Mad Hedge Biotech and Healthcare Letter

September 3, 2024

Fiat Lux

Featured Trade:

(ROLLING THE DICE ON BIOTECH)

(RHHBY), (VNDA), (ZVRA), (HALO), (BMY), (GILD)

Mad Hedge Biotech and Healthcare Letter

September 3, 2024

Fiat Lux

Featured Trade:

(ROLLING THE DICE ON BIOTECH)

(RHHBY), (VNDA), (ZVRA), (HALO), (BMY), (GILD)

Remember when you'd jump into a hot tub and the water was just right? That's what the biotech sector feels like right now - it's warming up and ready for a splash.

After years of treading water, biotech stocks are showing signs of life. High interest rates and cash crunches have kept this sector on the sidelines, but the game is changing.

September 2024 is shaping up to be a blockbuster month for the sector, with FDA decisions that could send stocks soaring - or sinking.

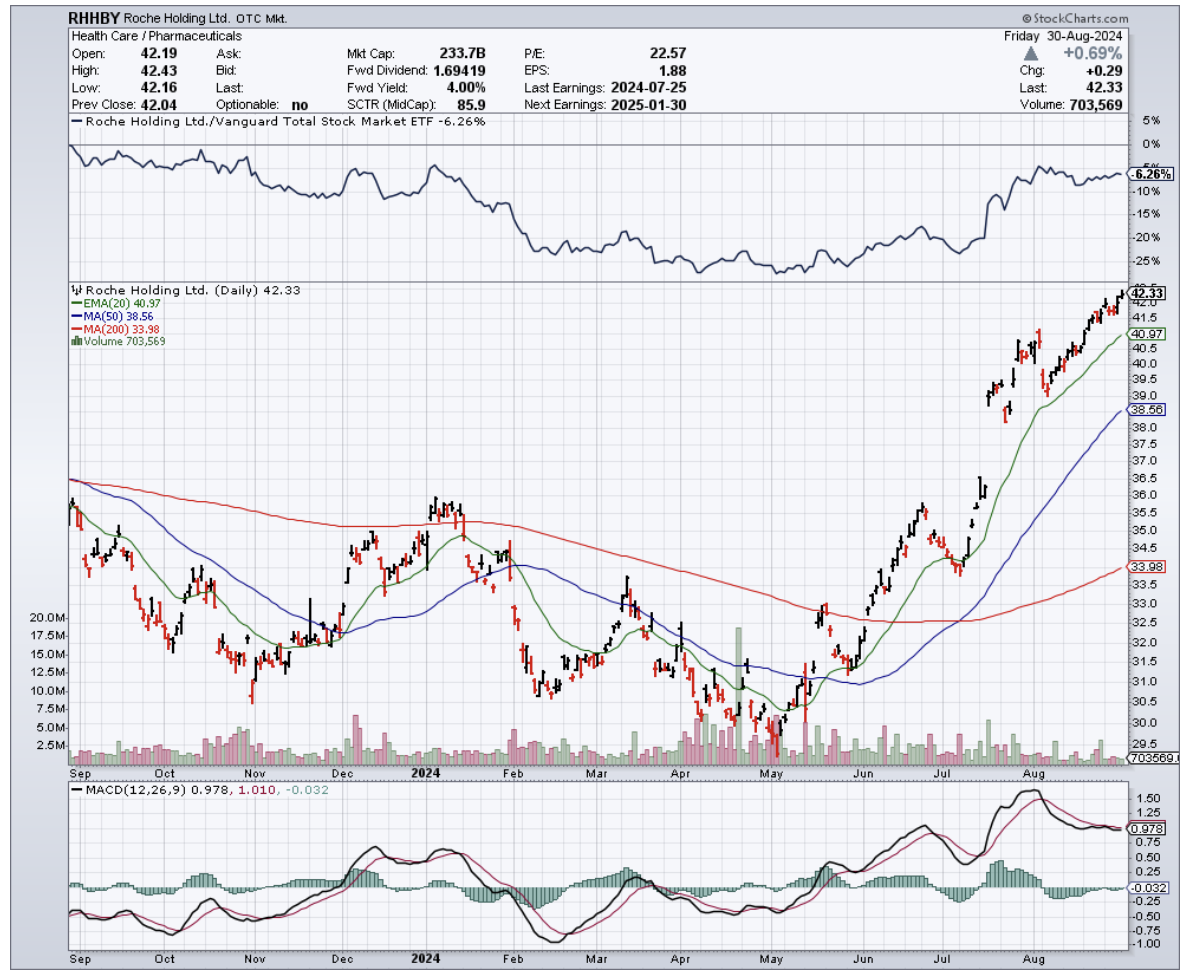

First up, Roche Holding AG (RHHBY) is waiting on pins and needles for the FDA's verdict on Ocrevus SC. This isn't just another drug - it's a new way to deliver their multiple sclerosis cash cow.

If the FDA gives the green light on September 13, Roche could be looking at a bigger slice of the MS pie. Why? Because this new version doesn't need fancy IV setups, opening doors to treatment centers that were previously off-limits.

But Roche isn't the only one with butterflies in its stomach.

