Mad Hedge Biotech and Healthcare Letter

May 28, 2024

Fiat Lux

Featured Trade:

(GET YOUR GEIGER COUNTERS READY)

(NVS), (LLY), (BMY), (AZN)

Mad Hedge Biotech and Healthcare Letter

May 28, 2024

Fiat Lux

Featured Trade:

(GET YOUR GEIGER COUNTERS READY)

(NVS), (LLY), (BMY), (AZN)

Hang on to your Geiger counters because we're about to dive deep into the world of radiopharmaceutical therapy. I bet even Marie Curie would be impressed by the mind-blowing leaps we've made since her ground-shattering discoveries a century ago.

Now, don't get me wrong, she's a tough act to follow. But the big guns in pharma have taken up the challenge, piling up billions on the roulette table of targeted radiopharmaceutical therapy.

And from where I'm sitting, the odds are looking pretty darn exciting.

Just picture the scene: Radiation that directly takes the fight to those nasty tumor cells, like a microscopic missile strike that zaps cancer cells while ignoring the innocent bystanders.

How? By hitching a radioactive particle to a targeting molecule - think Uber, but for cancer therapy.

This healthcare game-changer, dubbed radiopharmaceutical therapy is projected to become a whopping $25 billion goldmine.

Forget the clunky radiation therapy your grandparents endured – this is precision, it's innovation, and it could potentially enrich your investment portfolio.

Actually, everyone seems to be piling into the radiopharma race. Experts say we're merely at the start line and these next-gen technologies could bring a windfall.

Evidence? The recent flurry of acquisitions, with no less than four deals being sealed just these past months.

Now, let's put some names to this game.

