Global Market Comments

April 29, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DIGESTION TIME)

(NVDA), (FCX), (META), (MSFT), (TLT), (TSLA), (AAPL), (VISA), (FCX), (COPX), (GOOGL),

(A TRIP TO CUBA)

Global Market Comments

April 29, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DIGESTION TIME)

(NVDA), (FCX), (META), (MSFT), (TLT), (TSLA), (AAPL), (VISA), (FCX), (COPX), (GOOGL),

(A TRIP TO CUBA)

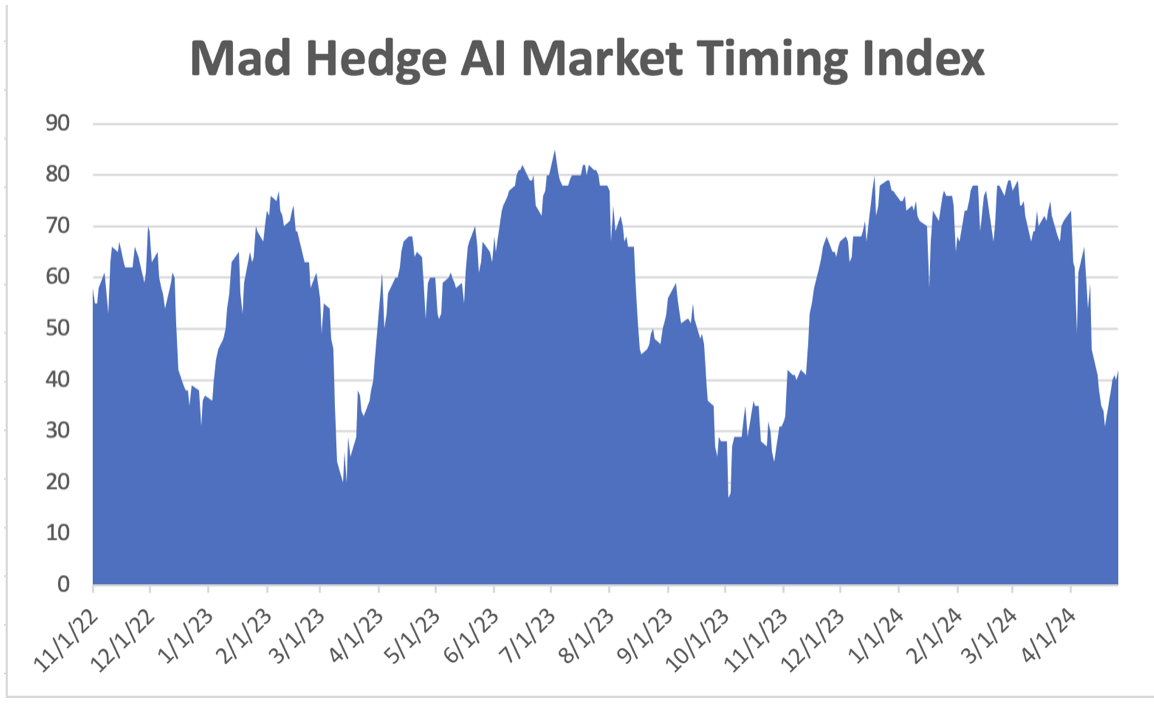

Before you even ask, I’ll give you the answer you’ve all been waiting for: It’s too late to sell and too early to buy.

Stocks may still have some digesting to do having soared by 27% in six months. Nobody wants to look like an idiot by buying a market top. As I have learned over the decades, investors fear looking stupid more than they fear losing money, especially if they are professionals.

Everyone knows the market is eventually going higher so they are not selling in any meaningful way unless they are short-term, algos, or day traders.

This means we may have a whole lot of nothing going on in the coming weeks or months.

That leaves us time to examine the most interesting trends going on in the markets right now, especially the new bull market in commodities. Believe it or not, we are still unwinding the long-term effects of Covid 19 and commodities have only recently come to the fore.

Remember Covid?

