Global Market Comments

June 27, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE RECESSION TRADE IS ON)

(MSFT), (NVDA), (TSLA), (BRKB), (TLT), (SPY)

Global Market Comments

June 27, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE RECESSION TRADE IS ON)

(MSFT), (NVDA), (TSLA), (BRKB), (TLT), (SPY)

Any doubts that financial markets are fully discounting a recession were completely smashed last week.

It isn’t just the economic data that are rolling over like the Bismarck. Oil plunged 19%, copper is off 22% from its top, and bond yields have collapsed an astonishing 46 bases points in only two weeks, from 3.48% to 3.02%, a cataclysmic move in the bond market.

Asset classes most sensitive to a recession, like industrial commodities, suffered the biggest falls. That’s because if commodities don’t get used immediately they have to be stored at great expense and a million barrels of oil don’t look very pleasant in your backyard.

How did the stock market respond? It loved it. Stocks delivered the first positive week in June. The Dow Average rallied a healthy 1,900 points off the bottom, some 6.41%.

So what gives? Why is every asset class in the world getting trashed while stocks rocket?

It's really very simple. Stocks love lower interest rates. Cut borrowing costs and equities catch a bid. Lower rates more and stocks should further appreciate.

It's not like we are out of the woods yet. We could get another interest rate spike as we move into the next Fed move on interest rates on July 27. That could take us to new lows in stocks, but not by much. Any declines from here will be limited and are worth buying, as I have been arguing for weeks.

Always focus on what is going to happen next for we are in the “what happens next business.”

While broker reports, research, and the news focus on what happened in the past, or rarely today, it is what happens next that determines the performance of your investment portfolio.

Live in the future and there are never any surprises, only rewards.

Powell Highlights the Fed’s Inflation Commitment, even though the principal drivers, OPEX+ and the Ukraine War, are completely out of his control, in testimony in front of congress. The next two 75 basis point rate rises are a sure thing. Number three won’t happen if a recession kicks in before then.

Oil Dives as Recession Fears Mount, off 20% in a week. Oil is the last thing you want to hold going into a recession, as storage fears are at record highs a few tankers are available for charter. Avoid all energy plays like the plague. Too many other better fish to fry.

American Airlines, United Airlines, and Delta are Cutting Routes, to deal with staff shortages. Small cities where no money is made, like Toledo, Islip, and Dubuque are the main targets. Reno lost much of its airline services in the last recession for the same reason.

A Real Estate Selloff is Going Global, the effect of rising interest rates worldwide. Auckland, New Zealand, Vancouver, Canada, and Sydney, Australia have suddenly seen homes go heavily offered as free money disappears. The US could be next. In Incline Village, NV homes priced under $1 million are seeing aggressive price cuts to sell, while those over $5 million are maintaining prices.

Electric Vehicles Could Reach a 33% Market Share by 2028 and 54% by 2035, says AlixPartners, a research firm. Automakers are going to have to invest $526 billion to meet this demand. EVs are becoming a dominant factor in the US economy. Keep buying (TSLA) on dips, which has a 12-year head start over everyone and has an 80% global EV market share. You just missed a chance to buy the shares at $635 last week.

Existing Home Sales plunge 3.4% in May to 5.41 million units, Dow 8.6% YOY. Inventories fell slightly, with 1.16 million homes for sale. The median home price rose to a new all-time high of $407,600. Home sales priced under $250,000 are down 27% YOY. Mansions are still selling well nationally.

Industrial Production rises by a modest 0.2% in May. Their recession hasn’t hit here yet.

Bitcoin hit a $17,900 low Asian trading. Bitcoin crash is particularly compelling to watch as it has become a great risk indicator for all asset classes. Ignore it at your peril. It turns out that the wonder of 24/7 trading means it can go down a lot faster. I have no idea where the bottom is so don’t ask. This amount of fear is impossible to quantify.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the greatest market volatility in market history, my June month-to-date performance exploded to +9.99%.

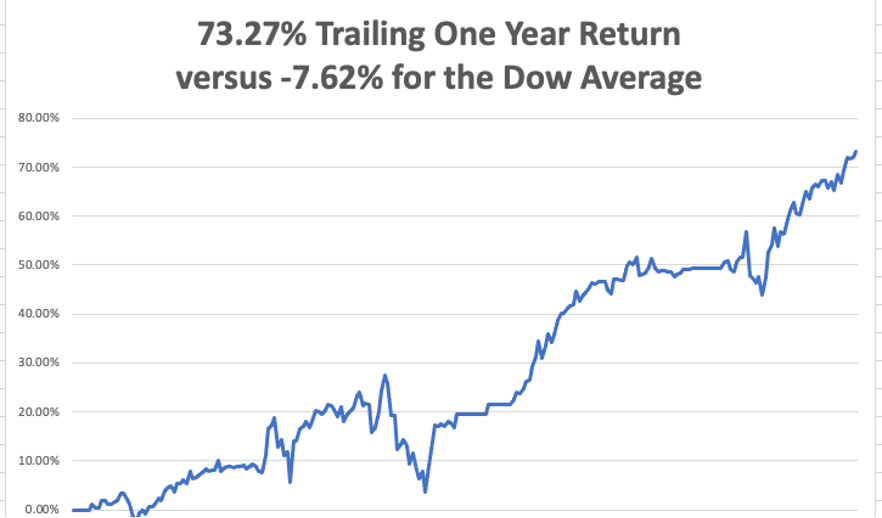

My 2022 year-to-date performance ballooned to 51.86%, a new high. The Dow Average is down -13.22% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 73.27%.

