Mad Hedge Technology Letter

August 16, 2023

Fiat Lux

Featured Trade:

(CORD CUTTING IS TAKING OVER)

(NFLX), (GOOGL), (AMZN), (CMCSA), (DIS)

Mad Hedge Technology Letter

August 16, 2023

Fiat Lux

Featured Trade:

(CORD CUTTING IS TAKING OVER)

(NFLX), (GOOGL), (AMZN), (CMCSA), (DIS)

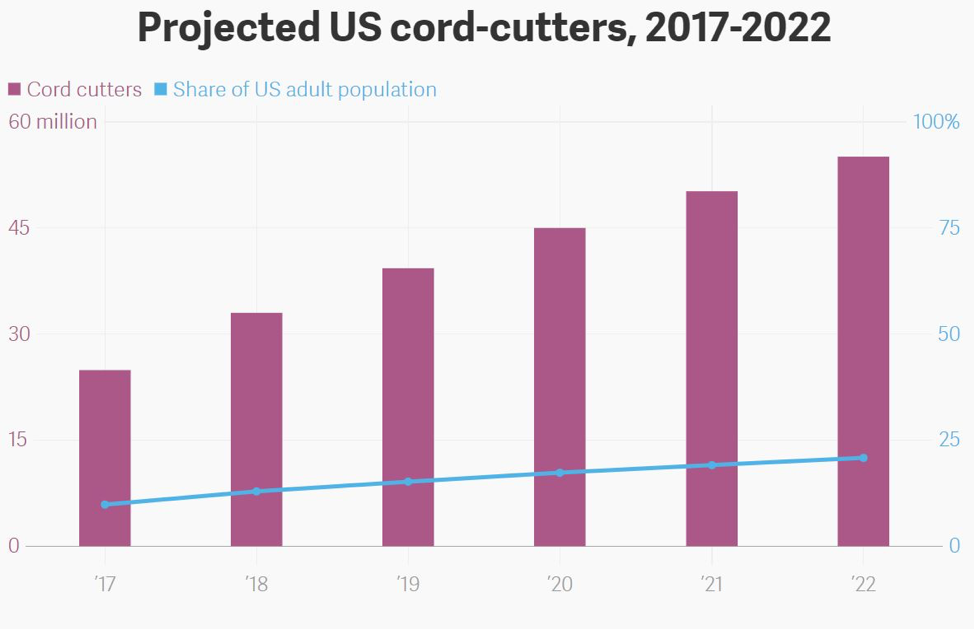

Cord-cutting is going into overdrive as linear TV viewership has just fallen below 50% nationally in July for the first time.

Big changes are about to happen.

This has major ramifications for not only the tech sector but for the broader economy, society, and geopolitics.

We are here to talk about the tech and the sinking of linear TV does mean relative gains for online streamers.

Broadcast and cable each hit a new low of 20% and 29.6% of total TV usage, respectively, to combine for a linear television total of 49.6%.

Has the quality of linear TV channels soured in quality or what is the deal?

It could be a functional reason, as Baby Boomers are watching linear tv because they haven’t figured out the streaming thing yet.

The ease of flipping on the tv with a remote cannot be understated.

In the future, the result is that linear tv penetration will be down to 20% level in around 20 years.

The players that will begin advancing further center stage into the national consciousness are YouTube (GOOGL), Netflix (NFLX), and Amazon Prime Video (AMZN).

They saw month-over-month viewership increases of 5.6%, 4.2%, and 5%, respectively, in July.

Don’t expect a rebound, because linear tv is bleeding viewers reflecting how bad TV channels have become.

Ad revenue across our media network coverage fell 13% on average in Q2, down from -8% in 1Q, which included the Super Bowl.

That being said, certain streamers haven’t exactly cracked the code either, as Peacock, Disney+, Hulu, ESPN+, Paramount+, Max and Discovery+ were down by about 500,000 combined.

