Mad Hedge Biotech and Healthcare Letter

March 18, 2025

Fiat Lux

Featured Trade:

(WHEN THE MARKET GIVES BACK WHAT IT ONCE TOOK AWAY)

(ABT), (ISRG), (SYK), (BSX)

Mad Hedge Biotech and Healthcare Letter

March 18, 2025

Fiat Lux

Featured Trade:

(WHEN THE MARKET GIVES BACK WHAT IT ONCE TOOK AWAY)

(ABT), (ISRG), (SYK), (BSX)

If Wall Street had a confessional booth, I'd be first in line. "Forgive me, market gods, for I underestimated how quickly sentiment could shift."

When I last wrote about Abbott Laboratories (ABT), the market was treating this medical device powerhouse like last week's leftovers—despite growth that would make most CEOs weep with joy.

Fast forward a few months, and Abbott's stock has rocketed 25%, outpacing the broader medical device sector by about 20%.

It has kept stride with Boston Scientific (BSX) while leaving Intuitive Surgical (ISRG) and Stryker (SYK) eating dust.

This kind of market whiplash reminds me of reporting from Tokyo trading floors in the 1980s—fortunes changing direction faster than a day trader after espresso, fundamentals barely shifting while sentiment performed aerial gymnastics.

So what changed? Abbott became a flight-to-safety darling.

While economic storms gather, it sits comfortably in its non-elective procedure fortress, with minimal tariff exposure and a recent legal victory reducing liability concerns.

The irony? Sentiment has now sprinted ahead of business performance. While Abbott remains a leader, its valuation leaves little room for missteps.

And if I'm overpaying for med-tech, I might as well reach for Boston Scientific instead, where growth is comparable but the valuation looks more reasonable.

Abbott’s fourth-quarter results weren’t showstopping, but they were reassuring.

Revenue landed slightly below expectations in some areas, but crucial segments—like Medical Devices—delivered strong results. Meanwhile, profit margins surprised pleasantly, reinforcing Abbott’s operational strength.

Overall revenue grew 9% organically, with Medical Devices leading at 14% growth.

The Diagnostics division posted just 1% growth, but that’s misleading—strip out COVID-19 testing effects, and underlying growth jumps to 6%.

Margins impressed, too. Gross margin improved to 56.9%, and adjusted operating income climbed 10%.

Abbott even managed a narrow revenue beat while missing slightly on EBITDA and free cash flow, largely due to tax timing that caught most analysts off guard.

I've spent decades analyzing companies across multiple sectors, and I can tell you Abbott’s medical device business deserves genuine admiration.

It maintained 14% growth from start to finish—a remarkable consistency while competitors slowed from 9.5% to 9.2% growth during the same period.

Looking at the fourth-quarter specifics, Structural Heart shone with 23% growth, outpacing Boston Scientific’s 20% and Medtronic’s 12%.

The Diabetes segment posted an impressive 20% growth, more than doubling DexCom’s 8%. Even in slower segments like Cardiac Rhythm (7%) and Neuromodulation (8%), Abbott still outperformed key competitors.

The bottom line: Abbott is executing at an exceptional level across its device portfolio.

Even its Diagnostics business, with 6% underlying growth, holds up well against Roche’s 8% and substantially outperforms Siemens Healthineers’ anemic sub-1% and Danaher’s 2% contraction.

There are three developments that investors should be paying attention to.

First, Abbott’s exposure to new tariffs is minimal—just 5% of COGS from Mexico and 1% from China. This translates to a low single-digit EPS impact, barely a rounding error in today’s environment.

Second, TriClip may have more growth potential than I previously thought. Recent data from Edwards Lifesciences’ (EW) competing Evoque device showed no mortality benefit and only modest hospitalization improvements.

This lets Abbott position TriClip as the safer approach without sacrificing quality-of-life benefits.

Third—and most significant—Abbott won a crucial legal victory in October regarding its infant formula.

A jury unanimously found the company not at fault in a necrotizing enterocolitis case, though the judge recently granted a new trial.

With 10,000 cases still pending, this development could strengthen Abbott’s settlement position and potentially cap damages below $1 billion—substantial but manageable.

