Global Market Comments

August 16, 2024

Fiat Lux

Featured Trade:

( AUGUST 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (CMG), (SBUX), (TLT), (CCI),

(FCX), (SLRN), (DAL), (TSLA), (LRCX)

Global Market Comments

August 16, 2024

Fiat Lux

Featured Trade:

( AUGUST 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (CMG), (SBUX), (TLT), (CCI),

(FCX), (SLRN), (DAL), (TSLA), (LRCX)

Below please find subscribers’ Q&A for the August 15 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from London, England

Q: Do you think we’ll still have another significant test of the lows for the year, or was that it last week? Stocks are rebounding huge this week.

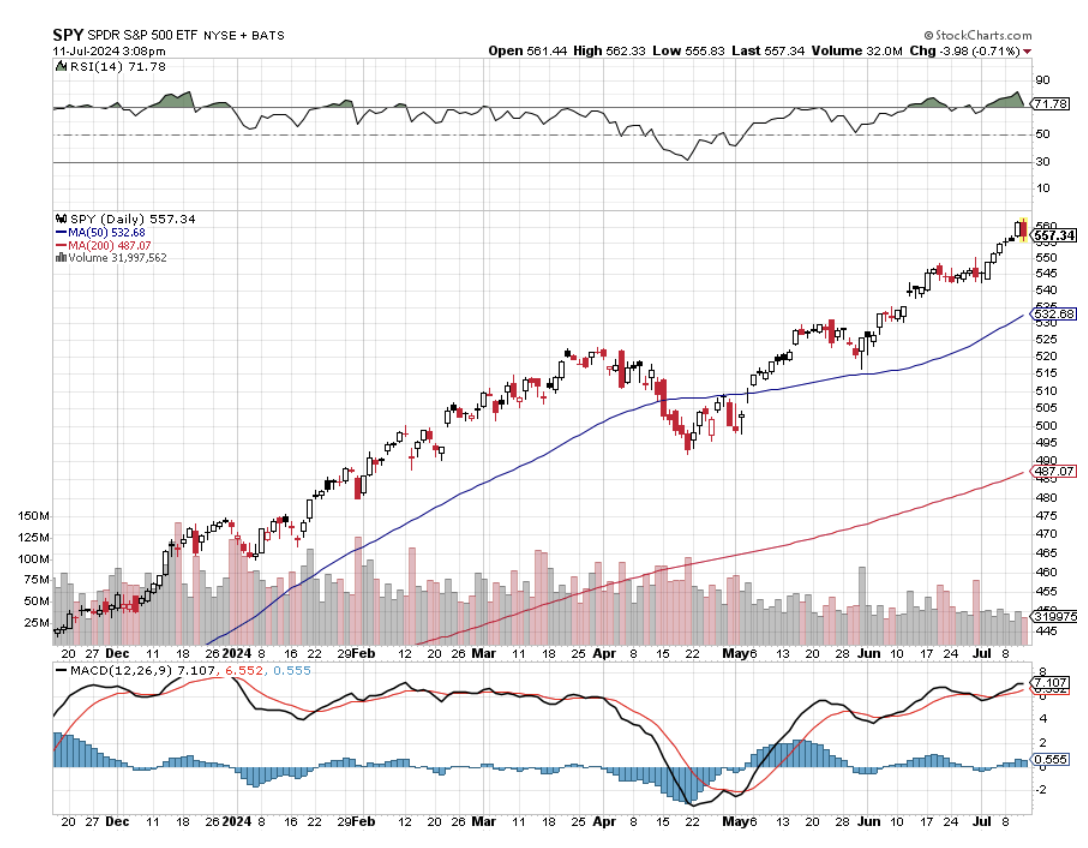

A: They never really went down very much. The average drawdown IN THE S&P 500 (SPY) in any given year is 15%. We only got a 10% drawdown this month because there is still $8 trillion dollars in cash sitting under the market, which never got into stocks. All of this year it's been waiting for a pullback, so I was kind of surprised we even got 10%. I was forecasting maybe 6%. So could we get a new low? You never discount the possibility, but we really have to have another shocking data point to get down to a 15% correction. That is exactly what triggered this sell-off with the Nonfarm Payroll we got in early July. So give me another rotten Nonfarm Payroll report, and we could be back at last week's lows. Which is why I'm 100% cash. I want to have tons of dry powder, if and when that happens.

