Mad Hedge Biotech and Healthcare Letter

February 4, 2025

Fiat Lux

Featured Trade:

(TOO RICH TO FAIL, TOO EXPENSIVE TO SUCCEED)

(MRNA), (TSLA), (NVS), (SNY), (JNJ), (BNTX), (RHHBY), (REPL), (CRSP), (ORCL)

Mad Hedge Biotech and Healthcare Letter

February 4, 2025

Fiat Lux

Featured Trade:

(TOO RICH TO FAIL, TOO EXPENSIVE TO SUCCEED)

(MRNA), (TSLA), (NVS), (SNY), (JNJ), (BNTX), (RHHBY), (REPL), (CRSP), (ORCL)

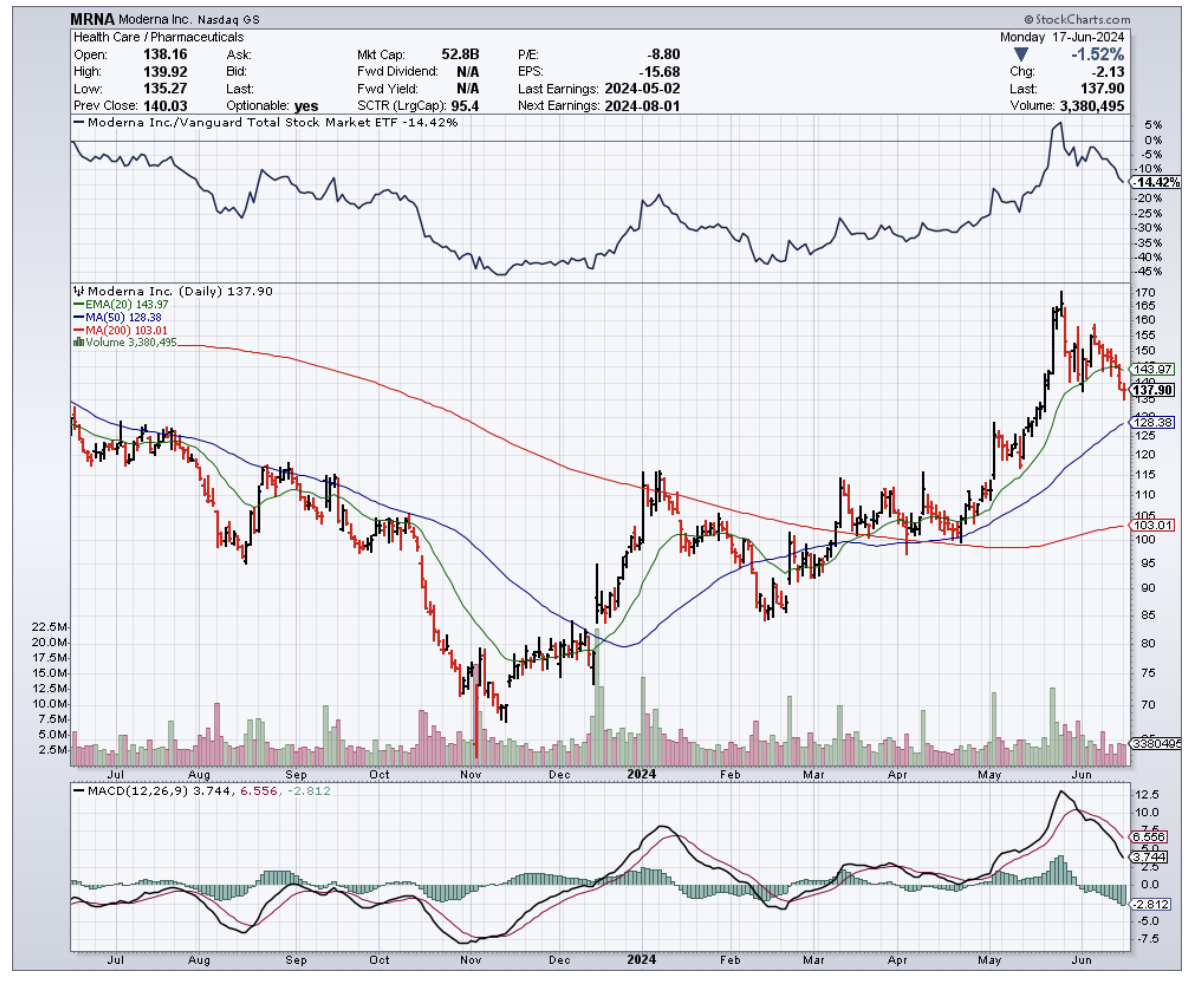

Last weekend, while organizing my home office, I stumbled across an old COVID vaccination card. Remember those? It got me thinking about Moderna (MRNA), the biotech darling that went from relatively unknown to household name faster than you can say "messenger RNA."

Now, in early 2025, this once up-and-coming company is already facing what my grandmother would call "champagne problems" - too much cash to be broke, but burning through it faster than a Tesla (TSLA) on Ludicrous mode.

First, let's talk about this biotech's cash burn. In just nine months of 2024, Moderna torched through over $4 billion - that's the same amount they burned in all of 2023, suggesting their cash cremation rate is actually accelerating.

This acceleration in spending wouldn't be as worrying if they had endless reserves, but their current position shows $7 billion in cash and $2 billion in non-current investments.

The math isn't complex: at this burn rate, their runway is shorter than many investors realize.

The recent Health and Human Services (HHS) grant of $176 million in July 2024 for bird flu research barely registers on their financial statements.

While we've seen about 70 bird flu cases in the U.S. with one fatality in an elderly patient with underlying conditions, this isn't going to be another COVID-style revenue stream.

I've analyzed enough pharmaceutical companies to know that betting on another pandemic windfall is like expecting lightning to strike twice in the same spot.

What really interests me is Moderna's position in the competitive landscape. I spent last week analyzing patent data and geographic reach metrics across the industry.

First, you've got the old-guard pharma giants like Novartis (NVS), Sanofi (SNY), and Johnson & Johnson (JNJ), who have been at this game since before mRNA was a gleam in a scientist's eye.

