Mad Hedge Biotech and Healthcare Letter

September 5, 2024

Fiat Lux

Featured Trade:

(A VERY STRONG CELL-ING POINT)

(TXG), (NSTG), (BRKR), (ILMN), (BMY), (GILD), (BIO)

Mad Hedge Biotech and Healthcare Letter

September 5, 2024

Fiat Lux

Featured Trade:

(A VERY STRONG CELL-ING POINT)

(TXG), (NSTG), (BRKR), (ILMN), (BMY), (GILD), (BIO)

Mad Hedge Biotech and Healthcare Letter

August 13, 2024

Fiat Lux

Featured Trade:

(THE RISE OF THE STEADY EDDIES)

(CNC), (UNH), (PFE), (JNJ), (ABBV), (LLY), (BIO), (UHS), (WAT), (AMGN), (REGN), (VRTX), (CRSP), (MRNA)

Think of the market as a body fighting off an infection. Tech stocks might be the flashy antibodies, but healthcare is the steady, reliable immune system, keeping things stable when the going gets tough. And right now, that immune system is looking stronger than ever.

Skeptical? I get it. We've heard the hype about healthcare before. But this time, it's different.

The Healthcare Select Sector SPDR ETF (XLV) has been on a tear, up 9.3% this year as of Thursday's close. That's nearly keeping pace with the broader S&P 500's 12% gain - a remarkable feat in a market that's been anything but stable.

But what's even more impressive is the turnaround. Back in mid-July, XLV was lagging behind like a three-legged horse in the Kentucky Derby, up only 8.3% while the S&P 500 was showing off with an 18% gain.

In fact, out of the 63 healthcare stocks in the S&P 500, only a dozen have been slacking off since July. The rest? They've been outperforming like it's going out of style.

So what changed?

Well, it wasn't so much that healthcare stocks suddenly discovered the fountain of youth. No, my friends, it was more like the rest of the market decided to take a swan dive off the high board.

You see, while tech stocks were busy doing their best Icarus impression – flying too close to the sun and then plummeting back to earth – healthcare stocks were steady as she goes. It's like the old tortoise and hare story, except in this version, the hare got distracted by shiny objects and ran off a cliff.

Now, let's shine the spotlight on some of the key players driving this healthcare rally.

Remember those health insurers everyone was worried about back in spring? The ones that had investors biting their nails over the future of Medicare Advantage? Well, they've made a comeback.

The S&P 500 Managed Health Care index was down 12% in mid-April, looking about as healthy as a chain smoker with a Big Mac habit. But now? It's up 4.5% since the start of the year.

Companies like Centene (CNC) and UnitedHealth Group (UNH) have bounced back faster than a rubber band on steroids.

And it's not just the insurers. Big Pharma's been flexing, too.

Pfizer (PFE), the company that became a household name faster than you can say "vaccine," is holding steady. Johnson & Johnson (JNJ) is up 2.2%, probably thanks to all that baby powder they're not selling anymore.

Meanwhile, AbbVie’s (ABBV) up 11% since July. These guys are like the Energizer Bunny of the pharma world – they just keep going and going.

But the real showstopper? Eli Lilly (LLY). This biopharma has been on a tear since the beginning of 2024. Up 45% on the year at one point, they've been climbing faster than a squirrel up a tree with a dog in hot pursuit.

