This morning, U.S. Treasury Secretary Steven Mnuchin mentioned that an effort was being made to get trade talks with China back on track. The Dow soared 160 points in a heartbeat.

Past murmurings by the Treasury Secretary demonstrate that his musings have zero credibility in the marketplace and the move vaporized in minutes. However, given the extreme moves made by the shares of trade war victims, I think it is time to review my “Trade Peace” portfolio and make some additions.

The shares have been so beaten up that I think you can start scaling in now with limited downside and a ton of potential upside.

It’s not a matter of if, but when Trump has to run up the white flag with his wildly unpopular trade wars. As they now stand the new tariffs are threatening to chop $10 off of S&P 500 earnings in 2018, from $168 down to $158, according to J.P. Morgan. Some two-thirds of all U.S. companies have been negatively impacted.

Tariffs have effectively wiped out the benefits of the corporate tax cuts for most companies enacted last December. Who has been the worst hit? Thousands of small manufacturers in Midwest red states that can’t function because they are missing crucial cheap parts they can only obtain from the Middle Kingdom.

At last count there are a staggering 37,000 applications for exemptions from tariffs filed with the U.S. Treasury and only a dozen people to process them. A mere 10% have been granted. It is a giant bureaucratic nightmare.

With the midterm elections now only 37 trading days away, the clock is ticking. If Trump doesn’t cut trade deals with all of our major counterparties around the world before then, the Republican Party stands to lose both the House of Representatives and the Senate on November 6. That will make Trump a “lame duck” president for two more years.

China Technology Stocks – Includes Alibaba (BABA), Baidu (BIDU), and Tencent (TCTZF). It’s not often that you get to buy a company with 61% sales growth, which has seen its shares plunge by 27% in three months, as is the case with (BABA). Just to get (BABA) back up to its June level it has to rise by 37%. This is a stock that will easily double or triple over the long term.

U.S. Semiconductor Stocks – With China buying 80% of its chips from the U.S., stocks such as Micron Technology (MU), Lam Research (LRCX), and KLA-Tencor (KLAC) have been taken out to the woodshed and beaten senseless. Micron is off a withering 41% since the trade war began in earnest in May.

Emerging Markets – China is the largest trading partner for most of the world, and a recession there sparks a global contagion effect. Reverse that, and you stimulate not only emerging markets, but the U.S. economy, too. Look at the charts for the iShares MSCI Emerging Markets ETF (EEM), the iShares China Large-Cap ETF (FXI), and the iShares MSCI Brazil ETF (EWZ) and you will salivate.

Oil – Boost the global economy and oil demand (USO) also. China is the world’s largest incremental buyer of new oil, and it will absorb all of the Iranian crude freed up by the U.S. abrogation of the treaty there.

Agricultural – No sector has been punished more than agriculture, where profit margins are small, lead times stretch into years, and mother nature plays her heavy hand. In this area you can include soybeans (SOYB), corn (CORN), and wheat (WEAT), as well as equipment makers Caterpillar (CAT) and Deere (DE).

Some 20 years of development efforts in China by American farmers have gone down the toilet, and much of this business is never coming back. Trust and reliability are gone for good. Storage silos across the country are full. Did I mention that red states are taking far and away the biggest hit? There are not a lot of soybeans grown in California, New York, or New Jersey.

Even if Trump digs in and refuses to admit defeat, as is his way, there is still a light at the end of the tunnel. Sometime in 2019, the World Trade Organization will declare virtually all of the new American tariffs illegal and hit the U.S. with its own countervailing duties. This is the Chinese strategy. Waiting for them to fold could be a long wait, a very long wait.

Global Market Comments

September 12, 2018 Fiat Lux

THE FUTURE OF AI ISSUE

Featured Trade: (THE NEW AI BOOK THAT INVESTORS ARE SCRAMBLING FOR), (GOOG), (FB), (AMZN), MSFT), (BABA), (BIDU), (TENCENT), (TSLA), (NVDA), (AMD), (MU), (LRCX)

If you have read any of our content in the first year of the Mad Hedge Technology Letter, the content is distinctly bullish technology stocks.

