Global Market Comments

November 19, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(RIVN), (WMT), (BAC), (MS), (GS), (GLD), (SLV), (CRSP), (NVDA),

(BAC), (CAT), (DE), (PTON), (FXI), (TSLA), (CPER), (Z)

Global Market Comments

November 19, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(RIVN), (WMT), (BAC), (MS), (GS), (GLD), (SLV), (CRSP), (NVDA),

(BAC), (CAT), (DE), (PTON), (FXI), (TSLA), (CPER), (Z)

Below please find subscribers’ Q&A for the November 17 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon Valley.

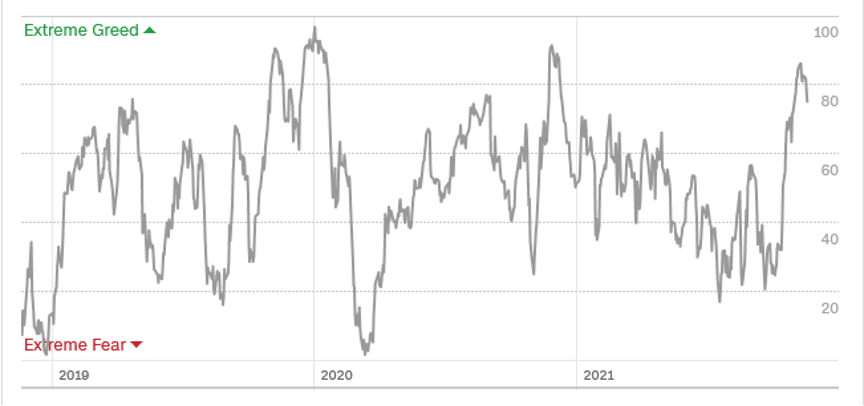

Q: Even though your trading indicator is over 80, do you think that investors should be 100% long stocks using the barbell names?

A: Yes, in a hyper-liquidity type market like we have now, we can spend months in sell territory before the indexes finally rollover. That happened last year and it’s happening now. So, we can chop in this sort of 50-85 range probably well into next year before we get any sell signals. Selling apparently is something you just do anymore; if things go down, you just buy more. It’s basically the Bitcoin strategy these days.

Q: What do you think about Rivian's (RIVN) future?

A: Well, with Amazon behind them, it was guaranteed to be a success. However, we mere mortals won't be able to buy any cars until 2024, and they have yet to prove themselves on mass production. Moreover, the stock is ridiculously expensive—even more than Tesla was in its most expensive days. And it’s not offering any great value, just momentum so I don’t want to chase it right here. I knew it was going to blow up to the upside when the IPO hit because the EV sector is just so hot and EVs are taking over the global economy. I will watch from a distance unless we get a sudden 40% drawdown which used to happen with Tesla all the time in the early days.

Q: Are you worried about another COVID wave?

A: No, because any new virus that appears on the scene is now attacking a population that is 80-90% immune. Most people got immunity through shots, and the last 10% got immunity by getting the disease. So, it’s a much more difficult population for a new virus to infect, which means no more stock market problems resulting from the pandemic.

Q: Is investing in retail or Walmart (WMT) the best way to protect myself from inflation?

A: It’s actually quite a good way because Walmart has unlimited ability to raise prices, which goes straight through to the share price and increases profit margins. Their core blue-collar customers are now getting the biggest wage hikes in their lives, so disposable income is rocketing. And really, overall, the best way to protect yourself from inflation is to own your own home, which 62% of you do, and to own stocks, which 100% of the people in this webinar do. So, you are inflation-protected up the wazoo coming to Mad Hedge Fund Trader. Not to mention we buy inflation plays like banks here.

Q: Why are financials great, like Bank of America (BAC)?

A: Because the more their assets increase in value, the greater the management fees they get to collect. So, it’s a perfect double hockey stick increase in profits.

