Mad Hedge Technology Letter

May 12, 2025

Fiat Lux

Featured Trade:

(THE FIGHT FOR AI SUPREMACY)

($COMPQ), (AMZN)

Mad Hedge Technology Letter

May 12, 2025

Fiat Lux

Featured Trade:

(THE FIGHT FOR AI SUPREMACY)

($COMPQ), (AMZN)

According to the betting markets, the odds of a recession

Overnight, have tanked from over 80% to just a fraction under 40%.

It is interesting to see such a development and speaks volumes to how volatile the tech markets are right now.

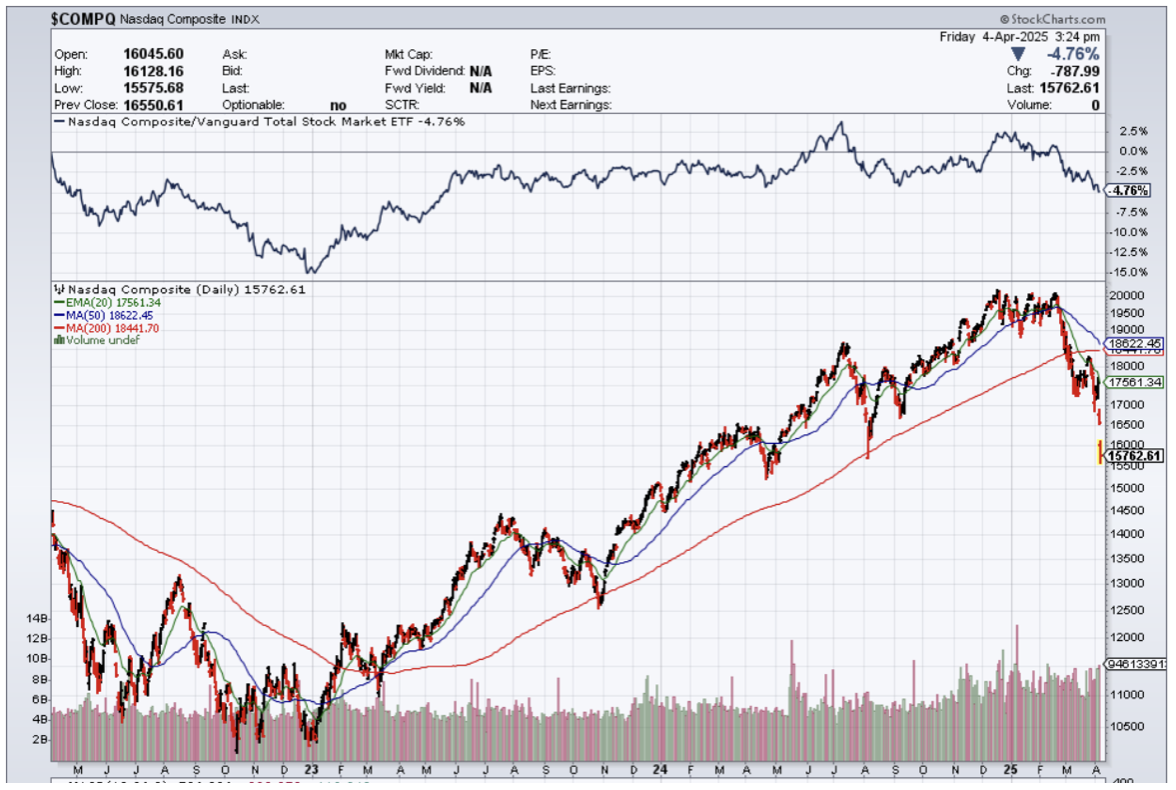

The V-shaped price action by the Nasdaq index ($COMPQ) perhaps forced the hand of decision makers.

Here we stand, only 6% from all-time highs after a vicious reversal to the upside.

I think it is fair to say that the belief in tech stocks has not corroded and is just resting.

Even though what was agreed was just a 90-day pause, the biggest takeaway is that the Americans aren’t willing to just blow the world order up.

