Mad Hedge Biotech and Healthcare Letter

September 22, 2022

Fiat Lux

Featured Trade:

(GOOD THINGS COME TO THOSE WHO WAIT)

(NTLA), (IONS), (TAK), (CRSP), (EDIT), (CRBU), (BEAM), (ALNY), (PFE), (REGN)

Mad Hedge Biotech and Healthcare Letter

September 22, 2022

Fiat Lux

Featured Trade:

(GOOD THINGS COME TO THOSE WHO WAIT)

(NTLA), (IONS), (TAK), (CRSP), (EDIT), (CRBU), (BEAM), (ALNY), (PFE), (REGN)

CRISPR technology has been receiving so much hype over the past years. However, the promise of this gene editing platform has yet to be realized.

Crispr gene-editing therapies can apply permanent modifications to our DNA by zeroing in on specific genes and then incapacitating them or reworking harmful segments of their genetic instructions.

While this could change in the coming years, investors have become impatient with the progress and lack of any major breakthrough in genomics. Some are losing confidence that this sector could experience explosive growth.

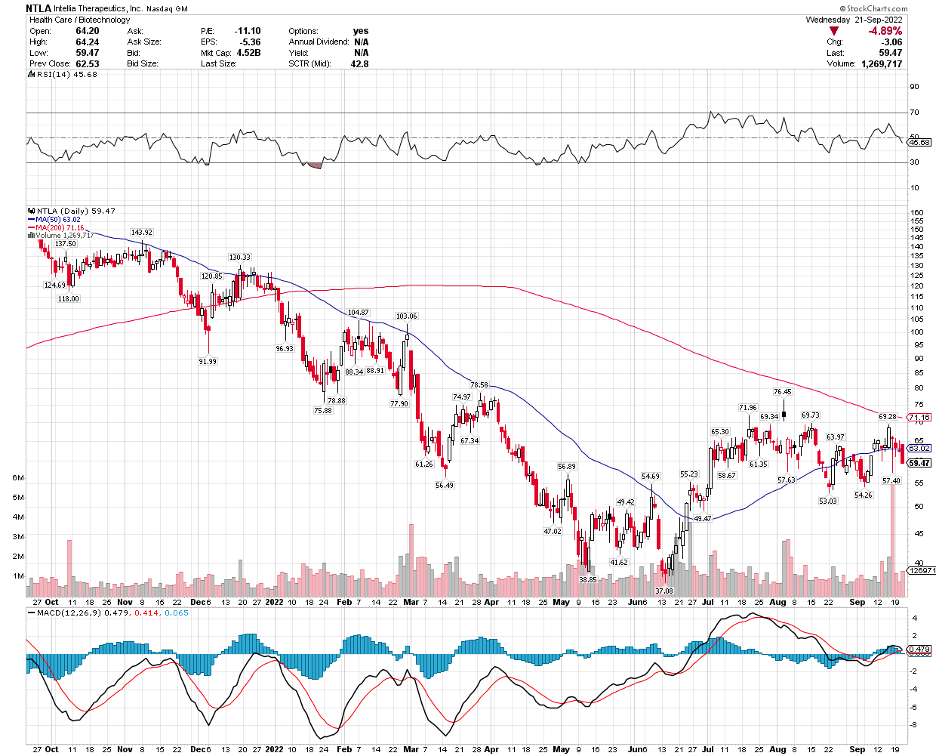

This is what happened with Intellia Therapeutics (NTLA).

Earlier this week, the company showed data that patients who received a one-time gene-editing infusion exhibited sustained improvement in a genetic condition that can result in fatal swelling when left untreated.

To be more specific, Intellia’s update means it could deliver a potentially permanent solution for hereditary angioedema. In this condition, a patient has a miswritten gene in their liver cells that produces a specific protein that triggers a dangerous swelling throughout the body.

Applying the treatment to 6 patients, Intellia’s one-time treatment lowered blood levels of the harmful proteins by more than 90% and decreased the swelling.