However, on the whole, subscriber growth was 8.5% year-over-year with highlights like Netflix adding 5.9 million subscribers in the second quarter.

Comcast's Peacock (CMCSA) was able to grow its subscriber base 84% year-over-year to 24 million, up from the prior 13 million, as the streamer works to catch up to its peers amid a significant lag.

Direct-to-consumer advertising (DTC) grew 27% on average across media companies including Disney (DIS), Comcast, Warner Bros. Discovery (WBD), and Paramount (PARA). That's double from the 13% growth posted in the first quarter.

Comcast is the farthest behind, as only 14% of its estimated revenues are expected to come from DTC in 2024 with the other 85% stemming from its linear networks. Disney is the farthest along, with DTC revenue expected to surpass linear network revenue for the first time in 2024.

As linear tv is headed to the dustbin of history, streaming is also getting more expensive.

Personally, that is what I have seen as many platforms are starting to push the $100 plus per month level.

Many might remember when streaming was $20-$40 per month.

Therefore, I am not surprised to see single-digit growth for streaming as high prices crimps demand.

It’s true that mass media is fracturing into different niches and communities and that isn’t so fantastic for big media corporations as it could mean higher costs and a smaller total addressable audience.

I still do believe there is growth in streaming but not at the elevated levels like the 20% or 30% range.

Customer acquisition will also become more difficult and expensive as people really need to be convinced to move platforms or online channels.

The golden age of streaming growth is over and now each inch will be fought tooth and nail by more competition.

In the short term, I believe a dip in CMCSA should be bought, as they are still driving users to the Peacock platform. NFLX is still worth a trade on the dip as well, but I would avoid DIS until they structurally upgrade the company.

Mad Hedge Technology Letter

March 15, 2023

Fiat Lux

Featured Trade:

(THE UNKNOWN IN THE DIGITAL AD SPACE)

(NFLX), (WBD), (DIS), (CMCSA), (ROKU)

The uncertain digital advertising environment has been a thorn in the side of legacy media giants for quite some time.

Companies from Comcast (CMCSA) to Warner Bros. Discovery (WBD) are feeling the pressure as profitability struggles pile up.

Unfavorable macroeconomic headwinds coupled with decreased ad budgets amid a decline in linear TV and digital search trends put the ad market through the wringer in 2022.

Recent ad market softness comes as media giants like Disney (DIS) and Netflix (NFLX) have embraced ad-supported streaming alternatives as the race for eyeballs escalate.

Disney's direct-to-consumer division lost an eye-popping $4 billion-plus in 2022.

Warner Bros Discovery is now targeting $4 billion in cost savings over the next two years.

Advertising revenue within NBCUniversal's media division increased by 4% in Q4 because of a boost from the incremental revenue from the FIFA World Cup.

Looking ahead, the lack of brand name events in 2023 such as the World Cup, Olympics, or U.S. midterm elections, will likely be a drag on ad spend in 2023.

Those events greatly aided the battered industry with the domestic ad market totaling $318 billion last year — an increase of 8% compared to 2021.

Similarly, Spotify (SPOT) CFO Paul Vogel told investors during the latest earnings call: "Advertising in Q4, overall, it's definitely continued to be very up and down."

Spotify's Q4 ad-supported revenue, boosted by podcasting, grew 14% on a year-over-year basis to €449 million — accounting for 14% of total revenue.

Disney and Netflix rolled out their ad tier products at a time when the ad market is in flux, but the move seems to have been a lucrative one.

At the time of the debut, the company said over 100 advertisers bought inventory for the launch — bucking the trend of a global ad spend slowdown.

Similar to Disney, Netflix is playing the long game when it comes to its recently launched ad-supported tier, which officially debuted in November.

In its latest shareholder letter, Netflix said engagement for ad-supported subscribers "is consistent with members on comparable ad-free plans, is better than what we had expected, and we believe the lower price point is driving incremental membership growth."