The Chinese won’t just be moved to the side and switched in for Indians like a 6th man coming off the bench.

In fact, this signals that China has a big role to play in the upward trajectory of tech stocks, and that is why the tech index has exploded to the upside this morning.

Some of the tape is mind-boggling.

At the time of this writing, Amazon (AMZN) is up 8% and the Nasdaq is up over 4% in just ONE DAY.

To say this is a victory for tech is an understatement as the world’s two biggest economies unwound for now most of the tariffs they had imposed on each other since April in a tit-for-tat battle that was threatening to stoke U.S. inflation, crash China’s export engine, and upend the global economy.

The U.S. agreed to lower the base level of tariffs on most Chinese goods to 30%, from 145%, while China said it would cut its levies on U.S. products to 10% from 125%.

The U.S. tariff on many Chinese products will be higher than 30%. U.S. duties on steel, aluminum, and autos remain in place, as do some earlier tariffs on certain Chinese goods imposed during President Trump’s first term in office and that of former President Joe Biden.

Washington and Beijing agreed to keep the new tariff levels in place for 90 days, with the goal of working toward a broader deal on trade in further talks.

For China, an unrestrained trade clash with the U.S. would threaten millions of jobs tied to serving U.S. consumers and potentially worsen trade tensions with other countries wary of a surge in Chinese imports. China was also worried about losing access to some U.S. products it still needs, such as Boeing planes, aircraft parts, and certain chips.

In the short-term, I believe we are ready for a short squeeze higher.

The market was taken by surprise by the sudden announcement, and many companies were bracing for another onslaught of negative news.

In the next 60 to 90 days, I can easily see the US dollar popping higher, tech firms reforecasting higher revenue targets, and the Nasdaq coalescing around the positive energy to surge higher.

That’s not to say that everything is hunky and dory, we are literally just one tweet away for the market collapsing and going into a tailspin.

The risk levels have never been higher, and I would urge readers to keep positions small.

Mad Hedge Technology Letter

April 14, 2025

Fiat Lux

Featured Trade:

(BIG TECH ANXIOUS FOR CLARITY)

(MSFT), (AAPL), ($COMPQ)

At this pace, nobody knows what the government policies will look like, and if this doesn’t change, the uncertainty will bleed into lower tech stocks ($COMPQ).

Tech has had a hard short-term run, and the unstable backdrop will lead to investors pausing on big tech stock purchases.

Tech businesses are also reigning in their investment spend, waiting to see what happens.

Microsoft (MSFT) has already made announcements on pausing its AI database build out and that has really chilled momentum in the wider AI trade.

If this electronics exemption announced Friday night is true, it represents an important temporary win for Apple (AAPL) and other China-dependent technology giants.

News reports that producing the iPhone in America could cause the price of a new iPhone to double send shockwaves throughout the investment community.

The federal government might have to pull back their aggressive policies when factoring in surging yield in interest rates and a short-term collapse of the dollar.

The president said these products are simply moving to a different tariff "bucket," telling reporters that a separate rate for semiconductor tariffs will be announced over this week.

Trump added that his goal is to "uncomplicate" things by moving production to the US but that companies will have a say.

Either way, the fact remains that Trump has offered at least a temporary boost to companies with close links to China, and investors are responding by sending stocks of directly impacted companies like Apple and Dell (DELL) higher this morning.

These technology companies' goods are still subject to 20% blanket tariffs on China over fentanyl and likely face legacy sector-specific tariffs from Trump 1.0 and the Biden era, but they are now able to sidestep the lion's share of the 145% rate that is now in place for other goods.

The move is also a significant walk back of Trump's overall tariff plans, with electronics representing the top exports from China to the US.

This weekend's move means the overall effective tariff rate on US imports is now 22% — down from 27% just last week.

The smaller the tech company is, the bigger they are impacted with this whipsawing strategy of threatening all your trading partners.