*Interest rates are rising

*Rising interest rates increase bank profit margins

*A recovering economy means default rates are collapsing

*Thanks to Dodd-Frank, banks are overcapitalized

*Banks shares are cheap relative to other stocks

*The bank sector has underperformed for a decade

*With rates rising value stocks like banks make the perfect rotation play out of technology stocks.

*Cryptocurrencies will create opportunities for the best-run banks.

Q: Do you think the market is in a state of irrational exuberance?

A: Yes. Warning: irrational exuberance could last for 5 years. That’s what happened when Alan Greenspan, the Fed governor in 1996, coined that phrase and tech stocks went straight up all the way up until 2000. We made fortunes off of it because what happens with irrational exuberance is that it becomes more irrational, and we’re seeing that today with a lot of these overdone stock prices.

Q: Should I hold cash or bonds if you had to choose one?

A: Cash. Bonds have a terrible risk/reward right now. You’re getting like a 1% coupon in the face of inflation that's at 6.2%. It’s like the worst mismatch in history. In fact, we made $8 points on our bond shorts just in the last week. So just keep selling those rallies, never own any bonds at all—I don’t care what your financial advisor tells you, these are worthless pieces of paper that are about to become certificates of confiscation like they did back in the 80s when we had high inflation.

Q: What’s your yearend target for Nvidia (NVDA)?

A: Up. It’s one of the best companies in the world. It’s the next trillion dollar company, but as for the exact day and time of when it hits these upside targets, I have no idea. We’ve been recommending Nvidia since it was $50, and it’s now approaching $400. So that’s another mad hedge 20 bagger setting up.

Q: What about CRISPR Therapeutics (CRSP)?

A: The call spread is looking like a complete write-off; we missed the chance to sell it at $170, it’s now at $88. So, I’m just going to write that one-off. Next time a biotech of mine has a giant one-day spike, I am selling. What you might do though with Crisper is convert your call spread to straight outright calls; that increases your delta on the position from 10% to 40% so that way you only need to get a $20 move up in the stock price and you’ll get a break-even point on your long position. So, convert the spreads to longs—that’s a good way of getting out of failed spreads. You do not need a downside hedge anymore, and you’ll find those deep out of the money calls for pennies on the dollar. That is the smart thing to do, however, you have to put money into the position if you’re going to do that.

Q: Would you buy a LEAP in Tesla (TSLA) at this time?

A: No, it’s starting a multi-month topping out process, then it goes to sleep for 5 months. After it’s been asleep for 5 months then I go back and look at LEAPS. Remember, we had a 45% drawdown last year. I bet we get that again next year.

Q: Will inflation subside?

A: Probably in a year or so. A lot depends on how quickly we can break up the log jam at the ports, and how this infrastructure spending plays out. But if we do end the pandemic, a lot of people who were afraid of working because of the virus (that’s 5 or 10 million people) will come back and that will end at least wage inflation.

Q: When is the next Mad Hedge Fund Trader Summit?

A: December 7, 8, and 9; and we have 27 speakers lined up for you. We’ll start emailing probably next week about that.

Q: Are gold (GLD) and silver (SLV) getting close to a buy?

A: Maybe, unless Bitcoin comes and steals their thunder again. It has been the worst-performing asset this year. The only gold I have now is in my teeth.

Q: Morgan Stanley (MS) is tanking today, should I dump the call spread?

A: I’m going to see if we hold here and can close above our maximum strike price of $98 on Friday. But all of the financials are weak today, it’s nothing specific to Morgan Stanley. Let’s see if we get another bounce back to expiration.

Q: Where can I view all the current positions?

A: We have all of our positions in the trade alert service in your account file, and you should find a spreadsheet with all the current positions marked to market every day.

Q: What is the barbell strategy?

A: Half your money is in big tech and the other half is in financials and other domestic recovery plays. That way you always have something that’s going up.

Q: Is Elon Musk selling everything to avoid taxes from Nancy Pelosi?

A: Actually, he’s selling everything to avoid taxes from California governor Gavin Newsom—it’s the California taxes that he has to pay the bill on, and that’s why he has moved to Texas. As far as I know, you have to pay taxes no matter who is president.