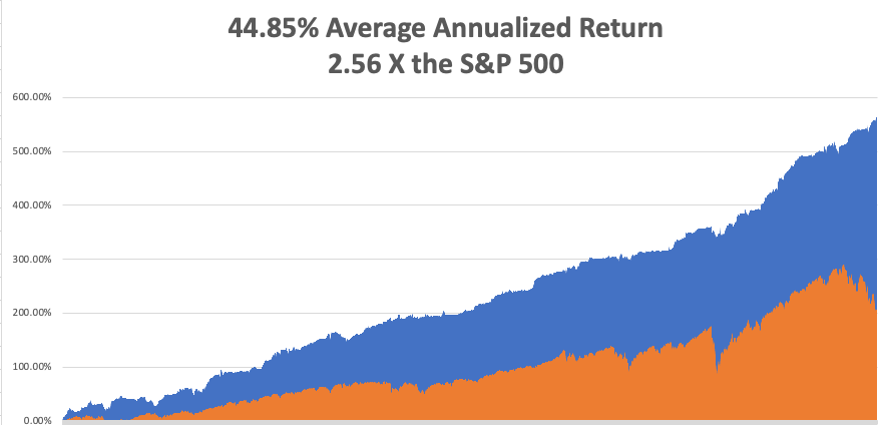

That brings my 14-year total return to 564.42%, some 2.56 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.85%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 87 million, up 300,000 in a week and deaths topping 1,016,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, June 27 at 8:30 AM, US Durable Goods for May are released.

On Tuesday, June 28 at 7:00 AM, the S&P Case Shiller National Home Price Index for April is out.

On Wednesday, June 29 at 7:00 AM, the final read of the US Q1 GDP is published.

On Thursday, June 30 at 8:30 AM, Weekly Jobless Claims are announced. We also get US personal Income & Spending.

On Friday, July 1 at 7:00 AM, the ISM Manufacturing PMI for June is disclosed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, as this pandemic winds down, I am reminded of a previous one in which I played a role in ending.

After a 30-year effort, the World Health organization was on the verge of wiping out smallpox, a scourge that had been ravaging the human race since its beginning. I have seen Egyptian mummies at the Museum of Cairo that showed the scarring that is the telltale evidence of smallpox, which is fatal in 50% of cases.

By the early 1970s, the dreaded disease was almost gone but still remained in some of the most remote parts of the world. So, they offered a reward to anyone who could find live cases.

To join the American Bicentennial Mt. Everest Expedition in 1976, I took a bus to the eastern edge of Katmandu and started walking. That was the farthest roads went in those days. It was only 150 miles to basecamp and a climb of 14,000 feet.

Some 100 miles in, I was hiking through a remote village, which was a page out of the 14th century, back when families though buckets of sewage into the street. The trail was lined with mud brick two-story homes with wood shingle roofs, with the second story overhanging the first.

As I entered the town, every child ran to their windows to wave, as visitors were so rare. Every smiling face was covered with healing but still bleeding smallpox sores. I was immune, since I received my childhood vaccination, but I kept walking.

Two months later, I returned to Katmandu and wrote to the WHO headquarters in Geneva about the location of the outbreak. A year later I received a letter of thanks at my California address and a check for $100. They told me they had sent in a team to my valley in Nepal and vaccinated the entire population.

Some 15 years later, while on customer calls in Geneva for Morgan Stanley, I stopped by the WHO to visit a scientist I went the school with. It turned out I had become quite famous, as my smallpox cases in Nepal were the last ever discovered.

The WHO certified the world free of smallpox in 1980. The US stopped vaccinating children for smallpox in 1972, as the risks outweighed the reward.

Today, smallpox samples only exist at the CDC in Atlanta frozen in liquid nitrogen at minus 346 degrees Fahrenheit in a high-security level 5 biohazard storage facility. China and Russia probably have the same.

That’s because scientists fear that terrorists might dig up the bodies of some British sailors who were known to have died of smallpox in the 19th century and were buried on the north coast of Greenland, remaining frozen ever since. If you need a new smallpox vaccine, you have to start from somewhere.

As for me, I am now part of the 34% of Americans who remain immune to the disease. I’m glad I could play my own small part in ending it.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

On Mt. Everest Smallpox Free in 1976

Global Market Comments

May 31, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHY I LOVE INFLATION),

(SPY), (TLT), (TBT), (GOOGL),

(AAPL), (MSFT), (BRKB), (NVDA), (V)

I love inflation.

Thanks to the relentless increase in prices, the value of my home has risen by $4 million over the last ten years, and $2 million over the last three years alone.

And I’m not the only one.

Some 66% of Americans own their own homes and may have seen similar price increases or more.

So, what if the price of a gallon of milk goes up by $1? I’ll happily pay that if it means my largest personal investment appreciates at triple-digit rates. Besides, I’m lactose intolerant anyway, and all my kids have grown up.

I’ll tell you what else inflation does. It makes stocks really cheap. That’s because investors fear that the Fed will raise interest rates by too much, destroy company earnings, and trigger a recession.

This is counterintuitive because companies actually benefit from inflation because they can get away with faster price increases more often, boosting profits. I took my kids out to a graduation dinner yesterday and practically had to take out a second mortgage to do so.

Personally, I believe that such a stock market bottom is close. But while the last bottom was within 10%, or 200 S&P 500 (SPX) points in terms of price, it is only 50% in terms of time. That signals a great new bull market for stocks beginning sometime this summer. Then anything you touch will double in three years.

