Global Market Comments

July 11, 2024

Fiat Lux

Featured Trade:

(JULY 10 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (NVDA), (COPX), (CMG), (TLT), (TBT)

Global Market Comments

July 11, 2024

Fiat Lux

Featured Trade:

(JULY 10 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (NVDA), (COPX), (CMG), (TLT), (TBT)

Below please find subscribers’ Q&A for the July 10 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village NV.

Q: Is the Fed waiting too long to cut interest rates?

A: Yes, they are. We are on a recession track if the Fed doesn’t move soon. In other words, the light at the end of the tunnel isn’t daylight—it’s an oncoming train. So, I think a September rate cut is a certainty. They want to see tomorrow’s data and make sure it’s cool. They need several months of really cool inflation data to justify the first rate cut and we probably are going to get that, so next update is tomorrow with the latest CPI number is crucial. Everybody’s sitting on their hands until then.

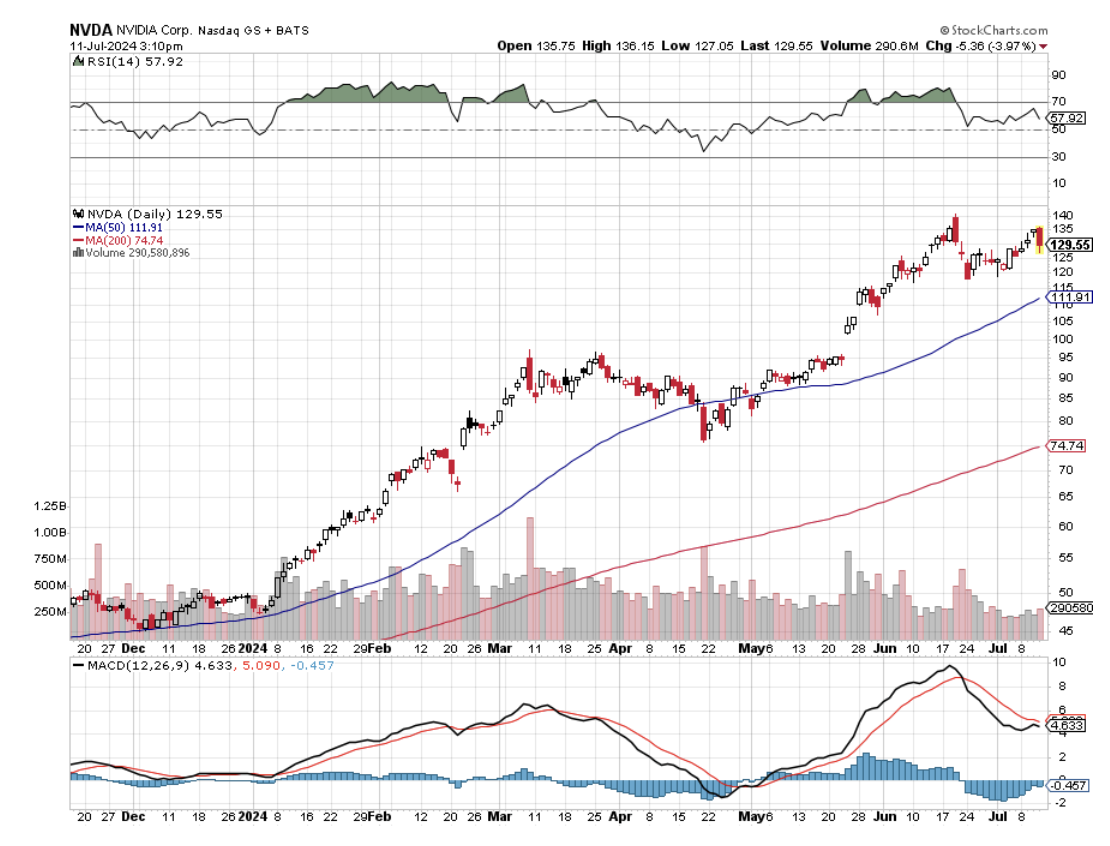

Q: When will NVIDIA (NVDA) hit a $4 trillion market valuation?

A: By the end of the year. We’re currently at $3.3 trillion, so another $700 billion is nothing for NVIDIA—you could do that in a day if you really wanted to. But give it until the end of the year, just to be conservative. The fact is, they have a global monopoly on the highest-priced product that everybody in the world has to buy or go out of business. It’s not a bad place to be—it’s kind of like where John D. Rockefeller was in the oil industry around 1900.

Q: What do you think about copper (COPX)? Should I maintain my longs?

A: Yes, all we need is further proof of falling interest rates and the entire commodities/precious metals sectors will take off like a rocket. So just sit with your positions. I put out a piece yesterday on copper. All that shines is not Copper, and it’s not dead it’s just resting, like the proverbial John Cleese parrot.

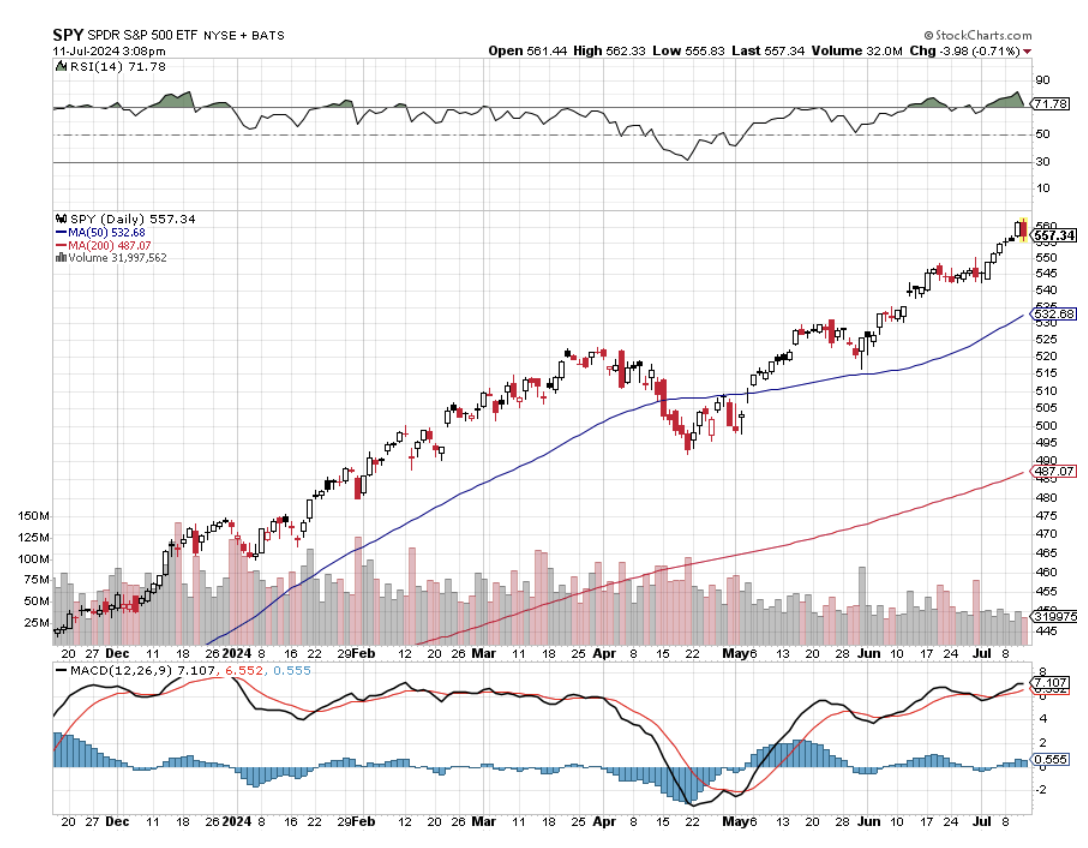

Q: Do you think a 10% stock market correction is likely before the election?

A: No, the most we’ve been able to get this year is 4% or 5% pullbacks, but not much more. We have a world with a cash glut that is underinvested in the face of a global monetary easing. Investors have been net sellers of stocks all of last year, so we were ripe for a meltup, which has, in fact, happened every day so far in July. So no, my S&P 500 target of 6,000 for the end of the year is starting to look too conservative given the moves that we’ve made lately. I’m very positive about that.

Q: Is the real estate market about to crash?

