Global Market Comments

July 26, 2024

Fiat Lux

Featured Trade:

(AUGUST 15 LONDON ENGLAND STRATEGY LUNCHEON)

(JULY 24 BIWEEKLY STRATEGY WEBINAR Q&A),

(UUP), (FXE), (FXC), (FXA), (FXB), (USO),

(FCX), (CCJ), (FXI), (CAT), (DE), (NVDA)

Global Market Comments

July 26, 2024

Fiat Lux

Featured Trade:

(AUGUST 15 LONDON ENGLAND STRATEGY LUNCHEON)

(JULY 24 BIWEEKLY STRATEGY WEBINAR Q&A),

(UUP), (FXE), (FXC), (FXA), (FXB), (USO),

(FCX), (CCJ), (FXI), (CAT), (DE), (NVDA)

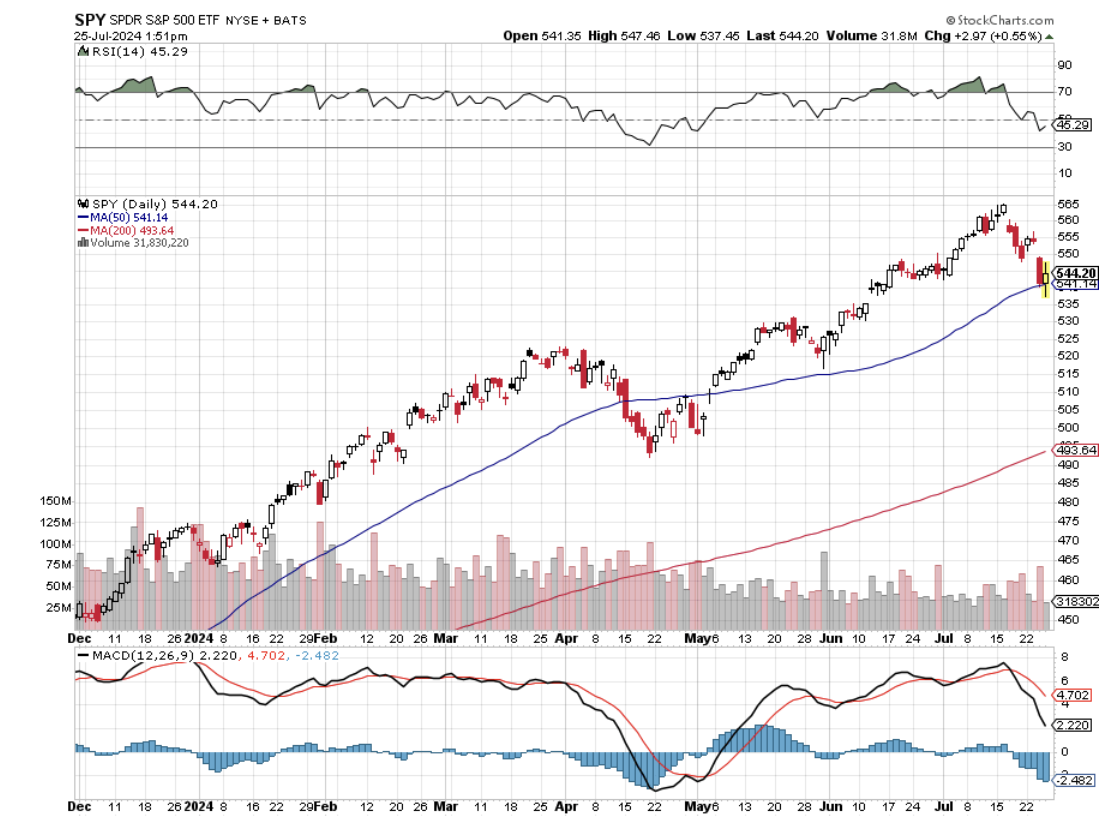

Below please find subscribers’ Q&A for the July 24 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Zermatt, Switzerland.

Q: Does the entry of Kamala Harris into the presidential election have any effect on the stock market?

A: No. I know someone who did research on markets and elections going all the way back to 1792 and the long-term effect has been absolutely zero over the 232-year period. Actually, what happens is you have the two candidates very close to each other in the polls, so uncertainty is at a maximum. Markets hate uncertainty, so they’ll wait until the uncertainty goes away, which will probably be about two weeks before the election. You can expect a really hot 4th quarter in the market though, so get all your cash freed up so you can pour all your money into the market for the last quarter of the year.

Q: How do falling interest rates affect the US dollar (UUP) and the currencies?

A: Currencies (FXE), (FXC), (FXA), (FXB) are always driven by interest rates. Those with high interest rates like the US dollar, are strong; those with low interest rates like Japan, are weak. Japan has had zero rates for over 20 years now. When that reverses, those currencies reverse, ending up with a weak US dollar and a strong euro, pound, etc. These changes in direction for the currency markets only happen every few years, so that will be a reliable trade.

Q: Why is oil (USO) so cheap when the rest of the economy is so strong?

A: There are many reasons. One is that the amount of barrels of oils needed to produce a unit of GDP has been falling for 30 years. That's a function of engines becoming more efficient at using gasoline. Plus more people are switching out of gasoline into electric, and more people flying instead of driving. The “work at home” movement hasn’t helped oil demand either. It’s also the most subsidized industry in the US, and you always get overproduction leading to price crashes, which we now seem to be witnessing.

Q: I have Freeport McMoRan (FCX) as a long-term hold; why has it recently been so weak?

A: Well, the number one reason is China (FXI). China is the biggest consumer of copper in the world and their economy is dead in the water. You know, 4.5% or 4.7% is a long way from the 13% we used to get during the 2000s and when copper was absolutely on fire. Eventually, I expect industrial demand in the US to make up for the shortage of demand from China, but that isn’t happening right now. It isn’t just copper—all the industrial metals have been weak the last couple of months and that is the reason.

Q: Cameco Corporation (CCJ) has been down lately, even with seemingly good news out of Kazakhstan. Is this a good buy here at the 200-day?

A: I would say it is. It’s being dragged down by the rest of the industrial metals and the energy plays. If you watch carefully, the uranium stocks trade very closely with oil, and we have an oil glut, so it tends to drag down all the other energy forms with it, including uranium and natural gas. I love uranium demand long term; it's growing far faster than oil demand and that’s why I own (CCJ).

Q: Do you think falling interest rates will bail out the real estate market?

A: Absolutely, yes. 30-year fixed-rate mortgages hanging around the mid-sixes, you get a couple of rate cuts and we could be back into the fives and even the fours in no time. So yes, big impact on real estate, all the subsidiary plays, on home builders, on the entire economy.

Q: If the market reverses today or tomorrow, what are some of the best call options to put money into?

A: Caterpillar (CAT), Deer & Co. (DE), and you might even go $50 into the money on Nvidia (NVDA). Home builders I would love to get into as well. All of these things have had great runs, but these are just the 1st leg of moves that could go on for years. So yes, this is where the barbell portfolio works: half big tech, half domestic recovery plays.

Q: Are you stopping at Edelweiss for a frosty beer on your hike?

A: Absolutely, I go to Edelweiss every year and don’t mind climbing the 1,200 feet to get there. You certainly have an appetite when you get to the top. It has a fantastic view of the town and you can stay there overnight there as well.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 12, 2024

Fiat Lux

Featured Trade:

(WHAT TO BUY AT MARKET TOPS?),

(CAT), ($COPPER), (FCX), (BHP), (RIO),

(TESTIMONIAL)

Global Market Comments

February 22, 2024

Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL)

Global Market Comments

January 3, 2024

Fiat Lux

2024 Annual Asset Class Review

A Global Vision

FOR PAID SUBSCRIBERS ONLY

Featured Trades:

(SPX), (QQQ), (IWM) (AAPL), (XLF), (BAC) (JPM), (BAC), (C), (MS), (GS),

(X), (CAT), (DE),(TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD), (FXE), (EUO),

(FXC), (FXA), (YCS), (FXY), (CYB), (DIG), (RIG), (USO), (DUG), (UNG), (USO),

(XLE), (AMLP),(GLD), (DGP), (SLV), (PPTL), (PALL), (ITB), (LEN), (KBH), (PHM)

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have a comfortable seat next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini can navigate it.

I am anything but Houdini, so I foray downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to ensure everything goes well during the long adventure and keep me up to date with the onboard gossip.

The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

Chicago’s Union Station

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way, like Omaha, Salt Lake City, and Reno, to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 15 Pro.

Here is the bottom line which I have been warning you about for months. In 2024 we will probably top the 70.44% we made last year, but you are going to have to navigate the reefs, shoals, hurricanes, and the odd banking crisis. Do it and you can laugh all the way to the bank. I will be there to assist you in navigating every step.

The first half of 2024 will be all about trading, making bets on when the Fed starts cutting interest rates. Technology will continue their meteoric melt-up. In the second half, I expect the cuts to actually take place and markets to go straight up. Domestic industrials, commodities, financials, energy foreign markets, and currencies will lead.

And here is my fundamental thesis for 2024. After the Fed kept rates too low for too long and then raised them too much, it will then panic and lower them again too fast to avoid a recession. In other words, a mistake-prone Jay Powell will keep making mistakes. That sounds like a good bet to me.