This is a more notable effect than the results from existing drugs like Takhzyro from Ionis Pharmaceuticals (IONS) and Takeda Pharmaceutical (TAK).

Despite the encouraging update, Wall Street still spurned the stock, and its price fell.

It looks like investors have lost patience with the slow progress of clinical studies in genetic treatments, pushing some to take advantage of the positive news from Intellia to abandon their positions.

Actually, it’s not only Intellia that suffered from this mistreatment by the market. Investors have also been dumping other stocks utilizing the Nobel-prize-winning technology, Crispr-Cas9, including CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), Caribou Biosciences (CRBU), and Beam Therapeutics (BEAM).

Intellia was hailed the top CRISPR stock in 2021 when the company and its co-collaborator, Regeneron (REGN), shared their promising interim results from a Phase 1 study assessing NTLA-2001, a treatment for a rare genetic disease called transthyretin (ATTR) amyloidosis.

This Crispr infusion candidate managed to knock out rogue genes in the liver cells of 12 patients, halting ATTR’s poisonous effects on their hearts or nerves. Based on clinical data, Intellia’s therapy caused an over 90% drop in the fatal protein triggered by the genetic condition.

If successful, this one-and-done ATTR treatment from Intellia would go head-to-head against other chronic drug therapies like Onpattro by Alnylam Pharmaceuticals (ALNY) or Pfizer’s (PFE) Vyndagel, which generates $2 billion in sales every year.

Many companies use Crispr technology to edit human genomes in an effort to treat and possibly even cure rare genetic diseases. Their treatments typically utilize either an ex vivo or an in vivo approach. With ex vivo therapies, the genes are altered outside the patient’s body.

However, Crispr’s use is not only limited to targeting genetic conditions. There are also gene-editing companies that are working on leveraging the technology to come up with treatments for various kinds of cancer.

In particular, Crispr technology has been a biotech favorite in the development of chimeric antigen receptor T-cell or CAR-T therapies. There are used to genetically engineer immune cells to target specific tumors.

Apart from these, some biotech companies are using Crispr technology to conduct screening. This is different from genetic testing, though.

When using Crispr for screening, the genes are modified in a manner that makes them nonfunctional or inoperative. Crispr screening allows biotechs to explore which genes take on particular functions, which can be critical in the development of drugs and treatments.

Intellia’s recent updates are clear indications that Crispr technology works. Since this will be applied to humans, we should expect the timeline and adaptation to take longer.

I have become more and more thrilled with developments in the gene editing space. Moreover, I believe it’s no longer about “if” but when it will happen.

Overall, the gene editing sector is not for fast-paced investors. This is for those willing to wait for a very long time, particularly for stocks like Intellia Therapeutics.

Mad Hedge Biotech and Healthcare Letter

May 24, 2022

Fiat Lux

Featured Trade:

(FROM A BORING BIOTECH TO A TRAILBLAZING PIONEER)

(VRTX), (ABBV), (MRNA), (CRSP), (EDIT), (BEAM), (NTLA)

When will the turmoil in the stock market come to an end? Unfortunately, nobody can offer a definitive answer.

At this point, there’s still no end in sight to high inflation, climbing interest rates, and the continuing war in Ukraine.

Needless to say, all these issues are affecting the stock market. However, not all stocks are getting negatively affected by the turmoil.

There are still relatively safe bets to buy, with some crushing the market these days.

One of them is Vertex (VRTX).

Vertex stock soared by over 30% year-to-date by mid-April.

While it has given up some of that gain in the past weeks, this biotechnology and healthcare stock is comfortably outperforming the rest of the market, with its shares still up by around 15%.

One reason for Vertex’s good performance is its undisputed monopoly in the cystic fibrosis (CF) market. In fact, its closest potential competitor is AbbVie (ABBV), which recently announced disappointing results for its Phase 2 trials for a CF combo.

This means Vertex’s dominance in the CF space is set to go on for quite some time.

Here’s a bit of background. Vertex has 4 CF treatments.