Then, there are companies like BioNTech (BNTX) and Roche (RHHBY) with significantly higher geographic reach, while Replimune Group (REPL) and CRISPR Therapeutics (CRSP) demonstrate superior application diversity.

In comparison, Moderna's position in this landscape shows relatively low scores on both metrics - not exactly what you want to see from a company burning cash at this rate.

Stéphane Bancel, Moderna's CEO, recently outlined their pipeline: 2 approved medicines, 7 Phase 3 trials, and 45 candidates in development. They're also targeting $1.1 billion in annual R&D cost reductions by 2027.

But here's what keeps bothering me: their SG&A expenses have ballooned to nearly 10 times their pre-COVID levels, yet management is focusing on R&D cuts instead of addressing this administrative bloat.

The insider trading patterns since early 2024 haven't exactly inspired confidence either.

When I see heavy selling from insiders while a company is promising future breakthroughs, I can't help but remember all the biotech stories I've covered where the promise didn't match the reality.

Speaking of promises, Oracle's (ORCL) Larry Ellison recently made headlines talking about 48-hour personalized cancer vaccines using AI and robots.

While the technology sounds promising, I'm more interested in the practical path to profitability. Moderna isn't alone in this race, and their well-capitalized competitors have the luxury of funding similar development programs while maintaining positive cash flow.

Given Moderna's cash burn trajectory, their next three quarters will be telling.

I'll be watching that $4 billion nine-month burn rate closely, along with their progress on cost reductions - particularly those inflated SG&A expenses that management seems reluctant to address.

I'm keeping my old vaccination card as a reminder of Moderna's impressive COVID-19 achievement, but I'm not ready to bet on lightning striking twice.

Sometimes the hardest part of investing is knowing when to appreciate history without banking on its repeat performance.

Mad Hedge Biotech and Healthcare Letter

July 18, 2024

Fiat Lux

Featured Trade:

(FROM GOLDEN EGG TO DUD, AND BACK AGAIN?)

(PFE), (LLY), (NVO), (VKTX), (GILD), (GPCR), (BNTX)

Remember when Pfizer (PFE) was strutting around Wall Street like a rooster in a henhouse, clucking about their $10 billion-a-year weight-loss wonder drug?

