Mad Hedge Biotech and Healthcare Letter

August 1, 2024

Fiat Lux

Featured Trade:

(THE PLAYBOOK FOR A BIOTECH TRIPLE CROWN)

(ABBV), (TEVA), (PFE), (AMGN), (AZN), (BGNE), (LLY), (CERE)

Mad Hedge Biotech and Healthcare Letter

August 1, 2024

Fiat Lux

Featured Trade:

(THE PLAYBOOK FOR A BIOTECH TRIPLE CROWN)

(ABBV), (TEVA), (PFE), (AMGN), (AZN), (BGNE), (LLY), (CERE)

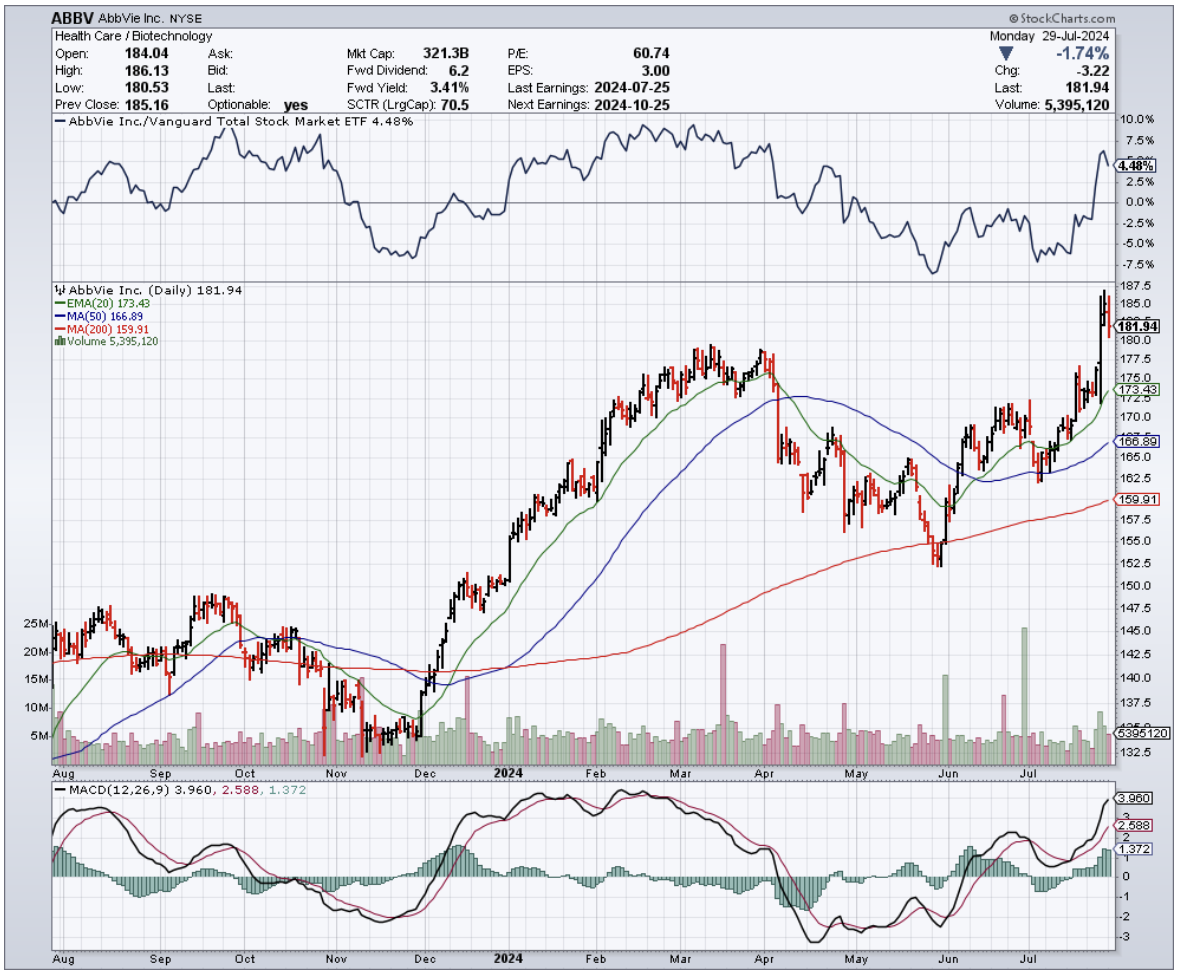

AbbVie (ABBV): A biotech stock that's been on my radar longer than most. If I could travel back to my UCLA biochem days, I'd tell young John to ditch the petri dishes and buy shares in this pharma giant. Why?

Because AbbVie isn't just another pharma play – it's a masterclass in diversification, innovation, and market-beating performance.

This is the stock that could turn a bright-eyed student into a savvy investor faster than you can say "immunology franchise."

In fact, if you've been paying attention to the market, you might have noticed that AbbVie's stock has been outperforming the broader U.S. market since mid-April, and for good reason.

This is a company that's been running at full throttle, posting some seriously impressive numbers in Q2 2024. We're talking $14.46 billion in revenue, a whopping 17.5% increase from the previous quarter and beating consensus estimates by a cool $430 million.

Earnings per share may have fallen just short of analysts' expectations, but they still climbed by a respectable 34 cents to $2.65.

But here's the thing: AbbVie's success isn't just a flash in the pan. This is a company with a diversified portfolio that's driving growth across multiple fronts.

I'm talking about their immunology, oncology, and neuroscience franchises, which together account for a staggering 75% of the company's total revenue.

Let's start with immunology. Now, I know what you're thinking - isn't that just Humira, AbbVie's blockbuster drug for Crohn's disease and ulcerative colitis? Well, yes and no.

While Humira has been facing some generic competition from the likes of Teva Pharmaceutical (TEVA), Pfizer (PFE), and Amgen (AMGN), resulting in a 30% year-over-year decline in global sales, AbbVie's got a couple of other tricks up its sleeve.

