Mad Hedge Technology Letter

August 9, 2024

Fiat Lux

Featured Trade:

(WARNING SIGNS LITTER THE TECH NARRATIVE)

(ABNB), (BKNG), (EXPE)

Mad Hedge Technology Letter

August 9, 2024

Fiat Lux

Featured Trade:

(WARNING SIGNS LITTER THE TECH NARRATIVE)

(ABNB), (BKNG), (EXPE)

It was early.

The real recession doesn’t kick into gear for another quarter or so.

This was just a quick fake-out.

The bond market freaking out and pricing in 1.25% Fed Funds’ cuts was a generous gift to tech stocks.

Why do I say that?

It is a dip in which we can get into tech prices at cheaper prices – probably the last time before the U.S. election.

We are starting to receive confirmation from many earnings reports that the consumer is starting to get cold feet.

The pullback in consumer strength runs the whole gamut from home improvement to restaurant eating.

I cover tech and the weakness is multi-pronged stemming from hardware to software.

The latest to ring the alarm about sluggish consumer spending was the digital accommodation platform Airbnb (ABNB).

Airbnb earned sales of $2.7 billion for the same quarter last year and now they have told investors that for next year they plan to target $2.5 billion of sales.

The culprit blamed by Airbnb management is the American consumer.

Americans are shortening their Airbnb stays and soon they could be sacrificing Airbnb altogether. Although we aren’t at that point yet, US consumers simply can’t stomach this new wave of price increases for the cost of living, and reigning back discretionary travel is this logical item to shave from the budget.

The second quarter continued a trend of decelerating bookings growth for Airbnb. The total value of all bookings through Airbnb grew 11% year over year to $21.2 billion for the three-month period. That's down from 12% booking growth in Q1, 15% growth in the final quarter of 2023, and 17% growth in September-ended third quarter of 2023.

In 2022 and 2023, Airbnb, Booking Holdings (BKNG), and Expedia Group (EXPE) benefited from a bounce-back in travel after the harsh lockdowns prevented many types of travel in 2020 and into 2021. So-called revenge travel powered strong sales growth for the companies. But the picture appears to be shifting.

It is hard to see the US consumer just bouncing back with a V-shaped trajectory and that could affect Airbnb sales.

Reports out of high costs states like Washington and New York peg $150,000 per year in income as “lower middle class.”

There has also been a huge migration shift from wealth moving out of blue states to red states in the hope of maintaining purchasing power through these high inflation times.

The fact of the matter is that $35 trillion in Federal debt is the most important topic for this upcoming U.S. President Election, but this topic has been completely sidelined from the national discourse.

This surely means higher debt down the road and a further deterioration in the US consumer profile.

Tech companies with large moats around their business models will get through these times, but for Airbnb, they don’t have this type of moat because consumers don’t necessarily need to travel. Consumers do need to eat, sleep, and drive a car to work.

They can simply just delay travel for a few years before they reload financially.

It is high time to unload stocks like Airbnb even if they are leaders in the home-sharing sub-sector in tech.

Airbnb shares are down around 32% in the past few months highlighting the need for overly expensive tech stocks to adjust to the new reality.

I do believe there is another leg down in shares before an optimal window to buy on the dip presents itself, but that appears to be around $90-$100 per share.

Global Market Comments

June 3, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE MALLARD MARKET and ME AND 23 AND ME),

(AAPL), (GOOGL), (AMZN), (TSLA), (MSFT), (META), (AVGO), (LRCX), (SMCI), (NVR), (BKNG), (LLY), (NFLX), (VIX), (COPX), (T), (NVDA), (LEN), (KBH)

There’s nothing like the comfort and self-satisfaction of having a 100% cash position in a falling market. While everyone else is bleeding red ink, I am happily plotting my next trades.

Of course, the rest of the market isn’t really bleeding red ink, just giving up windfall profits. Still, it’s better to trade from a position of strength than weakness. It makes identifying the next winners easier.

Think of this as the “Mallard Market”. On the surface, it seems calm and peaceful, while underwater, it is paddling along like crazy. The damage has been unmistakable. Dell, the faux AI stock (DELL) crashed by 28%, Salesforce (CRM) got creamed for 34%, and ServiceNow (NOW) got taken to the woodshed for 22%.

