Mad Hedge Biotech & Healthcare Letter

July 23, 2020

Fiat Lux

Featured Trade:

(WHY IT'S OFF TO THE RACES FOR BRISTOL MYERS),

(BMY), (PFE), (GILD), (REGN)

Mad Hedge Biotech & Healthcare Letter

July 23, 2020

Fiat Lux

Featured Trade:

(WHY IT'S OFF TO THE RACES FOR BRISTOL MYERS),

(BMY), (PFE), (GILD), (REGN)

For investors, compounding has long been considered the eighth wonder of the world.

Compounding refers to growing your initial capital over time, boosted by well-timed additions to increase your pool of funds. Warren Buffet calls it “snowballing.”

For compounding to work out, though, it’s important to have a long-term investment plan.

Naturally, the first step to successfully invest is choosing the most suitable stock for your portfolio. Ideally, these businesses should have growth runways set up to thrive in the long run and coupled with clear-cut competitive advantages.

These companies should be able to pay out decent dividends as well since these can later be reinvested to accelerate returns.

Among the companies in the biotechnology and healthcare sector today, Bristol-Myers Squibb (BMY) fits the bill.

The company’s strengths lie in its oncology and hematology departments, with sales for its pipeline of drug candidates estimated to beat expectations.

With the new drugs in late-stage trials, BMY raised its annual sales forecast to reach somewhere between $15 billion and $20 billion. This number is expected to be sustained over the next 10 years.

Many of BMY’s promising programs came from its Celgene acquisition in November 2019.

While the whopping $74 billion deal faced pushback at first, the merger is expected to yield $2.5 billion in savings for BMY. This offers the company more elbow room to invest in its R&D sector.

BMY is working on combining its cancer drugs Opdivo and Yervoy with Celgene’s top moneymakers Revlimid and Pomalys, effectively transforming the New York-based company into the largest seller of cancer treatments in the world.

Outside its immuno-oncology lineup, BMY is also performing quite well in the cardiovascular field.

Its blockbuster drug Eliquis, which is a collaborative effort with Pfizer (PFE), remains one of the highest-selling treatments among atrial fibrillation patients.

In 2019 alone, Eliquis raked in $7.71 billion in sales. As for its performance this year, this heart disease drug is estimated to add another $1 billion, pushing its 2020 annual sales to $8.79 billion.

So far, 8 of BMY’s drugs available in the market generate over $1 billion in yearly sales. The company also has 9 new products undergoing Phase 3 trials, with more than 20 drugs slated for review in the next 10 years.

For 2020, BMY is projected to earn $41.8 billion in revenue and roughly $6.20 per share compared to $4.69 last year.

BMY is also anticipated to generate over $14 billion in free cash this year. Thanks to its Celgene acquisition, the company’s revenue will experience a one-time jump of about 60%.

For 2021, BMY is expected to report a 7.5% revenue growth to reach $45 billion or $7.33 per share. This is just a conservative estimate though.

BMY is an attractive stock right now.

It’s currently trading at roughly $60. The company has about $136 billion in market capitalization and pays an annual dividend of $1.80 for a yield of 3%.

In the past 5 years, except for a single quarter in 2017, BMY reported positive quarterly earnings growth.

The shares trade for 8.6 times its expected earnings in the next 12 months, which is just ridiculous for a premium stock.

In terms of its long-term earnings per share, the company is expected to report a 9.3% growth rate.

Finding value among the biotechnology and healthcare sector has become increasingly tricky.

Since the pandemic broke, industry stalwarts like Gilead Sciences (GILD) and Regeneron Pharmaceuticals (REGN) have been receiving constant media attention for their COVID-19 vaccines and treatments. This pushed their valuations to skyrocket.

However, there remain a number of reasonably affordable biotechnology growth stocks.

While these are not making headlines in the fight against COVID-19, these companies offer attractively high long-term earnings-per-share growth rates – and BMY is one of them.

Global Market Comments

July 22, 2020

Fiat Lux

Featured Trade:

(MY NEWLY UPDATED LONG-TERM PORTFOLIO),

(PFE), (BMY), (AMGN), (CELG), (CRSP), (FB), (PYPL), (GOOGL), (AAPL), (AMZN), (SQ), (JPM), (BAC), (BABA), (EEM), (FXA), (FCX), (GLD)

