Global Market Comments

November 4, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (LLY), (TSLA), (GOOG), (GOOGL), (JPM), (BAC), (C), (BRK), (V), (TQQQ), (CCJ), (BLK), (PHO), (GLD), (SLV), (UUP)

Global Market Comments

November 4, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (LLY), (TSLA), (GOOG), (GOOGL), (JPM), (BAC), (C), (BRK), (V), (TQQQ), (CCJ), (BLK), (PHO), (GLD), (SLV), (UUP)

Below please find subscribers’ Q&A for the November 2 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: The country is running out of diesel fuel this month. Should I be stocking up on food?

A: No, any shortages of any fuel type are all deliberately engineered by the refiners to get higher fuel prices and will go away soon. I think there was a major effort to get energy prices up before the election. If that's the case, then look for a major decline after the election. The US has an energy glut. We are a net energy exporter. We’re supplying enormous amounts of natural gas to Europe right now, and natural gas is close to a one-year low. Shortages are not the problem, intentions are. And this is the problem with the whole energy industry, and the reason I'm not investing in it. Any moves up are short-term. And the industry's goal is to keep prices as high as possible for the next few years while demand goes to zero for their biggest selling products, like gasoline. I would be very wary about doing anything in the energy industry here, as you could get gigantic moves one way or the other with no warning.

Q Is the SPDR S&P 500 ETF (SPY) put spread, correct?

A: Yes, we had the November $400-$410 vertical bear put spread, which we just sold for a nice profit.

Q: I missed the LEAPS on J.P. Morgan (JPM) which has already doubled in value since last month, will we get another shot to buy?

A: Well you will get another shot to buy especially if another major selloff develops, but we’re not going down to the old October lows in the financial sector. I believe that a major long-term bull move has started in financials and other sectors, like healthcare. You won’t get the October lows, but you might get close to them.

Q: I’m waiting for a dip to get into Eli Lilly (LLY), but there are no dips.

A: Buy a little bit every day and you’ll get a nice average in a rising market. By the way, I just added Eli Lilly to my Mad Hedge long-term model portfolio, which you received on Thursday.

Q: Any thoughts about the conclusion of the Twitter deal and how it will affect tech and social media?

A: So far all of the indications are terrible. Advertisers have been canceling left and right, hate speech is up 500%, and Elon Musk personally responded to the Pelosi assassination attempt by trotting out a bunch of conspiracy theories for the sole purpose of raising traffic and not bringing light to the issue. All indications are bad, but I've been with Elon Musk on several startups in the last 25 years and they always look like they’re going bust in the beginning. It’s not even a public stock anymore and it shouldn’t be affecting Tesla (TSLA) prices either, which is still growing 50% a year, but it is.

Q: In terms of food commodities for 2023, where are prices headed?

A: Up. Not only do you have the war in Ukraine boosting wheat, soybean, and sunflower prices, but every year, global warming is going to take an increasing toll on the food supply. I know last summer when it hit 121 degrees in the Central Valley, huge amounts of crops were lost due to heat. They were literally cooked on the vine. We now have a tomato shortage and people can’t make pasta sauce because the tomatoes were all destroyed by the heat. That’s going to become an increasingly common issue in the future as temperatures rise as fast as they have been.

Q: Do I trade options in Alphabet (GOOG) or Alphabet (GOOGL)?

A: The one with the L is the holding company, the one without the L is the advertising company and the stock movements are really identical over the long term, so there really isn’t much differentiation there.

Q: Why can’t inflation be brought down by increasing the supply of all goods?

A: Because the companies won’t make them. The companies these days very carefully manage output to keep prices as high as possible. It’s not only the energy industry that does that but also all industries. So those in the manufacturing sector don’t have an interest in lowering their prices—they want high prices. If they see the prices fall, they will cut back supply.

Q: What do you think about growth plays?

A: As long as interest rates are rising, growth will lag and value will lead, and that has been clear as day for the last month. This is why we have an overwhelming value tilt to our model portfolio and our recent trade alerts. They’ve all been banks—JP Morgan (JPM), Bank of America (BAC), Citigroup (C), plus Berkshire Hathaway (BRK) and Visa (V) and virtually nothing in tech.

Q: I don’t know how to execute spread trades in options so how do I take advantage of your service?

A: Every trade alert we send out has a link to a video that shows you exactly how to do the trade. I have to admit, I’m not as young as I was when I made the videos, but they’re still valid.

Q: Is the US housing market about to crash?

A: There is a shortage of 10 million houses in the US, with the Millennials trying to buy them. If you sell your house now, you may not be able to buy another one without your mortgage going from 2.75% to 7.75%—that tends to dissuade a lot of potential selling. We also have this massive demographic wave of 85 million millennials trying to buy homes from 65 million gen x-ers. That creates a shortage of 20 million right there. That's why rents are going up at a tremendous rate, and that's why house prices have barely fallen despite the highest interest rates in 20 years.

Q: If we get good news from the Fed, should we invest in 3X ETFs such as the ProShares UltraPro QQQ (TQQQ)?

A: No, I never invest in 3X ETFs, because they are structured to screw the investor for the benefit of the issuer. These reset at the close every day, so do 2 Xs and not more. If you're not making enough money on the 2Xs, maybe you should consider another line of business.

Q: Do you think BlackRock Corporate High Yield Fund (HYT) will show the pain of slights because of their green positioning?

A: No I don’t, if anything green investing is going to accelerate as the entire economy goes green. And you’ll notice even the oil companies in their advertising are trying to paint themselves as green. They are really wolves in sheep’s clothing. They’ll never be green, but they’ll pretend to be green to cover up the fact that they just doubled the cost of gasoline.

Q: Where do you find the yield on Blackrock?

A: Just go to Yahoo Finance, type in (BLK), and it will show the yield right there under the product description. That’s recalculated by algorithms constantly, depending on the price.

Q: Do you like Cameco (CCJ)?

A: Yes, for the long term. Nuclear reactors have been given an extra five years of life worldwide thanks to the Russian invasion of Ukraine. Even Japan is opening theirs.

Q: Should I short the US dollar (UUP) here?

A: The answer is definitely maybe. I would look for the dollar to try to take one more run at the highs. If that fails, we could be beginning a 10-year bear market in the dollar, and bull market in the Japanese yen, Australian dollar, British pound, and euro. This could be the next big trade.

Q: What is your outlook on Real Estate Investment Trusts (REITs) now?

A: I think it looks great. REITs are now commonly yielding 10%. The worst-case scenario on interest rates has been priced in—buying a REIT is essentially the same thing as buying a treasury bond, but with twice the leverage, because they have commercial credits and not government credits. We’ll be doing a lot more work on REITS. We also have tons of research on REITS from 12 years ago, the last time interest rates spiked. I'll go in and see who’s still around, and I'll be putting out some research on it.

Q: How do you see the price development of gold (GLD)?

A: Lower—the charts are saying overwhelmingly lower. Gold has no place in a rising interest rate world. At least silver (SLV) has solar panel demand.

Q: Do you have any fear of Korea going into IT?

A: Yes, they will always occupy the low end of mass manufacturing, and you can see that in the cellphone area; Samsung actually sells more phones than Apple, but they’re cheaper phones with lower-end lagging technology, and that’s the way it’s always going to be. They make practically no money on these.

Q: When can we get some more trade alerts?

A: We are dead in the middle of my market timing index, so it says do nothing. I’m looking for either a big move down or big move up to get back into the market. This is a terrible environment to chase trades when you're trading, so I'm going to wait for the market to come to me.

Q: What about water as an investment? The Invesco Water Resources ETF (PHO)?

A: Long term I like it. There’s a chronic shortage of fresh water developing all over the world, and we, by the way, need major upgrades of a lot of water systems in the US, as we saw in Jackson, MS, and Flint, MI.

Q: Will REITs perform as well as buying rental properties over the next 10 to 20 years?

A: Yes, rental properties should do very well, as long as you’re not buying any city that has rent control. I have some rental properties in SF and dealing with rent control is a total nightmare, you’re basically waiting for your tenants to die before you raise the rent. I don’t think they have that in Nevada. But in Las Vegas, you have the other issue that is water. I think the shortage of water will start to drag on real estate prices in Las Vegas.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log on to www.madhedgefundtrader.com go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

It’s Been a Tough Market

Global Market Comments

June 14, 2022

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT IS ON FOR JUNE 14-16)

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or WHAT HAPPENS WHEN YOUR BEST FRIEND BECOMES YOUR WORST ENEMY?)

(SPY), (TLT), (TSLA), (CCJ), (TGT), NVDA), (JPM), (BAC), (C)

Of course, I am talking about the Federal Reserve.

The Fed was the best friend of share owners, pressing interest rates lower from March 2009. That remained the case for 12 years until November 2021 when its notorious pivot took place, flipping overnight from an easing to a tightening posture.

It's actually worst than that. In fact, our nation’s central bank morphed overnight from the easiest monetary policy in history to the most aggressive tightening.

Stock markets have noticed, the Dow average giving up 20% in six months, and the final lows are probably not in yet.

I would bet money that you are expecting the worst-case scenario to happen. After all, the last serious selloff in 2008-2009 took the index down a heart-palpitating 52%.

What’s more, every oil shock of the last 50 years was followed by a recession, and we are clearly in one now. So, you are right to fear for your net worth and retirement security.

However, my work suggests that the best-case scenario will happen. Who is right, you or me?

You already know the answer.

Let me tell you what is already priced in the stock market: a Russian invasion of Ukraine, inflation at a 40-year high and climbing, a doubling of mortgage interest rates in a half year, peaking of the housing bubble, popping of technology and Bitcoin bubbles, and 200 basis points of Fed interest rate hikes.

With all this negativity already in the market, I would say that it is impossible for stocks NOT to go up. All that is left is to suck in one last round of non-believers on the short side before the indexes start a move to new all-time highs. That could take months at the most.

The only question now is whether a further 5% decline to an S&P 500 of 3,600, or a final puke out low of 3,500, down 7.5%. That means you should start scaling into your favorite longs now, the Cadillacs at Volkswagen prices.

So, let’s do some thinking outside the box here.

Tech stocks are cheaper now than after the low point of the Great 2000 Dotcom Bust. But they are still expensive compared to the main market. The S&P without technology stocks is now valued at earnings multiple of 13X versus 17x main market.

That is well into decade-low territory. That’s why I have included financials like (JPM), (BAC), and (C) in my list of “must own sectors'.

It's clear that inflation will bedevil the market for months to come given the dramatic acceleration we saw in May, from 0.3% to 1%. Let me tell you that there are only two ways to end inflation, and they could be done overnight.

*End all US support for Ukraine and throw in with Vladimir Putin. That would shave $50 off the price of oil immediately and get gas prices below $3.00 a gallon. You might have a hard time selling this to the thousands of Americans going over to Ukraine to volunteer.

*Cause a sharp recession immediately. The Fed is already well on their way to doing this with three guaranteed 50 basis point rate hikes by September. The first thing to collapse in a recession is oil demand. In the last recession, it went to negative $37 in the futures market (I got stopped out at -$5). This is why the oil industry isn’t interested in investing a dime at these oil prices. They are responsible to their shareholders, not Biden’s reelection prospects.

If there is a recession, it’s an invisible one. It’s a recession where you can’t hire anyone, can’t buy anything, subcontractors give you a six-month timeline with a straight face, and it takes a year to get delivery of a damn sofa. This recession miserably fails my “look out the window test.”

But at my advanced age, I don’t get surprised anymore.

Boba tea anyone? Who knew?

Consumer Price Index slaughters stocks, taking the Dow Average down 1,600 points, or 5% in two days, the worst move in two years. It’s typical bear market action. May inflation hit 8.6%, a new 40-year high. But you have to more than double to hit the old 1980s peak. New stock lows are in easy reach.

Lumber crashes, down 50% from the highs in months, with the near-complete cessation of new orders from builders. They see a recession just around the corner with higher interest rates and no new home buyers. It’s proof that the current inflation is spiking and setting up for a big fall.

Luxury Home Sales are plunging in New York, in numbers, but not in prices. Anyone who needed debt to trade up is out of the picture.

US drop Covid Testing Requirement for international travelers. Too many Americans trying to get home were getting stranded overseas for weeks because they failed a Covid test. Wheww!! That was a close call!

Americans will spend an extra $730 Billion on energy this year. That’s a heck of a lot to take out of consumer spending. So far, there has been no decline in demand. Much of this money ended up in Russian coffers.

Amazon (AMZN) splits 20:1, triggering an avalanche of new retail buyers. The company is also at the low end of its valuation range anger a gut-punching 41% decline in the share price this year. It may be early, but (AMZN) is definitely a BUY.

Target (TGT) warns of more margin squeeze, with too much inventory and flagging demand. (TGT) has become a bellwether for all of retail, which points to inflation, labor, and supply chain problems.

Uranium Stocks soar on Biden’s plan to buy $4.3 billion worth of enriched uranium, or yellow cake. The move is aimed to replace Russian imports where Russia is one of the world’s largest suppliers. It is the most unexploited form of non-carbon energy out there. Mad Hedge recommended Cameco (CCJ), the world’s second-largest supplier, a month ago. It was up 15% yesterday at the high.

New Home Mortgages hit a 22-year low. With 30-year fixed-rate loans soaring from 2.8% to 5.58% in six months, how can they not? Refis have crashed 75% YOY. Now that the Fed has quit buying, investors won’t touch mortgage-backed securities with a ten-foot pole.

Weekly Jobless Claims pop 29,000 to a five-month high in another hint toward a recession. Continuing Claims are at 1.306 million. The preemptive layoffs by ultra-cautious companies have begun, especially in technology.

Tesla (TSLA) gets an upgrade by UBS, which sees 51% of upside from here to $1,200. Total sales should top 1.4 million vehicles in 2022, up 40% YOY, and that includes lost production of 60,000 in Shanghai. A new Gigafactory in Indonesia is planned with a locked-up supply of Nickel, where the world’s largest supply of the metal resides. Cheap labor helps a lot where 5,000 need to be hired. The company will need six gigafactories to reach 20 million annual production.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

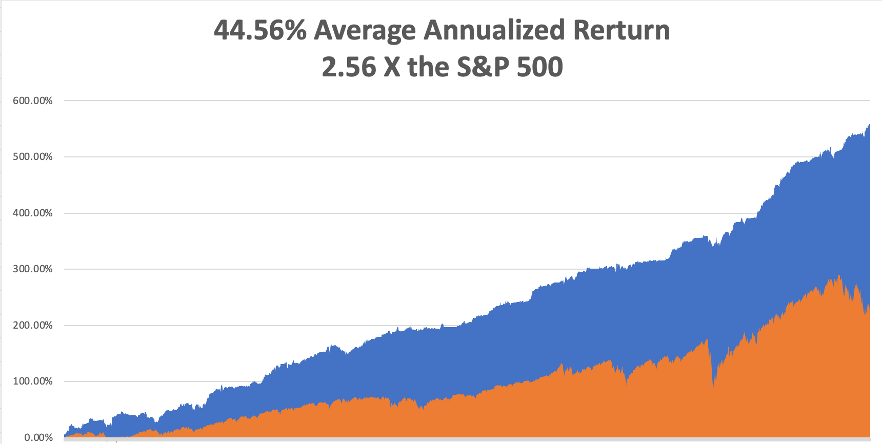

With some of the greatest market volatility seen since 1987, my June month-to-date performance recovered to +2.57%.

My 2022 year-to-date performance ratcheted up to 44.44%, a new all-time high. The Dow Average is down -13.52% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 66.63%.

That brings my 14-year total return to 557%, some 2.56 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.56%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 85.6 million, up 200,000 in a week, and deaths topping 1,011,200 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, June 13 at 8:00 AM EDT, US Consumer Inflation Expectations are out.

On Tuesday, June 14 at 8:30 AM, the Producer Price Index for May is published.

On Wednesday, June 15 at 10:30 AM, Retails Sales for May are announced. The Fed interest rates decision is out at 11:00 AM. The press conference follows at 11:30.

On Thursday, June 16 at 8:30 AM, Weekly Jobless Claims are out. We also get Housing Starts and Building Permits for May.

On Friday, June 10 at 8:15 AM, Industrial Production for May is published. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, I have benefited from many mentors and role models over the years, but Al Pinder, last of the New York-based Shipping and Trade News, is one of my favorites. Short with blown hair, glasses, and an always impish smile, he was a regular at lunch where we always played an old dice game called “ballout.”

I sat next to Al for ten years at the Foreign Correspondents Club of Japan high up in Tokyo’s Yukakucho Denki Building, we were pounding away on our antiquated Royal typewriters. At the end of the day, our necks would be stiff as boards. Al’s idea of work was to type for five minutes, then tell me stories for ten.

Saying that Al lived a colorful life would be the understatement of the century.

Al covered the Japanese invasion of China during the 1930s, interviewing several key generals like Hideki Tojo and Masaharu Homma, later executed for war crimes. He told me of child laborers in Shanghai silk processors who picked cocoons out of boiling water with their bare hands.

Al could see war with Japan on the horizon, so he took an extended tour of every west-facing beach in Japan during the summer of 1941, taking thousands of black and white pictures. The trick was how to get them out of the country without being arrested as a spy.

So he bought an immense steamer trunk and visited a sex shop in Tokyo’s red-light district where he bought a life-sized, blow-up doll of a Japanese female. His immensely valuable photos were hidden below a false bottom in the trunk and the blow-up doll placed on top.

When he passed through Japanese customs on the ship home from Yokohama, the inspectors opened the trunk, had a good laugh, and then closed it. These photos later became the basis of Operation Coronet, the American invasion of Japan in 1945.

Al was working for the Honolulu Star Bulletin when the Japanese attacked Pearl Harbor on December 7, 1941. Many antiaircraft shells fired at the attacking zeros landed in Honolulu causing dozens of casualties. Al told me every woman on the island wanted to get laid that night because they feared getting raped by the Japanese Army the next day.

Since Al knew China well, he was parachuted into western Yunan province to act as a liaison with Mao Zedong, then fighting a guerrilla war against the Japanese with his Eighth Route Army. Capture by the Japanese then meant certain torture and certain death.

In 1944, Al received a coded message in Morse code to pick up an urgent communication from Washington. So, he hiked a day to the drop zone and when the Army Air Corps DC-3 approached, he lit three signal fires.

A package parachuted to the ground, which he grabbed and then he fled for the mountains. Dodging enemy patrols all the way, he returned to his hideout in a mountain cave and opened the package. It was a letter from the Internal Revenue Service asking why he had not filed a tax return in three years.

When the second atomic bomb fell on Nagasaki, the war ended on August 15. Since Al was the closest man on the spot, he flew to Korea where he accepted the Japanese surrender there.

Al was one of the first to move into the Press Club, which housed war correspondents in one of the only buildings still standing in a city that had been bombed flat.

Al never left Japan because, as with many other war correspondents who arrived with the US military, it was the best thing that ever happened to him. After some initial hesitation, they were treated like conquering heroes, it was incredibly cheap at 800 yen to the dollar, and the women were beautiful.

During the Japanese occupation when the people were starving, Al bought an acre of land in Tokyo’s burned-out prime Akasaka district for a ten-pound can of ham. He spent the rest of his life living off this investment, selling one piece at a time, until it eventually became worth $10 million.

Al went to work for the Shipping and Trade News, an obscure industry trade publication which no one had ever heard of. I sat next to him when he artfully lifted every story out of an ancient book, Ships of the World. But Al always had plenty of money to spend.

When Al passed away in the early 2000s, an official from the American embassy in Tokyo showed up at the Press Club asking if anyone knew all Pinder. We eventually traced a bank branch which held a safe deposit box in his name. In it was proof that the CIA had been bribing every Japanese prime minister of the 1950s. He kept the evidence as an insurance policy against the day when his lucrative deal with the Shipping and Trade News was ever put at risk.

I flew in for Al’s wake and his Japanese wife was there along with most of the foreign press. Everyone was crying until I told the IRS story, then they had a good laugh.

A few years ago, I was invited to give the graduation speech at Defense Language Institute in Monterey, California. The latest bunch of graduates, including my nephew, were freshly versed in Arabic and headed for the Middle East.

The school was founded in 1941 to train Americans in Japanese to gain an intelligence advantage in the Pacific war.

General 'Vinegar Joe' Stillwell said their contribution shortened the war by two years. General Douglas MacArthur believed that an army had never before gone to war with so much advance knowledge about its enemy.

To this day, the school's motto is 'Yankee Samurai'. There on the wall with the school’s first graduates was a very young Al Pinder, still with that impish grin.

Al lived a full life and I still miss him to this day. I hope I can do as well.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Al Pinder

Press Club 1976

Global Market Comments

June 3, 2022

Fiat Lux

Featured Trade:

(JUNE 1 BIWEEKLY STRATEGY WEBINAR Q&A),

(AAPL), (GOOGL), (MSFT), (JPM), (BAC), (C), (UUP), (FXA), (FXC), (EEM),

(VIX), (CRM), (AAPL), (TSLA), (COIN), (EDIT), (CRSP), (LMT), (RTX), (GD)

Below please find subscribers’ Q&A for the June 1 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: What are the 3 best stocks to own for the end of the year?

A: Apple (AAPL), Alphabet Inc. (GOOGL), and Microsoft (MSFT). Those you want to buy on meltdown days, kind of like today. Make sure you scale into these—so maybe buy 20% on every down-500-point Dow day. Eventually, you’ll end up with a pretty decent position at a market low in a stock that will double in 3-5 years.

Q: Why these three stocks?

A: Lots of reasons: They’re huge, they’re safe, two out of three pay dividends, Alphabet is about to split, and they have huge moats so nobody can get into their sectors. They have near monopolies in what they do, and they have immense cash on the balance sheet. These are the kind of stocks that portfolio managers dream about. And watch what rallied the hardest in the last dead cat bounce we had—it was these three names. That tells you that they will lead any long-term bull market in the future. These are the stocks that people want to own.

Q: What will bring your predicted second half-bull market in the stock market?

A: Inflation drops from 8% to 4%. That will happen for a couple of reasons. The year-on-year comparisons become highly favorable starting from next month when inflation started to take off a year ago. Inflation numbers are going to be climbing the wall of worry from here on out. That could get us down to 4% by the end of the year. The second reason is the Ukraine War either ends or becomes a stalemate and is no longer a factor in the global markets, and we’ve had time to replace all the Russian oil and Ukrainian wheat.

Q: Are banks positioned to benefit from the coming rally?

A: Absolutely. I think big tech and banks will be the top-performing stock sectors for the next five years because inflation will go away, recession fears will go expire, and credit quality will improve, but interest rates will remain 300 basis points higher than they were during the pandemic. Buy (JPM), (BAC), and (C) on dips.

Q: What will be the worst performing sector?

A: Energy—anything energy-related will get absolutely slaughtered, which is why I don't want to touch it with a ten-foot pole right now. That includes oil companies, exploration companies, E&P companies, and master limited partnerships, as well as coal and other natural gas stocks. So, if you’re long these names don’t forget to sit down when the music stops playing. You could get your head handed to you at the end.

Q: Can we make lower lows?

A: Yes, that’s entirely possible. Market moves are basically random when you get down to these levels— down more than 20%. And on all future downturns, I would be spending your cash going back into the market expecting a second half rally.

Q: What about green energy?

A: Unfortunately, green energy is very tied to old energy because $120 oil makes green companies much more competitive from a cost point of view. So, I’m not going to go piling into green companies right here, especially if I think oil is topping out in the near future. Buying green energy companies here is the same as buying oil at $120 a barrel.

Q: What is the best way to play the declining US dollar?

A: Buy the iShares MSCI Emerging Markets ETF (EEM). Also, the Aussie dollar (FXA) and the Canadian Dollar (FXC), which benefit tremendously from commodity prices, which will rise for another decade in a global economic recovery.

Q: Why will energy be the worst sector?

A: If you end the war in the Ukraine or you replace Russian oil, either by finding new sources of oil, getting other producers to increase production which they can do (including the US), or by accelerating the move to alternatives, then you move oil back to pre-invasion prices which were about $70 a barrel or $50 lower than they are here.

Q: Best way to hedge a falling market?

A: Do what I'm doing: keep a balanced portfolio of longs and shorts, that way you always have something that’s going up. And if you do it through the options, you have time decay working for you on both sides of the equation. If you want to go outright, buy outright puts on individual stocks because they had double the moves of the indexes. And go to my short selling school which you can find by going to my website at https://www.madhedgefundtrader.com. There’s actually 12 different ways to benefit from falling markets.

Q: How deep in the money can we go on our call spreads?

A: Wait for the Volatility Index (VIX) to go over $30, and then go 15-20% in the money. And yes, you only make 10, 15, or 20% on those positions in a month but then you put together ten of them and that adds up to quite a lot of money. You want to find the position that has the greatest probability of happening—i.e. something that’s 20% in the money. Do that when the market has just dropped 20%, which it already has, and then you have a position that has a minuscule chance of losing money.

Q: How much longer do you see this current bear market bounce lasting?

A: Until yesterday.

Q: What's your favorite commodity ETF?

A: My favorite commodity stock is Freeport McMoRan (FCX), the world’s largest copper producer. Rather than pay the extra management fees for an ETF, I prefer just to go straight to the source and buy (FCX).

Q: When do you think the Fed will pivot to dovish or neutral?

A: This summer. It’s just a question of whether it’s the July or the September meeting.

Q: When you say “buy on dips”, what does that mean? 1%, 3%, 5%?

A: Well in this market, a dip would be a retest of the previous lows which is going to be down 10% or 15% on the major positions in your portfolio. If you’re day trading, a dip is only 1%, so it really depends on your timeframe and your risk tolerance. That’s why I always tell people to scale by doing everything in incremental pieces—20%, 25%, and so on. You never know what the market’s actually going to do on a short-term basis. Randomness can’t be predicted.

Q: If you plan to enter a LEAPS on Apple, what strikes would you do?

A: Well, first of all, I want to see if Apple drops all the way to $125, which is a lot of people’s downside target. If it did, then I would do the $125/$135 call spread two years out, and that will probably double. And if it starts a long term up trend, then I’ll keep rolling up the strike prices. If, say, Apple goes to $125, you put your LEAPS on. If the stock rises to 150, then take profits on the $125/$135 and roll into the $150/$160. That’s how you can get like 1,000% returns like we got on Tesla (TESLA) a few years ago. You just keep rolling up your strike prices on every weak day and maintain your leverage.

Q: When do we bet the farms on Editas Medicine Inc. (EDIT) and Crispr (CRSP) Therapeutics?

A: Never. These are small, highly speculative companies which will make money someday, but if the someday is in five years and you’re betting the farm with a LEAPS, you lose the farm. It's going to take a long time for these smaller biotech stocks to come back. If you want to play biotech, go with the big ones like Amgen. It takes a long time to convert cutting-edge technology into profits. The big companies already have a stable of reliable money-making drugs on hand.

Q: Salesforce Inc. (CRM) is up big on earnings—what should I do with the stock?

A: Buy the dips. It’s still way, way below its all-time highs, so use the weekdays to accumulate Salesforce for the long term. It’s one of the best cloud plays out there.

Q: What do you think about NVIDIA Corporation (NVDA)?

A: I absolutely love it. It rallied 20% off the bottom. Use any other additional weak days like today to increase your position. This stock someday is worth $1,000, up from today’s $195.

Q: Do you like SPACS?

A: No, I hate them and think they’re a rip-off. And a lot of them have become totally illiquid and untradable, so you have no choice but for them to shut down and return their money if they have any left. I’ve hated SPACS from day one and people are now getting their comeuppance on these.

Q: What do you think about the weakness in Coinbase Global Inc. (COIN) down here?

A: It’s just going down with all the other high-risk, speculative, meme stock type plays, which include all of the crypto plays like Bitcoin. I would avoid all of those. You want to buy quality at the discount now, and you want to buy the Cadillacs at Volkswagen prices and leave the speculative plays for the next generation, Gen Z, who are already highly interested in stocks.

Q: What is your favorite non-US country to invest in?

A: Australia, because you get a double play there on the currency, which should go up 30% from here, and they will benefit from a global commodity boom which continues for another ten years. They pretty much sell a lot of the major commodities like iron ore, wheat, sheep, and so on. It’s also a really nice country to visit. The only negative with Australia are the sharks.

Q: Biotech takeover targets?

A: Well (EDIT) and (CRSP) would be two of them. Things in the sector are so cheap that they are all potential takeover targets. M&A (Mergers and Acquisitions) will be a major play in the biotech sector for the foreseeable future.

Q: Should we sell short the defense industry here?

A: No, even if the war ends tomorrow, you might get some profit-taking, but the fact is that long term military spending is increasing permanently. The peace dividend now has to be paid back, and that is great for all the defense companies, so I would not be shorting them. If anything, I’d be buying on dips. Buy Lockheed Martin (LMT), Raytheon (RTX), who make the Javelin antitank missile for which there is now a two-year order backlog. You can also throw in General Dynamics (GD) for good measure which builds nuclear submarines and the Stryker armored vehicle.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Keep Those Defense Plays

Global Market Comments

May 20, 2022

Fiat Lux

Featured Trade:

(MAY 18 BIWEEKLY STRATEGY WEBINAR Q&A),

(C), (FXI), (BABA), (TSLA), (AAPL), (AMZN), (TGT), (FLR), (QQQ),

(FB), (ARKK), (TSLA), (WYNN), (UAL), (ALK), (DAL)

Below please find subscribers’ Q&A for the May 18 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: When do you see the banks returning to glory?

A: When recession fears go away, which should happen this summer. A recession will either have come and gone, or we will have confirmation by the end of summer that there is no recession in sight for the next few years at least. This will likely trigger a monster rally in the banks, which could all jump 50% from here. Obviously, Warren Buffet is putting his money where his mouth is by loading up on Citibank (C) yesterday. This would take us to new all-time highs by the end of the year. So, again, use these down-1000-point days to go cherry-picking among the generals who have been executed. If that’s not mixing metaphors, I don’t know what is!

Q: Should I listen to CNBC?

A: No, do not listen to the talking heads on TV. They are on TV because they don’t know how to make money. If they did know how to make money, they’d be locked up in a dark basement somewhere like me, grinding out millions for their firms. In fact, watching TV is the perfect money destruction machine because on down days, they bring out the uber bears, and on up days they bring up the hyper bulls. They are trying to egg you to get you to do the exact opposite of what you should be doing. They’re not interested in you making money; they’re interested in getting traffic on their websites and making money for themselves. CNBC can be highly dangerous to your financial health.

Q: Will we get stagflation?

A: No, because I think that once the year-on-year comparisons kick in—literally in a month or two—inflation will drop from the current 8.3% to down maybe 4% by the end of the year. That also is another factor in your monster second-half rally.

Q: Do you think the bounce in the market yesterday is the beginning of an upward trend or a dead cat bounce?

A: Definitely a dead cat bounce. I expect we’ll keep chopping around in the current range for the next 3, 4, and 5 months, and then we catapult into a monster year-end rally. That is a typical bottoming-type process.

Q: Is the wisdom “Go away in May” still alive or is your best bet that this year may prove different and the market goes up in the latter part of the year?

A: Actually, you should have gone away in November. That’s when all tech stocks peaked; only energy went up after that. If you’d gone away in November and said “come back in August” that would have been a good strategy because I think that’s when the year-end rally begins. If anything, May could be the bottom of the entire move.

Q: Is it time for LEAPS (Long Term Equity Anticipation Securities)?

A: Not yet—it’s too soon for LEAPS territory. You only want to do LEAPS when you are on a sustained long-term uptrend in a stock. We are nowhere near sustained anything, we are still in a bottoming phase, and could be there for months. At the end of those months is when we’ll be looking at LEAPS, where you can double your money every 6 months.

Q: Is it time to start nibbling on China stocks (FXI) now that COVID news is marginally better?

A: I’m going to avoid Chinese stocks because the American ones are so much better. You want to buy the quality at the discount, not the marginal, high-risk political footballs at a discount. And China will remain high-risk as long as they are abandoning capitalism. If you have to buy one Chinese stock, I would say Alibaba (BABA); you could get a double on that. But remember it is a high-risk trade—if the Chinese government wants to roll Jack Ma up in a carpet and kidnap him to Western Chinese re-education camp, the stock will get slaughtered. And that’s been happening increasingly with the heads of major companies in the Middle Kingdom.

Q: When this current route comes to an end, should we look to enter the market with 50% margin on stocks like Tesla (TSLA)?

A: It’s never sensible to go to 50% margin because if the stocks drop 50%, you are completely wiped out—you’ve lost everything. Plus, coming back from a loss is one thing; coming back from zero is impossible. So, I would not recommend that. You might do a safe stock like Apple (APPL), with a 2% dividend, and then at least you’re getting a double dividend. You only do the 50% margin on the safest, high dividend stocks.

Q: Amazon (AMZN) is on its way down. What is your expectation for the $3200/$3400 vertical bull call spread in January 2023?

A: I think you could make money on that. It may not be the full amount of the spread, but you’ll definitely get a big increase from current levels, because when we do get a second half rally, it will be tech-led, and Amazon has already had a horrific decline. What you might consider is rolling your strike down, taking the loss on the 3200/3400 and rolling down to like a $2,000/$2,200 in twice the size, and you’ll make your money back that way.

Q: For those of us thinking about LEAPS, how should we start to buy in—20, 30, 50% right now?

A: Well, first of all, you only do them on down days like today, when the market is down 800, and you scale in. 20% now, 20% higher or lower, and 20% again higher or lower. But you really want to be saving cash for days like this because You want to feel smarter than everybody else, and they absolutely will hit any bid on a down day, and that's where your LEAPS fills are really excellent, is on a down day like this.

Q: Can the Fed avoid another policy mistake? Because it seems that not only are they heading for high inflation, but layoffs are coming as well, and even with that I’m sure they will perform a soft landing of sorts.

A: For sure, when you take massive amounts of stimulus out of the economy, as we have in the last year, that is recessionary. In fact, the US government is close to running a balance budget right now because Biden can’t get anything through Congress other than money for Ukraine. Good for Ukraine economy, not for ours. And yes, they can do a soft landing, but has it ever been done before? No. Though this is the Fed that just keeps on surprising, so who knows. In the meantime, I'm willing to trade the ranges, and that may be all you get to do for a while.

Q: Target (TGT) shares are down 25%, as they cited higher costs that will result in rising prices for their customers. Would you buy the dip?

A: No, I generally don’t like retailers anyway. It’s a business that operates on a 2% profit margin. I like 40 or 50% profit margin businesses—those tend to be technology stocks.

Q: Would you buy retailers going into a recession?

A: No, that’s the worst thing in the world to own.

Q: Could Fluor Corp (FLR) be a Ukraine infrastructure stock?

A: Yes, once the war ends there will be a massive effort to rebuild Ukraine. Every company in the world will be involved, and Fluor and Bechtel will be the biggest, though Fluor is the only one where you can buy the stock. We already have the money to do this with all of the money that was seized from Russia. I predict discount sales on mega yachts.

Q: Why do you think all that money is going to Ukraine?

A: Because a weakened Russia is in the national interest of the United States, and it’s better that their soldiers are doing the dying than ours. I’ve done the latter and definitely prefer the former, using the other country's’soldiers as cannon fodder.

Q: On down days like today, should I be putting on one-month trades like the June options?

A: Yes, because the minimizes your risk and cuts the cost of mistakes. Waiting for the second half of the year when we get a prolonged uptrend to look at LEAPS—that is the correct way to do it.

Q: Over the next 12 months, do you think the S&P 500 will outperform Nasdaq?

A: No—for the next 3 months the S&P 500 will outperform NASDAQ. After that, NASDAQ will become an enormous outperformer for the rest of the decade. So, choose your entry points wisely.

Q: Do you think that housing is peaking out and will start to decline?

A: No, we still have a long-term structural shortage of 10 million homes in the US and I think we will flatline housing for years until we catch up with that shortfall.

Q: What are your thoughts on the Metaverse?

A: Too soon. Right now, the Metaverse involves spending only—no revenues. It could be years before you actually see any profits. So that’s why I'm avoiding Meta or Facebook (FB). But then, you could have made the same argument about the internet 25 years ago and semiconductors 50 years ago. If you waited long enough, however, you obviously made a fortune.

Q: China is hoarding 69% of their wheat reserves. Is this because they plan to invade Taiwan?

A: No, it’s because there’s a global food crisis going on. Many countries, like India, have banned exports of food to protect themselves. People miss this about China: China will never have a war or invade anybody, because the second they do, their food supplies get cut off by us, who are the world’s largest producer of food. Plus, their trade would get shut off to pay for it, so they can’t buy it from somewhere else, and that’s done with us also. So, they need to be in our good graces in order to eat. That's the bottom line and that’s why Taiwan will never get invaded. Russia’s economy can operate independently for a while, but China’s can’t.

Q: Is the baby food shortage further evidence of a food crisis?

A: No, the baby formula crisis is being caused by a monopoly of three companies that control 100% of the baby food market; and the largest of these companies, accounting for a 40% market share of the baby food making, is producing baby food that is poisonous. That's why they got shut down. This has been going on for years, and for some reason, they got a free pass on regulation and inspections by the previous administration, which is ending now, and all of a sudden we’re finding out that 40% of the country’s baby food is contaminated and is being pulled off the market. So, it really has nothing to do with the global food crisis. That’s more related to Climate change—surprise, surprise—as it’s not raining in the right places like California, the war in Ukraine, which removed 13% of the world’s calories practically overnight.

Q: Should I bet the farm here with the ARK Innovation Fund (ARKK)? I like Cathie Woods’ bet on innovation or five-year time horizon. It’s a great thing, don’t you think?

A: Not so great when you drop 70% in the last year. And it is a high-risk bet that of her ten largest holding companies, you only need one of them to work for the fund to bring in a decent return. Of course, you may have to write off nine other companies to do that. But yes, it’s a great thing to own on the way up, not so great on the way down. I know some people who started scaling into ARK in November and came to regret it. I would wait on it—this is your highest leverage technology play, and if you really want some punishment, there’s a hedge fund that’s bringing out a 2X long ARK fund in the next couple of months. Then it’s basically option money you’re throwing out. If you want to put some money in that, you could get a 10x on the 2x ETF if you’re playing a recovery in ARK. So watch it; don’t touch it now because ARK is having another heart attack today, but something to consider if you like gambling.

Q: I am full up with a thousand shares of PayPal (PYPL). It’s now down 76%. What should I do?

A: I recommend you learn the art of stop losses. I stopped out of this thing last fall, and it’s continued to go down virtually every day. Whenever you buy a new position, automatically enter into your spreadsheet your stop loss for that position. Because things can drop by 80 or 90% and you work too hard for your money to throw it away on these big losses.

Q: What do you think about Steve Wynn and Wynn Hotels?

A: I’d be buying down here down 62%; it was announced today that Steve Wynn has secretly been acting as an agent for the Chinese government where (WYNN) has a major part of its operations. Who knew? With all those high rollers being flown in on private jets from China, sitting at the tables in the closed rooms. So yes, this is a recovery play and it will do just as well as all other recovery plays, but remember it’s a China recovery play. And I think, in any case, his ex-wife owns a big part of the company anyway. So I don’t think Steve Wynn is that closely connected with Wynn hotels because of past transgressions with the female staff.

Q: Is it time to scale into Freeport-McMoRan (FCX)?

A: I’d say yes. On a longer-term view, I expect (FCX) to go to $100. And for those who have the May $32/$35 call spread that expires on Friday, my bet is that you get the max profit—but you may not sleep before then.

Q: What do you have to say about a post-Putin scenario and impact on the market?

A: The day Putin dies of a heart attack, you can count on the market being up 10%, if that happens right now—less if it happens at a later date. But it would be hugely bullish for the entire global stock market, and oil would also collapse, which is why I refuse to put on oil plays here. That is a risk. Putin can give up, have an accident, or get overthrown. When the Russian people see their standard of living decline by 90%, this is a country that has a long history of revolutions, putting their leaders in front of firing squads and throwing the bodies down wells. So, if I were Putin, I wouldn't be sleeping very well right now.

Q: What's the reason for air tickets (UAL), (ALK), (DAL) going up sharply?

A: 1. Shortage of airplanes 2. Soaring fuel costs 3. Labor shortages and strikes 4. It is all proof of an economy that is definitely NOT going into recession.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

With Lieutenant Uhuru

Global Market Comments

April 14, 2022

Fiat Lux

Featured Trade:

(JULY 22 ZERMATT, SWITZERLAND STRATEGY SEMINAR)

(THE BULL CASE FOR BANKS),

(JPM), (BAC), (C), (WFC), (GS), (MS)

Global Market Comments

October 18, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD NEWS IS HERE)

(GS), (MS), (JPM), (BAC), (C), (BLK), (TLT), (BRKB), (SPY)