Among these, the latest treatment, Trikafta, generates the lion’s share of the profits. It raked in $1.7 billion in the first quarter of 2022 alone, with the total revenue for the entire CF pipeline recording $2 billion.

Considering its approved indications and potential approvals, Trikafta is anticipated to treat 90% of the entire CF patient population.

Looking at its current performance and how strong its hold is in the CF market, it appears that Vertex’s prediction that it can sustain its dominance in this segment until at least the late 2030s will be proven right.

Moreover, it’s evident that Trikafta has yet to reach its peak revenue. However, Vertex isn’t depending on this particular treatment alone.

Rather, the company is working on developing a worthy competitor to this top-selling treatment.

That is, Vertex is working on a CF candidate that may potentially be even more effective than Trikafta.

So far, this new drug candidate not only has the capacity to beat Trikafta in terms of efficacy but also offers a more convenient option.

Trikafta is a twice-a-day oral drug that comes in the form of 3 tablets. Meanwhile, this potential competitor is a once-a-day alternative.

If everything goes according to plan, the Phase 3 trial for this Trikafta challenger could start by the end of 2022 or early 2023.

This means that the closest potential rival for the company’s top-selling treatment is its own candidate.

Apart from this, Vertex is working with Moderna (MRNA) to come up with an mRNA therapy for CF patients.

The goal is to offer an alternative option to patients who are not eligible for the current CF therapies.

Although this continued dominance in the CF sector is already a good enough reason to buy Vertex shares, they may be an even better one.

To date, Vertex has at least 6 programs queued in mid to late-stage clinical studies, all of which are projected to become multi-billion dollar revenue streams.

Outside its CF segment, Vertex could have another big winner in the form of gene-editing treatment CTX001.

This is a treatment for sickle cell disease and transfusion-dependent beta-thalassemia that the company has been working on with CRISPR Therapeutics (CRSP).

While CTX001 is promising, it won’t be entering the gene therapy market without any competition. It has to battle the likes of Editas (EDIT), Beam Therapeutics (BEAM), and Intellia (NTLA).

Nonetheless, CTX001, if approved, is a game-changer because it is developed as a one-time cure for genetic blood disorders.

So far, trial results have been positive, and the collaborating duo is expected to file for regulatory approval by the end of 2022 and possibly launch the product by the first half of 2023.

This gene-editing therapy is a significant milestone for Vertex, with CTX001 expected to become another blockbuster, raking in roughly $1 billion in annual sales for the company even after giving CRISPR its share of the profits.

Recently, Vertex added another $900 million to its collaboration with CRISPR to boost its share from 50% to 60%, indicating that it values CTX001 at roughly $10 billion.

Other critical treatments outside the CF space are VX548, an opioid alternative targeting acute pain, and VX800, a stem cell-derived therapy developed to treat Type 1 diabetes.

Vertex has been accused as a company scared of getting out of its comfort zone for quite some time.

With these new ventures, Vertex has become something of a pioneer—a strategy that is projected to open long-term and lucrative revenue streams for the company.

Overall, all these efforts paint an obvious picture. That is, Vertex is a well-balanced company with a main business that capably and reliably generates billions and is complemented by an exciting pipeline that holds the potential to replicate the success of its already established portfolio.

Mad Hedge Biotech and Healthcare Letter

February 15, 2022

Fiat Lux

Featured Trade:

(AN EMERGING LEADER IN THE HEALTHCARE REVOLUTION)

(CRSP), (VRTX), (EDIT), (NTLA), (PFE), (NVS), (GILD), (RHHBY), (BMRN), (QURE), (SGMO), (CLLS), (ALLO), (BEAM)

Mankind has always imagined a future filled to the brim with technological advancements serving as the panacea to all our ills.

One of the prevailing ideas focuses on the developments found in the healthcare sector.

Movies, television shows, graphic novels, and books have all pictured a world with such revolutionary technologies capable of not only diagnosing but also curing any and all types of diseases.

Since the introduction of these ideas, many have believed that these would remain in the fictional universe. However, these “ideas” have slowly transformed into reality.

One of the biggest indicators that we’re heading in that direction is the 2020 Nobel Prize in Chemistry by Jennifer Doudna and Emmanuelle Charpentier. The two were recognized for their pioneering work in CRISPR-Cas9.

Basically, Crispr-Cas9 functions like molecular scissors.

What makes this technology incredible is that Crispr-Cas9 can classify a single address out of 3 billion letters within the genome by using only a particular sequence. With this, we can repair thousands of genetic conditions and even offer more potent ways to battle cancer.

This Nobel Prize led to commercializing the 2012 discovery, Crispr-Cas9, at breakneck speed, with gene-editing companies like CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), and Intellia Therapeutics (NTLA) gaining a considerable boost in their values.

Surprisingly, the trajectory of these gene-editing stocks took a tragic turn in 2021.

In fact, the once-upon-a-time-market-darling CRISPR Therapeutics saw its market capitalization brutally shaved off from $8.7 billion to $4.55 billion in the past months.

No matter how we look at it, there’s genuinely no way to sugarcoat the reality: the market has been second-guessing CRISPR Therapeutics’ ability to truly deliver on its promise.

That is, investors have started to wonder whether the company’s early stage success would amount to anything commercially.

CRISPR Therapeutics is currently working on a treatment that would implant tumor-targeting immune cells on cancer patients. The company is also prioritizing therapies that could edit cells to treat diabetes.

So far, it has made significant progress in developing treatments for a genetic disorder called sickle cell.

In the US alone, at least 100,000 people suffer from sickle cell disease, with 4,000 more born every year. Conservatively, we can estimate at least 3,000 patients availing of this one-time treatment at over $1.6 million a pop.

To date, CRISPR Therapeutics has five candidates under clinical trials for diseases like B-thalassemia, sickle cell disease, and other regenerative conditions.

It has four more queued, which target diabetes, cystic fibrosis, and Duchenne muscular dystrophy.

Compared to its rivals in the space, it’s clear that CRISPR Therapeutics is ahead when it comes to product development and trials.

Two of its candidates, transfusion-dependent beta thalassemia treatment CTX001 and sickle cell disease therapy CTX110, have already been submitted for clinical tests for safety and efficacy.

Recently, Vertex (VRTX) boosted its 2015 agreement with CRISPR Therapeutics by 10%, with the deal reaching $900 million upfront to push for quicker results in developing CTX001.

This is a crucial move for Vertex, but more so for CRISPR Therapeutics as CTX001 holds a highly lucrative addressable market.

The additional funding significantly widened the gap between the Vertex-CRISPR team and bluebird bio (BLUE) in the race to launch a new gene-editing therapy targeting sickle cell disease and beta thalassemia.

To sustain its growth, CRISPR Therapeutics’ strategy is to develop drugs that only require mid-level complexity but can rake in generous financial rewards.

This is a similar tactic used by bigger and more established biotechnology companies like Pfizer (PFE), Novartis (NVS), and Gilead Sciences (GILD).

Evidently, this strategy is a great way to ensure cash flow.

Aside from its earnings from the commercialization of these products, CRISPR Therapeutics can also attract larger companies to buy the intellectual property of their breakthrough treatments.

After all, startups generally get 100% premiums in contracts with Big Pharma.

Good examples of this are Novartis that bought AveXis and Roche’s (RHHBY) purchase of Spark Therapeutics.

The Roche-Spark agreement led to the first ever FDA-approved treatment since gene therapy trials started in the 1990s. It was for the genetic blindness therapy Luxturna, which received the green light in 2017.

The second approved treatment was a muscle-wasting disease therapy Zolgensma, which was the fruit of the Novartis-Avexis acquisition.

Both conditions are rare, but the financial rewards are impressive.

At $2 million for each treatment, Zolgensma sales reached $1.2 billion annually. At the rate the therapy is selling, Novartis estimates that Zolgensma will surpass the $2 billion mark in 2021.

Novartis and Roche aren’t the only ones partnering with smaller gene editing companies.

Pfizer has been working with biotechnology companies BioMarin Pharmaceutics (BMRN) and UniQure (QURE) to develop a treatment for blood-clotting disorder hemophilia.

The COVID-19 frontrunner is also collaborating with Sarepta Therapeutics (SRPT) to come up with a treatment for Duchenne muscular dystrophy.

Gene editing has also served as the foundation for several biotechnology companies out there today like Sangamo Therapeutics (SGMO), Cellectis (CLLS), and Allogene Therapeutics (ALLO).

The market size for gene editing treatments is estimated to be worth $11.2 billion by 2025, with the number rising between $15.79 billion to $18.1 billion by 2027.

This puts the compounded annual growth rate of this sector to be at least roughly 17%.

While this is already groundbreaking with only a handful of companies knowing how to utilize the technology, the gene-editing world has come up with a more advanced technique than Crispr-Cas9.

The technology is founded on the “base editing” or “prime editing” technique, which is the simplest type of gene editing that alters only one DNA letter.

So far, one company holds exclusive rights to this technology: Beam Therapeutics (BEAM).

When the technology became public, Beam stock has increased sixfold since its IPO in February 2020.

This latest development can resolve thousands of genetic diseases. However, it still requires further trials since “base editing” can also trigger damaging responses from the body.

Overall, I think CRISPR Therapeutics is the most promising among these high-risk stocks.

The data from two of its candidates, CTX001 and CTX110, are promising. The added funding from Vertex boosts the confidence of investors that a regulatory approval is well on its way.

The company is also sitting on a massive cash pile and investing aggressively across different rare disease programs.

While the company has yet to be considered a major force in the biotechnology world, the potential multiple successes of its products could generate a company worth hundreds of billions.

This potential alone offers an investing opportunity with a substantial asymmetric advantage for its current share price.

However, bear in mind that the stock is not for conservative investors considering risks.

More importantly, its pipeline requires patience. Hence, CRISPR Therapeutics should be played as a long-term investment.

Mad Hedge Biotech & Healthcare Letter

August 24, 2021

Fiat Lux

FEATURED TRADE:

A GENE EDITING PURE PLAY UP FOR GRABS

(MRNA), (EDIT), (CRSP), (NTLA), (VRTX), (REGN), (BMY),

(BLUE), (NVO), (GRTS), (INBX), (BEAM), (VERV), (SGMO)

Moderna (MRNA) is faced with a dilemma. And it’s a pretty good problem to face at this point.

The biotechnology company has a flourishing cash stockpile courtesy of the increasing demand for its COVID-19 vaccine, and it needs to find something to do with its overflowing cash.

As of the end of the second quarter, the company has already reported a cash position of over $12 billion—a figure that offers Moderna the flexibility to go on a bit of a shopping spree.

So far, Moderna has set its sights on expanding its internal R&D programs on top of the $1 billion share repurchase program approved by its board of directors.

However, the most exciting news is the company’s plans to potentially make acquisitions soon.

This is where Editas Medicine (EDIT) enters the picture.

Moderna has not been shy in declaring that it wants to add gene editing therapies to its growing pipeline along with nucleic acid technologies and mRNA.

While Moderna did not specifically mention Editas in its plans, the smaller biotechnology company looks to be the most promising candidate for acquisition, especially if the COVID-19 vaccine leader plans to jump right into the action in the gene editing space.

After all, there are only three companies in this segment with therapies under clinical testing: CRISPR Therapeutics (CRSP), Intellia Therapeutics (NTLA), and Editas.

CRISPR Therapeutics is practically joined at the hip with Vertex Pharmaceuticals (VRTX). Meanwhile, Intellia has a strong ongoing partnership with Regeneron (REGN).

That leaves Editas, which currently has no partner for its lead program, making it a prime buyout candidate for Moderna.

