Global Market Comments

September 27, 2018 Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (RSX), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL), (TUESDAY, OCTOBER 16, 2018, MIAMI, FL,

GLOBAL STRATEGY LUNCHEON)

This morning, U.S. Treasury Secretary Steven Mnuchin mentioned that an effort was being made to get trade talks with China back on track. The Dow soared 160 points in a heartbeat.

Past murmurings by the Treasury Secretary demonstrate that his musings have zero credibility in the marketplace and the move vaporized in minutes. However, given the extreme moves made by the shares of trade war victims, I think it is time to review my “Trade Peace” portfolio and make some additions.

The shares have been so beaten up that I think you can start scaling in now with limited downside and a ton of potential upside.

It’s not a matter of if, but when Trump has to run up the white flag with his wildly unpopular trade wars. As they now stand the new tariffs are threatening to chop $10 off of S&P 500 earnings in 2018, from $168 down to $158, according to J.P. Morgan. Some two-thirds of all U.S. companies have been negatively impacted.

Tariffs have effectively wiped out the benefits of the corporate tax cuts for most companies enacted last December. Who has been the worst hit? Thousands of small manufacturers in Midwest red states that can’t function because they are missing crucial cheap parts they can only obtain from the Middle Kingdom.

At last count there are a staggering 37,000 applications for exemptions from tariffs filed with the U.S. Treasury and only a dozen people to process them. A mere 10% have been granted. It is a giant bureaucratic nightmare.

With the midterm elections now only 37 trading days away, the clock is ticking. If Trump doesn’t cut trade deals with all of our major counterparties around the world before then, the Republican Party stands to lose both the House of Representatives and the Senate on November 6. That will make Trump a “lame duck” president for two more years.

China Technology Stocks – Includes Alibaba (BABA), Baidu (BIDU), and Tencent (TCTZF). It’s not often that you get to buy a company with 61% sales growth, which has seen its shares plunge by 27% in three months, as is the case with (BABA). Just to get (BABA) back up to its June level it has to rise by 37%. This is a stock that will easily double or triple over the long term.

U.S. Semiconductor Stocks – With China buying 80% of its chips from the U.S., stocks such as Micron Technology (MU), Lam Research (LRCX), and KLA-Tencor (KLAC) have been taken out to the woodshed and beaten senseless. Micron is off a withering 41% since the trade war began in earnest in May.

Emerging Markets – China is the largest trading partner for most of the world, and a recession there sparks a global contagion effect. Reverse that, and you stimulate not only emerging markets, but the U.S. economy, too. Look at the charts for the iShares MSCI Emerging Markets ETF (EEM), the iShares China Large-Cap ETF (FXI), and the iShares MSCI Brazil ETF (EWZ) and you will salivate.

Oil – Boost the global economy and oil demand (USO) also. China is the world’s largest incremental buyer of new oil, and it will absorb all of the Iranian crude freed up by the U.S. abrogation of the treaty there.

Agricultural – No sector has been punished more than agriculture, where profit margins are small, lead times stretch into years, and mother nature plays her heavy hand. In this area you can include soybeans (SOYB), corn (CORN), and wheat (WEAT), as well as equipment makers Caterpillar (CAT) and Deere (DE).

Some 20 years of development efforts in China by American farmers have gone down the toilet, and much of this business is never coming back. Trust and reliability are gone for good. Storage silos across the country are full. Did I mention that red states are taking far and away the biggest hit? There are not a lot of soybeans grown in California, New York, or New Jersey.

Even if Trump digs in and refuses to admit defeat, as is his way, there is still a light at the end of the tunnel. Sometime in 2019, the World Trade Organization will declare virtually all of the new American tariffs illegal and hit the U.S. with its own countervailing duties. This is the Chinese strategy. Waiting for them to fold could be a long wait, a very long wait.

Featured Trade:

(LAST CHANCE TO ATTEND THE FRIDAY, AUGUST 3, 2018,

AMSTERDAM, THE NETHERLANDS GLOBAL STRATEGY DINNER), (STOCKS TO BUY ON THE OUTBREAK OF TRADE PEACE),

(QQQ), (SPY), (SOYB), (CORN), (WEAT), (CAT),

(DE), (BA), (QCOM), (MU), (LRCX), (CRUS),

(ORIENT EXPRESS PART II, or REPORT FROM VENICE)

So, how will the trade war end? It could be the crucial trading call of 2018.

