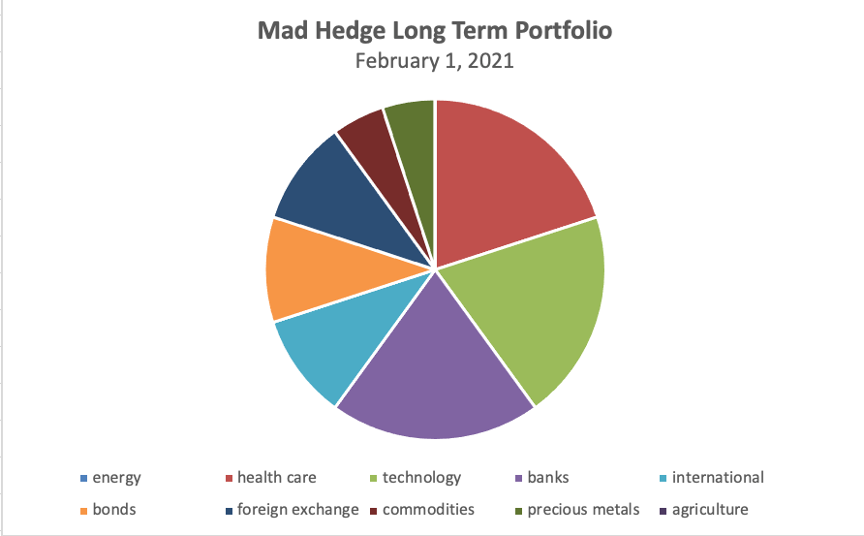

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on July 21, 2020. In fact, not only did we nail the best sectors to go heavily overweight, we also completely dodged the bullets in the worst-performing ones.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing, these are the investments you can make, and then not touch until you start drawing down your retirement funds at age 72.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted below.

To download the entire new portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go “My Account”, then “Global Trading Dispatch”, then click on the “Long Term Portfolio” button.

Changes

I am cutting back my weighting in biotech from 25% to 20% because Celgene (CELG) was taken over by Bristol Myers (BMY) at a 110% profit compared to our original cost. We also earned a spectacular 145% gain on Crisper Therapeutics (CRSP). I’m keeping it because I believe it has more to run.

My 30% weighting in technology also gets pared back to 20% because virtually all of my names have doubled or more. These have been in a sideways correction for the past six months but are still an important part of any barbell portfolio. So, take out Facebook (FB) and PayPal (PYPL) and keep the rest.

I am increasing my weighting in banks from 10% to 20%. Interest rates are finally starting to rise, setting up a perfect storm in favor of bank earnings. Loan default rates are falling. Banks are overcapitalized, thanks to Dodd-Frank. And because of the trillions in government stimulus loans they are disbursing, they are now the most subsidized sector of the economy. So, add in Morgan Stanley (MS) and Goldman Sachs (GS), which will profit enormously from a continuing bull market in stocks.

Along the same vein, I am committing 10% of my portfolio to a short position in the United States Treasury Bond Fund (TLT) as I think bonds are about to go to hell in a handbasket. I rant on this sector on an almost daily basis, so go read Global Trading Dispatch.

I am keeping my 10% international exposure in Chinese Internet giant Alibaba (BABA) and the iShares MSCI Emerging Market ETF (EEM). The Biden administration will most likely dial back the recent vociferous anti-Chinese stance, setting these names on fire.

I am also keeping my foreign currency exposure unchanged, maintaining a double long in the Australian dollar (FXA). The Aussie has been the best performing currency against the US dollar and that should continue.

Australia will be a leveraged beneficiary of the synchronized global economic recovery, both through strong commodity prices and gold which has already started to rise, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

As for precious metals, I’m baling on my 10% holding in gold (GLD), which delivered a nice 20% gain in 2020. From here, it is having trouble keeping up with other alternative assets, like Bitcoin, and there are better fish to fry.

Yes, in this liquidity-driven global bull market, a 20% return is just not enough to keep my interest. Instead, I add a 5% weighting in the higher beta and more volatile iShares Silver Trust (SLV), which has far wider industrial uses in solar panels and electric vehicles.

As for energy, I will keep my weighting at zero. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free. You are looking at the next buggy whip industry.