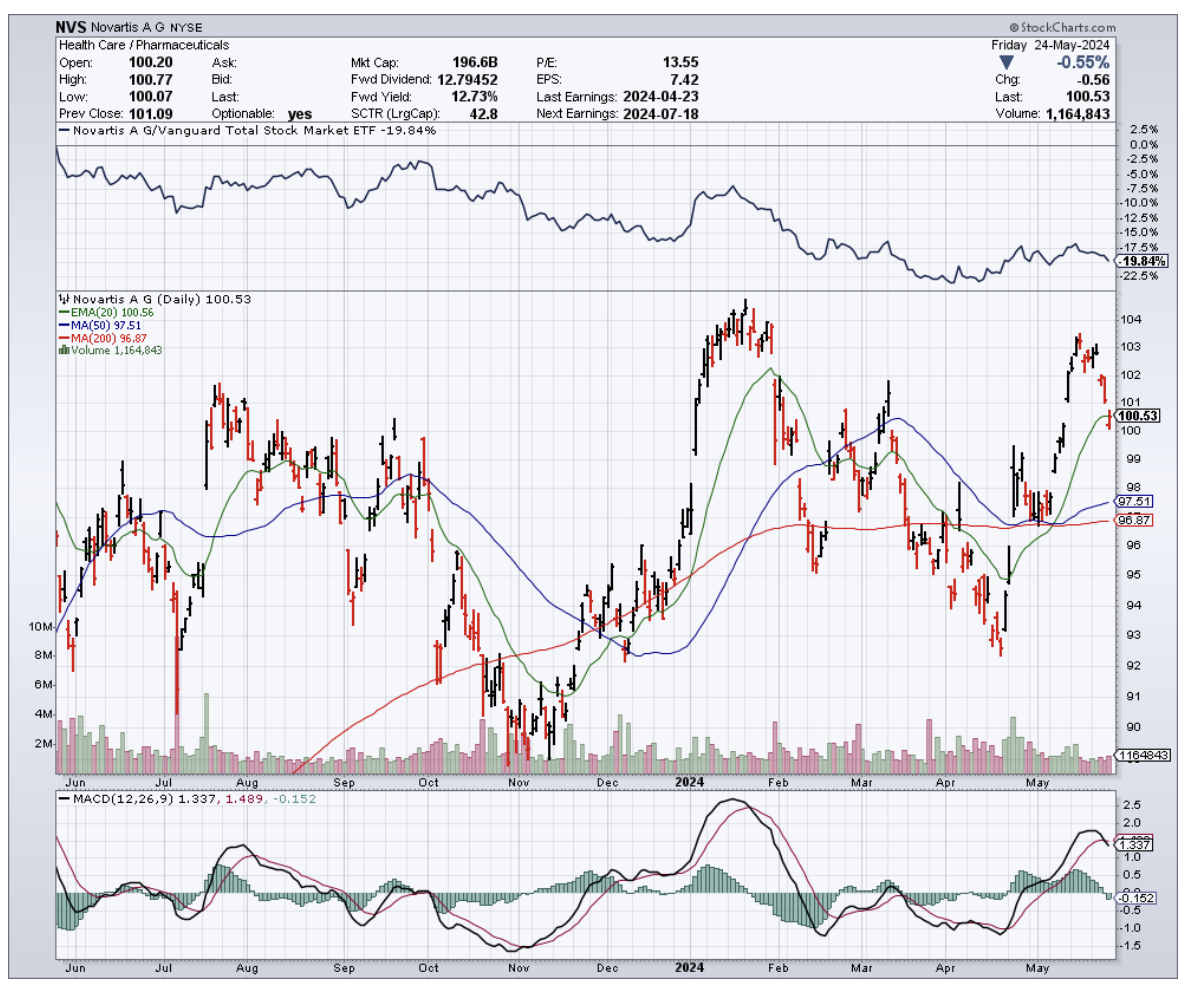

Novartis (NVS) is leading the pack with two radiopharmaceutical showstoppers under its belt. With their drugs Pluvicto and Lutathera, they're forecasted to rake in a whopping $5 billion by 2028 – that's more zeros than I can count on two hands.

Not just resting on their pile of success, they've scooped up Mariana Oncology in a $1 billion deal. This strategic move solidifies Novartis' dominion in the radiopharmaceutical arena – and you can quote me on that.

Inspired by Novartis' success, other pharmaceutical titans are catching the FOMO fever.