"That which can't continue, won't," I paraphrase the noted economist Herbert Stein. I think that logic neatly applies to our global trade wars today.

In 1970, some 25% of world GDP was accounted for by international trade. Today it is 52%. Germany has been the powerhouse, with trade growing from 25% to 80%, largely through exploding auto exports. Trade growth in the U.K. has been pitiful as the old colonial ties loosened, improving only from 40% of GDP to 52%.

In the U.S., trade has grown from 10% to 25% of GDP during this time. It is far lower than the rest of the G7 nations because of the massive size of its domestic economy.

Still, placing restraints on 25% of U.S. GDP, or about $5 trillion, is quite a big hit. Think an imminent recession, quite possible a severe one. The $13 billion in subsidies offered the agriculture sector is but a drop in the bucket. It would be like killing off the goose that laid the golden egg.

Trump has a weak hand, which is growing weaker by the day. It is just a matter of time before he folds. Not to do so would entirely wipe out the benefits of the December tax package, yet still leave the U.S. government with $2 trillion in new debt. It is a perfect money destruction machine.

My bet is that Trump will claim victory at some point soon, regardless of what transpires on the negotiation front. Take the trade war away, and stocks will immediately jump 10%. That's what the stock market thinks, with NASDAQ (QQQ) at an all-time high, and the S&P 500 (SPY) just short of one. Stocks are trading over the medium term as if Donald Trump doesn't exist.

Which stocks should you buy when trade peace breaks out? Buy those that have suffered the most. The ags have to be at the top of your list, such as Soybeans (SOYB), Corn (CORN), and Wheat (WEAT), the worst hit. The old industrials such as Caterpillar (CAT), John Deere (DE), and Boeing (BA) also have to be a priority.

In the technology area you have to rotate out of the FANGs and into chip stocks, the worst performers of the sector this year. Perhaps this is what the market is shouting at us with the horrific one-day decline in Facebook (FB) yesterday. China relies on the U.S. for 80% of its chips and all of its high-end graphics cards.

China's canceling of the QUALCOM (QCOM) takeover of its NXP Semiconductors shows to what extent it is willing to retaliate in the tech area. Chip stocks to buy for the rebound should include Micron Technology (MU), Cirrus Logic (CRUS), and Lam Research (LRCX).

Even if the trade war ends tomorrow, business conditions will never be the same. Confidence in American reliability will never completely recover. Sure, Trump will be gone in 2 1/2 years. But what if he is replaced by someone worse? Trading with the United States now incurs a level of political risk not seen since the War of 1812, when Washington burned.

But no trade war is certainly better than a trade war if you are a trader or investor.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-07-27 01:07:102018-07-27 01:07:10Stocks to Buy on the Outbreak of Trade Peace

Apparently, nobody told Netflix (NFLX) that we are smack dab in a tit-for-tat trade war between two of the greatest economic powers to grace mankind.

No matter rain or shine, Netflix keeps powering on to new highs.

The Mad Hedge Technology Letter first recommended this stock on April 23, 2018, when I published the story "How Netflix Can Double Again," (click here for the link) and at that time, shares were hovering at $334.

Since, then it's off to the races, clocking in at more than $413 as of today, a sweet 19% uptick since my recommendation.

It seems the harder I try, the luckier I get.

What separates the fool's gold from the real yellow bullion are challenging market days like yesterday.

The administration announced a new set of tariffs on $200 billion worth of Chinese imports.

The day began early on the Shanghai exchange dropping a cringeworthy 3.8%.

The Hong Kong Hang Seng Market didn't fare much better cratering 2.78%.

Investors were waiting for the sky to drop when the minutes counted down to the open in New York and futures were down big premarket.

Just as expected, the Dow Jones Index plummeted on the open, and in a flash the Dow was down 410 points intraday.