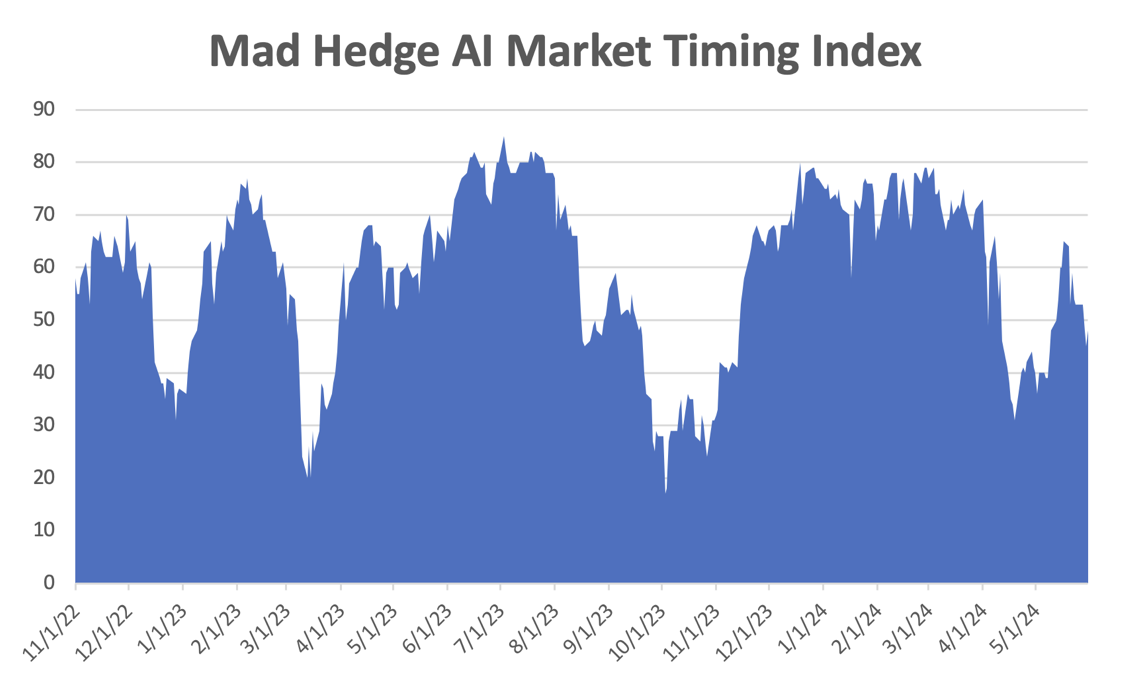

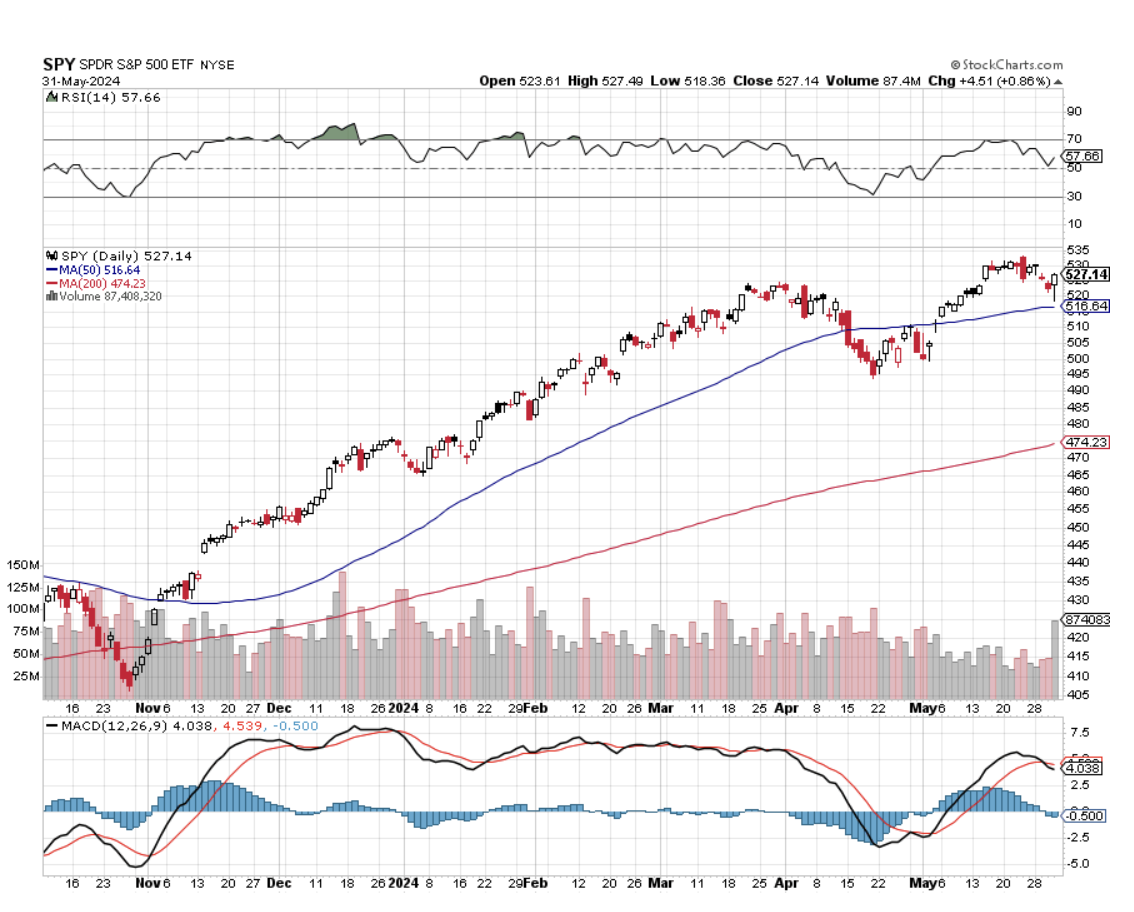

It all belies a market that is incredibly nervous and fast on the trigger. The tolerance for any bad news is zero. Yet there has been no market crash as I expected. The 5,300 level for the (SPX) seems to possess a gravitational field, powered by $250 earnings per share and a multiple of 51X.

