Below please find subscribers’ Q&A for the March 8 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, CA.

Q: Do you think the US dollar will drop this year?

A: Absolutely it will drop; in fact, the drop started in October last year. We’re actually six months into a bear market for the US dollar (UUP), and bull market for the yen (FXY), the British pound (FXB), the euro (FXE), and the Australian dollar (FXA). However, the rate-cutting scenario is on vacation, and when it comes back from that vacation, then we will see very sharply dropping interest rates, soaring bond prices, and a weak dollar. That scenario is certain to happen by year-end, probably by 10 or 20% —quite a lot. If you just want to buy the basket for foreign currencies, you can sell short the Invesco DB US Dollar Index Bullish Fund (UUP).

Q: Can stocks (SPY) and bonds (TLT) go up at the same time?

A: Well, they shouldn’t, and usually they don’t. But this time it’s different now because we’re all beholden to the interest rate decisions of the Fed. All asset classes are moving together like synchronized swimmers, which means that on days when the market believes that Powell is finished raising rates, you get big bull moves in stocks, bonds, commodities, precious metals, and beanie baby collectibles. And on the bad days like yesterday, where Powell really reiterates how tough his stance is on inflation is unchanged, everything falls in unison. It’s really become a liquidity/confidence/inflation on-off type market. We have been playing that like a maestro for the last six months and have made a ton of money. I hope it continues that way. “If it’s working, don’t fix it” is my philosophy on trading, which is constantly changing.

Q: Do small caps underperform or overperform in a rising rates era?

A: They always do poorly because small caps have fewer cash reserves, more leverage, and more exposure to interest rates, as opposed to large caps which, in the tech area, don’t borrow at all. They’re actually net creditors to the system so they make more money when interest rates go up. I imagine the interest income at Apple this year has to be absolutely gigantic. That said, small caps always lead recoveries because of their excess leverage, so that's why people are piling into small caps on dips right now. Going from terrible to just bad often generates the best stock returns.

Q: How long will “steering wheel falling off” news tank Tesla?

A: Well, it was worth a $6 dollar drop today in an otherwise weak market. First of all, if there are any actual problems with Tesla, they fix them immediately for free, and most of the fixes can be done with a software upgrade which they do at midnight the day of the recall. Second, a lot of these stories about Tesla problems are false, planted there by the oil industry, trying to head off their own demise. Third, when you go from making several thousand to several million cars a year, scaling up to mass production always uncovers some sort of manufacturing flaws. Tesla can fix them faster than anyone else. I remember when the first Model S came out 13 years ago, we had a hot day and all the sealants on the windows melted. They said they didn’t know because it doesn’t get that hot in Fremont California where they build the cars. They sent out a truck the next day and installed all new sealants on our windows. So that is part of living with Tesla, which seems bent on taking over the world. And I’m working on a major update on Tesla report. I listened to the whole 3.5-hour investors day, and I'll get that out when I get all the snow shoveled. Full disclosure: Elon Musk personally gave me a free $12,800 Tesla Powerwall three years ago. It’s the red one.

Q: I just bought the United States Natural Gas Fund (UNG) 14/15 2025 LEAP for $0.20 with UNG down 3%.

A: I’m going to share that LEAPS with all the Global Trading Dispatch members tomorrow. So far, only the Mad Hedge Concierge members have seen it. We’ll go into great detail in tomorrow’s letter about why you want to buy natural gas here and how you want to play it.

Q: It seems the Fed won’t be happy unless there’s a recession; am I reading this wrong?

A: I think Powell is striving for perfection—killing off inflation and lowering interest rates without a recession. I actually am hoping for a recession myself, even if it’s just for one quarter because that greatly increases market volatility and makes my bond long look like a stroke of genius. And let’s see if he can pull it off. He’s coming facing so many unprecedented challenges to the economy, like the pandemic, the end of liquidity, and the extreme worker shortage. It’ll be really interesting to see what happens. Multiple PhD theses in economics begging to be addressed in there.

Q: Will artificial intelligence cause another bubble?

A: Absolutely, yes. And if you’ve been in the market long enough, you become a bubble collector like me. Just off the top of my head, 3D printing, cold fusion, bitcoin, portfolio insurance, Nifty 50, eyeballs,—if I spent more time, I could come up with an endless list. And this is how Wall Street makes their money—they create bubbles by manufacturing compelling, irresistible stories that can be sold to the masses. Some of these like cold fusion, I know immediately won’t work for 20 years because of my physics background, and definitely not now. Some of these other ones are just flashes in the pan and never work. You just get used to an endless series of bubbles. AI is new only if you haven’t been watching. The share prices of Google, Amazon, Apple, have already had gigantic moves in the last 20 years, largely because of their use of artificial intelligence. So those are your plays—those and (NVDA), which provides the essential chips for artificial intelligence, and we’re active in all of these, both on the long and short side.