The risk off appetite toyed with traders' nerves and American companies with substantial China exposure being rocked the hardest such as Caterpillar (CAT).

After the Dow hit an intraday low, a funny thing happened.

The truth revealed itself and U.S. equities reacted in a way that epitomizes the nine-year bull market.

Tar and feather a stock as much as you want and if the stock keeps going up, it's a keeper.

Not only a keeper, but an undisputable bullish signal to keep you from developing sleep apnea.

In the eye of the storm, Netflix closed the day up a breathtaking 3.73%. The overspill of momentum continued with Netflix up another 2% and change today.

This company is the stuff of legends and reasons to buy them are legion.

As subscriber surveys flow onto analysts' desks, Netflix is the recipient of a cascade of upgrades from sell side analysts scurrying to raise targets.

Analysts cannot raise their targets fast enough as Netflix's price action goes from strength to hyper-strength.

Chip stocks have the opposite problem when surveys, portraying an inaccurate picture of the 30,000-foot view, prod analysts to downgrade the whole sector.

That is why they are analysts, and most financial analysts these days are sacked in the morning because they don't understand the big picture.

Quality always trumps quantity. Period.

Netflix has stockpiled consecutive premium shows from titles such as Stranger Things, The Crown, Unbreakable Kimmy Schmidt, and Orange is the New Black.

This is in line with Netflix's policy to spend more on non-sports content than any other competitors in the online streaming space.

In 2017, Netflix ponied up $6.3 billion for content and followed that up in 2018, with a budget of $8 billion to produce original in-house shows.

Netflix hopes to increase the share of original content to 50%, decoupling its reliance on traditional media stalwarts who hate Netflix's guts with a passion.

A good portion of this generous budget will be deployed to make 30 new anime shows and 80 new original films all debuting by the end of 2018.

Amazon's (AMZN) Manchester by the Sea harvested two Oscars for its screenplay and Casey Affleck's performance, foreshadowing the opportunity for Netflix to win awards next time around, potentially boosting its industry profile.

It will only be a matter of time because of the high quality of production.

Netflix's content budget will dwarf traditional media companies by 2019, creating more breathing room against the competitors who have been late to the party and scrambling for scraps.

This is what Disney's futile attempts to take on Netflix, which raised its offer for Fox to $71.3 billion to galvanize its content business.

Disney's (DIS) bid came on the heels of Comcast Corp. (CMCSA) bid for Disney at $65 billion.

The sellers' market has boosted all content assets across the board.

Remember, content is king in this day and age.

In 2017, Time Warner (TWX) and Fox (FOX) spent $8 billion each and Disney slightly lagged with a $7.8 billion spend on non-sports programming.

Netflix will certainly announce a sweetened content outlay of somewhere close to $9.5 billion next year attracting the best and brightest to don the studios of Netflix.

What's the whole point of creating the best content?

It lures in the most eyeballs.

Subscriber growth has been nothing short of spectacular.

Expectations were elevated, and Netflix delivered in spades last quarter adding quarterly total subscribers to the tune of 7.41 million versus the 6.5 million expected by analysts.

Not only a beat, but a blowout of epic proportions.

Inside the numbers, rumors were adrift of Netflix's domestic numbers stagnating.

Consensus was proved wrong again, with domestic subscribers surging to 1.96 million versus the 1.48 million expected.

The cycle replays itself over. Lather, rinse, repeat.

Quality content attracts a wave of new subscribers. Robust subscriber growth fuels more spending, which paves the way for more quality content.

This is Netflix's secret formula to success.

Netflix has executed this strategy systemically to the aghast of traditional media companies that are stuck with legacy businesses dragging them down and making it decisively difficult to compete with the nimble online streaming players.

Turning around a legacy business is tough work because investors expect profits and curse the ends of the earth if companies spend big on new projects removing the prospects of dividend hikes.

Netflix and the tech darlings usually don't make a profit but have a license to spend, spend, and spend some more because investors are on board with a specific narrative prioritizing market share and posting rapid growth.

The cherry on top is the booming secular story happening as we speak in Silicon Valley.

Effectively, all other sectors that are not tech have become legacy sectors thanks in large part to the high degree of innovation and cross-functionality of big cap tech companies.

