Mad Hedge Biotech & Healthcare Letter

December 5, 2019

Fiat Lux

Featured Trade:

(WHY 1 + 1 = 4 WITH THE BRISTOL MYERS/CELGENE MERGER),

(BMY), (CELG), (AMGN)

Mad Hedge Biotech & Healthcare Letter

December 5, 2019

Fiat Lux

Featured Trade:

(WHY 1 + 1 = 4 WITH THE BRISTOL MYERS/CELGENE MERGER),

(BMY), (CELG), (AMGN)

The treasure trove of Bristol-Myers Squibb’s (BMY) growth products expanded considerably following the completion of its $74 billion merger with Celgene (CELG). This deal marks the end of a long chapter in the industry’s history, as Celgene, founded way back in 1986, was one of the first biotech companies created.

From a financial standpoint, the combined company is hailed as one of the most exciting powerhouses of profitability until at least 2023. As things stand, the newly minted biotech behemoth is trading at roughly nine times forward earnings.

The current company also offers an attractive dividend yield of 2.9% -- and that’s not even the best part of the news. The most exciting part of the deal is the fact that the new company now owns one of the most valuable oncology franchises in the biotech sector.

Under the terms, Celgene shareholders got the following for every share: 1.00 share of BMY common, cash worth $50 without interest, and one Contingent Value Right (CVR) they can trade. If they choose to not trade it, then the Celgene shareholder will receive payment of $9 in cash depending on future milestones achieved. As for (BMY), the company received $13.4 billion following Celgene’s sale of blockbuster psoriasis and psoriatic arthritis drug Otezla to Amgen (AMGN) as part of regulatory requirements.

The CVRs are contingent on three drugs in Celgene’s pipeline. One is the multiple sclerosis treatment Ozanimod. Another is a liso-cel lymphoma drug, which is expected to get the green light by December 31, 2020. The third is multiple myeloma treatment bb2121, which is eyed for approval by March 31, 2021.

Ozanimod actually has a high chance of winning an FDA approval by early 2020. The drug’s peak annual sales is expected to be in the ballpark of $5 billion. Meanwhile, Celgene’s liso-cel treatments are anticipated to rake in an additional $4 billion or so in annual sales. The company’s recently approved Reblozyl is also estimated to tack on another $2 billion in peak sales.

Celgene’s CelMOD treatments, which are in their early-stage clinical studies, could be massive moneymakers as well. Another cell therapy under development with Massachusetts-based gene therapy developer bluebird bio (BLUE), bb21217, is also projected as a big winner.

While the Celgene cancer pipeline is promising, the company came into this union with a number of already top-selling oncology drugs like multiple myeloma medication Revlimid as well as blood cancer treatments Inrebic and Pomalyst.

As for BMY, the biopharma giant also has its own high-profile lineup led by leukemia target therapy Sprycel, atrial fibrillation treatment Eliquis, advanced stage lung cancer injection Opdivo, and metastatic melanoma treatment Yervoy.

In fact, Opdivo and Eliquis are projected to rank as among the highest-selling drugs globally in the succeeding years.

Although some BMY investors are voicing concerns over the impending sales decline for Revlimid courtesy of generic rivals by 2022, Celgene’s new candidates and already top-performing drugs could still give the combined company a firm growth runway.

Hence, BMY and Celgene have effectively built a prodigious economic moat that practically eliminates any fear of competition in several crucial areas. This is not to say that particular products won’t experience the usual rise and fall in sales. It simply means that BMY’s overall oncology portfolio wouldn’t exactly encounter major problems when it comes to income generation and growth in the years to come.

In a broader sense, the newly formed company should be able to withstand any slowing down in the economy. Cancer patients need continuous medication, and it’s highly unlikely that they would choose to put a stop to their treatment simply because the economy is taking a downturn. Consequently, this makes BMY one of the safest plays in the market right now.

Keep buying (BMY) on dips. There is far to go.

Mad Hedge Biotech & Health Care Letter

October 22, 2019

Fiat Lux

Featured Trade:

(SPECIAL CANCER ISSUE - PART 1)

(BMY), (MRK), (CELG), (AMGN), (ROG), (MRTX), (INCY)

Multiple times every year, leading oncology researchers gather to share and discuss the latest developments in the field. During these events, biotech companies actively seek ways to snatch top billing, hoping to amp up their value not only within the industry but also to the public.