You will look like a genius….again!

You can see who agrees with me by looking at which stocks are already getting bought up. Coca-Cola (KO), Johnson & Johnson (JNJ), and Procter & Gamble (PG) are the kind of safe, dividend-paying, brand name stocks that very long-term investors like pension funds love to own. They tend to buy and hold….forever.

No meme stocks here.

It isn’t just the Fed that is raising interest rates, which can only control overnight rates. The US budget deficit is falling at the fastest rate since WWII, possibly taking us to a budget surplus by year-end. As a result, the money supply is shrinking at the fastest rate in 60 years.

QT, or quantitative tightening, will fan the flames when it starts on January 1, ultimately taking up to $9 trillion out of the financial system.

Remember all that liquidity from QE, near-zero rates, and massive government spending that saved the economy from Armageddon? Play for movie in reverse and you get the oppositive result, i.e. falling share prices….at least for a while.

The battle as to who is right about the direction of the economy continues unabated. Is it bonds or stocks? At the rates that stocks have been plunging, stocks are essentially anticipating another Great Depression.

Ten-year US Treasury yields that soared from 1.33% to 3.12% in a mere six months are proclaiming that happy days are here again and will last forever. Since January, the average monthly mortgage payment has jumped by $450 a month. If that isn’t recessionary, I don’t know what is.

As a 53-year veteran of these markets, I can tell you that the bond market is always right. That’s because the money spent on equity research has shrunk to a shadow of its former self in recent decades, while bond research is as strong as ever.

Always listen to the guy with the $10 million budget and ignore the one with the $500,000 budget, which means that in the coming months, equity prognosticators will realize the error of their ways and come over to my way of thinking once again.

The Fed Minutes were not so horrible, downplaying the risk of a full 1% rate rise, triggering a 1,000-point rally in the Dow. With five up days in a row, this is starting to look like THE bottom. Is this the light at the end of the tunnel?

Q1 GDP dives 1.5% in its final read. It’s the worst quarter since the pandemic began during Q2 2022. Weekly Jobless Claims dropped 8,000 to 210,000.

NVIDIA Rips, surprising to the upside on almost every front, sending the stock up $30, or 18.75%. Mad Hedge followers bought (NVDA) last week. This is one of the best-run companies in the world. I expect the shares to rise from the current $178.51 to $1,000 in five years. Buy (NVDA) on dips.

The Consumer will keep driving the economy, says Bank of America CEO Brian Moynihan. Betting against the American consumer has always been a fool’s errand. I’m with Brian. Cash levels this high were never followed by recessions.

Only 18% of Americans will increase stockholdings this year, which is usually what you get at market bottoms. It was closer to 100% at the December top. Yet another signal that we are approaching the bottom in price, if not time.

New Home Sales dive in April, down 16.6% on a signed contract basis, the weakest in two years. The macro is definitely conspiring against the market. It’s all about interest rates. The average monthly mortgage payment has rocketed by $450 a month since January. Inventories have also soared from 6 to 9 months.

Advertising is in free fall, especially the online version, a usual pre-recession indicator. It is the easiest and first expense companies cut when they expect flagging sales. Look no further than yesterday’s astonishing 43% collapse in Snap (SNAP). Notice that TV commercials are getting endlessly repeated as the number of advertisers and ad rates fall. If I see one more ad for Interactive Brokers, I’ll shoot myself.

The EV Shortage worsens, with wait times for a new Tesla extending beyond a year. I can sell my Model X for more than I paid for it three years ago. Gasoline at $6.00 is converting a lot of drivers, and gas lines this summer loom. Big three dealers are price gouging on the few EVs they have, charging well over list. Good luck finding a Rivian pick-up; that’s a two-year wait. Maybe that makes (TSLA) a “BUY” down here?

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the greatest market volatility seen since 1987, my May month-to-date performance recovered to +8.80%.

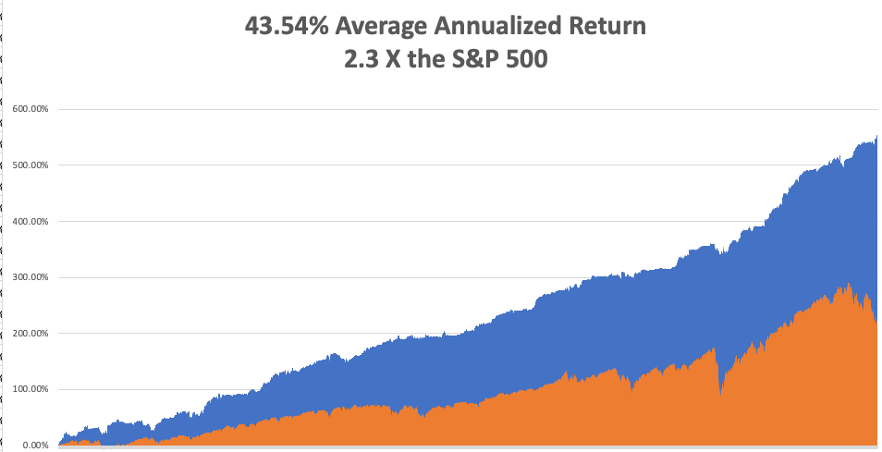

My 2022 year-to-date performance exploded to 38.98%, a new high. The Dow Average is down -9.30% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 61.22%.

Last week was a quiet one, with me using the monster rally to add new shorts in Apple (AAPL) and the S&P 500 (SPY).