The future legacy winners are the legacy stocks and sectors reinventing themselves as new tech players such as General Motors (GM), Walmart (WMT), and Target (TGT).

The rest will die a miserably and excruciatingly slow death.

The Game of Thrones M&A battle with the traditional media companies is a cry of desperate search for these dinosaurs.

They were too late to react to the Netflix threat and were punished to full effect.

Halcyon days are upon Netflix, and this company controls its own destiny in the streaming wars and online streaming content industry.

As history shows, nobody executes better than CEO Reed Hastings at Netflix, which is why Netflix maintains its grade as a top 3 stock in the eyes of the Mad Hedge Technology Letter.

"I got the idea for Netflix after my company was acquired. I had a big late fee for Apollo 13. It was six weeks late and I owed the video store $40. I had misplaced the cassette. It was all my fault," - said cofounder and CEO of Netflix Reed Hastings.

Anyone would be forgiven for thinking that the stock market has become bipolar.

According to the Commerce Department?s Bureau of Economic Analysis, the answer is that corporate profits accounts for only a small part of the economy.

Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly, or are too small to have much of an impact.

Wages and salaries are in a three decade long decline. Interest and investment income is falling, because of the ultra low level of interest rates. Farm incomes are up, but are a tiny proportion of the total. Income from non-farm unincorporated business, mostly small business, is unimpressive.

It gets more complicated than that.

A disproportionate share of corporate profits is being earned overseas. So multinationals with a big foreign presence, like Apple (AAPL), Intel (INTC), Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes.

They really get to have their cake, and eat it too. Many of their business activities are contributing to foreign GDP?s, like China?s, more than they are here. Those with large domestic businesses, like retailers, earn less, but pay more in tax, as they lack the offshore entities in which to park them.

The message here is to not put all your faith in the headlines, but to look at the numbers behind the numbers. Those who bought in anticipation of good corporate profits last month, got those earnings, and then got slaughtered in the marketplace.

For those of you who heeded my expert advice to buy the ProShares Ultra Short Euro ETF (EUO) last July, well done!

You are up a massive 48%! This is on a move in the underlying European currency of only 18.5%.

My browsing of the Galleria in Milan, the strolls through Spanish shopping malls, and my dickering with an assortment of dubious Greek merchants, all paid off big time. It turns out that everything I predicted for this beleaguered currency came true.

The European economy did collapse. Cantankerous governments made the problem worse by squabbling, delaying and obfuscating, as usual.

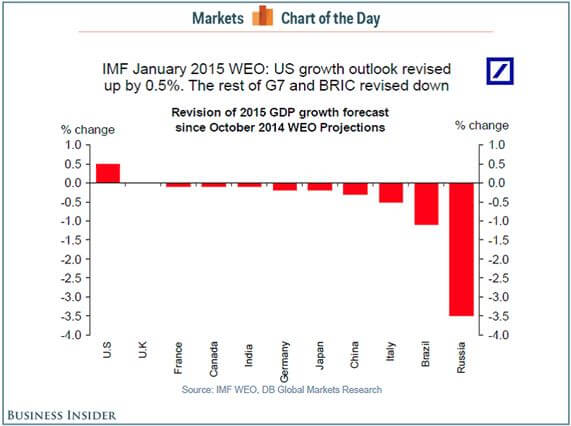

The European Central Bank finally threw in the towel and did everything they could to collapse the value of the Euro and reinvigorate their comatose economies. This they did by imitating America?s wildly successful quantitative easing, which they announced with local variations last Thursday.

And now for the good news: The best is yet to come!

Europe is now six days into a strategy of aggressive monetary easing which may take as long as five years until it delivers tangible, sustainable results. That?s how long it took for the Federal Reserve?s QE to restore satisfactory levels of confidence in the US economy.

The net net is that we have almost certainly only seen the first act of a weakening of the Euro which may last for years. A short Euro could be the trade that keeps on giving.

The ECB?s own target now is obviously parity against the greenback, which you will find predicted in my own 2015 Annual Asset Class Review released at the beginning of January (click here).