Vanda Pharmaceuticals (VNDA) is hoping to make history on September 18 with Tradipitant. This drug aims to tackle gastroparesis, a condition that's been stuck in treatment limbo for four decades. If Tradipitant gets the nod, Vanda could find itself as the big fish in a very lucrative pond.

And let's not forget about the underdogs.

Zevra Therapeutics (ZVRA) is crossing its fingers for Arimoclomol. This potential game-changer targets Niemann-Pick disease type C, a rare brain disorder that's been waiting for its medical knight in shining armor. September 21 could be that day.

These approvals aren't just good news for the companies involved. They're like a shot of adrenaline for the whole biotech sector. Investors love nothing more than seeing potential turn into profit.

But it's not all about solo acts in biotech. These days, it's all about partnerships.

Take Halozyme Therapeutics (HALO), for instance. They've buddied up with Roche to develop Ocrevus SC, bringing their ENHANZE technology to the party.

These kinds of collaborations are golddust for smaller biotech firms. They get access to resources and markets they could only dream of on their own, making them much more attractive to investors with deep pockets.

Speaking of deep pockets, big pharma companies are on the prowl, and several biotech firms are looking mighty tasty.

Bristol-Myers Squibb (BMY) just showed us how it's done by snatching up Karuna Therapeutics. Why? Two words: KarXT.

This antipsychotic drug is currently under FDA review for schizophrenia, and if approved, it could be another lucrative revenue stream. This kind of deal is a win-win. The big fish gets new toys for its pipeline, and the smaller fish gets a cushy new home.

Now, let's talk about the elephant in the room - interest rates.

Biotech companies and high interest rates go together like oil and water. These firms need cash like plants need water, and high rates make that cash harder to come by.

But here's the thing: the Federal Reserve is hinting at rate cuts.

For biotech, that's like Christmas coming early. Lower rates mean easier borrowing and easier borrowing means more research, more trials, and potentially more breakthroughs.

So if rates drop, don't be surprised to see biotech stocks shoot up faster than a rocket.

But it's not just about drugs in the pipeline. The biotech sector is also home to some serious innovation.

Take gene editing and CRISPR. This isn't your grandpa's genetics - it's like we've found the “track changes” function for DNA.

The market for this molecular magic is set to explode from $4 billion in 2024 to a whopping $17.8 billion by 2034. That's a 16.1% annual growth rate, for those of you keeping score at home.

With this technology, I’m not just talking about curing rare diseases here. I’m talking about the possibility of having your own home testing kits that could make your 23andMe results look like a fortune cookie.

And then there’s personalized medicine, which is turning healthcare into a bespoke tailor shop. Your DNA is becoming the blueprint for your treatments, and the market is following suit.

We're looking at a jump from $300 billion in 2021 to $869.5 billion by 2031. Why the boom? Well, sequencing your DNA used to cost more than a mansion.

Now it's cheaper than a decent night out in New York - from over $1 million in 2007 to about $600 today.

Stem cells and regenerative medicine are also getting investors hot under the collar. We're talking about potentially regrowing organs or giving Parkinson's the boot.

This market is set to grow at a spicy 9.74% annually from 2023 to 2030. Basically, it’s like we're entering the age of biological LEGO.

And let's not forget AI - the new brainiac in the lab. It's turning drug discovery into a high-speed chess game, with the AI market in healthcare expected to hit $95.65 billion by 2028.

With the innovations from this tech, scientists could have supercomputers as their lab partners – ones that never need coffee breaks and can crunch data faster than you can say "blockbuster drug."

Given all these possibilities, I think it’s a good time to talk about strategy. After all, investing in biotech isn't one-size-fits-all. It's more like a buffet - you pick what suits your taste and risk appetite.

For the adrenaline junkies who like to walk the tightrope without a net, there's the high-risk, growth investor approach. These brave souls get their kicks from cutting-edge stuff like gene editing and personalized medicine, often diving into early-stage biotech firms working on the next big breakthrough.

It's not for the faint of heart - these stocks can swing wilder than a monkey on espresso. But when they hit, oh boy, do they hit.

Just look at the personalized medicine market - it's set to explode from $300 billion in 2021 to a mind-boggling $869.5 billion by 2031. That's the kind of growth that could make your portfolio do backflips, assuming you can stomach the ride.

On the other side of the petri dish, we've got the value and low-risk investors. These are the steady hands who prefer their biotech stocks aged like fine wine and served with a side of sleep-easy. They're eyeing established companies with robust pipelines, diverse portfolios of approved drugs, and ongoing trials.

