Global Market Comments

December 7, 2021

Fiat Lux

Featured Trade:

(GET READY TO TAKE A LEAP BACK INTO LEAPS),

(AAPL), (BRK/B)

(TESTIMONIAL)

Global Market Comments

December 7, 2021

Fiat Lux

Featured Trade:

(GET READY TO TAKE A LEAP BACK INTO LEAPS),

(AAPL), (BRK/B)

(TESTIMONIAL)

Global Market Comments

September 24, 2021

Fiat Lux

Featured Trade:

(TESTIMONIAL)

(SEPTEMBER 22 BIWEEKLY STRATEGY WEBINAR Q&A),

(TLT), (TBT), (V), (AXP), (MA), (FSLR), (SPWR), (USO), (UNG), (PFE), (JNJ), (MRNA), (MS), (JPM), (FCX), (X), (FDX), (GLD), (UPS), (SLV), (AAPL), (VIX), (VXX), (UAL), (DAL), (ALK), (BRK/B), (BABA), (BITCOIN), (ETHEREUM), (YELL)

Below please find subscribers’ Q&A for the September 22 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon Valley.

Q: When’s the United States US Treasury bond fund (TLT) going to go down?

A: When J. Powell tapers, which will be either today or in 6 weeks. That's the time frame we’re looking at now, and people are positioning now for the taper—that's why financials are taking off like a rocket. Buy those financials and don't expect too much from your tech stocks for the next few months.

Q: What do you think of adding corporate or municipal bonds to my portfolio?

A: Don’t do that on pain of death please; you will lose money. Corporate bonds will get slaughtered the second interest rates turn because they have the most exposure from a credit point of view to any downgrades resulting from rising interest rates. Better to keep your money in cash than buy bonds here. It was a great idea 10 years ago, but a terrible idea today. Just buy cash or buy extremely deep-in-the-money LEAPS which will get you a 10-20% per year return.

Q: What are the chances that the government defaults?

A: Zero, because corporate profits this year will increase from $2 trillion to $10 trillion, spinning off massive tax revenues for the government. The deficit will come down substantially in the future as a result. Keep expecting upwards surprises in profits and taxable revenues. That may be why the (TLT) is staying so high.

Q: I need a customized LEAPS on a stock.

A: We do those for our concierge customers. If you’re interested, then email Filomena at customer support at support@madhedgefundtrader.com.

Q: What brand of shot did you get?

A: Pfizer (PFE).

Q: The Government is showing no sign of balancing a budget and the hole will only get deeper; what are your thoughts?

A: I agree, and that’s why I'm short the (TLT). All we need is a taper to really get some juice under that trade; we really don’t need that much. Ten-year US Treasury yields are now around 1.30% and we only need the yield to get up to about 1.70% for us to make a maximum profit on our positions. One taper hint and it could get us up to those levels.

Q: Why is Visa (V) dropping so much?

A: Fear of being replaced by Bitcoin. This is the big thing dragging all three credit card companies down, including American Express (AXP) and master Card (MA). That's why I have not added a Visa position among my financials in this go around.

Q: How can the Fed unwind their balance sheet and normalize interest rates to a historical average of 4-5%?

A: Quite easily: quit buying bonds. They’re still buying $120 billion/month worth. Technology has accelerated with the pandemic and we all know this is highly deflationary. I expect the next peak in interest rates to be only 3% or 3.5%, not the 6% we saw in the last peak in interest rates in the 2000s. So yeah, bonds are going to go down but not back to 2000’s level.

Q: Thoughts on the Johnson & Johnson (JNJ) shot?

A: No thank you. If you get to choose, Moderna (MRNA) is now producing the best immunity data on a year-to-date basis if you’re starting out from scratch. Some people are mixing, they start out with Pfizer and then get Moderna. They get a worse reaction because the Moderna initial reaction shot sees the Pfizer vaccine as a new virus, so you may get a small flu as a result of that.

Q: What is the put spread you’re recommending on the TLT?

A: The May 2022 $150-$155 vertical put spread. That is the sweet spot now on the short side on (TLT) LEAPS. You should earn a 115% profit in eight months on this trade if interest rates remain unchanged or fall.

Q: Do you expect the ProShares Ultra Short 20 year+ Treasury ETF (TBT) to make it to $20 this year?