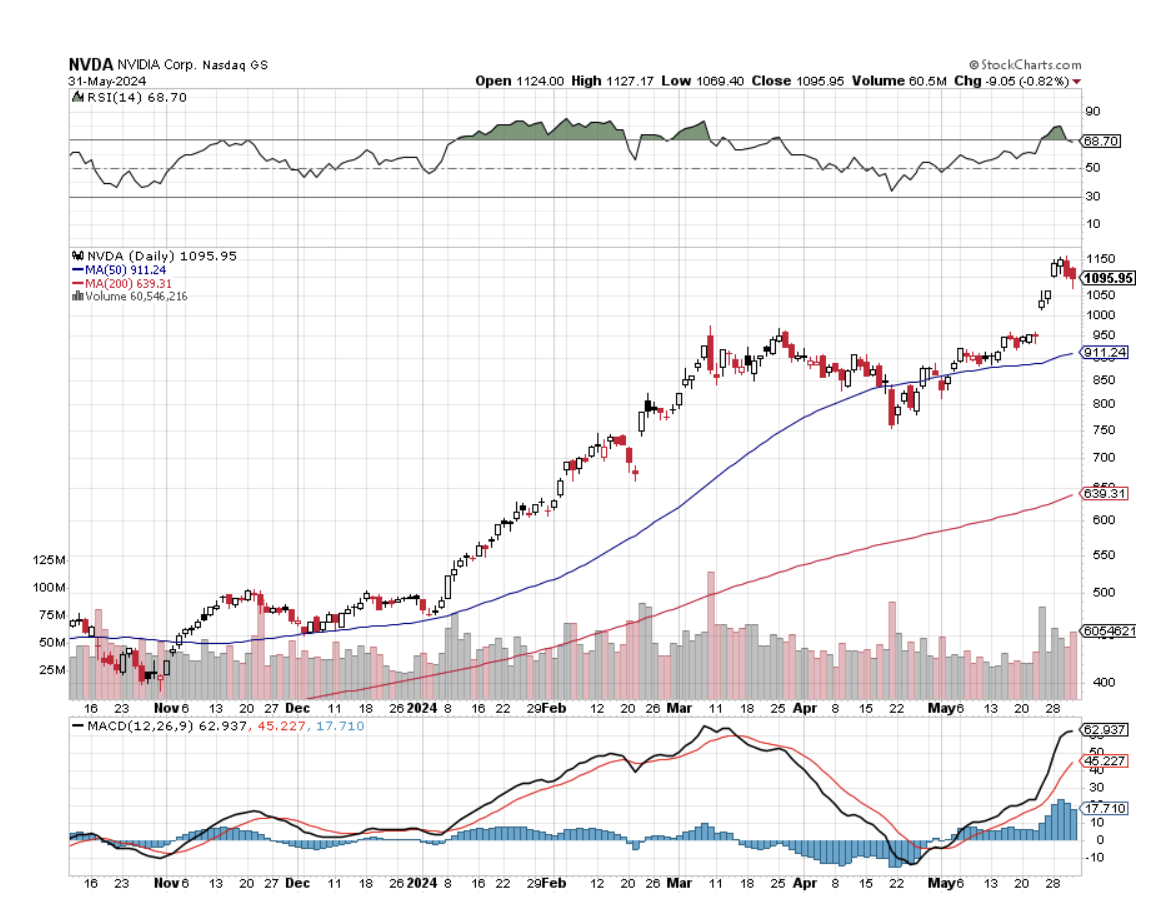

It was NVIDIA that put the writing on the wall by announcing a 10:1 split that has opened the floodgates for similar prosperous and high-priced companies.

There are now 36 stocks with share prices of $500 or more ripe for splits with $7 trillion in market cap, or 16% of the total market. While splits don’t change the value of a company, perceptions are everything, as they prove shareholder-friendly policies. While individual investors are confused by an onslaught of contradictory research recommendations, splits are a great “tell” on what to buy next.

Apple (AAPL), Alphabet (GOOGL), Amazon (AMZN), and Tesla (TSLA) have already carried out splits, some multiple times, to great success. Of the Magnificent Seven, only Microsoft (MSFT) and Meta (META) have yet to split.