I expect slight moderation next year, but Abbott should still deliver 7% growth over the next three to five years.

Newer products like Lingo (blood glucose monitoring for non-diabetics) are performing well, with significant potential in Amulet and upcoming PFA and lithotripsy offerings.

On margins, I expect EBITDA to climb above 28% within four years, with free cash flow margins reaching high-teens to low-20%.

This should drive high single-digit to low double-digit FCF growth—performance that typically earns management teams effusive praise.

Valuation, however, is challenging after the recent surge. My former 5x revenue multiple only gets to around $125, while a more aggressive 6x model approaches $150—making me about as comfortable as a cat in a dog show.

I’m surprised by how quickly sentiment shifted on Abbott, likely due to investors seeking safety amid economic uncertainty.

Whether this outperformance has staying power remains uncertain, but Abbott is certainly delivering growth that matches or exceeds competitors across most business lines.

For now, I'm watching Abbott with the same fascination I once had for Sierra mountain expeditions—impressed by the ascent but keenly aware that the air gets thinner the higher you climb.

After all, what's that old market adage? Oh right—the view is spectacular, but nobody rings a bell at the top.

Mad Hedge Biotech and Healthcare Letter

November 12, 2024

Fiat Lux

Featured Trade:

(BONE OF CONTENTION)

(AMGN), (NVO), (LLY), (PFE), (VKTX), (GPCR), (AZN)

Mad Hedge Biotech and Healthcare Letter

November 12, 2024

Fiat Lux

Featured Trade:

(MEDTECH’S TRUMP CARD)

(RMD), (STE), (TNDM), (JNJ), (BDX), (MDT), (BSX), (SYK), (ZBH)

After seeing Trump sweep back into office, my phone's been ringing off the hook with one question: "What happens to my portfolio now?"

Look, I've been around this circus since covering Reagan in the White House press corps, and I can tell you that market hysteria rarely matches reality.

But this time, we need to pay attention - especially in the $567 billion medtech industry that's about to face some serious disruption.

What's different now? Trump's not just talking about those 10% to 20% blanket tariffs anymore - he's dead serious about slapping a potential 60% tariff on Chinese imports.

And after spending years watching supply chains twist themselves into pretzels during COVID, this is going to hit different.

To understand just how big this could be, let's look at what's really at stake here.

In vitro diagnostics makes up 18% of the medtech industry, and cardiology devices are sitting at $75 billion in 2024, expected to hit $95 billion by 2028.

Those aren't just numbers on a page - they represent real money that could take a serious hit. If these tariffs go through, we're looking at a 3.2% hit to S&P 500 earnings per share in 2025.

And it gets worse - add another 1.5% drop if our trading partners decide to play hardball with retaliatory tariffs.

Given all this, where should you put your money? The answer lies in looking at who's already ahead of the curve.

Well, established players like Johnson & Johnson (JNJ) and Becton Dickinson and Co. (BDX) are looking increasingly shrewd with their local-for-local manufacturing strategy.

They might not give you the same adrenaline rush as scaling Mount Everest, but they're solid holds in this environment.