Larger companies certainly have more options than small businesses to dodge the tariffs due to their worldwide networks and political relationships.

Apple, as one example, also gained attention in recent days for reportedly chartering cargo flights to move as many as 1.5 million iPhones to the United States from India quickly to get ahead of tariffs there.

Tech shares are pricing in nothing positive emerging in the short-term.

Management doesn’t want to get burned by moving in one direction, only to see a product get wiped out due to high costs.

It is hard to change the issue of how the U.S. relocated the supply chain to cheaper foreign countries.

The consensus of higher prices comes after Americans have been dealing with uncontrollable inflation since 2020.

The extra price increase preceding Trump’s tariff crusade has consumers in a hole.

Even compared to 2024, I don’t see where the incremental dollar comes into the tech sector when margins are being squeezed in real time.

At best, we could experience a bear market or choppy sideways price action to reflect a tougher environment for doing tech businesses, whether it is streaming, software, hardware of EVs.

Global Market Comments

April 9, 2025

Fiat Lux

Featured Trade:

(TECH SHARES RECOVER ON MACRO NEWS)

(FXI), ($COMPQ)

Expect this type of showmanship to be the new normal as the U.S. government goes pedal to the medal hoping to extract better trade terms.

In the short term, expect wild swings in the prices of US tech stocks.

U.S. President Trump unilaterally raised the US tariff rate on China (FXI) to 125% and instituted a 90-day pause on steep 'reciprocal' tariffs.

The Nasdaq shot up by an intraday 10% - an unprecedented type of market reaction stemming from short-covering.

The entire tech index was heavily weighted for lower Nasdaq ($COMPQ) share prices and this one announcement torpedoed the short-term momentum to the downside.

2025 is presenting itself to be one of the hardest environments to trade in the last two decades plus as tech shares are the trajectory of them are reliant on the whims of an aggressive new federal government.

People are scared – scared more about the uncertainty this presents.

Uncertainty creates an environment to sell stock resulting in meaningful lower-tech shares.

Additionally, it is very obvious the federal government will target China and the way it does business to reign them in. They are the big fish.

Remember that China has a massive youth unemployment rate problem inching towards 30% and the Chinese Communist Party (CCP) knows they are playing with fire if Trump’s tariffs result in millions of new job layoffs.

Trump on Tuesday claimed that China, as well as other countries, are keen to negotiate. Those talks have reportedly begun with Japan and South Korea. But he has remained defiant as members of his own party and Wall Street billionaires start to push back.

On the negotiations front, both markets and trading partners still seem to be searching for what exactly Trump is seeking.

The president’s approach has prompted retaliation from China and caused other countries to draw up their own plans to hit American exports. As a result, economists have raised their expectations for a recession in the United States, and many now consider the odds to be a coin flip.

During the trade fight with China in Mr. Trump’s first term, U.S. agricultural exports plummeted after China imposed high retaliatory duties on soybean, corn, wheat, and other American imports, and the United States spent about $23 billion to support American farmers.

The Retail Industry Leaders Association, which represents major companies like Walmart, Target, and Best Buy, said this could drive up prices for the American consumer.

In the short term, this should first alleviate the pressure on the U.S. dollar and the price hikes for tech products.

I would stay away from companies that have exposure to China like Tesla and Micron.

Gradually, we will see countries come to the table and if this gets through, even in diluted form, it would be considered a victory for US tech stocks.

Sure, the Federal Government could again jump back on its horse and go insane with the tariffs, but I do believe this pause highlights the fact that they aren’t willing to nuke the economy and tech sector just yet.

I also believe there is a roadmap to claim victory in all of this.

It starts with East Asian countries like Japan and South Korea which will take a “bad deal” in exchange for stability.

We have seen this a few times with Japan and I don’t believe they will reject America’s approach when Japan’s economy, society, and direction are even worse than Europe and America combined.

Once we get a little bit more settled and predictable, it should be a great buy-the-dip opportunity in tech shares.