Needless to say, company stock prices tend to fluctuate dramatically based on the data and whether or not the companies lived up to the hype of their studies. Hence, these events have turned into must-attend conferences among the healthcare industry leaders and even institutional investors.

For everyday investors though, it’s too impractical to even consider the possibility of attending these grand shindigs. This is why we’re sharing with you a list of companies that are currently making strides or are anticipated to dominate the cancer research and treatment market in 2019 and in the years to come.

Bristol-Myers Squibb (BMY)

As always, no other field has been watched more intensely than the lung cancer market -- an area considered as the most lucrative in the immuno-oncology circle. In the recently concluded European Society for Medical Oncology Congress in Barcelona, all eyes were on the up-and-coming Opdivo/Yervoy combo of Bristol-Myers Squibb (BMY).

In the recent data it presented, Bristol disclosed that the combination of its cancer drugs Opdivo and Yervoy provided promising results to melanoma patients. According to their study, over 50% of melanoma patients survived after five years which is a huge leap from the 5% survival rate recorded over the same period prior to the introduction of immunotherapies.

With the company’s recent moves to beef up its cancer portfolio, the Opdivo/Yervoy combo is anticipated to turn into a strong competitor of Roche Holding Ltd. Genussscheine’s (ROG) Tecentriq. This combo also reinvigorates the ongoing rivalry between Bristol and Merck & Co. (MRK), with Opdivo/Yervoy aiming to dethrone the latter’s major moneymaker Keytruda.

However, this isn’t exactly the first time Bristol showed interest in dominating the oncology market. Wielding the power of its $81.05 billion market value, Bristol has signified its aggressive stance in pushing for the expansion of its cancer department.

The most highly publicized news from this front came in January this year courtesy of its announcement involving a $74 billion merger with Celgene Corporation (CELG). Now, it appears that we’re seeing the first of Bristol’s efforts to bolster its cancer drug lineup.

Although Bristol has been underperforming compared to its competitors for the majority of 2019, the stock has actually surpassed its rivals by roughly 5% in September. Following its 52-week low in July, the company has performed steadily higher to currently trading 6.5% below its 2019 high.

Hence, traders should be vigilant as a dip to a short-term trendline in the next weeks could offer a suitable entry point to eventually take advantage of the upside momentum.

Amgen (AMGN)

Another oncology frontrunner is Amgen (AMGN). The biotech giant recently presented its data on experimental treatments AMG 510 and AMG 160, which target some forms of colorectal cancer. So far, AMG 510 has provided higher response rates at 3% for patients across all levels of dosage.

These drugs form part of the rising trend of precision medicines, which zero in on particular gene mutations. This method is anticipated to be able to ward off cancer cells regardless of the organ where the disease originated.

In September, Amgen shared that the drug managed to shrink tumors by almost 50% during the trial period for advanced non-small lung cancer patients. Meanwhile, the drug’s disease control rate was recorded at 92%, with patients capable of tolerating AMG 510 without any dose-limiting toxicities.

These results prompted the FDA to send AMG 510 for “fast track” review. Aside from their own study, Amgen is also looking at a possible combination with Merck’s Keytruda in an effort to bolster its foothold in the lung cancer front.

If Amgen succeeds in the application of AMG 510 to colorectal cancer patients, the drug will be the first-ever approved treatment to target a mutated form of a gene commonly referred to as KRAS. This particular mutation called KRASG12C is prevalent in approximately 13% of non-small cell lung cancers, 3% to 5% of colorectal cancers, and almost 2% of solid tumor cancers.

In terms of revenue, the success of AMG 510 could lead to annual sales of $3 billion in the United States alone and $6.4 billion internationally. Aside from Amgen, Mirati Therapeutics Inc. (MRTX) has been actively pursuing treatments that aim to treat KRAS mutations as well.

Incyte Corporation (INCY)

At first blush, Incyte (INCY) is regarded as simply another young company striving to make a name for itself in the massive biotech market. Despite the success of bone marrow disorder drug Jakafi, a lot of investors still believe that the company only managed to stumble its way to growth. In fact, even those who actually started to invest in this biopharma firm still somehow see it as a company with an extremely limited potential.