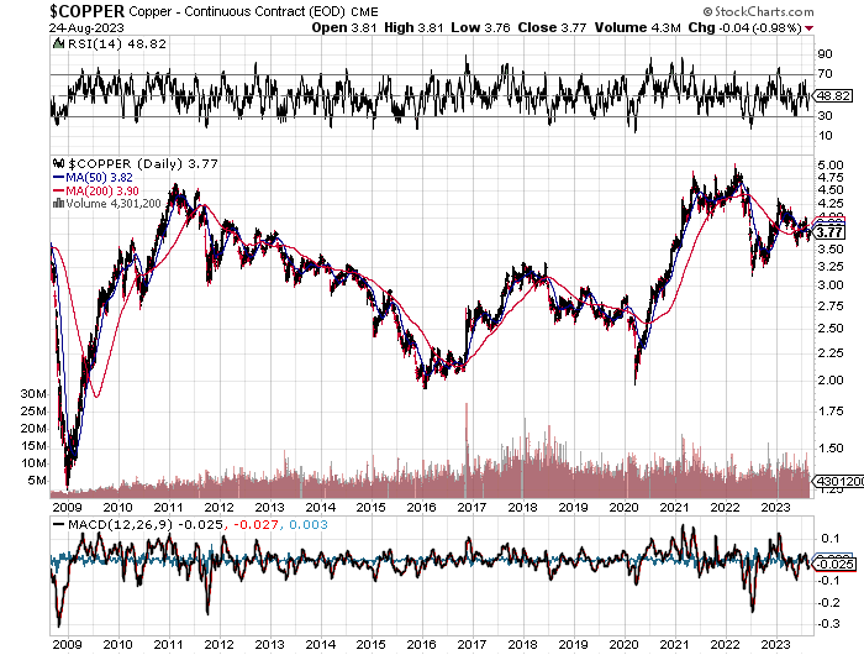

Since October, copper prices have risen by 22%, oil by 23%, gold by 34%, and uranium by a gobsmacking 83%. What’s causing this sudden new interest? It’s not a recovering Chinese economy, that’s for sure. Investors have been waiting for a bounce back in the Middle Kingdom seemingly forever. But China remains hobbled by the bitter fruit of a 40-year one-child policy and an ineffective government. History tells us that the United States does not make a great enemy.

So what’s driving the new demand? Remember Covid? Believe it or not, we are still unwinding the long-term effects of Covid 19 and commodities have only recently started to play catch up.

Commodities are unique in that they have such a long lead time to add new supply. It can take 5-10 years, to map out new sites, get government approvals, deliver heavy equipment, and mine, process, refine, and ship the final product.

In the meantime, enormous new demand has arisen. There have been 10 million EVs manufactured in recent years and each one needs 200 pounds of copper. AI means the electric power grid has to double in size quickly. Commodity markets are unable to meet the supply. Therefore, prices can only go up.

That enabled Freeport McMoRan (FCX), the world’s largest copper producer, to handily beat its earnings expectations, helped by higher production and easing costs. The mining giant said its quarterly production of copper rose to 1.1 billion pounds from 965 million pounds a year earlier, helped by a 49% jump in output from its Indonesia operations. (FCX) said it was working with the Indonesian government, which has put a ban on raw material exports, to obtain approvals to continue shipping copper concentrates and anode slimes. Its current license is set to expire in May. Buy (FCX) and (COPX) on dips.

Corporate raiders have taken notice.