Mad Hedge Technology Letter

April 4, 2025

Fiat Lux

Featured Trade:

(TECH STOCKS HURTING)

($COMPQ)

That was quick.

The Global Trade War has gone ballistic in a short amount of time and, tech stocks haven’t had time to digest this type of news.

Today’s sell-off at the time of this writing is over 5% intraday and around 10% over the past 5 days.

It is bad for everyone and accelerates an era of deglobalization that is picking up around the world.

China has hit back at new U.S. tariffs with sweeping levies of its own on American products, sharply escalating the trade war between the world's two biggest economies.

China's finance ministry said on Friday a 34% tariff will be imposed on all U.S. imports after the U.S. did the same to China.

Remember that many tech products are produced in China which is why the price of iPhones is only $1,000.

If iPhones are to be produced in the U.S., I expect a price of around $4,000 per iPhone.

The truth of the matter is that the U.S. onshoring manufacturing won’t make prices lower for average Americans.

Escalating trade rules between your biggest trading partners is a high-risk high-reward strategy.

It could easily backfire for the United States whose government also promises lower prices on tech devices and groceries.

In the short term, I don’t understand how lower consumer tech prices are on the table. There is no path to achieve that. In almost every model I play out, prices will go higher for almost everything.

This will be difficult for tech firms to pass on the costs to the end consumer. The consumer will simply not buy, kind of like a silent protest.

China's commerce ministry said it is adding 16 U.S. entities to an export control list, banning them from acquiring Chinese products designated as dual-use, for civilian and military purposes.

China’s economy is weakening and it will be fascinating to see what this does to the Chinese tech sector. The only guarantee is that Chinese factory workers who make American products face losing jobs in mass quantities.

Uncertainty is what the market hates and politics is delivering us a big dose of it.

In the short term, I see more volatility with governments escalating the fight further and getting entrenched in some of their positions.

Clearly, countries in Europe and China see the way they do business as normal, and having such a relative tax advantage has always helped foreign companies compete in the U.S.

The strategy is so good that American companies also began offshoring work to cheaper countries.

Almost every tech company publicly traded on the markets has the bulk of employees stationed outside of America.

At the same time, big tech companies are automating jobs and really shrinking their balance sheet to endure the turmoil.

Workers have lost negotiating leverage, and tech companies, in many cases, require 5 days per week in-office work.

What does this mean for tech?

Nothing good in the short-term.

Revenue targets will get slashed.

American jobs will be aggressively cut.

Management will force less workers to do more work for less pay while middle managers will get fired.

Expectations of less revenue have become more normalized in management circles in Silicon Valley.

Tariffs causing the cost of living to explode will mean less money on the table for tech.

For the time being, this will negatively impact the price of tech stocks. Brace yourself.

Mad Hedge Technology Letter

March 17, 2025

Fiat Lux

Featured Trade:

(WE HAVE CROSSED THE RUBICON IN THE SHORT-TERM)