A: Well, the Florida housing collapse that is being driven by the insurance industry feeing that state. Insurance companies don’t like the hurricane risk going forward, which can cost tens of billions of dollars per event. Nobody there can get insurance anymore unless they pay outrageous amounts of money. Some people are only buying fire insurance to save money and skipping the storm insurance and rolling the dice, hoping the storms hit somewhere else in Florida. The fact is, you can’t get a home mortgage without insurance. Banks aren't willing to take the environmental risk of a house without insurance. No insurance means no bank loans, which means the market shrinks to a cash-only market. And there is a cash-only market in Florida, but it’s not at the $500,000 level, it’s more at the $50 million level. So that is a problem unique to Florida. Could it spread to other areas? Yes. Texas is having another energy crisis, as it has twice every year, ever since the power system was privatized there. No reserves for emergencies, no contingency, nothing that costs money basically. And then California definitely has a wildfire problem, although we’ve been getting off pretty light last year and this year. But the insurance companies don’t think like that. They are the classic 20/20 hindsight type companies.

Q: What’s the impact of the election on the market?

A: Zero. But it will defer buying until after the election. So if you have a 50/50 split on polls, uncertainty is at a maximum. People don’t like investing in uncertainty, they like sure things. After the election, you can expect a massive melt-up in the market no matter who wins because the uncertainty will be gone, and tech stocks will lead once again.

Q: What should I do with Nvidia (NVDA)?

A: I put out a report on this on Monday. You keep your long and write calls against them. And you can get quite a lot of money for just the August calls. I think the August $140 calls were selling for $3.50—they’re higher than that now, so you could even go out to August $145, and just keep doing that every month. If Nvidia takes off and you get taken out of your stock, you’re selling it essentially at $143.50. So that is an excellent trade—a lot of the big institutions are doing that now.

Q: Tesla's (TSLA) been on a big rally for the past month; do you expect it to continue?

A: I expect it to take a break, but the long-term uptrend is now back for good, for lots of different reasons. The immediate headline reason was because the Chinese government allowed the buying of Teslas for the first time—they are made in China after all. Second, they had a good earnings beat, so this caused a massive short-covering rally. The shorts got crushed by Tesla once again, as they have been consistently doing for the last 15 years, really. I saw a number of cumulative losses on short positions on Tesla stock since inception: $100 billion. Most of those losses were incurred by oil companies trying to put Tesla out of business.

Q: What do you call a substantial dip?

A: It’s different for every stock—for some it’s 2%, for others like Tesla or Nvidia it’s 20%. It depends on the volatility of the stock; you just have to look at the charts and make your own call.

Q: What do you think for the next earnings season?

A: It’ll be great for technology stocks and not so great for domestics as their businesses cool off.

Q: Is there anything Europe and American EV producers can do to compete against the Chinese at these lower prices?

A: Yes: keep quality high, therefore profits high, therefore profit margins high. That was the Japanese strategy in the US from the 1980s onwards, and it was hugely successful. You can cede the money-losing part—the low-end part of the market, to the Chinese. The quality of the Chinese EVs is terrible, they start to fall apart after four years, and I learned this from several Chinese EV drivers in Ecuador where they have a substantial market share already. But at $15,000 plus the shipping, you don’t make a lot of money in EVs.

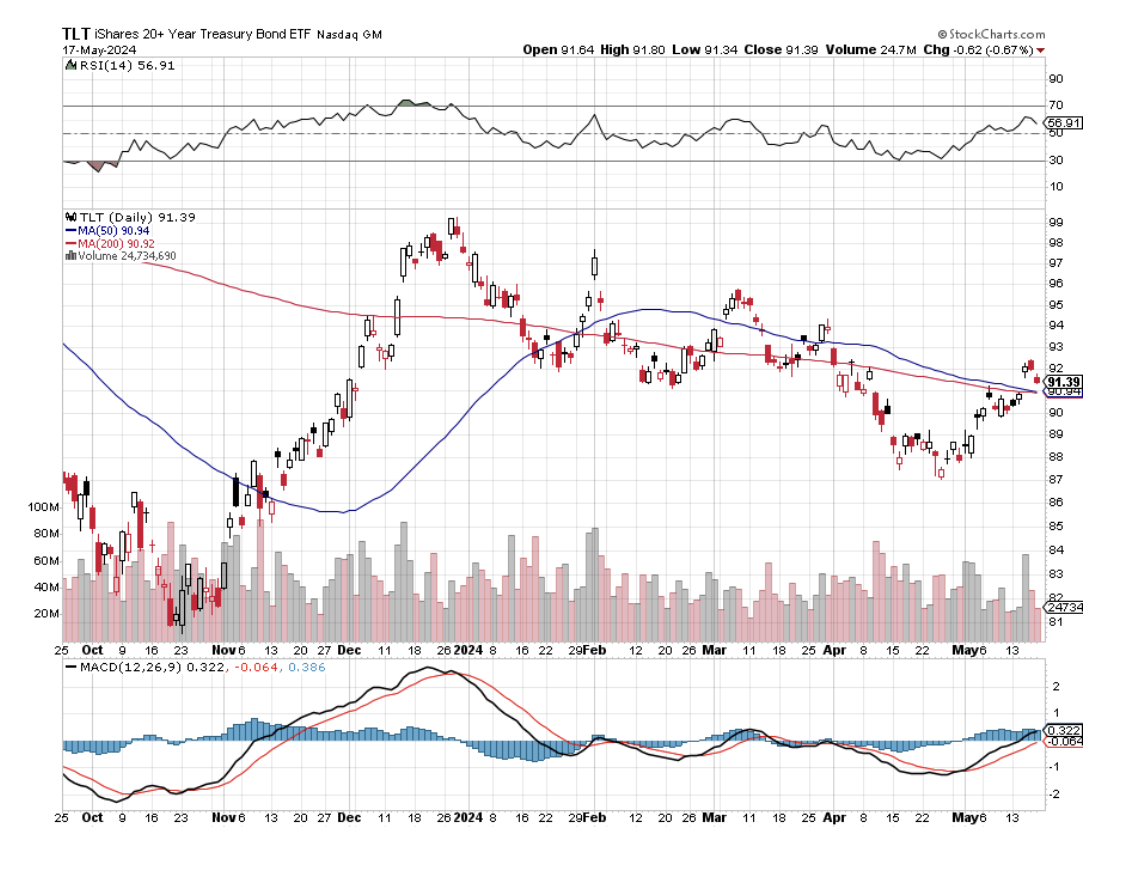

Q: Is it a good time to buy put LEAPS on the ProShares UltraShort 20+ Year Treasury (TBT)?

A: Yes, especially if you’re willing to do an at-the-money and bet that the interest rates stay here or lower for the next year. You’d probably get a 100% return on that, but why bother? Because on the TBT itself, you have a much wider trading spread than the (TLT), therefore the dealing costs are higher. You might as well just go and do the long (TLT) LEAP instead.

Q: Chipotle Mexican Grill (CMG) stock has been really successful for the last five years, but it just dropped 20%, should I get in?

A: It’s a very low-margin business—I avoid those. There’s not a lot of meat in the burrito business. It doesn’t have the key elements of success. (Not just Chipotle, but with the whole industry.) It's not like you’re designing 96 stock microprocessors.

Q: Are AI stocks overhyped at this point?

A: Absolutely yes, but they can stay overhyped for another three or four years, so I think we're just at the beginning of a very long-term run. And the people who have been involved so far are making the biggest money in their lives.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

July 9, 2024

Fiat Lux

Featured Trade:

(ALL THAT GLITTERS IS NOW NOT COPPER)

(FCX), (COPX)