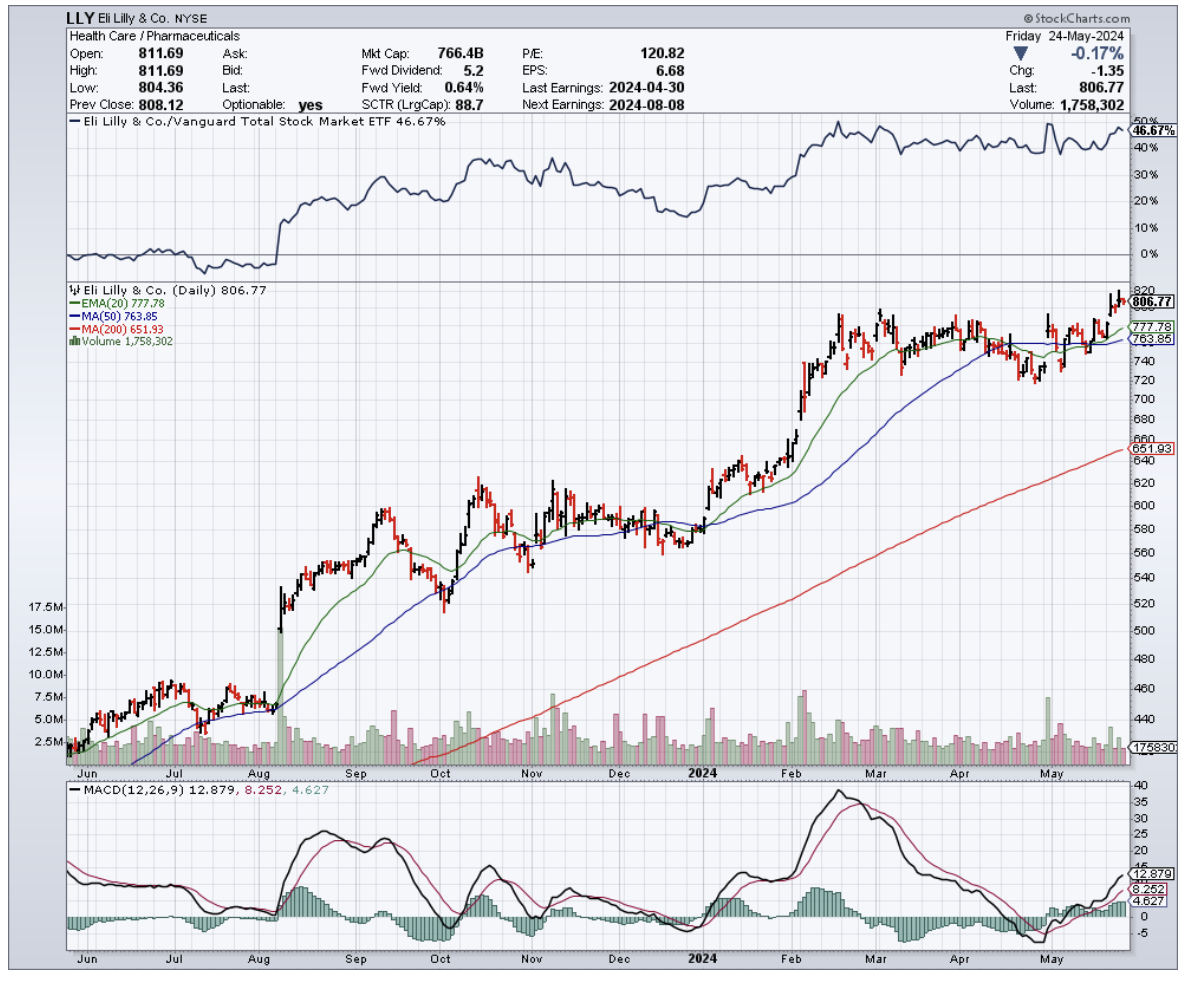

Eli Lilly (LLY), for instance, handed over $1.4 billion to acquire Point Biopharma and its promising radiation drug, PNT2002.

The investors’ darling this year with a near 38% surge in stock price (thanks to the overwhelming success of its obesity drugs), Eli Lilly is set to maintain its upward trajectory by venturing into the radiopharmaceutical space.

Bristol-Myers Squibb (BMY) isn't about to be left out of the radiopharmaceutical race either.

They ponied up a cool $4.1 billion for RayzeBio, snagging a promising pipeline of treatments. One standout is RYZ101, a late-stage targeted radiopharma therapy already making waves in trials for gastroenteropancreatic neuroendocrine tumors and small-cell lung cancer.

This acquisition followed closely on the heels of their $14 billion buyout of schizophrenia drug developer Karuna Therapeutics. Clearly, they’re feeling the heat as patents on some of their older cash cows are set to expire.

So, sure, BMY’s stock has been a bit sluggish lately, but this radiopharmaceutical gamble could be the shot in the arm they need.

And the acquisition spree doesn't stop there. AstraZeneca (AZN) also dove headfirst into the radiopharmaceutical pool, shelling out $2.4 billion for Fusion Pharmaceuticals in March.

Fusion's pipeline, including their Phase 2 candidate FPI-2265 for metastatic castration-resistant prostate cancer, adds another potential blockbuster to the mix.

Meanwhile, several biopharma companies are still standing tall, catching the eye of investors.

In fact, the venture capital poured into radiopharmaceutical drugs surged to $518 million last year, a cool 722% increase from 2017.

The race isn't slowing down anytime soon either. Researchers are exploring the use of radiopharmaceuticals alongside other treatments like immunotherapy, and even envision a future where this technology could be applied to any cancer, including ovarian, breast, or brain tumors.

And with only two products currently in the market, the potential for growth in targeted radiotherapies seems almost infinite.