A: Yes, I do; $16 to $20 isn’t that much of a move. Remember, the (TBT) is a two times short ETF.

Q: Are you recommending bank stocks?

A: Yes, Morgan Stanley (MS) and JP Morgan (JPM) are two of the best. They will lead the yearend rally starting from here.

Q: When do you expect the semiconductor shortage to end?

A: End of next year, or maybe even 2023, because what all the analysts keep underestimating is that the end of shortages is based on companies getting the chips they want today. The actual issue is that companies are designing billions of chips into their products at an exponential rate, and what they’ll need in a year from now is far higher than most people realize. The semiconductor shortage is much more structural than people realize—that's my theory. They don’t throw up a $2 billion fab overnight. So, this will keep going on for a while and be a drag on economic growth.

Q: Are you sure we won’t see $100 oil (USO)?

A: With oil, you're never sure about anything, although I highly doubt it. We’d have to have monster economic growth in China to get oil up to $100 a barrel. Right now, China is going the other way.

Q: What’s your view on the debt ceiling? Will it give us a good buying opportunity?

A: Probably not, our good buying opportunity was yesterday or Monday. These debt crises are always one minute before midnight solutions. They always get solved. Never underestimate the ability of Congressmen to spend money in their own district. So, I don’t think that would create a stock market crash like it might have done 20 years ago.

Q: What about Freeport McMoRan (FCX)?

A: It’s taking a dip here because of a possible real estate crash in China, and of course China is the world’s largest buyer of copper for apartment construction. I’m kind of taking a break here on Freeport McMoRan and US Steel (X) until we learn a little more about the China situation. They did move to start a bailout today. Let’s see if that continues.

Q: When will the airlines come back?

A: They’ll come back when business travel returns, which I think could be next year. If you eliminate the virus completely, these things double easily. That's the bet you’re making. Let’s see if the covid boosters work, the childhood shots work, and then you can take another look at Delta (DAL) and Alaska (ALK).

Q: If Bitcoin gains mass adoption, does that put banks out of business just like electric vehicles are making oil obsolete?

A: No, not if the banks go into the Bitcoin business. And the banks actually have the cash, resources, and infrastructure to take over the Bitcoin area once the technology matures. And the corollary to that is that the oil industry is that the majors have the infrastructure, the manpower, and the capital to take over the alternative energy business if they choose to do so and oil goes to zero, which it eventually will. The proof of that is the largest investor in all the Silicon Valley energy startups are Saudi Arabian venture capital funds. They’re huge investors in solar here. If Saudi Arabia has a lot of oil, they have even more solar. Believe me, I’ve been there.

Q: Will a lack of inventory and rising interest rates end the bidding wars on houses soon?

A: Only if you consider 10 years soon. That is how long it will take for the sizes of different generations to come into balance, the Millennials (85 million) versus the Gen Xers (45 million). That’s when the housing bubble will end, but that won’t be for another decade. We still have a structural shortage of new home construction (about 5 million units a year) because all the home builders who went bust in the financial crisis in 2008/2009 and never came back—all of that new construction is still missing. And the surviving ones haven’t increased production to meet that shortfall because they want to manage their risk. Eventually, they will and that probably will be the next top, but that’s really 2030 type business.

Q: What about Federal Express (FDX)?

A: Labor shortages. It's hitting (UPS), (FDX), the Post Office, and DHL too—all the couriers.

Q: When do you think gold (GLD) and silver (SLV) rise back to 2,000?

A: I am avoiding gold and silver as long as Bitcoin has buyers. The action in Bitcoin is 10x the movement you get in gold and that’s attracted all the speculative capital in the market, draining all interest from gold, which hit a new six-month low just last week.

Q: What’s your buy target for Apple (AAPL)?

A: I would say if you can get it at $135, that would be a gift. We did get close to $140 at the lows this week; that’s when you start nibbling, and then you double up again at $135. I doubt Apple is going down more than 10% in this cycle. There are too many people still trying to get into it. And they’re still the largest buyer of stock in the world. They only buy one stock, their own.

Q: I never got any IPath Series B S&P 500 VIX Short Term Futures ETN (VXX) alerts.