Global Market Comments

June 28, 2024

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

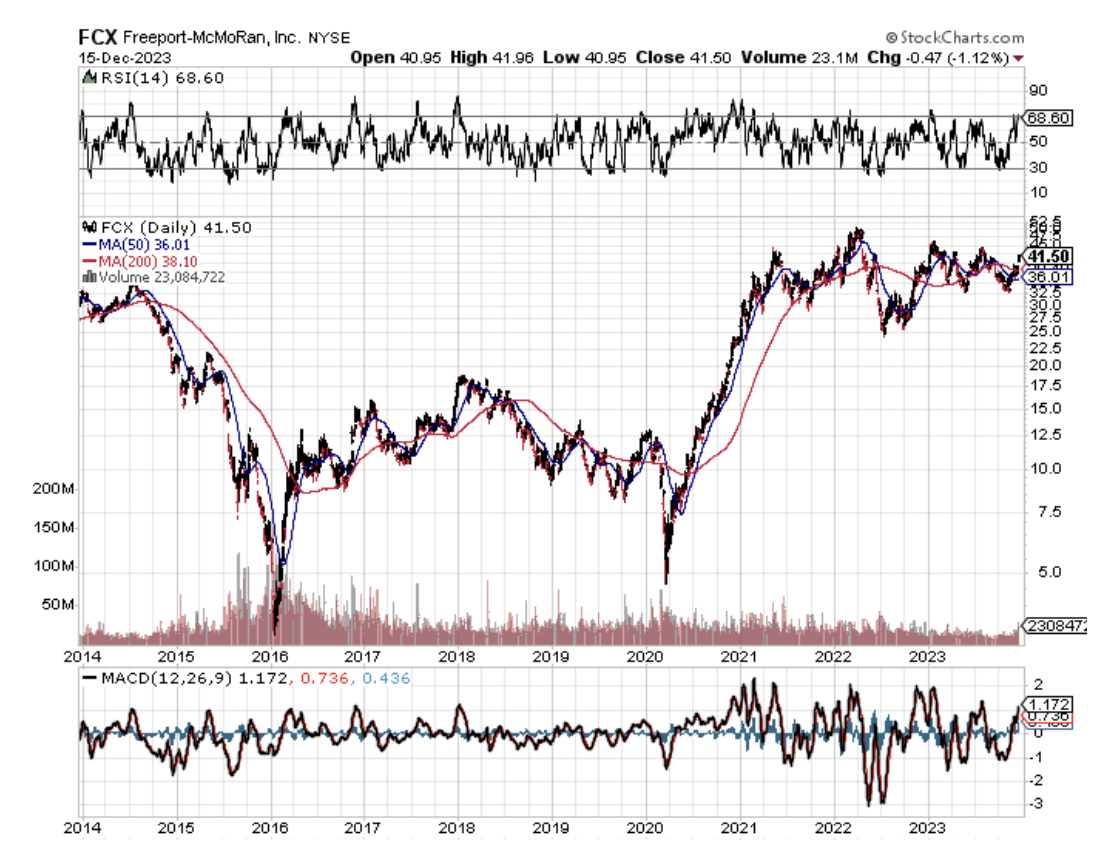

When I closed out my position in Freeport McMoRan (FCX) near its max profit earlier this year, I received a hurried email from a reader asking if he should still keep the stock. I replied very quickly:

“Hell, yes!”

When I toured Australia a couple of years ago, I couldn’t help but notice a surprising number of fresh-faced young people driving luxury Ferraris, Lamborghinis, and Porsches.

I remarked to my Aussie friend that there must be a lot of indulgent parents in The Lucky Country these days. “It’s not the parents who are buying these cars,” he remarked, “It’s the kids.”

He went on to explain that the mining boom had driven wages for skilled labor to spectacular levels. Workers in their early twenties could earn as much as $200,000 a year, with generous benefits.

The big resource companies flew them by private jet a thousand miles to remote locations where they toiled at four-week on, four-week off schedules.

This was creating social problems, as it is tough for parents to manage offspring who make far more than they do.

The Great Commodity Boom has started, and in fact, we are already years into a prolonged super cycle.

China, the world’s largest consumer of commodities, is currently stimulating its economy on multiple fronts, including generous corporate tax breaks and relaxed reserve requirements. Get a trigger like the impending settlement of its trade war with the US and it will be off to the races once more for the entire sector.

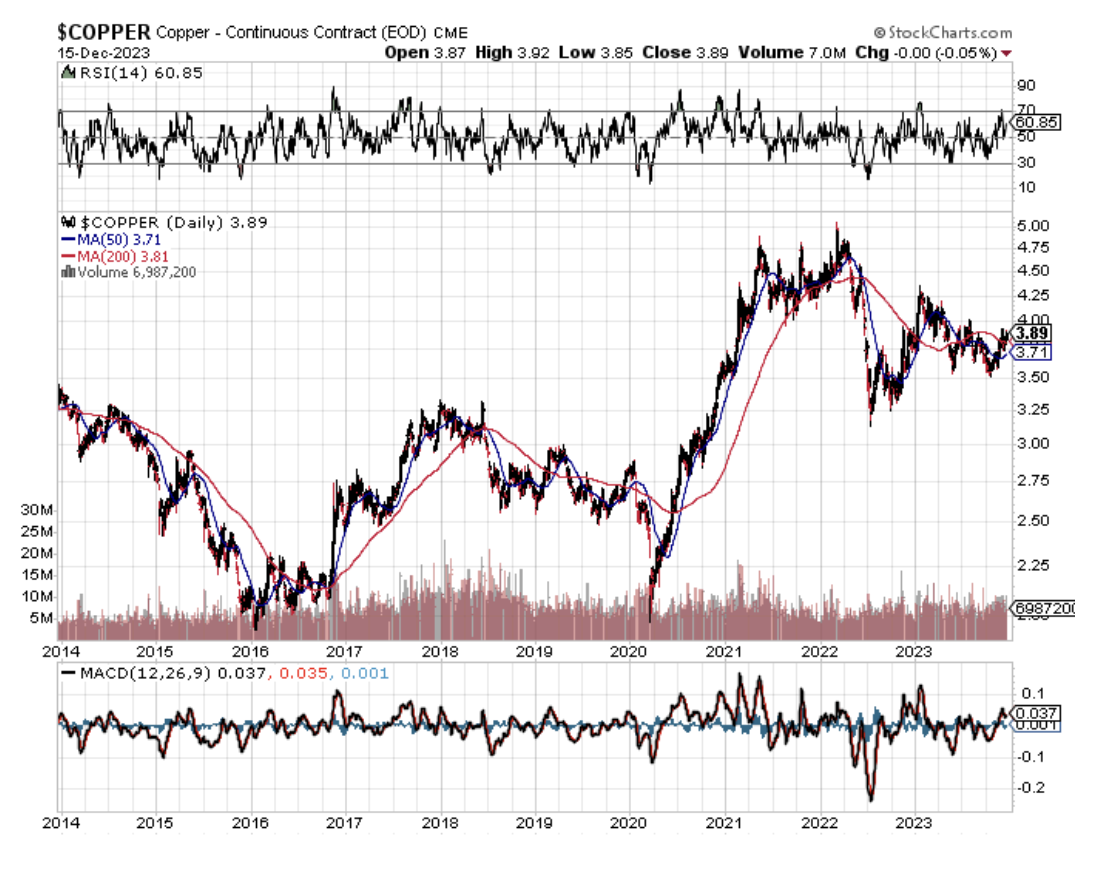

The last bear market in commodities was certainly punishing. From the 2011 peaks, copper (COPX) shed 65%, gold (GLD) gave back 47%, and iron ore was cut by 78%. One research house estimated that some $150 billion in resource projects in Australia were suspended or canceled.

Budgeted capital spending during 2012-2015 was slashed by a blood-curdling 30%. Contract negotiations for price breaks demanded by end consumers broke out like a bad case of chicken pox.

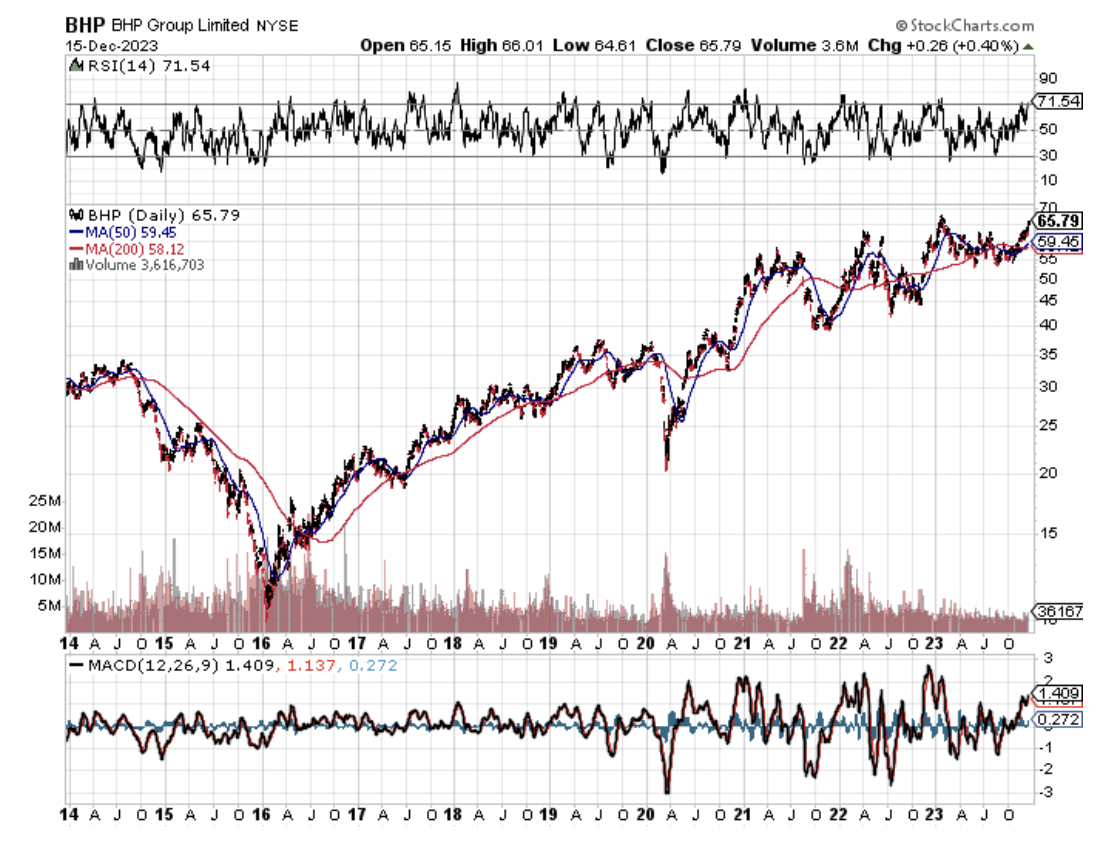

The shellacking was reflected in the major producer shares, like BHP Billiton (BHP), Freeport McMoRan (FCX), and Rio Tinto (RIO), with prices down by half or more. Write-downs of asset values became epidemic at many of these firms.