Q: We've seen a big increase in refi’s for homes in the last week. Is this going to be positive for the economy?

A: Absolutely yes, and that's why we're not going to have a recession. You get housing back into the economy which has been dead meat for almost 3 years now, and suddenly one quarter to one-third of the economy recovers. So that's what takes us into probably 3% economic growth for another year in 2025.

Q: What do you think of the Chipotle CEO (CMG) moving to take over Starbucks (SBUX)?

A: I think it's a very positive move. Starbucks was dead in the water. Their stores are old and dirty and products need refreshing. So if anyone needs a fresh view it's Starbucks, and the guy from Chipotle has a spectacular track record. Chipotle is probably one of the more successful fast-food companies out there. I usually don't ever play fast food—the margins are too low, but I certainly like to watch the fireworks when they happen.

Q: Should I be shorting airline stocks here like Delta Airlines (DAL), now that a recession risk is on the table?

A: Absolutely not. If anything, airlines are a buy here. They've had a major sell-off over the last 3 months for many different reasons, not the least of which was the software crash that they had a month ago. This is not shorting territory. That was 3 months ago for the airlines. Just because it's gone down a lot doesn't mean you now sell, it's the opposite. You should be buying airlines. I usually avoid airlines because they never have any idea if they're going to make money or not, so it's a very high-risk industry, and the margins are shrinking. Let me tell you, the airlines in Europe are absolutely packed. The fares are rock bottom and the service is terrible. Anybody who thinks the consolidation of the airline industry brought you great service has got to be out of their mind.

Q: Do you have any rules on when you stop loss?

A: The answer is very simple. If I do call spreads, whenever we break the nearest strike price, I'm out of there. That’s where the leverage works exponentially against you. Usually, you get a 1 or 2% loss when that happens, and you want to roll it into another trade as fast as you can and make the money back. Sometimes you have to do three trades to make up one loss because when you issue stop losses, everybody else is trying to get out of there at the same time. It's not a happy situation to be in, so we try to keep them to a minimum—but that is the rule of thumb. Keep your discipline. Hoping that it can recover your costs is the worst possible investment strategy out there. Hoping is not a winning strategy.

Q: Why don't you wait for the bottom?

A: Because nobody knows where the bottoms are. All you can do is scale. When you think things are oversold, when you think things are cheap, then you start buying things one at a time unless you get these giant meltdown days like we got on August 5th. So that's what I probably will be doing, is scaling in on the weak days on stocks that have the best fundamentals. That’s the only way to manage a portfolio.

Q: Is it a good time to buy REITs for income?

A: Absolutely. REITs are looking at major drops in interest rates coming. That will greatly reduce their overheads as they refi, and of course, the recovering economy is good for filling buildings. So I've been a very strong advocate of REITs the entire year, and they really have only started to pay off big time in the last month, and Crown Castle Inc (CCI) is my favorite REIT out there.

Q: I own Freeport McMoRan (FCX). Do you think China’s problems will make FCX a sell?

A: Not a sell, but a wait. China (FXI) is delaying any recovery in a bull market. If we get another move in (FCX) down to the thirties I would double up, because eventually American demand offsets Chinese weakness, and we’ll be back in a bull market on the metals. It's American demand that is delivering the long-term bull case for copper, not the return of Chinese construction demand, which led to the last bull market. So we really are changing horses as the main driver of the demand for copper. It still takes 200 pounds of copper to make an EV whose sales are growing globally.

Q: Is it time to buy (TLT) now?

A: No, the time to buy (TLT) was at the beginning of the year, seven months ago, three months ago, a month ago. Now we've just had a really big $12 point rally, and really almost $18 points off the bottom. I would wait for at least a 5-point drop-in (TLT) before we dive back into that. If you noticed, I haven't been doing any (TLT) trades lately because the move has been so extended. And in fact, if they only cut a quarter of a point in September, then you could get a selloff in (TLT), and that'll be your entry point there. You have to ditch your buy high, sell low mentality, which most people have.

Q: What bond should I buy for a 6 to 10-year investment?

A: I’d buy junk bonds. Junk bonds have always been misnamed, or I would buy some of the high-yield plays like the BB loans (SLRN). With junk bonds, the actual default rate even in a recession, only gets to about 2%. So it certainly is worth having. I still think they're yielding 6 or 7% now, so that's where I would put my money. Or you can buy REITs which also have similarly high yields, like the (CCI), which is around 5% now. Risks in both these sectors are about to decline dramatically.