A fundamental driver propelling this cogent argument is the dominant Software-as-a-Service (SaaS) industry booming inside the confines of Silicon Valley.

If you want to boil down your tech investment thesis to one indispensable rule – only invest in tech companies that carve out prominent SaaS businesses.

If you stick with this nostrum, you will be delivered profits in spades.

We have recently taken in a swarm of new tech letter subscribers and understanding the panacea that is SaaS will entrench your portfolio in a glorious position to reap untold profits.

What is SaaS?

SaaS is a distribution method in which software is diffused to paid subscribers, usually on an annual, reoccurring payment plan, and the software is remotely stored on a centralized cloud platform awaiting use.

Unsurprisingly, SaaS remains the most lucrative segment of the cloud market.

In 2017, the tech industry did $60.2 billion in annual SaaS sales, that number is poised to explode to $117.1 billion in 2021.

The near doubling of sales underscores the robust nature of these tech firms setting up businesses of this ilk, and the positive effects dripping down to the bottom line.

Simply put, no SaaS business, no reason to invest.

SaaS isn’t the only cloud revenue companies can carve out. Tech firms also offer platform-as-a-service (PaaS) and infrastructure-as-a-service (IaaS).

However, SaaS is by far the prominent growth lever in the high-margin cloud industry.

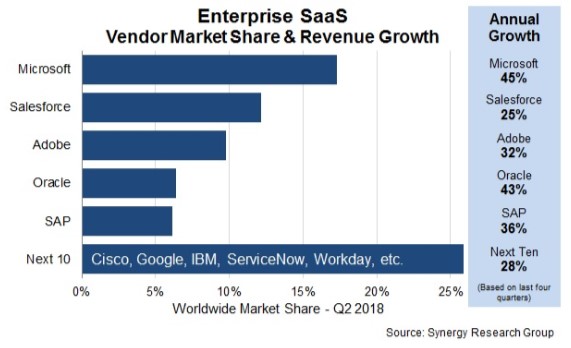

The indomitable presence inside the SaaS industry is Bill Gates’ creation Microsoft (MSFT).

Microsoft leads all companies with a 17% global share of the SaaS market.

The Redmond, Washington, outfit blew past stalwart Salesforce (CRM) nine quarters ago.

Microsoft’s sizzling SaaS business is an oversized contributor to its 45% revenue growth rate, which is head-and-shoulders above the industry average.

Salesforce (CRM), Adobe (ADBE), Oracle (ORCL) and SAP (SAP) fill out the top five largest global SaaS businesses, but it is really a tale of two stories.

Oracle and SAP, which are competing in the same market, are grappling with legacy database businesses and legacy tech, which are punished by investors.

John Dinsdale, a chief analyst at Synergy Research Group, mentioned two outliers of “Cisco (CSCO) and Google too who are making ever-bigger inroads into the SaaS market” leveraging Cisco’s multitude of software assets and Google’s G Suite.

The thing that makes SaaS the x-factor for tech companies is that inevitably every company from every walk of life will adopt this mode of software, giving legs to this distribution model.

Vendors are scrambling to put together some resemblance of a SaaS product together, and this trend is a vital contributor to an industry that is growing 32% YOY worldwide.

Kevin Cochrane, chief marketing officer of SAP Customer Experience lay bare his thoughts about this type of service describing it as the “Golden Age of SaaS.”

Companies are becoming digital first from end to end, explaining the sharp rise in IT professional salaries and rise in quality software products.

As we look around the corner to the IaaS part of the cloud industry, which is growing at around 30% YOY, there is one dominant player, and everybody knows its name.

Amazon (AMZN) is the No. 1 vendor with Microsoft, Alibaba (BABA), Google, and International Business Machines Corporation (IBM) trailing behind.