Well, that golden egg turned out to be a dud, with safety issues and side effects sending their experimental pills to the scrap heap faster than you can say "clinical trial failure."

Just when we thought Pfizer had thrown in the towel, they're back in the ring, swinging with a new once-daily version of danuglipron and pushing it towards bigger studies.

But let me tell you, the market's about as excited as I am for a vegan BBQ. Pfizer's shares nudged up a measly 0.4% upon announcement, after a brief 2.9% spike that fizzled faster than a diet soda.

Now, let's talk about the 800-pound gorillas in the room: Eli Lilly's (LLY) Zepbound and Novo Nordisk's (NVO) Wegovy.

These weekly jabs are the current darlings of the weight-loss world, but everyone and their grandmother are scrambling to get an oral GLP-1 to market. It's like watching a gold rush, except instead of pickaxes, they're wielding pipettes.

Lilly's got orfoglipron in Phase 3, with data coming faster than a day trader's heartbeat. Novo's already peddling Rybelsus, though it's about as effective as a chocolate teapot compared to the injectables.

And don't forget the up-and-comers: Viking Therapeutics (VKTX), Gilead Sciences (GILD), and Structure Therapeutics (GPCR) are all elbowing for a spot at the table.

Now, I know Pfizer's trying to convince us that their once-daily danuglipron is the bee's knees, with "encouraging pharmacokinetic data." But they're as tight-lipped about side effects as a politician at a press conference.

The research world’s not completely buying it, and frankly, neither am I. We might be waiting until the cows come home - or at least until 2026 - before we see if this pill's worth its weight in gold.

Meanwhile, Pfizer's stock has been sagging like a bulldog's jowls, down 1.5% this year and a gut-wrenching 21% over the past 12 months.

They're also staring down the barrel of a $17 billion revenue nosedive by 2030 as their patents fly the coop faster than pigeons at feeding time.

So, what has Pfizer been doing to deal with these? In recent months, the company has been on an acquisition bender that'd make a Vegas high-roller blush.

They snagged cancer specialist Seagen for a cool $43 billion, aiming to have eight blockbuster cancer drugs by 2030.

They're also playing footsie with BioNTech (BNTX) again, cooking up mRNA goodies like a COVID/flu combo vaccine. And let's not forget their partnership with Flagship Pioneering in the weight loss arena.

Over the past five years, Pfizer hasn’t been shy about spending money, securing over 20 new medicine approvals.

But Wall Street's been about as impressed as a cat with a new toy - they sniff at it and walk away. The stock took a 40% nosedive in 2023, partly thanks to their obesity program face-planting.

Still, Pfizer is not giving up so easily. In fact, they’ve worked to give their lineup a facelift. New approvals are rolling in faster than a greased pig at a county fair, and their pipeline's deeper than a philosopher on a bender.

Now, here's the million-dollar question: Is Pfizer a diamond in the rough or fool's gold? The market overreacted to their COVID-19 vaccine success, and now they might be overcorrecting in the other direction.

For those of you with nerves of steel and the patience of a Zen master, Pfizer could be a steal at these prices. If you don’t have the stomach for it, then I suggest you look elsewhere.

Mad Hedge Biotech and Healthcare Letter

July 16, 2024

Fiat Lux

Featured Trade:

(SMALL GIANTS RISING)

(GMAB), (OPHLY), (VRTX), (INCY), (BIIB), (AHKSY), (ALNY), (ARGX), (BGNE), (MRNA), (NBIX), (BNTX), (IPSEY), (CTLT), (NVO), (LLY), (JNJ), (GILD), (ABBV), (MRK), (SNY), (BMY), (GSK)

Remember when David took down Goliath? Well, history's repeating itself in the biotech arena, and this time, David's got deep pockets and a Ph.D.

Since April, I've been watching a trend on the so-called "next-generation" players in biotech and healthcare world. It reminds me of the massive changes I witnessed in Asian markets back in the '70s.