Editas is also the cheapest by far among all three clinical-stage biotech with $4.12 billion in market capitalization.

In comparison, CRISPR Therapeutics has a market cap of $8.93 billion, while Intellia has a market cap of $10.97 billion.

Moderna could find Editas’ lower market capitalization as an add-on, as it would allow the bigger biotech to not spend all its cash on the acquisition.

Moreover, Editas has another advantage.

While both CRISPR Therapeutics and Intellia only focus on CRISPR-Cas9, which is a way to locate and bind targeted genes, Editas has developed another option platform to do that.

Its alternative option, called Cas12, could boost the company’s capacity to develop gene editing treatments.

Simply put, its rivals only have one weapon in their arsenal, while Editas has come up with a dual-option CRISPR platform to double its chances of succeeding in gene therapy development.

If, for instance, Moderna does not acquire Editas, there are still a lot of options available for the bigger company.

One possibility is with Juno Therapeutics, which is part of Bristol-Myers Squibb (BMY), as the company is already collaborating with Editas on the development of genetically modified T-cells to come up with a powerful cancer therapy.

Meanwhile, if Editas’ pipeline and portfolio do not quite cut it with Moderna, another potential buyout candidate for this biotechnology giant is bluebird bio (BLUE).

While it’s not as advanced as CRISPR Therapeutics, Intellia, and Editas, bluebird bio has ongoing work with the likes of Bristol-Myers Squibb, Regeneron, Novo Nordisk (NVO), Gritstone Oncology (GRTS), and Inhibrx (INBX).

Other candidates that Moderna could take into consideration include Beam Therapeutics (BEAM), Verve Therapeutics (VERV), and Sangamo Therapeutics (SGMO).

Regardless of Moderna’s future decisions, its announcements that it plans to expand on the gene editing space could potentially spur other huge biopharmaceutical companies to explore their own business development agreements with up-and-coming biotechnology firms.

In fact, even if Moderna ends up not calling, there’s a big possibility that Editas could easily find others who will be interested in acquiring this pure play gene editing frontrunner.

Mad Hedge Biotech & Healthcare Letter

April 27, 2021

Fiat Lux

FEATURED TRADE:

(THE FUTURE OF MEDICINE)

(CRSP), (VRTX), (EDIT), (NTLA), (PFE), (NVS), (GILD), (RHHBY),

(BMRN), (QURE), (SGMO), (CLLS), (ALLO), (BEAM)

Winning the Nobel Prize in 2020 provided biotechnology companies more traction on Wall Street.

The victory led to commercializing the 2012 discovery, Crispr-Cas9, at breakneck speed, with gene editing companies like CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), and Intellia Therapeutics (NTLA) gaining considerable boost in their values.

Since then, the total market value for the products of these three has more than doubled in recent months to reach $23 billion.

Basically, Crispr-Cas9 functions like molecular scissors.

What makes this technology incredible is that Crispr-Cas9 can classify a single address out of 3 billion letters within the genome by using only a particular sequence. With this, we can repair thousands of genetic conditions and even offer more potent ways to battle cancer.

The market favorite among the gene editing companies so far is CRISPR Therapeutics, with $8.72 billion in market capitalization.

In comparison, Editas has $2.76 billion while Intellia Therapeutics has $4.15 billion.

CRISPR Therapeutics is currently working on a treatment that would implant tumor-targeting immune cells in cancer patients. The company is also prioritizing therapies that could edit cells to treat diabetes.

So far, it has made significant progress in developing treatments for a genetic disorder called sickle cell.

In the US alone, at least 100,000 people suffer from sickle cell disease, with 4,000 more born every year. Conservatively, we can estimate at least 3,000 patients availing of this one-time treatment at over $1.6 million a pop.

To date, CRISPR Therapeutics has five candidates under clinical trials for diseases like B-thalassemia, sickle cell disease, and other regenerative conditions.

It has four more queued, which target diabetes, cystic fibrosis, and Duchenne muscular dystrophy.