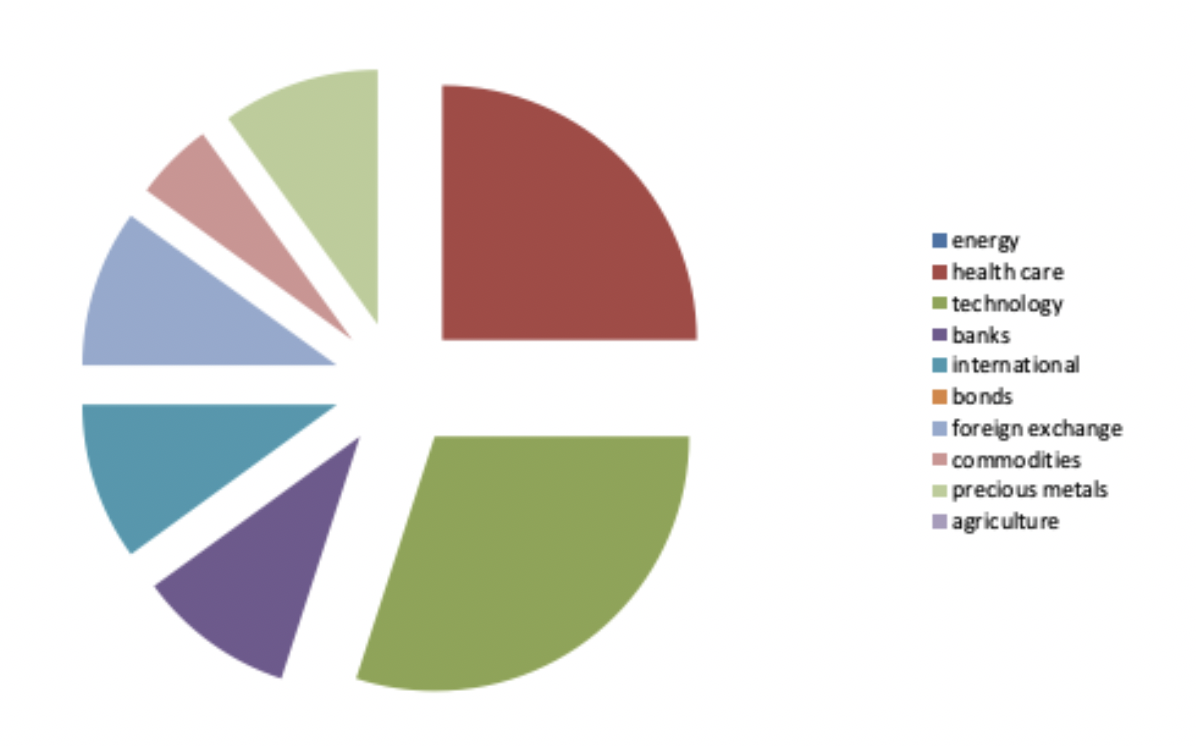

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on October 17, 2019. In fact, not only did we nail the best sectors to go heavily overweight, we completely dodged the bullets in the worst-performing ones, especially in energy.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing, these are the investments you can make, and then not touch until you start drawing down your retirement funds at age 70 ½.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted in red.

To download the entire portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com , log in, go to “My Account”, then “Global Trading Dispatch”, then click on the “Long Term Portfolio” button.

My 5% holding in Biogen (BIIB) was taken over by Bristol Myers (BMY) at a hefty premium at an all-time high, so I’ll take the win. I am replacing it with Covid-19 vaccine frontrunner Bristol Myers (BMY) itself.

I am also taking out healthcare provider Cigna (CI), whose profits have been hammered by the pandemic. A future Biden administration might also move to a national healthcare system that will cap profits. I am replacing it with another Covid-19 vaccine leader Pfizer (PFE).

My 30% weighting in technology remains the same. Even though these stocks are 30% more expensive than they were three years ago, I believe they will lead the charge into the 2020s. It’s where the big growth is. These have doubled or more over the past nine months.

I am sticking with a 10% weighting in banking. Thanks to trillions in stimulus loans, they are now the most government-subsidized sector of the economy. I also believe that massive bond issuance by the US Treasury will deliver a sharply steepening yield curve, another pro bank development.

With my 10% international exposure, I am taking out a 5% weight in slow-growth Japan and replacing it with Chinese Internet giant Alibaba (BABA). The US will most likely dial back its vociferous anti-Chinese stance next year and (BABA) will soar.

I am executing another switch in my foreign currency exposure, taking out a long in the Japanese yen (FXY) and a short in the Euro (EUO) and substituting in a double long in the Australian dollar (FXA).

Australia will be a leveraged beneficiary of a recovery in the global economy, both through a recovery on commodity prices and gold which has already started, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

I’m quite happy with my 10% holding in gold (GLD), which should move to new all-time highs imminently….and then go ballistic.

As for energy, I will keep my weighting at zero, no matter how cheap it has gotten. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free.

My ten-year assumption for the US and the global economy remains the same.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

June 11, 2020

Fiat Lux

Featured Trade:

(THE BIOTECH MERGER BOOM ACCELERATES)

(AZN), (GILD), (BMY), (ABBV), (AGN), (TAK), (CI), (SNY), (JNJ), (UNH), (RHHBY), (LLY)

Nothing can ever be absolutely shocking in the biotechnology and healthcare world.

I’ll admit though that the reports on AstraZeneca’s (AZN) interest in acquiring Gilead Sciences (GILD) surprised me.

The two companies touched base last month on a potential acquisition deal.

If this rumor turns into a reality, then we’re looking at what could be the biggest healthcare deal to date.

That’s saying something considering the massive mergers we’ve seen in the past years.

So far, the biggest biotechnology and healthcare deal is the $87.6 billion acquisition of Celgene (CELG) by Bristol-Myers Squibb (BMY) in 2019.

In the same year, AbbVie (ABBV) acquired Allergan (AGN) for a whopping $83.8 billion, making it the third biggest deal in the healthcare sector to date.

The year 2018 paved the way for two more massive deals in the form of Takeda’s (TAK) $81 billion acquisition of Shire, which ranks fourth overall, and Cigna’s (CI) $68.4 billion deal with Express Scripts (ESRX) in seventh place.

Fifth on the list is by Sanofi’s (SNY) $73.5 billion deal with Aventis in 2004.

Although it has been two decades since it happened, the $72.5 billion merger of Glaxo and SmithKline Beecham in 2000 still counts as one of the biggest deals in the industry. This agreement gave birth to GlaxoSmithKline (GSK).

Prior to Bristol-Myers Squibb and Celgene deal, it was Pfizer’s (PFE) $87.3 billion acquisition of Warner-Lambert in 1999 that topped the list.

AstraZeneca’s current market capitalization is roughly $140 billion. Meanwhile, Gilead Science’s market cap stands at approximately $96 billion.

With all these in mind, the AstraZeneca-Gilead Sciences merger is estimated to reach roughly $250 billion on top of the significant synergies expected throughout the years.

If these two health industry heavyweights merge, then their newly formed company would become the third biggest healthcare company in the world behind Johnson & Johnson (JNJ), which has a market cap of $384.55 billion, and UnitedHealth Group (UNH) with $293.85 billion.

Looking at this potential merger in the context of the coronavirus race, it’s safe to say that the combined efforts of AstraZeneca and Gilead would create a COVID-19 titan.

AstraZeneca’s partnership with the University of Oxford resulted in a COVID-19 vaccine candidate that was recently selected as one of the top five candidates worthy of US government support through Trump’s Operation Warp Speed program.

Meanwhile, Gilead’s antiviral medication Remdesivir has been constantly hailed as the standard of care for COVID-19 treatment since the pandemic broke.

The drug which was previously marketed as an HIV medication is now expected to generate $2 billion in sales as a COVID-19 treatment in 2020 alone.

In 2022, Remdesivir is estimated to rake in roughly $7.7 billion in sales. After that, the antiviral drug is projected to generate annual sales somewhere between $6 billion and $7 billion.

Although everything is hypothetical, let’s take a quick look at where each company stands at the moment outside their COVID-19 efforts.

AstraZeneca has been a consistent strong stock market performer throughout the years.

In the first quarter of 2020, sales improved in practically all of AstraZeneca’s territories. Although it has a diversified portfolio of drugs and a robust pipeline, the company’s hottest segment is its oncology business.

A good example of this is non-small cell lung cancer treatment Tagrisso, which is starting to live up to expectations as the next mega-blockbuster for AstraZeneca.

The cancer drug’s first quarter sales reached an impressive $982 million, showing off a 56% jump year over year.

This is promising considering that its competitors include Roche’s (RHHBY) Tarceva and Eli Lilly’s (LLY) Cyramza.

As for its 2020 revenue forecast, AstraZeneca is reported to rake in $25 billion, from which it will generate approximately $7.5 billion in operating profit.

On the other hand, Gilead also has an impressive portfolio that it can bring to the table.

In the first quarter of 2020, the company earned $5.47 billion in revenue compared to the $5.20 billion it generated in the same period last year.

Despite the decline in its hepatitis products from $790 million in the first quarter of 2019 to $729 in the same period of 2020, Gilead’s HIV line made up for the loss by bringing in over $4 billion in sales compared to the $3.6 billion it earned last year.

Not only that, some of Gilead’s other candidates are exciting.

For example, rheumatoid arthritis drug Filgotinib is expected to become another blockbuster and generate $5 billion in revenue annually.

Meanwhile, the anti-tumor treatment Magrolimab is estimated to rake in $3 billion in peak sales.

With the company’s older drugs still capable of generating strong revenue and its new candidates showing their potential for revenue expansion, Gilead can be assured of a continued cash flow well into the 2030s.

Regardless of whether this rumored mega-merger pushes through, both Gilead and AstraZeneca are attractive stocks worthy of their premium valuations.

Global Market Comments

March 5, 2020

Fiat Lux

SPECIAL MARKET BOTTOM ISSUE

Featured Trade:

(FRIDAY, APRIL 17 SAN FRANCISCO STRATEGY LUNCHEON),

(A LEAP PORTFOLIO TO BUY AT THE BOTTOM),

(TEN LONG-TERM BIOTECH & HEALTHCARE LEAPS TO BUY AT THE BOTTOM)

(UNH), (HUM), (AMGN), (BIIB), (JNJ), (PFE), (BMY)

Mad Hedge Biotech & Healthcare Letter

March 5, 2020

Fiat Lux

SPECIAL MARKET BOTTOM ISSUE

Featured Trade:

(TEN LONG TERM BIOTECH & HEALTH CARE LEAPS TO BUY AT THE BOTTOM)

(UNH), (HUM), (AMGN), (BIIB), (JNJ), (PFE), (BMY)

Joe Biden’s romp over Bernie Sanders in the Tuesday Democratic primary takes the lid off on the entire biotech and healthcare sector. Sanders has promised to dismantle the entire sector by promising Medicare for all and banning private coverage.

Sanders was also about to take a cudgel to drug pricing. While Sanders was leading in the primary, the threats hung over the industry like an 800-pound gorilla.

Yesterday, Sanders went down in flames. You can see this clearly in the price action of Humana (HUM), which rose a ballistic 14.44% yesterday. Similarly, United Health Group (UNH) was up a monster 10.72%.

It is safe to say that the bottom is in for biotech and healthcare stocks.

I am often asked how professional hedge fund traders invest their personal money. They all do the exact same thing. They wait for a market crash like we are seeing now and buy the longest-term LEAPs possible for their favorite names.

The reasons are very simple. The risk of a LEAP is limited. You can’t lose any more than you put in. At the same time, they permit enormous amounts of leverage.

Two years out, the longest maturity available for most LEAPs, allow plenty of time for the world and the markets to get back on an even keel. Recessions, pandemics, hurricanes, oil shocks, interest rate spikes, and political instability all go away within two years and pave the way for dramatic stock market recoveries.

You just put them away and forget about them. Wake me up when it is 2022.

I put together this portfolio using the following parameters. I set the strike prices just short of the all-time highs set two weeks ago. I went for the maximum maturity. I used today’s prices. And of course, I picked the names that have the best long-term outlooks.

If you buy LEAPs at these prices and the stocks all go to new highs, then you should earn an average 229% profit from an average stock price increase of only 11.4%. That is a return 20 times greater than the underlying stock gain. And let’s face it. None of the companies below are going to zero, ever. Now you know why hedge fund traders only employ this strategy.

There is a smarter way to execute this portfolio. Put in throw-away crash bids at levels so low they will only get executed on the next 1,000 point down day in the Dow Average.

You can play around with the strike prices all you want. Going farther out of the money increase your returns, but raises your risk as well. Going closer to the money reduces risk and returns, but the gains are still a multiple of the underlying stock.

Buying when everyone else is throwing up on their shoes is always the best policy. That way your return will rise to ten times the move in the underlying stock.

Amgen (AMGN) - January 21 2022 $235-$240 bull call spread at $3.68 delivers a 172% gain with the stock at $245, up 14% from the current level

Biogen (BIIB) - January 21 2022 $365-$375 bull call spread at $3.89 delivers a 157% gain with the stock at $375, up 14% from the current level

Johnson & Johnson (JNJ) - January 21 2022 $150-$155 bull call spread at $1.63 delivers a 206% gain with the stock at $155, up 8.3% from the current level

Pfizer (PFE) - January 21 2022 $40-$45 bull call spread at $1.05 delivers a 376% gain with the stock at $40.60, up 11.5% from the current level

Bristol Meyers Squibb (BMY) - January 21 2022 $65-$70 bull call spread at $1.50 delivers a 233% gain with the stock at $68, up 11.40% from the current level

Mad Hedge Biotech & Healthcare Letter

January 23, 2020

Fiat Lux

Featured Trade:

(BIOGEN’S BIG ALZHEIMER’S BET),

(BIIB), (BMY), (PFE), (IONS), (MYL)