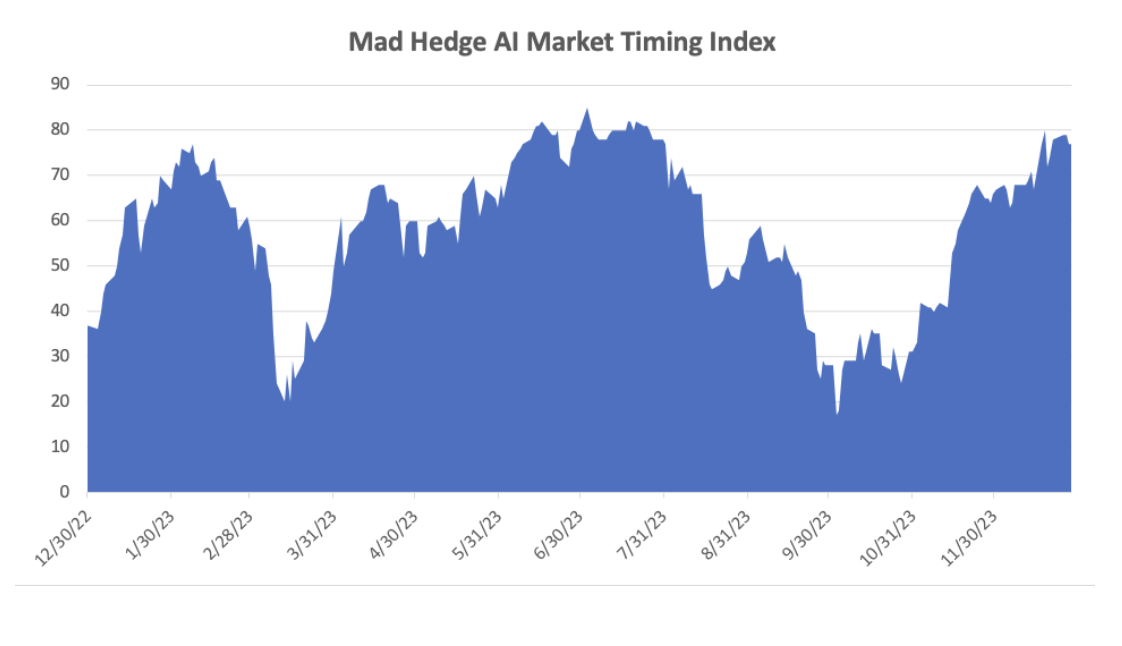

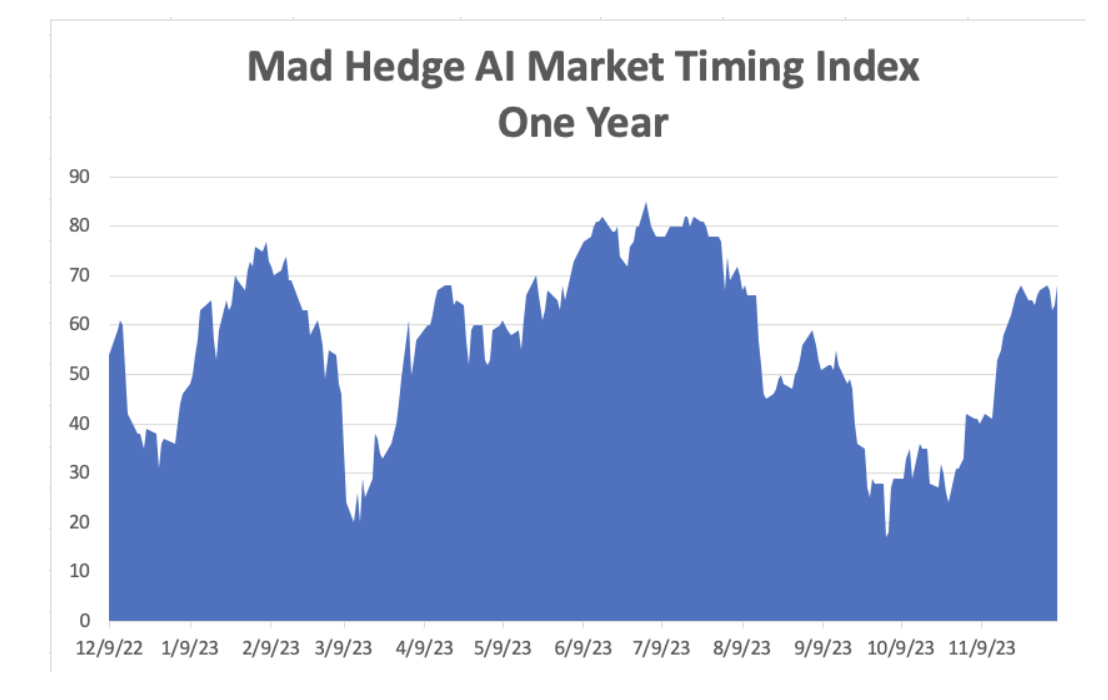

Keep in mind that the Mad Hedge AI Market Timing Index is at the absolute top end of its historic range the three-month likelihood of you making money on a trade is essentially zero. But adhere to the recommendations I make in this report today and you should be up about 30% in a year.

Let me give you a list of the challenges I see financial markets facing in the coming year:

The Ten Key Variables for 2024

1) When will the Fed pivot?

2) When will quantitative tightening end?

3) How soon will the Russians give up on Ukraine?

4) When will the rotation from technology to domestic value plays happen?

5)How much of falling interest rates will translate into higher gold prices?

6) When will the structural commodities boom get a second wind?

7) How fast will the US dollar fall?

8) How quickly will lower interest rates feed into a hotter real estate market?

9) How fast can the Chinese economy bounce back from Covid-19?

10) When does the next bull market in energy begin?

All the answers are below:

Somewhere in Iowa

The Thumbnail Portfolio

Equities – buy dips

Bonds – buy dips

Foreign Currencies – buy dips

Commodities – buy dips

Precious Metals – buy dips

Energy – buy dips

Real Estate – buy dips

1) The Economy – From Hot to Cool to Hot Again

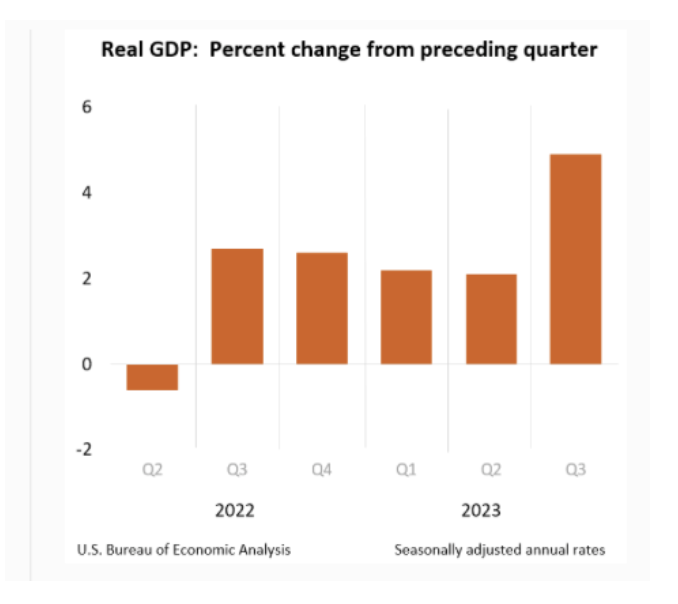

2023 was a terrible year for economists who largely got it wrong. Many will be driving Uber cabs from January.

The economy is clearly slowing now from the red-hot 5.2% GDP growth rate we saw in Q3 to a much more modest 2.0% rate in Q4. We’ll get the first read on the end of January.

Any more than that and the Fed will panic and bring interest rate cuts dramatically forward to head off a recession. That is clearly what technology stocks were discounting with a melt-up of Biblical proportions, some 19% in the last two months, or $65 in the (QQQ)’s.

Anywhere you look, the data is softening, save for employment, which is holding up incredibly well at a 3.7% headline Unemployment Rate. The labor shortage may be the result of more workers dying from COVID-19 than we understand. Far more are working from home not showing up in the data. And many young people have just disappeared off the grid (they’re in the vans you see on the freeways).

The big picture view of what’s going on here is that after 15 years of turmoil caused by the 2008 financial crisis, pandemic, ultra-low interest rates, and excessive stimulus, we may finally be returning to normal. That means long-term average growth and inflation rates of 3.0% each.

I can’t wait.

2) Equities (SPX), (QQQ), (IWM) (AAPL), (XLF), (BAC) (JPM), (C), (MS), (GS), (X), (CAT), (DE)

As I travel around the world speaking with investors, I notice that they all have one thing in common. They underestimate the impact of technology, the rate at which it is accelerating, its deflationary impact on the economy, and the positive influence they have on all stocks, not just tech ones. And the farther I get away from Silicon Valley the poorer the understanding.

Since my job is to make your life incredibly easy, I am going to simplify my equity strategy for 2024.

It's all about falling interest rates.

You should pay attention. In my January 4, 2023 Annual Asset Class Review (click here), I predicted the S&P 500 would hit $4,800 by year-end end. Here we are at $4,752.

I didn’t nail the market move because I am omniscient, possess a crystal ball, or know a secret Yaqui Indian chant. I have spent the last 30 years living in Silicon Valley and have a front-row seat to the hyper-accelerating technology here.