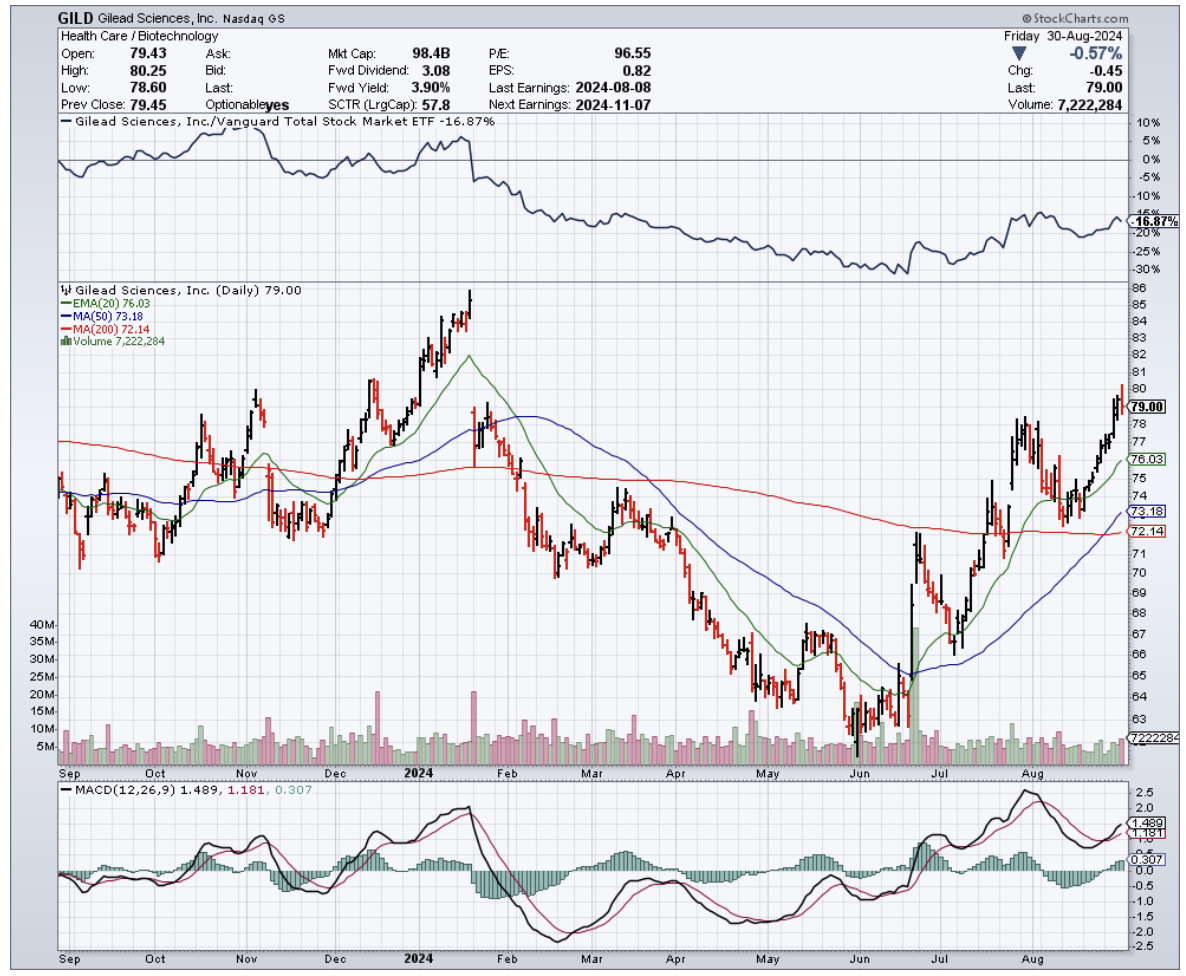

Think Roche with its Ocrevus SC, or old guards like Gilead Sciences (GILD) that have weathered more storms than a lighthouse.

These investors are the tortoises in the biotech race - slow and steady, but with a knack for crossing the finish line, often with a healthy dividend check in hand. They might not make headlines, but they're more likely to let you sleep soundly while your portfolio does the heavy lifting.

No matter which style you choose, one thing is undeniable: the biotech sector is like a sleeping giant, and it's starting to stir. The question is, will you heed the wake-up call or sleep through the alarm?

Mad Hedge Biotech and Healthcare Letter

August 29, 2024

Fiat Lux

Featured Trade:

(ONE TEST TO RULE THEM ALL)

(ILMN), (BAYRY), (LLY), (MRK), (BMY), (AZN), (RHHBY), (NVS), (GH), (TEM), (TMO)

“One test to rule them all, one test to find them, one test to bring them all, and in the lab bind them,” the scientists at Illumina (ILMN) whispered – probably.

Their latest creation just got the FDA nod, and it's set to turn the world of cancer diagnostics on its head. It's as if Gandalf himself handed oncologists a palantír that reveals tumors' deepest secrets.

For those less versed in Middle-earth lore, this is like inventing a universal remote for tumor profiling, and oncologists can't wait to start channel surfing.

Now, you might be thinking, "What's the big deal?" Well, let me break it down for you.

This test, called TruSight Oncology Comprehensive (TSO for short), is the first FDA-approved genomic in vitro diagnostic kit that can make pan-cancer companion diagnostic claims.

In plain English, that means it's a single test that can be used across multiple cancer types. We're talking about a game-changer in precision oncology here.

Let's get into the nitty-gritty. This TSO test is a beast. It screens for a whopping 517 genes and provides comprehensive information on tumor mutational burden (TMB) and microsatellite instability (MSI).

These are crucial biomarkers that help determine how a patient might respond to immunotherapies. The breadth of data this single FDA-approved test can collect is unprecedented.

Now, you might be wondering, "Haven't we had companion diagnostics before?" Sure, but they've typically been limited to specific drugs or cancer types.

This pan-cancer test from Illumina is different. It can be applied to a wider range of solid tumors, and let me tell you, oncologists are loving it.