Q: Is climate change a hoax or a bubble?

A: If you think it’s a hoax, will you please come over to Incline Village and get the 12 feet of snow off my damn roof before the house collapses. I already can’t close any doors in the house because the weight of the snow is buckling the house and bending the door frames. If you finish the roof, then you can get to work on my deck which also has about 8 ft of snow and is at risk of collapsing, like many in town already have. This has never happened before. The climate has changed.

Q: How come there’s never mention of demographic shift in other parts of the world when there is in the US?

A: The US is the only country in the world where you can earn enough money to retire early. If you live on the coasts, you can sell your house for cash, move inland and never work again, no matter your age. There is no other country where you can do that. Maybe there will be in the future, but definitely not right now. People who complain about how awful the economy is here forget that this is the best economy in the world and has been so for a very long time. I go with the Warren Buffet outlook on this, which is “Never bet against America.”

Q: How about an Entry point for Freeport McMoRan (FCX)?

A: It’s lower. You don’t want to touch it while the entire commodity sector is selling off in fears of higher interest rates in a recession. Once that’s over it goes to $100.

Q: What is the best way to play Natural Gas?

A: I’ll send an extended report tomorrow, but the short answer is United States Natural Gas Fund (UNG) and ProShares Ultra Bloomberg Natural Gas (BOIL), which is a 2x long day trading NatGas ETF.

Q: Are we entering LEAPS territory for Rivian (RIVN)?

A: Yes, just wait for the current selloff to end and then go to the longest possible expiration. This thing will have a multiple move 2x, 3x, or a 10x out the other side of any recession. The CEO is brilliant and people love the cars.

Q: What happens to housing prices when interest rates on mortgages are at 7%?

A: Well, they should go down 10-20%. What they’re actually doing is going sideways, and they’re still going up in the cheaper neighborhoods because of the structural shortage of 10 million houses in the US. The all-cash buyers are still out there buying. There is tremendous inventory shortage in the housing market now; every broker I know got cleaned out of all their inventory in January when we had a brief 100 basis point dip in rates back then, which has since gone away. I think we go sideways in housing until the end of the year, and then big interest rate cuts will be obvious by then, and the market takes off and we have another 10-year bubble. If you think housing is expensive now, go visit Sydney Australia or Shanghai, China and you’ll see how expensive housing can really get.

Q: How how high would Fed funds have to get to cause a real recession?

A: My guess is 6%. We might actually get there in the second quarter. That might trigger enough of a recession to start unemployment rising just enough to let them cut interest rates. My attitude is: rip the Band-Aid off, raise by 75 basis points on March, and get it over with. But Jay Powell is a very gradualist type of guy, even though he’s brought the sharpest interest rate rise in history.

Q: Should I chase Apple (AAPL) here at $150 a share?

A: In this kind of market, you never chase anything. Only buy Apple at $150 if you think happy days are here again and you think we’re going up forever. To me on the chart it looks like we’re double topping and may actually get a lower low, which you then buy. You may even want to do a LEAPS on Apple if we get down into the $130s or $120s again.

Q: Isn’t it hard for the economy to really tank when seniors and savers are now generating income again for their retirement, giving them more income to spend?

A: Well not only that but workers have had 10-20% pay increases also, and they have more money to spend. It’s really hard to see a severe recession in any kind of scenario, barring another pandemic, and that’s why we’re saying buy the dips—we are in fact in a new bull market that started in October. When you get these market reversals, you often don’t get confirmation on the charts for up to a year, and we’re in one of those periods now. That's why there are still a lot of non-believers in the bull scenario and no confidence.

Q: Would you buy Tesla LEAPS?

A: Yes, under $150 on Tesla shares. And, given its record of volatility, we may actually get there, because this is a $1,000 stock easily in 5 years. I'll send you a report giving you all the details of why. Detroit is basically screwed, someday it’ll just be reduced to building Teslas under license from Tesla and painting them different colors and giving them different names or something like that.

Q: What’s a buy-on-dip?

A: Sorry, but no easy answer here. It’s unique to every stock depending on the historic volatility and ranges of the stock. It’s going to be 1% for a stock, it can be 10% for an option, it could be 20% for a stock like Tesla. It’s vague but it really is unique to every single stock. A good rule of thumb is that after you execute a trade and then throw up on your shoes you’ve just done a great trade.