So, I'll say it one more time – get your Geiger counters ready. The radiopharmaceutical revolution is just getting started, ladies and gentlemen. It’s time to zero in on this hotbed of innovation and watch your investments go nuclear.

Mad Hedge Biotech and Healthcare Letter

March 12, 2024

Fiat Lux

Featured Trade:

(A BIOPHARMA'S RESURRECTION FROM PATENT PURGATORY)

(BMY), (PFE)

So, Bristol-Myers Squibb (BMY), that old stalwart of the biopharma world, is making a comeback, and not just any comeback.

After what seemed like an eternity in the doldrums, with sales taking a hit left and right thanks to the expiration of patents on blockbuster drugs like Revlimid, this giant is stirring again.

And let me tell you, it's about time. My take? Keep a keen eye on BMY because this phoenix is rising.

To put things in perspective (and explain why I’m excited about this), let's not forget this little nugget: in the past year, Bristol-Myers was practically the only biopharma not to get an invite to the price surge party, apart from Pfizer (PFE), which took a 33.4% nosedive. Ouch.

Now, for the important details. After five quarters of watching sales dip like a roller coaster on the downward run, Bristol-Myers is back with a bang — or at least, a firm step in the right direction.

Although the company reported a slight 2% dip in annual sales to $45 billion, the underlying story is one of renewal and optimism. For the first time in a while, there are tangible signs that the company is navigating its way out of the patent purgatory that had ensnared its revenue streams.

Diving into the deep end, their LOE drug revenue shrunk to $7.1 billion in 2023, with Revlimid sales plummeting 36% to a mere $1.45 billion in the fourth quarter alone.

Yet, there's a glimmer of hope with new bloods like Reblozyl and Breyanzi, racking up a cool $423 million in Q4 sales between them.

Meanwhile, the bread and butter of Bristol-Myers, their in-line product portfolio, pulled in $34.3 billion, managing a modest 3% growth last year.

But here’s where it gets interesting: their new product portfolio skyrocketed by 77%, touching $3.6 billion for the year. As we waved goodbye to Q4, these new products were nearly outselling the old guard.

Sure, they're still the newbies, but their slice of the revenue pie jumped from 4.4% in 2022 to about 8% in 2023.

Add to that the success of their cancer treatment Opdivo, which enjoyed a 9% revenue bump, and you've got reasons to be cheerful.

Plus, with the market whispering sweet nothings of a return to growth, with sales expected to hit $46 billion in 2024, it’s hard not to get a little enthusiastic.

Let’s also not forget where Bristol-Myers shines: they've got a knack for snapping up small biotechs, keeping R&D spending savvy while hunting for the next big breakthrough.

In 2023, they're sitting pretty with a $7.51 EPS and operating cash flows to the tune of $14.0 billion. Translation? They've got the war chest to fund their growth crusade starting in 2024.

More importantly, Bristol-Myers has an extremely diverse portfolio.

It's like they've got their fingers in every pie – or, in this case, a smorgasbord of drugs tackling everything from the nitty-gritty of Oncology and Hematology to the intricacies of Immunology/Fibrosis and Cardiovascular health.

This isn't your run-of-the-mill, all-eggs-in-one-basket kind of deal. While some pharma giants are playing a high-stakes game banking on a single blockbuster or a handful of hopefuls, Bristol-Myers’ playing it smart with a kaleidoscope of treatments across the board.

To date, they've got over 12 assets strutting towards the registrational phase with another 30 doing the early-stage clinical studies. If that doesn't scream "long-term growth and earnings potential," I don't know what does.

Looking ahead to 2024, the brass at Bristol-Myers is promising "low-single-digits" revenue growth, while eyeing an EPS somewhere in the neighborhood of $7.10 to $7.40.

Sure, that might look like a step back from 2023's $7.51, but let's not forget their bill for their shopping spree – snagging Mirati Therapeutics for $14 billion isn't exactly pocket change, and neither is giving their new product lineup the grand tour.

What happens next? Well, the market loves a comeback story, especially in biopharma, and Bristol-Myers is penning a gripping narrative.