In the tech area Broadcom (AVGO), Lam Research (LRCX), Super Micro Computer (SMCI), and Service Now (NOW) have yet to split. In the non-tech area, there are NVR Inc. (NVR), Booking Holdings (BKNG), Eli Lilly (LLY), and Netflix (NFLX). Many of these are well-known Mad Hedge recommended stocks.

History has shown that stocks rise 25% one year after a split compared to 12% for the market as a whole. A stock’s addition to the Dow Average or the S&P 500 (SPY) provides a boost. If both occur, stocks will absolutely explode. Stock splits are also much more attractive than buybacks at these high prices.

So, I’ll be trolling the market for split-happy candidates.

You should too.

Since it may be some time before we capitulate and take a worthwhile run at new highs, I thought I’d update you on the global demographic outlook, which is always a long-term driver of economies and markets.

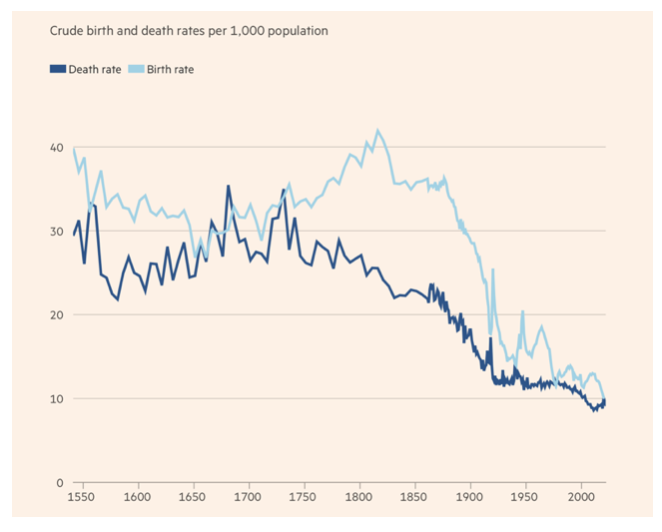

People are now living longer than ever before. But postponing death is only a part of the demographic story. The other is the decline in births. The combination of the two is creating huge changes in the global economy.

The notion of a “demographic transition” is almost a century old. Human societies used to have roughly stable populations, with high mortality matched by high fertility. Families had eight kids and 3-5 usually died in childhood, barely maintaining population growth.

In England and Wales in the 18th and 19th centuries, death rates suddenly plummeted. But fertility did not. The result was a population explosion. As the benefits of economic growth and advances in medicine and public health spread, most of the world has followed a similar transition, but far faster. As a result, human numbers rose fourfold over the last hundred years, from 2 billion to 8 billion.

In time, fertility followed mortality on a downward path across most of the world. As a result, fertility rates in more than half of all countries and territories in 2021 fell below the replacement level. For the world as a whole, the fertility rate was 2.3 in 2021, barely above the replacement of 2.1, down from 4.7 in 1960.

For high-income countries, the fertility rate was a mere 1.6, down from 3.0 in 1960. In general, poor countries still have higher fertility rates than richer ones, but they have been falling there, too.

What explains this collapse in fertility rates? An important part of the answer is the wonderful surprise that more children survived than expected. So, people started to practice various forms of birth control.

But the desire to have many children also shrank sharply. When husbands realized that smaller families meant high standards of living for themselves, family sizes dropped sharply. Even in ultra-conservative Iran, the fertility rate has collapsed from 6.6 in 1980 to only 1.7 in 2021.

A big reason for this shift was that, for their parents, children have moved from being a valuable productive asset in the 19th century to an expensive luxury today. That was back when 50% of our population worked on farms. Today it’s only 2%.

In the meantime, female participation in the economy rose dramatically in the 20th century, including in highly skilled careers. That raised the “opportunity cost” of producing children, especially for mothers. So, they have children later, or even not at all.

Where public childcare is more generous women are encouraged to combine careers with having children. The absence of such help helps explain the exceptionally low fertility rates in much of East Asia and Southern Europe, where parental support is limited.

This global shift towards very low fertility, with the exception (so far) of sub-Saharan Africa, is among the most important events driving the global economy. One implication is that the population of Africa is forecast to be larger than that of all today’s high-income countries, plus China by 2060, thanks to the elimination of many diseases there.

Why is all this important?

Because rising populations create larger markets, more profits for corporations, and rising share prices. Shrinking populations have the opposite effect, as China is learning about its distress now. One reason the US is growing faster than the rest of the world is that a continuous stream of new immigrants since its foundation has created endless numbers of new workers and customers. Dow 240,000 here we come!

Just thought you’d like to know.

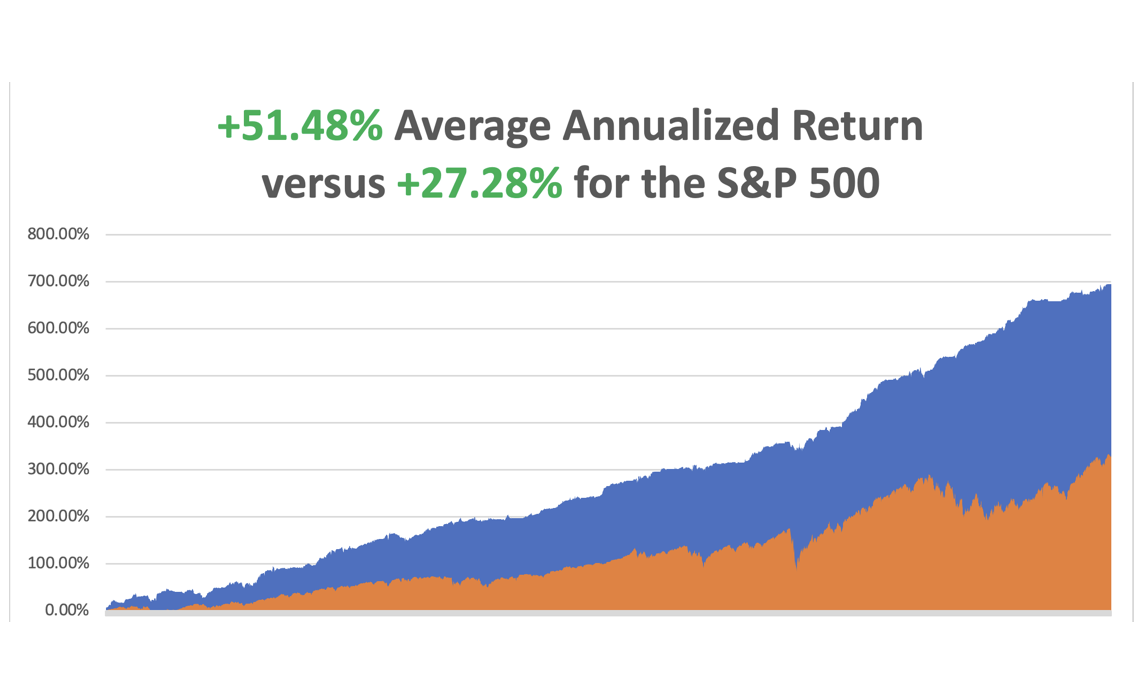

So far in May, we are up +3.74%. My 2024 year-to-date performance is at +18.35%. The S&P 500 (SPY) is up +10.48% so far in 2024. My trailing one-year return reached +35.74%.

That brings my 16-year total return to +694.78%. My average annualized return has recovered to +51.48%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I bailed on my last position early in the week, covering a short in Apple for a profit.

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

The Fed’s Favorite Inflation Gauge Cools by 0.2% in April, with the PCE, or the Personal Consumer Inflation Expectations Price Index. This one strips out the volatile food and energy components. It gives more credibility to a September rate cut and gave bonds a good day.

NVIDIA Shares Continues to Go Ballistic, creating another $800 billion in market capitalization in three trading days. That is the most in history. That took NASDAQ to a new all-time high at 17,000. At $2.8 trillion (NVDA) could become the largest publicly traded company in the world in another day. Today’s tailwind came from an Elon Musk comment that his new xAI start-up would buy the company's high-end H100 graphics cards. Buy (NVDA) on the next 20% dip.

Pending Home Sales Dive, down 7.7% in April, the worst since the Covid market three years ago. The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market. But the anticipated rate cuts later this year should lead to better conditions, with improved affordability and more supply. Buy (LEN) and (KBH) on dips.

Money Supply Rises for the First Time in More than a Year. Remember money supply? As measured by M2, it sums up the currency, coins, and savings deposits held by banks, balances in retail money-market funds, and more. Data for April released on Tuesday afternoon showed an increase of 0.6% from a year ago. The Fed balance sheet has shrunk by $1.5 trillion in two years, the fastest decline in history, slowing the economy.

AT&T’s (T) Copper is Worth More Than the Company, and with plans to convert half its copper network to fiber by 2025 could free up billions of tons of the red metal to sell on the market. Copper prices have doubled over the past two years, and they could double again by next year. Worldwide there are 7 trillion tons of copper wire in place. Fiber is cheaper and exponentially more efficient than copper, which is facing huge demands from AI, EVs, and the electrification of the grid. Buy copper (COPX) on dips.

Markets are Underpricing Low Volatility (VIX), not a good thing at all-time highs. Volatility across equity and currency markets is low. The Volatility Index (VIX) at $12.46 compares with an average over five years of $21.5 and over the longer term of $19.9. Markets are heavily discounting good news and a disinflationary environment. It is not only stocks. There is also low volatility across currency markets. The DB index of foreign exchange volatility is at $6.3 versus an average of $7.6 over five years and $9.3 over the longer term. This will end in tears.

S&P Case Shiller Jumps to New All-Time High, with its National Home Price Index. The index rose by 1.29%, the fastest growth since April 2023. All 20 major metro cities were up last month and gained 6.5% YOY. Four cities are currently at all-time highs: San Diego, Los Angeles, Washington, D.C., and New York. Prices in San Diego saw the biggest gain, up 11.4% from February of 2023. Both Chicago and Detroit reported 8.9% annual increases. Portland, Oregon, saw the smallest gain in the index of just 2.2%. Unaffordability is the big story in the market right now. The sunbelt is seeing the most weakness, thanks to a post-pandemic construction boom.

Space X’s Starlink Tops 3 million Subscribers, and is rapidly moving towards a global WiFi network. I set up a dozen of these in Ukraine last October and even the Russians couldn’t hack them. It sets a global 200 Mb standard usable in most countries, even the remote Galapagos Islands in the Pacific. It’s only a VC investment now but could become Elon Musk’s next trillion-dollar company.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 3, the ISM Manufacturing PMI is released.

On Tuesday, June 4 at 7:00 AM, the JOLTS Job Openings Report will be published.

On Wednesday, June 5 at 7:00 AM, the ISM Services PMI is published.

On Thursday, June 6 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Challenger Job Cuts Report.

On Friday, June 7 at 8:30 AM, the Nonfarm Payroll and headline Unemployment Rate are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when Anne Wojcicki founded 23andMe in 2007, I was not surprised. As a DNA sequencing pioneer at UCLA, I had been expecting it for 35 years. It just came 70 years sooner than I expected.

For a mere $99 back then they could analyze your DNA, learn your family history, and be apprised of your genetic medical risks. But there were also risks. Some early customers learned that their father wasn’t their real father, learned of unknown brothers and sisters, that they had over 100 brothers and sisters (gotta love that Berkeley water polo team!), and other dark family secrets.

So, when someone finally gave me a kit as a birthday present, I proceeded with some foreboding. My mother spent 40 years tracing our family back 1,000 years all the way back to the 1086 English Domesday Book (click here)

I thought it would be interesting to learn how much was actually fact and how much fiction. Suffice it to say that while many questions were answered, alarming new ones were raised.

It turns out that I am descended from a man who lived in Africa 275,000 years ago. I have 311 genes that came from a Neanderthal. I am descended from a woman who lived in the Caucuses 30,000 years ago, which became the foundation of the European race.

I am 13.7% French and German, 13.4% British and Irish, and 1.4% North African (the Moors occupied Sicily for 200 years). Oh, and I am 50% less likely to be a vegetarian (I grew up on a cattle ranch).

I am related to King Louis XVI of France, who was beheaded during the French Revolution, thus explaining my love of Bordeaux wines, women wearing vintage Channel dresses, and pate foie gras.

Although both my grandparents were Italian, making me 50% Italian, I learned there is no such thing as pure Italian. I come out only 40.7% Italian. That’s because a DNA test captures not only my Italian roots, plus everyone who has invaded Italy over the past 250,000 years, which is pretty much everyone.

The real question arose over my native American roots. I am one-sixteenth Cherokee Indian according to family lore, so my DNA reading should have come in at 6.25%. Instead, it showed only 3.25% and that launched a prolonged and determined search.

I discovered that my French ancestors in Carondelet, MO, now a suburb of Saint Louis, learned of rich farmland and easy pickings of gold in California and joined a wagon train headed there in 1866. The train was massacred in Kansas. The adults were all killed, and the young children were adopted into the tribe, including my great X 5 Grandfather Alf Carlat and his brother, then aged four and five.

When the Indian Wars ended in the 1880s, all captives were returned. Alf was taken in by a missionary and sent to an eastern seminary to become a minister. He then returned to the Cherokees to convert them to Christianity. By then, Alf was in his late twenties so he married a Cherokee woman, baptized her, and gave her the name of Minto, as was the practice of the day.

After a great effort, my mother found a picture of Alf & Minto Carlat taken shortly after. You can see that Alf is wearing a tie pin with the letter “C” for his last name Carlat. We puzzled over the picture for decades. Was Minto French or Cherokee? You can decide for yourself.

Then 23andMe delivered the answer. Aha! She was both French and Cherokee, descended from a mountain man who roamed the western wilderness in the 1840s. That is what diluted my own Cherokee DNA from 6.50% to 3.25%. And thus, the mystery was solved.

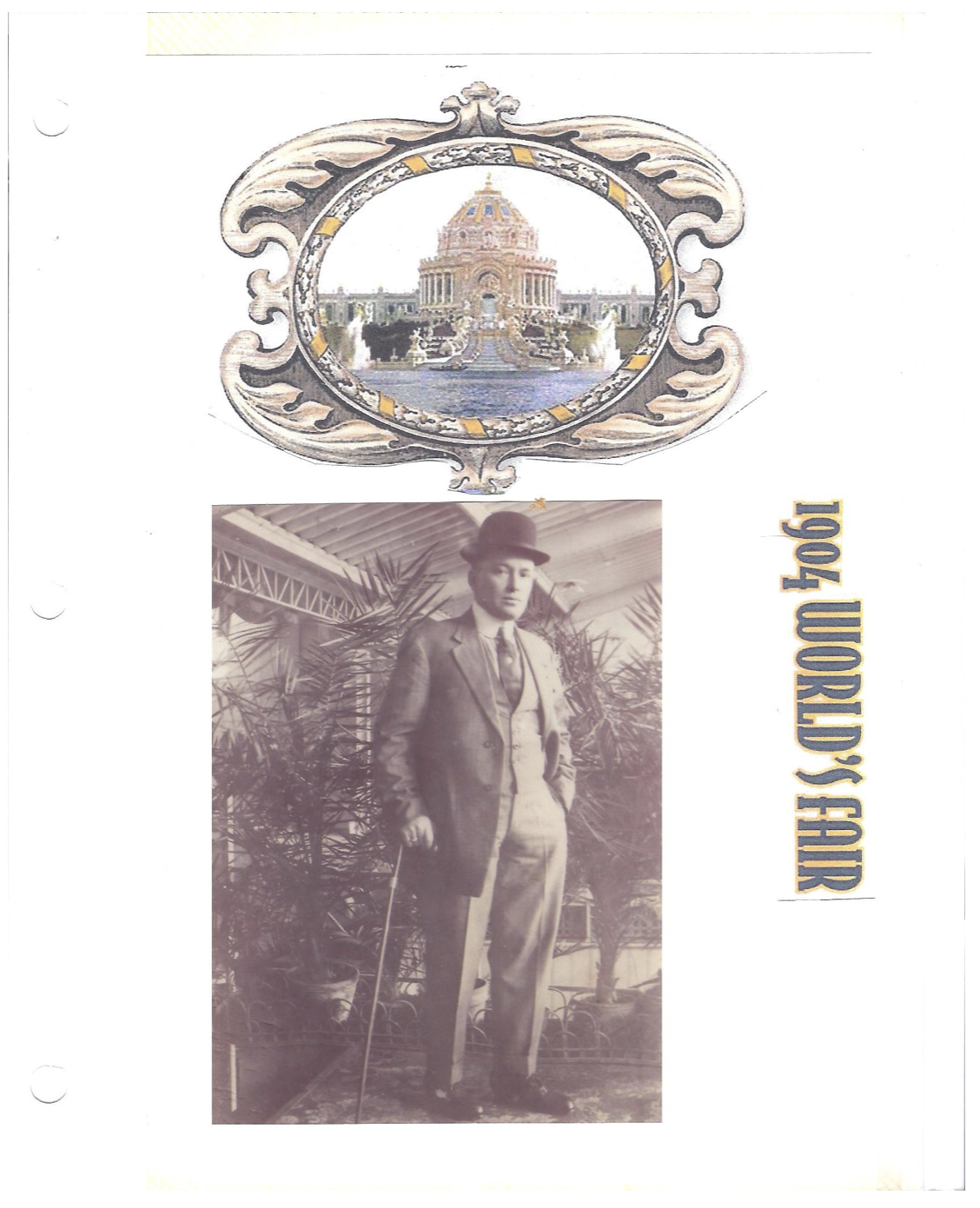

The story has a happy ending. During the 1904 World’s Fair in St. Louis (of Meet Me in St. Louis fame), Alf, then 46, placed an ad in the newspaper looking for anyone missing a brother from the 1866 Kansas massacre. He ran the ad for three months and on the very last day, his brother answered and the two were reunited, both families in tow.

Today, getting your DNA analyzed starts from $119, but with a much larger database, it is far more thorough. To do so, click here.

My DNA Has Gotten Around

It All Started in East Africa

1880 Alf & Minto Carlat, Great X 5 Grandparents

The Long-Lost Brother

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

November 2, 2022

Fiat Lux

Featured Trade:

(POOR OUTLOOK FOR TRAVEL TECH)

(ABNB), (BKNG), (EXPE)

The big sell-off in Airbnb (ABNB) this morning was not about the great quarter it just had, but what investors have guessed the company faces in 2023.

Prospects look weak next year.

The re-opening and revenge travel surge came through in such a way that growth was brought forward at a blistering rate.

The number's back up my thesis, with ABNBs revenue expanding by 29% or $2.9 billion, ahead of expectations at $2.84 billion.

On the bottom line, earnings per share jumped 47% to $1.79, breezing past the consensus at $1.47.

Yet the stock is down 9% in this morning’s trading, with a textbook “buy the rumor and sell the news” type of price action.

The US is barreling towards a recession in 2023, although the job numbers have stayed extremely resilient in the face of rate hikes.

If jobs can muscle through these next rate rises, then I do believe that a recession can be put off until 2024.

However, it will take time for the market to reflect the new realities and until then, ABNB is poised for a slowdown.

What do I mean by a slowdown?

The company forecasts around a 17% increase in sales which severely underperforms the 29% they registered last quarter.

While the forecast is not something to freak out about, investors are taking profits today and rotating capital elsewhere that isn’t growth.

Unless there is another forced lockdown, I don’t see ABNB beating the 29% expansion in revenue in the near future.

While sales won’t drop off a cliff next year, I don’t see how they get back to the 30% sales growth until we get to the other side of the recession which could be somewhere around 2024.

The downgrade in forecast in the travel industry was consensus.

At the individual level, the astronomical price rises for travel and leisure will have to abate somewhat to attract the incremental customer from now.

Most people have budgets, and they saved for 2 years to blow it all on a summer to remember (or forget).

Competitors such as Booking Holdings (BKNG) and Expedia (EXPE) have yet to report third-quarter earnings, and their guidance should be informative for overall travel trends. The two leading online travel agencies are likely to forecast a similar deceleration into the fourth quarter.

As the travel market evolves, Airbnb will continue to outperform because it’s a monopoly in the home-sharing business and other firms like booking.com don’t come close.

I would definitely classify ABNB as a solid long-term investment and to add on big down days.

Unfortunately, ABNB's core business is being overshadowed by the macro picture these days, which is highly negative for technology stocks.

The silver linings are there, as the business model has also turned from a net loss-making model to a nice profit machine this year.

Even if profits are under $1 billion per year, they were bleeding money just a few years ago as they worked to improve the unit economics in this unique industry.

The 17% increase next year will turn out to be a blip on the radar long term and I believe that once we get over the hump and interest rates start trending down, ABNB will be one stock that will shoot from the bottom left to the upper right.

Mad Hedge Technology Letter

December 13, 2021

Fiat Lux

Featured Trade:

(THE POTENTIAL NORMALIZATION OF 2022)

(ABNB), (BKNG), (ZM)

The last 2 years haven’t been a walk in the park for tech traders.

Before March 2020, the bull market and the trading patterns that followed were largely predictable.

Sure, there were our run-of-the-mill selloffs, but nothing like the Covid selloff of 2020.

Then the ensuing reversal that took us to new highs was a sugar high Fed-induced bounce that we are still buoying from, and that boost is largely wearing off.

As we near the end of 2021, it’s hard to believe that it’s been almost 2 years since the daily trading headline became a health care-driven headline.

There is the growing consensus that in the latter part of 2022, a synchronized global recovery story will emerge as the strongest plausible scenario.

This means that day-to-day business conditions which include international travel could revert back to what we had prior to March 2020 or a competing version of it.

I won’t get into the vaccine semantics of it, but a moderate health solution is only positive for tech stocks.

The “shelter at home” tech trade of 2020 was a one-off drawn-out event, and with normalization around the corner, we will return to the catalysts that originally drove tech shares — earnings growth, revenue growth, and financial engineering.

The lingering effects of this latest variant could start to wind down by early spring which will give way to the world of higher interest rates and costlier financing, but higher interest rates solving the inflation crisis.

Naturally, many things could side-swipe this scenario like another covid variant deadlier than the ones spreading around now.

If there is some iteration of normalization involved next year, a tech stock that will squarely harvest the gains from its strategic position at the intersection of the internet and remote working is accommodation sharing platform Airbnb (ABNB).

Airbnb will blast off from the biggest developing trend in the global economy today: workplace flexibility.

Like with Zoom (ZM) video conferencing tech making it possible to work from home. Airbnb makes it possible to physically work from any home, anywhere, and anytime.

While it’s not fair to draw a direct correlation from workplace flexibility to increasing Airbnb profits, it is clear that the company is poised to grow alongside the Web 3.0 revolution which will focus on decentralization, openness, and greater user utility.

As this new iteration of the internet takes hold and continues to spread, Airbnb's unique business structure will result in revenue produced from the sheer number of workers doing staycation remote working adventures.

This is a real thing.

Workers now go somewhere for a month then change their location to take in a different environment.

Riding this ongoing revolution and the steady reopening of global travel, Airbnb posted record revenue of $2.2 billion during its third quarter, which was 36% above Q3 2019.

If you want to look at the red-headed stepchild of the accommodation sharing platform services, then take a look at Booking.com (BKNG).

It’s not nearly as useful a platform as Airbnb and their exorbitant commission becomes quite prohibitive to hosts and users.

No wonder they do not grow their host volume like Airbnb.

Airbnb’s products also sell itself with the name of the company becoming a verb, while Booking.com is still reliant on spam-like internet searches using Google search to ramp up engagements.

This turns into an expensive marketing spend while Airbnb spends minimal to attract the next incremental customer.

ABNB shares have experienced a recent 20% pullback on the omicron threat, and I believe it’s a good time to start dollar cost averaging here into ABNB shares in the case that a bigger travel load 6 months from now follows through.

The upside to ABNB shares could be quite large if the business world somewhat normalizes next year because this scenario isn’t priced into ABNB shares yet.