My ten-year assumption for the US and the global economy remains the same. I’m looking at 3%-5% a year growth for the next decade.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient, productive, and profitable than the old.

You won’t believe what’s coming your way!

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/long-term-portfolio.png536864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-02 10:02:032021-02-02 10:37:30My Newly Updated Long-Term Portfolio

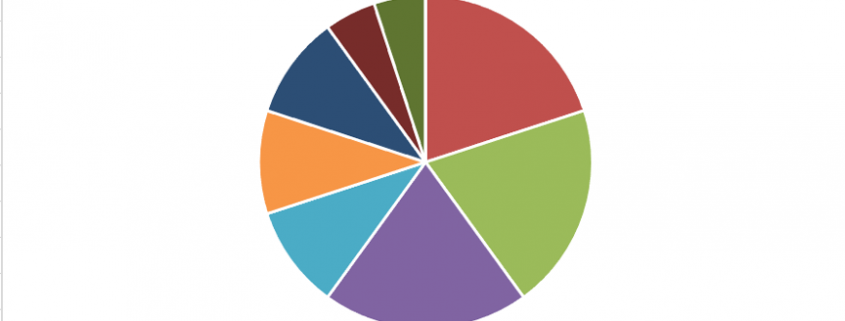

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on October 17, 2019. In fact, not only did we nail the best sectors to go heavily overweight, we completely dodged the bullets in the worst-performing ones, especially in energy.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing, these are the investments you can make, and then not touch until you start drawing down your retirement funds at age 70 ½.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted in red.

To download the entire portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go to “My Account”, then “Global Trading Dispatch”, then click on the “Long Term Portfolio” button.

My 5% holding in Biogen (BIIB) was taken over by Bristol Myers (BMY) at a hefty premium at an all-time high, so I’ll take the win. I am replacing it with Covid-19 vaccine frontrunner Bristol Myers (BMY) itself.

I am also taking out healthcare provider Cigna (CI), whose profits have been hammered by the pandemic. A future Biden administration might also move to a national healthcare system that will cap profits. I am replacing it with another Covid-19 vaccine leader Pfizer (PFE).

My 30% weighting in technology remains the same. Even though these stocks are 30% more expensive than they were three years ago, I believe they will lead the charge into the 2020s. It’s where the big growth is. These have doubled or more over the past nine months.

I am sticking with a 10% weighting in banking. Thanks to trillions in stimulus loans, they are now the most government-subsidized sector of the economy. I also believe that massive bond issuance by the US Treasury will deliver a sharply steepening yield curve, another pro bank development.

With my 10% international exposure, I am taking out a 5% weight in slow-growth Japan and replacing it with Chinese Internet giant Alibaba (BABA). The US will most likely dial back its vociferous anti-Chinese stance next year and (BABA) will soar.

I am executing another switch in my foreign currency exposure, taking out a long in the Japanese yen (FXY) and a short in the Euro (EUO) and substituting in a double long in the Australian dollar (FXA).

Australia will be a leveraged beneficiary of a recovery in the global economy, both through a recovery on commodity prices and gold which has already started, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

I’m quite happy with my 10% holding in gold (GLD), which should move to new all-time highs imminently….and then go ballistic.

As for energy, I will keep my weighting at zero, no matter how cheap it has gotten. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free.

My ten-year assumption for the US and the global economy remains the same.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/07/graph2.png7461196Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-07-22 09:02:112020-07-22 09:05:52My Newly Updated Long-Term Portfolio

In this current coronavirus market, discovering a stock that can survive the pandemic without suffering a major hit is akin to finding the Holy Grail.

This is why I’m on the lookout for undervalued names that offer strong dividends and a stable balance sheet.

In my search, I once again came across the biotechnology pioneer Amgen (AMGN), a 40-year-old company that has continuously proven its critics wrong.

After four decades in the business, this healthcare heavyweight has yet to show any signs of slowing down. If anything, Amgen has been consistent in its efforts to show off its promising pipeline.

In 2020 alone, the company reported at least 39 drug candidates in its pipeline, with practically half already in Phase 3 trials.

As one of the founding fathers of the biotechnology sector, Amgen, which was founded by my UCLA college biochemistry professor, would be remiss to skip on the coronavirus race. If I’d only stuck with him a little longer, I would be filthy rich by now.