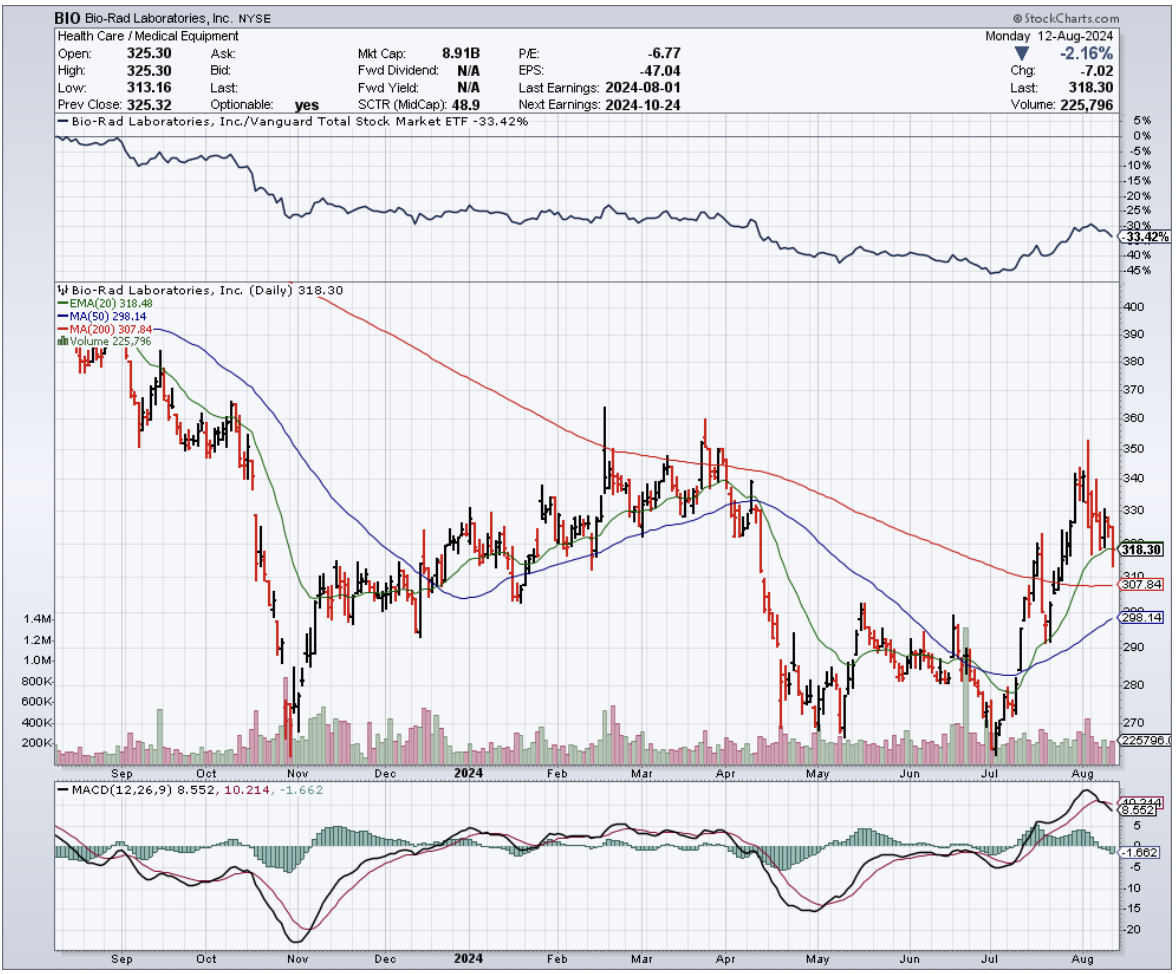

Then, there are companies like Bio-Rad Laboratories (BIO), up 20% since July. Universal Health Services (UHS)? Up 18% since July. Waters (WAT), the life sciences tools folks? Up 15%.

Even the biotechs are out to impress.

Amgen (AMGN), the granddaddy of biotech, is up 10% year-to-date. They're selling drugs like Prolia and Enbrel faster than hotcakes at a lumberjack convention.

And Amgen’s pipeline? It’s packed with potential blockbusters, setting the stage for further expansion in the future.

Gilead Sciences (GILD)? Up 15% year-to-date. Turns out, their COVID-19 treatment, Remdesivir, is back in vogue like bell-bottom jeans. And their HIV and hepatitis C drugs? They're still growing stronger.

But the real rock star of biotech? That'd be Regeneron Pharmaceuticals (REGN). These guys are up over 30% year-to-date. They're treating everything from eye diseases to cancer to inflammation.

Vertex Pharmaceuticals (VRTX) is another one to watch. Up 12% this year, they've got the cystic fibrosis market cornered. And they're not stopping there – they're expanding faster thanks to their collaboration with the likes of Crispr Therapeutics (CRSP).

Now that I’ve mentioned gene therapy, I know you're wondering about Moderna (MRNA). After all, weren’t they the darlings of the COVID era? Well, yes and no.

Their stock's down about 35% year-to-date, but don't count them out just yet. Their mRNA technology is hotter than a jalapeño popper fresh out of the fryer. They might be down, but they're definitely not out.

So, what's the takeaway here? I suggest you keep your eyes peeled on the biotechnology and healthcare sectors. After all, in this market, the best offense might just be a good defense – and what's more defensive than betting on the sector that keeps us all alive and kicking?