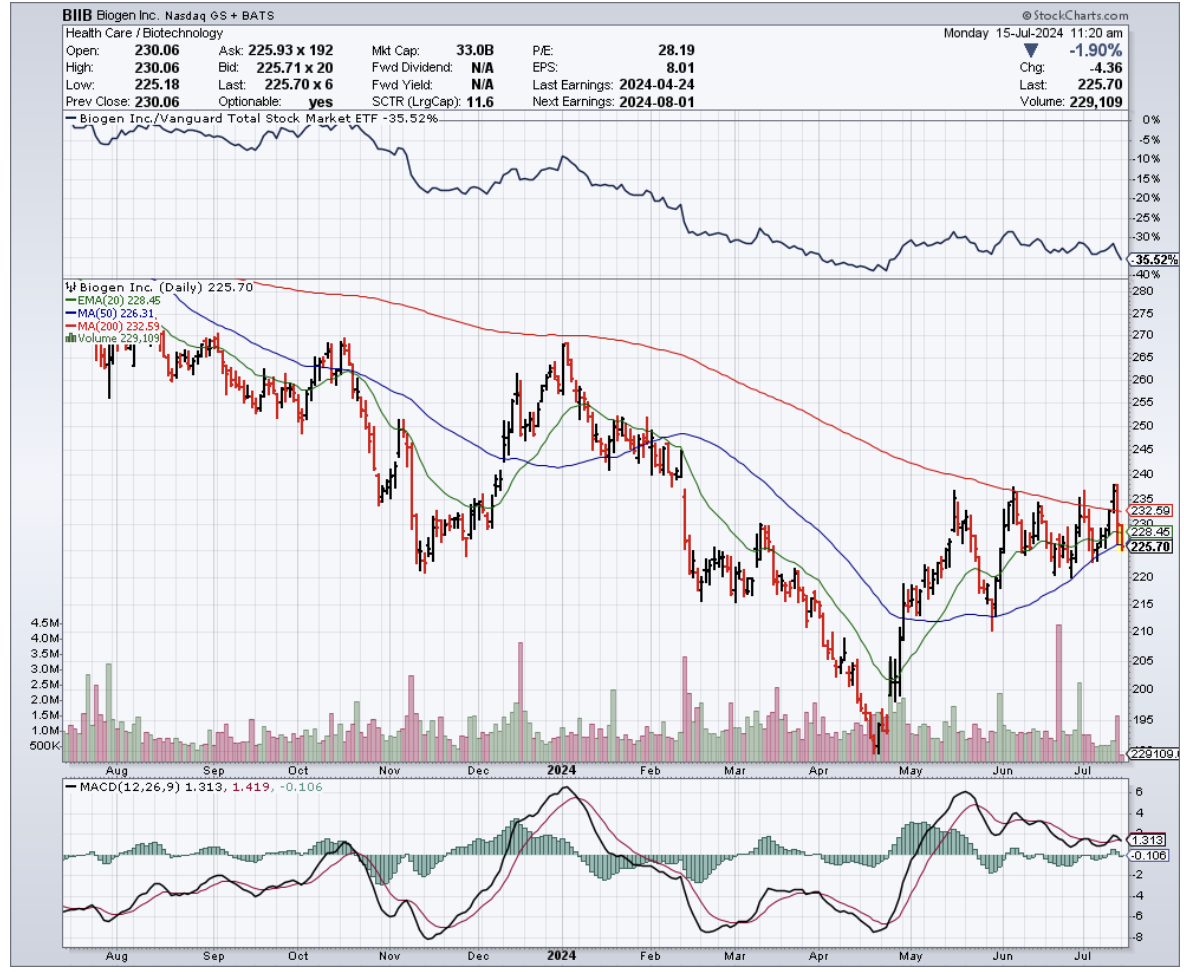

Over the past months, companies like Genmab (GMAB), Ono Pharmaceutical (OPHLY), Vertex (VRTX), Incyte (INCY), Biogen (BIIB), and Asahi Kasei (AHKSY) have been making waves that would impress even the most seasoned surfer. And these next-gen dealmakers aren't just dipping their toes in the M&A pool - they're doing cannonballs.

With cash reserves that would make Scrooge McDuck blush, these companies are overturning industry norms, already joining the prestigious $100 billion market cap club. At this celebration, the champagne flows freely.

So, what’s the play here?

With IPOs cooling down like day-old coffee, companies eyeing public debuts are now ripe targets for acquisition, more tempting than a juicy peach.