Investors should run to higher grounds to avoid the upcoming slaughter in legacy media.

The cord cutter phenomenon is real and the pivot to work-from-home culture has really stuck the fork in many traditional services that used to be part of American culture.

Legacy media is one of the big losers – nobody watches analog television anymore.

Investors will need to seek attractive properties such as NFLX to buy the dip.

They benefit from the first mover advantage, but Disney is also finding their way after firing former CEO Bob Chapek and replacing him with the guy before him - Bob Iger. It’s not a pure streaming play which is also an issue for the likes of Amazon and I do think Roku is a little too growth based at this point in the business cycle.

The overall message is to avoid unproven tech assets for the time being with bank turmoil and interest rate tumult.

The only exceptions are active traders who use volatility in their favor and play from the long and short side. Traders usually don’t discriminate and can jump in and out of these sharp movements.

If traders want to get into streaming or social media stocks, that is fine, but stick with the brand names and shun the exotic names for now.

Mad Hedge Technology Letter

December 13, 2019

Fiat Lux

Featured Trade:

(WHY THE FANGS ARE BREAKING INTO YOUR HOME)

(GOOGL), (AAPL), (AMZN), (ALRM), (ADT), (ARLO), (RESI), (PANW), (CRWD), (FTNT), (CSCO), (CMCSA), (BBY)

The house is the new smartphone and I will tell you why.

The projected market growth of 18% in smart home technology sales according to Acumen Researching and Consulting will deliver opportunities to shape and prioritize this sector.

The revenues up for grabs from the smart home mean that internet of things’ (IoT) companies will create systems that mesh together with the bare minimum human participation, meaning that tech will have a dramatic influence in our daily lives.

I get several moans and groans a day that the Mad Hedge Technology Letter only shines the spotlight on the FANGs.

But it is hard not to when it comes to the future of the home.

Just look at recent M&A activity.

Automation and connected smart appliances have consumed Amazon by recently acquiring Eero, producer of routers for apartments, houses, and multi-story homes, and after already paying $1 billion to acquire Ring, a doorbell-camera startup. It had also bought Blink, a smart camera maker in 2017.

Google hasn’t shied away either by investing in smart home products pocketing Nest, a firm producing smart home products, for $3.2 billion.

Nest took a few years to sort out its production phase but finally managed to launch new temperature sensors, a video doorbell, and an outdoor smart camera.

What are the trending IoT products now?

The flavors of the day are smart lights, security, entertainment systems, and temperature control.

They are the low hanging fruit of the smart home industry – a de facto gateway into this world.

Most of these smart devices operate with voice assistants, but because of the nature of competition, certain products are aligned with certain ecosystems and compatibility issues will persist until the competition flushes itself out.

A layman’s example would be Apple’s Homekit dovetailing nicely with Apple’s Siri.

Companies are in the first innings of the product iteration cycle and the variations of smart home products are endless stemming from showers that remember preferred water temperature and flow rates or climate-control systems that change in real-time to suit the user.

Security of home networks and connected devices are still a controversial question mark because the receiver of this type of data has the keys to the most intimate details of personal lives.

Even avid technologists are hesitant to dive in and put up smart home products all over the house, and most are being cautious.

In fact, privacy issues are the most distinct headwind to fresh adoption rates.

Many people simply aren’t willing to make the jump yet until they are more convinced of its use case.

Even with all the reservations, an alternative global shipment company believes smart home devices will post 24% in growth next year.

For the smart home device believers, this cohort averages 6 smart home devices per household and will certainly rise to 7 or 8 by the end of 2020.

Popular items include the Amazon Echo, Google Home, and Apple (AAPL) HomePod.

Smart speakers are already present in 36% of American homes and rising.

Consumers are also worried about technology invading their daily lives along with allowing artificial intelligence to dominate personal decision making.

Others have concluded that items such as smart microwaves are a waste of money and are unneeded when analog devices function admirably.