Q: Will there be an inflation spike next year?

A: No. Technology is accelerating so fast it's wiping out the prices of everything that's highly deflationary, and that pretty much has been the trend over the last 40 years. So don't expect that to change. The post-COVID inflationary spike was a one-time-only event, which then ended two years ago. We've gone from a 9% down to a 2.8% inflation rate; unless we get another COVID-induced inflation spike, there's no reason for inflation to return. Deflation is going to be the next game.

Q: What do you think of the UK economy now that you're in London?

A: Awful! Brexit was the worst thing that happened to England—that's why it was financed by the Russians. Brexit will have the effect of dropping both the economic growth rate and standards of living by half over the next 20 years. Expect England to beg their way back into Europe sometime in the future, although I may not live long enough to see it. There are no English people in London anymore. It's all foreigners. No one can afford it.

Q: Should I leap on Tesla (TSLA) where the current price is?

A: No. We’re waiting for the nuclear winter in EVs to end—no sign of it yet. And unfortunately, Elon Musk is scaring away buyers, especially in blue states, by palling around with Donald Trump, a well-known climate change denier. What's in that relationship? I have no idea. One of the first things Trump did was to dump subsidies for electric cars last time he was president. It's hard to tell who’s gone crazier, Trump or Musk.

Q: I have an empty portfolio, when should we expect your options trade to start coming in again?

A: As soon as I see a great sell-off or a great individual situation like we got a couple days ago with the Mad Hedge Technology Letter in Lam Research (LRCX). That's what we look for all day, every day of the year. There's no point in trading for the sake of trading, that only makes your broker rich, not you. There's no law that says you have to have a trade every day, and actually having cash isn't so bad these days. They're still paying 5% for 90-day T Bills. If you don’t know what T Bills are, look up 90-day T bills on my website.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

July 11, 2024

Fiat Lux

Featured Trade:

(JULY 10 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (NVDA), (COPX), (CMG), (TLT), (TBT)

Below please find subscribers’ Q&A for the July 10 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village NV.

Q: Is the Fed waiting too long to cut interest rates?

A: Yes, they are. We are on a recession track if the Fed doesn’t move soon. In other words, the light at the end of the tunnel isn’t daylight—it’s an oncoming train. So, I think a September rate cut is a certainty. They want to see tomorrow’s data and make sure it’s cool. They need several months of really cool inflation data to justify the first rate cut and we probably are going to get that, so next update is tomorrow with the latest CPI number is crucial. Everybody’s sitting on their hands until then.

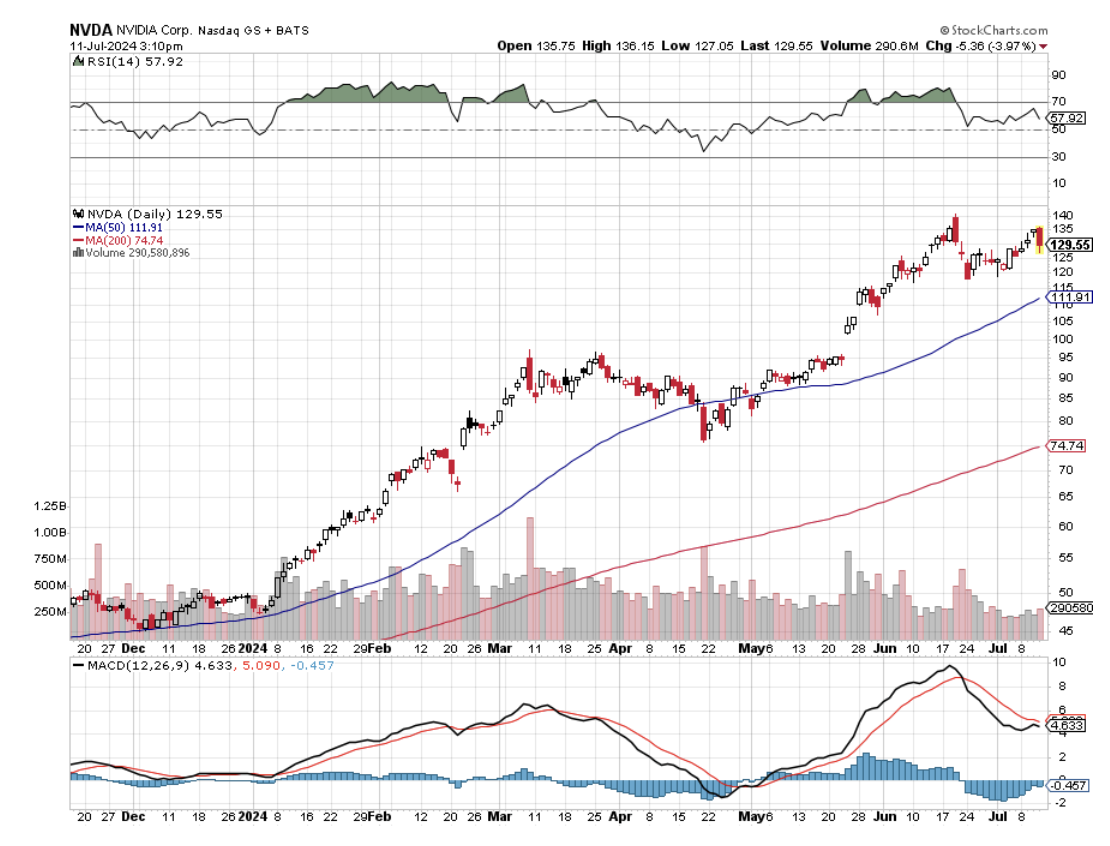

Q: When will NVIDIA (NVDA) hit a $4 trillion market valuation?

A: By the end of the year. We’re currently at $3.3 trillion, so another $700 billion is nothing for NVIDIA—you could do that in a day if you really wanted to. But give it until the end of the year, just to be conservative. The fact is, they have a global monopoly on the highest-priced product that everybody in the world has to buy or go out of business. It’s not a bad place to be—it’s kind of like where John D. Rockefeller was in the oil industry around 1900.

Q: What do you think about copper (COPX)? Should I maintain my longs?

A: Yes, all we need is further proof of falling interest rates and the entire commodities/precious metals sectors will take off like a rocket. So just sit with your positions. I put out a piece yesterday on copper. All that shines is not Copper, and it’s not dead it’s just resting, like the proverbial John Cleese parrot.

Q: Do you think a 10% stock market correction is likely before the election?

A: No, the most we’ve been able to get this year is 4% or 5% pullbacks, but not much more. We have a world with a cash glut that is underinvested in the face of a global monetary easing. Investors have been net sellers of stocks all of last year, so we were ripe for a meltup, which has, in fact, happened every day so far in July. So no, my S&P 500 target of 6,000 for the end of the year is starting to look too conservative given the moves that we’ve made lately. I’m very positive about that.

Q: Is the real estate market about to crash?

A: Well, the Florida housing collapse that is being driven by the insurance industry feeing that state. Insurance companies don’t like the hurricane risk going forward, which can cost tens of billions of dollars per event. Nobody there can get insurance anymore unless they pay outrageous amounts of money. Some people are only buying fire insurance to save money and skipping the storm insurance and rolling the dice, hoping the storms hit somewhere else in Florida. The fact is, you can’t get a home mortgage without insurance. Banks aren't willing to take the environmental risk of a house without insurance. No insurance means no bank loans, which means the market shrinks to a cash-only market. And there is a cash-only market in Florida, but it’s not at the $500,000 level, it’s more at the $50 million level. So that is a problem unique to Florida. Could it spread to other areas? Yes. Texas is having another energy crisis, as it has twice every year, ever since the power system was privatized there. No reserves for emergencies, no contingency, nothing that costs money basically. And then California definitely has a wildfire problem, although we’ve been getting off pretty light last year and this year. But the insurance companies don’t think like that. They are the classic 20/20 hindsight type companies.

Q: What’s the impact of the election on the market?

A: Zero. But it will defer buying until after the election. So if you have a 50/50 split on polls, uncertainty is at a maximum. People don’t like investing in uncertainty, they like sure things. After the election, you can expect a massive melt-up in the market no matter who wins because the uncertainty will be gone, and tech stocks will lead once again.

Q: What should I do with Nvidia (NVDA)?

A: I put out a report on this on Monday. You keep your long and write calls against them. And you can get quite a lot of money for just the August calls. I think the August $140 calls were selling for $3.50—they’re higher than that now, so you could even go out to August $145, and just keep doing that every month. If Nvidia takes off and you get taken out of your stock, you’re selling it essentially at $143.50. So that is an excellent trade—a lot of the big institutions are doing that now.

Q: Tesla's (TSLA) been on a big rally for the past month; do you expect it to continue?

A: I expect it to take a break, but the long-term uptrend is now back for good, for lots of different reasons. The immediate headline reason was because the Chinese government allowed the buying of Teslas for the first time—they are made in China after all. Second, they had a good earnings beat, so this caused a massive short-covering rally. The shorts got crushed by Tesla once again, as they have been consistently doing for the last 15 years, really. I saw a number of cumulative losses on short positions on Tesla stock since inception: $100 billion. Most of those losses were incurred by oil companies trying to put Tesla out of business.

Q: What do you call a substantial dip?

A: It’s different for every stock—for some it’s 2%, for others like Tesla or Nvidia it’s 20%. It depends on the volatility of the stock; you just have to look at the charts and make your own call.

Q: What do you think for the next earnings season?

A: It’ll be great for technology stocks and not so great for domestics as their businesses cool off.

Q: Is there anything Europe and American EV producers can do to compete against the Chinese at these lower prices?

A: Yes: keep quality high, therefore profits high, therefore profit margins high. That was the Japanese strategy in the US from the 1980s onwards, and it was hugely successful. You can cede the money-losing part—the low-end part of the market, to the Chinese. The quality of the Chinese EVs is terrible, they start to fall apart after four years, and I learned this from several Chinese EV drivers in Ecuador where they have a substantial market share already. But at $15,000 plus the shipping, you don’t make a lot of money in EVs.

Q: Is it a good time to buy put LEAPS on the ProShares UltraShort 20+ Year Treasury (TBT)?

A: Yes, especially if you’re willing to do an at-the-money and bet that the interest rates stay here or lower for the next year. You’d probably get a 100% return on that, but why bother? Because on the TBT itself, you have a much wider trading spread than the (TLT), therefore the dealing costs are higher. You might as well just go and do the long (TLT) LEAP instead.

Q: Chipotle Mexican Grill (CMG) stock has been really successful for the last five years, but it just dropped 20%, should I get in?

A: It’s a very low-margin business—I avoid those. There’s not a lot of meat in the burrito business. It doesn’t have the key elements of success. (Not just Chipotle, but with the whole industry.) It's not like you’re designing 96 stock microprocessors.

Q: Are AI stocks overhyped at this point?

A: Absolutely yes, but they can stay overhyped for another three or four years, so I think we're just at the beginning of a very long-term run. And the people who have been involved so far are making the biggest money in their lives.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

McDonald?s (MCD) has always figured large in my life.

I grew up next door to one of the first five stands built in the country, in the Los Angeles metropolitan area. That?s when visionary milkshake mixer salesman, Ray Kroc, started to franchise his revolutionary new ideas for delivering fast food.

One of my fondest childhood memories was when my mother used to take us out to dinner there. At 15 cents a burger you fed seven growing kids for a buck and still had money left over for French fries. We brought our own cokes in an ice chest to save money.

I always gummed up the works by asking for a hamburger that had mustard only and no pickles. I clearly did not fit into the company?s stripped down Speedee Service business model.

In high school, I managed to land a coveted minimum wage job ($1 an hour) under the Golden Arches. I learned first hand the harsh realities of working for a living, and that you didn?t necessarily want to know how the sausage was made.

Then, the Big Mac came out, the blockbuster beef equivalent of a Saturn V rocket. Chicken McNuggets, Egg McMuffins, and Filet of Fish followed (for the Catholics on Fridays), and it seemed the company could do no wrong.

In a few decades, the company grew into the world?s largest restaurant, expanding its list of franchises to a staggering 36,000 shops in 119 countries.

It became the planet?s largest consumer of beef and potatoes in the world. Its presence is ubiquitous on US military bases around the world. Its chocolate shake is said to be able to withstand a nuclear attack.

However, since 2011, the stock has largely failed to perform, and has greatly underperformed the S&P 500. Its business model is aging. Its menu needs a major reworking.

The company has suffered sales declines at existing locations in five out of the last six quarters, with the rate of decline accelerating this year.

The problem is that people just don?t want to buy what they make anymore.

I went into a store the other day, and I was appalled. It was almost empty.

The few customers it had all seemed sick, obese, or unemployed, wearing polyester clothes. They periodically ducked outside for a quick cigarette.

They needed a double bacon cheeseburger like a hole in the head. Health was not their priority. They were a market that was literally dying.

It is becoming increasingly clear that the American market is moving beyond McDonald?s. Can the long vaunted company now play catch up?

This is the big problem. Millennials, those aged 18-34, which should be the company?s highest growth market, aren?t showing much interest in the company?s secret sauce.

They are, in fact, adopting a complete different life style that doesn?t have Ronald McDonald anywhere in it. They are very cautious in what they put in their young bodies.

Think organic, locally grown, low fat, low calorie, non-GMO, high fiber, and no artificial hormones or coloring anywhere. Think of health food, and you don?t exactly run off to a McDonald?s to eat. McDonald?s has a serious brand problem.

Organic foods are booming, seeing sales growth of 30% a year nationally, with far higher profit margins.

If you don?t believe me, look no further than the stock chart of Whole Foods (WFM) below, which at one point, saw its shares gain 116% relative to (MCD).

This is also a generation that is vastly more environmentally conscious that the Gen Xer?s and baby boomers before them. Beef is the single most environmentally destructive food product you can buy, with all the waste and methane byproducts.

One quarter pound beef patty requires a profligate 450 gallons of water to produce. That?s double the daily ration for a family of four here in drought suffering California. And who knows what the hell they are putting in it to preserve it down a very long global supply chain.

McDonald?s did make some limited progress on this front by announcing that they would no longer put ?pink slime? into their beef patties. If you don?t know what ?pink slime? is, then you don?t want to know. Suffice it to say that it is definitely not a great new marketing angle for health food nuts.

The company is also encountering ferocious competition for the fast food dollar from the new, rapidly growing ?fast casual? industry. These include Five Guys, Shake Shack (SHAK), Chipotle Mexican Grill (CMG), and Panera Bread (PNRA).

These companies are all snapping up the high margin end of the market, even though any one of them is miniscule in size when compared to McDonald?s. Collectively, they are nipping at Ronald McDonald?s heels.

I can?t even get my own kids to eat at McDonald?s anymore, they preferring the legendary In and Out Burger on the West Coast (no double entendre intended), which emulates the McDonald?s stripped down menu of the early 1950?s.

(In and Out is a fascinating business story for another day, as the $2 billion, 300 stand LA based company is now controlled by a 33 year old four time married heiress named Lynsi Snyder.)

McDonald?s is one of the world?s largest and best managed companies. In 2014 it generated an impressive $4.8 billion profit on $27.4 billion in sales, producing a not too shabby net margin of 17.5%. So we?re not, by any means, talking chapter 11 material here.

But it is going ex growth, and that invites a lower stock multiple, and a lower stock price, something you, as equity investors should be aware of. Is (MCD)?s position in the Dow Average 30 at risk?

Yikes! That would be a disaster for shareholders!

The company has seen the writing on the wall. It recently brought in a new CEO, Steve Easterbrook, to shake things up. But so far, all of the changes he has implemented have been administrative in nature. There is no category killing super burger anywhere on the horizon.

McDonald?s does still have some huge advantages. Its efficiencies, purchasing power, and economies of scale are epic. But the business is so enormous that any incremental change is unlikely to move the needle on the earnings front.

It is the classic dilemma when navigating a supertanker.

Another headache arises from the snowballing minimum wage, or living wage movement, which has McDonald?s squarely in its crosshairs. This promises to be a big political campaign issue in 2016.

Several cities, like San Francisco and Seattle, have already boosted pay from $8 to $15 and hour, which would substantially increase (MCD)?s operating costs and cut its price advantage.

It is possible that McDonald?s could go the route of so many other legacy industries that were born here, and then migrated abroad when the home market disappeared. I?m thinking about cigarettes (Altria Group (MO), Kentucky Friend Chicken (YUM), and coal (PEA).

Indeed, on my last trip to China, I ate regularly at McDonald?s, and couldn?t help but notice that it had become the country?s hot high end date. But the burden of proof lies on the current management as to whether they can pull this off.

So, you won?t find me buying (MCD) shares anytime soon. If you must own it for that generous 3.6% dividend, at the very least you should be writing covered calls against your position to take in premium income to offset the lack of capital appreciation.

In the meantime, I?ll be grabbing a double cheeseburger and chocolate shake at In and Out Burger, even though the lines there can be miserable.

Watch Out, McDonald?s!

Watch Out, McDonald?s!