Unfortunately for these investors, they’re missing out on a crucial detail. Although Incyte’s trajectory isn’t exactly moving at a blistering pace, the steady revenue growth of the company in 2019 is a strong indicator of meaningful profits in the succeeding years.

This growth would eventually land the company in the watchlist of every biotech investor, with the company stock already gaining 18% this year alone to boost its $16.10 billion market value.

One of the most exciting developments from Incyte is its bile duct cancer research which led to a potential oncology blockbuster drug Pemigatinib. So far, 36% of its test patients saw their tumors shrink with a preliminary median overall survival of 21.1 months.

Despite the promising results though, the company cautions on the modesty of its projected revenue as Pemigatinib specifically targets cholangiocarcinoma, which is a rare type of bile duct cancer. Incyte plans to submit the drug for review to the FDA before the year ends.

For now, Incyte is focused on the commercialization and development of its existing moneymakers. Aside from Jakafi, the company is also making waves in the rheumatoid arthritis market with Olumiant. Its myeloid leukemia treatment Iclusig is another potential golden goose on the rise as well.

So far, Incyte’s share price has been trading at approximately $15 range since April. The past two months showed a pullback though, with the stock finding key support from the lower trendline of the trading range at $72. For investors who intend to open a long position within these levels, you should set your take-profit order somewhere near $88. However, simply cut your losses if Incyte stock fails to hold $72 support.

Global Market Comments

October 17, 2019

Fiat Lux

Featured Trade:

(UPDATING THE MAD HEDGE LONG TERM MODEL PORTFOLIO),

(USO), (XLV), (CI), (CELG), (BIIB), (AMGN), (CRSP), (IBM), (PYPL), (SQ), (JPM), (BAC), (EEM), (DXJ), (FCX), (GLD)

Mad Hedge Biotech & Healthcare Letter

October 8, 2019

Fiat Lux

Featured Trade:

(GET ON THE CELGENE BANDWAGON),

(CELG), (BMY), (GSK), (AMGN), (RHHBY), (ROG), (GMAB), (MOR)

If you’re looking for a biotech stock that just relentlessly grinds up every day, Celgene Corporation (CELG) has to be at the top of your list, one of the most dominant players in the industry today.

Thanks to its $74 billion merger with Bristol-Myers Squibb (BMY), the combined companies are expected to push out Amgen in the top spot by 2020. Perhaps a positive indicator that things are looking up is the 50.9% rise in Celgene stock this year.

While the deal with Bristol has been predictably riddled with setbacks and delays, the sale of blockbuster arthritis drug Otezla to Amgen last month over antitrust concerns has finally pushed the merger forward.

While waiting for the merger with (BMY) to be finalized by the end of 2019, Celgene has been busy coming up with ways to attract more investors.

One of the exciting efforts of the biotech giant is its recent collaboration with Immatics Biotechnologies. Celgene joins GlaxoSmithKline (GSK) in the T-cell treatment market. With these two behemoths providing resources for this field, researchers are hopeful that a breakthrough drug will be discovered soon.

This partnership with Immatics saw Celgene shell out $75 million to gain access to three of the smaller firm’s anti-cancer adoptive cell therapies. With Immatics’ focus on T-cell treatments, the collaboration with Immatics will provide Celgene a wider pool of candidates for their solid tumor programs.

Aside from the $75 million upfront payment, Immatics will also receive $505 million in milestone payments for every licensed drug if Celgene decides to exercise the option. That means Celgene will have the opportunity to pay for the full or partial rights on selected assets developed from the T-cell therapies.

Ideally, Immatics would earn over $1.5 billion from the collaboration plus tiered royalties on net profits. As for Celgene, the biotech company will share the rewards with Bristol-Myers.

This collaboration marks the biggest upfront payment received by Immatics since its creation in 2000. The company, which is a spinoff of Germany’s University of Tübingen, adds Celgene to its growing number of partners including Amgen (AMGN), Roche Holding Ltd.(RHHBY), Genussscheine (ROG), Genmab (GMAB), and Morphosys (MOR).

The Munich company’s work on adoptive cell treatments and bispecific antibodies also generated interest from the cancer center of the University of Texas.