Another legitimate reason is that the software and technology involve a perceived steep learning curve to operate which many people do not have the patience for.

And some are just burnt out by the volume of technology thrown in our faces.

Who wants to operate 50 apps on their phone to control their smart home devices when there are other pressing needs in life?

Companies with skin in the game are Alarm.com (ALRM), ADT (ADT), Arlo Technologies (ARLO) and Resideo Technologies (REZI) and they will be outsized winners if they can solve many of the industries lingering issues.

The value thesis in the case of home automation companies is that they are financially efficient, time-effective, boost wellness and will be easy to use.

About 11% of U.S. broadband households have smart thermostats and Nest’s smart thermostat is the most popular.

Networked security cameras by Arlo are in 10% of homes.

Video doorbells from Amazon.com (AMZN), Google are in 8% of homes and help deter theft of e-commerce packages.

Smart light bulbs and lighting are at 8% market share while smart door locks are at 7% penetration.

There are several second derivates bet on this as well.

The most common user interface for the smart home is apps on a smartphone or tablet and voice commands to smart speakers are second.

The conundrum of installation complexities leads to the demand of professional installers.

This demand has delivered opportunities for companies like Comcast's (CMCSA) Xfinity and Vivint.

Electronics retailer Best Buy (BBY) has stepped up its footprint in this market as well.

Another stock play would be cybersecurity companies because they will win contracts protecting the software that smart home products rely on.

Hackers are getting more sophisticated and a private cybersecurity company Firewalla can track where data is flowing to and from your devices.

Firewalla management recommends buying devices from reputable home automation companies like Amazon and Google because they have more accountability and are of higher quality.

There will be a huge onramp of cybersecurity contracts doled out to the likes of Palo Alto Networks, Inc. (PANW), CrowdStrike Holdings, Inc. (CRWD), Fortinet, Inc. (FTNT), and Cisco Systems, Inc. (CSCO).

We are in the first mile of a marathon and smart home product manufacturers, cybersecurity companies, 5G internet, and semiconductor companies will all benefit from the broad-based integration of these next-generation home consumer products.

Mad Hedge Technology Letter

August 7, 2019

Fiat Lux

Featured Trade:

(CORD-CUTTING IS ACCELERATING)

(DIS), (T), (NFLX), (CMCSA)

Cord-cutting is picking up steam – that is the last thing traditional media want to hear.

There are several foundational themes that this newsletter has glued onto readers' foreheads.

The generational pivot to cloud-based media is one of them.

It’s easy to denominate this phenomenon down to Netflix (NFLX) but in 2019, this trend is so much more than Netflix.

E-marketer published a survey showing that cord-cutters will surpass 20% of all U.S. adults by the end of 2019.

The rapid demise of traditional television has been equally as mind-numbing with the 100.5 million subscribers in 2014 turning into 86.5 million subscribers today.

Comcast (CMCSA) has tried to buck the trend by homing in on fast broadband internet, but that strategy can only go so far.

Disney (DIS), WarnerMedia, and NBCUniversal Disney have really gotten their ducks in a row and are on the verge of launching their own unique streaming services.

Disney's service entails a 3-segment strategy bringing in Hulu and ESPN Plus to the Disney fold.

The Disney service will revolve around family content at its core so don’t expect Game of Thrones lookalikes.

WarnerMedia's hopes to cash in on its HBO brand while peppering it with original series and programming from Warner Bros. and DC.

Disney will be able to lean on family brands of Marvel, Star Wars, and Pixar, and newly acquired National Geographic.

Marvel Cinematic Universe is a growth asset pumping out more than $22 billion at the box office across 23 movies.

Disney Plus will also have a solid collection of Disney films to play with, which could make it indispensable to parents and comes with no ads making it even more appealing to kids.

Disney will also deploy some mix of bundles to diversify its offerings and personalize services for viewers who do not want its entire lineup of content.