Since the time of the Roman Empire advancing technology has been highly deflationary (can I get you a deal on a chariot!). Now is no different, which meant that the Federal Reserve would have to stop raising interest rates in the first half of the year.

The predictions of a decade-long battle with rising prices like we saw in the seventies and eighties proved so much bunk, alarmism, and clickbait. In fact, the last 25 basis point rate rise took place on July 26, taking up from an overnight rate of 5.25% to 5.5%. That rendered the hard landing forecasts for the economy nonsense.

When interest rates are as high as they are now, you only look at trades and investments that can benefit from falling interest rates. All stocks actually benefit from cheaper money, but some much more than others.

In the first half, that will be technology plays like Apple (AAPL), (Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta (META), and NVIDIA (NVDA). Much of this move was pulled forward into the end of 2023 so this sector may flatline for a while.

In the second half, value plays will take the leadership like banks, (JPM), (BAC), (C), financials (MS), (GS), homebuilders (KBH), (LEN), (PHM), industrials (X), capital goods (CAT), (DE), and commodities (FCX). Everything is going to new all-time highs. My Dow average of 120,000 by the end of the decade is only one more triple away and is now looking very conservative.

That means we now have at hand a generational opportunity to get into the fastest-growing sectors of the US economy at bargain prices. I’m talking Cadillacs at KIA prices. Corporate profits powered by accelerating technology, artificial intelligence, and capital spending will rise by large multiples. Every contemporary earnings forecast will come up short and have to be upgraded. 2024 will be a year of never-ending upgrades.

After crossing a long, hot desert small-cap stocks can finally see water. That’s because they are the most leveraged, undercapitalized, and at the mercy of interest rates and the economic cycle. They always deliver the most heart-rending declines going into recessions. Guess what happens now with the economy headed for a soft landing? They lead to the upside, with some forecasts for the Russell 2000 going as high as a ballistic 50%.

Another category of its own, Biotech & Health Care which is now despised, should do well on its own as technology and breakthroughs are bringing new discoveries. Artificial intelligence is discovering new drugs at an incredible pace and then telling you how to cheaply manufacture them. My top three picks there are Eli Lily (ELI), Abbvie (ABBV), and Merck (MRK).

There is another equity subclass that we haven’t visited in about a decade, and that would be emerging markets (EEM). After ten years of punishment from a strong dollar, (EEM) has been forgotten as an investment allocation. We are now in a position where the (EEM) is likely to outperform US markets in 2024, and perhaps for the rest of the decade. The drivers here are falling interest rates, a cheaper dollar, a reigniting global economy, and a new commodity boom.

Block out time on your calendars, because whenever the Volatility Index (VIX) tops $20, up from the current $12, I am going pedal to the metal, and full firewall forward (a pilot term), and your inboxes will be flooded with new trade alerts.

What is my yearend prediction for the S&P 500 for 2024. We should reach $5,500, a gain of 14.58%. You heard it here first.

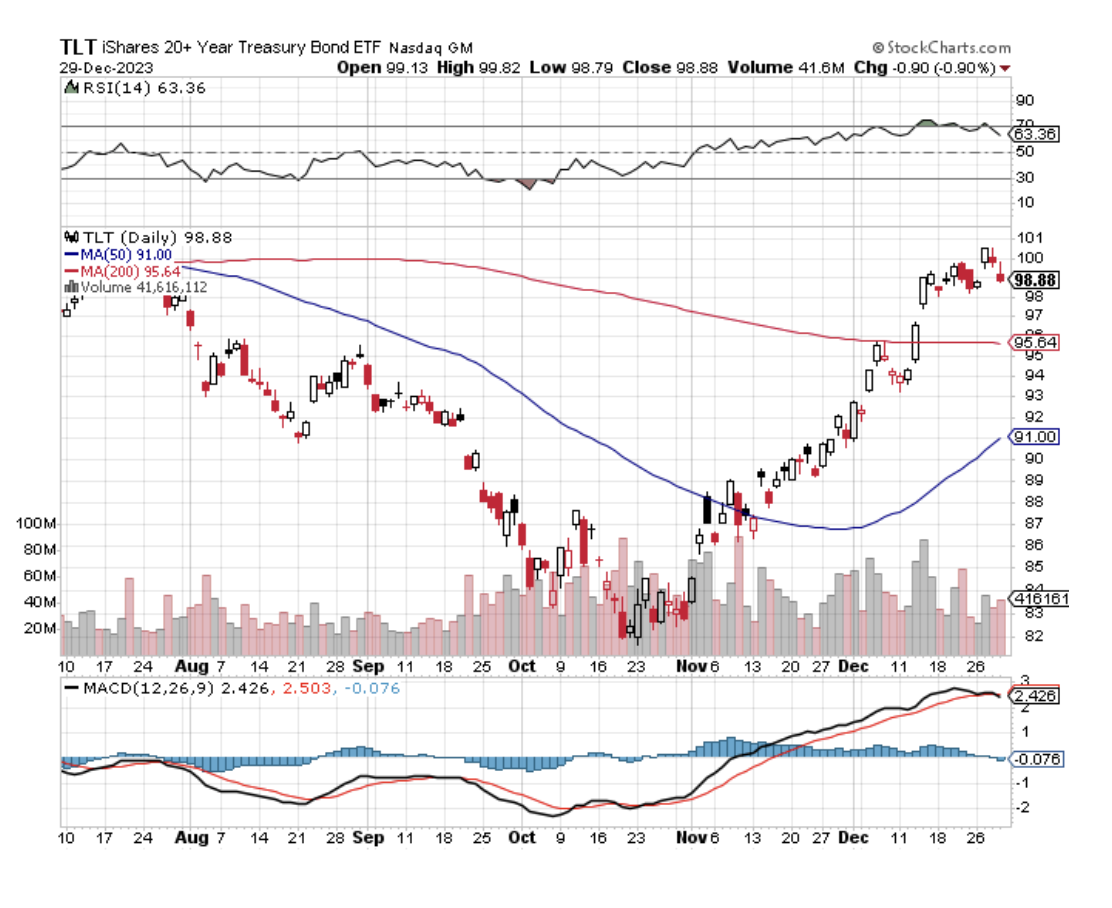

3) Bonds (TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD)

Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites returning home by train because their religion forbade automobiles or airplanes.

The old bond trade is dead.

Long live the new bond trade!

After selling short bonds (TLT) from $180 all the way down to $82, I flipped to the long side on October 17. The next week, bonds saw their biggest rally in history, making instant millionaires out of several of my followers. The (TLT) has since rocketed from $82 to an eye-popping $100, a 22% gain.

In a heartbeat, we went from super bear to hyper bull.

I am looking for the Fed to cut interest rates by 1.00% in 2024 but won’t begin until the second half of the year. All of the first half bond gains were pulled forward into 2023 so I am looking for long periods of narrow trading ranges. By June, economic weakness will be so obvious that a dramatic Fed rate-cutting policy will ensue.

In addition, the Fed will end its quantitative tightening program by June, which is currently sucking $90 billion a month out of the economy. That’s a lot of bond-selling that suddenly ends.

I’m looking for $120 in the (TLT) sometime in 2024, with a possible stretch to $130. Use every five-point dip to load up on shares in the (TLT) ETF, calls, call spreads, and one-year LEAPS. This trade is going to work fast. It is the low-hanging fruit of 2024.

We are never going back to the 0.32% yields, and $165 prices we saw in the last bond peak. But you can still make a lot of money in a run-up from $82 to $120, as many happy bondholders are now discovering.

It isn’t just bonds that are going up. The entire interest rate space is doing well including junk bonds (JNK), municipal bonds (MUB), REITS (NLY), preferred stock, and convertible bonds.

A Visit to the 19th Century

4) Foreign Currencies (FXE), (EUO), (FXC), (FXA), (YCS), (FXY), (CYB)

With a major yield advantage over the rest of the world for the last decade, the US dollar has been on an absolute tear. After all, the world’s strongest economy begets the world’s strongest currency.

That is about to end.

If your primary assumption is that US interest rates will see a sharp decline sometime in 2024, then the outlook for the greenback is terrible.

Currencies are driven by interest rate differentials and the buck is soon going to see the fastest shrinking yield premium in the forex markets.

That shines a great bright light on the foreign currency ETFs. You could do well buying the Australian Dollar (FXA), Euro (FXE), Japanese yen (FXE), and British Pound (FXB). I’d pass on the Chinese yuan (CYB) right now until their Covid shutdowns end.

Look at the 50-year chart of the US dollar index below and you’ll see that a 13-year uptrend in the buck is rolling over and will lead to a 5-10-year down move. Draw your weapons.

5) Commodities (FCX), (VALE), (DBA)

Commodities are the high beta players in the financial markets. That’s because the cost of being wrong is so much higher. Get on the losing side of commodities and you will be bled dry by storage costs, interest expenses, contangos, and zero demand.

Commodities have one great attribute. They predict recessions and recoveries earlier than any other asset class. When they peaked in March of 2022, they were screaming loud and clear that a recession would hit in early 2023. By reversing on a dime on November 13, 2023, they also told us that a rip-roaring recovery would begin in 2024.

You saw this in every important play in the sector, including Broken Hill (BHP), Peabody Energy (BTU), and Freeport McMoRan (FCX). And who but me noticed that Alcoa Aluminum (AA) was up an incredible 50% in December? Maybe you can’t teach an old dog new tricks, but the old tricks work pretty darn well!