Q: I see from your pictures that you lost weight? How do you do it?

A: I got COVID last May. I lost 20 pounds in two weeks because I couldn’t eat while I was sleeping 20 hours a day. I just woke up long enough to send out trade alerts. All of a sudden, a 40-year collection of expensive designer pants fit. My kids now call me Captain Fancy Pants. When I go through airport security now and take my belt off they fall down so I’m always careful to wear my best underwear, the ones with the dollar sing all over them.

Q: What’s the best way to play obesity drugs?

A: Unfortunately, There is no pure play on obesity drugs. It will be a $150 billion market that will grow very quickly. I will talk about it at length next week in the summit at the Biotech & Health Care webinar, which you’ll get registration links for tomorrow. Weight loss drugs are small pieces of very large drug companies, so the effect gets diluted by everything else they’re doing. The purest play may be Weight Watchers (WW). If you just need to go to Weight Watchers just to get a shot, that could be really good for them. The stock just doubled in one day on this.

Q: Commodity-based foreign stocks are the best bet on inflation protection; should I get involved?

A: Yes, use the current selloff to get into the whole commodity space (except for maybe food) because not only are they a commodity play, they’re a weak dollar play and that way you get a combined double leverage effect on prices, which I've seen happen many times in my life. So yes, look at foreign-type commodity stocks, and of course, the biggest one out there is Broken Hill Proprietary (BHP), which I always watch very closely. It’s the largest stock in Australia owned by virtually everybody in Australia who has any money, with great volatility, and which has recently just had a selloff.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2015 in Ouarzazate Morocco

https://www.madhedgefundtrader.com/wp-content/uploads/2023/03/john-thomas-morocco.png620630Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-03-10 09:02:522023-03-10 10:26:57March 8 Biweekly Strategy Webinar Q&A

Going against the market consensus has been working pretty well lately.

When the world prayed for a Santa Claus rally, I piled on the shorts. When traders expected a New Year January crash, I filled my boots with longs.

That’s how you earn an eye-popping 19.83% profit in a mere nine trading says, or 2.20% a day.

The other day, someone asked me how it is possible to get mind-blowing results like these. It’s very simple. Get insanely aggressive when everyone else is terrified, which I did on January 3. I also knew that with the Volatility Index (VIX) falling to $18, pickings would quickly get extremely thin. It was make money now, or never.

To quote my favorite market strategist, Yankees manager Yogi Berra, “No one goes to that restaurant anymore because it’s too crowded.”

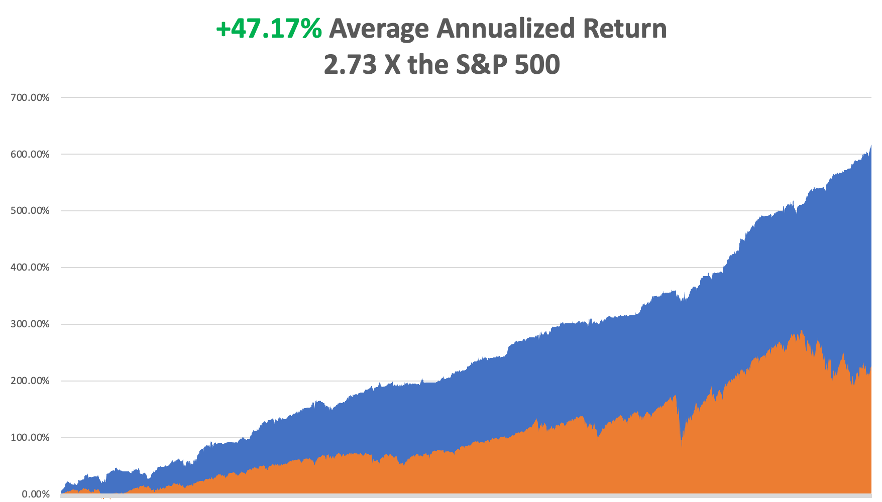

My performance in January has so far tacked on a welcome +19.83%. Therefore, my 2023 year-to-date performance is also +19.83%, a spectacular new high. The S&P 500 (SPY) is up +3.78% so far in 2023.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 15 years ago. My trailing one-year return maintains a sky-high +103.30%.

That brings my 15-year total return to +617.03%, some 2.73 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +47.17%, easily the highest in the industry.

I took profits in my February bonds last week (TLT), taking advantage of a $5 pop in the market. All my remaining positions are profitable, including longs in (GOLD), (WPM), (TSLA), (BRK/B), and (TLT), with 30% in cash for a 10% net long position.