In April, the company announced its collaboration with Adaptive Biotechnologies (ADPT) to develop antibodies to be used for COVID-19 treatment.

While the biotechnology giant isn’t the first to jump into the fray, it has an undeniable ace up its sleeve: Amgen is known as one of the leaders in the development of antibody-based treatments. This alone makes it a strong contender.

Outside its coronavirus work, Amgen has an extensive list of prospects in its pipeline along with a number of workhorse drugs.

However, not everything is as smooth sailing as investors would hope.

Previous blockbusters, rheumatoid arthritis drug Enbrel and chemotherapy medication Neulasta, which comprised 40% of Amgen’s product sales in the first quarter of 2019, failed to move the needle during the same period in 2020. Actually, Neulasta suffered a devastating 40% drop in sales.

Other top performers like multiple myeloma treatment Xgeva and anemia drug Aranesp are having trouble as well, eking out a measly 2% in sales gains in the said period.

As for anemia injection Epogen, the bestselling drug dropped by 29%. Even the sales of hyperparathyroidism medication Cinacalcet slid by 42%.

Overall, this doesn’t sound like an auspicious beginning for Amgen this 2020.

Nonetheless, the company’s robust growth in other areas made up for the laggards.

In fact, Amgen’s total product sales increased by 12%, jumping from $5.3 billion in the first quarter of 2019 to almost $5.9 billion in the same period in 2020.

For instance, sales of osteoporosis treatment Prolia jumped by 10%, pushing the drug in the second spot among the top 10 products in Amgen’s portfolio.

Meanwhile, cholesterol drug Repatha continues to impress, showing off a 62% increase in revenue from $141 million to $229 million.

Even the newer multiple myeloma treatment Kryprolis went up by 19%, while metastatic colorectal cancer injection Vectibix registered a 19% sales gain. Sales for cancer medication Blincyto also went up by 36% year over year to hit $94 million.

Another drug surging forward is kidney treatment Parsabiv, which reported a 39% increase in sales. Newcomer postmenopausal osteoporosis drug Evenity, which was launched in the US market just last year, recorded a respectable $100 million in sales.

In terms of developments that actually pushed the needle for Amgen, the first thing that comes to mind is definitely the acquisition of psoriasis and psoriatic arthritis medication Otezla.

This blockbuster drug, which the company bought for $13.4 billion in cash from the recently acquired Celgene Corporation (CELGN), raked in $479 million in revenues for the first quarter of 2020 alone.

Amgen executives estimate a low double-digit year-over-year sales increase for Otezla up until 2024.

Another exciting development for Amgen is its deal with BeiGene (BGNE), in which the biotechnology pioneer acquired a 20.5% stake in the Chinese company.

Part of this deal is BeiGene’s efforts to commercialize select drugs from Amgen’s oncology lineup to target the expansive Chinese market.

On top of this, the two companies are slated to develop 20 new cancer drugs as well. So far, AMG 510 and tezepelumab are eyed to be launched by 2021.

Amgen is also gearing up to ride the wave of biosimilars, which has a market estimated to surpass $69 billion in the next five years. Due to its lower costs, biosimilars are projected to save consumers roughly $160 billion during the same period.

Perhaps this lucrative opportunity is what made Amgen realize that if they can’t beat them, they might as well join them. That is, the company has already worked towards becoming a major player in the biosimilar space.

In fact, Amgen has started with this plan in 2017 courtesy of the company’s first-ever approved cancer-fighting biosimilar: Mvasi.

So far, Amgen has 10 biosimilars in its current pipeline. Four of which already received FDA approval.

Looking at Amgen’s financial records, it’s safe to say that the company has a strong financial position.

It offers a yield of approximately 2.8% and a payout ratio of over 47%. The dividend coverage ratio is roughly 212%, ensuring a safe dividend and a 5-year growth rate of almost 19%.

Amgen’s profit margin is recorded to be at least 23% in 9 of the recent 10 fiscal years, with growth expected since 1 in 5 cancer patients in the United States uses Amgen medication.

The company’s free cash flow in the first quarter of 2020 rose to $2 billion from the $1.7 billion reported during the same period in 2019.

These quarterly results along with its multitude of growth prospects are proof to Amgen’s capacity to navigate through the decline in other product offerings. The biotechnology company’s numbers in the first quarter of this year demonstrate there’s a good chance it will break through resistance because of its solid sales momentum.

