It’s official: Absolutely no one is confident in their long-term economic forecasts right now. I heard it from none other than the chairman of the Federal Reserve himself. The investment rule book has been run through the shredder.

It has in fact been deleted.

That explains a lot about how markets have been trading this year. It looks like it is going to be a reversion to the mean year. Forecasters, strategists, and gurus alike are rapidly paring down their stock performance targets for 2025 to zero.

When someone calls the fire department, it’s safe to assume that there is a fire out there somewhere. That’s what Fed governor Jay Powell did last week. It raises the question of what Jay Powell really knows that we don’t. Given the opportunity, markets will always assume the worst, that there’s not only a fire, but a major conflagration about to engulf us all. Jay Powell’s judicious comments last week certainly had the flavor of a president breathing down the back of his neck.

It's interesting that a government that ran on deficit reduction pressured the Fed to end quantitative tightening. That’s easing the money supply through the back door.

For those unfamiliar with the ins and outs of monetary policy, let me explain to you how this works.

Since the 2008 financial crisis, the Fed bought $9.1 trillion worth of debt securities from the US Treasury, a policy known as “quantitative easing”. This lowers interest rates and helps stimulate the economy when it needs it the most. “Quantitative easing” continued for 15 years through the 2020 pandemic, reaching a peak of $9.1 trillion by 2022. For beginners who want to know more about “quantitative easing” in simple terms,please watch this very funny video.

The problem is that an astronomically high Fed balance sheet like the one we have now is bad for the economy in the long term. They create bubbles in financial assets, inflation, and malinvestment in risky things like cryptocurrencies. That’s why the Fed has been trying to whittle down its enormous balance sheet since 2022.

By letting ten-year Treasury bonds it holds expire instead of rolling them over with new issues, the Fed is effectively shrinking the money supply. This is how the Fed has managed to reduce its balance sheet from $9.1 trillion three years ago to $6.7 trillion today and to near zero eventually. This is known as “quantitative tightening.” At its peak a year ago, the Fed was executing $120 billion a month quantitative tightening.

By cutting quantitative tightening, from $25 billion a month to only $5 billion a month, or effectively zero, the Fed has suddenly started supporting asset prices like stocks and increasing inflation. At least that is how the markets took it to mean by rallying last week.

Why did the Fed do this?

To head off a coming recession. Oops, there’s that politically incorrect “R” word again! This isn’t me smoking California’s largest export. Powell later provided the forecasts that back up this analysis. The Fed expects GDP growth to drop from 2.8% to 1.7% and inflation to rise from 2.5% to 2.8% by the end of this year. That’s called deflation. Private sector forecasts are much worse.

Just to be ultra clear here, the Fed is currently engaging in neither “quantitative easing nor “quantitative tightening,” it is only giving press conferences.

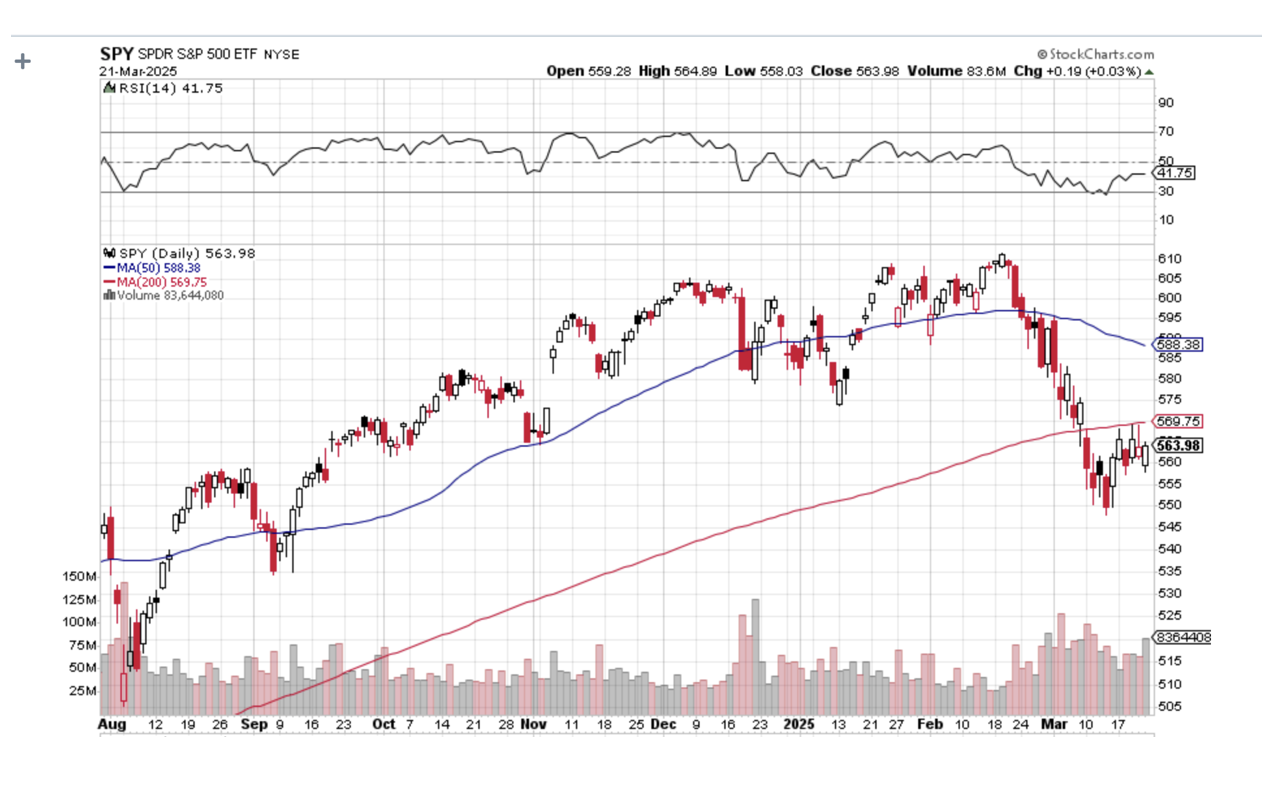

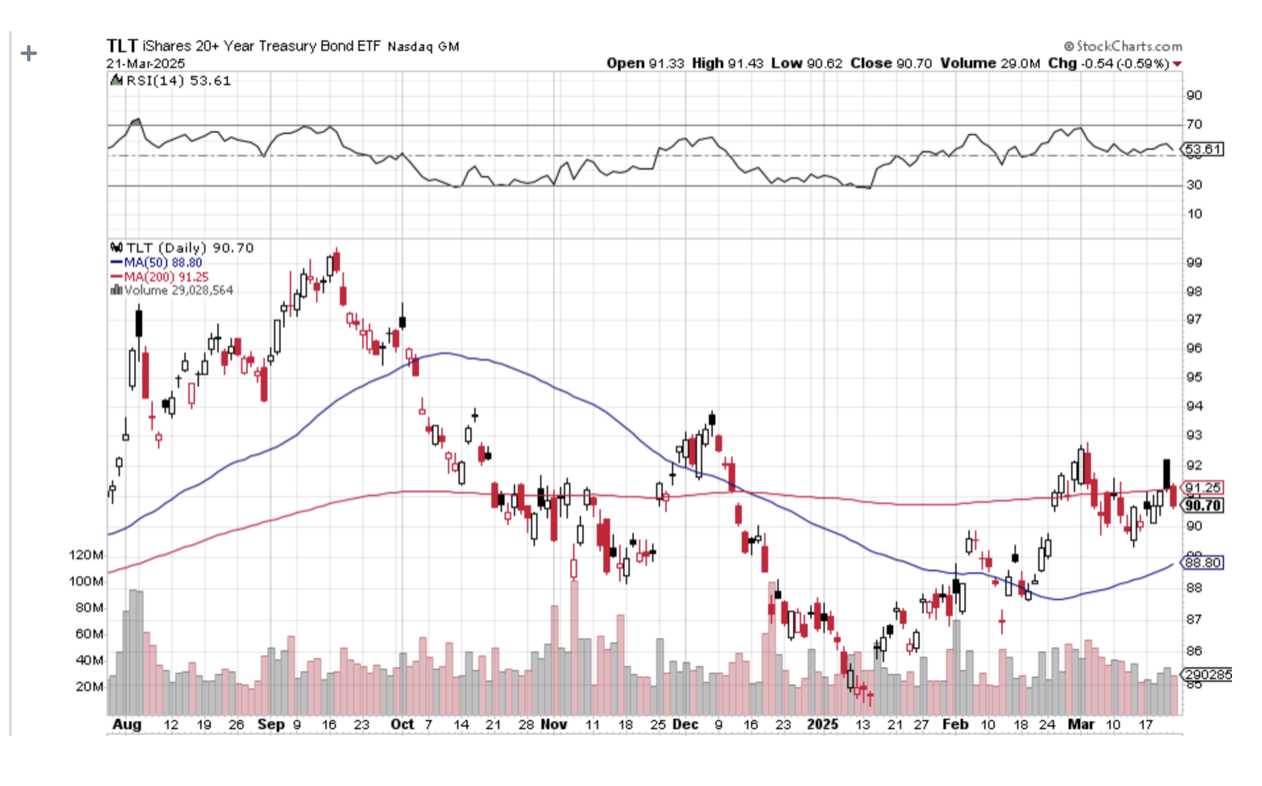

Bottom line: Keep selling stock rallies and buying bonds and gold on dips.

Another discussion you will hear a lot about is the debate over hard data versus soft data.

I’ll skip all the jokes about senior citizens and cut to the chase. Soft data are opinion polls, which are notoriously unreliable, fickle, and can flip back and forth between positive and negative. A good example is the University of Michigan Consumer Confidence, which last week posted its sharpest drop in its history. Consumers are panicking. The problem is that this is the first data series we get and is the only thing we forecasters can hang our hats on.

Hard data are actual reported numbers after the fact, like GDP growth, Unemployment Rates, and Consumer Price Indexes. The problem with hard data is that they can lag one to three months, and sometimes a whole year. This is why by the time a recession is confirmed by the hard data, it is usually over. Hard data often follows soft data, but not always, which is why both investors and politicians in Washington DC are freaking out now.

Bottom line: Keep selling stock rallies and buying bonds and gold (GLD) on dips.

A question I am getting a lot these days is what to buy at the next market bottom, whether that takes place in 2025 or 2026. It’s very simple. You dance with the guy who brought you to the dance. Those are:

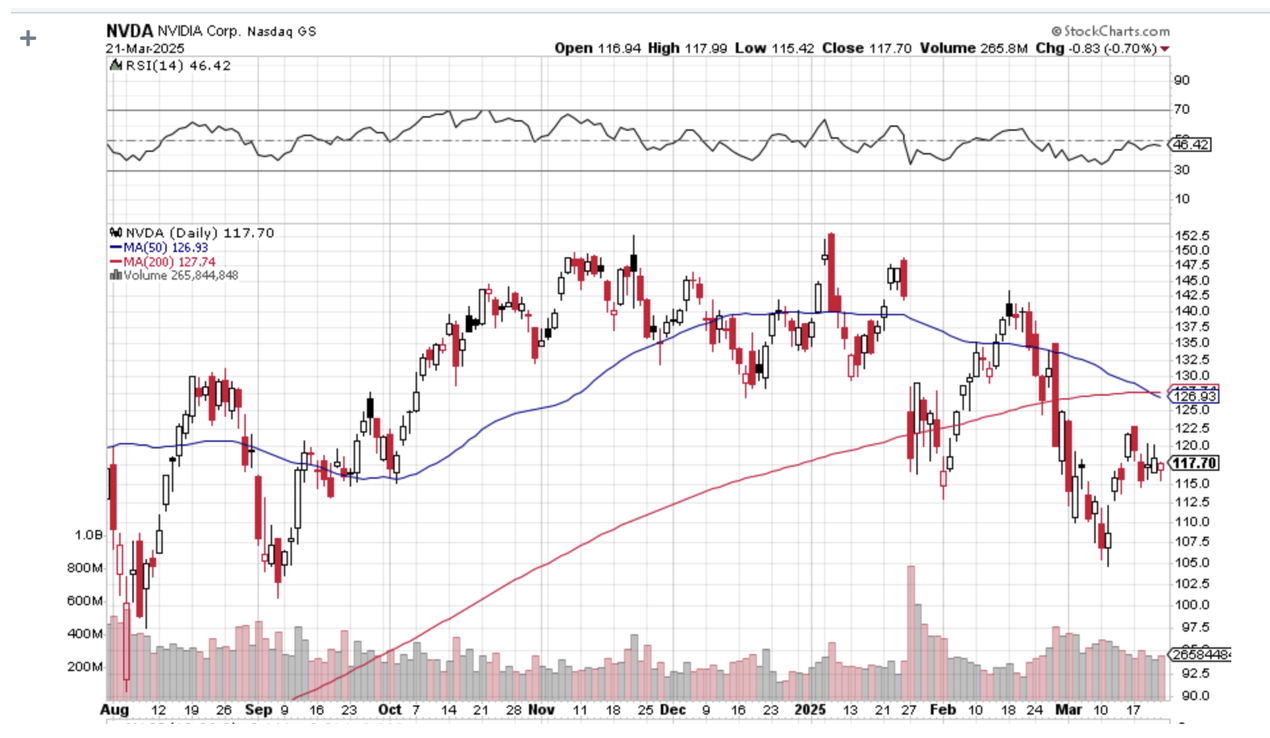

Best Quality Big Tech: (NVDA), (GOOGL), (AAPL), (META), (AMZN)

Big tech is justified by Nvidia CEO Jensen Huang’s comment last week that there will be $1 trillion in Artificial Intelligence capital spending by the end of 2028. While we argue over trade wars, AI technology and earnings are accelerating.

Cybersecurity: (PANW), (ZS), (CYBR), (FTNT)

Never goes out of style, never sees customers cut spending, and is growing as fast as AI.

Best Retailer: (COST)

Costco is a permanent earnings compounder. You should have at least one of those.

Best Big Pharma: (AMGN), (ABBV), (BMY)

Big pharma acts as a safety play, is cheap, and acts as a hedge for the three sectors above.

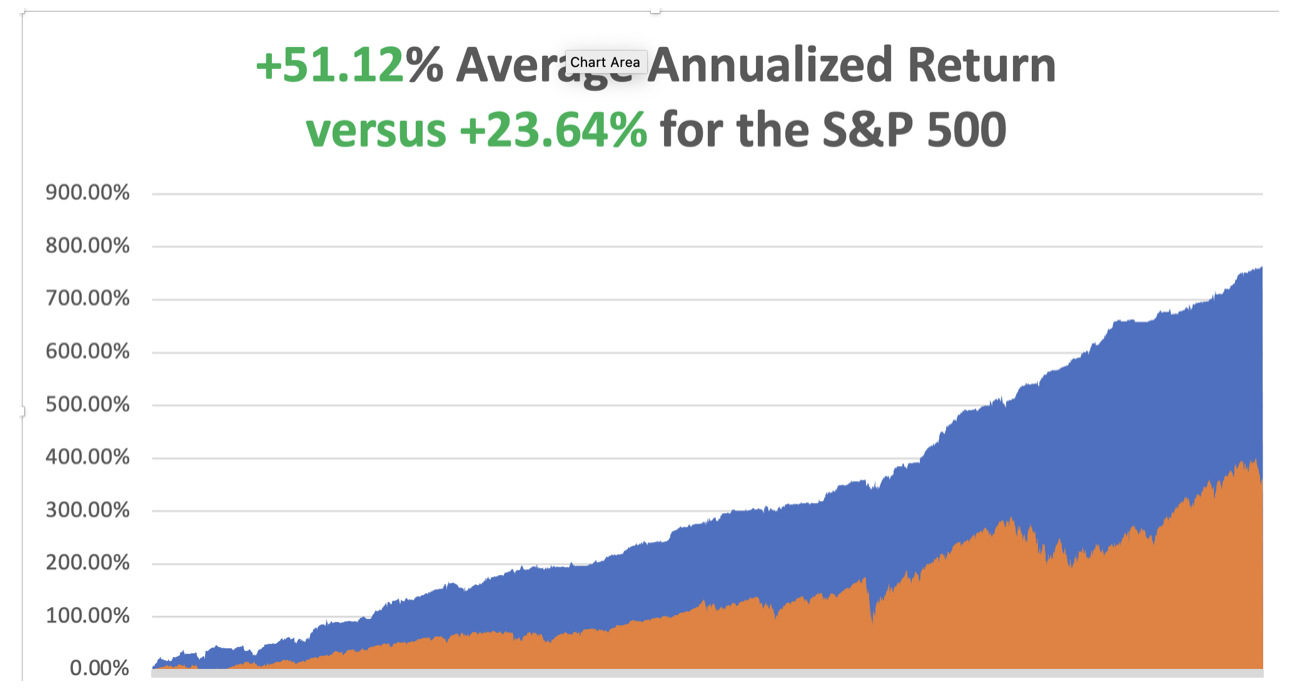

March is now up +2.92% so far. That takes us to a year-to-date profit of +12.29% in 2025. That means Mad Hedge has been operating as a perfect -1X short S&P 500 ETF since the February top. My trailing one-year return stands at a spectacular +82.50%. That takes my average annualized return to +51.12%and my performance since inception to +764.28%.

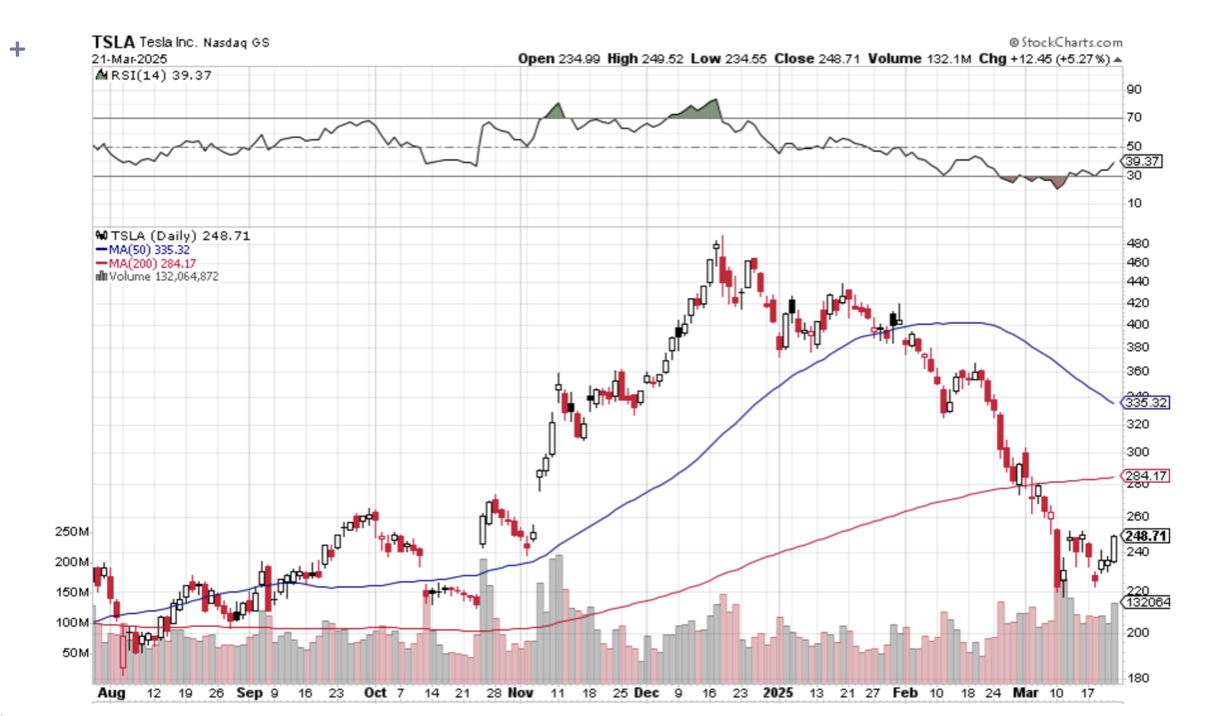

It has been another busy week for trading. I had four March positions expire at their maximum profit points on the Friday options expiration, shorts in (GM), and longs in (GLD), (SH), and (NVDA). I added new longs in (TSLA) and (NVDA). This is in addition to my existing longs in the (TLT) and shorts in (TSLA), (NVDA), and (GM).

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 74 of 94 trades have been profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

UCLA Andersen School of Business announced a “Recession Watch,” the first ever issued. UCLA, which has been issuing forecasts since 1952, said the administration’s tariff and immigration policies and plans to reduce the federal workforce could combine to cause the economy to contract. Recessions occur when multiple sectors of the economy contract at the same time.

Retail Sales Fade, with consumers battening down the hatches for the approaching economic storm. Retail sales rose by less than forecast in February and the prior month was revised down to mark the biggest drop since July 2021.

This Has Been One of the Most Rapid Corrections in History, leaving no time to readjust portfolios and put on short positions.

The rapid descent in the S&P 500 is unusual, given that it was accomplished in just 22 calendar days, far shorter than the average of 80 days in 38 other examples of declines of 10% or more going back to World War II.

Home Builder Sentiment Craters to a seven-month low in March as tariffs on imported materials raised construction costs, a survey showed on Monday. The National Association of Home Builders/Wells Fargo Housing Market Index dropped three points to 39 this month, the lowest level since August 2024. Economists polled by Reuters had forecast the index at 42, well below the boom/bust level of 50.

BYD Motors (BYDDF) Shares Rocket, up 72% this year, on news of technology that it claims can charge electric vehicles almost as quickly as it takes to fill a gasoline car. BYD on Monday unveiled a new “Super e-Platform” technology, which it says will be capable of peak charging speeds of 1,000 kilowatts/hr. The EV giant and Tesla rival say this will allow cars that use the technology to achieve 400 kilometers (roughly 249 miles) of range with just 5 minutes of charging. Buy BYD on dips. It’s going up faster than Tesla is going down.

Weekly Jobless Claims Rise 2,000, to 223,000. The number of Americans filing new applications for unemployment benefits increased slightly last week, suggesting the labor market remained stable in March, though the outlook is darkening amid rising trade tensions and deep cuts in government spending.

Copper Hits New All-Time High, at $5.02 a pound. The red metal has outperformed gold by 25% to 15% YTD. It’s now a global economic recovery that is doing this, but flight to safety. Chinese savers are stockpiling copper ingots and storing them at home distrusting their own banks, currency, and government. I have been a long-term copper bull for years as you well know. New copper tariffs are also pushing prices up. Buy (FCX) on dips, the world’s largest producer of element 29 on the Periodic Table.

Boeing (BA) Beats Lockheed for Next Gen Fighter Contract for the F-47, beating out rival Lockheed Martin (LMT) for the multibillion-dollar program. Unusually, Trump announced the decision Friday morning at the White House alongside Defense Secretary Pete Hegseth. Boeing shares rose 5.7% while Lockheed erased earlier gains to fall 6.8%. The deal raises more questions than answers, in the wake of (BA) stranding astronauts in space, their 737 MAX crashes, and a new Air Force One that is years late. Was politics involved? You have to ask this question about every deal from now on.

Carnival Cruise Lines (CCL) Raises Forecasts, on burgeoning demand from vacationers, including me. The company’s published cruises are now 80% booked. Cruise lines continue to hammer away at the value travel proposition they are offering. However, the threat of heavy port taxes from the administration looms over the sector.

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties is now looking at multiple gale-force headwinds. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. My Dow 240,000 target has been pushed back to 2035.

On Monday, March 24, at 8:30 AM EST, the S&P Global Flash PMI is announced.

On Tuesday, March 25, at 8:30 AM, the S&P Case Shiller National Home Price Index isreleased.

On Wednesday, March 26, at 1:00 PM, the Durable Goods are published.

On Thursday, March 27, at 8:30 AM, the Weekly Jobless Claims are disclosed. We also get the final report for Q1 GDP.

On Friday, March 28, the Core PCE is released, and important inflation indicator. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I received calls from six readers last week saying I remind them of Ernest Hemingway. This, no doubt, was the result of Ken Burns’ excellent documentary about the Nobel Prize-winning writer on PBS last week.

It is no accident.

My grandfather drove for the Italian Red Cross on the Alpine front during WWI, where Hemingway got his start, so we had a connection right there.

Since I read Hemingway’s books in my mid-teens I decided I wanted to be him and became a war correspondent. In those days, you traveled by ship a lot, leaving ample time to finish off his complete work.

I visited his homes in Key West, Cuba, and Ketchum Idaho.

I used to stay in the Hemingway Suite at the Ritz Hotel on Place Vendome in Paris where he lived during WWII. I had drinks at the Hemingway Bar downstairs where war correspondent Ernest shot a German colonel in the face at point-blank range. I still have the ashtrays.

Harry’s Bar in Venice, a Hemingway favorite, was a regular stopping-off point for me. I have those ashtrays too.

I even dated his granddaughter from his first wife, Hadley, the movie star Mariel Hemingway, before she got married, and when she was also being pursued by Robert de Niro and Woody Allen. Some genes skip generations and she was a dead ringer for her grandfather. She was the only Playboy centerfold I ever went out with. We still keep in touch.

So, I’ll spend the weekend watching Farewell to Arms….again, after I finish my writing.

Oh, and if you visit the Ritz Hotel today, you’ll find the ashtrays are now glued to the tables.

As for last summer, I stayed in the Hemingway Suite at the Hotel Post in Cortina d’Ampezzo Italy where he stayed in the late 1940’s to finish a book. Maybe some inspiration will run off on me.

Hemingway’s Living Room in Cuba, Untouched Since 1960

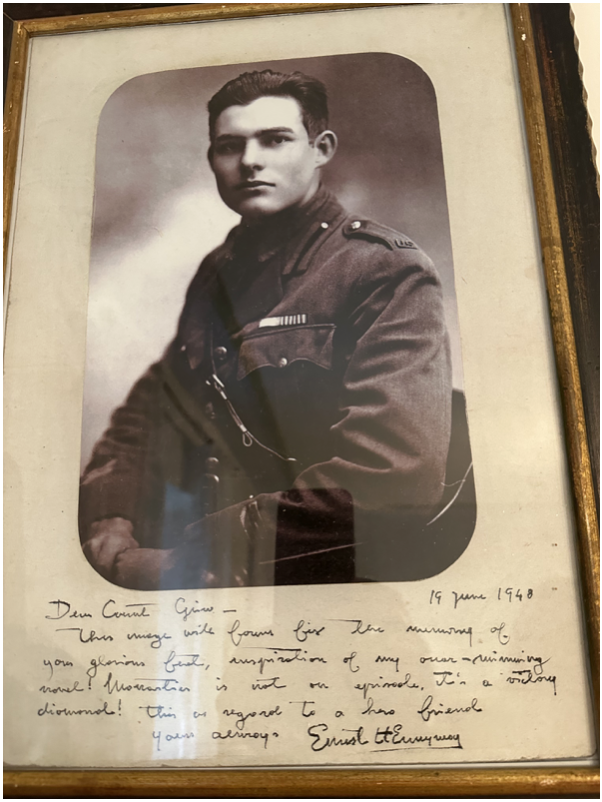

Earnest in 1918

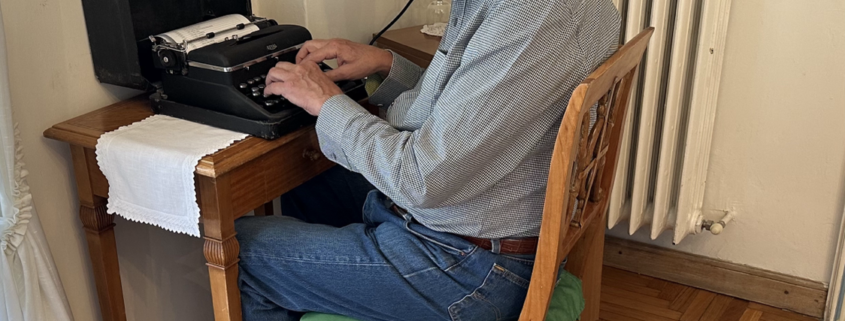

Typing at Hemingway’s Typewriter in Italy from the 1940’s

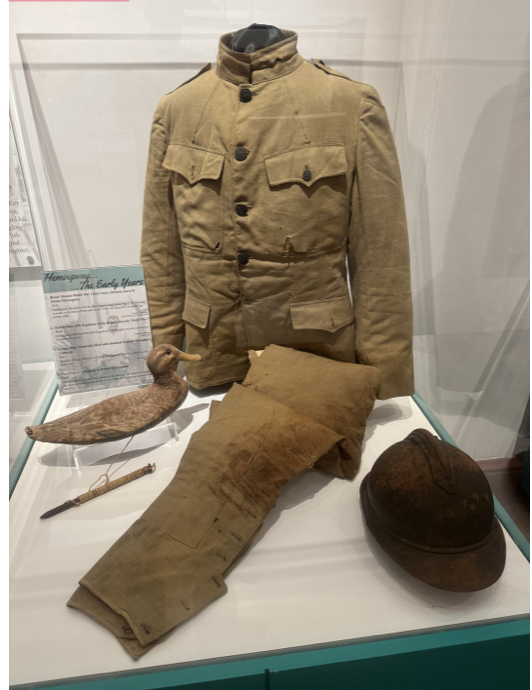

The Red Cross Uniform Hemingway Wore when He was Blown Up in 1917

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/01/John-thomas-typewriter.png11861124april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-24 09:02:532025-03-24 13:19:15The Market Outlook for the Week Ahead, or The Special No Confidence Issue

Below please find subscribers’ Q&A for the February 7 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: Have you ever flown an ME-262?

A: There's only nine of the original German jet fighters left from WWII in museums. One hangs from the ceiling in the Deutsches Museum in Munich (click here for the link), I have been there and seen it and it is truly a thing of beauty. You would have to be out of your mind to fly that plane, because the engines only had a 10 hour life. That's because during WWII, the Germans couldn't get titanium to make jet engine blades and used steel instead, and those fell apart almost as soon as they took off. So, of the 1,443 ME-262’s made there’s only nine left. The Allies were so terrified of this plane, which could outfly our own Mustangs by 100 miles per hour, that they burned every one they found. That’s also why there are no Japanese Zeros.

Q: Thoughts on Palantir (PLTR) long term?

A: I love it, it’s a great data and security play. Right now, markets are revaluing all data plays, whatever they are. But it is also overvalued having almost doubled in a week.

Q: What do you make of all these layoffs in Silicon Valley? What does this mean for tech stocks?

A: It means tech stocks go up. The tech stocks for a long time have practiced over-employment. They were growing so fast, they always kept a reserve of about 10% of extra staff so they could be put them to work immediately when the demand came. Now they are switching to a new business model: fire everybody unless you absolutely have to have them right now, and make everybody you have work twice as hard. That greatly increases the profitability of these companies, as we saw with META (META), which had its profits triple—and that seems to be the new Silicon Valley business model. If you're one of the few 100,000 that have been laid off in Silicon Valley, eventually the economy will grow back to where they can absorb you. That's how it's going to play out. In the meantime, go take a vacation somewhere, because you're not going to get any vacations once you get a new job.

Q: I have had shares of Alibaba (BABA) since 2020 and the stock has been in free fall since. Should I take the 80% loss or hold?

A: Well, number one, you need to learn about risk control. Number two, you need to learn about stop losses. I stop out when things go 10% against me; that's a good level. At 80%, you might as well keep the stock. You've already taken the loss and who knows, China may recover someday. It's not recovering now because no foreigners want to invest in China with all the political risk and invasion risk of Taiwan. After all, look at what happened to Russia when they invaded Ukraine—that didn't work out so well for them.

Q: On the Chinese economy (FXI), is the poorer performance due to the decision to move to a war economy? The move in the economic front was described in Xi's speech to the CCP in January of 2023.

A: The real reason, which no one is talking about except me, is the one child policy, which China practiced for 40 years. What it has meant is you now have 40 years of missing consumers that were never born. And there is no solution to that, at least no short-term solution. They're trying to get Chinese people to have more kids now, and you're seeing three and four child families for the first time in 40 years in China. But there is no short-term fix. When you mess with demographics, you mess with economic growth. We warned the Chinese this would happen at the time, and they ignored us. They said if they hadn't done the one child policy, the population of China today would be 1.8 billion instead of 1.2 billion. Well, they’re kind of damned no matter what they do so there was no good solution for them. Of course, threatening to invade your neighbors is never good for attracting foreign investment for sure. Nobody here wants to touch China with a 10-foot pole until there’s a new leader who is more pacifist.

Q: What do you think of Eli Lilly (LLY)?

A: I absolutely love it. If there's a never-ending bull market in fat Americans, which is will go on forever, they're one of two companies that have the cure at $1,000 a month. On the other hand, the stock has tripled in the last 18 months, so it’s kind of late in the game to get in.

Q: Are there any stocks that become an attractive short in the event of a Taiwan invasion, such as Taiwan Semiconductor (TSM)?

A: All stocks become attractive shorts in the event of another war in China. You don't want to be anywhere near stocks and the semis will have the greatest downside beta as they always do. You don't want to be anywhere near bonds either, because the Chinese still own about a trillion dollars’ worth of our bonds. Cash and T-bills suddenly looks great in the event of a third war on top of the two that we already have in Gaza and Ukraine.

Q: What do you think about the prospects of the Japanese stock market now?

A: I think the big move is done; it finally hit a new high after a 34-year wait. The next big move in Japan is when the Yen gets stronger, and that is bad for Japanese stocks, so I would be a little cautious here unless you have some great single name plays like Warren Buffett does with Mitsubishi Corp. (MSBHF). So that's my view on Japan—I'm not chasing it after being out for 34 years. Why return? The companies in the US are better anyway.

Q: What is the deal with Supermicro Computer (SMCI)? It went up 23 times in a year to $669 after not clear $30 for a decade.

A: The answer is artificial intelligence. It is basically creating immense demand for the entire chip ecosystem, including high end servers, which Supermicro makes. It also has the benefit of being a small company with a small float, hence the ballistic move. It was too small to show up on my radar. I’ll catch the next one. There are literally thousands of companies like (SMCI) in Silicon Valley.

Q: Will JP Morgan (JPM) bank shares keep rising, or will they fall when the Fed cuts rates?

A: (JPM) will keep rising because recovering economies create more loan demand, allow wider margins, and cause default rates to go down. It becomes a sort of best case scenario for banks, and JP Morgan is the best of the breed in the banking sector. It also benefits the most from the concentration of the US banking sector, which is on its way from 4,000 banks to 6 with help from the US government.

Q: Is India a good long-term play? Which of the two ETFs I recommend are the better ones?

A: Yes, India is a good long-term play. You buy both iShares India 50 (INDY) and the iShares MSCI India (INDA), which I helped create yonks ago. India is the new China, and the old China is going nowhere. So, yes, India definitely is a play, especially if the dollar starts to weaken.

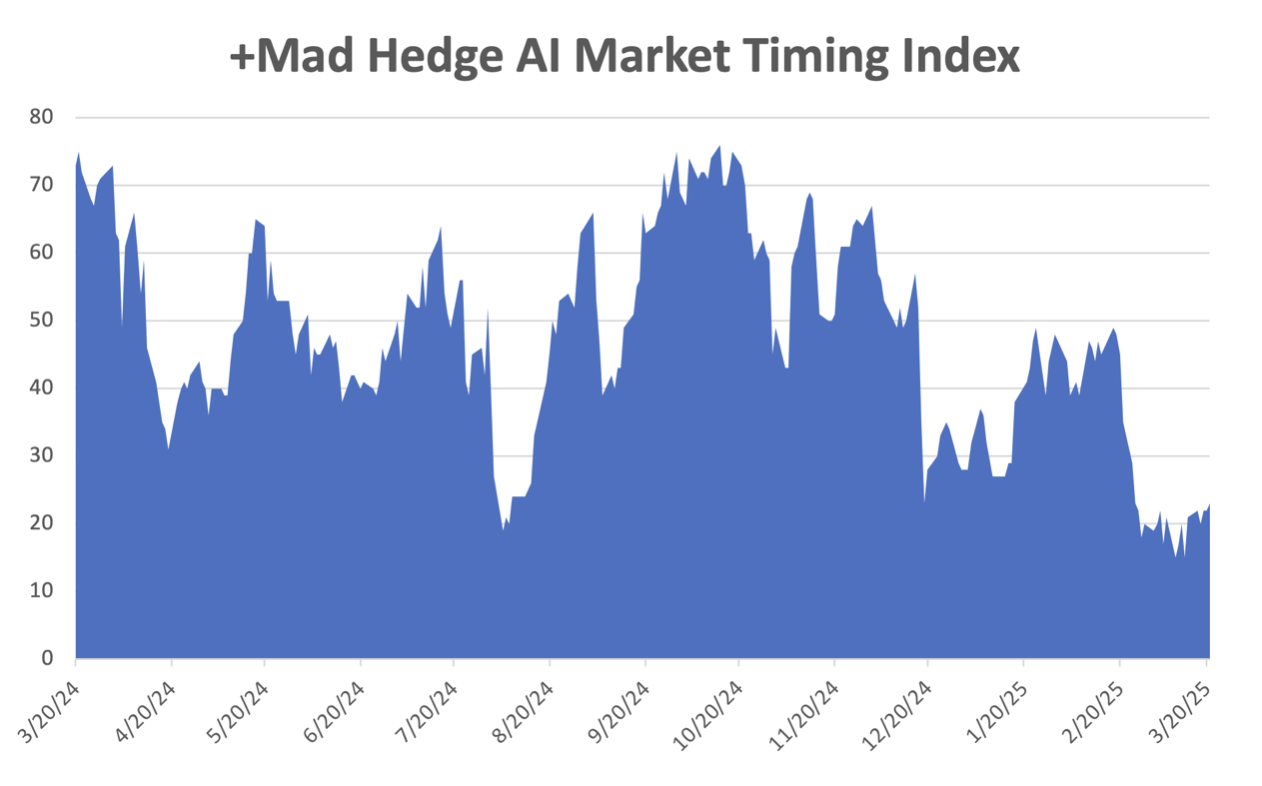

Q: Do you expect to pull back in your market timing index?

A: Yes, probably this month. Have I ever seen it go sideways at the top for an extended period? No, I haven't. On the other hand, we’ve never had a new thing like artificial intelligence hit the market, nor have we seen five stocks dominate the entire market like we're seeing now. So, there are a lot of unprecedented factors in the market now which no one has ever seen before, therefore they don't know what to do. That is the difficulty.

Q: Does India have an in-country built EV, and what is their favorite EV in India?

A: No, but Tesla (TSLA) is talking about building a factory there. And I would have to say BYD Motors (BYDDF) because they have the world’s cheapest EV’s. There is essentially no car regulation in India except on imports. Car regulation and safety requirements is what keeps the BYDs out of the United States, and it's kept them out for the last 15 years. So that is the issue there.

Q: What do you think about META as a dividend play?

A: I think META will go higher, but like the rest of the AI 5, it is desperately in need of a pull back and a refresh to allow new traders to come in.

Q: Why does Netflix (NFLX) keep going up? I thought streaming was saturated—what gives?

A: Netflix won the streaming wars. They have the best content and the best business strategy; and they banned sharing of passwords, which hit my family big time since it seemed like the whole world was using my Netflix password. And no, I'm not going tell you what my password is. I’ve already paid for Griselda enough times. Seems there is a lot of demand for strong women in my family. Netflix they seem to be enjoying a near monopoly now on profits.

Q: Has the NASDAQ come too far too fast, and does it have more to run?

A: Well it does have more to run, but needs a pull back first. I'm thinking we'll get one this month, but I'm definitely not shorting it in the meantime.

Q: Have you ordered your Tesla (TSLA) Cybertruck?

A: I actually ordered it two years ago and it may be another two year wait; with my luck the order will come through when I'm in Europe and I'll miss it. Some of my friends have already gotten deliveries because they ordered on day one. They love it.

Q: What happened to United States Natural Gas (UNG)?

A: A super cold spell hit the Midwest, froze all the pipes, and nobody could deliver natural gas just when the power companies were screaming for more gas. That created the double in the price which you should have sold into! Usually, people don't need to be told to take a profit when something doubles in 2 weeks, but apparently there are some out there as I've been here getting emails from them. Further confusing matters further is that (UNG) did a 4:1 reverse split right at this time. They have to do this every few years or the 35% a year contango takes the price below $1.00 and shares can’t trade below $1.00 on the New York Stock Exchange.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Below please find subscribers’ Q&A for the December 13 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: I think it's a good time to buy gold, do you agree? If so, what are your top picks for a long-term hold?

A: I was looking at some very long-term gold charts, and gold tends to have really hot and really cold decades, and we're just finishing a cold decade. In fact, the price of gold today is roughly where it was 12 years ago—it hasn't moved in 12 years. But if you look at the decade before that, it went up ten times from $200 to $2,000, so we're about to enter another hot decade. It may not go up 10X, but 5X is realistic. That would take us up from $2,000 to $10,000, and I think we could see $3,000 as early as 2025.

The best plays are always the gold miners. And my two favorite picks there are Barrick Gold (GOLD) and Newmont Mining (NEM). If you want to be even more aggressive than that, the underlying miners tend to go up at four times the rate of the gold metal. I can also go with junior minors who probably are losing money now, but if gold goes up to $5,000, they'll make money. Those are hugely leveraged, high-risk plays.

Q: Is it time to sell Tesla (TSLA) stock on all long-term accounts?

A: It is not. If you truly are long-term, I think Tesla goes to $10,000 eventually, but we are in the middle of a price war. Price wars are not when you want to be involved in the stock, so I wouldn't be adding to Tesla positions here—I want to see what the final bottom looks like, when the price wars end the prices start to go up, and we'll get that with an economic recovery next year.

Q: Who are Tesla's prime competitors?

A: I would say it's BYD CO., INC. (BYDDF) in China. BYD, which I visited in China 12 years ago, is actually out selling Tesla in China, and they have the ability to produce a super cheap car. They have a $25,000 car in Europe right now, and the fear is that they will make a $15,000 car, and then flood the United States with it. I doubt that will happen; they've never been able to reach American quality and safety standards, and that's why you don't see Chinese cars here. You do see them in other countries like Australia, Hong Kong, and parts of Africa; and they're currently making a big push in Europe, which certainly has all the German car producers worried. Competition is out there and does pose a risk to Tesla, but I think long-term Tesla still wins anyway. By the way, I hasten to mention there are no American competitors to Tesla. Tesla is so far ahead that the big three will never ever catch up and eventually just be reduced to selling Teslas on license.

Q: Where do you think the bottom in oil is?

A: The consensus in the market right now is $62 a barrel. That's about another $6 or $8 lower than here, and then I think we really do bottom out. Then you want to start piling into oil producers like ExxonMobil (XOM), which we had a position in last week, and Occidental Petroleum (OXY), which is the number one pick by Berkshire Hathaway. So those are two good names to go with. What drives these and all other commodities in the future? The answer is a recovering economy. Let's assume we drop from 5.2% last quarter to maybe 2% this quarter—we will accelerate to 5% next quarter, and that's what takes all of your commodity plays upward.

Q: Would you buy retailers here like Walmart (WMT) or Target (TGT)?

A: No. The time to buy retailers is in the run-up to Christmas. I don't know about you, but I'm finished with all my Christmas shopping! You want to buy in the run-up to Christmas shopping, not when it's peaking. Target on the other hand has done really well, and on a massive cost-cutting effort.

Q: When do you think is the first interest rate cut?

A: Since the market has a consensus of May, with some people saying March, I'll go for June. I think this Fed wants to torture us a little bit more and delay any interest rate cuts, but markets will discount that anyway. So it all sets up a great backdrop to buy stocks now, because markets discount things six months in advance, and six months from now is May. That's why we've had the ballistic moves that we've seen in stocks.

Q: Whatever happened to the natural gas trade United States Natural Gas Fund (UNG)?

A: The problem with all these commodity trades is that they are all in one way or another dependent on the weather, and we are having a warm winter, so you can't fool Mother Nature. Not only is it warm here, but it's warm in China, and in Europe. I think they have this thing called…global warming? It makes you ask yourself if you even want to be near an energy trade during a time of global warming, which is accelerating. So anyway, we had a nice profit on this in October—it completely went away. The (UNG) ETF went from $8 all the way down to $4.50, so we'll just have to wait for the cold weather and for (UNG) to ramp up. If it doesn’t happen soon, we may not have a rally this year in natural gas. Pray for snow!

Q: Is junk the best to buy in bonds?

A: It's the best risk-reward ratio; it has a yield roughly 50% higher than TLT with only slightly more risk. The default ratio on junk bonds is actually quite low. And in fact, before you buy (JNK) (SPDR Bloomberg High Yield Bond ETF) or (HYG) (iShares iBoxx $ High Yield Corporate Bond ETF), go to the website and look at their largest holdings and you’ll see what I mean, it's all airlines and cruise lines which had to load up on debt during the pandemic but are doing great right now.

Q: How can the market still rally if it's time to sell and take profit?

A: We get a round of profit-taking at some point, and there's your entry point. Right now, no professional trader is buying anything right now, they're just holding back and seeing when they take profits. And the way traders think is they don't want to trade anymore until they get paid! The year end is ending shortly and the risk-reward favors taking profits and then sitting on the profits. Guess what I'm doing? I'm taking profits and sitting on the profits because traders have bonuses that tend to get paid in January.

Q: On the (TLT) put trade, should one get out once it hits $95?

A: Yes, I always stop out when we hit the nearest strike on a call spread or a put spread. That's a good discipline to have. 90% of the time, if you hold on to expiration, you make the maximum profit in these, but that 10% of the time it's a total write-off, so you get to choose. I try to keep the volatility of the Mad Hedge service low so I always stop out quickly—easier to dig yourself out of a small hole than a big one.

Q: How do you think the next two government shutdowns in January and February will affect the market? Is this a buying opportunity?

A: Absolutely, yes, it is a buying opportunity. Shutdowns tend to be short, but you may get a lot of political turmoil, especially in the House. After the Long Island by-election to replace the disgraced George Santos the Republican majority is likely to shrink to only two seats. The House could fire another speaker, for example. We're kind of in unprecedented territory here in terms of the US government, but at any stock market decline, you would be a big buyer. That's how to play it. If people want to puke out on what's happening in Washington—thank you very much, I'll take your stock.

Q: Are we still bullish on the Barack Gold (GOLD) LEAPS?

A: Absolutely, especially if you have the 2025 expiration. There is an easy double or triple here.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The current chip war with China brings back memories of my five-decade-long relationship with the People’s Republic of China.

I normally avoid the diplomatic circuit, as the few non-committal comments and soggy appetizers I get aren’t worth the investment of time.

But I jumped at the chance to celebrate the 62nd anniversary of the founding of the People’s Republic of China with San Francisco Consul General Gao Zhansheng.

Happy Birthday, China!

When I casually mention that I survived the Cultural Revolution and interviewed major political figures like Premier Deng Xiaoping, who launched the Middle Kingdom into the modern era, and his predecessor, Zhou Enlai, modern-day Chinese are enthralled. It’s like going to a Fourth of July party and letting drop that I palled around with Thomas Jefferson and Benjamin Franklin.

Five minutes into the great hall, I ran into my old friend Wen, who started out her career with the Chinese Intelligence Service and had made the jump to the Foreign Ministry, as all their best people did. She was passing through town with a visiting trade mission.

When I was touring China in the seventies as a guest of the Bank of China, Wen was assigned as my guide and translator, and we kept in touch over the years. I was assigned a bodyguard who doubled as the driver of a tank-like Russian sedan.

The Cultural Revolution was on, and while the major cities were safe, we ran the risk of running into a renegade band of xenophobic Red Guards, with potentially fatal consequences.

I asked Wen when China was going to float the Yuan. She explained that this is something China knew it had to do, but it wasn’t going to be rushed into by some opportunistic foreign politicians.

If it moves too soon, millions will lose jobs, creating political instability, something the central government wants to avoid at all costs. Many of the largest scale employers were only marginally profitable, and a hike in the renminbi of only a few percent would force them out of business. I pointed out that that was exactly what was happening in the US.

Worth More Than Meets the Eye

I warned that if the Middle Kingdom waited too long, Washington would force them into an appreciation through punitive import duties and anti-dumping actions, as we did with Japan 50 years ago.

It was Nixon’s surprise ban on textile imports in 1971 that finally persuaded Japan to float the yen, then at ¥360. If that didn’t convince the Chinese, then imported inflation would. The longer China delays, the bigger the pop when their currency is finally set free.

Wen then went on the offensive, claiming that Chinese workers were being exploited by American companies keeping wages low. The product that China made for $1, and sold to the US for $2, was then sold by Walmart (WMT) for $20, which kept all the profits.

She pointed out that the Walton family had a combined net worth of $238 billion, more than the total worth of the lower 40% of the US population. This could never happen in China.

I told her that by selling the product at $20, Walmart wiped out another US company that used to make that product domestically and sold it for $40, throwing those people out of work.

Modern Times in China

I then asked Wen what were her country’s plans for its massive foreign exchange reserves, now at $3.2 trillion. She agreed that this was a problem because the reserves were pouring in so fast at an embarrassingly high rate of $10 billion a month and that it was the most rapid accumulation of wealth in history (click here for the data). In any case, reserves have been falling for the past year from a peak of $4.1 trillion.

While it had more than enough Treasury bonds, any attempt to sell might cause their value to collapse and freeze relations with the US. I suggested China should start hedging its gigantic holdings without selling them, or some managers would be facing a firing squad in the future.

China tried to recycle its surpluses by buying foreign companies that produce the natural resources it desperately needs. But takeover attempts were fought tooth and nail as a foreign invasion, or on national security grounds, such as the attempt to buy California’s Unocal in 2005 and Australia’s Oz Minerals in 2012.

It was now using a strategy of buying low profile minority stakes in foreign resource companies. China took a big stake in the Petrobras (PBR) secondary equity offering, which didn’t work out so well, as the company is now facing bankruptcy.

I asked her about the real estate bubble in China that was causing so many foreign investors to lose sleep. She said it was true that sales were slow at some luxury buildings in Beijing and Shanghai, but the great majority of developments were aimed at working people and were filling up as soon as they came on the market.

The 40% down payment demanded by the People’s Bank of China headed off the rampant speculation that brought the American financial system down. Buyers of second homes were required to pay entirely in cash.

Rooms With Views

Wen then complained about the aggressive military stance the US was taking towards China, ringing it in with the Seventh Fleet. Holding a knife so close to the country’s foreign supply line jugular vein made them nervous.

China was basically indefensible. All it would take was the sinking of a few grain ships, and 50 million would starve within a year.

Wen told me there is a school of thought in Beijing that as the country’s economic power grows- it passed Japan to become second in GDP in 2010– that the US will increasingly perceive it as a military threat. This would lead America to mete out the same hostile treatment to China as it has done to Russia since the Ukraine War began.

Walking Softly, But Carrying a Big Stick

I assured her that the Seventh Fleet was there to watch and listen, but to do nothing. It was really in a position to provide a security blanket for allies, like Japan and South Korea, but nothing more. China wasn’t engaging in the belligerent behavior that Russia was at the height of the Cold War, like blockading Berlin, basing missiles in Cuba, stationing fast attack nuclear submarines off our coasts, and invading Afghanistan.

I argued that if China truly has no expansionary intentions, the more we know about you, the better. It is always prudent for a potential adversary to conclude you are not a threat, and that no action is needed.

The more you help the US do that, the better. China is decades behind the US in military technology, and you really have nothing we want. Little more than 200 nuclear weapons without an ICBM or submarine delivery systems were hardly viewed as a major threat.

Wen seemed perturbed that I was aware of her country’s nuclear stockpiles, and asked how I knew this. I said that former CIA director Leon Panetta told me. She said “Oh.” I asked what was that test downing of a satellite in space about, anyway. She didn’t answer.

Looking at the world for the next 30 years, who is the Pentagon going to model and war game against, but China, with its 2.5 million-man army?

Wen countered that the People’s Liberation Army was purely a defensive force. With a 12,000-mile land border, an 11,000-mile coastline, and dubious neighbors like Russia, Iran, and India, they have no other choice. Its ability to project force over great distances, as the US can, is virtually nonexistent.

Its 1979 invasion of Vietnam was about reclaiming ten miles of lost territory. China got involved in Korea only after General Douglas MacArthur threatened to rain atomic bombs on the mainland, losing 2 million men, including Chairman Mao’s son. China could have done a lot more in the Vietnam War, but didn’t, limiting its participation to a supply, logistical, and advisory role.

That’s a Lot of Border to Defend

I then warned that if you really are worried about the Pentagon, you should stop hacking into our computers. She replied that the US started this by emptying out Chinese mainframes many times, and they were only responding in kind.

I said yes, but that China was targeting private companies, like Google (GOOG), Microsoft (MSFT), and Oracle (ORCL) that without military-grade software, were unable to defend themselves. The Chinese agencies involved then used the data to their own commercial advantage.

What Did You Say the Password Was Again?

By the time Wen married, China had already adopted its one-child policy. As much as she wanted more children, she understood the government’s need to adopt such a drastic policy. Without it, the population today would be 1.8 billion, not 1.2 billion, and all of the money that went into buying capital goods would have been spent on food imports instead.

The country would have stagnated at its 1980 per capita income of $100/year. There would have been no Chinese economic miracle. She was very proud of her one son, who was a software engineer at Microsoft (MSFT) in Beijing.

Her husband, a mid-level official at the Ministry of Commerce, fared less well, dying of lung cancer at a relatively early age. The US and Europe had exported their worst polluting industries to China to take advantage of lax environmental controls, turning the air in Beijing into a choking haze.

Sometimes her son would come home from school coughing and wheezing so badly that he couldn’t play outside. The two packs of cigarettes a day her husband smoked didn’t help either.

Imported From the USA

I asked if she recalled our first trip together and a dark cloud came over her face. We were touring a section of Fuzhou when three policemen marched up. They started shouting at Wen that we were in a restricted section of the city where foreigners were not allowed. They started mercilessly beating her with clubs.

I was about to intercede when my late wife, Kyoko, let go with a blood-curdling tirade in Japanese that froze them in their tracks. I saw from the fear in their faces that she had ignited their wartime fear of Japanese authority and the dreaded Kempeitai, or secret police, and they beat a hasty retreat.

To this day, I’m not exactly sure what Kyoko said. We took Wen back to our hotel room and bandaged her up, putting ice on the giant goose egg on her head. When I left, I gave her my copy of HG Well’s A Short History of the World, which she treasured, as the book was then banned in China.

Wen mentioned that she was approaching the mandatory retirement age of 60, and soon would be leaving the Foreign Service. I suggested she move to San Francisco, which offered a thriving Chinese community. She laughed. No matter how much prices had fallen, she could never afford anything here on a Chinese civil servant’s salary.

Wen told me that China was grateful for the billions of dollars that foreigners had poured into her country as a result of my writings. I replied that I was simply trying to show my readers where to make some money, nothing more. It was pure opportunistic self-interest.

One of my early recommendations, Chinese search engine Baidu (BIDU), was up more than tenfold in less than two years. Did she happen to know about any more future Baidu’s? Wen said that she wasn’t that close to the stock market, but that she would get back to me.

I asked Wen if she still had the book I gave her nearly five decades ago. She said it had become a family heirloom and was being passed down through the generations. As she smiled, I noticed the faint scar on her eyebrow from that unpleasantness so long ago.

In view of Wen’s comments, I think you have to pass on investing in China (FXI) for the short term.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/Chinese-Woman.jpg209366Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-10-25 09:02:072023-10-25 13:55:49An Evening With the Chinese Intelligence Service

For here it is September, and the stock market is behaving like it is only July. July was different from normal as well, going straight up almost every day when it is usually asleep. This year, July acted like May, when you’re supposed to sell and go away.

If you’re thoroughly confused by all of this, so am I. The historic cyclicality of the markets, the ebb and flow of share prices according to the calendar, has gone out the window. But then, what isn’t confusing these days?

I went to buy a green drink from Whole Foods on Friday and the counter was closed because of staff shortages. Whole Foods unable to sell a green drink?

I tried to climb the Matterhorn this summer but was told that the guides weren’t taking anyone up because of the extreme heat. The mountain was literally melting, dropping rocks on the heads of climbers. No climbing the Matterhorn in Switzerland? I went to the Dolomites instead where you climb ice-free shear rock faces.

I tried to get into the Pantheon in Rome this summer and was met with a five-hour line. The Sistine Chapel in the Vatican was worse. When I first went there in the 1960’s the place was empty. The fact is that Italy now has more tourists than Italians. Oh, and the pope is from Argentina.

Has the world gone mad?

What has happened is that there has been a great pull forward that took place in financial markets during the first half of the year. I’ve seen this before. When a conclusion becomes obvious, everyone jumps on the bandwagon and brings everything forward.

So from January to July stock markets saw the blatantly obvious future that inflation would fall, interest rates decline, the US dollar weaken, and commodities and precious metals would rise. That’s why the “Magnificent Seven” led.

What happens next?

Now shares have to wait until these predictions actually happen before they can move any further. Markets have moved as far as they can on faith alone. Next, we need facts. This could take weeks or even months.

I knew this was going to happen. That’s why I went pedal to the metal, full speed ahead, damn the torpedoes aggressive during the first half of the year and clocked a 60% profit. I expected that if you didn’t make a profit in the first half of the year, you wouldn’t have any profits in 2023 at all.

And the trade alert drought continues.

There isn’t a day that goes by when I am not asked if America’s $33 trillion national debt will destroy the economy, cause the stock market to crash, and bring the end of Western Civilization. The answer is no, never, not in our lifetimes.

The reason is very simple. Any dollar the government borrows today sees its purchasing power go to zero in 30 years. That’s where the massive Civil War debt went, that's where the WWI debt went, and that’s where the gigantic WWII debt went, some 105% of GDP. Today’s debt will similarly vaporize over time.

Who pays for this cataclysmic decline in value? US government debt holders, who similarly see their purchasing power disappear over time. It turns out that the ultimate avoiders of risk, investors in US government debt, not only don’t get paid for their cowardice, they lose their entire principal as well, at least in terms of purchasing power.

There is a wonderful article in Barron’s this week entitled “Government Debt Needs to Be Repaid, And Other Myths About the Federal Deficit” by Paul Sheard which explains how all this works, which I quote below in its entirety.

“The U.S. national debt currently stands at $32.91 trillion, and 10 months into this fiscal year, the U.S. government has spent $1.6 trillion more than it has collected in revenue. Those intimidating figures animate political battles that can shut down the government and even bring it to the brink of default. But the meaning of this money isn’t as simple as it seems. Five myths in particular deserve straightening out.

The first is that the government has to borrow in order to spend and run deficits. It’s the other way around. The government creates money (injects it into the economy) when it spends and destroys money (withdraws it from the economy) when it taxes. The government taxes variously to correct for negative externalities, to redistribute income, and to modulate aggregate demand; “raising revenue” is just a cover story.

A related myth is that the government needs to repay its debt. “Debt” is a misnomer; government debt is just money (or purchasing power) in another form. A $20 bill is a liability of the Fed, which makes it a liability of the federal government. A $20 bill never has to be repaid; it just is. Fundamentally, Treasuries aren’t much different.

That government debt never needs to be repaid doesn’t mean the government can or should create as much of it as it likes.

Too big a pile of debt because of prior and ongoing budget deficits may be inflationary, as too much money chases insufficient goods and services. That will require some combination of monetary and fiscal tightening. A mountain of debt may indicate a government that is too big and intrusive in the economy for many people’s liking, an issue that can be fought out at the ballot box.

A third myth is that the Fed prints money when it does quantitative easing. The money-printing happens when the government runs a budget deficit; QE just changes the form of that money.

QE is really just a debt refinancing operation of the consolidated government—that is, the government including the Fed—whereby it refinances one form of debt (government bonds or guarantees) into another (reserves). QE changes the composition of the (consolidated) government debt in the hands of the private sector, but it doesn’t directly add one iota of new purchasing power. For every dollar the Fed “pumps into” the economy by doing QE, it “sucks out” a dollar of assets. Conversely, quantitative tightening just returns assets to private sector portfolios, expunging reserves in the process.

Reserves are like banknotes: The Fed can withdraw them, but it never has to repay them as such. It looks like the government has to repay Treasuries, but this is an institutional artifact. In extremis, the Fed could convert all outstanding Treasuries into reserves, and it could maintain monetary control by it, rather than the fiscal authorities, paying interest on reserves.

Japan is the poster child for a miserable-looking fiscal picture. Yet, the Bank of Japan, the pioneer of QE, owns almost half of the stock of outstanding Japanese government securities and, at the same time, since 2016 has managed the 10-year yield, with some leeway, to be “around zero percent.”

It is precisely because the government can create money at will that the modern monetary and fiscal architecture has been designed to put shackles on its ability to do so: The creation of an “independent” central bank withinthe government, the central bank not allowing the government’s account with it to go into overdraft, the central bank not buying bonds directly from the government, and governments issuing debt securities rather than leaving their deficits in the form of reserves all serve that purpose. But what the government taketh away, it can give back. Faced with the need, it could loosen those shackles.

A fourth, and related, myth is that banks could, if so moved, “lend out” the excess reserves created by QE. Banks can lend these reserves to one another but they cannot turn them into lending to companies and households in the broader economy.

It isn’t just the government that creates money. Banks do, too. A fifth myth is that banks are just financial intermediaries “taking in” deposits and “lending them out.” Not so. Banks create money when they lend. For an individual bank making a new loan, it may not feel like this, because the first thing borrowers do is spend their money. If none of that money flows back into the same bank, its reserves at the central bank will decline by the amount of the loan. It will then probably want to attract deposits to “fund” the loan, but doing so will just top up its lost reserves. Bank lending for the system is entirely self-funding (so long as none of the money created leaks into bank notes).

The U.S. economy currently produces about $27 trillion of goods and services annually, a little more than the amount of federal debt held by the public and the QE-embracing Fed. The money needed to sustain this giant prosperity-generating machine comes from the government running deficits and from banks extending credit, with the Fed’s activities linking the two. Political debates and decisions currently are based on a befuddled grasp of how this monetary system works. The stakes for society are too high for that.”

So far in August, we are down -4.70%. My 2023 year-to-date performance is still at an eye-popping +60.80%. The S&P 500 (SPY) is up +17.10% so far in 2023. My trailing one-year return reached +92.45% versus +8.45% for the S&P 500.

That brings my 15-year total return to +657.99%. My average annualized return has fallen back to +48.15%, another new high, some 2.50 times the S&P 500 over the same period.

Some 41 of my 46 trades this year have been profitable.

Beige Book Shows Consumer Spending Slowing, long a pillar of this recovery, as the last of the pandemic bonuses work their way for the system. It’s putting a dent in corporate profits and hints at a shrinking economy, contrary to recent economic data.

The US Dollar (UUP) is Soaring, thanks to “higher interest rates for longer” and a strengthening US economy. Asian currencies are at ten-month lows and central bank intervention is looking. The dollar shorting selling opportunity of the decade is setting up.

China Restricts Sales of iPhones (AAPL), barring sales to government agencies. It’s only a small nick in overall sales, but certainly casts of cloud over doing business in the Middle Kingdom. Some $200 billion, (AAPL)’s market cap has been vaporized.

Weekly Jobless Claims Dive, down 13,000 to 216,000, a seven-month low. It’s the fourth consecutive decline and not what the Fed wanted to hear.

Rate Hikes Will Drag on the Economy for at Least a Decade, as the Fed's $8.24 trillion balance sheet unwinds, according to the San Francisco Fed. The balance sheet was only at $800 million before the 2008 Great Recession.

Saudi Arabia and Russia Engineer Short Squeeze on Oil (USO), taking the price over $90 a barrel this year. Large production cuts announced in June will be maintained until yearend. Will Biden counter with a release from the Strategic Petroleum Reserve, or SPR?

Tesla’s Chinese EV Deliveries Rise 9.3% in August, thanks to aggressive price cuts. There is a two-month wait for the Model Y. Chinese rival BYD (BYD), with its Dynasty and Ocean series of EVs and petrol-electric hybrid models, recorded deliveries of 274,086 passenger vehicles in August, a jump of 57.5% year-on-year. China has the world’s largest car market.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 11, US Consumer Inflation Expectations are announced.

On Tuesday, September 12 at 8:30 PM EST, NFIB Business Optimism Index is released. Apple announced the new iPhone 15.

On Wednesday, September 13 at 8:30 AM, the Core Inflation Rate for August is published.

On Thursday, September 14 at 8:30 AM, the Weekly Jobless Claims are announced. ARM started trading after its IPO, which was five times oversubscribed. NVIDIA tried but failed to take over the chip maker.

On Friday, September 15 at 2:30 PM, the Producer Price Index for August is published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, not just anybody is allowed to fly an aircraft in Hawaii. You have to undergo special training and obtain a license endorsement to cope with the Aloha State’s many aviation challenges.

You must learn how to fly around an erupting volcano, as it can swing your compass by 30 degrees. You must master the fine art of not getting hit by a wave on takeoff since it will bend your wingtips forward. And you’re not allowed to harass pods of migrating humpback whales at a low level, a sight I will never forget.

Traveling interisland can be highly embarrassing when pronouncing reporting points that have 16 vowels. And better make sure your navigation is good. Once a plane ditched interisland and the crew was found six months later off the coast of Australia. Many are never heard from again.

And when landing on the Navy base at Ford Island you were told to do so lightly, as they still hadn’t found all the bombs the Japanese had dropped during their Pearl Harbor attack in 1941.

You are also informed that there is one airfield on the north shore of Molokai you can never land at unless you have the written permission from the Hawaii Department of Public Health. I asked why and was told that it was the last leper colony operating in the United States.

My interest piqued, the next day found me at the Hawaiian state agency with an application in hand. I still carried my UCLA ID which described me as a DNA researcher, which did the trick.

When I read my flight clearance to the controller at Honolulu International Airport, he blanched, asking if I had authorization because he’d never seen one before. I answered that yes, I did, I really was headed to the dreaded Kalaupapa Airport, the Airport of no Return.

Getting into Kalaupapa is no mean feat. You have to follow the north coast of Molokai, a 3,000-foot-high series of vertical cliffs punctuated by spectacular waterfalls. Then you have to cut your engine and dive for the runway in order to land into the wind. You can only do this on clear days, as the airport has no navigational aids. The crosswind is horrific.

If you don’t have a plane it is a 20-mile hike down a slippery trail to get into the leper colony. It wasn’t always so easy.

During the 19th century, Hawaiians were terrified of leprosy, believing it caused the horrifying loss of appendages, like fingers, toes, and noses, leaving bloody open wounds. So, King Kamehameha I exiled lepers to Kalaupapa, the most isolated place in the Pacific.

Sailing ships were too scared to dock. They simply threw their passengers overboard and forced them to swim for it. Once on the beach, they were beaten a clubbed for their possessions. Many starved.

Leprosy was once thought to be a result of sinfulness or infidelity. In 1873, Dr. Gerhard Henrik Armauer Hansen of Norway was the first person to identify the germ that causes leprosy, the Mycobacterium leprae.

Thereafter, it became known as Hanson’s Disease. A multidrug treatment that arrested the disease, but never cured it, did not become available until 1981.

Leprosy doesn’t actually cause appendages to drop off as once feared. Instead, it deadens the nerves, and then rats eat the fingers, toes, and noses of the sufferers when they are sleeping. It can only be contracted through eating or drinking live bacteria.

When I taxied to the modest one-hut airport, I noticed a huge sign warning “Closed by the Department of Health.” As they so rarely get visitors the mayor came out to greet me. I shook his hand but there was nothing there. He was missing three fingers.

He looked at me, smiled, and asked, “How did you know?”

I answered, “I studied it in college.” Even today, most are terrified of shaking hands with lepers.

Not me.

He then proceeded to give me a personal tour of the colony. The first thing you notice is that there are cemeteries everywhere filled with thousands of wooden crosses. Death is the town’s main industry.

There are no jobs. Everyone lives on food stamps. A boat comes once from Oahu a week to resupply the commissary. The government stopped sending new lepers to the colony in 1969 and is just waiting for the existing population to die off before they close it down.

Needless to say, it is one of the most beautiful places on the planet.

The highlight of the day was a stop at Father Damien’s church, the 19th century Belgian catholic missionary who came to care for the lepers. He stayed until the disease claimed him and was later sainted. My late friend Robin Williams made a movie about him, but it was never released to the public.

The mayor invited me to stay for lunch, but I said I would pass. I had to take off from Kalaupapa before the winds shifted.

It was an experience I will never forget.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Airport of No Return

Father Damien

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-11 09:02:122023-09-11 16:04:06The Market Outlook for the Week Ahead, or The Big Pull Forward

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.