After a year that tested its mettle, Bristol-Myers is on the upswing, promising more thrills for investors. Admittedly, there might be some bumps along the way as they fold in their latest acquisitions, but any dips could be golden opportunities for the savvy investor.

I suggest you keep Bristol-Myers Squibb on your radar. This biopharma phoenix is just getting its second wind, and the journey ahead looks as promising as ever.

Mad Hedge Biotech and Healthcare Letter

March 7, 2024

Fiat Lux

Featured Trade:

(RALLY CAPS ON)

(VKTX), (LLY), (NVO), (AKRO), (GILD), (BMY), (AMGN), (PFE)

The biotech sector just flipped its rally cap inside out. After a brutal losing streak, it's clawing its way back. The SPDR S&P Biotech (XBI) exchange-traded fund, a barometer for the sector, started to show signs of life when it soared by 5.7% last month, cresting over $100 a share for the first time in two whole years.

While champagne might be premature, this comeback is heating up, and whispers of a full-fledged rally are echoing through Wall Street.

After a rough patch that kicked off in early 2021, seeing the fund take a nosedive of over 60% by late October 2023, the tide began to turn last fall. Initially, whispers of lower interest rates in 2024 sparked interest across small-cap indexes, including our biotech heroes.

Yet, lately, the buzz is all about biotech's own merits — think breakthrough medical trials and the juicy prospect of big pharma playing Pac-Man with smaller but promising biotech firms to beef up their drug pipelines.

And let me tell you, if the current rally's got legs, we might just be witnessing the most thrilling biotech comeback in over half a decade. Especially if the merger and acquisition scene stays hot, we could see biotech stocks climbing even higher.

Take everything that happened in the sector in February as an example. Viking Therapeutics (VKTX) threw down the gauntlet with promising data on its weight loss drug, VK2735, making investors sit up and take notice.

Actually, this candidate is shaping up to be a formidable rival to obesity treatments from Eli Lilly (LLY) and Novo Nordisk (NVO), sending Viking's shares skyward by a jaw-dropping 121% in a single day.