Once they hit that target, 87 cents to the Euro will become the new goal, and that could be achieved sooner than later.

However, you will not find me short the Euro up the wazoo this minute. I think we have just stumbled into a classic ?Buy the Rumor, Sell the News? situation with the Euro.

The next act will involve the ECB sitting on its hands for a year, realizing that their first pass at QE was inadequate, superficial, and flaccid, and that it is time to pull the bazooka out of their pockets once again.

This is a problem when the entire investment world is short the Euro. That paves the way for countless, rip your face off short covering rallies in the months ahead. Any smidgeon or blip of positive European economic data could spark one of these.

Trading the Euro for the past eight months has been like falling off a log. It is about to get dull, mean and brutish. So for the moment, my currency play has morphed into selling short the Japanese yen, which has its own unique set of problems.

As for the unintended consequences of the Euro crash, the Q4 earnings reports announced so far by corporate America tells the whole story.

Companies with a heavy dependence on foreign (read Euro and yen) denominated earnings are almost universally coming up short. On this list you can include Caterpillar (CAT), Procter and Gamble (PG), and Microsoft (MSFT).

Who are the winners in the strong dollar, weak Euro contest? US companies that see a high proportion of their costs denominated in flagging foreign currencies, but see their incomes arrive totally in the form of robust, virile dollars.

You may not realize it, but you are playing the global currency arbitrage game every time you go shopping. The standout names here are US retailers, which manufacture abroad virtually all of the junk they sell you here, especially in low waged China.

The stars here are Macy?s (M), Family Dollar Stores (FDO), Costco (COST), Target (TGT), and Wal-Mart (WMT).

You can see this divergence crystal clear in examining the behavior of the major stock indexes. The chart for the Guggenheim S&P 500 Equal Weight ETF (RSP), which has the greatest share of currency sensitive multinationals, looks positively dire, and may be about to put in a fatal ?Head and Shoulders? top (see the following story).

The chart for the NASDAQ (QQQ), where constituent companies have less, but still a substantial foreign currency exposure, appears to be putting in a sideways pennant formation before eventually breaking out to new highs once again.

The small cap Russell 2000, which is composed of almost entirely domestic, dollar based, ?Made in America? type companies, is by far the strongest index of the trio, and looks like it is just biding time before it blasts through to new highs.

If you are a follower of my Trade Alert Service, then you already know that I have a long position in the (IWM), which has already chipped in 2.12% to my 2015 performance.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/John-Thomas1-e1422462857973.jpg302400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-28 11:35:022015-01-28 11:35:02The Unintended Consequences of the Euro Crash

I often see one stock index outperform another, as different segments of the economy speed up, slow down, or go nowhere. Sometimes the reasons for this are fundamental, technical, or completely arbitrary.

Many analysts have been scratching their heads this year over why the S&P 500 has been moving from strength to strength for the past year, while the Dow Average has gone virtually nowhere. Since January, the (SPX) has tacked on a reasonable 7.9%, while the Dow has managed only a paltry 3.4% increase.

What gives?

The problem is particularly vexing for hedge fund managers, who have to choose carefully which index they use to hedge other positions. Do you use the broad based measure of 500 large caps or a much more narrow and stodgy 30?

What?s a poor risk analyst to do?

The Dow Jones Industrial Average was first calculated by founder Charles Dow in 1896, later of Dow Jones & Company, which also publishes the Wall Street Journal. When Dow died in 1902, the firm was taken over by Clarence Barron and stayed within family control for 105 years.

In 2007, on the eve of the financial crisis, it was sold to News Corporation for $5 billion. News Corp. is owned by my former boss, Rupert Murdoch, once an Australian, and now a naturalized US citizen. News then spun off its index business to the CME Corp., formerly the Chicago Mercantile Exchange, in 2010.

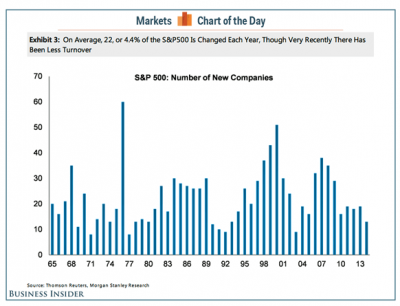

Much of the recent divergence can be traced to a reconstitution of the Dow Average on September 20, 2013, when it underwent some major plastic surgery.