The heady days of the 2011 commodity bubble top are about to replay. Now that this sector is convinced of a substantially weaker US dollar and lower inflation, it is once more a favorite target of traders.

China will finally rejoin the global economy as a growth engine in 2024 but at only half its previous growth rate. It will be replaced by India, which is turning into the new China and is now the most populous country in the world.

And here’s another big new driver. Each electric vehicle requires 200 pounds of copper and production is expected to rise from 2 million units a year to 20 million by 2030. Annual copper production will have to increase three-fold in a decade to accommodate this increase, no easy task or prices will have to rise.

The great thing about commodities is that it takes a decade to bring new supply online, unlike stocks and bonds, which can merely be created by an entry in an Excel spreadsheet. As a result, they always run far higher than you can imagine.

Accumulate all commodities on dips.

6) Energy (DIG), (RIG), (USO), (DUG), (UNG), (USO), (XLE), (AMLP)

Energy was the top-performing sector of 2023 until it wasn’t.

We got a nice boost to $90 a barrel from the Gaza War. But that faded rapidly as there was never an actual supply disruption, just the threats of one. Saudi production has been cut back so far, some 5 million barrels a day, that it risks budget shortfalls if it reduces any more. In the meantime, US fracking production has taken off like a rocket.

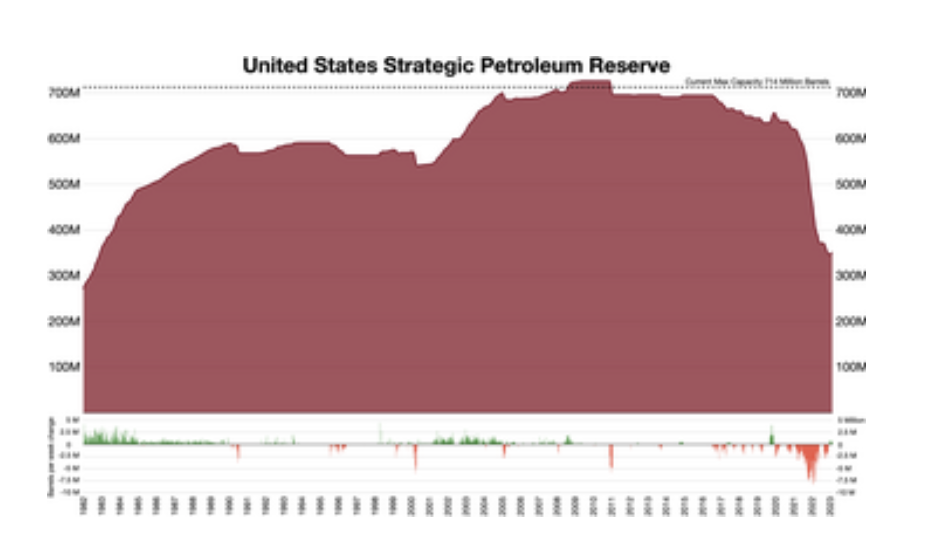

In the meantime, Joe Biden is sitting on the bid in an effort to refill the Strategic Petroleum Reserves that was drawn down from 723 to 350 million barrels during the last price spike.

The trade here is to buy any energy plays when Texas tea approaches $70 and take profits at $95. Your first picks should be ExxonMobile (XOM), Occidental Petroleum (OXY) where Warren Buffet has a 27% stake, Diamondback Energy (FANG), and Devon Energy (DVN).

The really big energy play for 2024 will be in natural gas (UNG), which was slaughtered in 2023. The problem here was not a shortage of demand because China would take all we could deliver. It was in our ability to deliver, hobbled by the lack of gasification facilities needed to export. One even blew up.

In 2024 several new export facilities came online and the damaged one was repaired. That should send prices soaring. Natural gas prices now at a throw-away $2.00 per MM BTU could make it to $8.00 in the next 12 months. That takes the (UNG) from $5.00 to $15.00 (because of the contango).

Buy (UNG) LEAPS (Long Term Equity Anticipation Securities) right now.

Remember, you will be trading an asset class that is eventually on its way to zero sooner than you think. However, you could have several doublings on the way to zero. This is one of those times. And you also have a huge 35% contango headwind working against you all the time.

They call this commodity the “widow maker” for a good reason.

The real tell here is that energy companies are bailing on their own industry. Instead of reinvesting profits back into their future exploration and development, as they have for the last century, they are paying out more in dividends and share buybacks.

Take the money and run. Trade, don’t marry this asset class.

There is the additional challenge in that the bulk of US investors, especially environmentally friendly ESG funds, are now banned from investing in legacy carbon-based stocks. That means permanently cheap valuations and share prices for the energy industry.

Energy now counts for only 5% of the S&P 500. Twenty years ago, it boasted a 15% weighting.

The gradual shutdown of the industry makes the supply/demand situation infinitely more volatile.

To understand better how oil might behave in 2024, I’ll be studying US hay consumption from 1900-1920. That was when the horse population fell from 100 million to 6 million, all replaced by gasoline-powered cars and trucks.

The internal combustion engine is about to suffer the same fate.

7) Precious Metals (GLD), (DGP), (SLV), (PPTL), (PALL)

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly, that it blew a passenger train over on its side.

In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th-century gold mines and broken-down wooden trestles leading to huge piles of tailings, and relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