Since my New Year forecasts have worked out so well, I will repeat the high points just in case you were out playing golf or bailing out from a flood when they were published.

Buy Falling Interest Rate Plays, as I expect the yield on the ten-year US Treasury yield to fall from 3.50% to 2.50% by yearend. That means Hoovering up any kind of bond, like (TLT), (MUB), (JNK), and (HYG). Falling interest rates also shine a great spotlight on precious metals like (GLD), (SLV), (GOLD), and (WPM).

The US Dollar Will Continue to Fall. Commodities love this scenario, including (FCX), (BHP), and emerging markets (EEM).

Inflation Will Decline All Year and should go below 4% by the end of 2023. In fact, we have had real deflation for the past six months. Financials do well here, like (MS), (GS), (JPM), (BAC), (C), and (BRK/B).

Which creates another headache for you, if not an opportunity. We may have a situation where the main indexes, (SPY), (QQQ), and (IWM) go nowhere, while individual stocks and sectors skyrocket. That creates a chance to outperform benchmarks…and everyone else. There has been a lot of discussion among traders lately about the collapse of the Volatility Index ($VIX) to $18, a two-year low and what it means.

They are distressed because a ($VIX) this low greatly shrinks the availability of low risk/high return trading opportunities. A ($VIX) this low is basically shouting at you to “STAY AWAY!”

Does it mean that an explosion of volatility is following? Or are markets going to be exceptionally boring for the next six months?

Beats me. I’ll wait for the market to tell me, as I always do.

Consumer Price Index Falls 0.1% in December, continuing a trend that started in June. Stocks popped and bonds rallied. YOY inflation has fallen to 6.5%. “RISK ON” continues. Now we have to wait another month to get a new inflation number. The economy has now seen de facto deflation for six months. Gas prices led the decline, now 9.4%. We might get away with only a 0.25% interest rate hike at the February 1 Fed meeting.

Bond Default Risk Rises, as well as a government shutdown, as radicals gain control of the House. This is the group that lost the most seats in the November election. Bonds are the only asset class not performing today, and paper with summer maturities is trading at deep discounts. It certainly casts a shadow over my 50% long bond position. However, I don’t expect it to last more than a month and my longest bond maturity is in February.

The US Consumer is in Good Shape, according to JP Morgan’s Jamie Diamond. Spending is now 10% greater than pre covid, and balance sheets are healthy. No sign of an impending deep recession here.

Boeing Deliveries Soar from 340 to 480 in 2022, and 479 new orders. A sudden aircraft shortage couldn’t have happened to a nicer bunch of people. The 737 MAX has shaken off all its design problems after two crashes four years ago. Cost-cutting here can be fatal. Europe’s Airbus is still tops, with 663 deliveries last year. Don’t chase the stock up here, up 79% from the October lows, but buy (BA) on dips.

Small Business Optimism Hits Six-Month Low to from 91.9 to 89.8, adding to the onslaught of negative sentiment indicators, so says the National Federation of Independent Business (NFIB).

Copper Prices Set to Soar Further with the post-Covid reopening of China, according to research firm Alliance Bernstein. After a three-year shutdown, there is massive pent-up demand. Copper prices are at seven-month highs. Keep buying (FCX) on dips.

Australian Metals Exports Soar, as the new supercycle in commodities gains steam. Shipments topped $9 billion in November, 20% higher than the most optimistic forecasts. Keep buying copper (FCX), aluminium (AA), iron ore (BHP), gold (GLD) and silver (SLV) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, January 16, markets are closed for Martin Luther King Day.

On Tuesday, January 17 at 8:30 AM EST, the New York Empire State Manufacturing Index is out

On Wednesday, January 18 at 11:00 AM, the Producer Price Index is announced, giving us another inflation read.

On Thursday, January 19 at 8:30 AM, the Weekly Jobless Claims are announced. US Housing Starts and Building Permits are printed.

On Friday, January 20 at 7:00 AM, the Existing Home Sales are disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, the University of Southern California has a student jobs board that is positively legendary. It is where the actor John Wayne picked up a gig working as a stagehand for John Ford which eventually made him a movie star.

As a beneficiary of a federal work/study program in 1970, I was entitled to pick any job I wanted for the princely sum of $1.00 an hour, then the minimum wage. I noticed that the Biology Department was looking for a lab assistant to identify and sort Arctic plankton.

I thought, “What the heck is Arctic plankton?” I decided to apply to find out.

I was hired by a Japanese woman professor whose name I long ago forgot. She had figured out that Russians were far ahead of the US in Arctic plankton research, thus creating a “plankton gap.” “Gaps” were a big deal during the Cold War, so that made her a layup to obtain a generous grant from the Defense Department to close the “plankton gap.”