Mad Hedge Biotech and Healthcare Letter

July 11, 2024

Fiat Lux

Featured Trade:

(FORGET THE CASINO, INVEST IN THE HOUSE)

(TMO), (BIO), (DHR), (A)

I've always had a soft spot for healthcare innovation. But let me tell you, picking winners in this sector is trickier than trying to nail jello to a wall. You've got regulatory hurdles, fierce competition, and funding risks that'd make a Vegas bookie sweat.

That's why I'm a big fan of buying the arms dealers in this war on disease. I'm talking about the suppliers. These companies are calmly sitting pretty, ready to cash in on the general need for innovation without getting their hands too dirty.

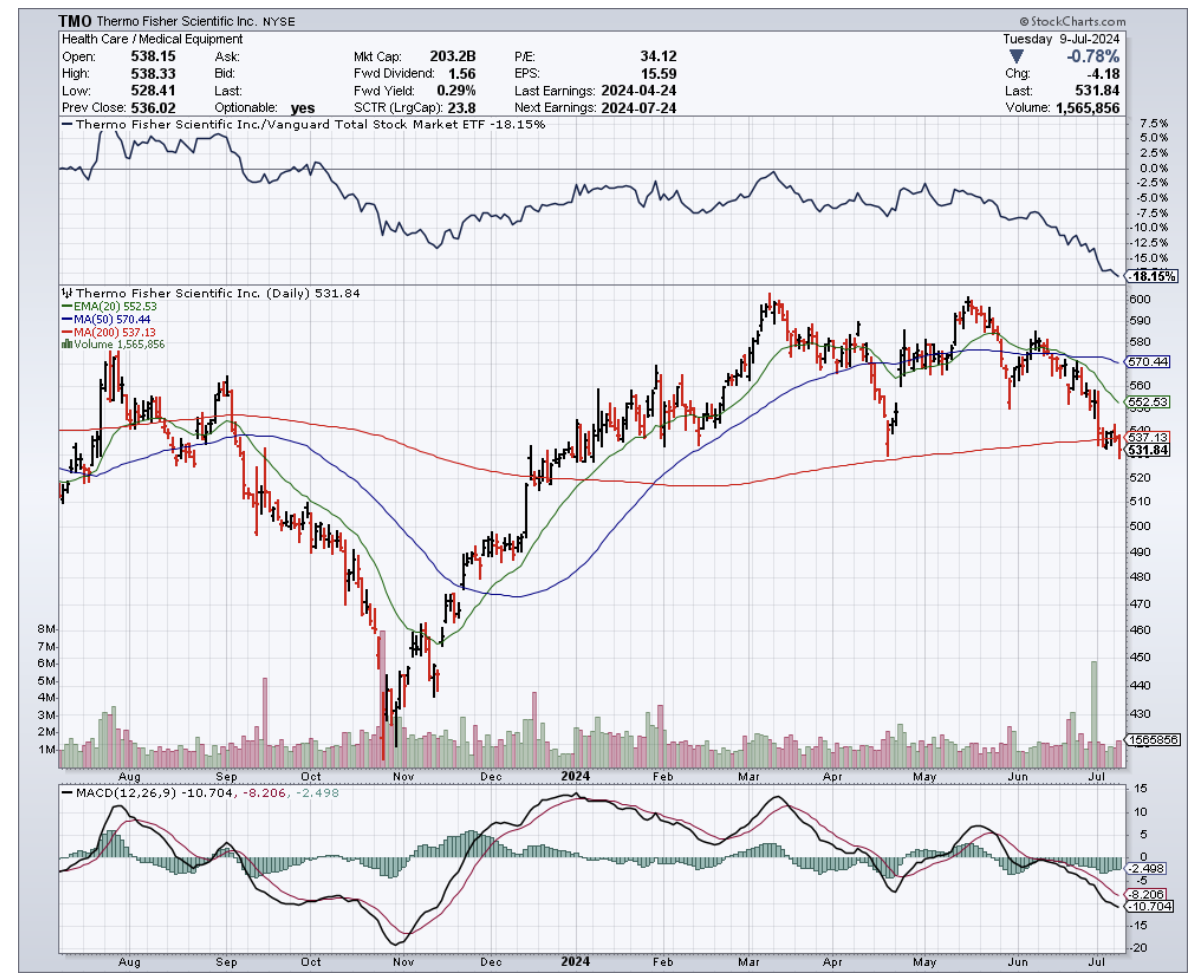

Enter Thermo Fisher Scientific (TMO), the Waltham, MA-based behemoth that's supplying everyone from big pharma to your local hospital. They're slinging lab equipment faster than a short-order cook at a greasy spoon, and business is booming.

