Followers of the Mad Hedge Fund Trader alert service have the good fortune to own deep-in-the-money options positions that expire on Friday, October 15, and I just want to explain to the newbies how to best maximize their profits.

These involve the:

(SPY) 10/$410-$420 call spread 10.00%

(GS) 10/$320-$330 call spread 10.00%

(JPM) 10/$130-$140 call spread 10.00%

(BLK) 10/$770-$790 call spread 10.00%

(MS) 10/$85-$90 call spread 10.00%

(BRKB) 10/$255-$265 call spread 10.00%

(C) 10/$62-$65 call spread 10.00%

Provided that we don’t have another 2,000-point move down in the market this week, these positions should expire at their maximum profit points.

So far, so good.

I’ll do the math for you on our deepest in-the-money position, the Goldman Sachs (GS) October 15 $320-$330 vertical bull call spread, which I most certainly will run into expiration. Your profit can be calculated as follows:

Profit: $10.00 expiration value - $8.50 cost = $1.50 net profit

(11 contracts X 100 contracts per option X $1.50 profit per options)

= $1,650 or 17.65% in 24 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning, October 18 and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and find it.

Although the expiration process is now supposed to be fully automated, occasionally machines do make mistakes. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload them pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market understandably disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration on Friday, October 15. So, if you plan to exit, do so well before the final expiration at the Friday market close.

This is known in the trade as the “expiration risk.”

One way or the other, I’m sure you’ll do OK, as long as I am looking over your shoulder, as I will be, always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next month-end.

Take your winnings and go out and buy yourself a well-earned dinner. Just make sure it’s take-out. I want you to stick around.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/09/john-and-girls.png322345Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-10-12 08:02:022021-10-12 11:31:04How to Handle the Friday, October 15 Options Expiration

(THE MAD HEDGE SUMMIT VIDEOS ARE UP),

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HAPPY DAYS ARE HERE AGAIN),

(GS), (MS), (JPM), (BAC), (C), (BLK), (TLT), (BRKB), (SPY)

(THE MAD HEDGE SUMMIT VIDEOS ARE UP),

(MARKET OUTLOOK FOR THE WEEK AHEAD, or IT’S SHOPPING TIME),

(MS), (GS), (JPM), (BLK), (BRKB), (C), (TLT), (F), (CRPT)

All indications are that we have a total nightmare of a Christmas coming up this year. Santa Claus and his elves can’t get any parts, and the reindeer are short of hay.

There are now a record 70 large container ships from China parked off the coast of Long Beach, CA and nobody to unload them. If they could be unloaded, there are no trucks to move the cargo or drivers to drive them. It turns out that stores don’t have enough staff to sell the products either.

You see this in share prices that are traditionally strong going into the holidays which have lately taken a pasting, like UPS (UPS) and FedEx (FDX).

Perhaps the US economy is losing up to a third of its total output due to parts and labor shortages. This will take at least a year to sort out.

Then there is the issue of 10 million missing workers. Are they afraid of dying of Covid? Or have they decided it’s time for a career change and that working for a minimum wage of $7.25 an hour is no longer worth it? This may take a decade to sort out.

Covid could be masking fundamental changes to the American economy and society which won’t become obvious until well into the 2030s.

Those of us who analyze these things can’t wait for the outcome. The global economy has just undergone more change than at any time since WWII. But what exactly happened we may not know for years.

Better to complete your Christmas shopping early this year or you may end up with a piece of coal in your stocking (where do I find coal in California?). And don’t forget to do some shopping for your retirement portfolio as well. Valuations are the best they have been in a year and this bull market in stocks has another nine years to run.

In the meantime, after dumping all of my technology stocks, I’ll be betting my entire persona net worth buying financial ones. These should lead the markets for the next six months, or until bond yields hit 2.0%, whichever comes first. Bonds now yield 1.46%.

With interest rates rising sharply, economic growth continuing at record levels, and default rates plunging, we are just entering a new golden age of banking.

Powell sees Inflation lasting higher for longer. It was enough to kill off a nascent rally in the bond market. The Dollar Store is about to become the $2 Store. Shortages from China are the reason.

Treasury Yields hit a three-month high. You can blame the coming taper, deal on a deficit-financed infrastructure bill, and drained Fed accounts against a coming massive supply of bonds. I’m already running a massive bond short. Keep selling rallies in the (TLT), or buy (TBT).