In fact, about 39% of U.S. oncologists have already said they strongly prefer using multi-gene panels over single-gene tests for guiding treatment decisions. That's a clear signal that there's demand for comprehensive diagnostic solutions like TSO.

Illumina's been busy across the pond, too. A version of this test has been available in Europe since 2022. But the U.S. version's got some new tricks up its sleeve.

It can help identify patients who might benefit from specific immunotherapies, including Bayer's (BAYRY) Vitrakvi and Eli Lilly's (LLY) Retevmo. The latter is a new addition compared to the EU version of the test.

Let's talk about these therapies for a second. Vitrakvi is used for adult and pediatric patients with certain NTRK mutations, regardless of their type of cancer. That's pretty cool, right?

But here's the kicker - these NTRK gene fusions are only found in about 0.1% to 0.3% of solid tumors, and they're tough to detect.

TSO's ability to scan both RNA and DNA means it can find multiple forms of this biomarker. That's a big deal for companies like Bayer, who've sometimes struggled to find eligible patients for this targeted therapy.

But Illumina's not resting on its laurels. They've got a growing pipeline of companion diagnostic claims in development, working hand in hand with drugmakers. They're planning to seek these in future regulatory submissions.

You see, Illumina's been playing the long game, forging partnerships with big pharma to co-develop companion diagnostics that align with targeted therapies.

Take their 2019 partnership with Merck (MRK), for instance. They teamed up to develop and commercialize a companion diagnostic using Illumina's TruSight Oncology 500 assay.

The goal? To identify genetic mutations in cancer patients that would respond to Merck's cancer drugs like Keytruda. This partnership boosted the adoption of Illumina's NGS platform in clinical oncology settings, contributing to both companies' growth.

The market liked what it saw at the time. Illumina's stock got a nice bump following the partnership announcement. And why wouldn't it?

The deal strengthened Illumina's position in the oncology diagnostics market, which is projected to grow at a CAGR of 12.4% from 2023 to 2030.

But Merck's not the only dance partner Illumina's got. They've also teamed up with Bristol-Myers Squibb (BMY) to use their TSO 500 assay as a companion diagnostic for immuno-oncology therapies.

This collaboration expanded Illumina's reach into new oncology applications, allowing BMY to use the TSO platform to identify patients most likely to benefit from its immune checkpoint inhibitors.

And there's more - Illumina's also forged partnerships with AstraZeneca (AZN), Roche (RHHBY), and Novartis (NVS) to develop companion diagnostic tests.

Next, let's talk numbers. Each new FDA-approved indication could potentially add $100 million to $200 million annually to Illumina's revenue. That's no chump change.

Unsurprisingly, Illumina's not the only player in this game.

Companies like Foundation Medicine (a Roche subsidiary), Guardant Health (GH), Tempus (TEM), Caris Life Sciences, Thermo Fisher Scientific (TMO), and GRAIL (another Illumina subsidiary) are all working towards pan-cancer or multi-cancer diagnostics.

Still, Illumina's TSO test is the first to secure FDA approval for pan-cancer companion diagnostic claims. This lead could translate into a significant market advantage.

Actually, Illumina already holds more than 70% market share in the global NGS market as of 2022. This means it’s well-positioned to benefit from this growth, and this latest FDA approval could further consolidate its market dominance.

Speaking of the FDA, they’ve been busy too. They've ramped up their support for precision medicine in recent years, approving a growing number of companion diagnostics and genomic tests.

From 2017 to 2021, they approved over 25 new companion diagnostics, a significant increase from the 5-10 approvals per year in the early 2010s. And a substantial portion of these approvals has been for oncology-related tests.

In 2021 alone, 68% of the FDA's new drug approvals were for cancer treatments.

Now, let's zoom out and look at the bigger picture. According to the World Health Organization, there were an estimated 19.3 million new cancer cases and 10 million cancer deaths worldwide in 2020.

The global cancer burden is expected to rise to 28.4 million cases by 2040, a 47% increase from 2020.

In the U.S., about 1.9 million new cancer cases are expected to be diagnosed in 2023.

The economic impact is also staggering. The economic burden of cancer in the U.S. was estimated at $157 billion in 2020, and it's projected to increase to over $246 billion by 2030.

These numbers stress the growing need for early detection and personalized treatment solutions.

But, unlike other companies, here's where advanced diagnostics like Illumina's TSO can make a difference. By ensuring patients receive the most effective treatments based on their genetic profiles, these tests can reduce unnecessary treatments and improve outcomes.

Studies have shown that using precision diagnostics can lower overall healthcare costs by 15% to 20% by avoiding ineffective therapies and hospitalizations.

Essentially, what we're seeing here is more than just a new test. It's a glimpse into the future of cancer treatment - more precise, more personalized, and potentially more effective.

For patients, it could mean better outcomes. For healthcare systems, it could mean more efficient use of resources. And for us? Well, it could mean significant opportunities in a rapidly growing market.

As Gandalf might say, "All we have to decide is what to do with the time that is given us." Illumina's chosen to use their time crafting this powerful new tool.

The quest to conquer cancer continues, and Illumina’s TSO might just be the ring-bearer we've been waiting for.