Compared to its rivals in the space, it’s clear that CRISPR Therapeutics is ahead when it comes to product development and trials.

Two of its candidates, transfusion-dependent beta thalassemia treatment CTX001 and sickle cell disease therapy CTX110, have already been submitted for clinical tests for safety and efficacy.

Recently, Vertex (VRTX) boosted its 2015 agreement with CRISPR Therapeutics by 10%, with the deal reaching $900 million upfront to push for quicker results in developing CTX001.

This is a crucial move for Vertex, but more so for CRISPR Therapeutics as CTX001 holds a highly lucrative addressable market.

The additional funding significantly widened the gap between the Vertex-CRISPR team and bluebird bio (BLUE) in the race to launch a new gene editing therapy targeting sickle cell disease and beta thalassemia.

To sustain its growth, CRISPR Therapeutics’ strategy is to develop drugs that only require mid-level complexity but can rake in generous financial rewards.

This is a similar tactic used by bigger and more established biotechnology companies like Pfizer (PFE), Novartis (NVS), and Gilead Sciences (GILD).

Evidently, this strategy is a great way to ensure cash flow.

Aside from its earning from the commercialization of these products, CRISPR Therapeutics can also attract larger companies to buy the intellectual property of their breakthrough treatments.

After all, startups generally get 100% premiums in contracts with Big Pharma.

Good examples of this are Novartis that bought AveXis and Roche’s (RHHBY) purchase of Spark Therapeutics.

The Roche-Spark agreement led to the first-ever FDA-approved treatment since gene therapy trials started in the 1990s. It was for the genetic blindness therapy Luxturna, which received the green light in 2017.

The second approved treatment was a muscle-wasting disease therapy Zolgensma, which was the fruit of the Novartis-Avexis acquisition.

Both conditions are rare, but the financial rewards are impressive.

At $2 million for each treatment, Zolgensma sales reached $1.2 billion annually. At the rate the therapy is selling, Novartis estimates that Zolgensma will surpass the $2 billion mark in 2021.

Novartis and Roche aren’t the only ones partnering with smaller gene editing companies.

Pfizer has been working with biotechnology companies BioMarin Pharmaceutics (BMRN) and UniQure (QURE) to develop a treatment for blood-clotting disorder hemophilia.

The COVID-19 frontrunner is also collaborating with Sarepta Therapeutics (SRPT) to come up with a treatment for Duchenne muscular dystrophy.

Gene editing has also served as the foundation for several biotechnology companies out there today like Sangamo Therapeutics (SGMO), Cellectis (CLLS), and Allogene Therapeutics (ALLO).

The market size for gene editing treatments is estimated to be worth $11.2 billion by 2025, with the number rising between $15.79 billion to $18.1 billion by 2027.

This puts the compounded annual growth rate of this sector to be at least roughly 17%.

While this is already groundbreaking with only a handful of companies knowing how to utilize the technology, the gene editing world has come up with a more advanced technique than Crispr-Cas9.

The technology is founded on the “base editing” or “prime editing” technique, which is the simplest type of gene editing that alters only one DNA letter.

So far, one company holds exclusive rights to this technology: Beam Therapeutics (BEAM).

When the technology became public, Beam stock has increased sixfold since its IPO in February 2020.

This latest development can resolve thousands of genetic diseases. However, it still requires further trials since “base editing” can also trigger damaging responses from the body.

Overall, I think CRISPR Therapeutics is the safest among these high-risk stocks.

The data from two of its candidates, CTX001 and CTX110, are incredibly promising. Plus, the added funding from Vertex boosts the confidence of investors that regulatory approval is well on its way.

The company is also capitalizing on the surging price of its stock and investing aggressively across different rare disease programs.

While the company has yet to be considered a major force in the biotechnology world, the potential multiple successes of its products could generate a company worth hundreds of billions.

This potential alone offers an investing opportunity with a substantial asymmetric advantage for its current share price.

However, bear in mind that the stock is still a risk and should be played as a long-term investment. Hence, you should buy on dips.