China bans Crypto, triggering a 7% plunge in Bitcoin. Financial systems the government can’t control are forbidden in the Forbidden City. It’s all part of a flight out of a restricted Yuan into unrestricted crypto by wealthy Chinese. China used to account for 99% of all Bitcoin mining and now it is at zero. The business will flock to the US, Canada, and any other country with cheap electricity. It’s a short-term negative for crypto but a long-term positive. Buy Bitcoin and Ethereum on the dip.

Case Shiller shatters all records, rising an astronomical 18.7% in June, a new record. Home prices are now 41% higher than the last peak in 2006. Phoenix was up an eye-popping 29.3%, San Diego by 27.1%, and Seattle by 25.0%. What are they putting in the water in these cities? My belief is that the structural shortfall of housing continues for another decade.

New Home Sales jump by 1.5% in August to a seasonally adjusted 740,000 units. The south saw the biggest gains at 6.0%. Median New Home Prices jumped an amazing 20.1% to 390,000 YOY. The exodus from the city to the burbs continues unabated. Inventory is at 6.1 months.

Pending Home Sales rocket, in August by 8.1% on a signed contract basis compared to only 1.2% expected. That’s a seven-month high. The Midwest led the charge with a 10.4% gain. Rising inventories and continued low interest rates were a big help. The bidding wars are abating.

China Energy Shortage causes Apple and Tesla cutback and they are buying 70% of America’s coal production to meet the shortfall. Several key chip packaging and testing service providers supplying Intel, Nvidia, and Qualcomm also received notices to suspend production at their facilities in Jiangsu for several days. It’s Another Black Swan from the Middle Kingdom.

The First Trust Skybridge Crypto Industry & Digital Economy ETF (CRPT) launched on September 23. It will be kicked off by my longtime friend and Mad Hedge Summit speaker Anthony Scaramucci. Get on the crypto train before it leaves the station.

Ford (F) announced massive $11.4 Billion in US EV factories in Kentucky and Tennessee in partnership with South Korea’s SK Innovations, creating 11,000 jobs. It is one of the largest US industrial investments in recent memory. It is all part of a plan to completely reposition the company and invest $30 billion in EVs by 2025. A smart move, (F) finally read the writing on the wall. My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a modest +1.03% gain in September. That’s against a Dow Average that was down -5.65% for the month. My 2021 year-to-date performance soared to 80.30%. The Dow Average was up 12.18% so far in 2021.

Figuring that we are either at or close to a market bottom, and being a man of my convictions, I am 80% invested in financial stocks. Those include (MS), (GS), (JPM), (BLK), (BRKB), and (C). In for a penny, in for a pound. I am also 10% invested in the (SPY) and 10% long bonds (TLT).

I quick trip by the Volatility Index (VIX) to $29 and a rapid 45 basis point leap in ten-year US Treasury bond yields gave us the entry point for all of these positions.

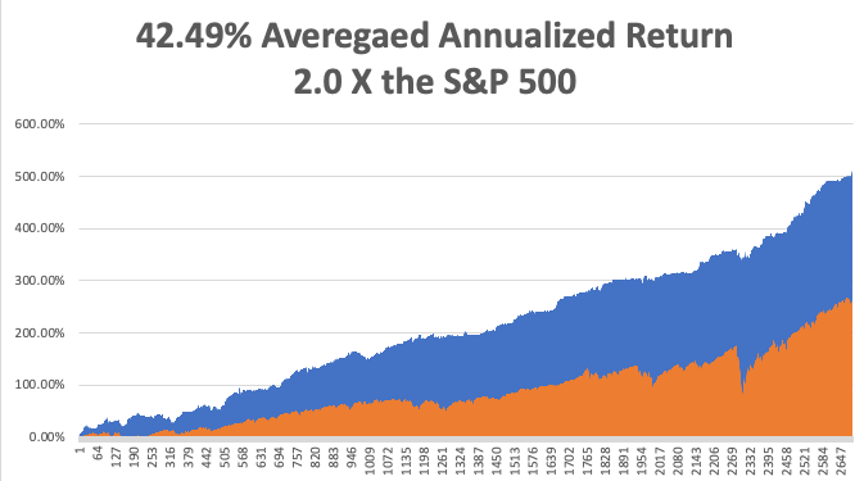

That brings my 12-year total return to 502.85%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.49%, easily the highest in the industry.