Just look at the numbers. Over the past decade, TMO's delivered a 400% total return. That's not just beating the S&P 500 – it's leaving it in the dust by 170 points.

And recently, Thermo Fisher just got the green light from those sticklers at the UK antitrust office to close a $3.1 billion deal for Olink, a Swedish outfit that's cooking up some serious magic in protein analysis.

We're talking about technology that can analyze hundreds of proteins faster than you can say "proteomics."

Speaking of proteomics, for those of you who slept through biology class, it's the study of proteins in biological systems. These little buggers are the muscle behind everything your body does.

While DNA is the blueprint, proteins are the construction crew that brings that blueprint to life. Figuring out how these microscopic workers operate is the golden ticket to a treasure trove of new drugs and therapies.

It's a growing field, with the global market expected to explode from $32.8 billion in 2023 to a whopping $161.9 billion by 2035. That translates to a compound annual growth rate of 14.2%.

As expected, Thermo Fisher isn't the only player in this game. You've got heavyweights like Bio-Rad Laboratories (BIO), Danaher Corporation (DHR), and Agilent Technologies (A) all jockeying for the top position.

But thanks to this recent Olink acquisition, Thermo Fisher's looking to pull ahead like a thoroughbred at the Kentucky Derby.

For better context, let's break down what this means for TMO's bottom line. Their mass spectrometry business, already a cash cow, could see a 5% bump in market share.

We're talking about an extra $475 million in revenue by 2028, with profit margins that'd make a hedge fund manager blush.

And that's just the tip of the iceberg. Their protein assays and kits business could see a 10% boost in market share, translating to another $450 million in revenue.

Despite these, Thermo Fisher isn't resting on its laurels. They're also partnering up with the likes of Bayer (BAYRY) to develop next-generation sequencing tools.

Next, let's talk dividends. I know, I know, a 0.3% yield isn't going to have you popping champagne. That's barely enough for a value meal at McDonald's. But don't let that fool you.

This company's been growing its dividend faster than a beanstalk on Miracle-Gro, with a five-year CAGR of 15.5%. It's not TMO's fault their stock price keeps outrunning their dividend.

Looking ahead, Thermo Fisher is projected to reach a 12% EPS growth in 2025 and 11% in 2026. It's like watching a rocket take off in slow motion.

Before you jump aboard though, I'll be honest with you.

At a P/E ratio of 26.6x, TMO isn't exactly on the bargain rack. It's priced like a fine wine, not a box of Franzia. But hey, quality costs money, and this is a company that's been delivering returns of 16.7% per year since 2004.

So, what's the takeaway here? Well, it’s clear that Thermo Fisher Scientific is a powerhouse in the healthcare and biotech sectors.

But, it's not going to give you the cheap thrills of a biotech startup that might cure cancer or go belly-up next week.

Instead, it's the steady Eddie that's going to keep chugging along, supplying the tools that make those moonshots possible.

If you're looking for income, well, this ain't your horse. But if you want growth with a side of stability, Thermo Fisher might just be the ticket. It's got more potential than a kid with a 4.0 GPA and a mean fastball.

Mad Hedge Bitcoin Letter

October 14, 2021

Fiat Lux

Featured Trade:

(WHAT’S NEW IN BIOTECH)

(CGTX), (BIIB), (LLY), (ABBV), (NVS), (TAK), (PYXS), (PFE),

(AZN), (GILD), (GSK), (IMGN), (ISO), (TMO), (BIO)

As the biotechnology world is ever-evolving, with several companies going public every few months, let me share some of the most promising names that recently emerged.