This fresh class of biotechs, unphased by the FTC's scrutiny that acts like kryptonite to pharma giants, are acting more like rocket fuel for these agile consolidators.

They slide through regulatory gaps faster than a greased pig at a county fair, grabbing six out of ten biopharma M&A deals in the second quarter alone. They’re not just taking a slice of the pie—they’re rewriting the recipe.

And if we're talking about firepower? These newcomers boast an average of $3.8 billion in pro forma adjusted cash, which isn't just walking-around money — that's "buy a small country" money.

But don't think for a second that this cash is just sitting pretty in their coffers. These upstarts are putting their money where their mouth is.

Take Incyte, for instance. They flexed their financial muscle with a $2 billion buyback in May 2024, sending a clear message to the market: "We're here to play, and we're playing to win."

And that's just the tip of the iceberg. The industry as a whole is lounging on a cool $1.5 trillion. That's enough liquidity to stretch the imagination — perhaps even to purchase a small planet. Mars, anyone? Elon might give us a discount.

But this financial might isn't just about buying power – it's about survival. As I said before, Big Pharma is teetering on a patent cliff that threatens to erode their revenue streams. To stay competitive, they're scrambling to replenish their pipelines, acquiring promising assets and gobbling up innovative technologies with the voracity of Pac-Man on steroids. And it's not just the usual suspects making moves.

This sense of urgency has created a fertile ground for an emerging cohort of aggressive dealmakers. Companies like Alnylam (ALNY), argenx (ARGX), BeiGene (BGNE), Moderna (MRNA), Neurocrine Biosciences (NBIX), BioNTech (BNTX), and Ipsen (IPSEY) are biting off more than the market expected them to chew, and they're coming to the table hungry.

And these companies aren't just nibbling around the edges. They're making bold moves, acquiring cutting-edge biotech firms with promising pipelines. We're talking oncology, epilepsy, kidney diseases, cardiovascular plays – it's like someone turned a medical textbook into a shopping catalog.

In fact, even the big boys are flexing their muscles.

Novo Holdings (NVO) dropped a jaw-dropping $16.5 billion on Catalent (CTLT). That's not even for a drug - it's for manufacturing. Talk about betting on the picks and shovels in this biotech gold rush.

Eli Lilly (LLY) just plunked down $3.2 billion on Morphic Therapeutic (MORF), betting big on inflammation, immunity, and oncology.

Johnson & Johnson's (JNJ) been on a shopping spree, too, snagging Numab's Yellow Jersey for $1.25 billion and Proteologix for $850 million. Both plays in inflammation and immunity - clearly, they've found their sweet spot.

Biogen's not twiddling its thumbs either, striking a deal with HI-Bio worth up to $1.8 billion.

Not to be outdone, Gilead (GILD) shook hands with CymaBay Therapeutics to the tune of $4.3 billion. Even AbbVie (ABBV), playing it cooler, still dropped a cool $250 million on Celsius.

Meanwhile, Merck's (MRK) set its sights on EyeBio for up to $3 billion, focusing on ophthalmology.