A: That's because we never sent any out. (VIX) has become an incredibly difficult game to play, accumulating positions for months and then trying to get out on a one-day spike that lasts a few minutes. The insiders have too much of a house advantage here, who only play from the short side. There are too many better fish to fry.

Q: What about the Apple electric vehicle?

A: I’ll believe it when I see it; I've been hearing about this for something like seven years. My guess is that Apple is more likely to supply consoles and parts to other EV makers and help them get into the game with software and so on. I think that will be Apple's role in all of this.

Q: How much has China Evergrande Group stock fallen?

A: It’s a really illiquid stock in China so we never got involved in it. I think it’s down more than half. Even the professional short-sellers like Jim Chanos and Kyle Bass, have been targeting that stock for 10 years are now screaming they’re vindicated. Of course, they lost fortunes in the meantime. So, I'll pass on that one.

Q: What about stop losses on LEAPS trades?

A: I don’t really run LEAPS portfolios or issue stop losses. The idea is to run these into expiration, and we’ve never had one expire out of the money, although I may break that record if TLT doesn’t turn around in the next three months.

Q: How would autonomous trucking impact rail transportation?

A: They’re two totally different things. Trucking companies like Yellow Corporation (YELL) carry smaller cargo for local deliveries or small long-distance deliveries. 7Some 70% of all railroad traffic is coal going to China, and the rest is bulk commodities like wood chips, iron ore, etc. Trucks don’t carry any of that, so they’re totally separate businesses. But, if we went totally autonomous on trucking, it would make all the main trucker companies massively profitable, as they get rid of their drivers. Right now, every trucking company in the US has a driver shortage.

Q: United Airlines (UAL) pilots are now ordered to get vaccinated.

A: I think within months to hold a job anywhere in the US, you will have to get vaccinated. They do not want you in the office without a vaccination. Jobs are not worth risking lives, and we hit 2,000 deaths again yesterday. The corporations are taking the lead, not the government. The exception will be the politically motivated companies, like the My Pillow Guy; I doubt they'll ever require vaccinations at My Pillow. And there are a few other companies such as Hobby Lobby that are also anti-vaxers. But all public transport companies, hospitals, etc., are going to say get vaccinated or get out—it’s very simple.

Q: Should I buy Berkshire (BRKB) here?

A: Yes, it’s a great entry point, even if you can't get my price. Go higher in the strikes or go farther out in maturity.

Q: Is copper metal (CPER) a buy here?

A: Probably long term, but short term will be subject to the whims of the Chinese real estate crisis if there is one.

Q: Won’t Natural Gas (UNG) outperform in the power grid since all EVs must be charged?

A: Not if the grid is 100% electric. Natural gas still has carbon in it, although only half as much as oil or gasoline. I think even natural gas eventually gets phased out because you can expect solar panels to improve by 80% over the next ten years. At that point, any other energy source won’t be able to compete—oil, natural gas, you name it. And that is why you don’t see any long-term money going into carbon energy sources.

Q: Iron ore has just gone from $200 to $100, why are you bullish?

A: Yes, Because it has just gone from $200 to $100. Eventually, China recovers, despite a short-term financial and housing crisis. Buy low, sell high—that’s my revolutionary new strategy.

Q: What are your thoughts on Bitcoin vs Ethereum?

A: I think Ethereum will outperform Bitcoin because it has a more modern technology. It’s only six years old, vs 12 years for Bitcoin. It’s also more efficient, using less energy in its production. In fact, we did get a double in Ethereum in August as opposed to only a 50% move in Bitcoin.

Q: Do you have any concerns on holding the financials through earnings in October?

A: No, I think the results will be fantastic, and I want to be long going into those.

Q: What does the current situation with China mean for Alibaba (BABA)?

A: Keep your stocks, you’ve already taken the hit—down 53%. The next surprise is that China quits beating up on capitalism and these things will all recover bigtime. However, any options you may have could expire before that happens. So, keep the stocks, get rid of the options, salvage whatever time value you can, and then wait for China to start doing the right thing.

Q: What are the best solar stocks?

A: First Solar (FSLR) and SunPower (SPWR), which have both done great.

Q: If bonds are a no-no, and governments are getting more indebted than ever, who will buy them?