Q: Will the price of oil hit $100?

A: I doubt it. How high can it go before it returns to zero?

Q: Is it time to buy a Caterpillar (CAT) LEAP?

A: We’re getting very close because guess what? We just got another $1.2 billion to spend on infrastructure. Not a single job happens here without a Caterpillar tractor or a tractor from Komatsu for John Deere (DE).

Q: Will small caps do well in 2022?

A: Yes, this is the point in the economic cycle where small caps start to outperform big caps. So, I'd be buying the iShares Russell 2000 ETF (IWM) on dips. That's because smaller, more leveraged companies do better in healthy economies than large ones.

Q: Is it too late to buy coal?

A: Yes, it’s up 10 times. The next big move for coal is going to be down.

Q: Peloton (PTON) is down 300%; should I buy here?

A: Turns out it’s just a clothes rack, after all, it isn't a software company. I didn’t like the Peloton story from the start—of course, I go outside and hike on real mountains rather than on machines, so I’m biased—but it has “busted story” written all over it, so don’t touch Peloton.

Q: Will spiking gasoline prices cause US local governments to finally invest in Subways and Trams like European cities, or is this something that will never happen?

A: This will never happen, except in green states like New York and California. A lot of the big transit systems were built when labor was 10 cents a day by poor Irish and Italian immigrants—those could never be built again, these massive 100-mile subway systems through solid rock. So if you want to ride decent public transportation, go to Europe. Unfortunately, that’s the path the United States never took, and to change that now would be incredibly expensive and time-consuming. They’re talking about building a second BART tunnel under the bay bridge; that’s a $20 billion, 20-year job, these are huge projects. And for the last five years, we’ve had no infrastructure spending at all, just lots of talk.

Q: Would Tesla (TSLA) remains stable if something happened to Elon Musk?

A: Probably not; that would be a nice opportunity for another 45% correction. But if that happened, it would also be a great opportunity for another Tesla LEAPS. My long-term target for the stock is $10,000. Elon actually spends almost no time with Tesla now, it’s basically on autopilot. All his time is going into SpaceX now, which he has a lot more fun with, and which is actually still a private company, so he isn’t restricted with comments about space like he is with comments about Tesla. When you're the richest man in the world you pretty much get to do anything you want as long as you're not subject to regulation by the SEC.

Q: How realistic is it that holiday gatherings will trigger a huge wave of COVID in the United States forcing another lockdown and the Fed to delay a rise in interest rates?

A: I would say there’s a 0% chance of that happening. As I explained earlier, with 90% immunity in much of the country, viruses have a much harder time attacking the population with a new variant. The pandemic is in the process of leaving the stock market, and all I can say is good riddance.

Q: What about the Biden meeting with President Xi and Chinese stocks (FXI)?

A: It’s actually a very positive development; this could be the beginning of the end of the cold war with China and China’s war on capitalism. If that’s true, Chinese stocks are the bargain of the century. However, we’ve had several false green lights already this year, and with stuff like Microsoft (MSFT) rocketing the way it is, I’d rather go for the low-risk high-return trades over the high-risk, high return trades.

Q: What’s your opinion of Zillow (Z)?

A: I actually kind of like it long term, despite their recent disaster and exit from the home-flipping business.

Q: Do you like copper (CPER) for the long term?

A: Yes, because every electric car needs 200 lbs. of copper, and if you’re going from a million units a year to 25 million units a year, that’s a heck of a lot of copper—like three times the total world production right now.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

An Old Fashioned Peloton (a Mountain)

Global Market Comments

September 30, 2021

Fiat Lux

Featured Trade:

(WHAT TO BUY AT MARKET TOPS?),

(CAT), ($COPPER), (FCX), (BHP), (RIO),

(EUROPEAN STYLE HOMELAND SECURITY),

(TESTIMONIAL)

I will start today’s letter by listing six more data points showing how overbought stocks have become.

1) While the number of outstanding shares in the US has remained unchanged since 2006, thanks to M&A, buybacks, bankruptcies, and privatizations, the average weighted share price has more than doubled from $50.15 to $137.00.