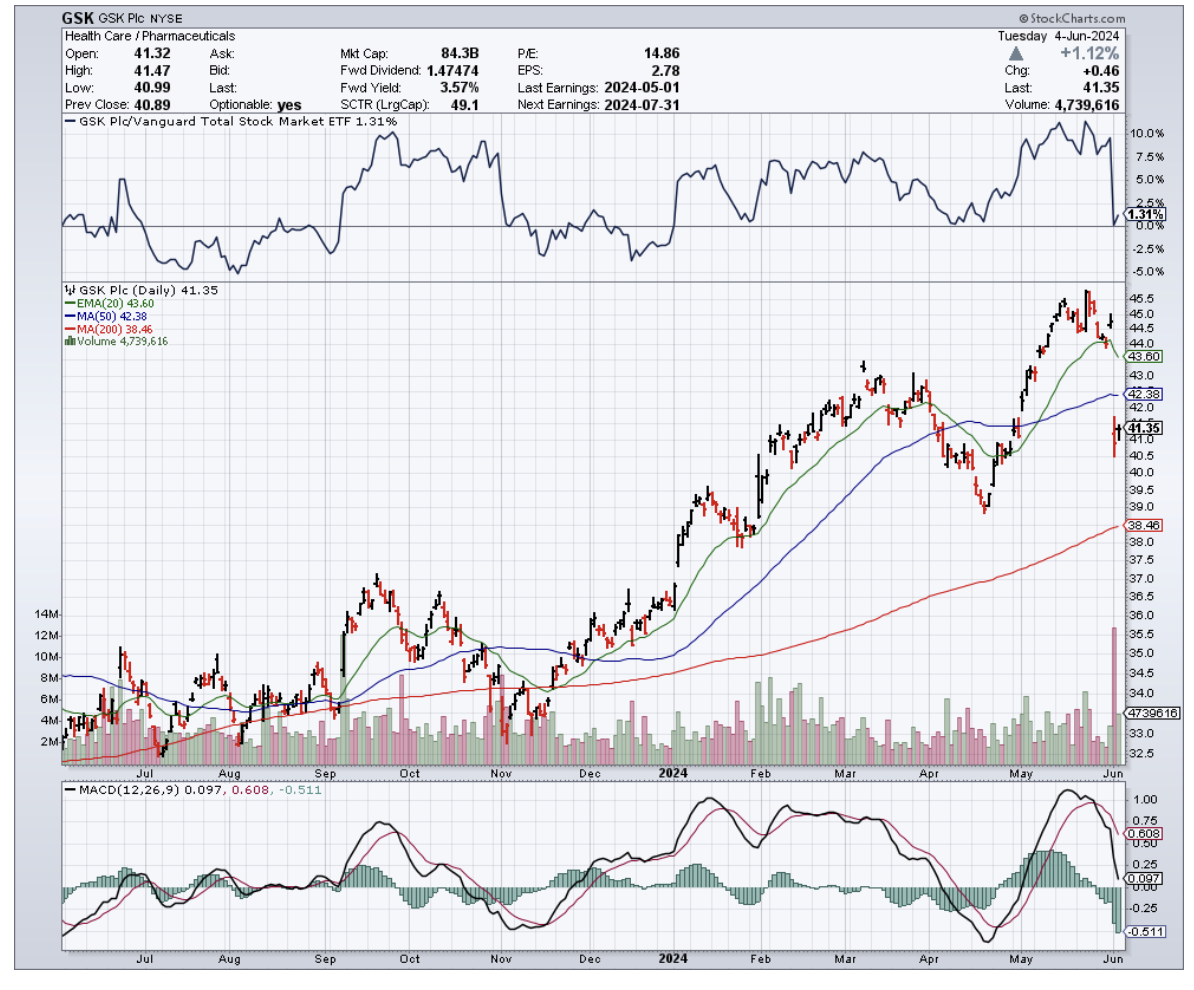

Sanofi (SNY), Bristol Myers Squibb (BMY), GSK (GSK) - they're all in, placing their chips on everything from rare diseases to generics to asthma. Clearly, the Big Pharma giants are also trying to keep up with this shift.

As the biotech field evolves, watching these underdogs will be like watching history in the making — where today's Davids become tomorrow's Goliaths. I suggest you keep a close eye on the names above. Adding them to your portfolio would mean you’re not just watching the giants rise — you’ll be a part of the story.

Mad Hedge Biotech and Healthcare Letter

June 20, 2024

Fiat Lux

Featured Trade:

(VAX TO THE FUTURE)

(AMGN), (RHHBY), (BNTX), (MRNA), (GNCA), (IOVA)

Let's have a heart-to-heart, you and me – about cancer, jabbers, and snake oil. If you think vaccines have been around for a while, you're on the money, my friend.

Over centuries, they've done a bang-up job wrestling down deadly infectious diseases and picking our collective life expectancy off the floor.

But what if I told you there's a different kind of magic we're still waiting for in the world of vaccines?

God's truth, I kid you not, science has been hammering away at this for years: creating vaccines to kick cancer square in the posterior. Yet, like an ardent investor waiting for the grand payoff, we've seen more flops than a fish outta water.

You can count on your one hand the number of cancer vaccines approved by the FDA since that first green-lit in 1990.