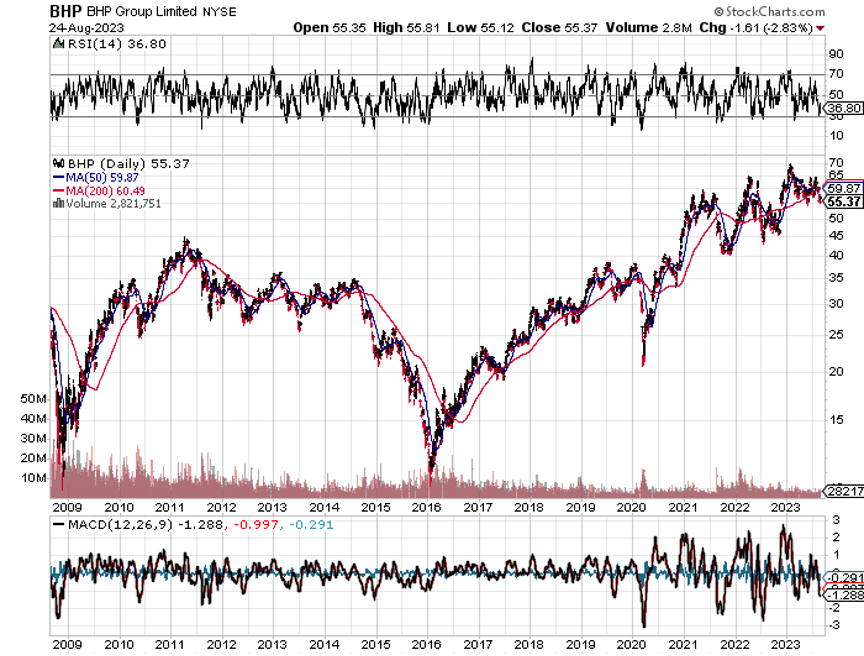

Activist Elliot is taking a Run at Mining Giant Anglo American, accumulating a $1 billion stake. BHP, the largest iron ore miner, is also making a takeover bid here on the coattails of which Elliot is trying to ride. It just highlights the global interest in mining shares.

Anglo American plc is a British multinational mining company that is the world's largest producer of platinum, with around 40% of world output, as well as being a major producer of diamonds, copper, nickel, iron ore, polyhalite, and steelmaking coal. On a side note, copper hit a two-year high above $10,000 per metric tonne in the London Market last week.

Needless to say, the commodity boom could continue for another decade.

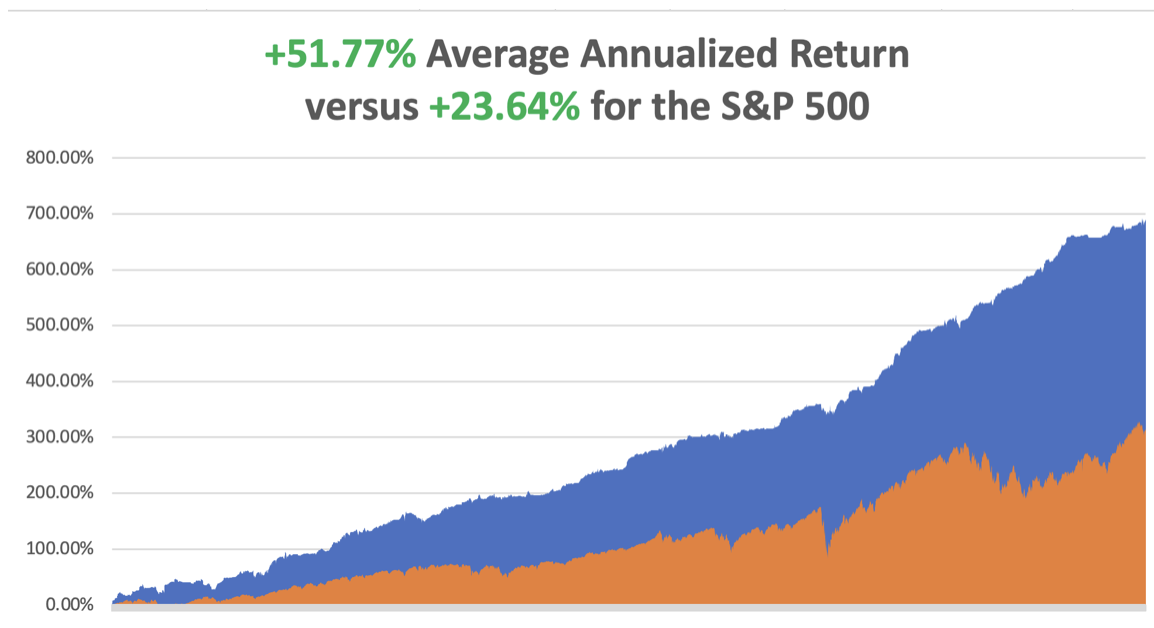

So far in April, we are up +4.24%. My 2024 year-to-date performance is at +13.61%. The S&P 500 (SPY) is up +6.50% so far in 2024. My trailing one-year return reached +32.40% versus +23.14% for the S&P 500.