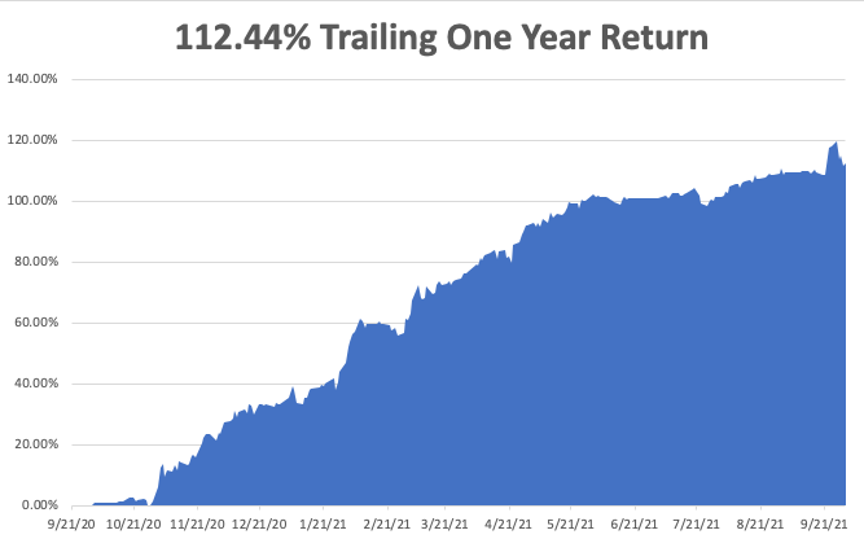

My trailing one-year return popped back to positively eye-popping 112.44%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 44 million and rising quickly and deaths topping 701,000, which you can find here.

The coming week will be slow on the data front.

On Monday, October 4 at 10:00 AM, US Factory Orders for August are out.

On Tuesday, October 5 at 8:30 AM, the US Balance of Trade for August is announced. On Wednesday, October 6 at 8:15 AM, we get the Challenger Private Jobs Report for September.

On Thursday, October 7 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, October 8 at 8:30 AM, we learn the September Nonfarm Payroll Report. At 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, in my many travels around the world, I never hesitate to visit places of historical interest. The London grave of Carl Marx, the Paris grave of Jim Morrison, the bridge of the cruiser of the USS San Francisco, which took a direct hit from an 18-inch Japanese shell, you name it.

After attending one of my global strategy luncheons in Charleston, South Carolina, where the Civil War began with the Confederates firing on Fort Sumter in 1861, I looked for something to do. Fort Sumter was a full day trip and there wasn’t much to see anyway.

So I pulled out my trusty iPhone to get some ideas. It only took me a second to decide. I attended Sunday church services at the Mother Emanuel African Methodist Episcopal Church, where 15 people were gunned down by a deranged white nationalist in 2014.

The church was built in 1891 by freed slaves and their children. The congregation dates back earlier to 1791. It has every bit a handmade touch with fine Victorian stained-glass windows.

The ushers stopped me at the door for 20 minutes where they suspiciously eyed me. Then they invited me in and sat me down next to the only other white person there, a Jewish woman from New York.

It was a working-class congregation and polyester suites and print dresses were the order of the day. Everyone was polite, if not respectful, and I sang the hymns with the air of a book in the pew in front of me.

The gospel singing was incredible, if not angelic. When I left, an usher thanked me for supporting their cause. Very moving. I praised them for their strength and tossed a $100 bill into the basket.

Charleston is a big wedding destination now, with young couples pouring in from all over the South to tie the knot. Saturday night on Market Street saw at least a dozen bachelor and hen parties going bar to bar and getting wasted, the women falling off their platform shoes.

The United States still has a lot of healing to go to recover from the recent years of turmoil. I thought this was one small step.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/10/methodist.png426560Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-10-04 12:02:552021-10-04 12:54:19The Market Outlook for the Week Ahead, or It’s Shopping Time

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE HIGHER WE GO THE CHEAPER WE GET),

(JPM), (BAC), (C), (GS), (MS), (BLK), (FCX), (X),

(WYNN), (MGM), (ALK), (LUV), (HAL), (SLB), (TLT)

I am sitting here holed up in my office in San Francisco.

Lake Tahoe is being evacuated as the Caldor fire is only ten miles away and the winds are blowing towards it. The visibility there is no more than 500 yards. The ski resorts are pointing their snow cannons towards their buildings to ward off flames.

Conditions are not much better here in Fog City. We are under a “stay at home” order due to intense smoke and heat. Even here, the fire engines are patrolling by once an hour.

The Boy Scout trip got cancelled this weekend, so the girls are having a cooking competition, chocolate chip waffles versus a German chocolate cake.