The top four IaaS players have carved out a total of 73% of the global market ravaging any resemblance of competition.

Amazon is the industry standard with the best record of customer success.

If Amazon branched off into the SaaS industry, it could unlock an additional $100 billion in annual revenue.

A shift into this direction could pad Amazon’s margin’s even more after successfully boosting North American e-commerce margins from 2.4% to 4.7%.

It’s not entirely inconceivable that Amazon could break the $2 trillion valuation in three to five years, as its revved up digital ad business registered growth of 129% YOY last quarter.

Microsoft seized the runner-up position in the IaaS market to Amazon by growing 98% YOY with sales eclipsing $3.1 billion in 2017.

Wherever you turn, whether toward the cloud business or gaming, investors can find Microsoft making sales.

Microsoft has been a favorite of the Mad Hedge Technology Letter and it’s hard pressed to find a better public tech company in operation now.

The SaaS industry is not a one-size-fits-all proposition.

Thus, there is abundant room for niche offerings that quench companies’ demand for specific services.

This is the reason why cloud companies have participated in a non-stop buying binge of smaller companies that fit their needs.

Microsoft purchased developer favorite GitHub for $7.5 billion earlier this year, and similar examples are scattered all over the tech ecosphere.

Artificial Intelligence (AI) will be the kicker that powers SaaS performance to new heights because incorporating this groundbreaking technology will enhance functionality and, in return, raise profits for all involved.

The scalability of SaaS products has allowed companies to offer software for affordable prices allowing the smallest of firms to adopt a digital-first strategy.

This software connects with other software seamlessly integrating an array of productive apps that help teams overperform and overdeliver.

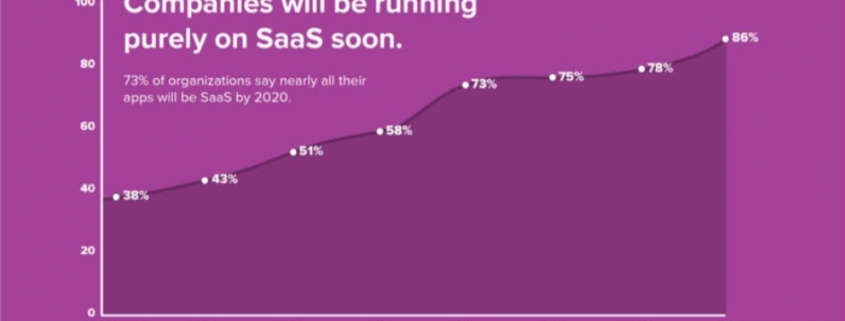

In the American workplace, 73% of companies will be exclusively using SaaS to function by 2020.

American companies are using 16 apps on average per day, a 33% jump in the number of apps they were using just two years ago.

The migration to mobile has swallowed up SaaS products as well with more mobile-specific software rolling out to mobile devices.

The meteoric rise of SaaS offerings has cut IT security budgets substantially as security has been delegated to the cloud instead of in expensive in-house security teams.

No longer do tech firms need to beef up guarding their own gates.

Protection is provided on a centralized cloud with a third-party company ensuring safety.

This development has helped a new industry rise – cloud security.

Whether people realize it or not, the SaaS industry is here to stay and will become more prevalent in every industry going forward.

This is incredibly bullish for companies that sell SaaS products as revenue will continue to rise.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/Saas-image-3-e1536717382380.jpg324580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-09-12 01:05:082018-09-12 02:12:03How to Play “Software as a Service”

Fintech is all the rage now, and it’s time for investors to grab a piece of the action.

The tech sectors’ stellar performance in 2018 is a little taste of things to come as every industry forcibly pushes toward software and artificial intelligence to enhance products and services.

Bull markets don’t die of old age and some of these tech stalwarts are truly defying gravity.

The fintech sector is no exception.

Square (SQ) led by tech visionary Jack Dorsey has been a favorite of the Mad Hedge Technology Letter practically from the newsletter’s inception.