The selloff was especially punishing for the gold miners, with lead firm, Barrack Gold (GOLD), seeing its stock down by nearly 80% at one point, lower than the darkest days of the 2008-9 stock market crash.

You also saw the bloodshed in the currencies of commodity-producing countries. The Australian dollar led the retreat, falling 30%. The South African Rand has also taken it on the nose, off 30%. In Canada, the Loonie got cooked.

The impact of China cannot be underestimated. In 2012, it consumed 11.7% of the planet’s oil, 40% of its copper, 46% of its iron ore, 46% of its aluminum, and 50% of its coal. It is much smaller than that today, with its annual growth rate dropping by more than half, from 13.7% to 2.3% in 2020.

What happens to commodity prices if China recovers the heady growth rates of yore? It boggles the mind. If China doesn’t step up then India certainly will.

The rise of emerging market standards of living will also provide a boost to hard asset prices. As China goes, so do its satellite trading partners, who rely on the Middle Kingdom as their largest customer. Many are also major commodity exporters themselves, like Chile (ECH), Brazil (EWZ), and Indonesia (IDX), who are looking to come back big time.

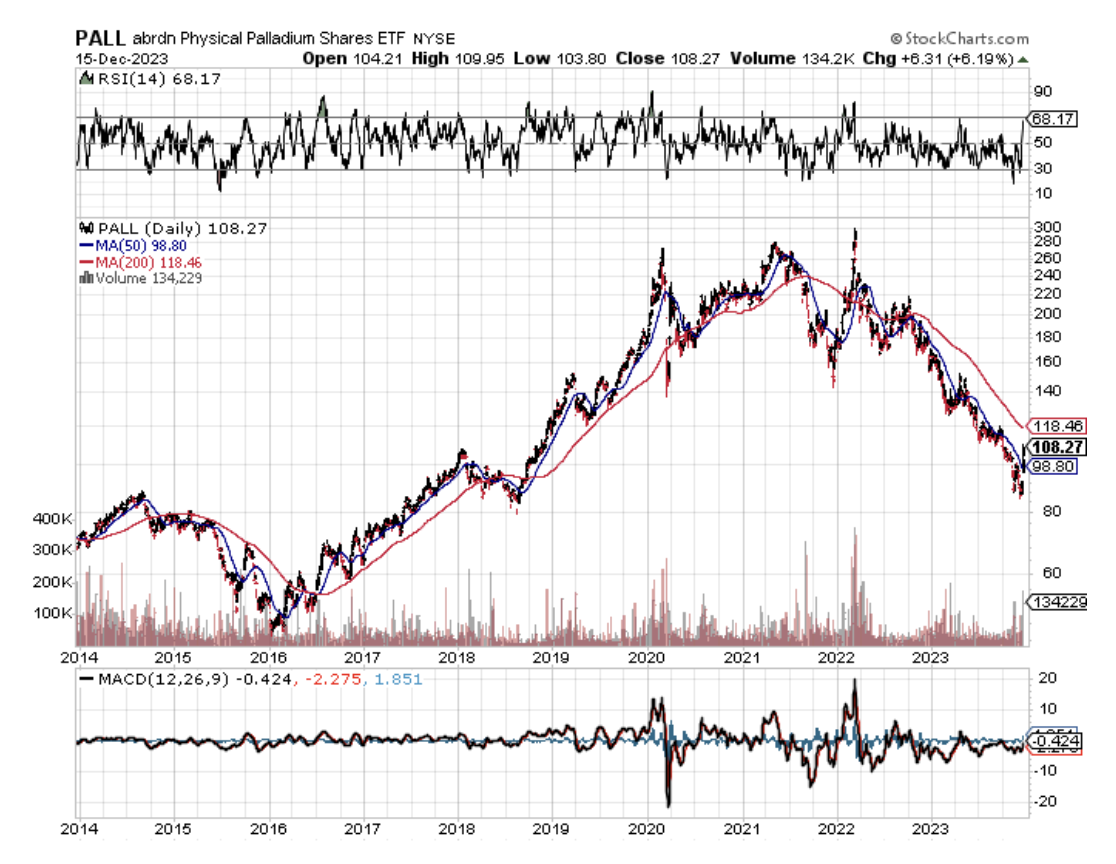

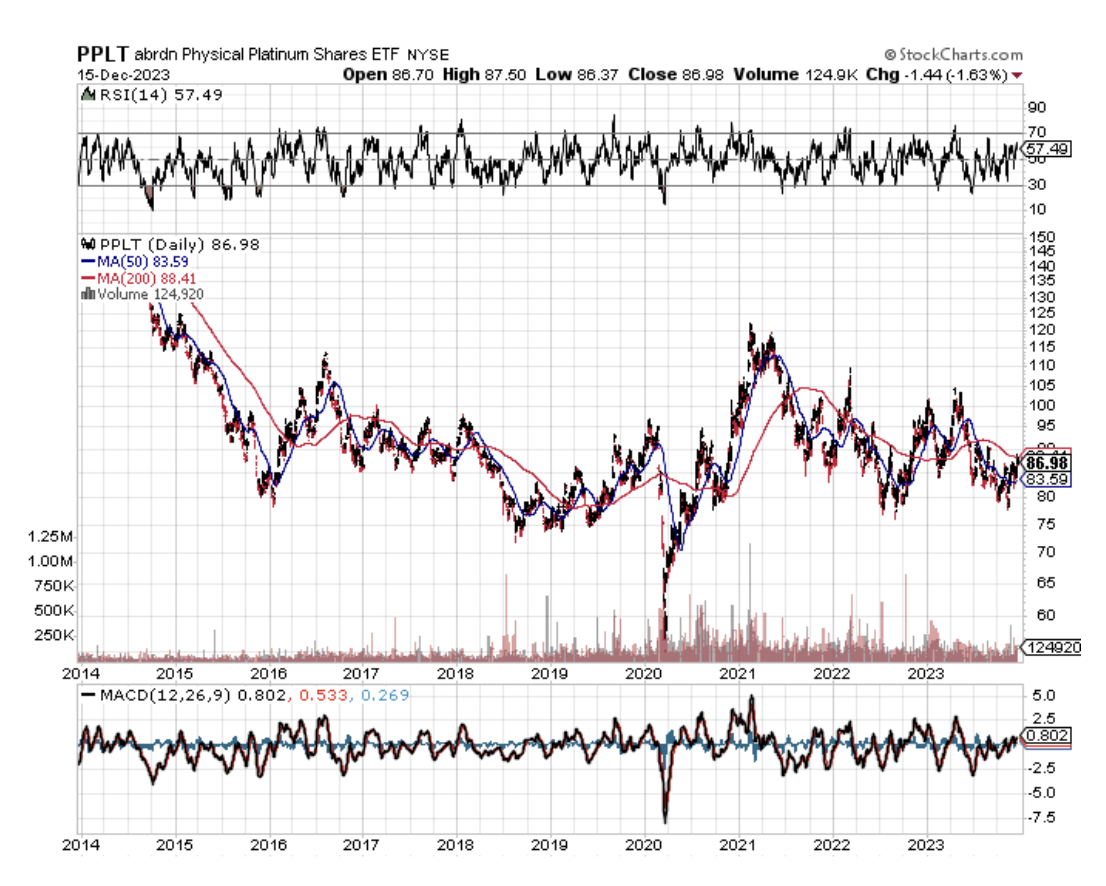

As a result, western hedge funds will soon be moving money out of paper assets, like stocks and bonds, into hard ones, such as gold, silver (SIL), palladium (PALL), platinum (PPLT), and copper.

A massive US stock market rally has sent managers in search of any investment that can’t be created with a printing press. Look at the best-performing sectors this year and they are dominated by the commodity space.

The bulls may be right for as long as a decade thanks to the cruel arithmetic of the commodities cycle. These are your classic textbook inelastic markets.