To make matters worse, I have been typing with only one finger all week, thanks to the elbow surgery I had on Tuesday. Next time, I’ll think twice before taking down a 300-pound steer. When I told the doctor how I incurred this injury, he laughed. “At your age?”

Which leaves me to contemplate this squirrelly stock market of ours. I have always been a numbers guy. But the higher the indexes rise, the cheaper stocks get. That’s not supposed to happen, but that is the fact.

We started out 2021 with an S&P 500 price earnings multiple of 25X. Now, we are down to a lowly 21X and the (SPY) is 20% higher, rising from $360 to $450.25.

The analyst community, ever the lagging indicator that they are, had S&P forward earnings for 2022 all the way down to $175. They have been steadily climbing ever since and are now touching $200 a share.

This is what 20/20 hindsight gets you. That and $5 will get you a cup of coffee at Starbucks. It takes a madman like me to go out on a limb with high numbers and then be right.

So what follows an ever-cheaper market? A more expensive one. That means stocks will continue to my set-in-stone target of $475 for the (SPY) for yearend, and (SPY) earnings of over $200 per share.

It gets better.

(SPY) earnings should hit $300 a share by 2025 and $1,400 a share by 2030. That makes possible my (SPY) target of $1,800 and my Dow Average target of 240,000 in a decade.

What are markets getting right that analysts and bears are getting wrong?

The future has arrived.

The pandemic brought forward business models and profitability by a decade. Technology is hyper-accelerating on all fronts.

Cycles are temporary but adoption is permanent. We are never going back to the old pre-pandemic economy. As a result, stocks are now worth a lot more than they were only two years ago.

So what do we buy now? There is a second reopening trade at hand, the post-delta kind. That means buying banks (JPM), (BAC), (C), brokers (GS), (MS), money managers (BLK), commodities (FCX), (X), hotels (WYNN), (MGM), airlines (ALK), (LUV), and energy (HAL), (SLB).

And what do we avoid like the plague? Bonds (TLT), which offer only confiscatory yields in the face of rising inflation with gigantic negative interest rates.

As for technology stocks, they will go sideways to up small in the aftermath of their ballistic moves of the past three months.

You all know that I am a history buff and there are particular periods of history that are starting to disturb me.

In August, we saw ten new intraday highs for the S&P 500 (SPY). That has not happened since 1987. Remember what happened in 1987?

We have not seen 11 new highs in August since 1929. The only negative three months seen since 1929 are August, September, and October. Remember what happened in 1929?

If that doesn’t scare the living daylights out of you, then nothing will. So, it seems we are in for some kind of correction, even if it’s just the 5% kind.

As for me, I’m looking forward to 2030.

The “Everything” Rally is on, according to my friend, Strategas founder Tom Lee. You can see it in the recent strength of epicenter stocks like energy, hotels, airlines, and casinos. It could run into 2022.

The Taper is this year and interest rate rises are later, said Jay Powell at Jackson Hole last week. Markets will be jumpy, especially bonds. Fed governor Jay Powell’s every word was parsed for meaning. Dove all the way. The larger focus will be on the August Nonfarm Payroll report out this week. Pfizer Covid vaccination gets full FDA approval, requiring millions more to get shots and bringing forward the end of the pandemic. All 5 million government employees will now get vaccinated, including the entire military. It’s the fastest drug approval in history. Some 37,000 new cases in one day. The stock market likes it. Take profits on (PFE) Bitcoin tops $50,000 after breaking several key technical levels to the upside. Next stop is a double top at $66,000. It helps that Coinbase is buying $500 million worth of crypto for its own portfolio. Buy (COIN) on dips. The US Dollar will crash in coming years, says Jeffry Gundlach and I think he is right. Emerging markets will become the next big play but not quite yet. Gold (GLD) will be a great hideout once it comes out of hibernation. China will soon return to outperforming the US. The dollars reserve currency status is at risk. The lumber crash is saving $40,000 per home, says Toll Brothers (TOL) CEO, Doug Yearly. Last year, lumber prices surged from $300 per board foot to an insane $1,700, thanks to a Trump trade war with Canada and soaring demand. It all flows straight through the bottom line of the homebuilders which should rally from here. Buy (TOL) on dips. China’s crackdown creates investment opportunities, says emerging investing legend Mark Mobius. He sees corporate governance improving over the long term. The gems are to be found among smaller companies not affected by Beijing’s hard-line. Mobius loves India too. My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a healthy +7.62% gain in August. My 2021 year-to-date performance appreciated to 76.83%. The Dow Average was up 15.87% so far in 2021.

That leaves me 80% in cash at 20% in short (TLT) and long (SPY). I’m keeping positions small as long as we are at extreme overbought conditions.

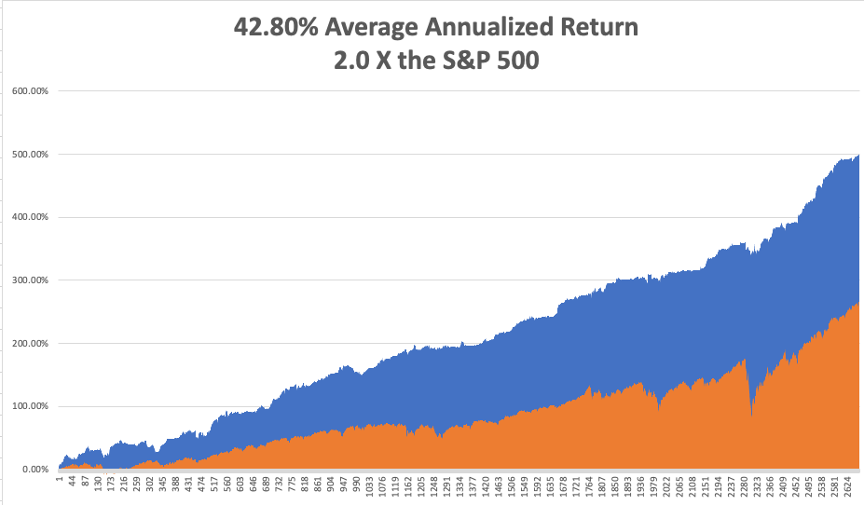

That brings my 12-year total return to 499.38%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.80%, easily the highest in the industry.

My trailing one-year return popped back to positively eye-popping 116.67%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 39 million and rising quickly and deaths topping 638,000, which you can find here.

The coming week will bring our monthly blockbuster jobs reports on the data front.

On Monday, August 30 at 11:00 AM, Pending Home Sales are published. Zoom (ZM) reports.

On Tuesday, August 31, at 10:00 AM, S&P Case Shiller National Home Price Index for June is released. CrowdStrike (CRWD) reports.

On Wednesday, September 1 at 10:45 AM, the ADP Private Employment report is disclosed.

On Thursday, September 2 at 8:30 AM, Weekly Jobless Claims are announced. DocuSign (DOCU) reports.

On Friday, September 3 at 8:30 AM, the all-important August Nonfarm Payroll report is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

Oh and the German chocolate cake won, but please don’t tell anyone.

As for me, given the losses in Afghanistan this week, I am reminded of my several attempts to get into this troubled country.

During the 1970s, Afghanistan was the place to go for hippies, adventurers, and world travelers, so of course, I made a beeline for straight for it.

It was the poorest country in the world, their only exports being heroin and the blue semiprecious stone lapis lazuli, and illegal export of lapis carried a death penalty.

Towns like Herat and Kandahar had colonies of westerners who spent their days high on hash and living life in the 14th century. The one cultural goal was to visit the giant 6th century stone Buddhas of Bamiyan 80 miles northwest of Kabul.

I made it as far as New Delhi in 1976 and was booked on the bus for Islamabad and Kabul ($25 one-way). Before I could leave, I was hit with amoebic dysentery.

Instead of Afghanistan, I flew to Sydney, Australia where I had friends and knew Medicare would take care of me for free. I spent two months in the Royal North Shore Hospital where I dropped 50 pounds, ending up at 125 pounds.

I tried to go to Afghanistan again in 2010 when I had a large number of followers of the Mad Hedge Fund Trader stationed there, thanks to the generous military high-speed broadband. The CIA waved me off, saying I wouldn’t last a day as I was such an obvious target.

So, alas, given the recent regime change, it looks like I’ll never make it to Afghanistan. I won’t live long enough to make it to the next regime change. It’s just one more concession I’ll have to make to my age. I’ll just have to content myself reading A One Thousand and One Nights at home instead. The Taliban blew up the stone Buddhas of Bamiyan in 2001.

In the meantime, I am on call for grief counseling for the Marine Corps for widows and survivors. Business has been thankfully slow for the last several years. But I’ll be staying close to the phone this weekend just in case.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-india.png576864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-30 09:02:562021-08-30 10:27:35The Market Outlook for the Week Ahead, or The Higher We Go the Cheaper We Get

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-22 11:06:552021-03-22 13:19:50March 22, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visist to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.