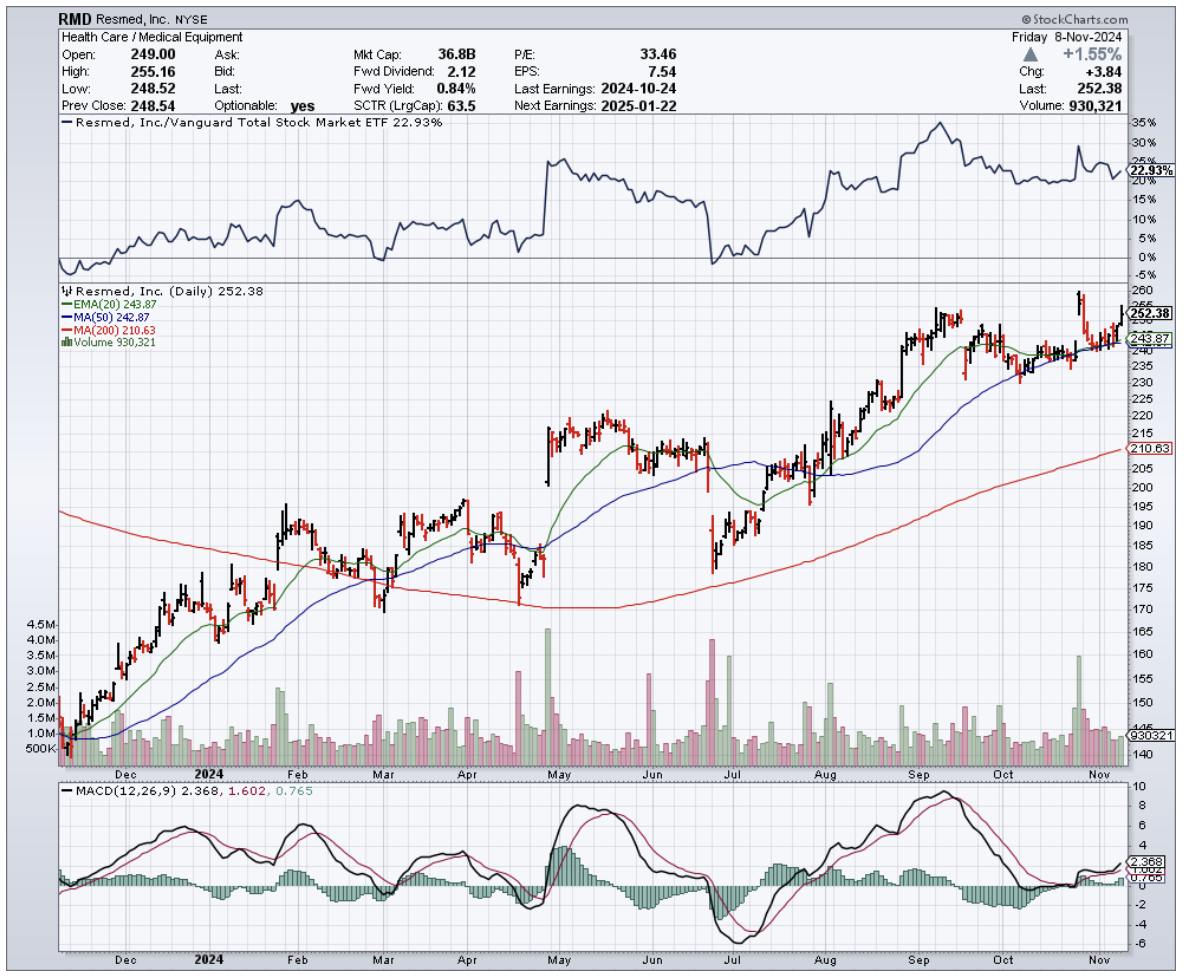

But they’re not the only companies securing their positions. ResMed (RMD), for instance, just posted third-quarter sales up 11% to $1.22 billion, with adjusted earnings jumping 34% to $2.20 per share.

That's not just good numbers - that's a company that knows how to execute regardless of who's in the White House.