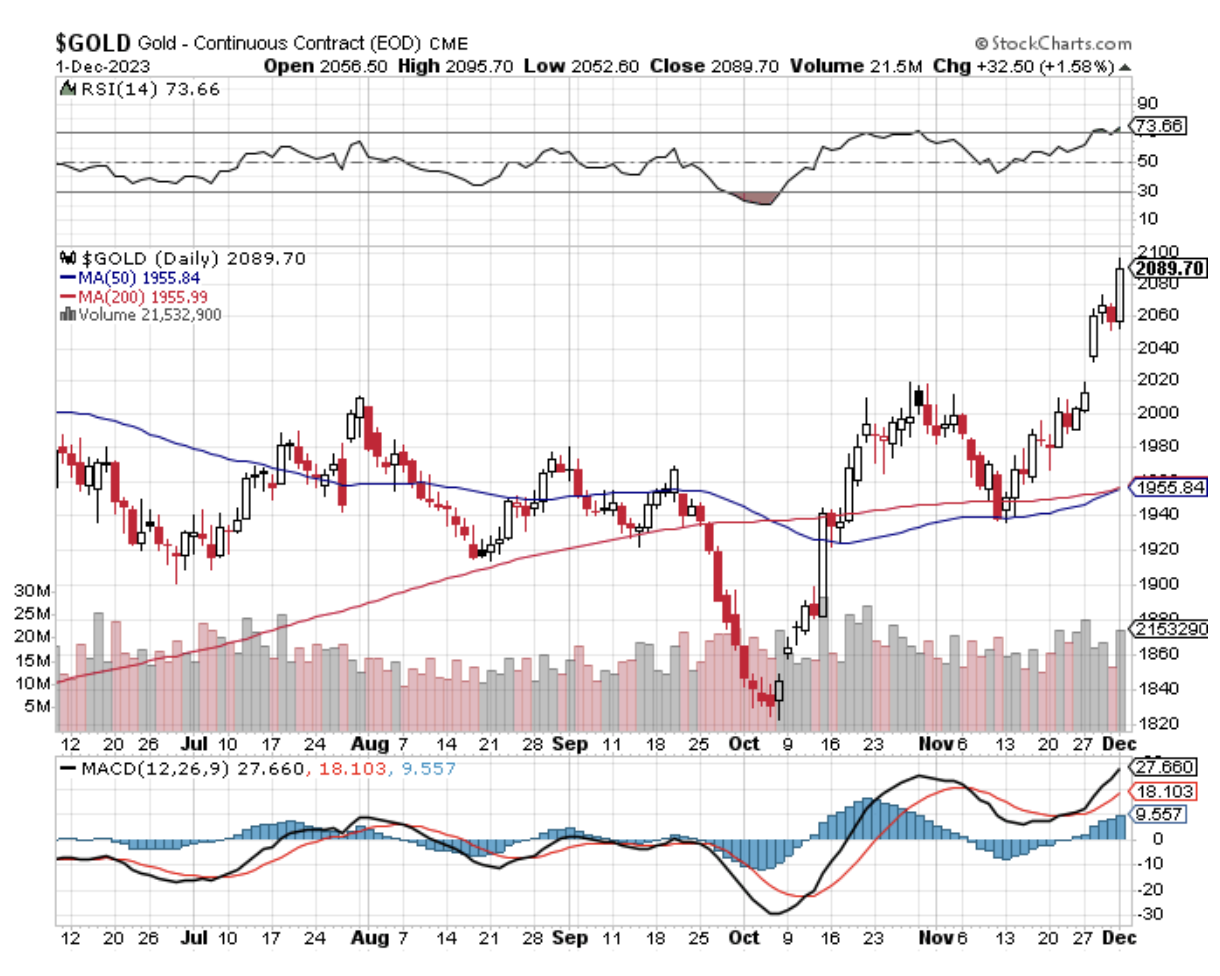

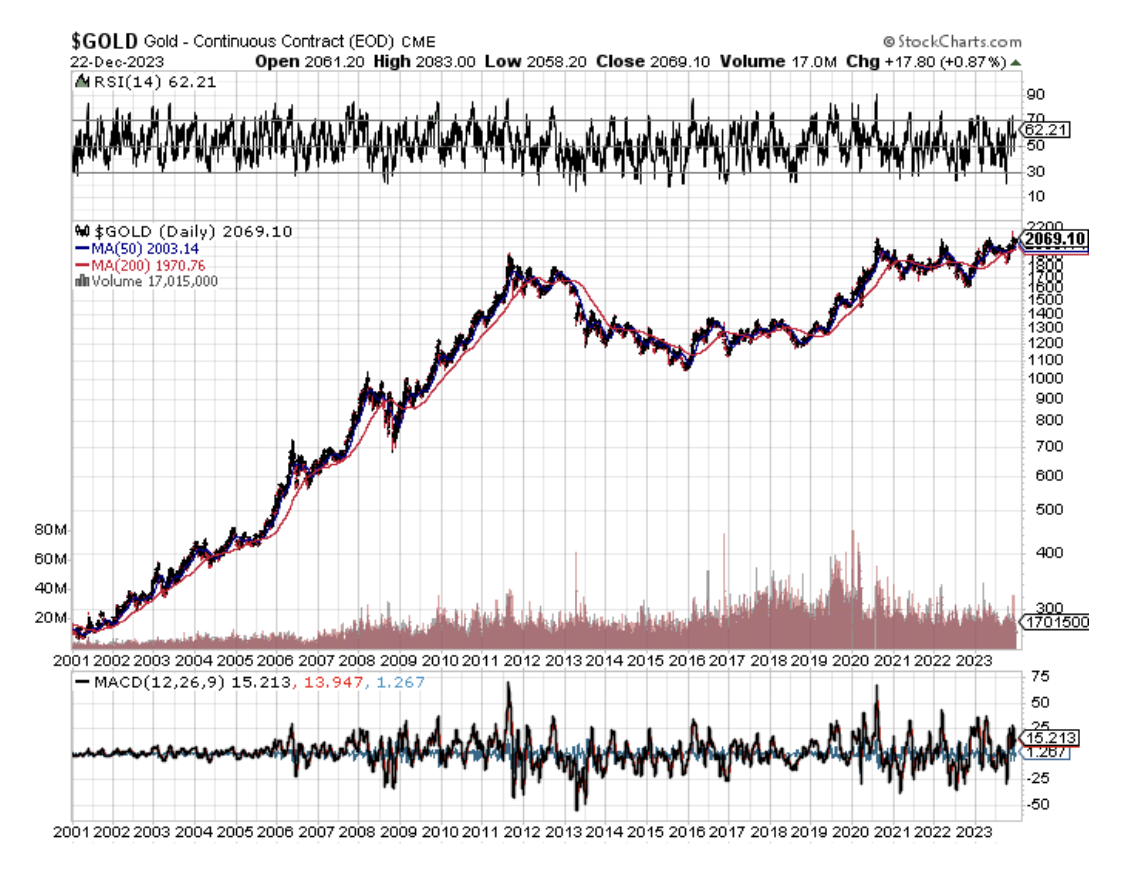

Here it’s important to look at the long view on gold. The barbarous relic tends to have good and bad decades. During the 2000’s the price of the yellow metal rose tenfold, from $200 to $2,000. The 2010s were very boring when gold was unchanged. Gold is doing well this decade, already up 40%, and a double or triple is in the cards.

2023 should have been a terrible year for precious metals. With inflation soaring, stocks volatile, and interest rates soaring, gold had every reason to collapse. Instead, it was up on the year, thanks to a heroic $325, 17.8%% rally in the last two months.

The reason is falling interest rates, which reduce the opportunity costs of owning gold. The yellow metal doesn’t pay a dividend, costs money to store and insure, and delivery is an expensive pain in the butt.

Chart formations are looking very encouraging with a massive upside breakout in place. So, buy gold on dips if you have a stick of courage on you, which you must if you read this newsletter.

Of course, the best investors never buy gold during a bull market. They Hoover up gold miners, which rise four times faster, like Barrack Gold (GOLD), Newmont Mining (NEM), and the basket play Van Eck Vectors Gold Miners ETF (GDX).

Higher beta silver (SLV) will be the better bet, as it already has been because it plays a major role in the decarbonization of America. There isn’t a solar panel or electric vehicle out there without some silver in them and the growth numbers are positively exponential. Keep buying (SLV), (SLH), and (WPM) on dips.

8) Real Estate (ITB), (LEN), (KBH), (PHM)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving bands of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the Transcontinental Railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

Those tormented by the shrinking number of real estate transactions over the past two years take solace. The past excesses have been unwound and we are now on the launching pad for another decade-long bull market.

There is a generational structural shortage of supply with housing which won’t come back into balance until the 2030’s. You don’t have a real estate crash when we are short 10 million homes.

The reasons, of course, are demographic. There are only three numbers you need to know in the housing market for the next ten years: there are 80 million baby boomers, 65 million Generation Xers who follow them, and 86 million in the generation after that, the Millennials.

The 76 million baby boomers (between ages 62 and 79) have been unloading dwellings to the 72 million Gen Xers (between age 41 and 56) since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis. That has created the present shortage of housing, both for ownership and rentals.

There is a happy ending to this story.

The 72 million Millennials now aged 25-40 are now the dominant buyers in the market. They are transitioning from 30% to 70% of all new buyers of homes. They are also just entering the peak spending years of middle age, which is great for everyone. Hot on their heels are 68 million Gen Z, which are now 12 to 27 years old.

The Great Millennial Migration to the suburbs and Middle America has just begun. Thanks to the pandemic and Zoom, many are never returning to the cities. That has prompted massive numbers to move from the coasts to the American heartland.

That’s why Boise, Idaho was the top-performing real estate market in 2023, followed by Phoenix, Arizona. Personally, I like Reno, Nevada, where Apple, Google, Amazon, and Tesla are building factories as fast as they can, just a four-hour drive from Silicon Valley.

As a result, the price of single-family homes should continue to rise during the 2020s, as they did during the 1970s and the 1990s when identical demographic forces were at play.

This will happen in the context of a labor shortfall, rising wages, and improving standards of living.

Increasing rents are accelerating this trend. Renters now pay 35% of their gross income, compared to only 18% for owners, and less, when multiple deductions and tax subsidies are considered. Rents are now rising faster than home prices.

Remember, too, that the US will not have built any new houses in large numbers in 17 years. The 50% of small home builders that went under during the Financial Crisis never came back.

We are still operating at only half of the 2007 peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

There is a new factor at work. We are all now prisoners of the 2.75% 30-year fixed-rate mortgages we all obtained over the past five years. If we sell and try to move, a new mortgage will cost double today. If you borrow at a 2.75% 30-year fixed rate, and the long-term inflation rate is 3%, then, over time, you will get your house for free. That’s why nobody is selling, and prices have barely fallen.

This winds down in 2024 as the Fed realizes its many errors and sharply lowers interest rates. Home prices will explode…. again.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now after you throw in all the tax breaks. It’s also a great inflation play.

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) are a buy on the dip. But don’t forget to sell your home by the 2030s when the next demographic headwind resumes. That’s when you should unload your home to a Millennial or Gen Xer and move into a cheap rental.

A second-hand RV would be better.

9) Postscript

We have pulled into the station at Truckee amid a howling blizzard.

My loyal staff have made the ten-mile trek from my estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 50 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just coming into view across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro and iPhone 15 Pro, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above, which should be soon.

Good luck and good trading in 2024!

John Thomas

The Mad Hedge Fund Trader

Global Market Comments

December 11, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or POWELL’S VICTORY LAP),

(GS), (KEY), (WBS), (COLB), (PNFP),

(NLY), (BRK/B), (GOOGL), (CAT), (TLT)

With almost all economic data now universally slowing, Fed Governor Jay Powell is limbering up to take his victory lap. That’s put inflation in full retreat and well on its way to our central bank’s 2% target by summer. Interest rate cuts are just a matter of time.

That sets up a fabulous year in 2024. While this year was mostly a hard slog, next year should be a piece of cake. I can’t wait until it starts!

That puts my 4,800 target for the end of 2023 well within range. People told me I was crazy when I made such an outlandish forecast last January 1, yet here we are.

Investors missed the mark by a mile this year because they thought the Fed's extreme moves in interest rates would trigger a recession.

It didn’t.

Those who bet on falling inflation this year were big winners. That gave the Fed permission to cancel any further rate rises. Economists were too bearish and the technical picture flipped from bearish to bullish in a heartbeat on October 26.

The kinds of moves you are seeing in the stock market, with banks and industrials turning upward, signal that we are not in a bear market, but the start of a new long-term bull one.

Stocks are looking for at least 15% gains in 2024 with earnings consistently surprising to the upside. Domestics will catch fire in the second half. Inflation will fall further than expected, well into the 2% handle, thanks to hyperaccelerating technology crushing prices.

The Fed has won the war on inflation so there is room for 10-year US Treasury bond yields to hit 3.0% next year, taking mortgage interest rates under 5.0%. That will be a shot of adrenaline for the residential real estate market.

A (SPY) target of 5,500 by the end of 2024 is entirely within reason.

It turns out that when ten-year bond yields are between 4.00% and 5.00%, stocks sport a price-earnings multiple of 20X. That allows S&P 500 earnings to hit $2.65 per share in 2025, up from today’s $2.20.