2) The Volatility Index (VIX) has just jumped from a recent high of $29 to $21 today.

3) The Mad Hedge Market Timing Index has just soared from a recent low of 19 eight months ago to 30 today, still in “BUY” territory.

4) 2022 forward stock earnings growth maintains at 20%.

5) Almost every investor is bullish once more, now that their stocks are going up.

6) The stock market has had its best 18 months in history. Grizzled, long in the tooth readers can’t be more cautious right now.

This all leads to the urgent question of the day, WHICH stocks do you buy as we approach market tops? The answer is very simple. You buy cheap ones. And what are the cheapest stocks out there?

Commodity stocks.

My friend, Jim Umpleby, said that we are just entering a ten-year super cycle in commodities.

Jim should know. He is the CEO of Caterpillar (CAT), a company I have been following for 45 years. I even have one of their cool worn yellow baseball caps from years past.

Thanks to the 2017 tax bill, companies can now buy Caterpillar’s bulldozers, backhoes, and heavy trucks, and expense 100% of the investment in the first year. (Last year, I bought a new $162,500 Tesla Model X using the same break). That makes a purchase of (CAT)’s products one of the best tax breaks ever.

Needless to say, this has created a stampede to buy the companies heavy machinery because they fear this tax windfall will be reversed by the next administration. This is equipment with a 30-year life or longer.

Industrial commodities are in fact the perfect sector to buy right now. Take a look at the long-term chart for copper prices, which are a great bellwether for the entire industry. They are imminently poised to make a long-term upside breakout.

Copper last peaked at the beginning of 2011, when the Chinese infrastructure build-out suddenly outdrew to a juddering halt. Prices cratered from $4.60 a pound to a lowly $1.90. Mines were sold off, mothballed, or permanently closed at a record rate.

Copper prices fell so low that the US Mint finally started making a profit on pennies they struck.

Then a funny thing happened.

Copper will soon bottom, assisted by the global synchronized economic recovery I have been writing about for years. The recent collapse of the Chinese real estate market prompted by the China Evergrande Group will eventually give us a great entry point.

The share prices of copper and other major commodity producers will go ballistic. Freeport McMoRan (FCX), the world’s largest copper producer, (whose management is a long-time reader of this letter) has just seen its stock jump ten-fold from a near $4.00 a share to $46.00. It is now back at $33.00.

You may think that it’s too late to get into the commodities space, but you’d be wrong. Having covered the sector for nearly a half-century there is one thing you learn quickly. While you can shut down a mine in weeks, it can take years to bring them back on line.

As for developing a new mine from scratch, that can take a decade by the time you get design, permits, infrastructure, equipment, and labor in place.

My Australian readers tell me that (BHP) is flying young skilled workers from Brisbane an incredible 2,000 miles to work in Northwest mines in a six weeks on - six weeks off work schedule and paying them $200,000 a year to do it. And they’re making a profit doing this!

The bottom line here is that a short squeeze has developed for industrial commodities which will last for years.

Oh, and that global economic recovery? It is on vacation until delta ends. That could happen in a few months, and no more than a year.

At least you have something to buy now besides more technology stocks. As much as we here at the Mad Hedge Fund Trader all love them for the long term, they are extremely overbought for the short term.

Tech always comes back.

Global Market Comments

July 29, 2021

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (RSX), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL)

Global Market Comments

June 18, 2021

Fiat Lux

Featured Trade:

(JUNE 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(MS), (XOM), (FXI), (MSFT), (AMZN), (FB), (GOOGL), FCX), (CAT),

(GLD), (DIS), (GME), (AMC), (UBER), (LYFT), (TLT), (VIX)

Below please find subscribers’ Q&A for the June 16 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Lake Tahoe, NV.

Q: Does Copper (FCX) look like a buy now or wait for it to drop?