Since its creation, Immatics has managed to raise $220 million in venture capital plus roughly $130 million in non-dilutive funding. The Celgene deal puts the company’s total capital at $420 million.

So far, Celgene has reported three quarters of consistently accelerating earnings per share increase and a quarter of notable sales growth. However, the Bristol-Myers deal has yet to be completed. More importantly, some blockbuster products face uncertain futures due to rival copycats.

One major factor contributing to the doubts surrounding the company’s future is the recent sale of Otezla. Since this drug has been Celgene’s major moneymaker for years, it remains to be seen how the company will cope with its loss.

Aside from Otezla, another Celgene blockbuster facing pressure is blood cancer treatment Revlimid. While the multiple myeloma drug reported an 11.4% jump in its second quarter sales this year, the company has yet to fully safeguard it from the patent challenges aiming to end its reign in the market.

While the effects of the Immatics collaboration and the recent developments on the Bristol-Myers merger have yet to concretely manifest themselves, Celgene is expected to display strength when the next earnings release of 2019 draws nearer.

In the third quarter report, the company is projected to post an earnings per share of $2.73. This would indicate a 19.21% year-over-year increase. Meanwhile, its earnings per share for the full year of 2019 is expected to rise by over 23% to reach $10.91. As for its revenue, Celgene is estimated to earn $17.44 billion this year, marking a 14.11% rise from 2018.

In terms of its merger with Bristol-Myers, the two pharmaceutical giants are anticipated to have a combined total of 10 drugs already in the late-stage testing phase and six drugs ready to be released soon.

Additionally, the companies disclosed that they have roughly 50 drugs slated for early and mid-stage testing. Among those, 21 are reported to be focused on oncology treatments.

Buy Celgene on the next 5% dip in the shares. It seems to be on a tear.

Mad Hedge Biotech & Healthcare Letter

October 1, 2019

Fiat Lux

Featured Trade:

(THE PLAYERS GUIDE TO BIOTECH INVESTING)

(AMGN), (PFE), (NOVN), (ABBV), (ABT),

(AGN), (ROG), (GSK), (CELG), (JNJ), (BMY)

You can’t watch a game without a program, and the lineup for biotech and healthcare is truly astonishing. No surprise then that the fields account for more or less than 17% of US GPD.

Here is a listing of the biggest $100 billion plus products you have never heard of. The good news is that you have just stumbled across a sector that will generate no less than a staggering $1.4 trillion in sales over the next five years.

That means it’s certainly worth your time getting to know this field. With this amount at stake, it’s no wonder companies manufacturing these blockbuster drugs are sparing no expense to fight off patent vultures.

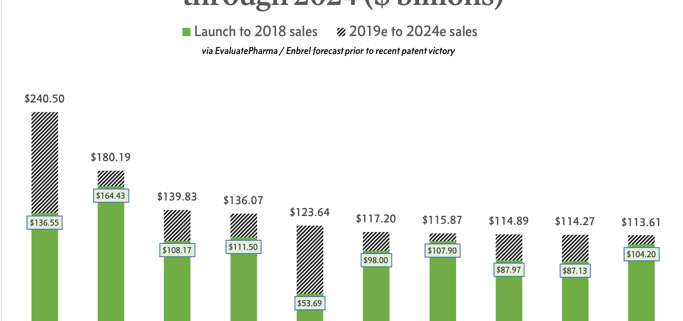

A good example is Amgen (AMGN), which recently won its case to extend the patent life of rheumatoid arthritis biological Enbrel against Novartis AG’s (NOVN) biosimilar arm Sandoz. Since each extra hour added to patent life means millions of dollars (and sometimes billions) in sales, the additional 10 years of exclusivity for Enbrel is a massive victory for Amgen.

In a recent study released by Evaluate Pharma, Enbrel was ranked third in the top 10 biggest sellers up to 2024. The forward-looking consensus projection anticipates Amgen’s golden goose to hit roughly $140 billion in total revenues in five years – a truly impressive performance particularly for a drug that has been around for more than 20 years. However, Enbrel’s longevity pales in comparison to the other behemoths in the biopharma realm.