Financials (JPM), industrials (CAT), energy (XOM), and small caps (IWM) will take over market leadership sometime in 2024. The best market risk reward is here. Financials now trading in the dumps have huge multiple expansion potential.

The $240 billion in cash that left equities in 2023 will have to fight their way back in. That’s why we haven’t seen any substantial pullbacks in share prices since October. Once investors got the cash weightings they were happy with, they could never get back into stocks.

Hedge fund equity weightings are at five-year lows. Small caps have very heavy weightings in regional banks, while large banks have great capital spending plays.

Big techs, the meteoric performers of 2023, will likely take a rest sometime in Q1.

Europe and China took the big hits this year, but we didn’t. If they turn around, it will supercharge our economy….and the stock market.

Which brings me to the subject of bank stocks. Banks have had an atrocious 2023, when their shares were either flat or down big, underperforming the S&P 500 by a massive 30%. However, they are looking pretty darn attractive for 2024.

Banks now offer pretty cheap balance sheets relative to next year’s profit outlook, with many still trading at big discounts to book value. A recovering economy means new capital spending jumps, which is great for big banks. Exposure to high-risk office loans which get so much print from the financial media account for less than 5% of their loan books.

Small banks will put the March crisis behind them by recapitalizing or merging. It turns out that only a handful of banks were badly managed (no downside hedge on (TLT) holdings while they were crashing from $166 to $82!!). The survivors will build market share at higher margins.

Economic recovery also means default rates on loans ebb.

Goldman Sachs (GS) is my top pick, after being taken to the woodshed for a very expensive unwind of their poorly thought-out consumer business this year. Key Corp (KEY) is also looking good on a possible 70% earnings growth.

If you are looking for a pure small bank play, you can buy Webster Financial (WBS) based in Stamford, CT, Columbia Banking (COLB) of Tacoma, WA, or Pinnacle Financial (PNFP) from Nashville, TN.

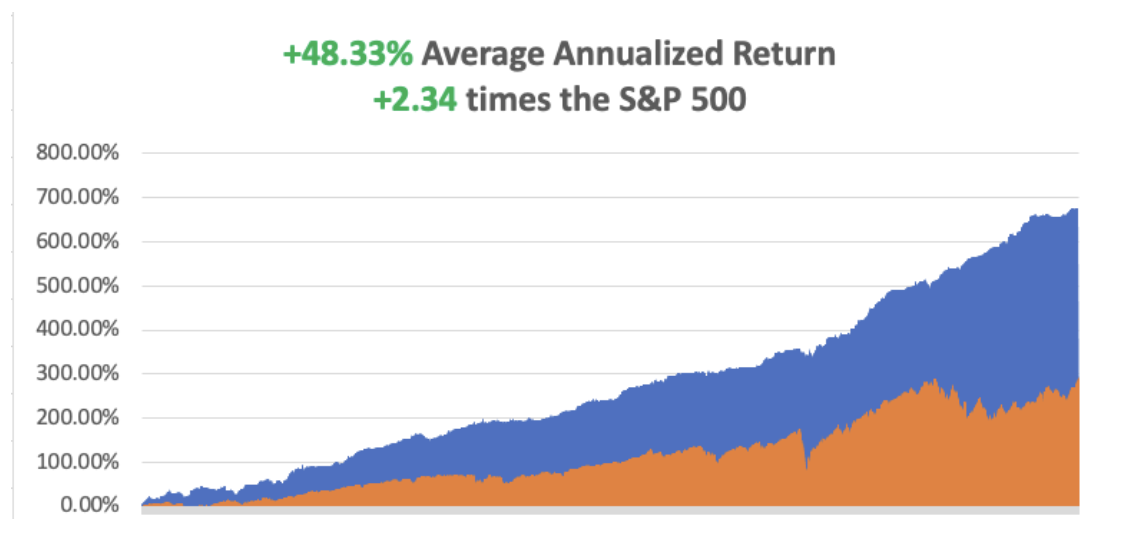

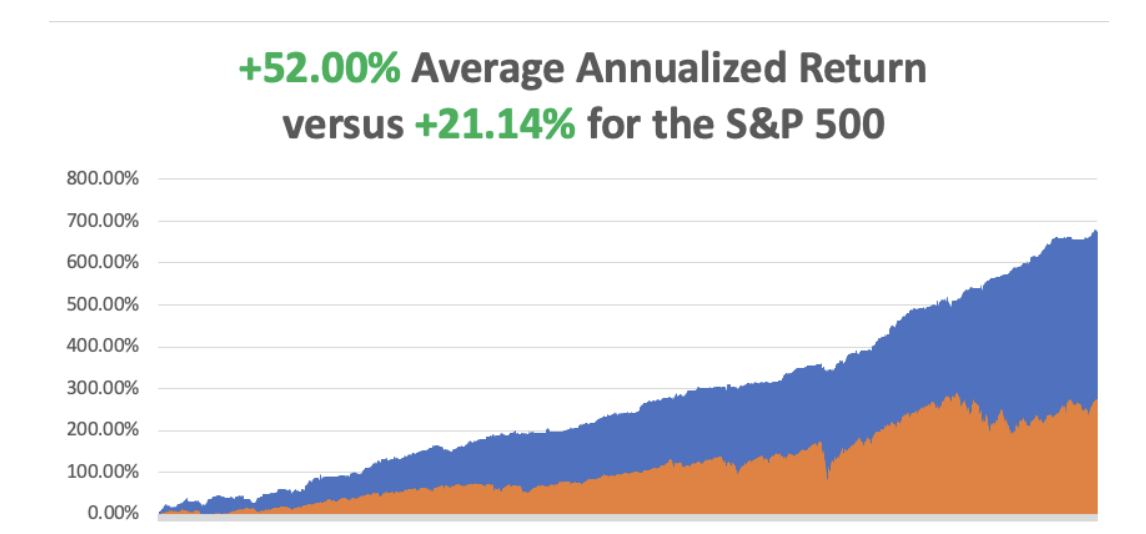

So far in December, we are down -2.85%. We’ve had a heck of a run and the market was bound to bite back sometime. My 2023 year-to-date performance is still at an eye-popping +78.86%. The S&P 500 (SPY) is up +21.05% so far in 2023. My trailing one-year return reached +75.38% versus +24.75% for the S&P 500.

That brings my 15-year total return to +676.05%. My average annualized return has exploded to +52.00%, another new high.

I am 40% invested with 60% in cash, with longs in (NLY), (BRK/B), (GOOGL), and (CAT). Last week, I got stopped out of a long in (XOM), thanks to the oil price dive, and a short in (TLT).

Some 63 of my 70 trades this year have been profitable this year.

Nonfarm Payroll Comes in Soft, in November at 199,000. The headline Unemployment Rate fell to 3.7%, near a 50-year low. Healthcare was the biggest growth industry, adding 77,000. Other big gainers included government (49,000), manufacturing (28,000), and leisure and hospitality (40,000). Average hourly earnings, a key inflation indicator, increased by 0.4% for the month and 4% from a year ago, close to expectations. It was a Goldilocks number for the Fed.

Refi Demand Rockets, as interest rates plunge to four-month lows. The rate for the popular 30-year mortgage fell back toward 7% after hitting 8% earlier this fall. Applications to refinance a home loan index increased 14% from the previous week and were 10% higher than the same week a year ago.

Exploding Sales of EVs Are Ringing the Bell for Oil, leading forecasters to speed up their projections for when global oil use will peak, as public subsidies and improved technology help consumers overcome the sometimes eye-popping sticker prices for battery-powered cars.

Panic Buying Drives Treasury Yields to 4.10%, down nearly a full percentage point in little more than a month on weakening economic data. It’s hard to believe that we drop below 4.10% but anything is possible in this market.

Uber Entered S&P 500, on December 18, taking the stock up 10% on the news. A company needs to fulfill certain criteria to be included in the S&P 500. Firstly, its market capitalization should be at least $14.5 billion. As of Dec 1, 2023, the market capitalization of UBER was $118.02 billion. Additionally, U.S. firms that meet profitability, liquidity, and share-float standards are the ones that can qualify for the S&P 500.

Pending Home Sales Collapse, dropping to the lowest level since the National Association of Realtors began tracking them in 2001. Sales were down 8.5% from October of last year. Tight supply and still-strong demand have kept pressure on home prices, which not only continue to hit new highs but appear to be accelerating in their gains. ales of homes priced above $750,000 have been increasing simply because there is more supply on the high end of the market.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, December 11, at 8:30 AM EST, the Consumer Inflation Expectations are out, one of the Fed’s favorite inflation reads.

On Tuesday, December 12 at 8:30 AM, the Consumer Price Index will be released. The Federal Reserve Open Market Committee starts a two-day meeting.

On Wednesday, December 13 at 2:00 PM, the Federal Reserve will release its interest rate decision. No change is expected. At 2:30, the Producer Price Index is out.

On Thursday, December 14 at 8:30 AM, the Weekly Jobless Claims are announced. We also get Retail Sales.

On Friday, December 15 at 2:30 PM, the October New York Empire State Manufacturing Index is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

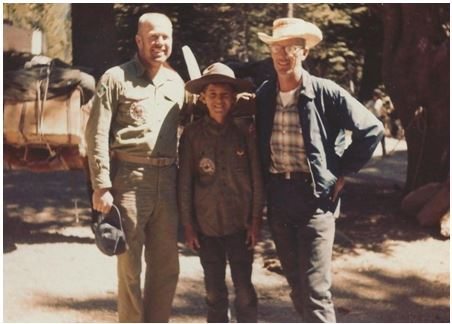

As for me, it was with a heavy heart that I boarded a plane for Los Angeles to attend a funeral for Bob, the former scoutmaster of Boy Scout Troop 108.