A: Governments. The only buyers of bonds now are non-economic buyers. Those would be governments, central banks, and banks who are required by law to own certain amounts of bonds to meet regulatory capital requirements. No individual in their right mind is buying any bonds here at all, nor is any financial advisor recommending them.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

April 6, 2021

Fiat Lux

FEATURED TRADE:

(HIGH-YIELD STOCK UP FOR GRABS)

(ABBV), (PFE), (BRK.B), (BLK)

Something curious is happening at the FDA, and it’s causing investors to be jittery. Drugs that are sure to gain approval keep encountering roadblocks.

What began as a handful of biotechnology stocks getting trampled is turning out to be a broader pullback caused by fears of a tougher and stricter regulatory environment for drug developers.

Following these changes, the SPDR S&P Biotech (XBI) slid by roughly 12% this month.

The idea that the somewhat predictable regulatory results in the past four or five years may no longer be as predictable obviously ramped up the perceived riskiness of this industry.

One bellwether of this change is AbbVie (ABBV), which submitted an application for the expanded use of rheumatoid arthritis Rinvoq in March. It recently announced that the regulatory board is extending the evaluation for three months.

While this isn’t a cause for alarm, it’s enough to unsettle some investors since Rinvoq is expected to replace AbbVie’s blockbuster drug Humira when the latter loses its patent exclusivity in 2023.

However, the reason behind FDA’s extension is likely because of the safety concerns found in a similar drug, Xeljanz, by Pfizer (PFE).

Considering the similarities of the two, it makes sense for the regulatory board to exercise more caution on AbbVie’s product.

The rise and fall of AbbVie has always centered on Humira, with this top-selling drug raking in $19.8 billion in sales in 2020 alone. That’s actually lower than its usual revenue a few years back.

Humira’s loss of exclusivity is projected to result in medium-term headwind to the company as more and more biosimilars pressure revenue.

However, AbbVie has been working on offsetting the estimated losses by expanding its other programs.

For instance, the revenue for AbbVie’s non-Humira immunology sector, led by Skyrizi and Rinvoq, is projected to double to reach $4.6 billion in 2021.

By 2025, AbbVie expects Rinvoq and Skyrizi sales to reach $15 billion annually.

Meanwhile, a considerable uptick is anticipated from its neuroscience division’s revenue, led by Vraylar, to generate $5.7 billion in 2021.

As for its hematologic oncology franchise, spearheaded by Imbruvica and Venclexta, this sector’s revenue is expected to increase in double digits to reach $7.5 billion this year as well.

On top of these, AbbVie has been busy looking for suitable acquisitions to diversify its revenue stream.

A notable deal it made was in 2015 with Pharmacyclics. This acquisition actually added the mega-blockbuster drug Imbruvica to AbbVie’s portfolio.

In May 2020, AbbVie completed its deal to purchase Allergan. This $63 billion merger is expected to boost the global distribution capacity of AbbVie and bolster its therapeutic sales channels.

By 2023, sales of the products acquired from Allergan’s pipeline are estimated to add at least $2 billion to AbbVie’s annual revenue.

All in all, these sectors are all well-positioned to substantially offset the fall of Humira’s revenue thanks to the rapid growth and aggressive indication expansion efforts of the company.

Nonetheless, the anxiety of the delayed FDA approval for Rinvoq’s expanded use is understandable.

After all, AbbVie expects this particular drug to contribute to doubling the 2021 sales of the franchise from $2.3 billion to $4.6 billion.

Moreover, this is a cornerstone in the company’s post-Humira era in less than two years.

However, the three-month delay will have a minimal impact on the 2021 revenues of the company and a negligible effect when we consider the long term.

Realistically, this would cost AbbVie roughly less than $1 billion in sales, which amounts to less than 2% of the total projected revenues of the company this year.

During times like these, it’s crucial to remember that the pharmaceutical industry is an extremely bumpy road.

There’s no such thing as a linear progression in this line of business, which is why it’s vital to choose companies with established track records and highly capable management teams.

If it helps ease any anxiety, then it might be useful to think that AbbVie is a favored stock by Warren Buffett’s Berkshire Hathaway (BRK.B).

The Oracle of Omaha currently holds 4.27 million shares of this company. Meanwhile, BlackRock (BLK) holds 2.41 million shares, while Ken Griffin’s Citadel Advisors has 786,000 shares.