That brings my 14-year total return to 551.54%, some 2.40 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 43.54%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 84 million, up 1.5million in a week, and deaths topping 1,004,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, May 30, markets are closed for Memorial Day.

On Tuesday, May 31 at 9:00 AM EST, the S&P Case Shiller National Home Price Index for March is released.

On Wednesday, June 1 at 10:00 AM, JOLTS Job Openings for April are published.

On Thursday, June 2 at 8:30 AM, Weekly Jobless Claims are out. We also learn the ADP Private Employment Report for May.

On Friday, June 3 at 8:30 AM, the big Nonfarm Payroll Report for May is disclosed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, as a lifetime oenophile, or wine lover, I long searched for the Holy Grail of the perfect bottle. I finally found my quarry in 1989.

During the 19th century, Russia was still an emerging country that sought to import advanced European technology. So, they sent agents to the top wine-growing regions of the continent to bring back grapevine cuttings to create a domestic wine industry. They succeeded beyond all expectations building a major wine industry in Crimea on the Black Sea.

Then the Russian Revolution broke out in 1918.

Czar Nicholas II and his family were executed, and eventually, the wine industry was taken over by the Soviet state. They kept it going because wine exports brought in valuable foreign exchange with which the government could use to industrialize the country.

Then the Germans invaded in 1941.

Not wanting the enemy to capture a 100-year stockpile of fine wine, the managers of the Massandra winery dug a 100-yard-deep cave, moved their bottles in, bricked up the entrance, and hid it with shrubs. Then everyone involved in storing the wine was killed in the war.

Some 45 years later, looking to expand the facility, some Massandra workers stumbled across the entrance to the cave. Inside, they found a million bottles dating back to the 1850s kept in perfect storage conditions. It was a sensation in the wine collecting world.

To cash in, they hired Sotheby’s in London to repackage and auction off the wine one case at a time. It was the auction event of the year. For years afterwards, you could buy glasses of 100-year-old ports and sherries from the Czar’s own private stock at your local neighborhood restaurant for $5, the deal of the century.

I attended the auction at Sotheby’s packed Bond Street offices. The superstars of the wine collecting world were there with open checkbooks. I sat there with my paddle number 138 but was outbid repeatedly and wondered if I would get anything. In the end, I managed to pick up some of the less popular cases, a 1915 Madeira, a 1936 white port, and a 1938 sherry for about $25 a bottle each.

For years, these were my special occasion wines. I opened one when I was appointed a director of Morgan Stanley. Others went to favored clients at Christmas. My 50th, 60th, and 70th birthdays ate into the inventory. So did the birth of children number four and five. Several high school fundraisers saw bottles earn $1,000 each.

One of the 1915’s met its end when I came home from the Gulf War in 1992. Hey, the last Czar didn’t drink it and looked what happened to him! Another one bit the dust when I sold my hedge fund at the absolute market top in 1999. So did capturing 6,000 new subscribers for the Mad Hedge Fund Trader in 2010.

It turns out that the empties were quite nice too, 100-year-old hand-blown green glass, each one is a sculpture in its own right.

I am now reaching the end of the road and only have a half dozen bottles left. I could always sell them on eBay where they now fetch up to $1,000 a bottle.

But you know what? I’d rather have six more celebrations than take in a few grand.

Any suggestions?

Stay Healthy,

John Thomas

CEO & Publisher

Global Market Comments

May 23, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ALL QUIET ON THE WESTERN FRONT)

(SPY), (TLT), (TBT), (GOOGL), (AAPL), (MSFT), (BRKB), (NVDA), (JPM), (BAC), (WFC), ($BTCUSD)

When I first joined Morgan Stanley in 1983, a number of my clients were old enough to have experienced the 1929 stock market crash and the Great Depression that followed.

One was Sir John Templeton, who confided in me over lunch at his antebellum-style mansion at Lyford Cay in the Bahamas, that his long career started with a lot of excitement, and then became incredibly boring for a decade.

It looks like we entered the incredibly boring phase on January 4, when the stock market began its current downtrend. Last week brought the longest weekly losing streak since 1923, some eight weeks so far.

The market is actually down a lot more than it looks, meaning that we are a lot closer to the bottom than you think. Some 87% of the S&P 500 is down more than 10% and 61% is down 20%. The damage is far worse with the NASDAQ, with some 93% of shares down 10%, and a gut-punching 73% down 20% or more.

While tech has already gone down a lot, some 32% so far this year, it is still trading at an 18% premium to the main market. Remember, in this business, timing is everything. If you invested in tech at the Dotcom peak in 1999, it took you 14 years to break even. Latecomers in this cycle could suffer a similar duration of pain and suffering.

And while these are the kind of moves that usually precede a recession, there is still an overwhelming amount of data that says it won’t happen. We here at Mad Hedge Fund Trader analyze, dissect, and examine data all day long.

I will once again repeat what my UCLA math professor told me a half-century ago. “Statistics are like a bikini bathing suit; what they reveal is fascinating, but what they conceal is essential.”

For a start, 3.6% unemployment rates are not what recessions are made of. Double-digit ones are. The next jobless rate print in June is likely to be down, not up. The country in fact is suffering its worst worker shortage in 80 years. There are currently 6 million more jobs than workers. And wages are rising, putting more money in the pockets of consumers.

Last month, airline ticket prices rose by 25%. Good luck trying to get a plane anywhere as all are full. Last winter, I bought a first-class round-trip ticket from San Francisco to London for $6,000. Today, the same ticket is $10,000. During recessions, planes fly empty, routes get cancelled, and staff laid off. Airlines also go bust and are not subject to the takeover wars we are seeing now.