But another company has caught my eye that most of you already know about – PayPal (PYPL).

PayPal, a digital payments company, has extraordinary core drivers and a splendid growth trajectory.

Its arsenal of services includes digital wallets, money transfers, P2P payments, and credit cards.

It also has Venmo.

Venmo, a digital payment app, is the strongest growth lever in PayPal’s umbrella of assets right now, and was the first meaningful digital payment app in America.

It was established by Andrew Kortina and Iqram Magdon-Ismail, who were roommates at the University of Pennsylvania, and the company was bought out by PayPal for $800 million in 2014, marking a new chapter in PayPal’s evolution.

Funny enough, Venmo’s original use was to buy mp3 formatted songs via email in 2009.

Venmo is wildly popular with tech savvy millennials. A brief survey conducted illustrates how fashionable Venmo is by recording higher user statistics than Apple Pay.

The app is commonly used for ordering pizza through Uber Eats or Grubhub (GRUB), or even shelling out for monthly rent.

If you want to stir up your imagination even more, Venmo has a prominent social feed where users can view other Venmo users’ purchases.

Financial models suggest Venmo could contribute $300 million to the PayPal top line in 2021. If Venmo executes perfectly, revenue could surpass the $1 billion mark in 2021, with much higher operating margins than PayPal’s core products.

Even though management declines to speak specifically about Venmo, the dialogue in the earnings call usually provides some color into what is going on underneath the hood.

Xoom, a digital remittance distributor app with offices in San Francisco and Guatemala City owned by PayPal, along with Venmo grew payment volume by 50% YOY, surging to $33 billion annually.

Of that $33 billion in volume, $19 billion was contributed by Venmo and Xoom chipped in with $14 billion.

More than 60,000 new merchants joined PayPal’s array of platforms, adding up to more than 19.5 million total merchants.

All in all, PayPal locked in $3.86 billion of sales last quarter, which was a 23% YOY jump in revenue, at a time where widespread acceptance of fintech platforms is brisk.

PayPal raised its end-of-year forecast and rewarded shareholders with authorization of a $10 billion buyback.

Upward margin expansion, expanding market share, multiple revenue stream, and untapped pricing power is the recipe to PayPal’s meteoric rise.

PayPal’s share price has climbed higher from a base of $73 at the beginning of the year to an all-time high of more than $90.

Offering more proof fintech is alive and kicking is Jack Dorsey’s Square’s dizzying rise of more than 200% YOY in its share price.

The company is exceeding all revenue growth expectations and is poised to ramp up subscription revenue.

As with the Venmo app, Square’s Cash app has unrealized potential and will be one of the outperforming profit drivers going forward.

Square hopes to be the one-stop-shop for all types of digital payment needs including consumer finance, equity purchases, possibly international transfers, and cryptocurrency.

All of this is happening amid a robust secular story that could have seen traditional banks swept into the dustbin of history.

Rewind a few years ago, perusing the data about the movement to digital payments must have frightened the living daylights out of the executives from major Wall Street mainstays.

Digital wallets assertive migration into mainstream money payment services could have detached traditional banks’ core businesses.

Slogging your way to a physical bank to put in a wire transfer was not appealing.

Archaic methods of business are painful to see, and traditional banks were still operating this way as of 2015.

Time is money and technology has crashed the traditional waiting time to almost zero.

The way these tech companies operate is simple.

They compete to hire a hoard of advanced computer developers or shortcut the process using the time-honored tradition of poaching the competition’s best talent.

Then snatch market share at all costs and grow like crazy.

Banks badly needed introducing some functions to their array of services such as linking with third-party payment APIs to facilitate online payments and enabling cross-platform digital payments.

Other functions such as establishing modern peer-to-peer payment systems or adopting QR code technology that are wildly popular in East Asia could enhance optionality as well.

These are several instruments they could have amalgamated into their arsenal of fintech technology that could have freshened up these dinosaur institutions.

Harmonizing banking tasks with mobile functionality was fast coming and would be the standard.

Anyone not on board would sink like the Titanic.

Ultimately, banking institutions needed to up their game and acquire one of these digital wallet processors or watch from the sidelines.

They chose the former when a consortium called Early Warning Services (EWS) jointly created by behemoth American banks, including JPMorgan Chase & Co. (JPM), Capital One (COF), Bank of America (BAC), and Wells Fargo (WFC) to “prevent fraud and reduce detection risk” made a game-changing decision.

(EWS) acquired digital payment app Zelle in 2016, and this was its aggressive response to Square Cash and PayPal’s Venmo.

Results have been nothing short of breathtaking.

Leveraging the embedded base of existing banking relationships, Zelle took off like a scalded chimp and never looked back.

In a blink of an eye, Zelle had already signed up more than 30 banks and over 100 financial institutions to its platform.

Banks couldn’t bear being left out of the fintech party.

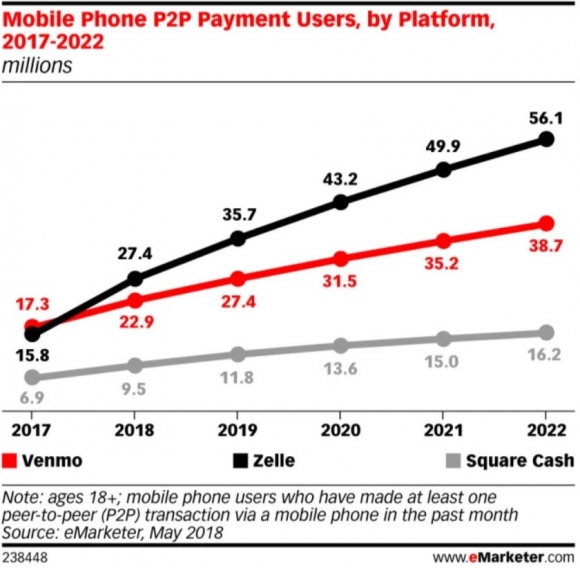

With hearty conviction, Zelle is signing up users at a pace of 100,000 per day, and the volume of payments in 2017 eclipsed $75 billion.

Zelle projects to expand more than 73% in 2018, integrating 27.4 million new accounts in the U.S., head and shoulders above Venmo’s 22.9 million and Square Cash due to add 9.5 million more users.

Make no bones about it, Zelle was in prime position to convert existing relationships into digital converts. The banks that do not have an interest in Zelle have an uphill climb to stay relevant.

The United States is rather late to this secular growth story. That being said, already 57% of Americans have used a mobile wallet at least once in their lives.

Innovative ideas bring supporters galore and even more adoptees.

That is why the strong pivot into technological enhanced ideas bear unlimited fruit.

Using a mobile platform to just open an app then send funds within a split second with minimal costs is appealing for the Netflix (NFLX) crazed generation that can hardly get off the couch.

Ironically, it’s those in the emerging parts of the world leading this fintech revolution by skipping the traditional banking experience completely and downloading digital wallet apps on their mobile devices.

It’s entirely realistic that some fresh-faced youth have never been present at a physical banking branch before in India or China.

Download an app and your fiscal life commences. Period.

The volume of funds passing through the arteries of Chinese digital wallet apps surpassed $15 trillion in 2017.

And by 2021, 79.3% of the Chinese population are projected to use digital wallets as their main source of splurging Chinese yuan.

America lags a country mile behind China, but the Chinese progress has offered American tech companies a crystal-clear blueprint to springboard digital payment initiatives.

Chinese state banks are already starting to become marginalized, and the Wall Street banks are not immune to the same fate.

Devoid of a digital strategy will be a death knell to certain banking institutions.

Compare the pace of adoption and some must question why American adoption is tardy to a fault.

Highlighting the lackadaisical pace of American fintech integration was Alibaba’s (BABA) smash-and-grab attempt at MoneyGram International Inc. (MGI), as it sought to gain a foothold into the American fintech market.