AbbVie is a mature, larger-cap biopharmaceutical stock that’s selling at an affordable price these days.

Despite the revenue declines and plunges in earnings of countless businesses in 2020, AbbVie still managed to deliver strong operating and financial results—and the company still has a long way to go.

AbbVie is expected to deliver at least 4.8% in annual earnings growth over the course of the next five years—a highly conservative estimate considering that the company reported 21.9% growth in the past five years.

Moreover, AbbVie is safely positioned to deliver 6% long-term annual dividend growth.

AbbVie was able to generate 3.3% growth in its operational revenue in 2020, recording $45.804 billion in net revenues.

In the past weeks, I’ve seen AbbVie shares go down by roughly 6%. However, I think the fear here is exaggerated and the market might be overreacting to the uncertainty caused by stricter FDA guidelines.

Instead of letting the anxiety take control, I believe it’s best to heed the advice of Warren Buffett in this situation: “The market is a device for transferring money from the impatient to the patient.”

Therefore, I think patient investors should take a look at AbbVie stock today.

Mad Hedge Biotech & Healthcare Letter

February 18, 2021

Fiat Lux

FEATURED TRADE:

(WARREN BUFFETT’S BIOPHARMACEUTICAL BETS)

(MRK), (ABBV), (BMY), (PFE), (NKTR), (VZ), (CVX), (AAPL), (BRK.B)

Aside from the recent big moves involving Verizon Communications (VZ), Chevron (CVX), and Apple (AAPL), Warren Buffett has also been busy with biopharmaceutical stocks.

Just before 2020 ended, Berkshire Hathaway (BRK.B) made notable changes in its positions particularly in Merck (MRK), AbbVie (ABBV), Bristol-Myers Squibb (BMY), and Pfizer (PFE).

Berkshire boosted its investment in Merck by 28.1% to reach 28.7 million shares.

Meanwhile, its AbbVie holdings were increased by 20% to hit 25.5 million shares.

It also added 11.2% in its investments in Bristol, totaling to 33.3 million shares.

In contrast, the company cut 3.7 million shares from its Pfizer holdings.

In terms of growth potential, these biopharmaceutical companies hold the most promising prospects in the next decade.

Merck, hailed as a vaccine stalwart, is behind the blockbuster cancer treatment Keytruda.

For context, Keytruda generated $14.4 billion in sales in 2020 alone.

Despite fears over the expiring patent exclusivity of this drug, the company still trades at roughly 11.5 times earnings and is actually projected to achieve 11% long-term EPS growth rate.

Merck also continues to leverage Keytruda in the development of the next generation of treatments in its pipeline.

In fact, the company recently sealed a clinical collaboration with Nektar Therapeutics (NKTR) to assess the effectiveness of Keytruda when combined with Nektar’s own bempegaldesleukin in the treatment of squamous cell carcinoma.

Other than expanding its oncology sector, Merck has been developing its animal health business as well. So far, this particular segment has grown by 7% year over year, reaching $4.7 billion in 2020.

If things work out, then Merck could emerge as a huge competitor against Pfizer’s own animal healthcare spinoff, Zoetis (ZTS), in the future.

To date, Merck has at least 31 candidates in Phase 2 trials and 25 more undergoing Phase 3 studies.

Needless to say, these will be valuable in enriching the company’s lineup especially with the challenges that Keytruda will face in the next years.

As for AbbVie, this company trades at approximately 8.3 times the earnings estimated in the next 12 months. This is well below its five-year average of 10.4 times earnings.

However, the company is projected to show at least 13% EPS growth rate in the long term.

Despite the challenges of 2020, with the company going down 2.6%, the long-term prospects for AbbVie remain positive.

Although AbbVie broke through the dermatology market following its acquisition of Botox-maker Allergan in the past year, it still has to contend with a major problem: arthritis medication Humira.

Humira is not only AbbVie’s top-selling treatment but also the best selling drug in the world today.

In 2020 alone, this anti-inflammatory treatment raked in $19.8 billion in sales. However, AbbVie might soon lose this edge since its exclusive rights to Humira in the US will expire in 2023.

Amidst the anxiety over this issue though, AbbVie continues to defy expectations.

Last year, the company reported a 65.9% growth in its net revenue despite the overall slowdown caused by the pandemic.