This makes Amgen attractive to long-term biotechnology and healthcare investors. With its strong record, promising pipeline, and decent dividend, the company will be able to sustain its status as a good buy.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/06/amgen.png216462Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-02 09:30:072020-06-02 20:56:04Ten More Reasons to Buy Amgen

Forecasting drug revenue can be a tricky business -- just ask the biotech leaders who overpromised but underdelivered.

These days, more and more variables are coming into play, with the US elections looming over us and the threat of generic meds overtaking market leaders becoming more tangible by the minute.

Another threat is the entry of biosimilars in the US, knocking down big-name drugs even in the most lucrative markets. Payers are also constantly seeking discounts, forcing tougher competition among crowded markets like diabetes and hepatitis.

However, the oncology sector remains a booming sector for the biotech industry.

Practically all major companies are either developing oncology treatments or already marketing these as blockbuster treatments, with 63 cancer drugs launched in just the past five years.

Unfortunately, not all cancer drugs are created equal. Looking at the spending on the treatments in recent years, it can clearly be seen that almost 80% of the money has been hogged by the industry leaders with the rest of the group lagging far behind.

To put things in perspective, bear in mind that the annual sales of the top 20 cancer drugs have reached over $50 billion, with $31 billion distributed among industry leaders Merck and Co (MRK), Celgene (CELG), and Roche Holdings (RHHBY).

These numbers hardly come as a surprise especially in light of over $133 billion recorded in spending for cancer treatments.

The top-selling oncology drug to date is multiple myeloma treatment Revlimid. Technically a Celgene product, the company’s $74 billion acquisition by Bristol-Myers Squibb (BMY) means the drug will be joining the other powerhouse offerings in the newly formed company’s lineup in the years to come.

With over a decade of dominance in the market and an impressive $9.7 billion in global sales annually, Revlimid has yet to hit its peak.

In fact, this mega-blockbuster is projected to exceed $15 billion in sales next year.

As if that wasn’t impressive enough, this oncology leader is estimated to bring more than double that amount come 2022.

Another dominant player in the oncology market is lung cancer drug Keytruda. Since its launch, this Merck immunotherapy leader has been able to usher in a boatload of cancer treatments using its core indications -- and it’s not yet done.

With an FDA approval eyed on June 29, 2020 for yet another indication for Keytruda, specifically for treating cutaneous squamous cell carcinoma (cSCC), its goal to dethrone Revlimid as the leader in this space now looks achievable.

Right now, Keytruda is used for various cancer types.

Aside from dominating the large addressable lung cancer market, it’s also used to treat head and neck cancer as well as melanoma. This makes Keytruda’s contributions indispensable to Merck’s overall top-line and continuous growth in sales in the past years.

Hence, it comes as no surprise that Merck’s recent third-quarter earnings had Keytruda is the starring role once again. Sales for this oncology drug jumped 62% year over year, reaching almost $3.1 billion.

One more dominant force in the oncology sector is Roche, with breast cancer drug Herceptin serving as the primary moneymaker of the company in the past 15 years.

With Herceptin raking in roughly $7 billion in annual sales in recent years, Roche has been proactive in securing its position in the oncology space by adding blockbusters ovarian cancer drug Avastin and leukemia medication Rituxan in the list.

For years, these three cancer drugs have formed the foundation of Roche’s continuous growth in the oncology sector. However, these treatments are now in danger of facing competition.

A particularly aggressive competitor is Pfizer (PFE), with its breast cancer drug Ibrance gaining traction as shown by its growing sales from $0.7 billion in 2015 to a promising $4.1 billion in 2018. Other competitors include Eli Lilly’s (LLY) Verzinio and Novartis’ (NOVN) Piqray.

To maintain its stronghold, Roche has been aggressive as well in developing new drugs.

Word has it that the company is expecting an addition $5 billion in sales for its new cancer treatments like breast cancer drugs Perjeta and Kadycla along with lung cancer medications Tecentriq and Alecensa.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/12/celgene.png339385Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-12-26 07:30:122019-12-26 07:27:52The Boom in Cancer Drugs

The biotech industry is breaking out, with the sector witnessing tremendous growth in the later part of 2019. With the stocks surging, it looks like the new year is setting up to a strong start that could continue well up into 2020.