The attempt was rebuffed by the federal government.

The nascent state of the digital payment world in America must alarm Silicon Valley experts. And the run-up in Square and PayPal includes calculated bets that these two standouts will leapfrog into the future with guns blazing along with Zelle.

The parabolic nature of Square’s mystifying gap up means that a moderate pullback is warranted to put capital to work in this name.

Investors should wait for a timely entry point into PayPal as well.

These two stocks have overextended themselves.

As the fintech pie extrapolates, there will be multiple victors, and these victors are already taking shape in the form of Zelle, PayPal, and Square.

“In the not-too-distant future, commerce is just going to be commerce. It won't be online commerce or offline commerce. It's just going to be commerce. And that will happen because of the phone,” – said CEO of PayPal Dan Schulman.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/mobile-phone-p2p-payments-transaction-image-4-e1536176894297.jpg531580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-09-06 01:05:212018-09-05 20:00:17The Smart Plays in Fintech

Warren Buffett preaches searching among your “circle of competence” to find those gems of companies that will offer abundant value in the far future.

His time horizon has always been long – 10, 20, 30 years where a company has sufficient time to execute its business strategy.

The celebrated investor’s track record is unrivaled.

Another critical rule to his playbook of uncanny success is to invest in companies within your area of expertise to avoid erroneous investment decisions.

If an investor is uncertain if a company is within its “circle of competence,” then it is likely outside the circle and best to skip investing in the company for now.

The Oracle of Omaha has taken his investment playbook to the chicken tikka masala-loving country of India, dropping a few Benjamín’s on One97 Communications Ltd., the parent company of Paytm, an Indian fin-tech firm.

This disrupting digital payments company based in Noida, India, is the nation’s largest mobile-payments firm and quite an achievement in a country that loves paper cash.

It boasts a popular smartphone app used in daily lives, and mirrors digital payment businesses of the likes of China’s Alipay or Tencent’s WeChat payment platform.

When the Indian government laid down the heavy hand of fiscal regulation on the paper currency market with an eye toward the digital currency market, an outsized winner was Paytm.

The cost of printing paper money in India per year is more than $90 million by itself.

I am not saying that the Indian government is going into overdrive adopting bitcoin tomorrow, but its pivot toward fin-tech mobile payments and Buffett’s vote of approval show where all the deep lying tech value is marinating in the world.

It is not Silicon Valley that gets more expensive by the day.

Silicon Valley is largely saturated with venture capitalist firms cherry-picking the best firms before they go public and making many times their investment once they hit the New York public markets.

Well, we are still in the early stages of India’s rapidly developing tech scene. And 2018 has seen some blockbuster cash injections such as Walmart’s investment in e-commerce juggernaut Flipkart.

Buffett has championed investing into companies with a “margin of safety,” allowing him to buy stakes at levels he believes that are well below market value.

This allows him to sleep at night because even if the company tanks short-term, he knows that eventually it will pull it together.

India can now lay claim to more than 390 Internet users, and 300 million of those use Paytm.

When 77% of a country’s population is using an app, you know there is some staying power, as the first mover advantage in the tech world has a powerful and long-term network effect such as the AWS’s foray into the cloud business.

Paytm does have a crowded lineup of heavyweights breathing capital into its company in the form of investments from Masayoshi Son’s SoftBank Vision Fund and Jack Ma’s Alibaba (BABA).

China’s presence in the Indian tech scene is strong, but it has not doubled down there as it has in Southeast Asia, where it enjoys a healthier political connection that is largely void of border skirmishes.

India is the largest democracy in Asia and a strong ally of the United States. Although American tech companies won’t be welcomed with a pristine red carpet, they do have ample opportunity to invest in the burgeoning Indian tech scene.

Buffett’s stake amounts to a 3% to 4% stake in Paytm, and the valuation has spiked to more than $10 billion.