A: I would buy ⅓ now, ⅓ lower down, ⅓ lower down still. Worst case we get down to $30 in Freeport McMoRan (FCX) from $37 today. A new internal combustion engine requires 40 lbs. of copper for wiring, but new EVs require 200 lbs. per car, and the number of EV cars is about to go from 700,000 last year to 25 million in 10 years. So, you can do the math here. It's basically 24.3 million times 200 lbs., or 1.215 billion tons, and that's the annual increase in demand for copper over the next 10 years. There aren’t enough mines in the world to accommodate that, so the price has to go up. However, (FCX) has gone up 12 times from its 2020 low and was overdue for a major rest. So short term it's a sell, long term it's a double. That's why I put the LEAPS out on it.

Q: Lumber prices are dropping fast, should I bet the ranch that it’ll drop big?

A: No, I think the big drop has happened; we’re down 40% from the highs, the next move is probably up. And that is a commodity that will remain more or less permanently in short supply due to the structural impediments put into the lumber market by the Trump administration. They greatly increased import duties from Canada and all those Canadian mills shut down as a result. It’s going to take a long time to bring those back up to speed and get us the wood we need to build houses. Another interesting thing you’re seeing in the bay area for housing is people switching over to aluminum and steel for framing because it’s cheaper, and of course in an earthquake-prone fire zone, you’d much rather have steel or aluminum for framing than wood.

Q: I didn’t catch the (FCX) LEAP, can you reiterate?

A: With prices at today's level, you can buy the 35 calls in (FCX), sell short the 40 calls, and get nearly a 177% return by January 2022. That's an absolute screamer of a LEAPS.

Q: How do you see the working from home environment in the near future after Morgan Stanley (MS) asked everyone to return?

A: Well that’s just Morgan Stanley and that’s in New York. They have their own unique reasons to be in New York, mostly so they can meet and shake down all their customers in Manhattan—no offense to Morgan Stanley, but I used to work there. For the rest of the country, those in remote places already, a lot of companies prefer that people keep working from home because they are happier, more productive, and it’s cheaper. Who can beat that? That’s why a lot of these productivity gains from the pandemic are permanent.

Q: Is there a recording of the previous webinar?

A: Yes, all of the webinars for the last 13 years are on the website and can be accessed through your account.

Q: What makes Microsoft (MSFT) a perfect-looking chart?

A: Constant higher lows and higher highs. They also have a fabulous business which is trading relatively cheaply to the rest of tech and the rest of the main market. Of course, they were a huge pandemic winner with all the people rushing out to buy PCs and using Microsoft operating software. I expect those gains to improve. The new game now is the “wide moat” strategy, which is buying companies that have near monopolies and can’t be assailed by other companies trying to break into their businesses. The wide moat businesses are of course Microsoft (MSFT), Amazon (AMZN), Facebook (FB) and Alphabet (GOOGL). That's the new investment philosophy; that's why money has been pouring back into the FANGs for a month now.

Q: Do you have any concerns about Facebook’s (FB) advertising ability, given the recent reduction of tracking capabilities of IOS 4.5 users?

A: Well first of all, IOS 4.5 users, the Apple operating system, are only 15% of the market in desktops and 24% of mobile phones. Second, every time one of these roadblocks appears, Facebook finds a way around it, and they end up taking in even more advertising revenue. That’s been the 15-year trend and I'm sticking to it.

Q: Is Caterpillar (CAT) a LEAP candidate right now?

A: Not yet, but we’re getting there. Like many of these domestic recovery plays, it is up 200% from the March lows where we recommended it. The best time to do LEAPS is after these big capitulation selloffs, and all we’ve really seen in most sectors this year is a slow grind down because there's just too much money sitting under the market trying to get into these stocks. Let’s see if (CAT) drops to the 50-day moving average at $185 and then ask me again.

Q: If you have the (FCX) LEAPS, should you keep them?

A: I would keep them since I'm looking for the stock to double from here over the next year. If you have the existing $45-$50 LEAPS, I would expect that to expire at its max profit point in January. But you may need to take a little pain in the interim until it turns.

Q: Should I bet the ranch on meme stocks like (AMC) and GameStop GME)?