As for 2021, AbbVie is anticipating an even better year thanks to its portfolio diversification efforts.

To date, the company’s lineup now spans neuroscience, immunology, eye care, women’s health, and of course, aesthetics.

Meanwhile, Bristol Myers has been pegged to achieve roughly 8% growth rate in the long term. Right now, the stock trade at 7.9 times earnings estimated over the next 12 months.

Like AbbVie and Merck, Bristol has been dealing with patent expiration issues—a problem that pushed its stock down by 4.1% so far this year.

One of the major updates involving Bristol is its massive $74 billion acquisition of Celgene in 2019.

While the deal raised a lot of eyebrows at the time, it brought cancer blockbuster Revlimid into the company’s fold.

Revlimid, which still enjoys protection from a flood of generics for a few more years, has been pumping up sales for Celgene nonstop for over a decade. The drug is expected to generate the same, if not higher, profits for Bristol.

Two more blockbuster drugs in Bristol’s lineup are facing impending patent exclusivity issues, Opdivo, which would expire in 2028, and Eliquis in 2026.

Nonetheless, the positives outweigh the negatives for Bristol. After all, this company invested so much in diversification.

Sales of Opdivo, Revlimid, and Eliquis continued to trend upwards last year.

Opdivo alone managed to generate $7 billion in annual revenue, prompting Bristol to expand the indications for this product.

However, the more promising news lies in the updates that the recently launched products, like multiple sclerosis drug Zeposia and anemia treatment Reblozyl, are gaining traction in the market.

Thanks to the development of its pipeline, the company expects that its new product lineup would account for roughly 27% of its total revenues by 2025.

Overall, Berkshire’s choice of biopharmaceutical companies are offering promising growths in the next several years despite the setbacks they are facing today.

While some investors get alarmed over negative updates, it looks like the Oracle of Omaha is following his own advice: “Whether we're talking about socks or stocks, I like buying quality merchandise, when it is marked down.”

Global Market Comments

February 10, 2021

Fiat Lux

Featured Trade:

(GET READY TO TAKE A LEAP BACK INTO LEAPS),

(AAPL), (BRK/B)

(TESTIMONIAL)

Just as every cloud has a silver lining, every stock market crash offers generational opportunities.

In a month or two, there will be spectacular trades to be had with LEAPS. What are LEAPS, you may ask?

This is the best strategy with which to cash in on the gigantic market swoons, which have become a regular feature of our markets.

Since the advent of the recent incredible market volatility, I have been asked one question.

What do you think about LEAPS?

LEAPS, or Long Term Equity Anticipation Securities, are just a fancy name for a stock option spread with a maturity of more than one year.

You execute orders for these securities on your options online trading platform, pay options commissions, and endure option like volatility.

Another way of describing LEAPS is that they offer a way to rent stocks instead of buying them, with the prospect of enjoying years’ worth of stock gains for a fraction of the price.

While these are highly leveraged instruments, you can’t lose any more money than you put into them. Your risk is well defined.

And there are many companies in the market where LEAPs are a very good idea, especially on those gut-wrenching 1,000 point down days.

Interested?

Currently, LEAPS are listed all the way out until August 2023.

However, the further expiration dates will have far less liquidity than near month options, so they are not a great short-term trading vehicle. That is why limit orders in LEAPS, as opposed to market orders, are crucial.

These are really for your buy-and-forget investment portfolio, defined benefit plan, 401k, or IRA.

Because of the long maturities, premiums can be enormous. However, there is more than one way to skin a cat, and the profit opportunities here can be astronomical.

Like all options contracts, a LEAP gives its owner the right to "exercise" the option to buy or sell 100 shares of stock at a set price for a given time.

LEAPS have been around since 1990, and trade on the Chicago Board Options Exchange (CBOE).

To participate, you need an options account with a brokerage house, an easy process that mainly involves acknowledging the risk disclosures that no one ever reads.

If a LEAP expires "out-of-the-money" – when exercising, you can lose all the money that was spent on the premium to buy it. There's no toughing it out waiting for a recovery, as with actual shares of stock. Poof and your money is gone.

LEAPS are also offered on exchange-traded funds (ETFs) that track indices like the Standard & Poor's 500 index (SPY) and the Dow Jones Industrial Average (INDU), so you could bet on up or down moves of the broad market.