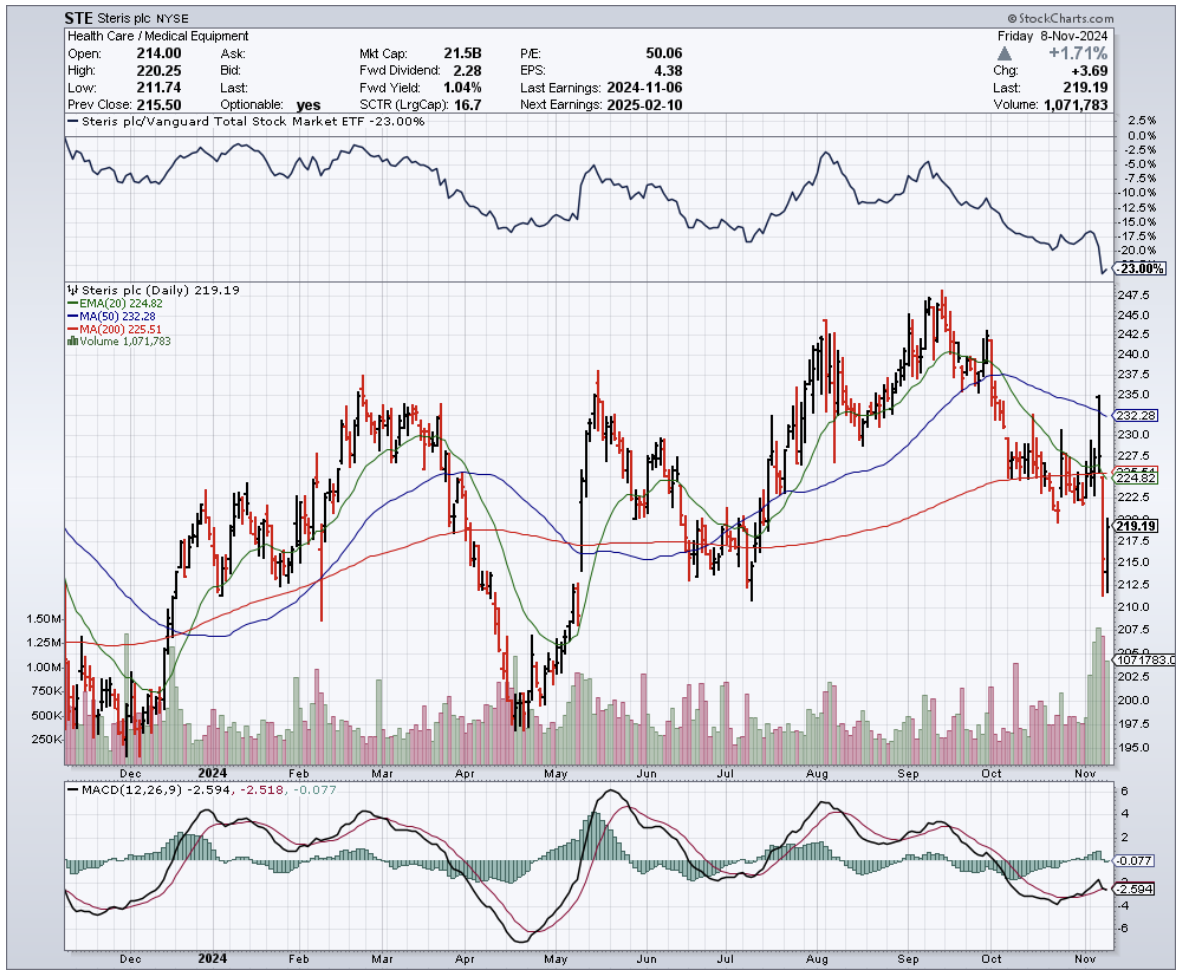

In the same vein, Steris deserves attention. Their "front-shoring" strategy in Malaysia isn't just smart - it's prescient. After years of covering Asia for The Economist, I can spot smart positioning when I see it.