A: Absolutely not, I’m amazed you haven't lost everything already.

Q: Do you think Exxon-Mobile (XOM) could rise 30% from here?

A: Yes, if we get a 30% rise in oil. We are in a medium-term countertrend rally in oil which will eventually burn out and take us to new lows. Trade against the trend at your own peril.

Q: Disneyland (DIS) in Paris is set to open. Is Disneyland a buy here?

A: Yes, we’re getting simultaneous openings of Disneyland’s worldwide. I’ve been to all of them. So yes, that will be a huge shot in the arm. Their streaming business is also going from strength to strength.

Q: How long will the China (FXI) slowdown last?

A: Not long, the slowdown now is a reaction to the superheated growth they had last year once their epidemic ended. We should get normalized growth in China at around 6% a year, and I expect China to rally once that happens.

Q: Have you changed your outlook on inflation, real or imagined?

A: I don’t think we’re going to have inflation; I buy the Fed's argument that any hot inflation numbers are temporary because we’re coming off of a one-on-one comparisons from when the economy was closed and the prices of many things went to zero. If you look at that inflation number, it had trouble written all over it. Some one third of the increase was from rental cars. One of the hottest components was used cars. You’re not going to get 100% year on year increases next year in rental or used cars.

Q: When you issue a trade alert, it’s always in the form of a call spread like the Microsoft (MSFT) $340-$370 vertical bull call spread. What are the pros and cons of doing this trade on the put side, like shorting a vertical bear put spread?

A: It’s six of one, half a dozen of the other. There are algorithms that arbitrage between the two positions that make sure that they’re never out of line by more than a few cents. I put out call spreads because they’re easier for beginners to understand. People get buying something and watching it go up. They don’t get borrowing something, selling it short, and buying it back cheaper.

Q: Will gold (GLD) prices go up?

A: Yes, when inflation goes up for real.

Q: What is the future of the gig economy? How will that affect Uber (UBER) and Lyft (LYFT)?

A: I like both, because they just got a big exemption from California on part time workers, and that is very positive for their business models.

Q: Do you think the government doesn’t want to cancel student debt because it will unleash inflation?

A: It’s the exact opposite. The government wants to forgive student debt because it will unleash inflation. If you add 10 million new consumers to the economy, that is very positive. As long as former students have tons of debt, horrible credit ratings, and are unable to buy homes or get credit cards, they are shut out of the economy. They can’t participate in the main economy by buying homes, shopping, or getting credit. The fact that the US has so many college grads is why businesses succeed here and fail in every other country. That should be encouraged.

Q: Where is the United States US Treasury Bond Fund (TLT) headed?

A: Short term up, long term down.

Q: Options premiums are not melting away much today; I hope they start decaying after the Fed announcement.

A: In these elevated volatility periods—believe it or not, the (VIX) is still elevated compared to its historic levels—they hang on all the way to the very last day, before expiration, before they really melt the time value on options. It really does pay to run these into expiration now. When the VIX was down at like $9-$10, that was not the case.

Q: I bought a short term expiration going long the (TLT) to hedge my position; was this smart?

A: Yes, but only if you are a professional short-term trader. If you are in front of your screen all day and are able to catch these short term moves in (TLT), that is smart. My experience is that most individual investors don’t have the experience to do that, don’t want to sit in front of a screen all day, and would rather be playing golf. Such hedging strategies end up costing them money. Also, remember that half of the moves these days are at the opening; they’re overnight gap openings and you can’t catch that intraday trading—it’s not possible. So over time, the people who take the most risk make the most money. And that means the people who don’t hedge make the most money. But you have to be able to take the pain to do that. So that’s my philosophy talk on risk taking.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trade

Global Market Comments

December 16, 2020

Fiat Lux

FEATURED TRADE:

(WHAT TO BUY AT MARKET TOPS?),

(CAT), ($COPPER), (FCX), (BHP), (RIO),

(EUROPEAN STYLE HOMELAND SECURITY),

(TESTIMONIAL)

I will start today’s letter by listing six more data points showing how overbought stocks have become.

