple tablets, watches, computers, iPhones for their extended circle of friends and distant relatives because they are “cheaper in America than in China” mainly due to the heavy import duties levied on Apple products in China.

As for tech equities, what this does is blunt short-term positive sentiment for tech stocks and particularly chip stocks that I have told readers to stay away from like the plague.

Apple’s supply chain frenemies don’t have the luxury of selling 80 million luxury phones at $1,000 per quarter and are often the recipient of indiscriminate sell-offs shellacking shares.

Even with the overhanging issue of rising tariffs, tech stocks should produce great earnings next year.

Look at Apple and the consensus EPS outlook for next quarter comes in at $4.73 and that is after EPS increasing 41% sequentially from the quarter before.

Apple will soon become a $300 billion of sales per year company with profitability expanding at a rapid clip.

They are a company that prints money then buys back their own stock profusely. Not many companies can do that.

These negative reports that have been coming fast and furious don’t help the momentum, but the share’s weakness solely means that better entry points are available for investors before Apple launches over $200 again.

There is a high chance that the administration is using Apple as a bargaining chip and nothing will come of it.

Think about it, after all this commotion about the trade war with China, revenue was up almost 20% last quarter in greater China, so what gives?

It means that things aren’t as dire as it seems. A lot of hot steam over nothing is a gift to long-term investors, but short-term traders will feel the pain of the temporarily elevated headline risk.