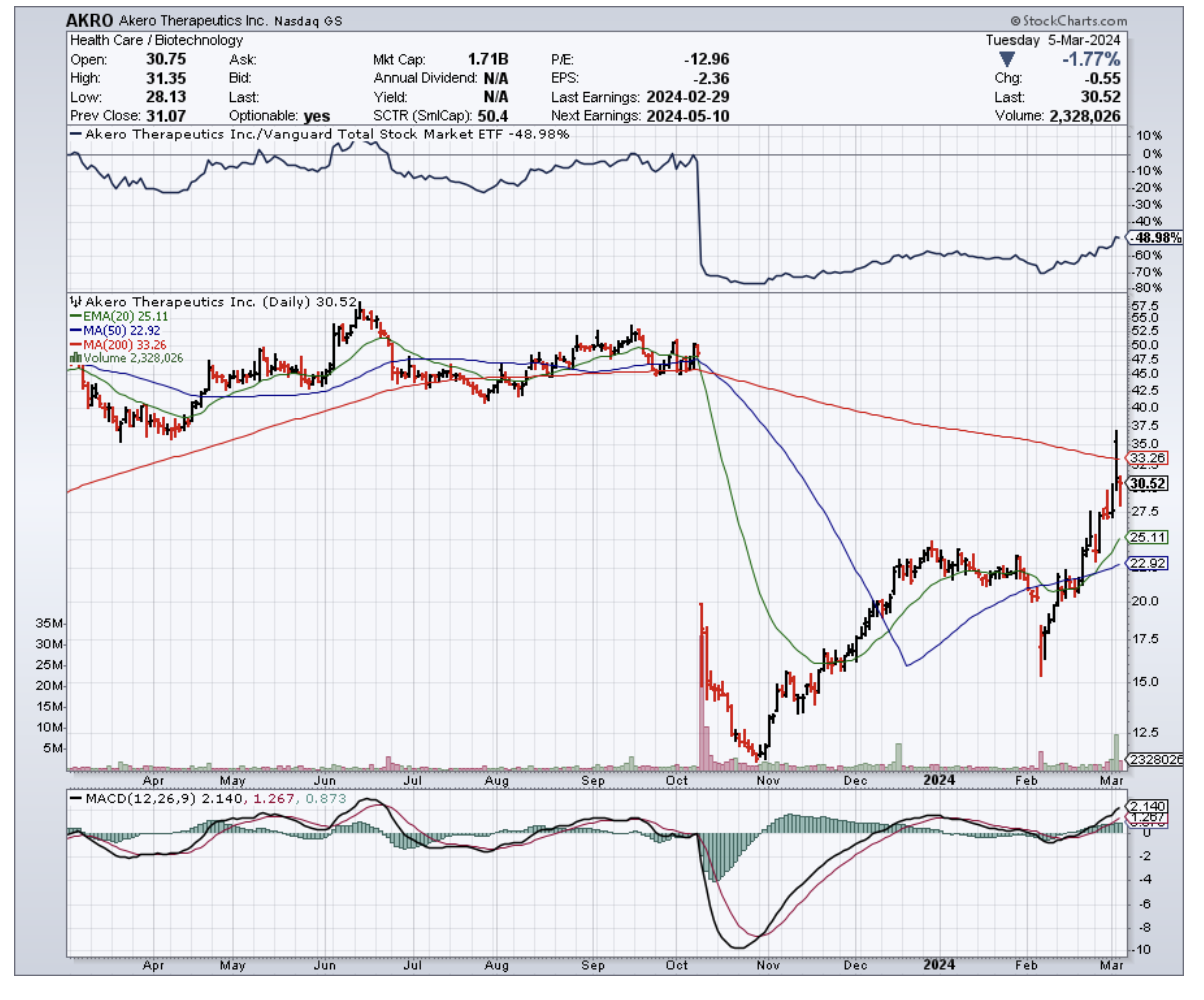

And it's not just Viking stealing the spotlight. Another biotech named Akero Therapeutics (AKRO) also bounced back with some impressive data of its own, challenging the doom and gloom that settled over biotech firms following Eli Lilly's bombshell MASH trial results.

Akero's mid-stage study showed that their drug, efruxifermin, could significantly roll back liver fibrosis in MASH patients — putting a whopping 75% of high-dose recipients on the mend, a stark contrast to the 24% placebo group.

This revelation was a game-changer, especially after Lilly's tirzepatide threw the sector for a loop, hinting at a potential endgame for MASH-specific treatments. But while Lilly's announcement left many details to the imagination, Akero's clear-cut results have reignited excitement over what might be the best MASH treatment yet seen.

As expected, in the midst of this resurgence, the likes of Viking and Akero are catching eyes not just for their groundbreaking treatments but also as tantalizing acquisition targets. Heavyweights like Gilead Sciences (GILD), Bristol Myers Squibb (BMY), Amgen (AMGN), and Pfizer (PFE) are said to be circling, each eyeing a slice of the biotech pie.

As for the biotech investment landscape in general, it's buzzing with renewed vigor. The early months of 2024 have welcomed a smattering of biotech IPOs, a refreshing change after a long drought. CG Oncology's late January debut practically set the market ablaze, doubling in value on its first trading day.

Moreover, public biotechs have found a lifeline in PIPE deals, sidestepping the regulatory hoops of secondary offerings. For instance, Denali Therapeutics' (DNLI) recent PIPE deal, expected to rake in $500 million, is proof of the sector's warming investment climate.

So, dust off those rally caps because the biotech sector isn't just back in the game – it's swinging for the fences.

Breakthrough treatments, a sizzling M&A market, and investors throwing their support behind innovation — this rally has all the ingredients to paint a bright future for the industry. While there will be bumps along the road, one thing's for sure: the biotech sector is poised for a season no one wants to miss.