Mines often take 10-15 years to progress from conception to production. Deposits need to be mapped, plans drafted, permits obtained, infrastructure built, capital raised, and bribes paid in certain countries. By the time they come online, prices have peaked, drowning investors in red ink.

So a 1% rise in demand can trigger a price rise of 50% or more. There are not a lot of substitutes for iron ore. Hedge funds then throw gasoline on the fire with excess leverage and high-frequency trading. That gives us higher highs, to be followed by lower lows.

I am old enough to have lived through a couple of these cycles now, so it is all old news for me. The previous bull legs of supercycles ran from 1870-1913 and 1945-1973. The current one started for the whole range of commodities in 2016. Before that, it was down from seven years.

While the present one is short in terms of years, no one can deny how business cycles will be greatly accelerated by the end of the pandemic.

Some new factors are weighing on miners that didn’t plague them in the past. Reregulation of the US banking system has forced several large players, like JP Morgan (JPM) and Goldman Sachs (GS) to pull out of the industry completely. That impairs trading liquidity and widens spreads— developments that can only accelerate upside price moves.

The prospect of falling US interest rates is also attracting capital. That reduces the opportunity cost of staying in raw metals, which pay neither interest nor dividends.

The future is bright for the resource industry. While the gains in Chinese demand are smaller than they have been in the past, they are off of a much larger base. In 20 years, Chinese GDP has soared from $1 trillion to $14.5 trillion.

Some 20 million people a year are still moving from the countryside to the coastal cities in search of a better standard of living and improved prospects for their children.

That is the good news. The bad news is that it looks like the headaches of Australian parents of juvenile high earners may persist for a lot longer than they wish.

Buy all commodities on dips for the next several years.

Global Market Comments

June 3, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE MALLARD MARKET and ME AND 23 AND ME),

(AAPL), (GOOGL), (AMZN), (TSLA), (MSFT), (META), (AVGO), (LRCX), (SMCI), (NVR), (BKNG), (LLY), (NFLX), (VIX), (COPX), (T), (NVDA), (LEN), (KBH)

There’s nothing like the comfort and self-satisfaction of having a 100% cash position in a falling market. While everyone else is bleeding red ink, I am happily plotting my next trades.

Of course, the rest of the market isn’t really bleeding red ink, just giving up windfall profits. Still, it’s better to trade from a position of strength than weakness. It makes identifying the next winners easier.

Think of this as the “Mallard Market”. On the surface, it seems calm and peaceful, while underwater, it is paddling along like crazy. The damage has been unmistakable. Dell, the faux AI stock (DELL) crashed by 28%, Salesforce (CRM) got creamed for 34%, and ServiceNow (NOW) got taken to the woodshed for 22%.

It all belies a market that is incredibly nervous and fast on the trigger. The tolerance for any bad news is zero. Yet there has been no market crash as I expected. The 5,300 level for the (SPX) seems to possess a gravitational field, powered by $250 earnings per share and a multiple of 51X.

It was NVIDIA that put the writing on the wall by announcing a 10:1 split that has opened the floodgates for similar prosperous and high-priced companies.

There are now 36 stocks with share prices of $500 or more ripe for splits with $7 trillion in market cap, or 16% of the total market. While splits don’t change the value of a company, perceptions are everything, as they prove shareholder-friendly policies. While individual investors are confused by an onslaught of contradictory research recommendations, splits are a great “tell” on what to buy next.

Apple (AAPL), Alphabet (GOOGL), Amazon (AMZN), and Tesla (TSLA) have already carried out splits, some multiple times, to great success. Of the Magnificent Seven, only Microsoft (MSFT) and Meta (META) have yet to split.

In the tech area Broadcom (AVGO), Lam Research (LRCX), Super Micro Computer (SMCI), and Service Now (NOW) have yet to split. In the non-tech area, there are NVR Inc. (NVR), Booking Holdings (BKNG), Eli Lilly (LLY), and Netflix (NFLX). Many of these are well-known Mad Hedge recommended stocks.

History has shown that stocks rise 25% one year after a split compared to 12% for the market as a whole. A stock’s addition to the Dow Average or the S&P 500 (SPY) provides a boost. If both occur, stocks will absolutely explode. Stock splits are also much more attractive than buybacks at these high prices.

So, I’ll be trolling the market for split-happy candidates.

You should too.

Since it may be some time before we capitulate and take a worthwhile run at new highs, I thought I’d update you on the global demographic outlook, which is always a long-term driver of economies and markets.

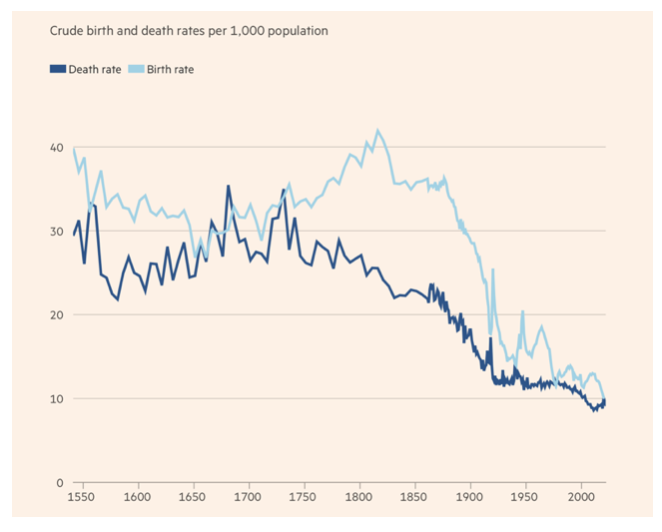

People are now living longer than ever before. But postponing death is only a part of the demographic story. The other is the decline in births. The combination of the two is creating huge changes in the global economy.

The notion of a “demographic transition” is almost a century old. Human societies used to have roughly stable populations, with high mortality matched by high fertility. Families had eight kids and 3-5 usually died in childhood, barely maintaining population growth.

In England and Wales in the 18th and 19th centuries, death rates suddenly plummeted. But fertility did not. The result was a population explosion. As the benefits of economic growth and advances in medicine and public health spread, most of the world has followed a similar transition, but far faster. As a result, human numbers rose fourfold over the last hundred years, from 2 billion to 8 billion.

In time, fertility followed mortality on a downward path across most of the world. As a result, fertility rates in more than half of all countries and territories in 2021 fell below the replacement level. For the world as a whole, the fertility rate was 2.3 in 2021, barely above the replacement of 2.1, down from 4.7 in 1960.

For high-income countries, the fertility rate was a mere 1.6, down from 3.0 in 1960. In general, poor countries still have higher fertility rates than richer ones, but they have been falling there, too.

What explains this collapse in fertility rates? An important part of the answer is the wonderful surprise that more children survived than expected. So, people started to practice various forms of birth control.

But the desire to have many children also shrank sharply. When husbands realized that smaller families meant high standards of living for themselves, family sizes dropped sharply. Even in ultra-conservative Iran, the fertility rate has collapsed from 6.6 in 1980 to only 1.7 in 2021.

A big reason for this shift was that, for their parents, children have moved from being a valuable productive asset in the 19th century to an expensive luxury today. That was back when 50% of our population worked on farms. Today it’s only 2%.

In the meantime, female participation in the economy rose dramatically in the 20th century, including in highly skilled careers. That raised the “opportunity cost” of producing children, especially for mothers. So, they have children later, or even not at all.

Where public childcare is more generous women are encouraged to combine careers with having children. The absence of such help helps explain the exceptionally low fertility rates in much of East Asia and Southern Europe, where parental support is limited.

This global shift towards very low fertility, with the exception (so far) of sub-Saharan Africa, is among the most important events driving the global economy. One implication is that the population of Africa is forecast to be larger than that of all today’s high-income countries, plus China by 2060, thanks to the elimination of many diseases there.

Why is all this important?

Because rising populations create larger markets, more profits for corporations, and rising share prices. Shrinking populations have the opposite effect, as China is learning about its distress now. One reason the US is growing faster than the rest of the world is that a continuous stream of new immigrants since its foundation has created endless numbers of new workers and customers. Dow 240,000 here we come!

Just thought you’d like to know.