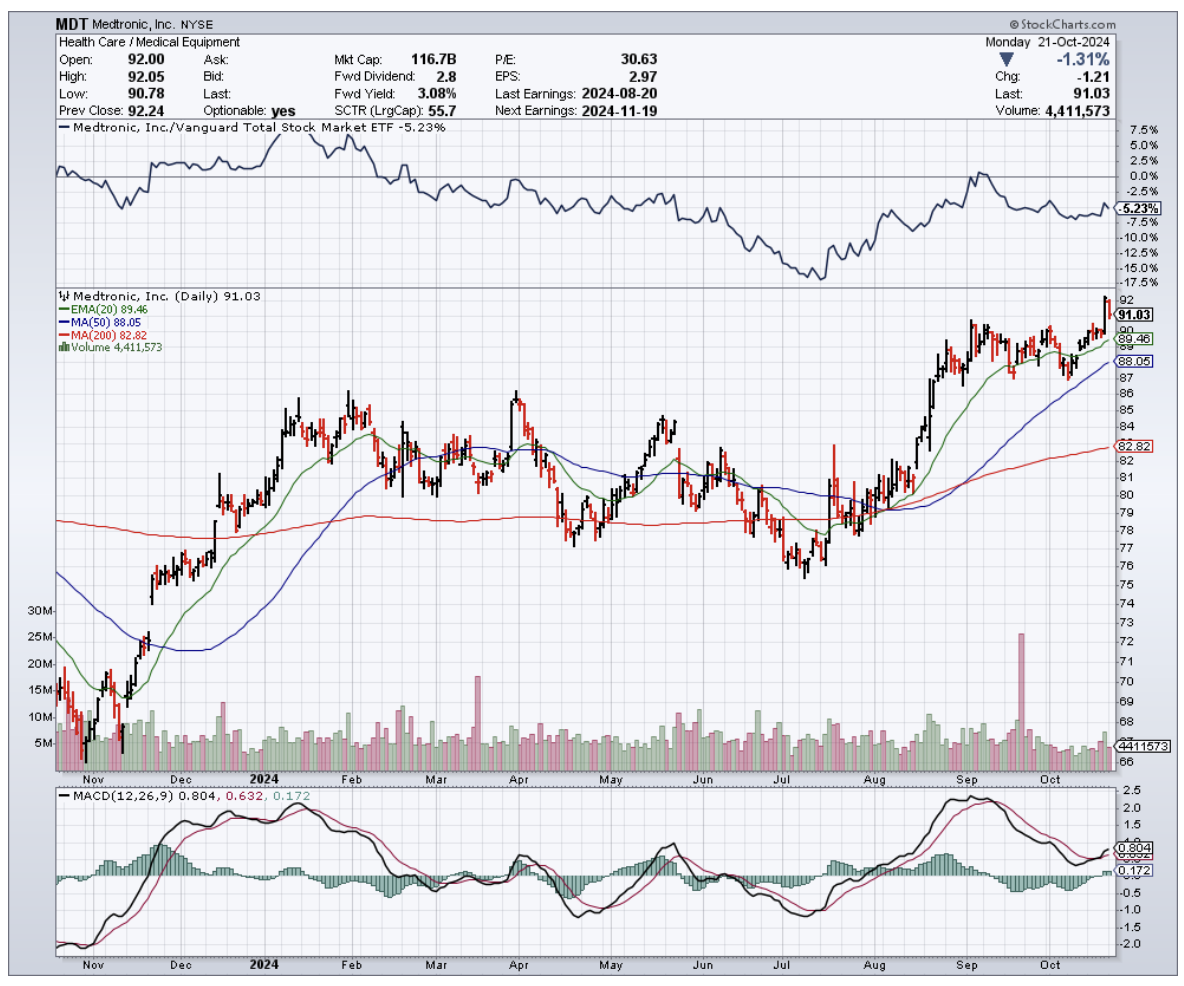

Now, let's talk about some of the bigger players in the room. Medtronic (MDT), our industry giant, is giving me pause.

Sure, they're a global leader, but their heavy reliance on Chinese manufacturing and components is about to become a serious headache under these new tariffs.