That brings my 16-year total return to +690.24%. My average annualized return has recovered to +51.77%.

Some 63 of my 70 round trips were profitable in 2023. Some 25 of 33 trades have been profitable so far in 2024.

Tesla Delivers Worst Earnings in 12 Years, with a 9% revenue drop, but the stock rallies big as the disappointment was well telegraphed. Revenue declined from $23.33 billion a year earlier and from $25.17 billion in the fourth quarter. Net income dropped 55% to $1.13 billion, or 34 cents a share, from $2.51 billion, or 73 cents a share, a year ago. The drop in sales was even steeper than the company’s last decline in 2020, which was due to disrupted production during the Covid-19 pandemic. Tesla’s automotive revenue declined 13% year over year to $17.38 billion in the first three months of 2024. I’ll watch (TSLA) from the sidelines from now.

Personal Consumption Expenditures (PCE) Comes in Warm for March, up 2.8% YOY, the same as for February. Service prices led. But the numbers were not as hot as feared so both bonds and stocks rose.

Big Tech Crashes, with all of the Magnificent Seven breaking 50-day moving averages. (NVDA) alone gave up 10% on Friday. The next stop is the 200-day moving averages, which are far, far away. If those hold this is just a correction. If they don’t the bear market is back.

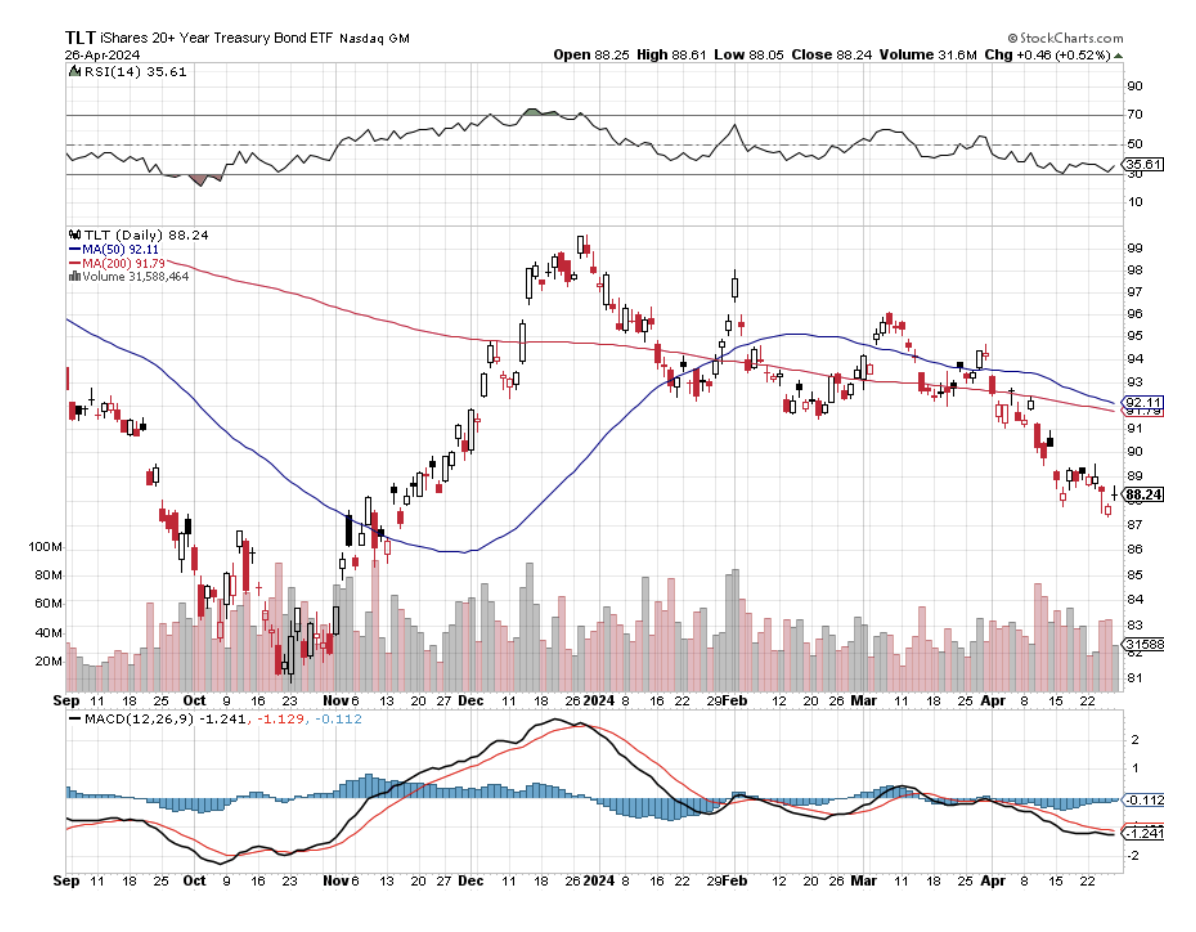

Biggest Treasury Bill Auction in History is a Huge Success, at $69 billion for a two-year paper with a 4.898% yield. That is almost a risk-free government-guaranteed 10% yield in two years. Another $70 billion of five-year notes go on sale today. Half of this is going to foreign investors and central banks. Faith in America and the US dollar remains strong. Who else’s bonds would you rather buy? Passage of the Ukraine aid bill was probably a help. Wait for (TLT) to bottom.

Visa Pops on Earnings Beat, continuing as the powerhouse that it has been for years. Reported at $4.7 billion, showing a 10% increase year-over-year, slightly above the estimate of $4.943 billion. Visa is a call option on the growth of the Internet. Buy (V) on dips.