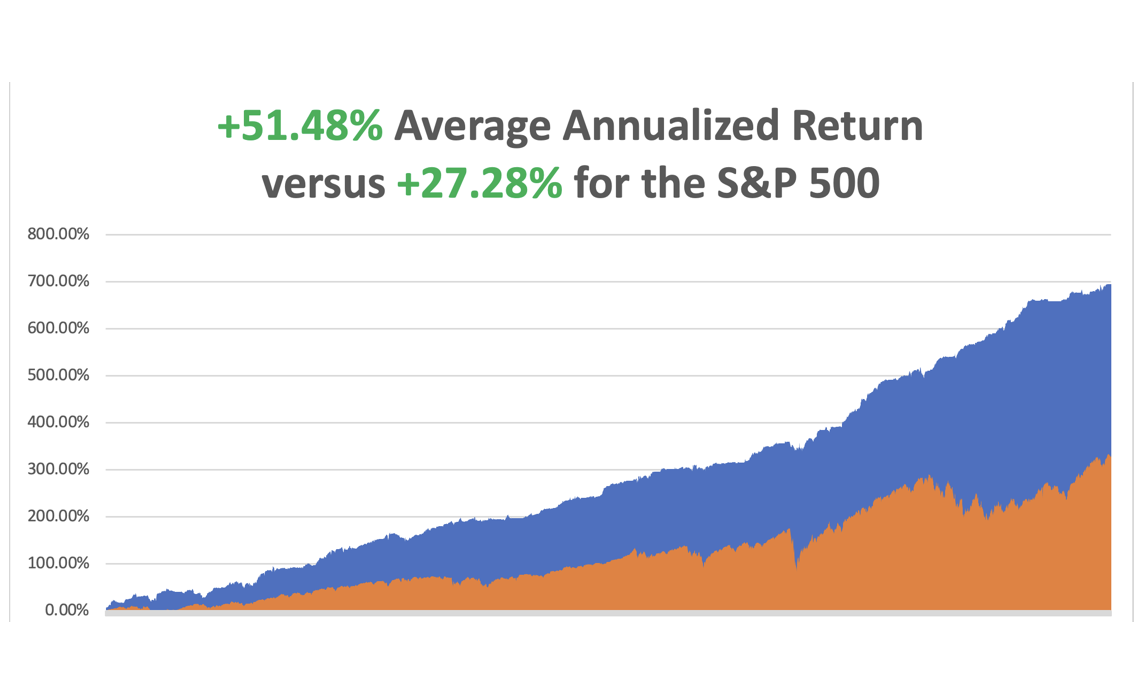

So far in May, we are up +3.74%. My 2024 year-to-date performance is at +18.35%. The S&P 500 (SPY) is up +10.48% so far in 2024. My trailing one-year return reached +35.74%.

That brings my 16-year total return to +694.78%. My average annualized return has recovered to +51.48%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I bailed on my last position early in the week, covering a short in Apple for a profit.

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

The Fed’s Favorite Inflation Gauge Cools by 0.2% in April, with the PCE, or the Personal Consumer Inflation Expectations Price Index. This one strips out the volatile food and energy components. It gives more credibility to a September rate cut and gave bonds a good day.

NVIDIA Shares Continues to Go Ballistic, creating another $800 billion in market capitalization in three trading days. That is the most in history. That took NASDAQ to a new all-time high at 17,000. At $2.8 trillion (NVDA) could become the largest publicly traded company in the world in another day. Today’s tailwind came from an Elon Musk comment that his new xAI start-up would buy the company's high-end H100 graphics cards. Buy (NVDA) on the next 20% dip.

Pending Home Sales Dive, down 7.7% in April, the worst since the Covid market three years ago. The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market. But the anticipated rate cuts later this year should lead to better conditions, with improved affordability and more supply. Buy (LEN) and (KBH) on dips.

Money Supply Rises for the First Time in More than a Year. Remember money supply? As measured by M2, it sums up the currency, coins, and savings deposits held by banks, balances in retail money-market funds, and more. Data for April released on Tuesday afternoon showed an increase of 0.6% from a year ago. The Fed balance sheet has shrunk by $1.5 trillion in two years, the fastest decline in history, slowing the economy.

AT&T’s (T) Copper is Worth More Than the Company, and with plans to convert half its copper network to fiber by 2025 could free up billions of tons of the red metal to sell on the market. Copper prices have doubled over the past two years, and they could double again by next year. Worldwide there are 7 trillion tons of copper wire in place. Fiber is cheaper and exponentially more efficient than copper, which is facing huge demands from AI, EVs, and the electrification of the grid. Buy copper (COPX) on dips.

Markets are Underpricing Low Volatility (VIX), not a good thing at all-time highs. Volatility across equity and currency markets is low. The Volatility Index (VIX) at $12.46 compares with an average over five years of $21.5 and over the longer term of $19.9. Markets are heavily discounting good news and a disinflationary environment. It is not only stocks. There is also low volatility across currency markets. The DB index of foreign exchange volatility is at $6.3 versus an average of $7.6 over five years and $9.3 over the longer term. This will end in tears.

S&P Case Shiller Jumps to New All-Time High, with its National Home Price Index. The index rose by 1.29%, the fastest growth since April 2023. All 20 major metro cities were up last month and gained 6.5% YOY. Four cities are currently at all-time highs: San Diego, Los Angeles, Washington, D.C., and New York. Prices in San Diego saw the biggest gain, up 11.4% from February of 2023. Both Chicago and Detroit reported 8.9% annual increases. Portland, Oregon, saw the smallest gain in the index of just 2.2%. Unaffordability is the big story in the market right now. The sunbelt is seeing the most weakness, thanks to a post-pandemic construction boom.

Space X’s Starlink Tops 3 million Subscribers, and is rapidly moving towards a global WiFi network. I set up a dozen of these in Ukraine last October and even the Russians couldn’t hack them. It sets a global 200 Mb standard usable in most countries, even the remote Galapagos Islands in the Pacific. It’s only a VC investment now but could become Elon Musk’s next trillion-dollar company.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 3, the ISM Manufacturing PMI is released.

On Tuesday, June 4 at 7:00 AM, the JOLTS Job Openings Report will be published.

On Wednesday, June 5 at 7:00 AM, the ISM Services PMI is published.

On Thursday, June 6 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Challenger Job Cuts Report.

On Friday, June 7 at 8:30 AM, the Nonfarm Payroll and headline Unemployment Rate are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when Anne Wojcicki founded 23andMe in 2007, I was not surprised. As a DNA sequencing pioneer at UCLA, I had been expecting it for 35 years. It just came 70 years sooner than I expected.

For a mere $99 back then they could analyze your DNA, learn your family history, and be apprised of your genetic medical risks. But there were also risks. Some early customers learned that their father wasn’t their real father, learned of unknown brothers and sisters, that they had over 100 brothers and sisters (gotta love that Berkeley water polo team!), and other dark family secrets.

So, when someone finally gave me a kit as a birthday present, I proceeded with some foreboding. My mother spent 40 years tracing our family back 1,000 years all the way back to the 1086 English Domesday Book (click here)

I thought it would be interesting to learn how much was actually fact and how much fiction. Suffice it to say that while many questions were answered, alarming new ones were raised.

It turns out that I am descended from a man who lived in Africa 275,000 years ago. I have 311 genes that came from a Neanderthal. I am descended from a woman who lived in the Caucuses 30,000 years ago, which became the foundation of the European race.

I am 13.7% French and German, 13.4% British and Irish, and 1.4% North African (the Moors occupied Sicily for 200 years). Oh, and I am 50% less likely to be a vegetarian (I grew up on a cattle ranch).

I am related to King Louis XVI of France, who was beheaded during the French Revolution, thus explaining my love of Bordeaux wines, women wearing vintage Channel dresses, and pate foie gras.

Although both my grandparents were Italian, making me 50% Italian, I learned there is no such thing as pure Italian. I come out only 40.7% Italian. That’s because a DNA test captures not only my Italian roots, plus everyone who has invaded Italy over the past 250,000 years, which is pretty much everyone.

The real question arose over my native American roots. I am one-sixteenth Cherokee Indian according to family lore, so my DNA reading should have come in at 6.25%. Instead, it showed only 3.25% and that launched a prolonged and determined search.

I discovered that my French ancestors in Carondelet, MO, now a suburb of Saint Louis, learned of rich farmland and easy pickings of gold in California and joined a wagon train headed there in 1866. The train was massacred in Kansas. The adults were all killed, and the young children were adopted into the tribe, including my great X 5 Grandfather Alf Carlat and his brother, then aged four and five.

When the Indian Wars ended in the 1880s, all captives were returned. Alf was taken in by a missionary and sent to an eastern seminary to become a minister. He then returned to the Cherokees to convert them to Christianity. By then, Alf was in his late twenties so he married a Cherokee woman, baptized her, and gave her the name of Minto, as was the practice of the day.

After a great effort, my mother found a picture of Alf & Minto Carlat taken shortly after. You can see that Alf is wearing a tie pin with the letter “C” for his last name Carlat. We puzzled over the picture for decades. Was Minto French or Cherokee? You can decide for yourself.

Then 23andMe delivered the answer. Aha! She was both French and Cherokee, descended from a mountain man who roamed the western wilderness in the 1840s. That is what diluted my own Cherokee DNA from 6.50% to 3.25%. And thus, the mystery was solved.