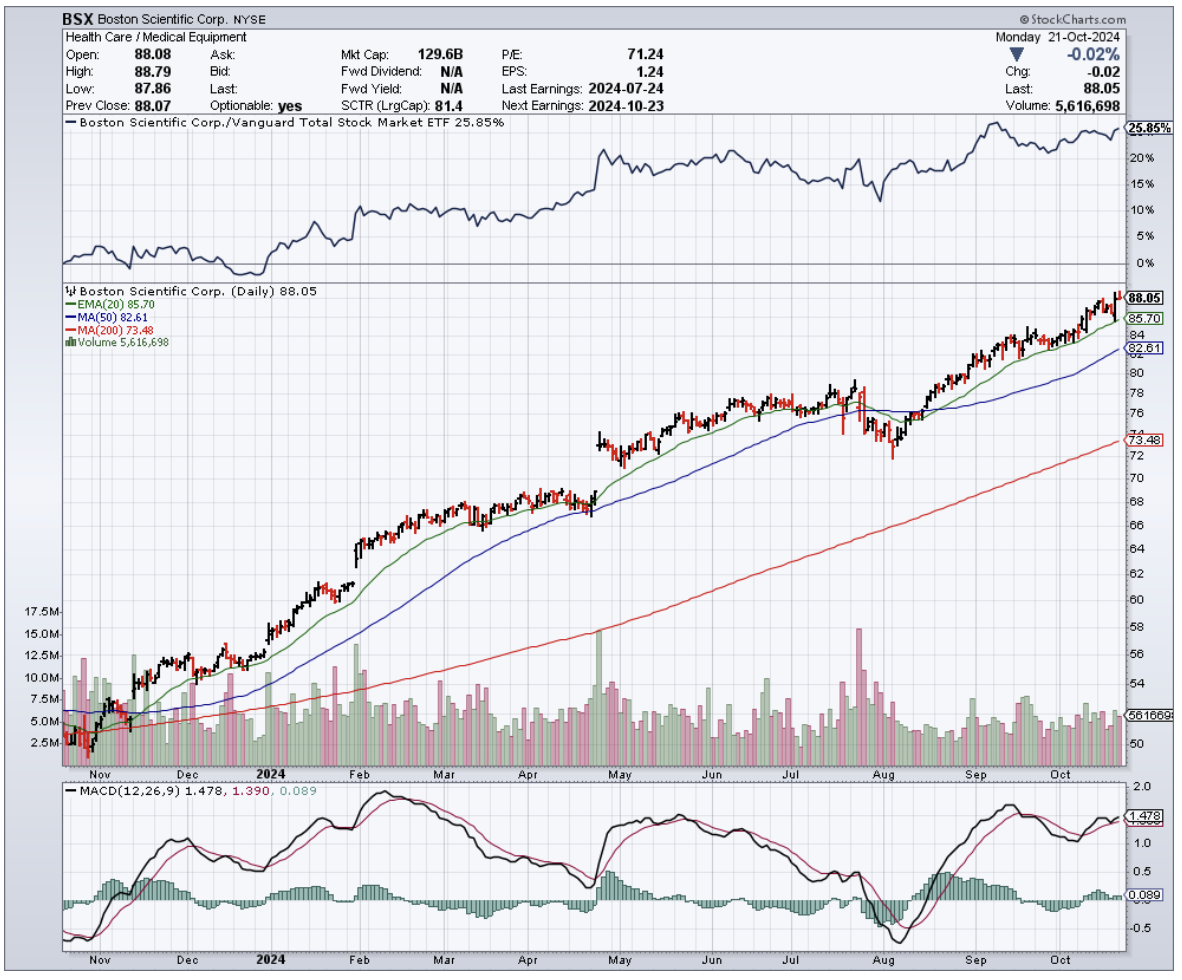

Same story with Boston Scientific (BSX) - they've got manufacturing facilities in China that could turn from assets to liabilities pretty quickly.

Stryker (SYK) and Zimmer Biomet (ZBH) are in the same boat, but with a twist. Both companies have been smart enough to spread their supply chains globally, but they're still catching enough Chinese exposure to make me nervous.

When those tariffs hit their component costs, watch their margins. This isn't just about bottom lines - it's about how much wiggle room these companies have to absorb higher costs without passing them on to hospitals and patients.

On the flip side, I'm watching companies like Tandem Diabetes Care (TNDM) with growing concern.

Their heavy Asian supply chain exposure under Trump's trade policies is going to be about as comfortable as my MIG-25 flight at 90,000 feet - and trust me, that wasn't comfortable at all.

But, what’s really telling is where the smart money is flowing.

Keep your eyes on three key trends that are reshaping the industry: supply chain resilience, M&A activity (now up 18% to $57.7 billion), and digital transformation.

About 30% of medtech companies are getting serious about digitizing their operations - and they're the ones to watch.

So, here's my bottom line: Trump's return is going to shake up medtech, but not every tremor is an earthquake.

The winners in this new landscape will be companies that have already diversified their manufacturing outside China, built up strong balance sheets to absorb these tariff impacts, and proven they can adapt - like ResMed and Steris have shown us.

The real champions will be those making serious investments in digital transformation. These are the companies that won't just survive Trump's trade policies - they'll thrive under them.

And if you're still holding onto companies with heavy Chinese exposure?

Well, let's just say it might be time to look for higher ground - and I'm speaking as someone who's made that call at both 20,000 feet on Everest and during the 2008 crash.