Enter Skyrizi and Rinvoq, two immunology drugs that are picking up the slack in a big way. Sales of these bad boys climbed 45% and 56%, respectively, in Q2 2024.

Skyrizi, in particular, has been an absolute beast, raking in $2.73 billion and growing 44.8% year-over-year. And with the FDA giving it the green light for moderate-to-severe ulcerative colitis in June 2024, the sky's the limit for this game-changer.

But AbbVie's not content to rest on its laurels. They're pushing the envelope with Rinvoq, a JAK inhibitor that's been approved for a wide range of indications and is showing some serious promise.

In Q2 2024, Rinvoq brought in $1.43 billion, a 30.8% quarter-over-quarter increase, thanks to strong demand in the U.S., excellent clinical trial results, and FDA approval for treating children with psoriatic arthritis and juvenile idiopathic arthritis.

And let's not forget about giant cell arteritis, a condition that AbbVie's been targeting with Rinvoq.

Recent trials have shown some impressive results, with 46% of adult patients taking Rinvoq 15 mg experiencing sustained remission, compared to just 29% of those on placebo.

No wonder AbbVie's been submitting applications left and right to get this drug approved for even more indications.

But it's not just immunology where AbbVie's making waves. Their oncology portfolio, bolstered by the acquisition of ImmunoGen in mid-February 2024, is also delivering the goods.

Sure, demand for Imbruvica may be declining due to newer BTK inhibitors from AstraZeneca (AZN), BeiGene (BGNE), and Eli Lilly (LLY), but Elahere, an antibody-drug conjugate for ovarian cancer, is quickly becoming a rising star.

In Q2 2024, Elahere sales jumped 65.4% quarter-over-quarter to $128 million, driven by increased marketing, growing awareness among physicians, and promising data from clinical trials.

Finally, let's not overlook AbbVie's neuroscience franchise, which generated a cool $2.16 billion in Q2 2024, a 14.7% year-over-year increase.

Headlining this portfolio are Qulipta and Ubrelvy for migraine treatment, and Vraylar for a range of psychiatric conditions.

Qulipta, specifically, has been a standout, with sales surging 56.3% year-over-year to $150 million, thanks to its convenient oral administration and long-term efficacy data.

Looking ahead, AbbVie's got even more irons in the fire. Their $8.7 billion acquisition of Cerevel Therapeutics (CERE) is set to close soon, bringing promising neuroscience candidates like emraclidine for schizophrenia and davapidon for Parkinson's into the fold.

With all these positive developments, it's no wonder AbbVie's feeling confident enough to raise its full-year adjusted EPS guidance to $10.71-$10.91, up from the previous range of $10.61-$10.81. Talk about a biochemistry experiment gone right!

So, there you have it. AbbVie: a healthcare powerhouse that's firing on all cylinders and poised for even greater success in the years to come. If only I could've shown this to my younger self back in those UCLA labs – he might've traded his test tubes for trading terminals a lot sooner.

Now, if you're ready to take a ride on this rocket ship, I suggest you buckle up and hang on tight. Because let me tell you, dissecting AbbVie's financial DNA has been more thrilling than any fracking adventure or hedge fund rodeo I've ever been on.

And if there's one thing I've learned in my years hopscotching from biochem labs to Wall Street, it's that the view from the top of a well-diversified, innovative pharma giant is always worth the climb. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

July 16, 2024

Fiat Lux

Featured Trade:

(SMALL GIANTS RISING)

(GMAB), (OPHLY), (VRTX), (INCY), (BIIB), (AHKSY), (ALNY), (ARGX), (BGNE), (MRNA), (NBIX), (BNTX), (IPSEY), (CTLT), (NVO), (LLY), (JNJ), (GILD), (ABBV), (MRK), (SNY), (BMY), (GSK)

Remember when David took down Goliath? Well, history's repeating itself in the biotech arena, and this time, David's got deep pockets and a Ph.D.

Since April, I've been watching a trend on the so-called "next-generation" players in biotech and healthcare world. It reminds me of the massive changes I witnessed in Asian markets back in the '70s.

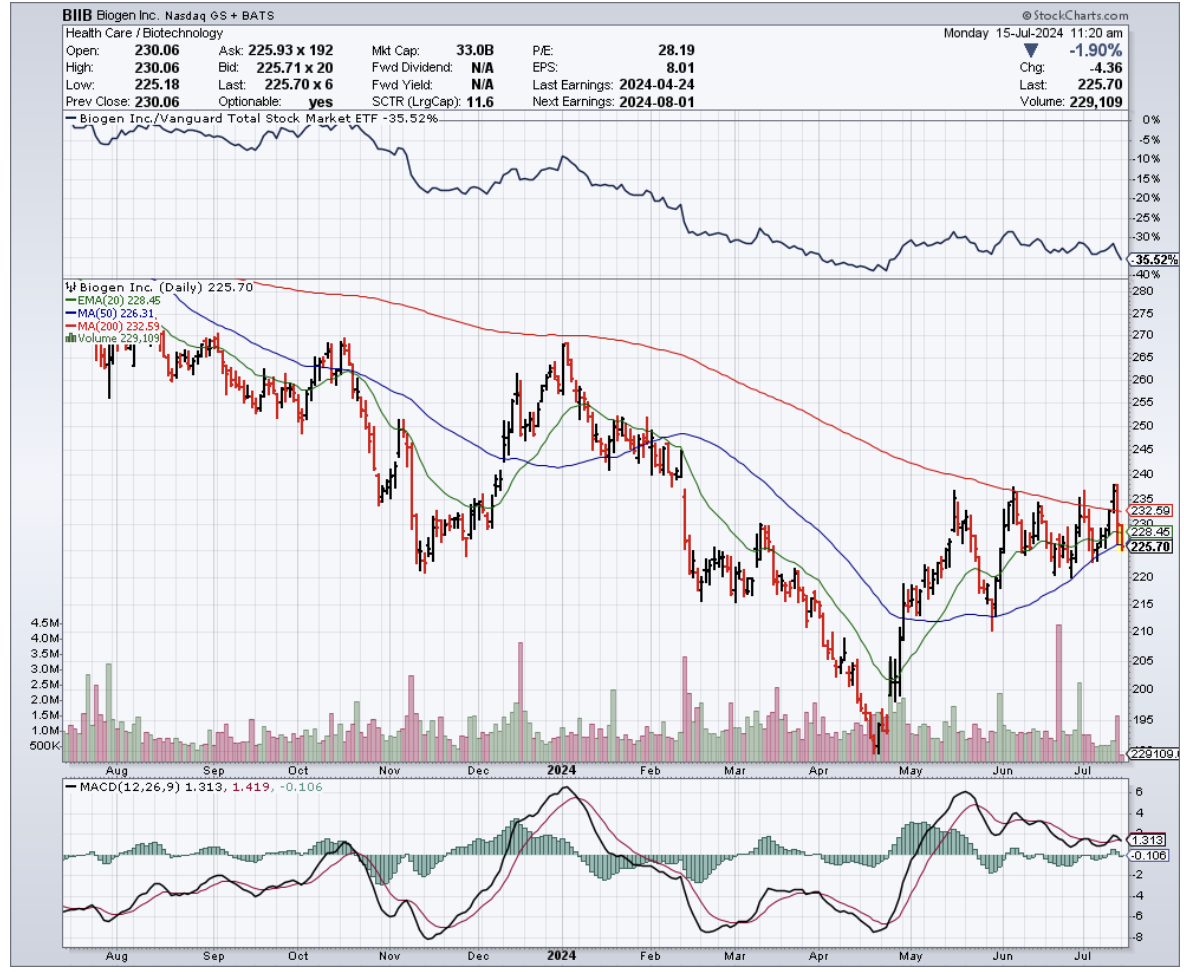

Over the past months, companies like Genmab (GMAB), Ono Pharmaceutical (OPHLY), Vertex (VRTX), Incyte (INCY), Biogen (BIIB), and Asahi Kasei (AHKSY) have been making waves that would impress even the most seasoned surfer. And these next-gen dealmakers aren't just dipping their toes in the M&A pool - they're doing cannonballs.

With cash reserves that would make Scrooge McDuck blush, these companies are overturning industry norms, already joining the prestigious $100 billion market cap club. At this celebration, the champagne flows freely.

So, what’s the play here?

With IPOs cooling down like day-old coffee, companies eyeing public debuts are now ripe targets for acquisition, more tempting than a juicy peach.

This fresh class of biotechs, unphased by the FTC's scrutiny that acts like kryptonite to pharma giants, are acting more like rocket fuel for these agile consolidators.

They slide through regulatory gaps faster than a greased pig at a county fair, grabbing six out of ten biopharma M&A deals in the second quarter alone. They’re not just taking a slice of the pie—they’re rewriting the recipe.

And if we're talking about firepower? These newcomers boast an average of $3.8 billion in pro forma adjusted cash, which isn't just walking-around money — that's "buy a small country" money.

But don't think for a second that this cash is just sitting pretty in their coffers. These upstarts are putting their money where their mouth is.

Take Incyte, for instance. They flexed their financial muscle with a $2 billion buyback in May 2024, sending a clear message to the market: "We're here to play, and we're playing to win."

And that's just the tip of the iceberg. The industry as a whole is lounging on a cool $1.5 trillion. That's enough liquidity to stretch the imagination — perhaps even to purchase a small planet. Mars, anyone? Elon might give us a discount.

But this financial might isn't just about buying power – it's about survival. As I said before, Big Pharma is teetering on a patent cliff that threatens to erode their revenue streams. To stay competitive, they're scrambling to replenish their pipelines, acquiring promising assets and gobbling up innovative technologies with the voracity of Pac-Man on steroids. And it's not just the usual suspects making moves.

This sense of urgency has created a fertile ground for an emerging cohort of aggressive dealmakers. Companies like Alnylam (ALNY), argenx (ARGX), BeiGene (BGNE), Moderna (MRNA), Neurocrine Biosciences (NBIX), BioNTech (BNTX), and Ipsen (IPSEY) are biting off more than the market expected them to chew, and they're coming to the table hungry.

And these companies aren't just nibbling around the edges. They're making bold moves, acquiring cutting-edge biotech firms with promising pipelines. We're talking oncology, epilepsy, kidney diseases, cardiovascular plays – it's like someone turned a medical textbook into a shopping catalog.

In fact, even the big boys are flexing their muscles.

Novo Holdings (NVO) dropped a jaw-dropping $16.5 billion on Catalent (CTLT). That's not even for a drug - it's for manufacturing. Talk about betting on the picks and shovels in this biotech gold rush.

Eli Lilly (LLY) just plunked down $3.2 billion on Morphic Therapeutic (MORF), betting big on inflammation, immunity, and oncology.

Johnson & Johnson's (JNJ) been on a shopping spree, too, snagging Numab's Yellow Jersey for $1.25 billion and Proteologix for $850 million. Both plays in inflammation and immunity - clearly, they've found their sweet spot.

Biogen's not twiddling its thumbs either, striking a deal with HI-Bio worth up to $1.8 billion.

Not to be outdone, Gilead (GILD) shook hands with CymaBay Therapeutics to the tune of $4.3 billion. Even AbbVie (ABBV), playing it cooler, still dropped a cool $250 million on Celsius.

Meanwhile, Merck's (MRK) set its sights on EyeBio for up to $3 billion, focusing on ophthalmology.

Sanofi (SNY), Bristol Myers Squibb (BMY), GSK (GSK) - they're all in, placing their chips on everything from rare diseases to generics to asthma. Clearly, the Big Pharma giants are also trying to keep up with this shift.

As the biotech field evolves, watching these underdogs will be like watching history in the making — where today's Davids become tomorrow's Goliaths. I suggest you keep a close eye on the names above. Adding them to your portfolio would mean you’re not just watching the giants rise — you’ll be a part of the story.

Mad Hedge Biotech and Healthcare Letter

September 19, 2023

Fiat Lux

Featured Trade:

(A SHOT AT HOPE)

(MRNA), (IMTX), (MRK), (PFE), (BMY), (GH), (ILMN), (NVS), (RHHBY), (BGNE), (AZN)

In a quaint Boston lab, as the first rays of dawn broke, a team of scientists, led by Moderna (MRNA), embarked on a mission. Their goal? To craft a solution to one of humanity's most persistent adversaries: cancer.

The grim reality remains that cancer is a leading cause of death in the United States. The statistics are daunting, with over 1.9 million new cases anticipated in 2023 and a projected death toll exceeding 600,000. The financial implications mirror this gravity, with costs expected to soar from $156 billion in 2018 to a staggering $246 billion by 2030.

As the world watched with bated breath, Moderna, already a household name for its COVID-19 vaccine, was silently weaving a narrative that could redefine the future of oncology.

Needless to say, the biotechnology sector, a realm of ceaseless innovation, has been abuzz with Moderna's latest venture. Earlier this month, the biotech announced its agreement with the German drug developer Immatics (IMTX) to develop cancer vaccines and therapies. As part of the deal, Moderna will pay $120 million in cash and will also make additional milestone payments.

This collaboration is not just about the financials; it's a beacon of hope for millions.

The partnership is set to merge Moderna's mRNA technology with Immatics’s T-cell receptor platform, focusing on various therapeutic modalities such as bispecifics, cell therapies, and cancer vaccines. Their combined research aims to leverage mRNA technology for in vivo expression of Immatics's half-life extended TCR bispecifics targeting cancer-specific HLA-presented peptides, among other innovative approaches.

With an upfront investment of $120 million, Moderna has made it clear: they're in it to win it. And the stakes? Potentially life-changing cancer vaccines.

However, this isn’t Moderna’s first foray into the realm of cancer treatments.

Building on the momentum of the technology of its highly potent COVID-19 shots, Moderna announced a partnership with Merck (MRK) earlier this year, combining their efforts to come up with treatments that can drastically reduce the spread of skin cancer. By leveraging Merck's Keytruda with its own innovative vaccine, Moderna has showcased the potential of such collaborations in advancing cancer treatment.

After all, the global community oncology services market is not just growing; it's clearly thriving.

From $47.95 billion in 2022 to a projected $53.79 billion in 2023, the numbers speak for themselves. By 2027, this figure is set to skyrocket to $81.33 billion. Such exponential growth underscores the immense potential and critical importance of advancements in oncology.

Yet, as expected, Moderna isn't the only player on the field.

Giants like Novartis (NVS) and Roche (RHHBY) have also thrown their hats in the ring, collaborating with known international cancer organizations to democratize access to cancer medicines. Among the myriad of promising stocks these days, though, Moderna, China’s BeiGene, Ltd. (BGNE), and the UK’s AstraZeneca PLC (AZN) shine the brightest.

Other notable contributors to the fight against cancer include Bristol Myers Squibb (BMY), Guardant Health (GH), Illumina (ILMN), and Pfizer (PFE). Their diverse portfolios and relentless pursuit of innovation are set to shape the future of oncology.

But as the curtains draw on this narrative, the spotlight remains firmly on Moderna. Their success with the COVID-19 vaccine has already etched their name in the annals of medical history. With their sights now set on cancer vaccines, the world waits with eager anticipation.

In the grand tapestry of medical advancements, Moderna's endeavors in the cancer vaccine domain promise to be a golden thread. Their journey, fraught with challenges and uncertainties, is proof of human resilience and ingenuity. As investors, we're not left standing on the sidelines watching history unfold; we're granted an active role in it.

The potential of Moderna's innovations in oncology beckons a promising horizon. For those looking to make a mark in the annals of medical investments, this biotech offers a gateway to the future of oncology. Act now, and be part of this groundbreaking narrative.

Mad Hedge Biotech and Healthcare Letter

January 31, 2023

Fiat Lux

Featured Trade:

(A SAFE HARBOR IN TUMULTUOUS TIMES)

(JNJ), (AZN), (BGNE)

Investors are still determining what to expect in 2023. The stock market could either gradually make a recovery or plummet deeper. In any case, it’s an excellent plan to add some high-quality stocks to your portfolio.

When choosing which company to invest in, it’s good to keep in mind Warren Buffett’s advice: "If you aren't willing to own a stock for 10 years, don't even think about owning it for 10 minutes.”

A safe and reliable stock to bet on is Johnson & Johnson (JNJ).

JNJ recently disclosed its fourth quarter and full-year financial report, wrapping up a resilient showing in 2022 amid the macro headwinds. In fact, the stock is up compared to 2021, outperforming the broader market and underscoring JNJ’s position as an undisputed “blue-chip” leader.

Apart from highlighting JNJ’s position, this healthcare titan’s earnings typically serve as a bellwether for the rest of the companies in the biopharma space. This means that the relative rosiness of JNJ’s report could back up the belief that Big Pharma is one of the defensive havens in this tumultuous market environment.

In its fourth-quarter earnings call, JNJ shared some ambitious sales growth projections for the following years. For instance, pharmaceutical sales that reached $52.6 billion in 2021 are anticipated to hit $60 billion in 2025. While this is exciting for investors, the road to that goal would be challenging.

JNJ has recently been struggling with the declining sales of two major drugs. The first is its blood cancer treatment called Imbruvica, which has been losing its market share to newer drugs like AstraZeneca’s (AZN) Calquence and BeiGene’s (BGNE) Brukinsa.

On top of the falling sales for Imbruvica, JNJ would also need to battle it out with biosimilars of its top-selling anti-inflammatory injection called Stelara by the end of 2023.

Nonetheless, JNJ’s overall sales climbed by 6.2% in 2022, with the business’ pharmaceutical sector expanding a little faster at 6.8%. As for its medtech segment, it grew a bit slower at 6.1%.

Then, JNJ has the consumer health sector. The segment’s operational sales recorded only 3.9% growth, which was well below the company’s two key business units. Clearly, this division is holding back JNJ’s overall development.

In an effort to resolve this situation and enable the company to grow into a more streamlined business, JNJ plans to spin off the consumer health sector into a new and separate company. This will be Kenvue, which is expected to be launched by the second half of the year.

This move will turn JNJ into a nimbler and more rapidly growing business with a renewed focus on medtech and pharmaceuticals. Moreover, the planned spinoff could offer a short-term catalyst for JNJ stock.

On top of all these, JNJ will most likely announce its 61st consecutive annual dividend increase in April. It’s expected that the company will pay shareholders $4.52 per share every year, showing off a dividend yield of 2.67%. In comparison, the industry average is approximately 2.15%.

These issues cast some doubt on JNJ’s ability to hit its $60 billion target. Nevertheless, it reported a positive outlook for 2023. In its full-year guidance, JNJ projected sales to be between $96.9 billion and $97.9 billion. This indicates an annual growth rate of 5%.

Let’s circle back to the idea that JNJ serves as a good bellwether for the rest of the broader market. This Big Pharma leader is a part of the Dow Jones Industrial Average (DIA) and is included in the Top 10 names in the S&P 500. These are critical factors in using JNJ as an indicator for the rest of the companies.

If JNJ can deliver, or even exceed, EPS estimates and report positive earnings this 2023, then the projections are optimistic for other big companies expected to face similar headwinds.

Big Pharma notably outperformed the broader market in 2022, with investors looking into this segment as a safe harbor amid the economic and financial meltdowns. For context, the S&P 500 Pharmaceuticals industry sector increased by 5.6%. Meanwhile, the broader index fell by 19.4%.

Overall, JNJ is a top-quality stock that maintains a positive outlook in the long run amidst the short-term macro headwinds.

Mad Hedge Biotech & Healthcare Letter

March 25, 2021

Fiat Lux

FEATURED TRADE:

DON’T MISS THE BOAT ON THIS BEST OF BREED BIOTECHNOLOGY STOCK

(AMGN), (MRNA), (PFE), (BNTX), (JNJ), (LLY), (ABBV), (BMY), (FPRX), (BGNE)

The past few weeks have been hectic for the healthcare industry, with Moderna (MRNA), Pfizer (PFE), BioNTech (BNTX), and even Johnson & Johnson (JNJ) working hard to manufacture and distribute their COVID-19 vaccines all over the world.

There’s one major player in the healthcare industry that has been out of the spotlight for quite some time: Amgen (AMGN).

While Amgen has been doing its part from the sidelines by helping out companies like Eli Lilly (LLY) with the manufacturing of their COVID-19 drugs, it looks like investors are flocking towards businesses that allocate more resources toward fighting off the pandemic.

In fact, JNJ recently reached a new high at $170 per share.

Nonetheless, I think investors are missing out on a great opportunity by ignoring Amgen these days.

The biotech world, which basically involves formulating drugs and treatments for living organisms, was somewhat limited back in 1980.

Over the past decades, however, this industry has shifted and managed to successfully launch groundbreaking drugs commercially.

Before, only a handful of legacy companies had occupied this space. Now, so many up-and-coming companies try to conquer the biotech world.

For context, an FDA report in 2019 showed that 64% of drugs approved in the previous year were developed by biotech companies.

Moving forward, it’s reasonable to say that the biotech industry will continue to come up with breakthrough treatments for rare and complex conditions compared to our traditional pharmaceutical companies.

Actually, this sector has been hot in recent years, with companies like AbbVie (ABBV) and Celgene, now with Bristol-Myers Squibb (BMY), coming up with mega-blockbuster treatments, such as Humira and Revlimid, that rake in billions in sales annually.

Among them, Amgen has emerged as one of the most consistent and aggressive players in the biotech world, with competitors still struggling to topple some of its products after decades of being in the market.

This biotech giant has also been busy boosting its pipeline of newly developed treatments. It’s even bolstering its biosimilar lineup to ensure its dominance in the sector.