Despite the anxiety over the feared government price controls in the drug sector, the early thinking in the biotech world remains optimistic. In fact, the stage seems to be set for even bigger news come 2020. This prediction comes on the heels of the over $7 billion deals closed just this summer alone.

To date, approximately $100 billion total potential value of research and development have been spent by biotech companies since June 2019, with $11 billion paid upfront in cash.

Among those deals, the biggest so far is Bristol-Myers Squibb’s (BMY) $74 billion acquisition of Celgene (CELG). Another massive agreement is Novartis AG’s (NOVN) $9.7 billion acquisition of The Medicines Company (MDCO).

Eli Lilly and Co’s (LLY) $8 billion takeover of rare genetic mutation drug Vitakvi creator, Loxo Oncology (LOXO), also signified notable movements in the industry along with Johnson and Johnson’s (JNJ) $5.8 billion buyout of robotic surgery company Auris Health. Even Roche Holding AG (ROG) is expected to complete its $4.3 billion merger with gene therapy company Spark Therapeutics (ONCE) before the year ends.

Not far behind are Merck and Co’s (MRK) $2.7 billion acquisition of ArQule (ARQL) as well as Sanofi SA’s (SAN) $2.5 billion buyout of clinical-stage DNA base pair treatment company Synthorx Inc (THOR).

The majority of the deals were in the oncology space, with three times as many oncology deals made compared to the number two sector, the neurology sector. To put things in perspective, seven of the top 10 deals made in 2019 involved oncology treatments.

What can we expect in 2020?

A number of drug candidates remain in the pipeline, but one mid-cap biotech company is anticipated to make big bucks next year. The catch? It’ll need the help of a bigger and more established company to make it happen. That is, this promising company has become the most eligible buyout candidate for 2020.

Amarin Corporation (AMRN) has taken center stage when it became the first-ever company to hit positive results for its prescription omega-3 treatment, Vascepa -- a feat that none of the other biotech giants managed to accomplish. Actually, competitor GlaxoSmithKline (GSK) created its own omega-3 treatment, Lovaza, only to have it fail to reach its goal.

Barring any major setback, Vascepa is slated as the next blockbuster treatment in the cardiovascular disease space -- possibly even displacing Pfizer’s (PFE) Lipitor as the king of this segment. In fact, several major healthcare groups like the American Heart Association, American Diabetes Association, the European Society of Cardiology have already endorsed Vascepa as an effective treatment for LDL cholesterol.

The Amarin medication is projected to peak at $4 billion in annual revenues by 2028. Considering that its manufacturer’s reported third-quarter earnings this 2019 is only at $112.4 million, the approval of Vascepa will undoubtedly be a game-changer for its investors.

However, Vascepa’s incredible potential along with the fact that Amarin has no other drug candidate in its pipeline makes the company ripe for a takeover. For one, it’s not financially capable of juggling both the marketing of Vascepa and developing or building a solid pipeline to support its growth. With the omega-3 treatment’s projected blockbuster status, a bigger and more established company could undoubtedly be more fit to help it reach its potential.

Who are the potential suitors?

Three heavyweights have been repeatedly linked to Amarin: Pfizer, Novartis, and Amgen (AMGN). Since all three have a budding cardiovascular unit, it could be anyone’s game.

However, Novartis’ recent acquisition of The Medicines Company makes it the least likely candidate in the list right now. After all, the latter already has a potential blockbuster cholesterol-lowering drug in Inclisiran.

That paves the way for a new suitor in the form of Gilead Sciences (GILD). Just a few weeks ago, Gilead added Vascepa to one of its ongoing trials involving nonalcoholic steatohepatitis. Whether or not this signifies interest in buying out Amarin is anybody’s guess.

Heading into the next year, the biotech sector is expected to welcome the new year with strong fundamentals and great opportunities for outperformance. While the election may bring changes to policies, the ongoing growth and innovation in this industry make it impossible to be excited for what’s in store for the future.

After all, more and more life-extending and even life-saving treatments are getting discovered by the day. Aside from following the developments in the industry, why not use your knowledge to fatten your pocketbook along the way?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-12-17 04:00:382019-12-17 03:56:24Why the M&A Boom Will Spill Into 2020

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.