Recessions also bring dramatic credit crises. Rising default rates force banks to retreat from lending, FICO scores tank, and debt markets dry up. It’s all quiet on the western front now, with all fixed income and liquidity indicators are solidly in the green. And while interest rates are higher, they are nowhere near the peaks seen during past recessions.

All this may explain that after the horrific market moves we have already seen but we may be only 4% from the final bottom in this bear move to an S&P 500 at $3,600, or 7% from an (SPX) of $3,500. That means it is time to start scaling into long-term positions now in the best quality names.

That’s why I have been aggressively piling on call spreads in technology that are 10%-20% in the money with only 19 days to expiration, making money hand over fist.

An interesting headline caught my attention last week. The Russians were stealing farm equipment from Ukraine on an epic scale. When they couldn’t steal it, such as when the electronics were disabled, they were destroying it.

That means the Russians didn’t invade Ukraine to get more beachfront territory on the Black Sea, although that is definitely a plus. They want to destroy a competitor’s agricultural production in order to raise the value of their own output.

Yes, this is the beginning of the Resource Wars that could continue for the rest of this century. Resource producers like the US, Russia, Canada, Australia, and Ukraine will be the big winners. Resource consumers like China, India, and the Middle East will be the big losers.

JP Morgan cuts US GDP Forecasts, with the second half marked down from 3% to 2.4% and 2023 from 2.1% to 1.5%. This means no recession, which requires two back-to-back negative quarters.

China’s Industrial Production collapses by 2.9%, and Retail Sales fell by a shocking 11.1%. The Shanghai shutdown is to blame. It means longer supply chain disruptions for longer and another drag on our own economy. If Tesla has a bad quarter, it will be because of a shortage of vehicles in China. So, will the end of Covid in China bring the bull market back in the US?

The US Budget Deficit is in free fall, putting our hefty bond shorts at risk. While Trump was president the national debt exploded by $4 trillion, a dream come true for bond shorts. Since Biden became president, the annual budget deficit has plunged from $3.1 trillion to $360 billion for the first seven months of fiscal 2022, and we could approach zero by yearend. An exploding economy has sent tax revenues soaring, and taxpayers still have to pay a gigantic bill for last year’s monster capital gains in the stock market. Biden has also been unable to get many spending bills through the Senate, where he lacks a clear majority.

India Bans Food Exports. Climate change is destroying its output with heat waves, while the Ukraine War has eliminated 13% of the world’s calories. This is a problem when you have 1.2 billion to feed. Expect food inflation to worsen.

Consumer Sentiment hits an 11-year low according to the University of Michigan, dipping from 64 to 59.1. Record gas prices and soaring inflation are the reasons, but spending remains strong off the super strong jobs market.

Homebuilder Sentiment hits a two-year low, down from 77 to 69 in May, according to the National Association of Homebuilders. Recession fears and soaring interest rates are the big reasons.

Building Permits dive in April by 3.2%, and single family permits were down 4.6%. The onslaught of bad news for housing continues. Avoid.

Target implodes on terrible earnings, taking the stock down 25%, the worst in 40 years. They finally got the inventory they wanted. Too bad consumers are too poor to buy it with $6.00 a gallon.

Commodities send Battery Costs soaring by 22%. Who knew you were going long copper, lithium, and chromium when you bought your Tesla? It’s a good thing you did. Now you can give the middle finger salute when you drive past gas stations.

Average Household now spending $5,000 a year on gasoline, which is $5,000 they’re not spending on anything else. Just ask Target (TGT) and Walmart (WMT).

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

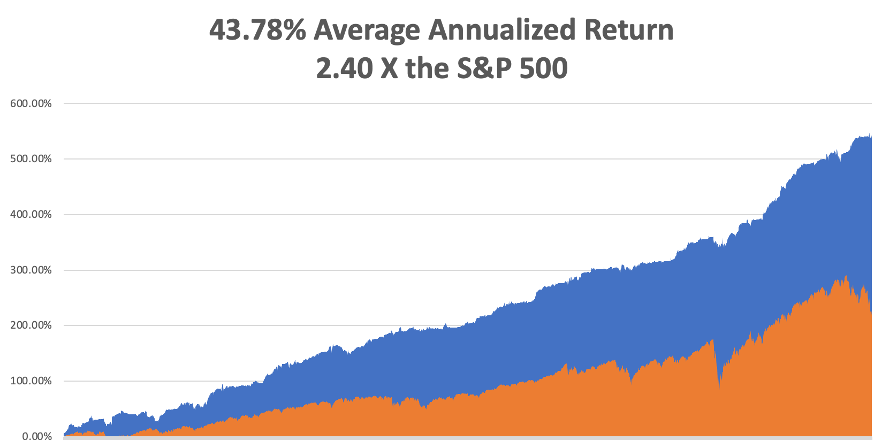

With some of the greatest market volatility seen since 1987, my May month-to-date performance recovered to +4.79%.

My 2022 year-to-date performance exploded to 34.97%, a new high. The Dow Average is down -16.4% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 62.99%.

This week, I added new long positions in Visa (V) and Microsoft (MSFT) when the Volatility Index (VIX) was in the mid $30s. I also did a nice round trip on an Apple (AAPL) short which brought in $1,740. I also took profits on two longs in the (SPY) and two shorts in the (TLT). Overall, it was a great week!

That brings my 14-year total return to 547.53%, some 2.40 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 43.78%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 82.5 million, up 300,000 in a week and deaths topping 1,000,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, May 23 at 8:30 AM EST, the Chicago Fed National Activity Index for April is out.