Apple China Sales Dive, by 19% as Chinese switch to cheaper Huawei phones for nationalism reasons. It’s also another sign of a slow Chinese economy. China remains one of the company’s biggest markets, but business there has grown harder after Beijing escalated a ban on foreign devices in state-backed firms and government agencies. Avoid (AAPL) until the turnaround.

Alphabet Earnings Beat Delivers Monster 10% Move, recovering a $2 trillion market cap. It also announced its first-ever dividend and a $70 billion share back, the second largest after Apple. Buy (GOOGL) on dips.

March New Home Sales Jump, by 8.1% when only 1.1% is expected, to 693,000. The median price of a home sold fell to $430,700 as builders pulled back on incentives like those cherry cabinets. It’s an uphill slog with those 7.0% mortgage rates.

CDC Birth Data Fall to Lowest Level Since the Great Depression, 1.1 births per 1,000 people. That is well below the Great Depression levels. Only 3,664,292 new Americans were born in 2021. It means there will be a shortage of consumers in 20 years so be out of stock by then. The good news is that Covid deaths have fallen from 4,000 per day to only 19 a day since January 2020.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 29, at 10:30 AM EST, the Dallas Fed Manufacturing Index is announced.

On Tuesday, April 30 at 9:00 AM, S&P Case Shiller National Home Price Index is released.

On Wednesday, May 1 at 2:00 PM, the ADP Private Employment Change report will be published

On Thursday, May 2 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, May 3 at 8:30 AM, the April Nonfarm Payroll Report is announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I have wanted to visit Cuba for decades. But relations with the US have run hot and cold over the years and whenever I had the time and money to go, the was a chill on, sometimes an extreme one.

So when I arrived in Key West and learned they were offering Cuba tour packages, I jumped at the chance. Unfortunately, you need to book three months in advance so that option was out.