Let's not stammer about the bush, it's three – Provenge by Dendreon Pharmaceuticals, Imlygic by Amgen (AMGN), and Tecentriq by Roche (RHHBY).

Meanwhile, our old reliables – chemo, radiation, and the surgeon's knife – have, like battle-weary soldiers, been holding the fort for decades. But even they face formidable foes: nasty side effects, a bill that'll make a Rockefeller blanch and a diminishing punch against advanced cancer.

And the stats tell a story, but it ain't a happy one. Barely 59% of cancer patients treated with standard chemo make it through the five-year mark.

Until now.

Looking back, it's clear we've been a few beans short of a chili in our understanding of how the immune system and tumors get along — or rather, don't.

Now we know these devious cancers have been hoodwinking us with a starter kit of escape tools, literally tricking the immune system into playing “hide and seek.”

That’s where the likes of BioNTech (BNTX), Moderna (MRNA), Genocea (GNCA), and Iovance (IOVA) come in. To date, there are over 350 clinical trials focused on this field.

And if these new kids on the block deliver, we'll be singing hallelujahs with 83% five-year survival odds instead of the grim 59% chemo gives us.

As for those already in late-stage battles, where chemo only offers a bleak 4% five-year survival, immunotherapy could boost that to 23%.

So, what's the game-changer? Immune-modulating cancer vaccines.

Unlike traditional treatments that attack cancer cells directly, these vaccines train your immune system to recognize and destroy cancer cells like a well-trained bouncer booting out unruly party crashers.

Contrasted to the old brute force methods like chemo, and trust me, I’ve had some friends go through that ordeal, these vaccines are more like a sniper - taking precise aim only at cancer cells.

Plus, side effects? Minimal, my friends. But the cherry on top? These vaccines could potentially be your long-term bodyguards against cancer.

Now, I'm sure you love crunching numbers as much as I do, so here's some food for thought - the global cancer vaccine market was worth a cool $4.06 billion in 2019 and is projected to triple to $12.85 billion by 2027.

I mean, come on, that's a compound annual growth rate of 17.4%. It’s like watching your favorite sports team go on a championship run, season after season.

And the broader cancer immunotherapy market, sitting pretty at $75 billion in 2022, is on track to hit $120 billion by 2030, boasting a 14% CAGR.

These are not just empty promises either. We're seeing real progress - BioNTech and Moderna are developing personalized cancer vaccines that target unique tumor antigens.

Then there’s Genocea and Iovance, busy rolling out “off-the-shelf” cancer vaccines like fresh donuts off a conveyor belt.

This is a critical development, as around 70% of cancer patients develop resistance to chemotherapy.

These new immunotherapy contenders, with an overall survival rate of 50% compared to just 22% for those resistant to chemo, with every single patient potentially scoring against the dreaded C, and not fretting about chemoresistance. Talk about a fighting chance.

Overall, I think the cancer vaccine field is the Wild West of biotech – exciting, unpredictable, and potentially very rewarding. With companies pouring money into R&D, fueled by rising cancer rates and expedited FDA approvals, the race is on.

Immune-modulating cancer vaccines might just be the sheriff that this Wild West of cancer treatment needs, flipping the script on what used to be a death sentence into something we can manage.

Now, I'm not saying you should throw all your eggs in one basket, but keep a close eye on those mavericks like BioNTech, Moderna, Genocea, and Iovance. They could be the dark horses in this race.

Add them to your watchlist, and when the market hiccups and those share prices dip, that could be your chance to get a piece of the action.

Mad Hedge Biotech and Healthcare Letter

June 11, 2024

Fiat Lux

Featured Trade:

(THE CAPITAL CURE)

(ABBV), (MRK), (PFE), (RHHBY), (JNJ), (AZN), (GSK), (MRNA), (BNTX), (CRSP), (NTLA), (BEAM), (TPTX), (ZNTL), (MRTX), (BPMC), (MGNX), (TYRA), (SPRT), (VRTX), (FOLD), (RARE), (CRBU)

Imagine you're the CEO of a major pharmaceutical company. You've got blockbuster drugs that are raking in billions, a cushy corner office, and a corporate jet at your disposal. Life is good.