On Tuesday, May 24 at 8:30 AM, New Home Sales for April are released.

On Wednesday, May 25 at 8:30 AM, Durable Goods for April are published.

On Thursday, May 26 at 8:30 AM, Weekly Jobless Claims are disclosed. The first look at Q2 GDP is printed.

On Friday, May 27 at 8:30 AM, Personal Income & Spending is out. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, one of my fondest memories takes me back to England in 1984 for the 40th anniversary of the D-Day invasion of France. On June 6, 160,000 Americans stormed Utah and Omaha beaches, paving the way for the end of WWII.

My own Uncle Al was a participant and used to thrill me with his hair-raising D-Day experiences. When he passed away, I inherited the P-38 Walther he captured from a German officer that day.

The British government wanted to go all out to make this celebration a big one as this was expected to be the last when most veterans, now in their late fifties and sixties, were in reasonable health. President Ronald Reagan and prime minister Margaret Thatcher were to be the keynote speakers.

The Royal Air Force was planning a fly past of their entire fleet that started over Buckingham Palace, went on the to the debarkation ports at Southampton and Portsmouth, and then over the invasion beaches. It was to be led by a WWII Lancaster bomber, two Supermarine Spitfire, and two Hawker Hurricane fighters.

The only thing missing was American aircraft. The Naval and Military Club in London, where I am still a member, wondered if I would be willing to participate with my own US-registered twin-engine plane?

“Hell yes,” was my response.

Of course, the big concern was the weather, as it was in 1944. Our prayers were answered with a crystal clear day and a gentle westerly wind. The entire RAF was in the air, and I found myself the tail end Charlie following 175 planes. I was joined by my uncle, Medal of Honor winner Colonel Mitchell Paige.

We flew 500 feet right over the Palace. I could clearly see the Queen, a WWII veteran herself, Prince Philip, Lady Diana, and her family waving from the front balcony. Massive shoulder-to-shoulder crowds packed St. James Park in front.

As I passed over the coast, much of the Royal Navy were out letting their horns go full blast. Then it was southeast to the beaches. I flew over Pont du Hoc, which after 40 years still looked like a green moonscape, after a very heavy bombardment.

In one of the most courageous acts in American history, a company of Army Rangers battled their way up 100-foot sheer cliffs. After losing a third of their men, they discovered that the heavy guns they were supposed to disable turned out to be telephone poles. The real guns had been moved inland 400 yards.

We peeled off from the air armada and landed at Caen Aerodrome. Taxiing to my parking space, I drove over the rails for a German V2 launching pad. I took a car to the Normandy American Cemetery at Colleville-sur-Mer where Reagan and Thatcher were making their speeches in front of 9,400 neatly manicured graves.

There were thousands of veterans present from all the participating countries, some wearing period uniforms, most wearing ribbons. At one point, men from the 101st Airborne Division parachuted overhead from vintage DC-3’s and landed near the cemetery.

Even though some men were in their sixties and seventies, they still made successful jumps, landing with big grins on their faces. The task was made far easier without the 100 pounds of gear they carried in 1944.

The 78th anniversary of the D-Day invasion is coming up shortly. I won’t be attending this time but will remember my own fine day there so many years ago.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Pont du Hoc

Global Market Comments

May 16, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SIFTING THROUGH THE WRECKAGE),

(SPY), (TLT), (TBT), (GOOGL), (AAPL), (MSFT), (BRKB), (NVDA), (JPM), (BAC), (WFC), ($BTCUSD)LA),

I have many superpowers, but one of the most useful ones is picking market bottoms. It looks like another one is at hand.

The past week has been one of epic wreckage in the stock market. It’s as if Hurricanes Sandy and Katrina both hit at the same time and were followed by a good old California earthquake.

Your favorite share prices have gone from mildly irritating to disappointing to absolutely gobsmackingly awful in only five months.

As a result, some of the best buying opportunities of the decade are setting up, the kind that you will be able to will on to your grandchildren. This is when mortgages get paid off, college debt is retired, and retirements financed.

There are a couple of key measurements here to watch. When the number of stocks above their 200-day moving averages falls below 20%, it always signifies an important market bottom. At the Thursday low, we were at 15% for the (SPY) and 12% for NASDAQ. It’s just another technical indicator among the hundreds, but a useful one, nonetheless.

Another one that helps is that on Friday, we also saw the first 90% advancing day since June 2020. All correlations went to one last week, meaning that all asset classes went down in unison.

That puts the bottom for the S&P 500 at $3,800 with an initial upside target of $4,200. We are way overdue for an 8%-12% relief rally. If I am wrong, we are only dropping another 200 points, or 5%.

Except that this time, it’s different.

At $3,600, down 25% from the January high, the market will have fully discounted a fairly severe recession that isn’t going to happen. Amazing as it may seem, some of the stocks having the biggest falls are still seeing earnings grow nicely. They are simply being sold because they are widely owned. That snares them in all of the algorithm-driven high-frequency trading that is going on.

I know I’ve said this a million times, but you use markets like this to buy Rolls Royces at Volkswagen prices. I’m talking about Alphabet (GOOGL), Microsoft (MSFT), and Apple (AAPL).

These companies are solid as the Rock of Gibraltar, with massive cash flows, huge cash balances, unassailable moats, and steady, if not spectacular earnings prospects. People have not suddenly abandoned Google as a search engine, Microsoft still has a near-monopoly in PC operating software, and Apple will sell more new and more expensive iPhones than ever.