The soon-to-be HBO Max will implement HBO original content along with WarnerMedia brands like Warner Bros., DC Entertainment, TBS, TNT, and CNN.

HBO Max will have a treasure trove of old Warner Bros. movies and TV shows, like "Friends" and "The Fresh Prince of Bel Air," that has played extremely well on Netflix.

HBO will get those titles back at the end of 2019.

HBO has also tied up with BBC Studios to stream "Doctor Who."

"You should assume that HBO Max will have live elements," said Randall Stephenson, chairman and CEO of AT&T, on the company's second quarter conference call.

This roughly translates into HBO Max snapping up live sports and music events to complement scripted content.

This is something that Netflix has shied away from and live events are best monetized through live ads.

The last big label service to go into effect is NBC’s yet to be named streaming service.

NBCUniversal will have the luxury of offering their cable subscribers a chance to pivot to an in-house online streaming service making the move seamless.

At first, the 21 million US cable-TV subscribers will receive the streaming content for free.

Some of the assets that will trot out on the NBC platform are "The Office," because NBC is removing it from Netflix for 2021.

As cord-cutters hasten their move to streaming, this trio of loaded content-creating firms will benefit as long as they maintain a high quality of content and the pipeline to please fidgety consumers.

Global Market Comments

April 3, 2019

Fiat Lux

Featured Trade:

(WHO WILL BE THE NEXT FANG?)

(FB), (AMZN), (NFLX), (GOOGL), (AAPL),

(BABA), (TSLA), (WMT), (MSFT),

(IBM), (VZ), (T), (CMCSA), (TWX)

FANGS, FANGS, FANGS! Can’t live with them but can’t live without them either.

I know you’re all dying to get into the next FANG on the ground floor, for to do so means capturing a potential 100-fold return, or more.

I know because I’ve done it four times. The split adjusted average cost of my Apple shares is only 25 cents compared to today’s $174, so you can understand my keen interest. My average on Tesla is $16.50.

Uncover a new FANG and the riches will accrue rapidly. Facebook (FB), Amazon AMZN), Netflix (NFLX), and Alphabet (GOOGL) didn’t exist 25 years ago. Apple (AAPL) is relatively long in the tooth at 40 years. And now all four are in a race to become the world’s first trillion-dollar company.

One thing is certain. The path to FANGdom is shortening. It took Apple four decades to get where it is today, Facebook did it in one. As Steve Jobs used to tell me when he was running both Apple and Pixar, “These overnight successes can take a long time.”

There is also no assurance that once a FANG always a FANG. In my lifetime, I have seen far too many Dow Average components once considered unassailable crash and burn, like Eastman Kodak (KODK), General Electric (GE), General Motors (GM), Sears (SHLD), Bethlehem Steel, and IBM (IBM).

I established in an earlier piece that there are eight essential attributes of a FANG, product differentiation, visionary capital, global reach, likeability, vertical integration, artificial intelligence, accelerant, and geography.

We are really in a “What have you done for me lately” world. That goes for me too. All that said, I shall run through a short list for you of the future FANG candidates we know about today.

Alibaba (BABA)

Alibaba is an amalgamation of the Chinese equivalents of Amazon, PayPal, and Google all sewn together. It accounts for a staggering 63% of all Chinese online commerce and is still growing like crazy. Some 54% of all packages shipped in China originate from Alibaba.

The juggernaut has over half billion active users, and another half billion placing orders through mobile phones. It is a master of AI and B2B commerce. There is nothing else like it in the world.

However, it does have some obvious shortcomings. Its brand is almost unknown in the US. It has a huge problem with fakes sold through their sites.

It also has an ownership structure for foreign investors that is byzantine, to say the least. It is a contractual right to a share of profits funneled through a PO box in the Cayman Island. The SEC is interested, to say the least.