The medtech industry isn't going anywhere - people will always need medical devices. But which companies thrive under Trump's second term? That's going to depend on who's prepared for the storm and who's still standing in the open.

Now, if you'll excuse me, I've got some vintage wine to open. Making sense of these markets is thirsty work.

Mad Hedge Biotech and Healthcare Letter

October 22, 2024

Fiat Lux

Featured Trade:

(TICK TALK)

(AAPL), (ABT), (BSX), (MDT), (RMD), (INSP), (DXCM), (PODD)

While waiting two hours to vote at the Incline Village Library this weekend, I counted the number of smartwatches in the line.

Seemed like everyone was checking their heart rates in the cold. One woman's Apple Watch even suggested she sit down after standing too long in the 40-degree weather.

That got me thinking about the billions flowing into medical wearables - and where that money should really be going instead.

Let's start with some sobering numbers about atrial fibrillation (AFib), the crown jewel of smartwatch detection capabilities.

Yes, Apple's (AAPL) 2020 study showed their watches can detect 84% of AFib cases during monitoring sessions. Sounds impressive, until you dig deeper.

Of the 50 million Americans wearing smartwatches, these devices identify only about 5,000 new AFib cases annually - a mere 0.083% of the 6 million Americans affected by the condition.

Plus, the real money tells a different story. The U.S. performs 250,000 ablation procedures yearly, creating a $3.2 billion market growing at 10% annually.

Abbott Laboratories (ABT), Boston Scientific (BSX), and Medtronic (MDT) dominate this space, with combined annual revenues of $12.4 billion from their cardiac rhythm management divisions alone.

Those 5,000 smartwatch-detected cases? They represent just 2% of annual ablation procedures. Not exactly the revolution we've been promised.

The story doesn't improve when we look at sleep apnea detection.

While Apple and Samsung tout their sleep-monitoring capabilities, their watches identify only about 60,000 of the 2 million new sleep apnea cases diagnosed yearly - that's 3% of new diagnoses.

Meanwhile, ResMed (RMD) and Inspire Medical Systems (INSP) generated combined revenues of $4.8 billion last year from sleep apnea treatments.

The smartwatch contribution to their patient pipeline is barely a rounding error.

Still, it’s not like this sector is a complete waste. The global smartwatch market stands at $58 billion and is projected to reach $98 billion by 2027, growing at 10.5% annually. Impressive, until you compare it to the traditional medical device market: $495 billion, reaching $718 billion by 2029.

The cardiac monitoring device segment alone represents $24.5 billion, expanding at 6.9% annually.

More importantly, traditional medical device companies are growing their revenues faster than smartwatch detection is adding to their patient base.

But, like I said, don't write off the sector entirely. The next generation of smartwatches promises some intriguing possibilities.

Continuous blood pressure monitoring could tap into a $23 billion market.

Non-invasive glucose tracking might crack the $28 billion diabetes monitoring space by 2027.

Enhanced sleep diagnostics could open up another $12.8 billion in opportunities.

So what's the smart play here?

Near term, keep your focus on established leaders like Abbott and Medtronic. Their upcoming Q4 earnings reports will tell us more about traditional patient acquisition trends than any smartwatch sales figures.

Watch for FDA clearances too - Abbott's new cardiac mapping system, expected in Q1 2025, could be a game-changer.

Looking out 12-24 months, keep your eye on companies like Dexcom (DXCM) and Insulet (PODD) as glucose monitoring moves mainstream.

ResMed's new sleep diagnostic platforms, launching mid-2025, could redefine how we think about sleep medicine.

Meanwhile, Boston Scientific's push into AI-enhanced cardiac monitoring might just bridge the gap between consumer tech and serious medical devices.

For long-term thinkers, watch for companies developing hybrid solutions that combine traditional devices with consumer tech.

The real breakthrough will come when medical device makers start acquiring wearable technology companies. That's when you'll know the revolution is real.

Remember, following the patient flow matters more than following the hype flow. Just like timing your visit to avoid a two-hour voting line, timing in the market is everything.

And right now, the time is right for medical device stocks, not their flashier smartwatch cousins.