Mad Hedge Biotech and Healthcare Letter

February 15, 2024

Fiat Lux

Featured Trade:

(TACKLING THE BIG C)

(PFE), (BNTX), (BMY), (ABBV), (AZN)

Super Bowl Sunday: not just a day for football fanatics but a golden opportunity for brands to shine brighter than the halftime show, captivating over 100 million pairs of eyes.

Amid the usual suspects of beers, cars, and fizzy drinks, an unexpected name popped up on the screen: Pfizer (PFE). The Big Pharma titan threw its hat in the ring with a multimillion-dollar message that could be summed up as a toast to science itself.

Here’s how Pfizer’s ad went: animated legends of science — from Newton to Einstein, alongside Rosalind Franklin and Katalin Karikó — belting out an ode to medical milestones to the tune of Queen’s “Don’t Stop Me Now.” Add a dash of whimsy with a cameo from penicillin and a crooning tardigrade, culminating in the heartwarming sight of a young cancer survivor leaving the hospital to applause.

This cinematic piece wasn’t just about selling a product; it was about selling a dream, one where science leads the charge against cancer, underscored by Pfizer’s new rallying cry, "Outdo Yesterday," and a nudge towards LetsOutdoCancer.com.

Shrouded in mystery is the exact price Pfizer paid for this 60-second spectacle — shortened from its original 90-second glory.

But, my sources say that the pharma giant shelled out around $6.5 million to $7 million for half that time, making Pfizer’s splurge no drop in the bucket, especially juxtaposed against a recent $15 million pledge to the American Cancer Society.

This grand gesture comes at an important milestone, marking Pfizer’s 175th year and a concerted push to cast a vibrant, forward-looking shadow across its brand, appealing to the public, investors, and its own ranks alike.

After all, it’s an open secret that Pfizer’s looking to weather a storm, with its COVID-19 vaccine sales dwindling.

Despite riding high on the COVID-19 vaccine wave in partnership with BioNTech (BNTX), raking in roughly $57 billion across 2021 and 2022, Pfizer's financial seas have been anything but calm. The stock’s dramatic descent from its late 2021 peak paints a picture of uncertainty, rooted in the sobering performance of its COVID-19 titans, Comirnaty and Paxlovid.

Yet, as we can see, Pfizer’s narrative isn’t one of gloom. Stripping away the pandemic’s shadow reveals a company in robust health, with a 7% operational growth and a record seven FDA nods in 2023 alone.

Speaking of making it rain, Pfizer's not just throwing its COVID-earned billions around for kicks. For example, they've laid down a cool $43 billion on the table to bring oncology biotech Seagen into the fold.

This acquisition isn't your everyday shopping spree either. It's a move designed to transform Pfizer into the leader of the antibody-drug conjugate (ADC) movement in cancer therapy, potentially beating the likes of Bristol Myers Squibb (BMY), AbbVie (ABBV), and AstraZeneca (AZN).

Think of this move as the biopharma eyeing Seagen's $3 billion in 2023 revenue and saying, "Let's crank this up to $10 billion by 2030." Ambitious? Absolutely. But if anyone's got the blueprint to make it happen, it's Pfizer.

The pivot to cancer isn’t just a strategic shift but a play for the heartstrings of a global audience. With cancer touching lives universally, Pfizer’s Super Bowl gambit seeks to transcend its COVID-19 narrative, aiming for a connection that’s both deeper and more universal. The deliberate omission of its vaccine from the ad speaks volumes, aiming to bridge divides in a viewership as diverse as the Super Bowl’s.

Still, the true measure of its Super Bowl splash — beyond the ad’s immediate sparkle — may lie in subtler indicators, from stock movements to talent retention and a potential surge in interest around its cancer-fighting mission.