Up until 2018, Pfizer’s (PFE) Lipitor held the title of earning the highest lifetime sales in the industry. Since its launch in 1997, the cholesterol drug has raked in $164.4 billion in revenues so far with the number estimated to reach $180 billion by 2024. Lipitor’s success is highlighted more by the fact that it's under a small molecule status and holds approval for a very narrow indication.

Overtaking Lipitor to take the top spot is AbbVie’s (ABBV) rheumatoid arthritis treatment Humira, which closed with $20 billion in sales in 2018 alone. While some AbbVie investors frown upon the over-reliance of the company on Humira, it appears that the efforts to protect the drug has paid off big time.

With patent protection (132 approved patents!) safeguarding its exclusivity in the market, Humira is projected to reach a total of $240 billion in revenues by 2024. Clearly, the rewards they’ve been reaping show no signs of abating anytime soon.

More importantly, Humira’s robust sales, which makes up almost 70% of the company’s profits, has provided AbbVie with the financial capacity to finally get out of the shadow of parent company Abbott Laboratories (ABT) and come up with its own pipeline. As it happens, AbbVie’s efforts towards this direction have already started with the massive purchase of Allergan (AGN) for $63 billion this year.

Apart from Lipitor, Humira, and Enbrel, there are three more blockbuster products with sales that hit the $100 billion mark as of 2018 -- a figure that would make Ecuador proud to claim as their annual GDP. These are Roche Holding Ltd. Genussscheine’s (ROG) chemotherapy drug Rituxan, Amgen’s anemia treatment Epogen, and GlaxoSmithKline’s (GSK) asthma medication Advair.

One biopharma bestseller that leapfrogged a lot of other drugs in the market is multiple myeloma medication Revlimid -- aka the drug that built Celgene (CELG). With an entry date of 2008, this drug is the newest one on the list. While Revlimid’s sales are impressive, what’s actually quite exciting is the fact that its projected revenues easily outstrip its already notable sales of $53.69 billion.

By 2024, this Celgene blockbuster is estimated to reach $123.64 billion in sales. There’s a caveat to this though as Revlimid’s success in the years to come is dependent on how Celgene plans to deal with generic competition chomping at the bit and ready to attack once the drug reaches its 2022 patent expiration date.

Another big-ticket drug that might see a bit of a decline in sales soon is from Johnson & Johnson (JNJ). While the company has always been aggressive when it comes to dominating the market for its Crohn's Disease drug Remicade, an investigation by the Federal Trade Commission (FTC) might put a damper on things soon. According to recent reports, JNJ has been suspected of contracting payers to ensure market control and stave off competitors.

Meanwhile, the three horsemen of Roche, namely, Rituxan, cancer and eye disease medication Avastin, and breast cancer treatment Herceptin, reached a collective amount of $365 billion in total sales. These three are anticipated to stay put on top of the industry in the next five years as well, thanks to their competitive pricing and aggressive strategies to protect their patents.

Rounding out the list is Amgen’s Epogen, which is expected to add $107.90 billion to the already astounding $115.87 billion it generated for the company. Meanwhile, GSK’s Advair, which brought in $113.61 billion, is expected to pour in an additional $104.20 billion by 2024.

Interestingly, the majority of the top 10 franchise drugs are biologics except for Sanofi’s (SAN) ulcer treatment Zantac, Bristol-Myers Squibb Co’s (BMY) heart medication Plavix, Advair, and of course, Lipitor. In fact, this is considered as the primary reason for their capability to fight off potential copycats for years.

In some cases, their monopoly of the market has allowed them to expand to include various other indications in their coverage. The massive sales of biologics are also rooted in their ability to demand big-ticket reimbursements. Unlike their generic competitors, brand recognition alone makes it more convenient for patients to ask for compensation.

Needless to say, the success stories of these drugs make it quite obvious why these biopharma companies employ a battalion of legal experts to fend off the rise of generics. While the onslaught of biosimilars cannot be helped, these lawyers ensure that patients opting for these versions of the medication would find it incredibly difficult to ask for biosimilar reimbursements.

Global Market Comments

July 17, 2019

Fiat Lux

SPECIAL BIOTECH ISSUE

Featured Trade:

(FIVE BIOTECH STOCKS TO BUY AT THE BOTTOM),

(SPY), (VRTX), (JNJ), (ISRG), (CELG), (BMY), (AMGN), (ILMN)