Keep your eyes peeled, fellow adventurers. The journey into precision oncology is only just beginning, and it promises to be an epic saga indeed.

Mad Hedge Biotech and Healthcare Letter

July 16, 2024

Fiat Lux

Featured Trade:

(SMALL GIANTS RISING)

(GMAB), (OPHLY), (VRTX), (INCY), (BIIB), (AHKSY), (ALNY), (ARGX), (BGNE), (MRNA), (NBIX), (BNTX), (IPSEY), (CTLT), (NVO), (LLY), (JNJ), (GILD), (ABBV), (MRK), (SNY), (BMY), (GSK)

Remember when David took down Goliath? Well, history's repeating itself in the biotech arena, and this time, David's got deep pockets and a Ph.D.

Since April, I've been watching a trend on the so-called "next-generation" players in biotech and healthcare world. It reminds me of the massive changes I witnessed in Asian markets back in the '70s.

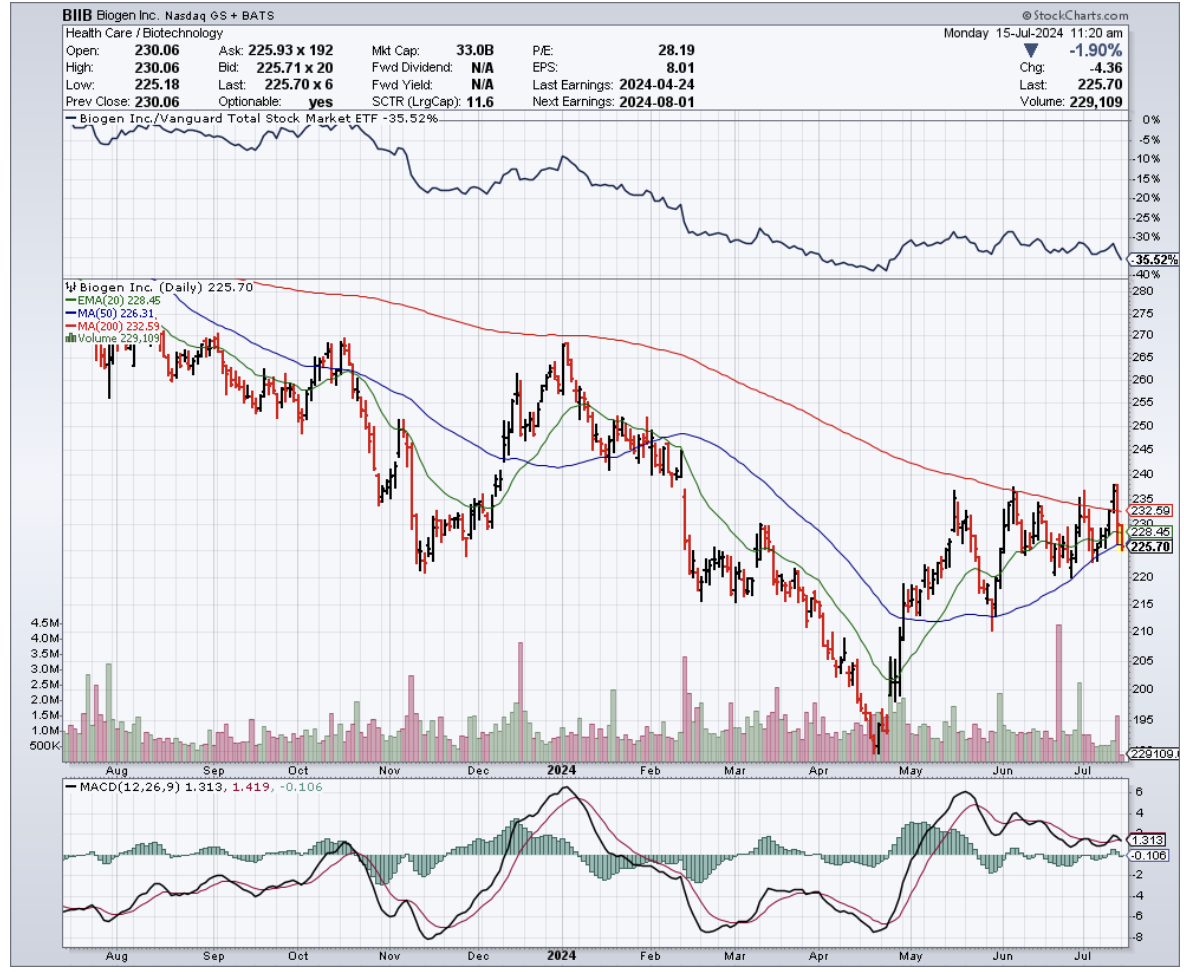

Over the past months, companies like Genmab (GMAB), Ono Pharmaceutical (OPHLY), Vertex (VRTX), Incyte (INCY), Biogen (BIIB), and Asahi Kasei (AHKSY) have been making waves that would impress even the most seasoned surfer. And these next-gen dealmakers aren't just dipping their toes in the M&A pool - they're doing cannonballs.

With cash reserves that would make Scrooge McDuck blush, these companies are overturning industry norms, already joining the prestigious $100 billion market cap club. At this celebration, the champagne flows freely.

So, what’s the play here?