The event brought a convocation of ex-scouts from up and down the West Coast and said much about our age.

Bob, 85, called me two weeks ago to tell me his CAT scan had just revealed advanced metastatic lung cancer. I said, “Congratulations Bob, you just made your life span.”

It was our last conversation.

He spent only a week in bed and then was gone. As a samurai warrior might have said, it was a good death. Some thought it was the smoking he quit 20 years ago.

Others speculated that it was his close work with uranium during WWII. I chalked it up to a half-century of breathing the air in Los Angeles.

Bob originally hailed from Bloomfield, New Jersey. After WWII, every East Coast college was jammed with returning vets on the GI bill. So he enrolled in a small, well-regarded engineering school in New Mexico in a remote place called Alamogordo.

His first job after graduation was testing V2 rockets newly captured from the Germans at the White Sands Missile Test Range. He graduated to design ignition systems for atomic bombs. A boom in defense spending during the fifties swept him up to the Greater Los Angeles area.

Scouts I last saw at age 13 or 14 are now 60, while the surviving dads were well into their 80s. Everyone was in great shape, those endless miles lugging heavy packs over High Sierra passes yielding lifetime benefits.

Hybrid cars lined both sides of the street. A tag-along guest called out for a cigarette and a hush came over a crowd numbering over 100.

Some things stuck. It was a real cycle of life weekend. While the elders spoke about blood pressure and golf handicaps, the next generation of scouts played in the backyard or picked lemons off a ripening tree.

Bob was the guy who taught me how to ski, cast rainbow trout in mountain lakes, transmit Morse code, and survive in the wilderness. He used to scrawl schematic diagrams for simple radios and binary computers on a piece of paper, usually built around a single tube or transistor.

I would run off to Radio Shack to buy WWII surplus parts for pennies on the pound and spend long nights attempting to decode impossibly fast Navy ship-to-ship transmissions. He was also the man who pinned an Eagle Scout badge on my uniform in front of beaming parents when I turned 15.

While in the neighborhood, I thought I would drive by the house in which I grew up, once a modest 1,800 square-foot ranch-style home to a happy family of nine. I was horrified to find that it had been torn down, and the majestic maple tree that I planted 40 years ago had been removed.

In its place was a giant, 6,000-square-foot marble and granite monstrosity under construction for a wealthy family from China.

Profits from the enormous China-America trade have been pouring into my hometown from the Middle Kingdom for the last decade, and mine was one of the last houses to go.

When I was class president of the high school here, there were 3,000 white kids and one Chinese. Today, those numbers are reversed. Such is the price of globalization.

I guess you really can’t go home again.

At the family's request, I assisted in liquidating his investment portfolio. Bob had been an avid reader of the Diary of a Mad Hedge Fund Trader since its inception and attended my Los Angeles lunches.

It seems he listened well. There was Apple (AAPL) in all its glory at a cost of $21. I laughed to myself. The master had become the student and the student had become the master.

Like I said, it was a real circle of life weekend.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Scoutmaster Bob

1965 Scout John Thomas

The Mad Hedge Fund Trader at Age 11 in 1963

Global Market Comments

December 4, 2023

Fiat Lux

Featured Trade:

Featured Trade:

(The Mad Hedge December Traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GOLDILOCKS IS BACK!),

(TLT), (FCX), (CAT), (JNK), (HYG), (NLY), (GM), (MSFT), (NLY), (BRK/B), (CCJ), (GOOGL), (SNOW), (XOM), (CRM)

After too long of an absence, Goldilocks has moved back in once again. She arrived with Santa Claus too, a month ahead of schedule.

Can life get any better than that, Goldilocks and Santa Claus?

Santa confused Thanksgiving with Christmas this year. I saw it coming a mile off, and it’s not because my failing eyesight has suddenly improved.

Since October 26, Mad Hedge followers have earned an impressive 25%. We are on track to top an 86.5% profit for 2023, the best in the 15-year history of the service.

Concierge members who own our substantial LEAPS portfolio, now at 33 names, are up much more.

I hate to boast but let me take my victory lap. I earned it.

Stocks and bonds should continue rising but at a much slower rate. More likely is the diversification of the rally from Big Tech and big bonds (TLT) to medium tech, commodities (FCX), industrials (CAT), junk bonds (JNK), (HYG), and REITS (NLY).

Buy everything on dips.

And here are your assumptions. Collapsing energy prices will lead the inflation rate down to the Fed’s well-publicized 2% inflation rate target in the coming months. Accelerating technology and AI will reign in this year’s runaway wage increases, if not reverse them.

The UAW’s 25% salary increase over four years will only hasten the demise of General Motors (GM), as well as their own. Interest rates have to take a swan dive, supercharging all risk assets.

Goldilocks is not moving in for a fling, but a long-term relationship. Your retirement funds will love it.

Last spring, with 75 feet of snow over the winter, the rivers pouring out of the High Sierras were at record levels. That brought the solo hobbyist gold miners out in force.

It is widely believed that the 1849 gold rush extracted only 10% of the gold in the mountains and the remaining 90% is still up there. Heavy rainfalls like we received last winter flushed out some of the rest.

Rounding a turn in the river, I spotted a group of modern-day 49ers equipped with shoulder-high waders and inner tubes floating pumps and sluice boxes. So I parked the car and waded out in the freezing, fast-running water to get an update on this market.

One man proudly showed off a one-ounce gold nugget that he had found only that morning worth about $1,800. Nuggets are worth more than spot gold because they attract a collector’s market.

A record eight-ounce nugget was discovered in a river near Merced the week earlier. This year, the state government in Sacramento issued a record number of gold mining licenses.

I explained to my newfound friend that he should hang on to his gold because it would be worth a lot more the following year. Inflation was falling and that would eventually induce the Federal Reserve to cut interest rates sharply.

That meant less interest rate competition for gold and silver, which yielded nothing taking prices upward. Personally, I think this gold could hit $3,000 an ounce and silver $50 an ounce in 2025.

In addition, there was a constant bid from Russia, China, and North Korea looking to dodge financial sanctions. Money managers are also picking up the yellow metal as a hedge against any unanticipated volatility in 2024.

My friend looked at me quizzically, wondering if perhaps I was some kind of nutjob who had waded out mid-river to rob him of his prized nugget.

I’ll do anything to gain a trading edge, even freezing off my cajones.

It was a tough week for 90- and 100-year-olds with the passing of Charlie Munger, Henry Kissinger, and Supreme Court Justice Sandra Day O’Connor. I had the privilege of knowing all three.

I was in the White House Press Room one day when the press secretary James Brady asked if any of the press could ride a horse. Sheepishly, I was the only one to raise a hand.

I was ordered to pick up my riding boots and report to the White House Stables on 17th Street. I had no idea why. Back then, even the press didn’t ask some questions.

When I arrived, I understood why. Supreme Court Justice Sandra Day O’Connor was already there kitted out ready to ride. It turns out that the justice from Arizona rode weekly with Ronald Reagan. This week, an international crisis prevented the president from doing so. I was the fill-in escort.

We talked about growing up in the Colorado Desert, and pre-air conditioning, as we enjoyed a peaceful ride along the Potomac River. A security detail kept a safe distance.

A lot of history is being in the right place at the right time.

The clock is ticking.