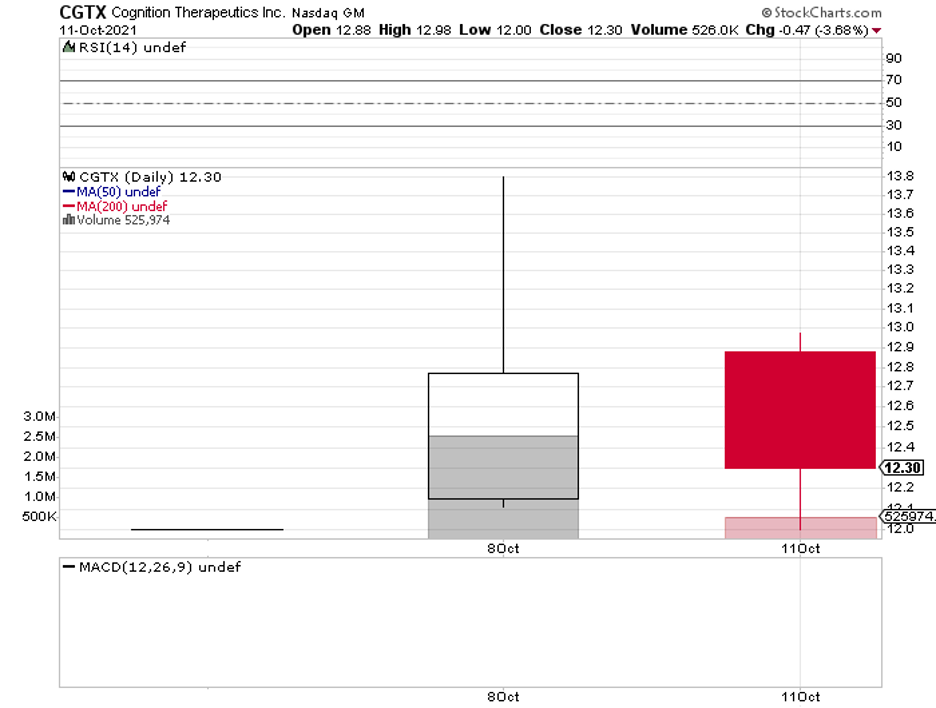

The first is Cognition Therapeutics (CGTX), a company working on treatments for Alzheimer’s disease and macular degeneration.

Its most promising candidate is an Alzheimer’s treatment called CT1812, which is currently under Phase 2 trials. Looking at the timeline, CGTX expects to release topline data by 2023.

With the expected growth of the aging population, focusing on treating various forms of Alzheimer’s is a promising direction for Cognition Therapeutics.

In fact, the global market for this neurodegenerative disease is projected to grow from $2.9 billion in 2018 to a whopping $10.5 billion by 2025.

So far, the major competitors of Cognition Therapeutics in this area include Biogen (BIIB), Eli Lilly (LLY), AbbVie (ABBV), Novartis (NVS), and Takeda (TAK).

The second promising biotech company is Pyxis Oncology (PYXS), which is a spinoff from Pfizer (PFE).

Pyxis is focused on developing next-generation treatments targeting difficult-to-treat types of cancer.

Basically, the company’s goal is to create therapies that can directly kill tumor cells. It also wants to get rid of the underlying problems that lead to the uncontrollable spread of tumors and the weakening of the immune system.

To do this, Pyxis has come up with novel antibody drug conjugate (ACT) candidates and other monoclonal antibody (mAb) pipelines.

Its lead candidate is called ADC PYX-201, a potential treatment for non-small cell lung cancer and breast cancer.

The goal of ADC PYX-201 is to target actively multiplying tumors while boosting the immune response of the patient’s body. Pyxis plans to submit it as a non-small cell lung cancer treatment candidate by mid-2022.

If approved, then ADC PYX-201 will be under patent protection until 2037.

This holds great potential for Pyxis’ cashflow, as the market for non-small cell lung cancer worldwide is anticipated to rise from $6.2 billion in 2016 to over $12 billion by 2025.

With this potential of ADC treatments, Pyxis can expect competition from the likes of AstraZeneca (AZN), Gilead Sciences (GILD), GlaxoSmithKline (GSK), and ImmunoGen (IMGN).

The last name on today’s list is IsoPlexis Corporation (ISO).

This company is the first to focus on dynamic proteomics and single-cell biology in an effort to develop “walk-away automation” products that aid in shortening the therapeutic development timelines by acquiring “multiplexed proteomics with very low sample volumes that reflect in vivo biology to clarify lead candidates.”

In layman’s terms, IsoPlexis is working on a technology that aims to identify every protein in the body to speed up the development of new therapies for rare diseases.

This is a lucrative business, with IsoPlexis targeting at least $34 billion in the total addressable market.

Considering that IsoPlexis is a pioneer in this field, it is possible for it to gain the lion’s share of the segment and position itself as an undisputed leader for years.

More importantly, IsoPlexis can use its patented technology, “Proteomic Barcoded,” to expand the use cases to cover other lucrative markets.

For example, IsoPlexis can apply its technology to cancer immunology and targeted oncology by predicting the progression of cancer cells in the body.

Adding cell therapies to the company’s pipeline is also a very realistic possibility since its technology can be utilized to create CAR-T cell therapies as well.

In fact, IsoPlexis’ approach is already being used in developing treatments for leukemia and melanoma.

Another profitable avenue for IsoPlexis’ technology is the vaccines sector.

Since the development of vaccines requires profiling the responses of the respiratory and immune systems, the company’s data would accelerate the entire process.

So far, the major rivals of IsoPlexis in this space include Thermo Fisher Scientific (TMO) and Bio Rad Laboratories (BIO).

While all these biotech companies offer promising products and technologies, they’re all still in the early stages of development.

This makes them high-risk investments and are likely suitable for those who are willing to invest in the long term.

For those who want to see movement faster and sooner, it might be best to watch these stocks from the sidelines.

Mad Hedge Biotech & Healthcare Letter

January 7, 2020

Fiat Lux

Featured Trade:

(WHAT’S NEXT IN THE BIOTECH PIPELINE?)

(ITCI), (AIMT), (BIO), (JNJ)

Investing in biotech stocks demands prudence combined with a sprinkling of optimism. This means taking in announcements from companies bragging about potential blockbuster drugs with a grain of salt.

After all, a single misstep towards gaining FDA approval could easily set back any progress, erase any hope of salvaging the discovery, and eventually, send their share prices spiraling down.

On the other hand, choosing a biotech stock that would deliver on its promise means reaping rich dividends in the future.

With all the developments in store though, it’s hard to see why 2020 can’t easily go down as The Year of Biotech. Here are some things that caught my eye.

Christmas came early for Intra-Cellular Therapies (ITCI) as its long-awaited schizophrenia drug, Caplyta, received the green light from the FDA.

Although it has taken a few years for the biotech firm to announce the results of its schizophrenia trials, its investors are confident that Calpyta’s journey from this highly sought approval to marketing will be smooth sailing.

While the number of people suffering from schizophrenia and bipolar disorder is not as many as those facing major depressive disorder, treatments for the former conditions remain lacking. In fact, health specialists have been looking for more convenient options -- one that won’t hinder the daily lives of patients taking it.

This blockbuster drug, pegged as a safer and better alternative to Johnson and Johnson’s (JNJ) Risperidone, is expected to expand Lumateperone’s reach in the mental health market.

Despite earning an early victory, ITCI is already gearing up to tweak Calpyta’s indications and seek bipolar depression approvals as well. At the moment, this schizophrenia drug is estimated to cross $1 billion in sales following its 2020 launch in the market.

Meanwhile, there’s another big market drug that’s projected to make a major launch in 2020. Aimmune Therapeutics’ (AIMT) AR101. Otherwise known Palforzia, this will be the first-ever treatment for peanut allergies.

Although there’s no price tag released yet, a year’s supply of Palforzia is estimated to cost $4,200 per patient.

These pull-apart capsules, which are basically comprised of unmodified peanut flour plus a bunch of inactive ingredients, aim to provide medication for a food allergy that affects one in 13 children today.

The FDA is expected to release its decision on Palforzia sometime in January 2020, so it’ll definitely be a prosperous New Year for its investors.

Another biotech company that’s set to make a splash in a lucrative market is Bluebird Bio (BIO).

At the moment, investors are chomping at the bit for good news concerning the company’s future crown jewel: genetic blood disease treatment Zynteglo.

In 2019, Zynteglo gained approval in the European market. Now, Bluebird is setting its sights to also conquer the US market as one in every 100,000 people is afflicted by this rare condition.

More than that, the only approved therapy for this genetic blood ailment is a blood transfusion done regularly.

Given the rarity of the disease and the efficacy of the treatment, Zynteglo’s price tag will obviously be on the high end.

This therapy is expected to cost roughly $1.8 million in total for every patient. To ease the burden though, Bluebird shared that it’s open to four- and five-year installment plans. That puts every gene therapy infusion at $355,000 per session.

Despite this massive expense, Bluebird actually believes that it’s selling its treatment at a discount of about 15% compared to the actual market value of $2.1 million.

This conviction comes from the fact that the company estimates adding 22 quality-adjusted life years to the lives of every successfully treated patient.

All three biotech stocks could easily skyrocket, especially Bluebird Bio. As for Aimmune Therapeutics, the company is currently financially healthy so it shouldn’t encounter any trouble meeting obligations. Meanwhile, ITCI has been gifting its investors with early Christmas presents since it first released promising results of its schizophrenia study.