But then, you look at the calendar and realize that your patents are about to expire. Suddenly, that jet feels more like a crop duster, and your corner office starts to feel like a broom closet.

That's the reality facing Big Pharma right now. These pharma big shots are sweating bullets over losing their golden geese like AbbVie's (ABBV) Humira and Merck's (MRK) Keytruda.

That’s roughly $300 billion in products about to get kicked to the curb.

But these guys didn't get to the top by sitting on their hands. They've got a war chest of $1 trillion, and they're not afraid to use it.

Major pharmaceutical giants like Pfizer (PFE), Roche (RHHBY), Johnson & Johnson (JNJ), AstraZeneca (AZN), and GlaxoSmithKline (GSK) are about to go on the mother of all shopping sprees.

Why the rush? Because they're staring down the barrel of a patent cliff that's going to make the Grand Canyon look like a pothole.

We're talking $198 billion worth of branded drugs going off the patent cliff between 2021 and 2025. That's a gut-wrenching 56% jump from the last five years.

But don't think for a second that they're just going to sit back and watch their profits go up in smoke. No sir, they're on the hunt for the next big thing, and they've got their sights set on some juicy targets – and biotech is at the top of their list.

Leading the biotech charge are mRNA pioneers Moderna (MRNA) and BioNTech (BNTX), each sitting on a gold mine of potential blockbusters taking on everything from flu to cancer vaccines.

Underdogs like CRISPR (CRSP) biotech stars Intellia (NTLA) and Beam Therapeutics (BEAM) are also squarely in Big Pharma's acquisition crosshairs for their cutting-edge work in genetic disease treatments.

But beyond the headliners, don't overlook the sleeper hits that could catalyze the next big boom.

Oncology, in particular, is a prime hunting ground, accounting for 37% of pharma M&A deal value in 2023 as the $392 billion global cancer drug market continues to boom.

Companies like Turning Point Therapeutics (TPTX) and Zentalis Pharmaceuticals (ZNTL), with their promising targeted therapies for various solid tumors, are particularly attractive prospects.

Mirati Therapeutics (MRTX), focused on KRAS inhibitors, and Blueprint Medicines (BPMC), specializing in precision therapies, have also caught the eye of big pharma with their innovative approaches.

Additionally, companies with late-stage assets like MacroGenics (MGNX), Mereo BioPharma (MREO), and Tyra Biosciences (TYRA) could offer promising near-term revenue opportunities for acquiring companies looking to bolster their oncology portfolios.

Close behind are rare disease treatments, snagging 16% of new drug approvals and 9 of the top 100 deals last year in this $262 billion market ripe for more growth.

This lucrative sector has captivated pharma giants, who see potential in companies like Sarepta Therapeutics (SRPT) and Vertex Pharmaceuticals (VRTX), leaders in rare disease therapies with strong financial performance and consistent growth.

Aside from these, smaller biotechs like Amicus Therapeutics (FOLD) and Ultragenyx Pharmaceutical (RARE), focused on developing innovative therapies for a range of rare diseases, are attracting attention for their potential to address unmet medical needs and deliver substantial returns on investment.

But the real wild card everyone wants a piece of is cell and gene therapies. This medical Wild West is projected to explode to $66.8 billion by 2030, with the FDA already greenlighting 6 cutting-edge therapies like next-gen CAR-T treatments from Caribou Biosciences (CRBU) in 2023 alone.

Notably, the buying frenzy is very much already underway. In fact, 2023 saw the biggest biotech M&A spree in a decade, with a staggering $122.2 billion changing hands as the FDA approved 50% more new therapies.

Pharma mega-mergers also hit $135.5 billion as firms raced to reload pipelines.

Interestingly, these deals are only the tip of the iceberg. As Wall Street predicts, with record-smashing deals, sky-high demand, and new approvals surging, "biotech's got plenty of reasons to be cautiously optimistic."

Especially if interest rates finally cooperate, throwing gasoline on the M&A bonfire and making biotech the belle of the ball as soon as late 2024.

So keep your eyes peeled and your powder dry. I suggest you add these innovative biotech names to your watchlist, and you might just discover the next blockbuster drug or breakthrough therapy that could reshape medicine – and deliver explosive returns in the process.