Whether this move translates into a long-term win for Big Pharma titan remains to be seen, but for now, the spotlight isn’t just on the Chiefs’ victory but on Pfizer’s leap into the hearts and minds of millions, championed by science and the indomitable spirit of innovation. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

January 30, 2024

Fiat Lux

Featured Trade:

(BRAIN GAINS)

(BIIB), (ESALY) (LLY), (REGN), (ALNY), (MRK), (AMGN), (PFE), (BMY)

Let's talk about a golden opportunity knocking at our doors – the booming market of Alzheimer's disease treatments in biopharma. We're not just talking about a small uptick here. With a slew of new meds on the horizon, this market is gearing up for some serious growth, and you might want to grab a piece of this pie.

The dominant name on our radar is Biogen (BIIB), ticking at $260 per share with a market cap that's flirting with $39 billion.

Now, with a solid $10 billion in sales and trading at a nifty 16 times its 2024 estimated earnings, Biogen's got some serious mojo. I've been eyeing it since last year, but boy, have things changed since then.

A critical game-changer was Chris Viehbacher, the new CEO since November 2022. He's already played a couple of aces – slicing $800 million in costs (which, by the way, could pump up earnings by $5 a share by 2025) and wrapping up the acquisition of Reata Pharmaceuticals in September 2023.

This new addition to Biogen’s portfolio has a hot ticket item, Skyclarys, for treating Friedreich’s ataxia. It's a rare find, but it could add a cool $5 per share in earnings in a few years.

But the most exciting name in Biogen’s arsenal is Leqembi, the company’s Alzheimer’s treatment. They're splitting the pot with Eisai (ESALY), and this drug is a little like turning back the clock on cognitive decline – think a two-year rewind button.

The big bucks talk here: we're eyeballing $2 billion in revenue by 2028 and maybe a whopping $4 billion by 2033. And hey, there might even be more where that came from.

Let's chew on a few things here. Biogen has the potential to snag a 60% market share against Eli Lilly’s (LLY) donanemab – the only worthy opponent in the market so far. And given Leqembi's safety creds, this might be playing it safe.

Aside from Eli Lilly, there’s Roche (RHHBY), with candidates in Phase 2 and Phase 1 trials, but they're not quite hitting the jackpot yet. As for other competitors in the space like Regeneron (REGN) and Alnylam (ALNY)? Well, they're cooking up something different in Phase 1, but it's a bit early to call.

Meanwhile, Biogen's got another trick – a home-use version of Leqembi coming this fall. And get this: doctors are buzzing about nipping Alzheimer’s in the bud, way before it crashes the party. Imagine getting a jab of Leqembi as part of your routine check-up when you're only 50. If this works, then we could be kissing Alzheimer’s goodbye by 2040.

For the longest time, Biogen was like that one-hit wonder with its multiple sclerosis treatments. But now, they're swinging for the fences with the largest unmet health need out there. If Leqembi hits it big, and I mean really big, we could be talking about sales far beyond that $4 billion mark by 2033.

But let's not get ahead of ourselves. The big pharma world is about to hit a few speed bumps with a wave of patent cliffs from 2025 to 2029. That’s a headache for the likes of Merck (MRK), Amgen (AMGN), Pfizer (PFE), and Bristol Myers Squibb (BMY).

Biogen, though, is sitting pretty with two growth products and a pipeline that’s got pizzazz. Plus, they're a hot catch for any big pharma looking for a dance partner without stepping on regulatory toes.

As we roll into the next decade, keep your eyes peeled for investment opportunities popping up like daisies. And don't feel like you've got to jump on the first bandwagon that rolls by. This market's just stretching its legs, and today's champs might just be tomorrow's old news.

So, what's the smart play here? Spread your bets across a few horses in the Alzheimer's race, and make sure they're not one-trick ponies.

Eli Lilly, for instance, is more than just an Alzheimer's bet – they're making waves in diabetes and soon, obesity treatments. Biogen, despite its Alzheimer's experience, is a bit of a gamble, especially after its first drug's rocky start.

Remember, investing in Alzheimer's treatments now is like catching the early wave – it's riskier, sure, but the potential for a big payoff is there. This is an emerging market, and it's revving up for an exciting ride. I suggest you add these names to your watchlist.