Then I thought, “Why not fly there myself?” After payment of some hefty fees, commissions, and some outright bribes, I scored a Cuban visa and an aging Britten-Norman Islander twin built in the UK some 40 years ago. It was perhaps the smallest twin I have ever flown, with two minuscule 270 horsepower engines.

Although it was only 90 miles to Cuba, I had to load up with full tanks. Cuban aviation fuel is often contaminated with sludge or water and is unsafe to use. Losing both engines over shark-infested waters doesn’t fit in with my retirement plan. So I needed enough 100LL avgas to make the round drip, which meant skipping breakfast to stay within my weight limitations.

It was a clear and balmy morning when I received my clearance for takeoff, the sky dotted with fluffy white cumulus clouds. Of course, I had to skirt the Bermuda Triangle to get there, but no worries.

Amazingly Cuban air traffic control spoke English. Soon, the green hills of Cuba appeared on the horizon, and I received the words I will never forget: “N686KW you are cleared for landing in Havana.” I haven’t felt like that since I last landed in Moscow.

Much to my surprise, I found other US aircraft there as I was parked near jets from Southwest and American Airlines. I was greeted by an immigration officer who escorted me into the country, putting my Spanish skills to the test.

I had some concerns that I might be arrested in case Russia put me on a wanted list due to my recent work in Ukraine. But my fears proved unwarranted. You see, you get paranoid in your old age. A private car, a French Citroen van, a driver, and a government guide were waiting for me outside the airport.

Suddenly, I found myself in a strange new world. A darkly tanned people wore tired polyester clothes. Everyone was rail thin and the only obese people I saw were foreign tourists. There was an incredible variety of vehicles on the road, including ancient cars from Russia, China, Poland, and Japan. Apparently, Chevrolet had a great year in Cuba in 1956 because no American cars have entered the country since then and they are everywhere.

We headed straight for Earnest Hemingway’s Cuban home, known as Finca Vigia, or “Lookout Farm” built in 1886 on a hilltop overlooking Havana. The building was falling apart and showed large cracks, but going inside I was transported in time back to 1960, when Hemingway left the property ahead of the Cuban Revolution.

Finca Vigia has been untouched since. The walls are covered with an assortment of hunting trophies from Africa, including springboks, cape buffalo, lions, and leopards. They were collections of African spears and gun cases. Mounted on the walls were paintings of bullfights in Spain, cartoons about Hemingway, and family photos.

Magazine racks were stuffed with the 1960 issues of Life, Look, and The Saturday Evening Post. The National Geographic issues looked positively prehistoric. And there were thousands of books. Anyone who read his books would recognize all of this.

Hem, as his friends called him, bought the property in 1940 for $8,000, living there with wife three for five years, the famed war correspondent Martha Gellhorn, and wife four, Time magazine reporter Mary Welsch, who became his widow.