It took three near-do-wells out, Bank of America (BAC), Hewlett Packard, (HPQ), and Alcoa (AA). In their place were added three more robust and virile companies, Goldman Sachs (GS), Visa (V), and Nike (NKE).

Call it a nose job, a neck lift, and a tummy tuck all combined into one (Not that I?ve been looking for myself!).

And therein lies the problem. Like many attempts at cosmetic surgery, the procedure rendered the subject uglier than it was before.

Since these changes, the new names have been boring and listless, while the old ones have gone off to the races. Hence, the differing performance.

This is not a new problem. Dow Jones has been terrible at making market calls over its century and a half existence. As a result, these rebalancings have probably subtracted several thousand points over the life of the Dow.

They are, in effect, selling lows and buying highs, much like individual retail investors do. It is almost by definition the perfect anti-performance index. When in doubt, always measure your own performance against the Dow.

Dow Jones takes companies out of its index for many reasons. Some companies go bankrupt, whereas others suffer precipitous declines in prices and trading volumes. (BAC) was removed because, at one point, its shares took a 95% hit from its highs and no longer accurately reflected a relevant weighting of its industry. Citigroup (C) suffered the same fate a few years ago.

Look at the Dow Average of 1900 and you wouldn?t recognize it today. In fact, there is only one firm that has stayed in the index since then, Thomas Edison?s General Electric (GE). Buying a Dow stock is almost a guarantee that it will eventually do poorly.

This is why most hedge funds rely on the (SPX) as a hedging vehicle and how its futures contracts, options and ETF?s, like the (SPY), get the lion?s share of the volume.

Mind you, the (SPX) has its own problems. Apple (AAPL) has far and away the largest weighting there and is also subject to regular rebalancings, wreaking its own havoc.

Because of this, an entire sub industry of hedge fund managers has sprung up over the decades to play this game. Their goal is to buy likely new additions to the index and sell short the outgoing ones.

Get your picks right and you are certain to make money. Every rebalancing generates massive buying and selling in single names by the country?s largest institutional investors, which in reality are just closet indexers, despite the hefty fees they charge you.

Given their gargantuan size these days, there is little else they can do. Rebalancings also give brokerage salesmen talking points on otherwise slow days and generate new and much needed market turnover.

What has made 2014 challenging for so many managers is that so much of the action in the Dow has been concentrated in just a handful of stocks.

Caterpillar (CAT), the happy subject of one of my recent Trade Alerts, accounts for 35.3% of the Index gain this year. Walt Disney (DIS) speaks for 24.2% and Intel (INTC) 23.4%.

Miss these three and you are probably trolling for a new job on Craig?s? List by now, if you?re not already driving a taxi for Uber.

It truly is a stock picker?s market; a market of stocks and not a stock market.

Believe it or not, there are people that are far worse at this game than Dow Jones. The best example I can think of are the folks over at Nihon Keizai Shimbun in Tokyo (or Japan Economic Daily for most of you), who manage the calculation of the 225 stocks in the Nikkei Average (once known as the Nikkei Dow).

In May, 2000, out of the blue, they announced a rebalancing of 50% of the constituent names in their index. Their goal was to make the index more like the American NASDAQ, the flavor of the day. So they dumped a lot of old, traditional industrial names and replaced them with technology highfliers.

Unfortunately, they did this literally weeks after the US Dotcom bubble busted. The move turbocharged the collapse of the Nikkei, probably causing it to fall an extra 8,000 points or more than it should have.

Without such a brilliant move as this, the Nikkei bear market would have bottomed at 15,000 instead of the 7,000 we eventually got. The additional loss of stock collateral and capital probably cost Japan an extra lost decade of economic growth.

So for those of you who bemoan the Dow rebalancings, you should really be giving thanks for small graces.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/07/Mickey-Mouse.jpg352339Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-07-10 01:05:012014-07-10 01:05:01Why is the S&P 500 Beating the Dow?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visist to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.