Last year, Amgen’s revenue rose by 9%, with more growth indicators lighting the way for a brighter future for the company.

While Amgen has been working on many conditions, its portfolio still looks focused on particular diseases.

In 2020 alone, Amgen’s seven blockbusters each generated over $1 billion in revenue. Among these, four managed to rake in more than $2 billion in annual sales.

Amgen’s impressive lineup of drugs includes psoriatic arthritis treatment Enbrel, osteoporosis and bone cancer injection Prolia, and even newcomer heart disease medication Repatha.

With its rivals nipping at the heels of its first-generation blockbusters like Neupogen, Amgen has been hustling to find ways to reinvent itself.

Apart from developing new drugs, the company has been looking into acquisitions to sustain its position at the top.

Recently, Amgen has been doubling down on its newest shining star: Otezla.

Otezla was one of the company’s biggest purchases, with Amgen acquiring this drug for a whopping $13.4 billion from Celgene in August 2019.

In 2019, Otezla sales rose by 25% to reach $1.6 billion. By 2020, the drug generated $2.2 billion in sales, showing off a 36.5% jump.

Over the next few years, Amgen estimates that Otezla sales will climb by over 10% annually.

Riding the momentum of not only Otezla but its entire portfolio and programs in the pipeline, Amgen aims to dominate the immunology sector.

Among the candidates in Amgen’s pipeline, the most promising is its lung cancer medication Sotorasib, which should complete Phase 2 in the first half of 2021.

Meanwhile, Amgen’s latest deal outside its own pipeline is the $1.9 billion acquisition of Five Prime Therapeutics (FPRX), which is a small biotech company developing treatments for stomach cancers. The agreement should be finalized by June 2021.

Five Prime’s experimental treatment, Bemarituzumab, perfectly aligns with the other stomach cancer medications queued in Amgen’s pipeline.

If this proves successful, then Bemarituzumab will be a strong contender against Bristol-Myers Squibb’s blockbuster treatment Opdivo.

While Opdivo has been in the market longer, Five Prime’s candidate has consistently shown stronger and more promising results since the trials started.

Prior to its deal with Prime Five, Amgen acquired a 20% stake in Beijing-based biotech company BeiGene (BGNE). This is a telling move as it indicates the company’s efforts to expand its reach in Asia, particularly in China and Japan.

Another revenue stream that Amgen has been pushing for expansion is its biosimilars sector.

The company released its first-ever blockbuster, Epogen, in 1989. Since then, this anemia drug has been a top seller. However, biosimilar competition eventually caused a decline in its sales starting in 2015.

Learning from the fall of Epogen in the hands of biosimilars, Amgen decided to turn its weakness into its strength.

Since 2015, the company has been expanding its work on biosimilars. In that year alone, Amgen developed 29 biosimilars for its own products and launched 18 more to compete with other companies.

To date, biosimilars have been generating at least $2 billion in revenues, with 10 more queued in Amgen’s pipeline.

Considering the accelerated growth of the biotechnology sector, now is not the time to count out Amgen.

Today, Amgen has transformed itself into one of the leaders in the biotech world, generating over $25 billion in revenue.

Since 1988, the company has only reported a decline in its year-over-year revenue three times: 2009, 2018, and 2019.

This performance shows tangible proof that Amgen is not a “one-hit-wonder” type of biotech stock. Instead, it demonstrates its capacity to generate solid earnings and sustainability.

Currently, Amgen trades at a price-to-earnings multiple that’s actually 40% lower than the average S&P 500 stock. Its EPS is estimated to rise in the high single digits in the next several years.

Simply looking at its 2020 fiscal report, it’s obvious that Amgen delivered an impressive performance considering the recession and the pandemic.

The company also continues to reward its shareholders with double dividend increases plus an aggressive repurchase program, which Amgen plans to spend roughly $3 billion to $4 billion.

Recently, the stock has been trading at a roughly 30% discount. This is a real bargain considering everything Amgen has to offer.