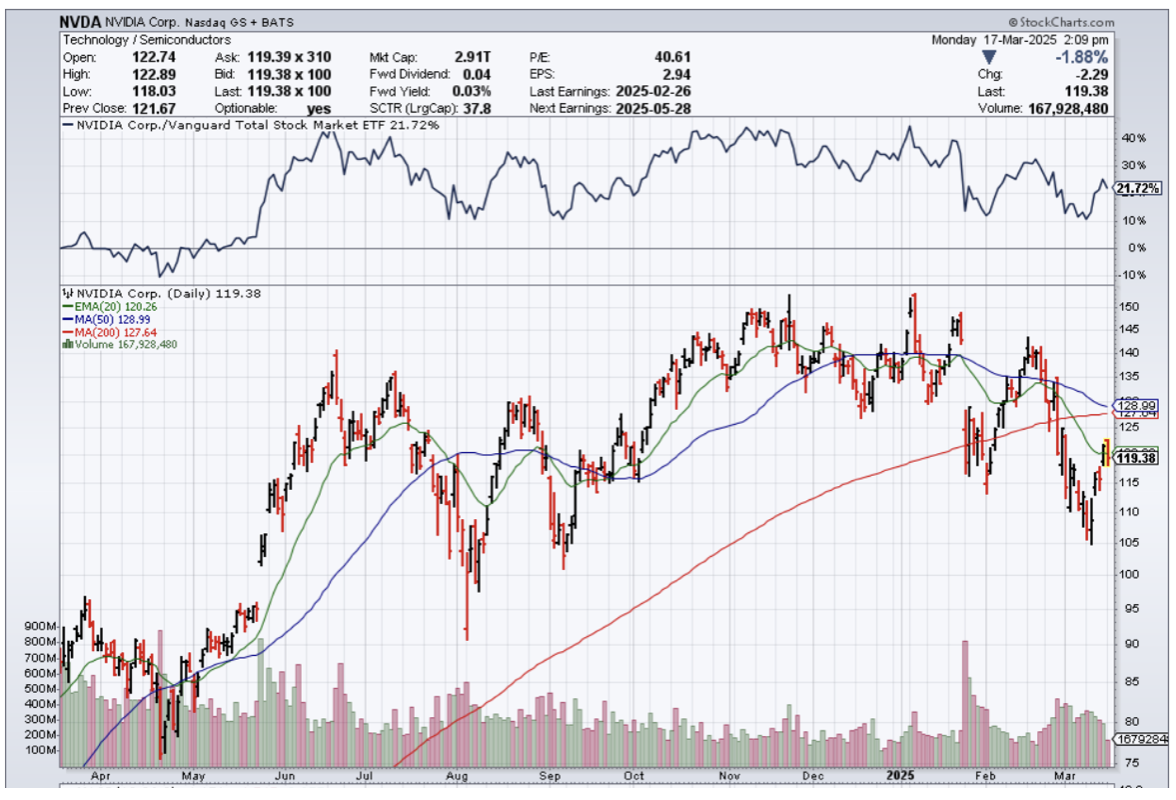

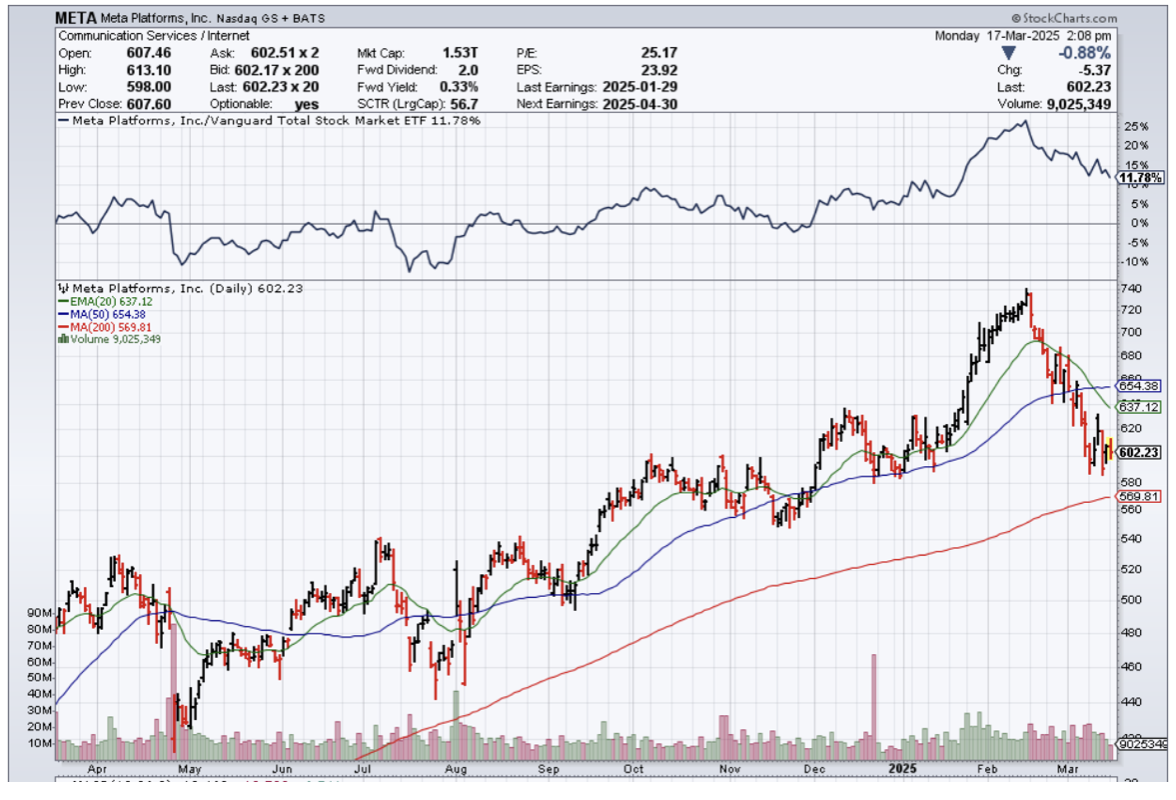

(META), ($COMPQ), (NVDA)

The pain trade for tech stocks just recently was up and that has now been broken.

It has been a tough fall and the Nasdaq ($COMPQ) has gone from up handsomely for the year to down 8%.

The tough point in this was that it was hard to go bearish until we finally crossed the Rubicon.

That moment is here and I think we are in a clear “sell the tech rally” mode for the short-term.

I don’t believe that investors are willing to bid up tech stocks in the short-term considering there is nothing coming down the pipeline from the business models that suggest we are in for some outsized growth.

I do believe that surprises will be to the downsides with many tech companies rerating their stocks negatively.

Then there is the issue that the American consumer is tapped out, and the ex-America rich countries are doing even worse.

For right now, I don’t believe traders should aggressively buy the dips.

My META (META) trade went horribly wrong and that shows that even the best of class got clobbered by the market.

Our bellwether barometer Nvidia (NVDA) is also demonstrably down from its highs of $150 per share and I don’t believe it will reach that level for the rest of the foreseeable future.

Don’t get me wrong, I do believe we can stage a bear market rally just from the very fact that we are in extremely oversold conditions.

It’s also clear that the problem in American politics is now rearing its ugly head and stocks will need to stomach a lot of headline risk in the short-term.

When countries’ politics devolve into 3rd world level type of politics then markets will tell investors to get ready to bear risk and America is no exception.