It turns out that I was the only one who applied for the job, as postwar anti-Japanese sentiment then was still high on the West Coast. I was given my own lab bench and a microscope and told to get to work.

It turns out that there is a vast ecosystem of plankton under 20 feet of ice in the Arctic consisting of thousands of animal and plant varieties. The whole system is powered by sunlight that filters through the ice. The thinner the ice, such as at the edge of the Arctic ice sheet, the more plankton. In no time, I became adept at identifying copepods, euphasia, and calanus hyperboreaus, which all feed on diatoms.

We discovered that there was enough plankton in the Arctic to feed the entire human race if a food shortage ever arose, then a major concern. There was plenty of plant material and protein there. Just add a little flavoring and you had an endless food supply.

The high point of the job came when my professor traveled to the North Pole, the first woman ever to do so. She was a guest of the US Navy, which was overseeing the collection hole in the ice. We were thinking the hole might be a foot wide. When she got there, she discovered it was in fact 50 feet wide. I thought this might be to keep it from freezing over but thought nothing of it.

My freshman year passed. The following year, the USC jobs board delivered up a far more interesting job, picking up dead bodies for the Los Angeles Counter Coroner, Thomas Noguchi, the “Coroner to the Stars.” This was not long after Charles Manson was locked up, and his bodies were everywhere. The pay was better too, and I got to know the LA freeway system like the back of my hand.

It wasn’t until years later when I had obtained a high-security clearance from the Defense Department that I learned of the true military interest in plankton by both the US and the Soviet Union.

It turns out that the hole was not really for collecting plankton. Plankton was just the cover. It was there so a US submarine could surface, fire nuclear missiles at the Soviet Union, then submarine again under the protection of the ice.

So, not only have you been reading the work of a stock market wizard these many years, you have also been in touch with one of the world’s leading experts on Artic plankton.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/10/john-thomas-peleliu-island-1975.png434628Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-17 09:02:252023-01-17 14:36:18The Market Outlook for the Week Ahead, or Going Against the Consensus

Below please find subscribers’ Q&A for the November 16 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: What do you see Tesla (TSLA) moving to from here until next year?

A: Not much; I mean if you’re lucky, Tesla won’t move at all. The problem is Twitter is looking like a disaster of huge proportions—firing half the staff on day one? Never good for building a business. Tesla has also been tied to the rest of big tech, which has been in awful condition and may not see a continuous move upward until the Fed actually starts lowering interest rates in the second quarter of next year. Tesla could be dead money here for a while; eventually, a company growing at 50% a year will go up—especially when it’s just had a 50% decline in the share price. As to when that is, I don’t know, and asking me 15 more times will get you just the same answer.

Q: Should we start piling into iShares 20 Plus Year Treasury Bond ETF (TLT) longs now or wait?

A: You go now. Every day you waited meant paying one point more in TLT. I think the bottom is in; we have a 20-30 point move ahead of us. Everybody in the world is now trying to get into this trade, just like I spent all this year trying to get out of it. And if anything, November CPI could be a long term-term top in inflation, especially if we came in with another cold number. So, I would start scaling in now, even though we’re over $100 in the (TLT) today and I first recommended this around $95.

Q: If the Fed keeps raising interest rates, will the US Treasury market fall?

A: Probably not because the Fed only has control of overnight interest rates—the discount rate, the interbank rate—whereas the (TLT) is a 10-to-20-year maturity bond. No matter what short term rates do, the inversion will just keep getting bigger, but in fact, the bond market itself was yielding 4.46%, yielding 8% with junk, has bottomed and will probably start going up from here. So that is the difference between the Fed and what the actual market does.

Q: Do you prefer Junk (JNK), (HYG), or (TLT)?

A: I always go for the highest risk. Junk has about an 8% yield here compared to 3.75% for the TLT. By the way, if you want to do one trade and go to sleep, buy the junk on 2 to 1 margin, get your 16% yield next year, and just take a one-year vacation. That’s what some people do.

Q: When you say the dollar is going to go down what do you mean?

A: I mean the US dollar, while Canadian (FXC) and Australian dollars (FXA) will go up.

Q: What is the best time to buy US dollars?

A: Maybe in five years, as it could go down for five or 10 years from here, now that it’s going to imminently give up its yield advantage.

Q: What's the forecast for casinos?

A: I think casinos do better. Las Vegas was absolutely packed, you couldn’t get into the best hotels—people are spending money like crazy.

Q: What’s the best way to play (TLT)?