1) While the number of outstanding shares in the US has remained unchanged since 2006, thanks to M&A, buybacks, bankruptcies, and privatizations, the average weighted share price has more than doubled from $50.15 to $137.00.

2) The Volatility Index (VIX) has just collapsed from a high of $41 in November to $20 today.

3) The Mad Hedge Market Timing Index has just soared from a record low of 2 eight months ago to 76 today, deep into “SELL” territory.

4) 2000 forward stock earnings growth has collapsed from 26% a year ago, to 0% in a few months.

5) Almost every investor now bullish once more, now that their stocks are going up.

6) The stock market has had its best month since 1987. Grizzled, long in the tooth readers can’t be more cautious right now.

This all leads to the urgent question of the day, WHICH stocks do you buy as we approach market tops? The answer is very simple. You buy cheap ones. And what are the cheapest stocks out there?

Commodity stocks.

My friend, Jim Umpleby, said that we are just entering a ten-year super cycle in commodities.

Jim should know. He is the CEO of Caterpillar (CAT), a company I have been following for 45 years. I even have one of their cool worn yellow baseball caps from years past.

Thanks to the 2017 tax bill, companies can now buy Caterpillar’s bulldozers, backhoes, and heavy trucks, and expense 100% of the investment in the first year. (Last year, I bought a new $162,500 Tesla Model X using the same break). That makes a purchase of (CAT)’s products one of the best tax breaks ever.

Needless to say, this has created a stampede to buy the companies heavy machinery because they fear this tax windfall will be reversed by the next administration. This is equipment with a 30-year life or longer.

Industrial commodities are in fact the perfect sector to buy right now. Take a look at the long-term chart for copper prices, which are a great bellwether for the entire industry. They are imminently poised to make a long-term upside breakout.

Copper last peaked at the beginning of 2011, when the Chinese infrastructure build-out suddenly outdrew to a juddering halt. Prices cratered from $4.60 a pound to a lowly $1.90. Mines were sold off, mothballed, or permanently closed at a record rate.

Copper prices fell so low that the US Mint finally started making a profit on pennies they struck.

Then a funny thing happened.

Copper bottomed, assisted by the global synchronized economic recovery I have been writing about for years. Then at the beginning of this year, investors smelled a recovery in a severely oversold, bargain basement, lagging sector. Copper prices jumped from $2.60 to $3.6, up 42% since June.

The share prices of copper and other major commodity producers went ballistic. Freeport McMoRan (FCX), the world’s largest copper producer, (whose management is a long-time reader of this letter) has just seen its stock jump six-fold from a near $4.00 a share to $24.00. If this sounds rich, recall that the peak during the last cycle was at $51.

Other big commodity producers did as well. Australia’s BHP Billiton (BHP) leaped 41% in a month!

You may think that it’s too late to get into the commodities space, but you’d be wrong. Having covered the sector for nearly a half-century there is one thing you learn quickly. While you can shut down a mine in weeks, it can take years to bring them back on line.

As for developing a new mine from scratch, that can take a decade by the time you get the design, permits, infrastructure, equipment, and labor in place.

My Australian readers tell me that (BHP) is flying young skilled workers from Brisbane an incredible 2,000 miles to work in Northwest mines in a six week on, six week off work schedule and paying them $200,000 a year to do it. And they’re making a profit doing this!

The bottom line here is that a short squeeze has developed for industrial commodities which will last for years.

Oh, and that global economic recovery? It is on vacation until the pandemic ends. That could happen in a few months, and no more than a year.

At least you have something to buy now besides more technology stocks. As much as we here at the Mad Hedge Fund Trader all love them for the long term, they are extremely overbought for the short term. Up 50% in a month? I’ll pass.

Global Market Comments

December 15, 2020

Fiat Lux

FEATURED TRADE:

(A NOTE ON OPTIONS CALLED AWAY),

(TSLA), (TLT), (BABA), (JPM), (CAT)