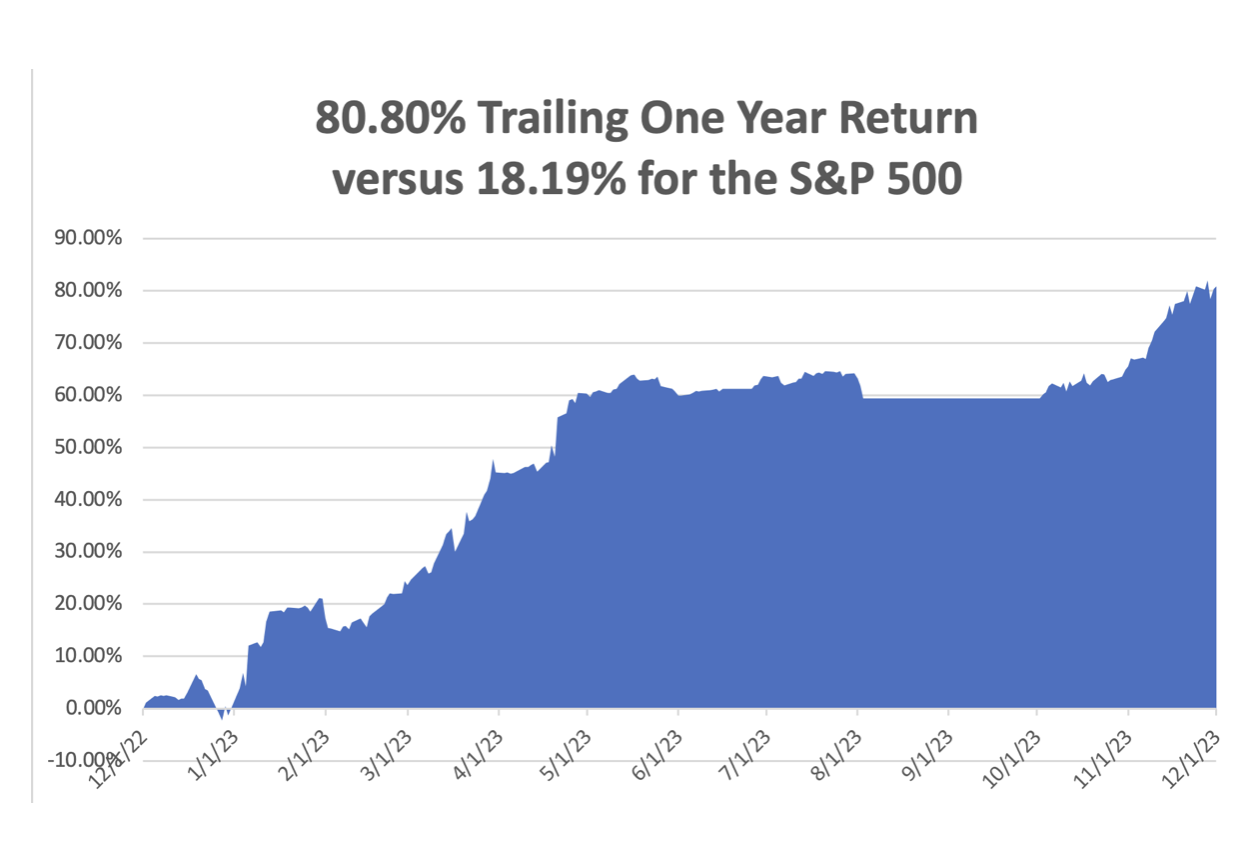

November closed out at +15.54%. My 2023 year-to-date performance is still at an eye-popping +81.71%. The S&P 500 (SPY) is up +19.73% so far in 2023. My trailing one-year return reached +80.80% versus +18.19% for the S&P 500.

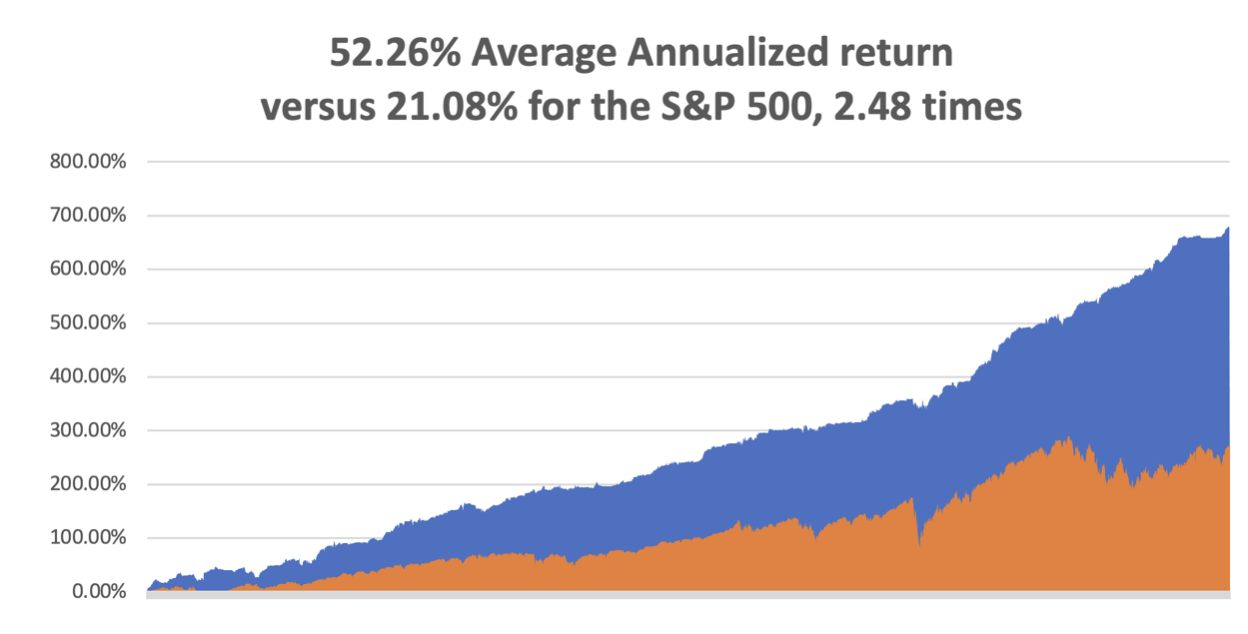

That brings my 15-year total return to +678.90%. My average annualized return has exploded to +52.26%, another new high, some 2.48 times the S&P 500 over the same period.

I am 90% fully invested, with longs in (MSFT), (NLY), (BRK/B), (CCJ), (GOOGL), (SNOW), (CAT), and (XOM). I have one short in the (TLT). I took profits on (CRM) on Friday.

Some 56 of my 61 trades this year have been profitable this year.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, December 4, at 8:30 AM EST, the US Factory Orders are out.

On Tuesday, December 5 at 2:30 PM, the JOLTS Job Openings Report is released.

On Wednesday, December 6 at 8:30 AM, the ADP Private Employment Report is published.

On Thursday, December 7 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, December 8 at 2:00 PM the Baker Hughes Rig Count is printed and at 2:30 PM, the November Nonfarm Payroll Report is published.

As for me, back in the early 1980s, when I was starting up Morgan Stanley’s international equity trading desk, my wife Kyoko was still a driven Japanese career woman.

Taking advantage of her near-perfect English, she landed a prestige job as the head of sales at New York’s Waldorf Astoria Hotel.

Every morning we set off on our different ways, me to Morgan Stanley’s HQ in the old General Motors Building on Avenue of the Americas and 47th street and she to the Waldorf at Park and 34th.

One day, she came home and told me this little old lady living in the Waldorf Towers needed an escort to walk her dog in the evenings once a week. Back in those days, the crime rate in New York was sky-high, and only the brave or the reckless ventured outside after dark.

I said “Sure” “What was her name?”

Jean MacArthur.

I said THE Jean MacArthur?

She answered “Yes.”

Jean MacArthur was the widow of General Douglas MacArthur, the WWII legend. He fought off the Japanese in the Philippines in 1941 and retreated to Australia in a dramatic night PT Boat escape.

He then led a brilliant island-hopping campaign, turning the Japanese at Guadalcanal and New Guinea. My dad was part of that operation, as were the fathers of many of my Australian clients. That led all the way to Tokyo Bay where MacArthur accepted the Japanese in 1945 on the deck of the battleship USS Missouri.

The MacArthur then moved into the Tokyo embassy where the general ran Japan as a personal fiefdom for seven years, a residence I know well. That’s when Jean, who was 18 years the general’s junior, developed a fondness for the Japanese people.

When the Korean War began in 1950, MacArthur took charge. His landing at Inchon Harbor broke the back of the invasion and was one of the most brilliant tactical moves in military history. When MacArthur was recalled by President Truman in 1952, he had not been home for 13 years.

So it was with some trepidation that I was introduced by my wife to Mrs. MacArthur in the lobby of the Waldorf Astoria. On the way out, we passed a large portrait of the general who seemed to disapprovingly stare down at me taking out his wife, so I was on my best behavior.

To some extent, I had spent my entire life preparing for this job.

I had stayed at the MacArthur Suite at the Manila Hotel where they had lived before the war. I knew Australia well. And I had just spent a decade living in Japan. By chance, I had also read the brilliant biography of MacArthur by William Manchester, American Caesar, which had only just come out.

I also competed in karate at the national level in Japan for ten years, which qualified me as a bodyguard. In other words, I was the perfect after-dark escort for Midtown Manhattan in the early eighties.

She insisted I call her “Jean”; she was one of the most gregarious women I have ever run into. She was grey-haired, petite, and made you feel like you were the most important person she had ever run into.

She talked a lot about “Doug” and I learned several personal anecdotes that never made it into the history books.

“Doug” was a staunch conservative who was nominated for president by the Republican party in 1944. But he pushed policies in Japan that would have qualified him as a raging liberal.

It was the Japanese that begged MacArthur to ban the army and the navy in the new constitution for they feared a return of the military after MacArthur left. Women gained the right to vote on the insistence of the English tutor for Emperor Hirohito’s children, an American Quaker woman. He was very pro-union in Japan. He also pushed through land reform that broke up the big estates and handed out land to the small farmers.

It was a vast understatement to say that I got more out of these walks than she did. While making our rounds, we ran into other celebrities who lived in the neighborhood who all knew Jean, such as Henry Kissinger, Ginger Rogers, and the UN Secretary-General.

Morgan Stanley eventually promoted me and transferred me to London to run the trading operations there, so my prolonged free history lesson came to an end.

Jean MacArthur stayed in the public eye and was a frequent commencement speaker at West Point where “Doug” had been a student and later the superintendent. Jean died in 2000 at the age of 101.

I sent a bouquet of lilies to the funeral.

Kyoko passed away in 2002.

In 2014, Chinas Anbang Insurance Group bought the Waldorf Astoria for $1.95 billion, making it the most expensive hotel ever sold. Most of the rooms were converted to condominiums and sold to Chinese looking to hide assets abroad.

The portrait of Douglas MacArthur is gone too. During the Korean War, he threatened to drop atomic bombs on China’s major coastal cities.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader