Mad Hedge Biotech and Healthcare Letter

August 13, 2024

Fiat Lux

Featured Trade:

(THE RISE OF THE STEADY EDDIES)

(CNC), (UNH), (PFE), (JNJ), (ABBV), (LLY), (BIO), (UHS), (WAT), (AMGN), (REGN), (VRTX), (CRSP), (MRNA)

Mad Hedge Biotech and Healthcare Letter

August 13, 2024

Fiat Lux

Featured Trade:

(THE RISE OF THE STEADY EDDIES)

(CNC), (UNH), (PFE), (JNJ), (ABBV), (LLY), (BIO), (UHS), (WAT), (AMGN), (REGN), (VRTX), (CRSP), (MRNA)

Think of the market as a body fighting off an infection. Tech stocks might be the flashy antibodies, but healthcare is the steady, reliable immune system, keeping things stable when the going gets tough. And right now, that immune system is looking stronger than ever.

Skeptical? I get it. We've heard the hype about healthcare before. But this time, it's different.

The Healthcare Select Sector SPDR ETF (XLV) has been on a tear, up 9.3% this year as of Thursday's close. That's nearly keeping pace with the broader S&P 500's 12% gain - a remarkable feat in a market that's been anything but stable.

But what's even more impressive is the turnaround. Back in mid-July, XLV was lagging behind like a three-legged horse in the Kentucky Derby, up only 8.3% while the S&P 500 was showing off with an 18% gain.

In fact, out of the 63 healthcare stocks in the S&P 500, only a dozen have been slacking off since July. The rest? They've been outperforming like it's going out of style.

So what changed?

Well, it wasn't so much that healthcare stocks suddenly discovered the fountain of youth. No, my friends, it was more like the rest of the market decided to take a swan dive off the high board.

You see, while tech stocks were busy doing their best Icarus impression – flying too close to the sun and then plummeting back to earth – healthcare stocks were steady as she goes. It's like the old tortoise and hare story, except in this version, the hare got distracted by shiny objects and ran off a cliff.

Now, let's shine the spotlight on some of the key players driving this healthcare rally.

Remember those health insurers everyone was worried about back in spring? The ones that had investors biting their nails over the future of Medicare Advantage? Well, they've made a comeback.

The S&P 500 Managed Health Care index was down 12% in mid-April, looking about as healthy as a chain smoker with a Big Mac habit. But now? It's up 4.5% since the start of the year.

Companies like Centene (CNC) and UnitedHealth Group (UNH) have bounced back faster than a rubber band on steroids.

And it's not just the insurers. Big Pharma's been flexing, too.

Pfizer (PFE), the company that became a household name faster than you can say "vaccine," is holding steady. Johnson & Johnson (JNJ) is up 2.2%, probably thanks to all that baby powder they're not selling anymore.

Meanwhile, AbbVie’s (ABBV) up 11% since July. These guys are like the Energizer Bunny of the pharma world – they just keep going and going.

But the real showstopper? Eli Lilly (LLY). This biopharma has been on a tear since the beginning of 2024. Up 45% on the year at one point, they've been climbing faster than a squirrel up a tree with a dog in hot pursuit.

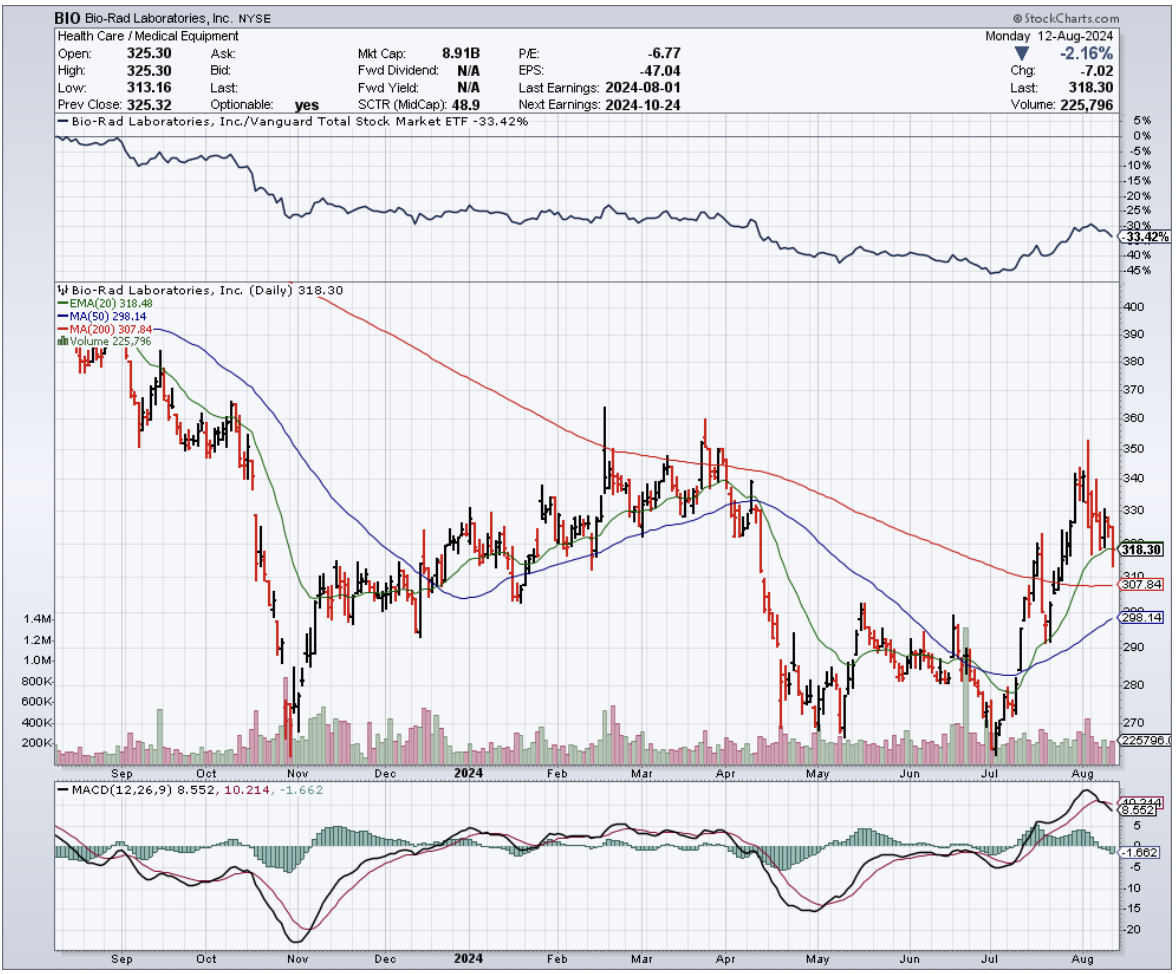

Then, there are companies like Bio-Rad Laboratories (BIO), up 20% since July. Universal Health Services (UHS)? Up 18% since July. Waters (WAT), the life sciences tools folks? Up 15%.

Even the biotechs are out to impress.

Amgen (AMGN), the granddaddy of biotech, is up 10% year-to-date. They're selling drugs like Prolia and Enbrel faster than hotcakes at a lumberjack convention.

And Amgen’s pipeline? It’s packed with potential blockbusters, setting the stage for further expansion in the future.

Gilead Sciences (GILD)? Up 15% year-to-date. Turns out, their COVID-19 treatment, Remdesivir, is back in vogue like bell-bottom jeans. And their HIV and hepatitis C drugs? They're still growing stronger.

But the real rock star of biotech? That'd be Regeneron Pharmaceuticals (REGN). These guys are up over 30% year-to-date. They're treating everything from eye diseases to cancer to inflammation.

Vertex Pharmaceuticals (VRTX) is another one to watch. Up 12% this year, they've got the cystic fibrosis market cornered. And they're not stopping there – they're expanding faster thanks to their collaboration with the likes of Crispr Therapeutics (CRSP).

Now that I’ve mentioned gene therapy, I know you're wondering about Moderna (MRNA). After all, weren’t they the darlings of the COVID era? Well, yes and no.

Their stock's down about 35% year-to-date, but don't count them out just yet. Their mRNA technology is hotter than a jalapeño popper fresh out of the fryer. They might be down, but they're definitely not out.

So, what's the takeaway here? I suggest you keep your eyes peeled on the biotechnology and healthcare sectors. After all, in this market, the best offense might just be a good defense – and what's more defensive than betting on the sector that keeps us all alive and kicking?

Mad Hedge Biotech and Healthcare Letter

August 3, 2023

Fiat Lux

Featured Trade:

(A FUTURE-PROOF INVESTMENT)

(UNH), (CI), (HUM), (CNC)

With a staggering market cap of $472 billion and a network reaching scores of policyholders, UnitedHealth Group (UNH) is an undisputed titan in the health insurance industry.

To put this into perspective, its competitors such as Cigna (CI), Humana (HUM), and Centene (CNC) have market caps of $86.42 billion, $56.64 billion, and $36.32 billion, respectively.

However, the past year witnessed a slight dip in UnitedHealth’s share price by 2%, which noticeably lags the broader market's return of 17%.

This raises a question: Is UnitedHealth’s investment appeal dwindling, or is it merely in a brief pause?

One can't discuss the health insurance sector without addressing the brewing storm of growth in its forecast. This sector is expected to welcome a turbocharged surge fuelled by an escalating burden of maladies and an expanding aging population worldwide.

The global landscape is witnessing a steep rise in various chronic afflictions - from cardiovascular and respiratory conditions to neurological disorders, cancer, musculoskeletal diseases, and diabetes. With the world population growing savvier about the financial cushioning health insurance provides, we're staring at a potential boom in this sector.

Take a gander at the numbers: The global health insurance industry was valued at a hefty USD 2.17 trillion in 2022.

Fast forward to 2032, and we're talking about a market swelling to an eye-watering USD 4.37 trillion. And with a projected CAGR of 7.3% from 2023 to 2032, we can safely say the health insurance express isn't slowing down anytime soon.

With this backdrop, let's dive into the compelling aspects of investing in UnitedHealth.

First, let's delve into the favorable aspects of investing in UnitedHealth. The core rationale is simple: healthcare is perennial. As long as human beings exist, healthcare will always be needed.

In the United States, individuals or their employers inevitably need to secure health insurance on a monthly basis. The constant evolution and improvement of healthcare services create a fertile ground for potentially substantial earnings in both the insurance and healthcare delivery sectors.

UnitedHealth, a veritable powerhouse, operates two key divisions - one specializing in health insurance and prescription coverage, and the other focused on healthcare provision. This dual-pronged approach has the potential to create sustained shareholder value.

Finding a flaw in this favorable proposition is challenging, particularly when examining the figures.

The company amassed an impressive $93 billion in revenue in the second quarter of 2023 alone, making it one of the world's largest corporations. It outperformed analysts' predictions of $91 billion, and the earnings per share of $6.14 surpassed Wall Street estimates of $5.99.

Although the company's medical care ratio did increase from 81.5% to 83.2% as expected, this was offset by a robust revenue growth that outpaced the rise in medical and operational costs.

UnitedHealth provides insurance to over 51 million individuals, with an addition of over a million new policyholders in 2023. UnitedHealth's scale allows it to keep costs low, forming a formidable entry barrier for new market contenders.

Moreover, its quarterly revenue experienced a notable 63% increase over the past five years, hinting at significant growth potential. This suggests that UnitedHealth's future growth prospects remain robust.

Straight from the company itself, UnitedHealth anticipates growing its earnings per share (EPS) between 13% and 16% annually. Moreover, the company has shown consistent dividend growth, with an annual increase of 10% since 2010.

This indicates a company that excels in operating its business model over time, suggesting potential stability and growth in both share price and dividends.

One key strategy of UnitedHealth is its diverse portfolio, developed over the years through strategic acquisitions like home health company LHC Group and analytics firm Change Healthcare. This diversity has allowed the company to maintain a growth rate exceeding 10% over the last five years.

UnitedHealth's most significant growth driver remains its premiums, but the company also saw an additional $2 billion in revenue from services and $1.2 billion from product sales last quarter.

Although it faces potential increases in medical costs, the company's diversified portfolio helps it maintain strong profit growth, with adjusted earnings per share rising 10% to $6.14 year-on-year.

Despite the overall positive outlook, it's worth noting that UnitedHealth's shares have decreased by about 4% this year. While the stock is trading at 23 times trailing earnings, slightly below the healthcare industry average of 25, the company's consistent growth could justify a higher valuation.

Overall, UnitedHealth remains a promising investment in the long run despite some short-term volatility, as it offers a blend of stability and growth. It may well be a stock worth considering for those looking for a long-term hold in the healthcare sector. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

May 23, 2023

Fiat Lux

Featured Trade:

(HUNTING FOR OPPORTUNITIES IN HEALTHCARE STOCKS)

(LLY), (NVO), (VTRS), (OGN), (MRK), (TEVA), (GI), (CNC), (PFE), (GILD), (AMGN)

I've been riveted by the healthcare sector's most extravagant stocks lately.

Just look at Eli Lilly (LLY), with its jaw-dropping market value of $412 billion, making it the richest pure-play biopharma company ever. And right on its heels is Novo Nordisk (NVO), boasting a market value of $377 billion. It's enough to make your head spin.

But if you're on the hunt for value, these sky-high prices might leave you feeling a bit queasy. That's why I embarked on a mission to uncover some hidden gems in the healthcare sector.

Now, don't get me wrong. These stocks may be cheap for a reason, and it's crucial to exercise caution. When it comes to investment opportunities, it's essential to separate the diamonds in the rough from the fool's gold.

Enter Viatris (VTRS), a rising star in the generic drug manufacturing arena that has caught the attention of savvy investors seeking long-term holdings. But is it the real deal, or just another flash in the pan?

Viatris shows potential with solid revenue from branded generics like Lipitor, Viagra, and EpiPens. These household-name medicines have a lasting market demand. Plus, its generous 5.2% dividend yield surpasses the market average.

But here's the catch: Viatris is currently undervalued and has yet to prove its growth potential. Its stock price took a hit, and sales in the core generic and branded segments dipped. However, there's hope in the pipeline.

With a range of injectable generic medicines awaiting approval, Viatris could be at the forefront of the market.

By 2027, these programs could yield over $1 billion in annual revenue. While not a game-changer for the company's overall revenue, it sets the stage for future earnings growth.

At this stage, I don’t see Viatris as a slam-dunk investment. However, monitoring their strategic plan to reduce debt, improve efficiency, and drive growth is prudent. It's a work-in-progress worth monitoring for future opportunities.

Another company that caught my attention is Organon (OGN), a recent spinout from Merck (MRK) that focuses on women's health and biosimilars. This hidden gem trades at an attractive valuation of just 4.8 times earnings.

Organon & Co. is a pioneering developer and provider of prescription therapies and medical devices catering to contraception and fertility needs.

The female contraceptive market is projected to experience robust growth, with a compound annual growth rate (CAGR) of 8.5% from 2022 to 2027. Notably, Organon is among the top 5 major corporations addressing the demands in this market segment.

But that's not all.

Organon boasts a diverse portfolio that extends beyond women's health. They also offer biosimilar immunology products, two oncology treatments, hypertension therapies, respiratory solutions, dermatology products, non-opioid pain management pills, and cures for male pattern hair loss.

On its first day of official existence, June 3, 2021, Organon's management proudly announced a lineup of over 60 drug products to enhance female health, along with Merck's (MRK) former biosimilars portfolio.

The biosimilars market is projected to soar to $44.7 billion by 2026, showing an impressive CAGR of 23.5%.

As expected, the biosimilars arena has become a bustling hub with both established and emerging companies eagerly entering the space. For instance, Teva Pharmaceutical Industries Limited (TEVA) has high hopes for its biosimilar drug targeting arthritis treatment, expecting it to boost Teva's revenue significantly.

Organon has already witnessed promising revenue growth from its biosimilar drugs, with a remarkable 17% increase amounting to $116 million.

Several drug sales have experienced a surge of over 30% in the United States, Canada, and Brazil. Moreover, Organon's brands have shown strong performance in China and the Asia Pacific/Japan region.

Investing in women's health is not only a wise choice; it's a strategic move that can yield significant rewards for individual investors and portfolios. With Organon's innovative solutions, broad product portfolio, and forward-thinking approach, it stands out as a compelling opportunity in the market.

Now, let's take a look at some intriguing names that have found their way onto the list.

We have health insurance behemoth Cigna Group (GI), trading at a mere 9.9 times earnings, alongside the health insurer Centene (CNC) at 10.3 times earnings. Not to mention the presence of renowned drugmakers Pfizer (PFE), Gilead Sciences (GILD), and Amgen (AMGN) gracing this list of bargain stocks.

These seemingly cheap healthcare stocks warrant close attention for the savvy investor seeking hidden gems. Sure, the term "cheap" can sometimes be misleading, but within these underappreciated names lies the potential for hidden value waiting to be discovered.

Mad Hedge Biotech & Healthcare Letter

April 20, 2021

Fiat Lux

FEATURED TRADE:

(A DEPENDABLE BUT UNDERVALUED HEALTHCARE STOCK)

(UNH), (ANTM), (CI), (HUM), (CNC), (CHNG)

The ongoing seesaw fights in the stock market are causing too much drama that cunning investors can—and definitely should—steer clear from.

Instead of fretting over speculative and risky investments, it’s better off staying with tested and proven big-name companies that will remain solid buys for the years to come and continue to deliver positive results despite periods of uncertainty.

Among the huge names in the healthcare industry, United Health (UNH) is a strong contender that meets the criteria.

After almost a decade of delivering high returns, which shows off fast-rising earnings expectations, it’s interesting to see that the market has recently backed away from this blue-chip stock.

Nonetheless, the market’s skittishness offers an opening for investors looking to buy in the dip a company that pays dividends and promises to steadily boost your savings in the years to come.

Founded way back in 1974, UNH has become a top name in the healthcare industry, landing in seventh place on the Fortune 500 list.

To date, UNH has four main divisions handling its over 50 million members both in the US and across the globe: its private health insurance business UnitedHealthcare, its pharmacy benefits segment OptumRx, its healthcare services provider branch OptumHealth, and its analytics platform OptumInsight.

UNH has a market capitalization of $354 billion.

In comparison, the closest competitor is Anthem (ANTM), with $87.93 billion. In terms of market cap, the two are followed by Cigna (CI) with $85 billion, Humana (HUM) with $53.81 billion, and Centene (CNC) with $36.19 billion.

Amid the financial crisis brought about by the pandemic, UNH still reported a 6.2% jump in its revenue in 2020 to reach $257.1 billion.

The company’s most prominent growth driver is its Optum line, and UNH is making sure that this division continues to grow.

One of the most indicative moves towards that direction is UNH’s $7.8 billion acquisition announcement of technology and data analytics company Change Healthcare (CHNG), which should be completed by the second quarter of 2021.

In the agreement, UNH is offering Change Healthcare $25.75 for its shares, representing a premium of roughly 41% above the latter’s stock price.

UNH plans to merge Change Healthcare’s operation into OptumInsight, which currently handles hospital systems health plans, life sciences companies, and even governments.

In the first nine months of 2020 alone, OptumInsight generated over $1.9 billion, contributing to roughly 11% of UNH’s total bottom line.

The combination of these two will all but guarantee that UNH’s possession of the biggest and most powerful platform in the entire healthcare industry, with the acquisition projected to add approximately $470 million to the company’s adjusted earnings in 2022.

The decision to acquire Change Healthcare is part of the string of M&A deals executed by UNH to stay ahead of the game.

In 2019, it bought two companies to expand its operations: the DaVita Medical Group for $4.3 billion and Equian for $3.2 billion. Prior to these, UNH splurged on a $12.8 billion acquisition of Catamaran in 2015.

For 2021, UNH projects its earnings to increase, estimating its per-share profits to be somewhere between $16.90 and $17.40—and that estimate already took into consideration the headwinds involving COVID-19 that could still weigh on the company’s bottom line.

While this may appear optimistic, the truth is, generating strong results isn’t a novel accomplishment for UNH.

In the past three years, the company reported a net income of $10 billion or higher, with net margins recorded at 5% above its revenue.

Over the course of the last 12 months, UNH stock has climbed 24%, beating the S&P 500, which rose 18% during the same period. It also offers a decent dividend of 1.5%, which is admittedly slightly lower than the S&P 500 average at 1.6%.

Overall, UNH is a safe stock that you will not have to anxiously watch over and can hold in your portfolio for years.

More importantly, this company remains undervalued and still shows a lot of room for growth.

So if you’re a value investor looking with an interest in the insurance and healthcare services industry, then this market leader is a sustainable addition to your portfolio.

Although late to the party, giant biopharmaceutical company AbbVie (ABBV) is now going all-out on its coronavirus disease (COVID-19) treatment program.

The Illinois-based company, which has a market capitalization of $162.95 billion, aims to come up with a treatment that can block the SARS-CoV-2 coronavirus that causes COVID-19. The drug is currently dubbed 47D11.

AbbVie is working on this cure alongside Netherlands’ Erasmus Medical Center and Utrecht University as well as China’s bio-therapeutics developer Harbour BioMed.

It’s worth noting that AbbVie isn’t the first company to use this approach.

Earlier this year, Regeneron (REGN) announced a similar strategy to beat COVID-19. Its experimental cure, called REGN-COV2, is an antibody cocktail composed of two to three proteins working together to fight off the virus. The company plans to start clinical trials sometime this month.

Aside from AbbVie and Regeneron, Eli Lilly (LLY) is also utilizing the same technology.

In fact, the Indiana-based biotechnology leader already started dosing actual patients with COVID-19 with its experimental treatment, LY-CoV555.

Eli Lilly’s drug was actually developed using the antibodies collected from one of the first patients in the US to recover from the disease.

Using the same approach to find a COVID-19 cure isn’t the only thing Regeneron and AbbVie have in common, though.

To bulk up its oncology pipeline, AbbVie forged a partnership with Danish biotechnology company Genmab (GMAB) earlier this month.

Interestingly, Genmab is the same company behind the clinical progress of the bispecific antibody treatments of both Regeneron and Roche Holding (RHHBY).

AbbVie and Genmab agreed to collaborate on bispecific antibody development to come up with treatments that can target cancer cells and strengthen immune cells. The three drugs included in the deal are epcoritamab (DuoBody-CD3xCD20), DuoHexaBody-CD37, and DuoBody-CD3x5T4.

Aside from the three candidates already lined up, the two companies are also ironing out details on four additional cancer treatments.

The deal is estimated to be worth almost $4 billion, with AbbVie paying $750 million upfront.

On top of that, Genmab will also be entitled to get potential payments of up to $3.15 billion in milestone payments. The four potential cancer treatments could also entitle Genmab with an additional $2 billion.

Since bispecific antibodies are hailed as the “next-generation cancer therapy,” this market continues to attract big names in the industry.

So far, the list of companies working on bispecific antibodies includes Amgen (AMGN), Johnson & Johnson (JNJ), Novartis (NVS), GlaxoSmithKline (GSK), Merck (MRK), AstraZeneca (AZN), and Sanofi (SNY).

Aside from improving its oncology lineup, Abbvie has shown more creativity in diversifying its products.

Throughout the years, AbbVie had been considered as a strictly pharmaceutical company in the past. However, its recent purchase of Allergan set off a series of decisions that showcased the company’s plan to expand its portfolio.

With AbbVie’s revenue reaching $33.3 billion in 2019, several experts disagreed with the company’s decision to buy Allergan (AGN).

However, the move is estimated to add roughly $50 billion to the company’s annual revenue and help AbbVie’s bottom line.

One of the biggest products added to AbbVie’s portfolio is Botox, which has been long-regarded as Allergan’s prized cash cow.

In fact, this widely popular injectible raked in $1.02 billion in sales for Allergan in the fourth quarter of 2019 alone. Another promising product is the dermal filler Juvederm, which brought in $347.3 million in the same period.

Despite the excitement from the newly formed partnerships, a lot of investors remain apprehensive over AbbVie’s future.

These fears are rooted in the doomsday countdown for the company’s blockbuster rheumatoid arthritis drug Humira — and for good reason.

In its 2020 first quarter report, AbbVie recorded $8.6 billion in revenue, indicating a 10.1% jump year over year.

From this, Humira contributed nearly 58% despite the growing number of biosimilar rivals in Europe. In fact, Humira sales reached $4.7 billion, showing a 14.5% climb from the same period last year.

In 2019, experts predicted that Humira is poised to overtake Pfizer’s (PFE) Lipitor as the top-selling drug of all time by 2024.

AbbVie’s rheumatoid arthritis drug is estimated to reach a whopping $240 billion in sales in the next four years.

As expected, biosimilar competition, led by Amgen, has been licking their chops to get a piece of the action for years now, and they would do everything to dethrone AbbVie from its top spot in the autoimmune diseases sector.

Hence, AbbVie implemented two strategies to address this issue.

The first is forestalling the inevitable. In a recent court victory, AbbVie secured patent exclusivity for Humira until 2023.

Although this only leaves AbbVie with three short years to deal with the problem, it’s sufficient period for the company to execute its second plan: “Humira on steroids.”

Since Humira’s patent exclusivity has been a sore issue for AbbVie for years, the company decided to solve it by creating a stronger version of the drug.

The new antibody treatment, called ABBV-3373, is said to be more effective than Humira.

If all goes well in its clinical trials, then this “new Humira” can very well be AbbVie’s next megablockbuster and main moneymaker after 2023.

Humira isn’t the only big seller in AbbVie’s lineup.

Other blockbusters include cancer drug Imbruvica, which recorded $1.2 billion in revenue in the first quarter, up by 20.6% compared to the same period last year. Another cancer drug, Venclexta, is also performing well, bringing in $317 million in net revenue.

AbbVie has been boosting its next-generation treatments as well.

So far, two more Humira-like drugs stand out --severe plaque psoriasis medication Skyrizi and rheumatoid arthritis treatment Rinvoq.

Skyrizi’s annual sales are projected to grow from $1 billion to hit $4.4 billion by 2025, with the numbers going higher than $7.4 billion in the following years.

Rinvoq is expected to bring in $3.7 billion in sales by 2025 and increasing to reach $5.9 billion after that.

Right now, AbbVie appears to be oddly cheap as its shares are trading at only 9 times its expected earnings this year. This is possibly due to the anxiety over the loss of Humira’s patent exclusivity by 2023.

As AbbVie has shown in the past months, it has solid plans on how to deal with the impending loss. Its acquisition of Allergan, partnership with Genmab, and development of the “next Humira” all prove that claim.

Mad Hedge Biotech & Healthcare Letter

June 16, 2020

Fiat Lux

Featured Trade:

(THE ONE BRIGHT STAR IN THE HEALTHCARE INDUSTRY),

(ANTM), (TDOC), (CVS), (HUM), (CNC), (UNH)