The other baby that is being thrown out with the bathwater here are the banks. Recession fears have given these shares a haircut by a third by recession fears that damage the credit quality of their loan books.

What if there is no recession? Then the bear market in banks goes up in a puff of smoke. It helps that this time, there is no liquidity or capital crisis to be seen whatsoever. Add JP Morgan (JPM), Bank of America (BAC), and Wells Fargo (WFC) to your growing “BUY” lists.

Buying the best stocks with a recession already baked in the price? Sounds like a winner to me.

As for the smaller tech stocks, I’d take a pass, at least for now. Most of these companies, which never made any money, now have shares down 70% to 90% and are not coming back. They provided to be perfect money destruction machines. Never confuse “gone down a lot” with “cheap.” Take away the punch bowl and suddenly the party becomes very boring.

The Mad Hedge Market Timing Index certainly earned its weight in gold last week. We saw a multi-year low of 6 on Thursday and I was sending out trade alerts to “BUY” as fast as I could write them. A 1,200-point snap-back rally ensued, setting up a bottom that could last for weeks, if not forever.

The other great thing to come out of this selloff is that we learned what a fantastic leading indicator of risk-taking Bitcoin has become. While the S&P 500 plunged by 20%, Bitcoin absolutely cratered by 60%. We saw the correlation on both the upside and the downside.

Bitcoin is basically the (SPY) X 3. Ignore Bitcoin at your peril, even if you think the whole thing is a scam. And keep reading your Mad Hedge Bitcoin Letter.

Was this the grand finale? Big tech stocks like Apple (AAPL) and Microsoft (MSFT) stubbornly held their ranges for months, supporting the market as a whole. That ended last week on no news with the decisive breakdown of the key names. Apple has lost a staggering $350 billion in market cap in a week. Does this signal the final washout of this correction? It could. The Volatility Index (VIX) has ceased rising, and bonds have begun a short-covering countertrend rally.

Jay Powell warns of more 50-basis point rate rises if the economic conditions justify it. He also can’t guarantee a soft landing for the economy. Thanks for telling us precisely nothing. The comments were made on NPR Radio’s marketplace program and immediately tanked Dow futures by 100 points.

Core Inflation moderates slightly, down from 8.5% to 8.3% in April, sparking a stock market rally. That is 0.2% lower than last month’s 8.5% print, hence the bond rally. It was the first decline in the inflation rate in seven months. The probability of a peak in inflation is increasing.

Producer Price Index soars 11.0% YOY and 0.5% in April alone. It is a red-hot number showing that inflation is getting worse. The Producer Price Index (PPI) program measures the average change over time in the selling prices received by domestic producers for their output.

Goldman Sachs quit the SPAC Market, citing unmanageable liability. More likely, they don’t want to get stuck with illiquid longs on SPACS they brought to the market. I warned you this was a roach motel market; you can check in but you can never check out. I have to admit that I never believed in this asset class for two seconds, regarding it as nothing more than a license to steal money from investors.

Bitcoin drops below $28,000, taking the cryptocurrency down to more than half its November peak. It’s acting more like a small-cap tech stock every day, not the thing to be right now. With the Fed shrinking liquidity at a record rate, this is not a favorable backdrop either.

Another crypto bites the dust, as the free fall continues. Tether, a stablecoin tied to the US dollar, has fallen to 69% of its face value. It turns out that backing by the US government is more reliable than support from a PO Box in the Cayman Islands. Expect more to fail. Avoid crypto at all cost.

Ford to unload 8 million Rivian shares, once a lockup expires. Other pick institutional blocks are waiting in the wings. The EV truck is smoking hot on the road, but the shares have been dead as a doorknob, down 85% from the peak and 16% on the day. Avoid (RIVN) while the sector is death warmed over.

Biden mulling dropping Chinese Tariffs to make a dent in inflation. It might help a bit. It just depends on what we might get in return. Such a move wouldn’t exactly protect American workers, a top Biden priority. Relations with China are still fraught at best.

US Dollar blasts through to 20-year high, but a cooling inflation number on Wednesday may signal the top. Soaring interest rates, a strong economy, and a weak Europe and Japan are the drivers. There’s a short play here someday, but not yet.

Housing Supply improves for the first time in three years. Supply of mid-sized single-family loans takes the lead. Inventories are showing smallest declines in a year. Finally, the buyers get a break….now that prices are falling. Almost all new loans are 5/1 ARMS.

Air Ticket Prices are through the roof and were the biggest single factor keeping the CPI inflation figure sky-high yesterday. Buyers cite as reasons a long time since visiting relatives, desperation to get outdoors, and a rush to travel before the next Covid wave hits. It may be a one-time pop only, as used car prices were in previous months.

30-Year Fixed Rate Mortgages Top 5.5% in the fastest rate rise in history. The housing market is still hot, now fueled by exploding adjustable-rate mortgages 1.5% cheaper. Refi’s, however, have gone to zero.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the greatest market volatility seen since 1987, my May month-to-date performance recovered to +0.91%. Friday was up +5.12%, the biggest one-day gain in the 14-year history of the Mad Hedge Fund Trader.

My 2022 year-to-date performance exploded to 31.09%, a new high. The Dow Average is down -12.67% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 58.48%.

I used last week’s meltdown to cover shorts in the (SPY) and bonds (TLT) and to buy new longs in technology like (AAPL), (NVDA), and (BRKB). I would have sent out more trade alerts if I had more time and didn’t have Covid and a 102 degrees temperature.