A: With a one-year LEAP. I put out the $95/$100 last week for my concierge members. Here, you probably want to do the $100/$105; that’ll still give you a one-year return of 100%.

Q: How do you short the dollar?

A: There are loads of short dollar ETFs out there, or you can just sell short the Invesco DB US Dollar Index Bullish Fund (UUP), which is the dollar basket, or buy the (FXA) or (FXE).

Q: Freeport McMoRan (FCX) just went from 25 to 38; is it time to take a profit and re-enter at a lower point?

A: Short term yes, long term no. My long-term target for (FCX) is $100 because of the exponential growth of copper demand caused by EV production going from 1.5 million to 20 million a year in the next 10 years. Each EV needs 200 pounds of copper, so by 2030, annual copper demand for EVs only will be 20 billion pounds. In 2021, the total annual global copper production was 46.2 billion pounds. In order words, global copper production has to double in eight years just to accommodate EV growth only.

Q: Do you think there’ll be a rail worker strike?

A: I have no idea, but it will be a disaster if there is. There’s your recession scenario.

Q: What strike prices do you like for a Tesla LEAP?

A: Anything above here really. You could be cautious and do something like a $200/$210 two years out—that has a double in it. Or you could be more adventurous and go for a 400% return with like a $250/$260 in two years. I’m almost sure that we’ll have a major recovery in Tesla within two years.

Q: What’s your opinion on PayPal (PYPL) and Albemarle (ALB)?

A: I’m trying to stay away from the fintech area, partly because it’s tech and partly because the banks are recapturing a lot of the business they were losing to fintech a couple of years ago by moving into fintech themselves. That is the story and we’re clearly seeing that in the share prices of both banks and PayPal. I like Albemarle because the demand for lithium going forward is almost exponential.

Q: What’s your thought on the Australian dollar (AUD)?

A: Buy it with both hands as it is going to parity. Australia is a great indirect play on trade with China (FXI), gold (GLD), uranium (CCJ), and iron ore (BHP). It’s a great play on the recovery of the global economy, which will start next year.

Q: What do you think about Royal Caribbean Cruises Ltd (RCL)?

A: Probably a buy but remember all the cruise lines will be impaired to some extent by the massive debts they had to take on to survive two years of shutdown with the pandemic. I took the Queen Victoria last July on their Norwegian Fjord cruise, and it had not been operated for two years. None of the staff had any idea what to do. I had to show them.

Q: Will big tech have a good second half?

A: Probably, but it’s going to be a slow first quarter, and I think if we start getting actual cuts in interest rates, then it’s going to be off to the races for tech and they’ll all go to all-time highs as they always do.

Q: How come you haven’t issued any trade alerts yet on the currencies?

A: Calling a five-year turnaround is a big job. Now that we have the turnaround in play, we’re in dip-buying mode. So, you will see these in the future. But I also have to look at what currency trades are offering compared to other trades in other asset classes. And for the last year or two, the big opportunities have all been in stocks. You had volatility constantly visiting the mid $30s, you didn’t get that in the currencies, and more money was to be made in stock trades than foreign currency trades. That is changing now; let's see if we have a sustainable trend and if we get a good entry point. There’s a lot that goes into these trade alerts that you don’t always get to see. We only get a 95% success rate by being very careful in sending out trade alerts and that means long periods of doing nothing when the risk/reward is mediocre at best, which is right now. The services that guarantee you a trade alert every day all lose money.

Q: What is the recommended minimum portfolio size to amortize the cost of the concierge service?

A: I tell people to have a half a million in assets because we want people who are financially sophisticated to understand what we’re telling them. That said, we do have people with as little as 100,000 in the concierge service and they usually make the money back on the first trade. This is a very sophisticated high-return, very active service. You get my personal cell phone number and all that, plus your own dedicated website, and specific concierge-only research. It’s a much higher level of service. It’s by application only and we currently have no places available for new concierge members. However, if you’re interested, we can put you on the waitlist so that when another millionaire retires, we can open up a space.

Q: Despite recent moves, the algo looks bearish. There are lots of mixed signals.

A: Yes, it does. And yes, that’s often the case when the market timing index hangs around 50.

Q: Do concierges go for short term moves?

A: No, concierges are looking for the big, long-term trades that they can just buy and forget about. That is where the big money is made. At least 90% of the people that try day trading lose money but make all the brokers rich.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or Technology Letter, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/John-with-fish-story-3-e1524263315551.jpg378300Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-18 10:02:302022-11-18 11:44:34November 16 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the February 2 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, Nevada.