With IPOs cooling down like day-old coffee, companies eyeing public debuts are now ripe targets for acquisition, more tempting than a juicy peach.

This fresh class of biotechs, unphased by the FTC's scrutiny that acts like kryptonite to pharma giants, are acting more like rocket fuel for these agile consolidators.

They slide through regulatory gaps faster than a greased pig at a county fair, grabbing six out of ten biopharma M&A deals in the second quarter alone. They’re not just taking a slice of the pie—they’re rewriting the recipe.

And if we're talking about firepower? These newcomers boast an average of $3.8 billion in pro forma adjusted cash, which isn't just walking-around money — that's "buy a small country" money.

But don't think for a second that this cash is just sitting pretty in their coffers. These upstarts are putting their money where their mouth is.

Take Incyte, for instance. They flexed their financial muscle with a $2 billion buyback in May 2024, sending a clear message to the market: "We're here to play, and we're playing to win."

And that's just the tip of the iceberg. The industry as a whole is lounging on a cool $1.5 trillion. That's enough liquidity to stretch the imagination — perhaps even to purchase a small planet. Mars, anyone? Elon might give us a discount.

But this financial might isn't just about buying power – it's about survival. As I said before, Big Pharma is teetering on a patent cliff that threatens to erode their revenue streams. To stay competitive, they're scrambling to replenish their pipelines, acquiring promising assets and gobbling up innovative technologies with the voracity of Pac-Man on steroids. And it's not just the usual suspects making moves.

This sense of urgency has created a fertile ground for an emerging cohort of aggressive dealmakers. Companies like Alnylam (ALNY), argenx (ARGX), BeiGene (BGNE), Moderna (MRNA), Neurocrine Biosciences (NBIX), BioNTech (BNTX), and Ipsen (IPSEY) are biting off more than the market expected them to chew, and they're coming to the table hungry.

And these companies aren't just nibbling around the edges. They're making bold moves, acquiring cutting-edge biotech firms with promising pipelines. We're talking oncology, epilepsy, kidney diseases, cardiovascular plays – it's like someone turned a medical textbook into a shopping catalog.

In fact, even the big boys are flexing their muscles.

Novo Holdings (NVO) dropped a jaw-dropping $16.5 billion on Catalent (CTLT). That's not even for a drug - it's for manufacturing. Talk about betting on the picks and shovels in this biotech gold rush.

Eli Lilly (LLY) just plunked down $3.2 billion on Morphic Therapeutic (MORF), betting big on inflammation, immunity, and oncology.

Johnson & Johnson's (JNJ) been on a shopping spree, too, snagging Numab's Yellow Jersey for $1.25 billion and Proteologix for $850 million. Both plays in inflammation and immunity - clearly, they've found their sweet spot.

Biogen's not twiddling its thumbs either, striking a deal with HI-Bio worth up to $1.8 billion.

Not to be outdone, Gilead (GILD) shook hands with CymaBay Therapeutics to the tune of $4.3 billion. Even AbbVie (ABBV), playing it cooler, still dropped a cool $250 million on Celsius.

Meanwhile, Merck's (MRK) set its sights on EyeBio for up to $3 billion, focusing on ophthalmology.

Sanofi (SNY), Bristol Myers Squibb (BMY), GSK (GSK) - they're all in, placing their chips on everything from rare diseases to generics to asthma. Clearly, the Big Pharma giants are also trying to keep up with this shift.

As the biotech field evolves, watching these underdogs will be like watching history in the making — where today's Davids become tomorrow's Goliaths. I suggest you keep a close eye on the names above. Adding them to your portfolio would mean you’re not just watching the giants rise — you’ll be a part of the story.

Mad Hedge Biotech and Healthcare Letter

June 6, 2024

Fiat Lux

Featured Trade:

(IS THIS THE COMEBACK TRAIL AFTER A CLIFFHANGER?)

(BMY)

I once scaled a mountain everyone swore was cursed after a landslide. They missed out on stunning vistas and the thrill of conquering a challenge. Turns out, the best views often come after a little rock bottoming.

That brings to mind Bristol-Myers Squibb (BMY), the pharma giant fresh off a stock price landslide of its own.

Bristol-Myers Squibb shares have been in a freefall lately, plunging to nearly half their 2022 peak of $80. The culprit? You guessed it: those dreaded patent expirations and a whole lot of hand-wringing about future growth.

However, as a contrarian investor, I see this doom-and-gloom scenario as an opportunity rather than a setback.

Remember those times when the market turned its back on the likes of Meta Platforms (META) and NVIDIA (NVDA)? They were trading for peanuts not so long ago and look at them now.

Now, you might be thinking, "So, BMY's taken a hit. Is it really that undervalued?"

Well, I've been digging through the stock's history, all the way back to 2012, and something interesting popped up: since 2013, BMY has rarely dipped below its 200-week simple moving average (that fancy brown line on your charts). It just recently broke through that floor, which could mean we're looking at a once-in-a-decade buying opportunity.

Every time this stock has even gotten close to that 200-week line, it's been a signal to buy, and the stock has always bounced back.

Let's not forget that just a couple of years ago, this stock was cruising at over $80 a share. Now it's practically a penny stock compared to that. Has the company really lost half its value?