In response, investors have retreated from risk assets and taken profits on their holdings of the tech giants, which have been the biggest winners, by far, during the bull market in US stocks that began in October 2022.

Over the past decade, investors have been taught time and time again that it pays off handsomely to buy Big Tech stocks when they are down. Even prolonged slumps like the one that sent the Nasdaq 100 down 33% in 2022 proved to be a great buying opportunity as beaten-down stocks like Meta soared to new heights in the two years that followed.

There’s the near-universal belief that tech giants are still the highest quality companies in the world, thanks to their market dominance, immense profitability, and balance sheets loaded with cash. The question is whether these advantages are already baked into the share prices, and may now be under threat if the economy slows and big bets on artificial intelligence don’t pay off as expected.

Since closing at a record high 17 trading sessions ago, the Nasdaq 100 has bounced back on six days. But so far, none of the advances have lasted long.

Instead of catching a falling knife, traders should wait to get confirmation that we have support.

It is easier said than done, but the headline risk has shot to the forefront as the biggest risk to tech stocks when we wake up.

It is also clear that the federal government wants the market to digest as much political risk as possible at the beginning of the new term to smoothen its policy targets for the rest of the 4 years.

Whether it will work is up to debate and I don’t believe tech stocks are able to just shrug off these imminent risks as of yet.

It could be until the summer or fall when tech stocks start to become immune to belligerent politics and until then, we will most likely to see lower lows.

The market has rolled over and we have to shake and bake with it.