Q: Thoughts on Palantir Technologies Inc. (PLTR)?

A: Well, we got out of this last summer at $28 because the CEO said he didn’t care what the share price does, and when you say that, the market tends to trash your stock. But Palantir is also in a whole sector of small, non-money-making, expensive stocks that have just been absolutely slaughtered. And of course, PayPal (PYPL) takes the prize for that today, down 25% and 60% from the top. So, we’re giving up on that whole sector until proven otherwise. Until then, these things will just keep getting cheaper.

Q: Given the weakness in January, do you think we still have to wait until the second half of the year for a viable bottom?

A: Definitely, maybe. If things are going to happen, they are going to happen fast; we got the January selloff, but that’s nowhere near a major selloff of 20%. And the fact is, the economy is still great so that’s why this is a correction, not a bear market. At some point, you want to buy into this, but definitely not yet; I think we take another run at the lows again sometime this month. We just have to let all the shorts come out and take their profits so they can reestablish again.

Q: Why are bank stocks struggling?

A: A lot of the interest rate rises that we’re getting now were already discounted last year—banks had a great year last year—so they were front running that move, which is finally happening. To get more moves out of banks, you’re going to have to get more interest rate rises, which we will get eventually. We still like the banks long term, we still like financials of every description, but they are taking a break, especially on the “sell everything” index days. A lot of the recent selling was index selling—banks have a heavy weighting in the index, about 15%. So, they will go down, but they will also be the ones that come back the fastest. We’re seeing that in some of the financials already, like Berkshire Hathaway (BRKB) and Morgan Stanley (MS) which are both close to all-time highs now.

Q: What about the situation with Russia and Ukraine?

A: It’s all for show. This is a situation where both the US and Russia need a war, or threat of a war, because the leaders of both countries have flagging popularity. Wars solve those problems—that’s why we have so many of them by the United States. We’ve been at war essentially for most of the last 40 years, ever since Ronald Reagan came in.

Q: I didn’t exit my big tech positions before the crash, should I just hang onto them at this point?

A: The big ones—yes. The Apples (AAPL), the Googles (GOOGL), the Amazons (AMZN) —they’re only going to drop about 20% at the most, maybe 25%, and then they’ll go to new highs, probably before the end of the year. If you’re good enough to get out and get back in again on a 20% move, go for it. But most people can’t do that unless they’re glued to their screens all day long. So, if you have stock, keep the stock; if you have options, get out of the options, because there the time decay will wipe you out before a turnaround can happen. This is not an options environment, unless you’re playing on the short side in the front month, which is what we’re doing.

Q: When you send out the trade alerts, I have a hard time getting them executed. How do you advise?

A: Move the strike price, go out in maturity, and you can get our prices at slightly higher risk. Or, just leave it and, quite often, people’s limit orders get done at the end of the day when the algorithms have to dump their positions at the close because they’re not allowed to carry overnight positions. Also, even if you get half of my trade alerts, you’re doing pretty good—we’re running at a 23% rate in 6 weeks, or 200% annualized. And remember, when I send out a trade alert, you’re not the only one trying to get in there, so you can even go onto a similar security. If I recommend Alphabet (GOOGL), consider going over to Microsoft (MSFT), because they all tend to move together as a group.

Q: I am sitting on a 16% profit in the ProShares Ultra Technology (ROM), which you recommended. Should I take the money and run, and get back in at a lower price?

A: Yes, this is just a short covering rally in a longer-term correction, and you make the money on the volume. You win games by hitting lots of signals, not hanging on to a few home runs where people usually strike out.

Q: You said inflation will be short lived, so why would there be 9 interest rates after the initial 4?

A: It’s going to take us 8 interest rates just to get us back to the long-term average interest rate. Remember the last 2% is totally artificial and only happened because there was a financial crisis 13 years ago. So, to normalize rates you really need to get overnight rates back up to about 3.0%. And that means 12 interest rate hikes. If you don’t do that, you risk inflation going from controllable to uncontrollable, and that is the death of the Fed. So, that’s why I expect a lot more interest rate rises.

Q: Will the tension between Russia and the Ukraine affect the market?

A: No, it hasn’t so far and I don’t expect it to. Although, it’s hard to imagine going through all of this and not seeing a shot fired. When that one shot gets fired, then maybe you get a down-500-point day, which it then makes back the next day.

Q: Anything to do with Alphabet (GOOGL) announcing its 20 to one split?