Not all stocks have options, and not all stocks with ordinary options also offer LEAPS.

Note that a LEAPS owner does not vote proxies or receive dividends because the underlying stock is owned by the seller, or "writer," of the LEAP contract until the LEAP owner exercises.

Despite the Wild West image of options, LEAPS are actually ideal for the right type of conservative investor.

They offer more margin and more efficient use of capital than traditional broker margin accounts. And you don’t have to pay the usurious interest rates that margin accounts usually charge.

And for a moderate increase in risk, they present outsized profit opportunities.

For the right investor, they are the ideal instrument.

Let me go through some examples to show you their inner beauty.

By now, you should all know what vertical bull call spreads are. If you don’t, then please click here for a quickie video tutorial (you must be logged in to your account).

Let’s go back to February 9, 2018 when the Dow Average plunged to its 23,800 low for the year. I then begged you to buy the Apple (AAPL) June 2018 $130-$140 call spread at $8.10, which most of you did. A month later, that position is worth $9.40, up some 16.04%. Not bad.

Now let’s say that instead of buying a spread four months out, you went for the full year and three months, to June 2019.

That identical (AAPL) $130-$140 would have cost $5.50 on February 9. The spread would be worth $9.40 today, up 70.90%, and worth $10 on June 21, 2019, up 81.81%.

So, by holding a 15 month to expiration position for only a month, you get to collect 86.67% of the maximum potential profit of the position.

So, now you know why we leap into LEAPS.

When the meltdown comes, and that could be as soon as today, use this strategy to jump into longer term positions in the names we have been recommending and you should be able to retire early.

What’s out there today?

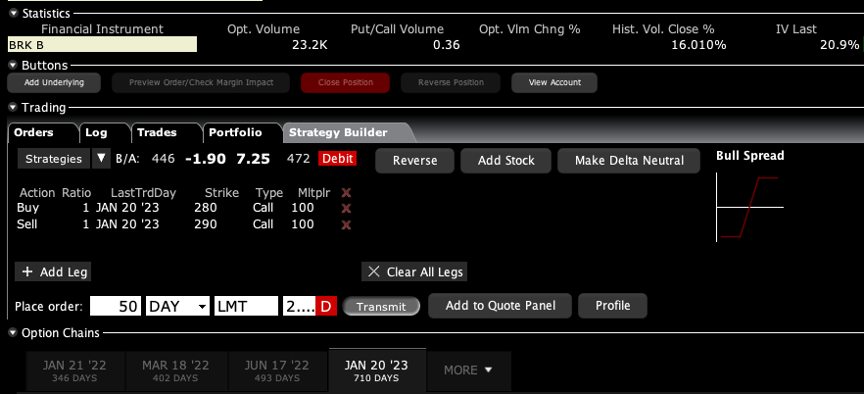

Take a look at Berkshire Hathaway “B” shares (BRK/B), one of the best plays on boring old high cash flow domestic cyclical stocks. It has a very heavy weighting in banks and has a 10% holding in Apple (AAPL) as a kicker.

Today, (BRK/B) shares were trading at $240. Let say that Berkshire shares recover to $290 by January 20, 2023. You can buy a January 2023 $280-$290 vertical bull call spread for $2.00. If Berkshire makes it to $290 by the January 20, 2023 options expiration, the LEAP will expire worth $10, an increase of 400%.

Another way of looking at this is a mere 20.8% move up in the stock in two years delivers a return of 400%, and you can't lose any more money than you put up. That implies a leverage in the position of 19.2X once the shares rise above $280.

Caution: If the shares only make it to $280 the position becomes worthless.

Now you know why I like LEAPS so much. Please play around with the names and the numbers and I’m sure you will find something you like. But remember one thing. LEAPS are only a trade to consider at long time market bottoms, not tops!

They are also the perfect positions to own if you believe we have just entered a second Roaring Twenties and a second American Golden Age, as I do.

Time to Leap Into LEAPS

Global Market Comments

August 14, 2020

Fiat Lux

Featured Trade:

(AUGUST 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (TLT), (TSLA), (AAPL), (FB), (AMZN), (VXX), (VIX), (JPM), (BAC), (GDX), (NUGT), (MRNA), (BRK/B), (SLV), (FCX)