Mad Hedge Biotech and Healthcare Letter

September 21, 2023

Fiat Lux

Featured Trade:

(HEALTH MEETS WEALTH)

(BSX), (ABT), (JNJ), (MDT), (SYK)

In a state-of-the-art medical facility, a surgeon's hands move with precision, guiding a catheter towards the basivertebral nerve. Their mission is clear: to halt the persistent pain signals traveling to the brain, offering relief to those burdened by vertebrogenic pain. This is the real-world application of the Intracept system, a breakthrough in healthcare.

Boston Scientific Corporation (BSX) has recently made headlines by announcing its definitive agreement to acquire Relievant Medsystems, Inc., the very creators of the Intracept Intraosseous Nerve Ablation System. This power move, sealed with a cool $850 million upfront cash payment, also includes some exciting performance-based bonuses over the next three years.

Let's zoom in on the Intracept system for a moment. It's the only kid on the block with a nod from the U.S. Food and Drug Administration, specifically tailored for vertebrogenic pain. This sleek, implant-free outpatient procedure employs radiofrequency energy, acting like a mute button for the pain-causing basivertebral nerve.

And with over 5.3 million Americans wrestling with vertebrogenic pain, the ripple effect of this innovation is monumental. So, mark your calendars: the acquisition is set to be finalized in the first half of 2024 once all the formalities are squared away.

On the financial front, the future's looking bright for Relievant. They're gearing up to clock sales north of $70 million in 2023, with a growth spurt expected to zoom past 50% in 2024. And while the 2024 earnings per share (EPS) might not cause a big splash, 2025 and beyond are looking sunny.

While the acquisition is a major step, Boston Scientific's journey doesn't stop there.

Their Watchman device, which dominates its market segment, is poised to bring transformative changes to atrial fibrillation treatments. Just think of this gadget as a guardian angel for patients with non-valvular atrial fibrillation, shielding them from stroke risks without the ball-and-chain of long-term blood thinners.

Apart from this, Boston Scientific dropped some exciting news earlier this year about their ADVENT Study of the FARAPULSE Pulsed Field Ablation System (PFA). This nifty gadget uses electric fields to treat atrial fibrillation (AF), sidestepping the need to heat up the tissue. The study was a trailblazer, being the first to pit the FARAPULSE system against traditional AF treatments.

However, Boston Scientific's game plan goes beyond just gadgets and gizmos.

Their keen interest in Shockwave (SWAV) and a track record of smart acquisitions hint at a company that's always two steps ahead. This forward-thinking mindset has earned them nods of approval from both the medical community and sharp-eyed investors. The success of its ADVENT study, for instance, has further underscored its growing prominence in the sector.

In today's roller-coaster financial world, with storm clouds of economic downturns gathering, investors are on the hunt for solid ground. This is where Boston Scientific comes through. They're not just a safe harbor; they're also a vessel of growth.

With two solid quarters in the bag and a projected 11% revenue growth on the horizon, they're on a skyward journey. And while there might be some chatter about its share valuation, their blend of innovation and strategy makes every penny worth it.

In a nutshell, Boston Scientific is more than a company name; it's a promise of a brighter, healthier tomorrow. Moreover, the stock has consistently outpaced the broader medical device sector, gaining an edge of about 10% over notable competitors like Abbott (ABT), Johnson & Johnson (JNJ), Medtronic (MDT), and Stryker (SYK). This performance was evident even before the company unveiled the impressive results of its ADVENT study on the Farapulse ablation.

Currently, I remain optimistic about the potential of BSX shares. Granted, a forward revenue multiple of 6.5x isn't exactly modest, and the valuation might appear ambitious when assessed through traditional metrics like discounted free cash flow. However, top-tier growth med-tech stocks rarely come with a discount tag.

Given the prospects of Farapulse, Watchman label extension studies, innovative CRM products, the Agent drug-coated balloon, and growth avenues in peripheral intervention, endoscopy, and urology, Boston Scientific stands out as a unique growth narrative. Historically, investors have shown a willingness to pay premium multiples for such consistent growth in this market segment.

Mad Hedge Biotech and Healthcare Letter

June 8, 2023

Fiat Lux

Featured Trade:

(THE AI INFUSION)

(MDT), (NVDA), (GEHC), (LLY)