We also don’t know to what extent founder Jack Ma has sold his soul to the Beijing government. It’s probably a lot. That could be a problem if souring trade relations between the US and the Middle Kingdom get worse, a certainty with the current administration.

Tesla (TSLA)

Before you bet on a new startup breaking into the Detroit Big Three, go watch the movie “Tucker” first. Spoiler Alert: It ends in tears.

Still, Tesla (TSLA) has just passed the 270,000 mark in the number of cars manufacturered. Tucker only got to 50.

Having led my readers into the stock after the IPO at $16.50, I am already pretty happy with this company. Owning three of their cars helps too (two totaled). But Tesla still has a long way to go.

It all boils down to the success of the $35,000, 200-mile range Tesla 3 for which it already has 500,000 orders. So far so good.

It’s all about scale. If it can produce these cars in sufficient numbers, it will take over the world and easily become the next FANG. If it can’t, it won’t. It’s that simple.

To say that a lot is already built into the share price would be an understatement. Tesla now trades at ten times revenues compared to 0.5 for Ford (F) and (General Motors (GM). That’s a relative overvaluation of 20:1.

Any of a dozen competing electric car models could scale up with a discount model before they do, such as the similarly priced GM Bolt. But with a ten-year lead in the technology, I doubt it.

It isn’t just cars that will anoint Tesla with FANG sainthood. The firm already has a major presence in rooftop solar cell installation through Solar City, utility sized solar plants, industrial scale battery plants, and is just entering commercial trucks. Consider these all seeds for FANGdom.

One thing is certain. Without Tesla, there wouldn’t be s single mass-market electric car on the road today.

For that, we can already say thanks.

Uber

In the blink of an eye, ride sharing service Uber has become essential for globe-trotting travelers such as myself.

Its 2 million drivers completely disrupted the traditional taxi model for local transportation which remains unchanged since the days of horses and buggies.

That has created the first $75 billion of enterprise value. It’s what’s next that could make the company so interesting.

It is taking the lead in autonomous driving. It could also replace FeDex, UPS, DHL, and the US post office by offering same day deliveries at a fraction of the overnight cost.

It is already doing this now with Uber Foods which offers immediate delivery of takeouts (click here if you want lunch by the time you finish reading this piece.)

UberCopters anyone? Yes, it’s already being offered in France and Brazil.

Uber has the potential to be so much more if it can just outlive its initial growing pains.

It is a classic case of the founder being a terrible manager, as Travis Kalanick has lurched from one controversy to the next. The board finally decided he should spend much time on his new custom built 350-foot boat.

Its “bro” culture is notorious, even in Silicon Valley.

It is also getting enormous pushback from regulators everywhere protecting entrenched local interests. It has lost its license in London, the only place in the world that offered a decent taxi service pre-Uber. Its drivers are getting beaten up in Paris.

However, if it takes advantage of only a few of the doors open to it, status as a FANG beckons.

Walmart (WMT)

A few years ago, I was heavily criticized for pointing out that half the employees at my local Walmart (WMT) were missing their front teeth. They have since received a $2 an hour's pay raise, but the teeth are still missing. They don’t earn enough money to get them fixed.

The company is the epitome of bricks and mortar in a digital world with 12,000 stores in 28 countries. It is the largest private employer in the US, with 1.4 million workers, mostly earning minimum wage.

The Walmart customer is the very definition of the term “late adopter.” Many are there only because unlike Amazon, Wal-Mart accepts cash and Food Stamps.

Still, if Walmart can, in any way, crack the online nut, it would be a turbocharger for growth. It moved in this direction with the acquisition of Jet.com for $3 billion, a cutting-edge e-commerce firm based in Hoboken, NJ.

However, this remains a work in progress. Online sales account for only 4% of Walmart’s total. But they could only be a few good hires at the top away from success.

Microsoft (MSFT)

Talk about going from being the 800-pound gorilla to an 80 pound one, and then back to 800 pounds.