Bristol-Myers Squibb's been facing some headwinds, no doubt about it. Revlimid, their blockbuster cancer treatment, lost patent protection in 2022, and Eliquis, their anti-stroke champ, is set to follow suit in 2026.

But don't count them out just yet. The company still has plenty of promising drugs in its arsenal that aren't facing patent cliffs anytime soon.

Plus, they've been on a shopping spree, snatching up high-potential companies like Karuna, RayzeBio, and Mirati in 2023. These acquisitions could be just the ticket to reignite growth and fill the void left by those expiring patents.

In a strategic move to streamline operations and boost future earnings, Bristol-Myers Squibb also announced a $1.5 billion plan to cut expenses, including eliminating around 2,200 jobs.

Sure, 2024 might be a bit of a transition year with some one-time charges, but this bold move could pave the way for a leaner, meaner, and ultimately more profitable company in the years to come.

Turning to the financials, analysts are forecasting a bit of a slow year for Bristol-Myers Squibb in 2024, with earnings per share of $0.56 on about $46 billion in revenue.

But they're expecting a major rebound in 2025, with earnings soaring to $6.94 per share on similar revenue.

And even though 2026 projections show a slight dip to $6.30 EPS on $43.85 billion revenue, this isn't a company you're buying for explosive growth.

The current stock price is roughly seven times the 2025 earnings estimate. That's a steal, my friends. Sure, they've got a bit of debt on the books – $57.46 billion to be exact, with $9.67 billion in cash. But hey, they still earned a respectable "A2" credit rating, so they're not exactly teetering on the brink.

Now, let's talk about another star of BMY’s show: that sweet, sweet dividend.

Bristol-Myers Squibb is dishing out $0.60 per share each quarter, which adds up to a juicy 5.5% yield. Think about that for a second.

That's more than most money market funds are offering right now, and with the Fed likely to slash interest rates in the near future, those yields are only going to shrink.

Remember that "Fed dot plot" they released earlier this year? It's hinting at a 2.25-point drop in the Fed Funds rate by the end of 2026. That could take us from the current 5.25% to 5.5% range all the way down to 3% to 3.25%.

Imagine how much more tempting that 5.5% dividend yield from Bristol-Myers Squibb will look when money market rates are potentially 40% lower.

That makes Bristol-Myers Squibb's current situation practically irresistible to a contrarian investor like me. We're talking about a stock trading at a price we haven't seen in over a decade, relative to the 200-week simple moving average. That's the kind of bargain that makes my palms sweat.

And that's not all. With a valuation hovering around seven times the 2025 earnings estimate and a dividend yield that makes money market funds look like pocket change, this could be a recipe for serious upside.

Sure, patent expirations are a pain in the you-know-what for every pharma company. But let's not forget those initial years of patent protection are like a golden ticket. Plus, Bristol-Myers Squibb has a proven track record of developing and acquiring blockbuster drugs.

Of course, there's no sugarcoating the challenges and risks, but when a stock's 5.5% yield and a rock-bottom P/E ratio are staring you in the face, it's hard to ignore the potential upside. That's why I'm dipping my toes in with a small initial position, gradually building it up over time.

I'm playing the long game here, folks. I believe that eventually, just like with other beaten-down stocks, investors will wake up and realize the incredible value this historically successful company offers.

In the meantime, that generous dividend will keep those money market-like payouts rolling in while we wait for the share price to rebound.

Mad Hedge Biotech and Healthcare Letter

May 30, 2024

Fiat Lux

Featured Trade:

“SCALING THE CLIFF”

(PFE), (BMY)

Bob Dylan was right: "The times they are a-changin'". And for Pfizer (PFE), those changing times mean navigating a post-pandemic world and a looming patent cliff. Can they rise to the challenge, or will they be singing the blues?

Pfizer hardly needs an introduction. Founded 175 years ago in 1849 and publicly listed in 1942, Pfizer boasts a market cap of over $160 billion, with highly liquid options trading against its equity.

However, this stock has been on a bit of a rollercoaster lately.

With revenues exceeding $240 billion between 2021 and 2023, largely from vaccines and cancer treatments sold in over 200 countries, Pfizer's reach is undeniable.

But after hitting a record high of $61.71 a share in December 2021, it's taken a nosedive – more than a 50% drop.

So, what gives? Well, it's mostly a combo of waning demand for their Covid-19 products and the dreaded patent cliff looming over some of their top-selling drugs.

At the moment, Pfizer's portfolio paints a mixed picture, with some drugs shining brightly and others facing a cloudier future.

Their pneumonia vaccine duo, Prevnar 13 and 20, remains a reliable workhorse, raking in $6.4 billion in FY23, a 3% increase. With Prevnar 20's patent secure until 2033, it's a safe bet for continued success.

Eliquis, the blood thinner co-marketed with Bristol-Myers Squibb (BMY), is also holding its own, bringing in a respectable $6.7 billion in FY23, up 5%. However, the looming threat of generic competition in 2028 could put a damper on its future prospects.

On the other hand, Vyndaqel, a combination heart and nerve drug, has been a true standout, boasting a remarkable 36% jump in revenue to $3.3 billion in FY23.

Doctors have embraced it for treating a heart condition called ATTR-CM, but its patent situation remains uncertain with a potential expiration in 2024, unless Pfizer's extension to 2028 is approved.