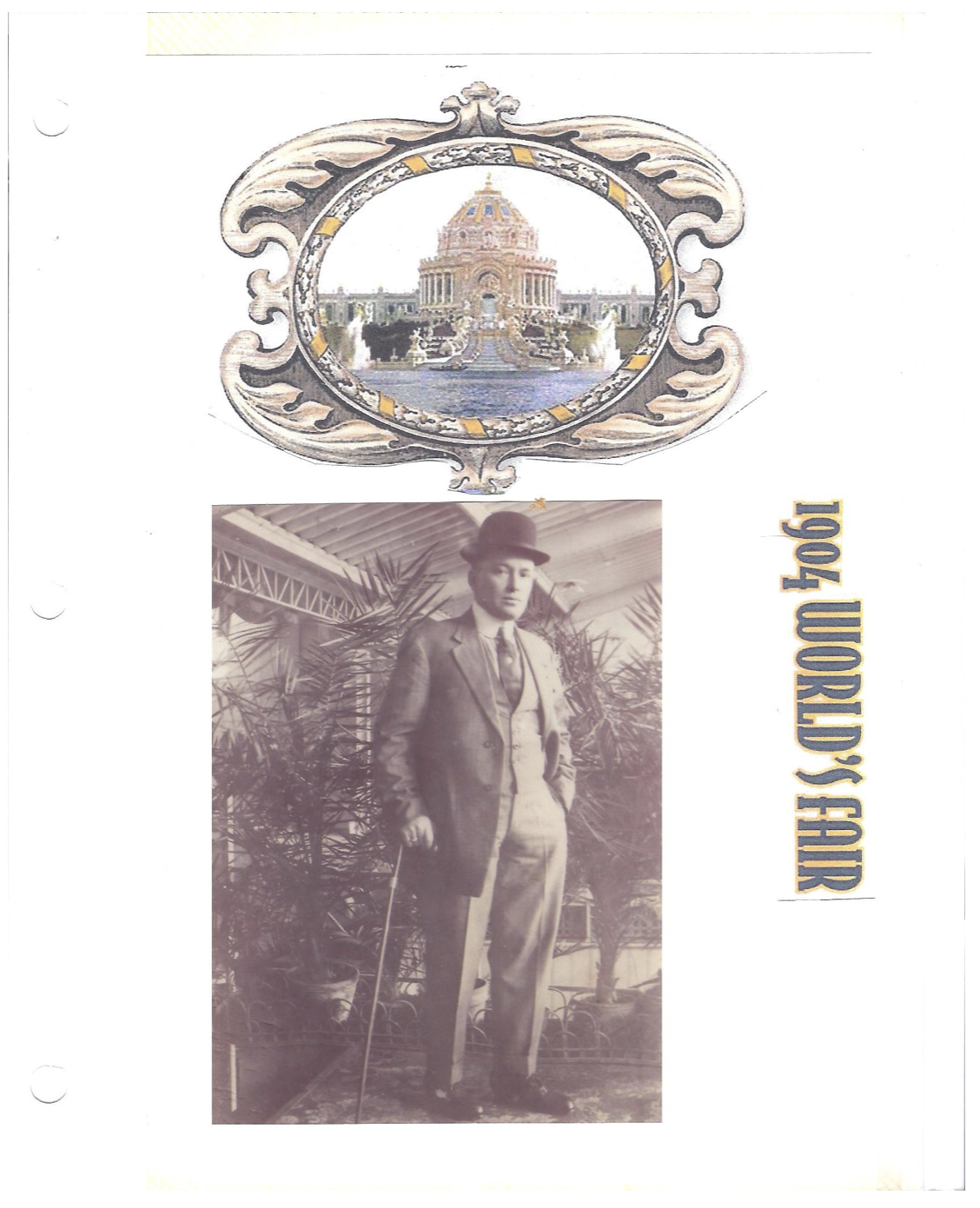

The story has a happy ending. During the 1904 World’s Fair in St. Louis (of Meet Me in St. Louis fame), Alf, then 46, placed an ad in the newspaper looking for anyone missing a brother from the 1866 Kansas massacre. He ran the ad for three months and on the very last day, his brother answered and the two were reunited, both families in tow.

Today, getting your DNA analyzed starts from $119, but with a much larger database, it is far more thorough. To do so, click here.

My DNA Has Gotten Around

It All Started in East Africa

1880 Alf & Minto Carlat, Great X 5 Grandparents

The Long-Lost Brother

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 20, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DOW 40,000 AND HANGING WITH THE AMAZON HEADHUNTERS)

(TLT), (JNK), (WES), (ET), (GLD), (SLV), (MSFT),

(NVDA), (AAPL), (SPY), (FXI), (COPX), (FCX)

When I entered the stock market in 1982 when the Dow was at 600 and you told me the Average would reach 40,000 in 42 years, I would have thought you delusional, out of your mind, and stark raving mad.

Yet, here it is 2024 and here we are, with the index up an eye-popping 66.6 times. The good news is that we are now only one triple away from reaching my long-term target of 120,000. Never underestimate the power of compounding, which my friend Warren Buffet describes as a snowball.

You can’t help but be impressed with the performance of precious metals over the last two weeks, up 6.50% for (GLD) and a ballistic 20% for (SLV). Metals producers are unable to rush supplies to the market fast enough to cover their shorts in the futures market, creating a massive short squeeze.

Long may it continue.

The moves validate my own forecasts for the barbarous relic to hit $3,000 and the white metal to reach $50 sometime in 2025.

One cannot underestimate the power of the weakening economic data over the last fortnight. As a result, we have gone from “Higher for longer” to “Lower sooner”, with huge consequences for all asset classes.

That brings to the fore investment in fixed-income securities. There are two ways to make money on a fixed income. Coupon interest rates are still at historically high levels. And as rates fall, fixed-income prices rise, opening the door to capital gains, which could reach 10%-20% in the coming year.

The fixed-income market, at $100 trillion is double the size of the stock market. And there are many more bond listings than stock ones. So the number of possible investments is almost endless. I shall give you a brief overview of some of the more interesting subsectors.

US Government bonds – are the gold standard with a guaranteed return. But you pay for the extra security with lower rates; the current ten-year US Treasury bond yield is 4.42%, much lower than the present 90-day T-bill of 5.25%. The easiest way to buy these is through the (TLT). The 30-year government bond should be avoided as the extra 0.14% in yield doesn’t adequately compensate you for the extra 20 years of risk

Junk Bonds – Also known as “high yield” bonds have always been misnamed. The default rates never remotely approached the levels that justified their high yields, not even during the financial crisis, as my old friend former junk bond king Michael Milliken has amply proven. The (JNK) is currently yielding 6.59% and has the potential for larger capital gains than government bonds.

Master Limited Partnerships – These are partnerships granted generous tax benefits with the goal of producing oil. They issue annual Form K-1’s to include with your tax return. Dividends are deferred until the MLP’s investment reaches the end of its useful lives, which can be decades. MLP’s used to be a huge industry with dozens of listed companies.

When the price of oil went to negative numbers during the pandemic, most of them got wiped out. Because of this rocky past, there are a handful of large, well-capitalized MLP’s that with extremely high yields. One is Western Midstream Partners (WES) with a 9.20% yield. Energy Transfer Partners (ET) pay a 7.96% yield.

These yields will remain safe as long as oil prices are stable or rising, as I expect in a long-term global economic recovery. Take oil back to zero again in another pandemic and these returns will get turned on their head.

With the normalizing of interest rates, it's time to normalize investment strategies as well. That means bringing back the old 60/40 strategy where one half of the portfolio ensures the other, with a modern twist. You can put 60% of your assets in stocks, with half on technology and half on domestic cyclicals.

The other 40% should be allocated to some mix of the above fixed-income investments guaranteeing annual high returns. In not a bad strategy for mature investors, especially if they would rather be on a golf course instead of spending all day in front of a screen picking bottoms and tops for stocks, like Millennials.