That brings my 14-year total return to 543.65%, some 2.40 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 43.78%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 82.5 million, up 300,000 in a week, and deaths topping 1,000,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, May 16 at 8:30 AM EST, the New York Empire State Manufacturing Index is released.

On Tuesday, May 17 at 8:30 AM, Retail Sales for April are released.

On Wednesday, May 18 at 8:30 AM, Housing Starts and Building Permits for April are published.

On Thursday, May 19 at 8:30 AM, Weekly Jobless Claims are disclosed. Existing Home Sales for April are printed.

On Friday, May 20 at 8:30 AM, the Baker Hughes Oil Rig Count is out.

As for me, the 1980s found me heading the Japanese equity warrant trading department for Morgan Stanley in London, a unit which eventually produced 80% of the company’s equity division profits. It was like running a printing press for $100 bills.

My east end kids in their twenties were catapulted from earning $10,000 a year to a half million. After buying West End condos, the latest Ferrari or Jaguar, and picking up fashion model girlfriends, they ran out of ideas on how to spend the money.

Maybe it was time to upgrade from pints of Fosters at the local pub to fine French wines?

The problem was that no one knew what to buy. Bordeaux alone produced 5,000 labels, and Burgundy a further 7,000. France had 360 appellations in 11 major wine-growing regions. Worse yet, all the names were in French!

Following a firmwide search, it was decided that I should become the in-house wine connoisseur. After all, I was from a wine-growing region in California, spoke French, and was part-French. How could they lose?

As with everything I do, I intensively threw myself into research. It turns out that the insurance exchange, Lloyds of London, was suffering the first of its claims in its history. US asbestos-related insurance claims were exploding. Then, a giant offshore natural gas rig, Piper Alpha, blew up. Suddenly Lloyd’s syndicates were getting their first-ever cash calls.

These syndicates were sold to members as guaranteed risk-free cash flow. Suddenly many members had to come up with $250,000 each in months. No one was ready. How did many meet their cash calls? By selling off 100-year-old wine cellars through auctions at Sotheby’s in London.

Now let me tell you about the international wine auction business. Single cases of the first growth wines, like the 1983 Chateaux Laffite Rothchild, are traded on open markets like any other investment. They appreciate in value like bonds, about 5% a year. However, mixed cases filled with odds and ends from different wineries and different years, have no investment value and traded at enormous discounts.

I found my market!

In short order, I put together a syndicate of 20 new wine consumers and went to work.

To separate out the sheep from the goats, I relied on a wine guide that The Economist magazine included at the back of every wallet diary. As each auction catalog came out, I rated every bottle in the mixed cases coming for sale. I then showed up at the bi-monthly auctions and bought every case.

It wasn’t long before I became the largest buyer of wine at Sotheby’s, picking up 20 cases per auction. The higher the Japanese stock market rose, the more money the traders made, and the more they had to spend on better French wines.

It wasn’t long before Morgan Stanley became famed for being a firm of wine authorities. Our guys were getting invited to high-end dinners just so they could pick the wines, including me.

Sotheby’s took note, and set me up with their in-house wine expert, the famed Serena Sutcliffe. I became her favorite customer. Serena knew everyone in Bordeaux. Who is the most popular person in any wine-growing area? Not the one who makes the wine but the one who sells it.

It wasn’t long before Serena set me up with private tours of the top Bordeaux wineries. I’m talking about Laffite Rothchild, Haut-Brion, Yquem (once owned by US Treasury Secretary C. Douglas Dillon), Chateaux Margaux, and Pomerol. I then flew the two of us down to Bordeaux in my twin-engine Cessna 340 for the wine tasting opportunity of a lifetime. I came back full up, with about 10 cases per flight.

I was guided through ancient, spider web-filled, fungus-infused caves and invited to drink their prime stock. Let me tell you that the 1873 Laffite Rothchild is to die for but is bested by the 1848 Chateaux Yquem.

The stories I heard were incredible. During WWII, one winery dumped its entire stock in a nearby pond to keep the Germans from getting it. But the labels floated to the surface. After the war, they fished out the bottles. But they couldn’t identify them until they opened the bottles, where the vintage was printed on the cork. It was free fishing for years for the locals and there are probably a few bottles still in there.

In sommelier school, you have to taste 5,000 wines to graduate. They tell you up front that it will change your life. After my experience as the biggest wine buyer in London for five years, I can tell you this is true.

One of my treasured buys was a bottle of 1952 Laffite Rothchild, the year I was born. Then it was only 40 years old and went down well with a fine dinner of Beef Wellington. I had the bottle for years until a cleaning lady found it on a shelf after a party and put it in the recycling bin.

A few months ago, I was at the Marin French Antique Show browsing for hidden treasures. What did I find but an empty case of 1985 Romanee Conti, the greatest Burgundy of France. The vendor had no idea what he had. To him, it was just a wood box. I offered him $10. He said thanks. It now adorns a place of honor in my own wine cellar to remind me of this grand experience.

And if we ever meet for dinner, don’t bother with the wine list. I’ll be making the pick.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Fill Her Up with Bordeaux

Global Market Comments

May 11, 2022

Fiat Lux

Featured Trade:

(JOIN ME ON CUNARD’S MS QUEEN VICTORIA

FOR MY JULY 9, 2022 SEMINAR AT SEA)

Global Market Comments

May 10, 2022

Fiat Lux

Featured Trade:

(MAY 4 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (ROM), (ARKK), (LMT), (RTN), (USO), (AAPL), (BRKB), (TLT), (TBT), (HYG), (AMZN)