This comes on the heels of Buffett’s adding to his position in Apple (AAPL) that sees him now own 5%.

Apple’s services division is its new cash cow and is on track to eclipse $50 billion in annual revenue next year.

Apple’s services division surpassed $30 billion in the first three quarters of 2018. Its evolution comes at a timely period where smartphone growth has peaked while invaded by low-quality Chinese substitutes.

After sliding to annual low’s in April 2018 of $160, Apple has literally gone ballistic, powering past the $1 trillion valuation mark and is trading at all-time highs around $230.

Apple is another example of why this bull market is predominantly propped up by tech companies that continue to grow earnings at an insane pace.

Only a few companies have fallen into booby traps set forth by the regulatory hurdles first set by the Europeans and General Data Protection Regulation (GDPR).

Apple is losing its smartphone battle in India, but Indians can’t afford iPhones yet and even Netflix (NFLX) is seen as an expensive streaming service.

The average Indian does not possess the purchasing power that North America and Europe have.

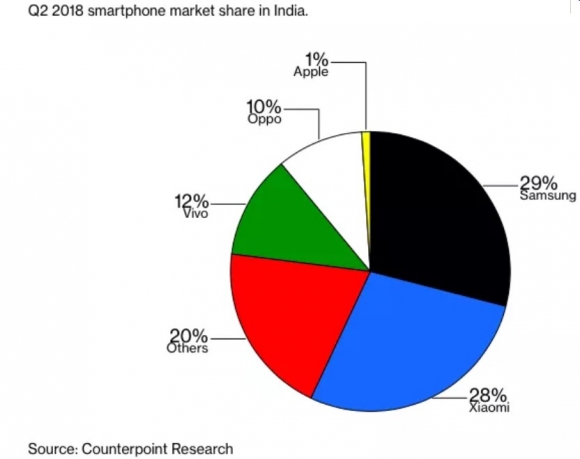

Apple has only extracted 1% of smartphone sales in India compared to leader Xiaomi, which leads the market with a 28% share. Further down-market Chinese phone maker Oppo lags with 10% and Vivo with 12%.

It doesn’t matter for Apple.

Apple continues to milk the North American and European markets to great effect padding profits with its high-quality services business.

China was the undeveloped market that launched Apple’s profits sky high. And American tech companies are ostensibly using this same strategy in India and hoping to cement the best strategy for revenue down the road.

Buffett’s investment is finally a green light for India if there ever was one, and every Silicon venture capitalist has to be licking their chops to squeeze value out of India.

The value is deep lying, but it will pay dividends within five to 10 years as India’s economy rises with its citizen’s discretionary income.

With every Tom, Dick, and Harry lusting after the India market, it will drive valuations firmly higher for the foreseeable future.

The fear of missing out (FOMO) will expedite the pivot toward India where many of the most conservative investors could ironically end up.

The tech relationship between America and India is demonstrably synergistic with Indian born CEOs heading Google (GOOGL) and Microsoft (MSFT) among other influential tech companies.

Berkshire’s (BRK/B) funds join the Chinese, Japanese, and Silicon Valley venture capitalist’s capital queuing at India’s front door awaiting to unlock value.

Buffett even opted out of investing in ride-sharing behemoth Uber, because apparently the “margin of safety” was not sufficient enough in the proposal.

Buffett was even quoted on a local Indian television station gushing about the country saying, “If you’ll tell me a wonderful company in India that might be available for sale, I’ll be there tomorrow.” That day has surfaced in the form of his investment in Paytm.

Apparently, Buffett’s expertise lies in India now and Indian-born Ajit Jain is one of four Berkshire executives running the company on a day-to-day basis.

This will pave the way for more tech investments in the swiftly evolving Indian tech scene, and Berkshire will ring in the profits of these Indian assets down the road.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/Smartphone-pie-chart-image-4-e1536092245855.jpg459580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-09-05 01:05:342018-09-04 20:21:48Warren Buffett’s Great Tech Find in India

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visist to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.