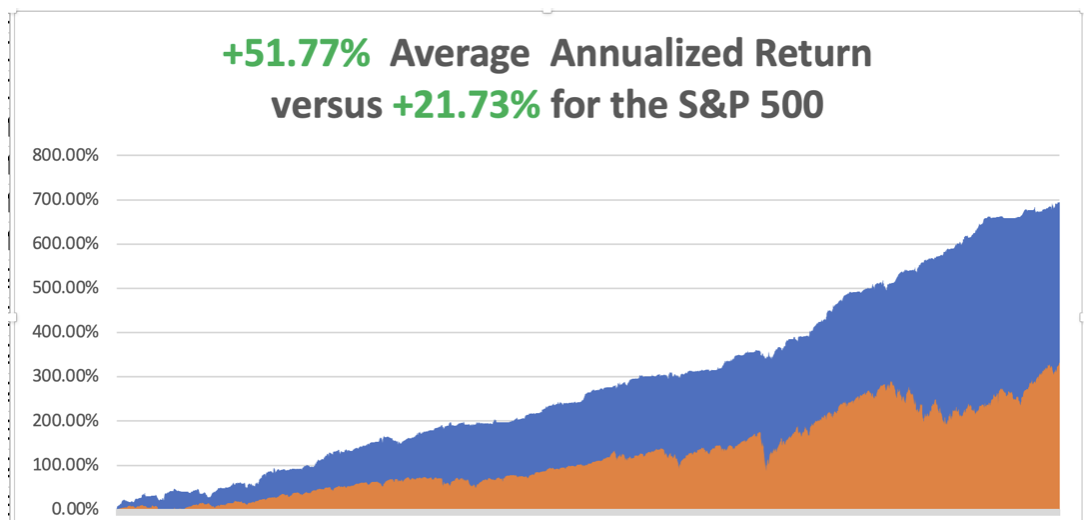

So far in May, we are up +3.01%. My 2024 year-to-date performance is at +17.62%. The S&P 500 (SPY) is up +10.90% so far in 2024. My trailing one-year return reached +32.80% versus +29.02% for the S&P 500.

That brings my 16-year total return to +694.56%. My average annualized return has recovered to +51.77%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I let my (GLD) and (SLV) positions expire at max profit. I did the same with my (MSFT) short. I sold my (NVDA) and (TLT) shorts for a nice profit. That leaves me with just two positions, a long in (SLV), which has gone ballistic, and a short in (AAPL).

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

The Bull Market has Five More Years to Run, with S&P 500 (SPY) growing earnings at 10% a year for the foreseeable future. Last year brought in $222 per share, 2024 will see $250, 2025 $270, and $300 for 2026. The Great American Golden Age has only just begun. Profit margins will expand to all-time record highs. Falling rates and a weak dollar will boost exports to a recovering Europe and Japan. Inflation should hit the Fed’s 2% in 2025 as AI chatbots replace workers at a breakneck rate, cutting costs dramatically. The future is happening fast. Buy everything on dips, even bonds.

CPI Comes in Cool, in April at 0.3% versus 0.4% expected, taking stocks to new all-time highs. Inflation resumed its downward trend at the start of the second quarter in a boost to financial market expectations for a September interest rate cut. Buy em!

PPI Comes in Hot at 0.5%, and up 2.2% YOY, putting up another potential roadblock to interest rate cuts anytime soon. The PPI is a gauge of prices received at the wholesale level that came in higher than the 0.3% estimate. Higher for longer rules. The last mile, or the last 1$ drop in inflation is always the hardest and usually requires a recession. Higher for longer rules.

Retail Sales Come in Surprisingly Flat in April, setting up a Goldilocks economy for the Fed to cut rates in September. The unchanged reading in retail sales last month followed a slightly downwardly revised 0.6% increase in March, the Commerce Department's Census Bureau said on Wednesday. Retail sales were previously reported to have risen 0.7% in March.

Biden to Increase China Tariffs (FXI) to 100%, on key sectors including electric vehicles, batteries, solar cells, steel, and aluminum. Biden has previously announced the steel and aluminum tariffs, which will increase to 25% on some products that have a 7.5% rate or no tariffs now. The EV rate aims to protect the US from a potential flood of Chinese autos that could upend the politically sensitive auto sector. The total tariff on Chinese electric vehicles will rise to 102.5% from 27.5. Biden’s union support is clear for all to see.

Copper Hits Record Highs, as hedge funds, trend followers, bearish shorts, and Chinese speculators pile in. New York prices hit $5 a pound, while London reached $11,000 per metric tonne. The price action is similar to other commodities with disrupted supplies like Cocoa and Nickel. The runaway market will continue. Buy (FCX) and (COPX) on dips.

As the Dow Tops 40,000, investors are pouring money into both bonds and stocks, according to the Bank of America. Equity funds saw $11.9 billion in inflows, while bond funds drew in $11.7 billion. Within fixed income, Treasury inflation-protected securities (TIPS) saw outflows of $700 million, the most in nine weeks. Keep buying those dips.

Weekly Jobless Claims Drop 10,000, to 222,000, after seasonal factors caused a significant increase in New York claims in the prior week. The four-week moving average, which helps smooth short-term fluctuations in weekly claims figures, increased to 217,750, the highest level since November.

Solar Storm Hits Starlink, taking out several hundred satellites and degrading service, says Elon Musk. Starlink, the satellite arm of Elon Musk's SpaceX, is suffering as the Earth is battered by the biggest geomagnetic storm due to solar activity in two decades. Starlink owns around 60% of the roughly 7,500 satellites orbiting Earth and is a dominant player in satellite internet. The U.S. National Oceanic and Atmospheric Administration has said the storm is the biggest since October 2003 and is likely to persist over the weekend, posing risks to navigation systems, power grids, and satellite navigation.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 20, nothing of note takes place.

On Tuesday, May 21 at 1:30 PM EST, API Crude Oil Stocks are released.

On Wednesday, May 22 at 2:00 PM, the Existing Homes Sales are published

On Thursday, May 23 at 7:00 AM, we get New Home Sales. And at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, May 24 at 8:30 AM, the Durable Goods Report is announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, when I crossed the Continental Divide at 13,300 in the Andes Mountains of Ecuador last week, the vast expanse of the Amazon Basin lay before me. Clouds danced in and out of the treetops, waterfalls plunged down precipitous slopes, and the jungle spread out for 2,000 miles east. I was somewhat buzzed by the altitude but still enjoyed every minute.

My destination was the Termos Papallacta spa on the slopes of an ancient volcano which offered steaming hot sulfuric waters and a brisk massage for $50. Colorful exotic flowers abounded. This is where the wealthy of Quito come to salve arthritis and aches and pains in magical waters.

How do you get wealthy in Ecuador? Bananas, tourism, real estate speculation, and flower exports to the US. Given my experience with Japanese onsens, I had no problem with their ultra-hot waters.

This is the land of the Jivaro Clan, the world’s last known headhunters. Their final victim was a National Geographic Society explorer in 1961. Recently, his grandson traveled to Ecuador to retrieve the head and return it to the US for a respectful burial, all to great fanfare in the local press. The Jivaro still shrinks heads, but only of animals which they sell to tourists just to keep the practice alive.

Ecuador is the great test bed for monetary experts around the world. In 1999, they suffered a financial crisis where the value of their currency, the Sucre, collapsed to 25,000 to the dollar. The central bank responded by changing the national currency to the US dollar and only permitting conversion from the old currency at $2 per person.

The move had several unintended consequences. The savings of everyone in the country were wiped out overnight. But it also eliminated their debt. Those with relatives sending back remittances from the US suddenly became wealthy and bought up all the real estate they could. In the end, it created an economic boom that continues to today.

Today, Ecuador is one of the friendliest, and cheapest countries in South America. It elected Daniel Noboa as president in 2023, the scion of a banana fortune, who has been hugely popular. The government cracked down on the drug gangs, arresting everyone with a suspect tattoo. Today the police and army are everywhere, and the streets are safe. There are armed checkpoints at key intersections. The ownership of firearms and even long knives has been banned.

The country has no seasons, sitting right on the Equator, and is temperate all year long. Even at 13,300 feet, there is no snow. I had no problem with the food, but then I had a cast iron stomach battle-tested in 135 countries. Not even the locals drink the tap water, which is only used for washing. It has to be all bottled water all the time or you die and you often see people lugging around one-gallon bottles.

Retiring Americans have noticed and some 20,000 now live in the country on their Social Security checks at one-third the cost of home. They concentrate on cultural hot spots, like the ancient city of Cuenca, where the local hospitals speak English, are experts in gerontology, and accept Medicare. You can buy a nice home in a mountain urban area for $250,000 and beachfront digs for $500,000. The Marriot Hotel in Quito cost me $160 a night and a steak dinner was $19 and to die for.

You can’t go to Quito without visiting the Equator for which the country was named, a tourist mecca where everyone gets pictures straddling the northern and southern hemispheres. The country has two summer solstices a year, one in the spring and one in the fall, as the sun transits from north to south, then south to north.

I passed on the shrunken head, which I thought grotesque, and got the T-shirt instead. Besides, US Customs might have questions (Do you have any shrunken heads to declare?). I think I’ll be returning to Ecuador soon.

Descending into the Amazon

Jivaro Indian

Shopping for Breakfast

A Slow Day at the Flower Market

A Smoothie for Lunch

Standing on the Equator, One Foot in Each Hemisphere

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 16, 2024

Fiat Lux

Featured Trade:

(THE COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)