I don’t know why Microsoft (MSFT) lost its way for 15 years, but it did. Blame Bill Gates’s retirement from active management and his replacement by his co-founder Steve Ballmer.

Since Ballmer’s departure in 2014, the performance of the share price has been meteoric, rising by some 125% over the past two years.

You can thank the new CEO Satya Nadella who brought new vitality to the job and has done a complete 180, taking Microsoft belatedly into the cloud.

Microsoft was never one to take lightly. Windows still powers 90% of the world’s PCs. No company can function without its Office suite of applications (Word, Excel, and PowerPoint). SQL Server and Visual Studio are everywhere.

That’s all great if you want to be a public utility, which Microsoft shareholders don’t.

LinkedIn, the social media platform for professionals, could be monetized to a far greater degree. However, specialization does come at the cost of scalability.

It seems that the future is for Microsoft to go head to head against next door neighbor Amazon (AMZN) for the cloud services market while simultaneously duking it out with Alphabet (GOOGL).

My bet is that all three win.

Airbnb

This is another new app that has immeasurably changed my life for the better. Instead of cramming myself into a hotel suite with a wildly overpriced minibar for $600 a night, I get a whole house for $300 anywhere in the world, with a new local best friend along with it.

Overnight, Airbnb has become the world’s largest hotel chain without actually owning a single hotel. At its latest funding round in 2017, it was valued at $31 billion.

The really tricky part here is for the firm to balance out supply and demand in every city in the world at the same time. It is also not a model that lends itself to vertical integration. But who knows? Maybe priority deals with established hotels are to come.

This is another firm that is battling local regulation, that great barrier to technological innovation. None other than its home town of San Francisco now has strict licensing requirements for renters, a 30 day annual limitation, and a $1,000 a day fine for offenders.

The downtowns of many tourist meccas like Florence, Italy and Paris, France have been completely taken over by Airbnb customers, driving rents up and locals out.

IBM (IBM)

There was a time in my life when IBM was so omnipresent we thought like the Great Pyramids of Egypt it would be there forever. How times change. Even Oracle of Omaha Warren Buffet became so discouraged that he recently dumped the last of his entire five-decade long position.

A recent 20 consecutive quarters of declining profits certainly hasn’t helped Big Blue’s case. It is one of the only big technology companies whose share price has gone virtually nowhere for the past two years.

IBM’s problem is that it stuck with hardware for too long. An entrenched bureaucracy delayed its entry into services and the cloud, the highest growth areas of technology.

Still, with some $80 billion in annual revenues, IBM is not to be dismissed. Its brand value is still immense. It still maintains a market capitalization of $144 billion.

And it has a new toy, Watson, the supercomputer named after the company’s founder, which has great promise, but until now has remained largely an advertising ploy.

If IBM can reinvent itself and get back into the game, it has FANG potential. But for the time being, investors are unimpressed and sitting on their hands.

The Big Telecom Companies

My final entrant in the FANGstakes would be any combination of the four top telecommunication companies, Verizon (VZ), AT&T (T), Comcast (CMCSA), and Time Warner (TWX), which now control a near monopoly in the US.

There is a reason why the administration is blocking the AT&T/Time Warner merger, and it is not because these companies are consistently cited in polls as the most despised in America. They are trying to stop the creation of another hostile FANG.

Still, if any of the big four can somehow get together, the consequences would be enormous. Ownership of the pipes through which the modern economy courses bestows great power on these firms.

And Then….

There is one more FANG possibility that I haven’t mentioned. Somewhere, someplace, there is a pimple-faced kid in a dorm room thinking up a brand-new technology or business model that will take the world by storm and create the next FANG.

Call me crazy, but I have been watching this happen for my entire life.

I want to thank my friend, Scott Galloway, of New York University’s Stern School of Business, for some of the concepts in this piece. His book, “The Four” is a must read for the serious tech investor.

Creating the Next FANG?