Not all is rosy in Pfizer's garden though.

Comirnaty, their COVID-19 vaccine, may still be pulling in a hefty $11.2 billion in FY23, but it's a far cry from its FY22 peak. Sales have plummeted 70%, and those booster shots aren't exactly flying off the shelves anymore.

As for Paxlovid, the once-promising COVID-19 treatment, this drug has suffered an even more dramatic fall from grace, with revenue crashing 92% to $1.3 billion in FY23. To add insult to injury, Uncle Sam returned a staggering 6.5 million treatment courses.

Meanwhile, Ibrance, their breast cancer treatment, is also feeling the heat, with sales down 6% to $4.8 billion in FY23. It's facing tough competition overseas and its patent is set to expire in 2027, adding further pressure on its future performance.

To make matters worse, several other Pfizer blockbusters – Inlyta, Xeljanz, and Xtandi – are also staring down the barrel of patent expiration in the next few years.

This looming patent cliff poses a significant challenge for Pfizer, as these drugs have been major contributors to their revenue stream.

The company will need to rely on its pipeline of new drugs and strategic acquisitions to offset the potential losses and maintain its position as a leading player in the pharmaceutical industry.

Does that mean, then, that the $43 billion Seagen acquisition in December 2023 could become a lifeline for Pfizer?

Facing a double whammy of declining blockbuster sales and the looming patent cliff, Pfizer isn't sitting idly by. Seagen brings a fresh arsenal of patent-protected cancer-fighting drugs to the table, including three promising antibody-drug conjugates (ADCs).

Two of these, Adcetris for Hodgkin lymphoma and Padcev for urothelial cancer are already showing blockbuster potential, having raked in $751 million and $479 million, respectively, in the first nine months of 2023, despite the acquisition's timing.

But Pfizer's ambition doesn't stop there.

With five new therapies and six label expansions slated for oncology alone by 2026, they're banking on biologics like ADCs to fuel their growth.

They predict these cutting-edge treatments will surge from 6% to 60% of their cancer revenues by 2030, potentially yielding eight new blockbusters.

For now, Seagen's arrival is a much-needed boost to their oncology sales, which dipped 4% to $11.6 billion in FY23, even with Seagen's $120 million contribution in the final weeks of the year.

While the Seagen acquisition helps Pfizer tackle its goals of dominating oncology and fueling pipeline innovation, it's not the whole picture.

Pfizer's got a few other tricks up its sleeve: maximizing new product performance, trimming costs, and playing the capital allocation game to keep shareholders happy.

They're even planning a $3 billion spending spree from late 2023 through 2024, aiming for a cool $4 billion in annual cost savings. Talk about tightening the belt while expanding the empire.

Speaking of empires, Pfizer's 4Q23 results were a bit of a wake-up call.

Earnings per share (EPS) tanked to $0.10 (non-GAAP) on revenue of $14.2 billion, a far cry from the $1.14 EPS and $24.3 billion revenue of the previous year.

For the full year, EPS dropped a whopping 72% to $1.84 (non-GAAP), with revenue down 42% to $58.5 billion.

But, if you ignore those pesky Covid-19 products (Comirnaty and Paxlovid), the top line actually grew a bit – 8% in Q4 and 7% for the whole year.

Just remember, that Paxlovid revenue reversal in Q4 wasn't pretty, slashing both GAAP and non-GAAP EPS by $0.54.

Fast forward to Q1 2024, and Pfizer's numbers were a bit more cheerful, at least compared to what the analysts expected.

Non-GAAP EPS came in at 82 cents, a solid 30 cents above the consensus.

Revenue did fall 19.5% year-over-year to $14.9 billion, but even that beat estimates by $900 million.

Management's still sticking to their FY2024 guidance of $58.5 billion to $61.5 billion in revenue and $2.15 to $2.35 in non-GAAP EPS. We'll see if they can deliver.

That Seagen deal wasn't cheap, though, adding a hefty $31 billion to Pfizer's debt pile. As of March, they had about $12 billion in cash and marketable securities against over $61 billion in long-term debt. Yikes.

Still, management's determined to keep raising those quarterly dividends, now up to $0.42 a share in early 2024. That's a lot, considering it ate up 91% of their non-GAAP earnings in FY23 and is projected to gobble 78% in FY24.

With all that debt, don't expect any more stock buybacks in 2024. Pfizer's taking a break from that game, just like they did last year.

Despite Wall Street's lukewarm reception to Pfizer's patent cliff strategy, it's important to remember that this pharmaceutical giant is far from down for the count.

So, sure, Pfizer's 2023 revenue took a 42% nosedive compared to 2022, but let's not forget: over 620 million people worldwide still rely on their meds.

They actually scored nine FDA approvals, sold more pharmaceuticals than anyone else on the planet, and they're not sitting idly by while their product sales decline. Clearly, they're making moves.

The current bargain-basement price of Pfizer's stock, trading at a P/E of 10.4 on FY25E EPS, coupled with a juicy 5.9% yield, might just be the cherry on top for savvy investors willing to bet on the company's ability to navigate these turbulent times. Whether they can pull it off is anyone's guess, but at this price, it might be worth a gamble.