A: No, it’s too late. We had a trade alert out on a Google 20 call spread which we actually took profits on this morning. So, nice win for the Mad Hedge Technology Letter there. There’s nothing to do with these splits, it’s not like they’re going to un-announce it, this isn’t a risk-arbitrage situation where there’s always an antitrust risk hovering over the deal that may crash it. This is pretty much a done deal and doesn’t even happen until July 1. People think bringing the share price from $3,000 down to $150 makes it available for a lot more potential retail buyers, which it does. It also makes call spreads on the options a lot cheaper too. When we put out these alerts, we can only do one or two contracts, even tying up $10,000—divide that by 20 and all of a sudden your cheapest Google call spread cost $500 instead of $10,000.

Q: Can you speak about the liquidity on your strikes? Sometimes we’re trading against strikes that have no open interest.

A: Whenever you put in an order for one strike, even if there’s nothing outstanding on that strike, algorithms will arbitrage against that strike—where your order is—against all the other strikes on the whole options chain. So, don’t worry if you have limited open interest or no open interest on our trade alerts. They will get done, and it may get done by some algorithm or some market maker taking more of another strike, that’s how these things get done. It’s all thanks to the magic of computers.

Q: Do you have thoughts about Freeport-McMoRan (FCX)? I have some profitable LEAP positions open.

A: It’ll go higher, keep them. And I like the whole commodity space, which means iron ore (BHP), copper, steel (X), etc.

Q: Would you trade Barclays iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX) at this point?

A: No, because we’re dead in the middle of the recent range. That’s a horrible place to enter—you only enter (VXX) on extremes on the upsides and the downside.

Q: What should I do about Airbnb (ABNB) at this price? They’ve been profitable for 2-3 years, with revenues rising.

A: I think Airbnb is one of the best run companies in the world, and I expect their earnings to keep growing like crazy, especially once we get out of the pandemic. I am also a very frequent Airbnb user, having stayed in Airbnb’s in at least 10 countries, so I’m a big fan of them. The stock just got dragged down by the small tech bust but it will come back. This is a “throwing the baby out with the bathwater” situation.

Q: Are there any good LEAPS candidates now?

A: I’m not doing any LEAPS until we reach the final cataclysmic selloff of the correction. Otherwise, the time value will run against you enormously; I’d rather wait for better prices.

Q: Do you see a cataclysmic selloff?

A: Yes, I do. Maybe in a few more weeks, and maybe next week if we get a really hot 8%+ inflation rate—that would really kill the market.

Q: What will tell you if inflation is ending or slowing labor?

A: Labor is 70% of the inflation calculation. So, when these huge pay awards slow down, that's when inflation slows down. By the way, a lot of pay increases that are happening now are catch-up from the last 40 years of no pay increases for American workers in real inflation adjusted terms. So, a lot of this is catch-up—once that’s done, you can forget about inflation. Also, the long-term pressure of technology on prices is downwards, so allow that to reignite deflation, and that will be your bigger issue over the long term.

Q: What should I do about Editas Medicine Inc (EDIT) or CRSPR Therapeutics AG (CRSP)?

A: Don’t touch the sector, it’s out of favor. Let this thing die a slow death. When they come up with profitable products, that’s when the sector recovers. So far, everything they have works in labs but there are no mass-produced Crispr products, they’re trying for mass production on sickle cell anemia and a couple of other things, but still very early days in CRSPR technology.

Q: When will this recording be posted?

A: In two hours, it will be posted on the website. Go to “My Account” and you’ll find the last 13 years of recorded webinars.

Q: What do you mean by “stand aside from Foreign Exchange”?

A: The volatility in the foreign exchange market is just so low compared to equities and bonds, it’s not worth trading right now. When you can trade everything in the world—foreign exchange is at the bottom of the list. If I see a good entry point, I’ll do a trade; but do I trade Tesla (TSLA) with a volatility of 100%, or foreign exchange with a volatility of 5%? Those are the choices.

Q: Should I do any short plays in oil (USO)?

A: Generally, you don’t want to short any commodity unless you're a professional; I say that having been short beef futures when Mad Cow Disease hit in 2003 and you had three limit-up days in a row in the futures market. That happens in the commodity areas—liquidity is so poor compared to stocks and bonds that if you get caught in one of these one-way moves, you can’t get out. So that is the risk; and I’ve known people who have gone bust trading oil both long and short, so this is for professionals only. With stocks you get vastly more data and information than you do in the commodity markets where industry insiders have a much bigger advantage.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Aga Sophia Mosque in Istanbul

https://www.madhedgefundtrader.com/wp-content/uploads/2022/02/john-thomas-in-instanbul.png560420Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-04 11:02:562022-02-04 14:06:17February 2 Biweekly Strategy Webinar Q&A

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.