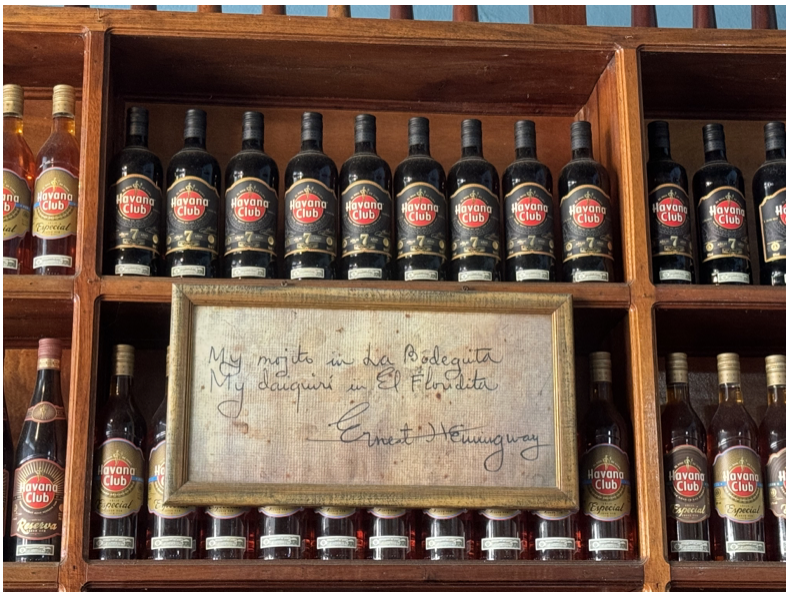

After passing on a Che Guevara T-shirt in the gift shop, I enjoyed a glass of freshly squeezed sugar cane juice. Then I headed into Havana, escorted by my guide, Eliar. The trip turned into a Hemingway bar crawl. I visited the well-known La Floridita, which made Hem’s favorite Daiquiri, La Bodegita, which mixed the best mojito and had lunch at his favorite roof terrace restaurant.

Cuba has long been one of the worst-managed countries in the world, second only to North Korea, and I learned why after grilling my guide all day about economic conditions. It’s 11.2 million people earn a per capita of $11,255, with 71% living below the poverty line. The real figure is a third of that as there are now 300 pesos to the US dollar, not the fictitious 120 that the government pretends.

When the Soviet Union collapsed in 1992, generous subsidies ended and Cuba quickly lost 33% of its GDP. With some of the richest farmland in the world, it imports 80% of its food and is currently suffering a food crisis. Even the bottled water I drank came from Panama.

Oil accounts for 100% of its energy supply which mostly comes from Russia and is paid for with raw sugar. Cuba’s largest exports are tobacco, nickel, and zinc most of which are exported to China. China also provided $11 billion in loans which Cuba promptly defaulted on.

The country would have been much better off if only Fidel Castro had accepted an offer from the Washington Senators to play US major league baseball in the early 1950s. Cuba is officially one of the last communist countries in the world, with Russia and China abandoning it years ago. After reforms in the 1990s, what they now practice is an odd mixture of communism and capitalism, with the government and the private sector competing side by side.

With thousands fleeing the country every year the real estate market has collapsed. You can buy a two-bedroom apartment in Havana for $30,000. Flying over the countryside at low altitude you fund vast expanses of agricultural land undeveloped for want of machinery and parts. There is unused labor everywhere. Cuba should be one of the richest countries in the world with all those beaches. The tourism possibilities are enormous. But with a 60-year trade and investment ban from the US, nothing can happen.

American credit cards and cell phones don’t work, so I brought in $200 in ones. You can’t bring back to the US the country’s only two worthy exports, rum and cigars. But there are buskers everywhere and by the end of the trip, I ended up giving it all away in tips. I did OK with the food, but only ate overcooked meals in high-end restaurants. Salads were out of the question but drink all the local beer and rum you can.

I ended my trip with a tour of the enormous Revolution Square where Fidel Castro used to give four-hour speeches to one million. One area the government did not skimp on spending was on the massive ministry buildings that surround the square. It seems the image of a strong government, especially the police, is essential in a workers’ socialist paradise.

Then it was back to the airport where surprisingly I obtained immediate clearance for takeoff. No passport stamps, as the government wanted to leave no evidence of my visit in an American passport. I returned to Key West just in time to catch a magnificent sunset over the Gulf of Mexico. US customs recognized my face and waved me right through.

Damn! Should have picked up some of those $5 bottles of rum.

It's all just another day in the life of John Thomas.

At Hemingway’s Cuban Home

A Look Back into 1960

Where Hem Wrote “Old Man and the Sea”, Standing

Hemingway’s Office

I passed on Che

Meeting an Old Friend for a Round at Floridita

Mixing it up with the Locals

One of Cuba’s Only Exports

Looks Like Chevy had a Great Year in 1956

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

December 26, 2023

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPERCYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

August 25, 2023

Fiat Lux

Featured Trades:

(THE NEXT COMMODITY SUPERCYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

CLICK HERE to download today's position sheet.

When I closed out my position in Freeport McMoRan (FCX) near its max profit earlier this year, I received a hurried email from a reader if he should still keep the stock. I replied very quickly:

“Hell, yes!”

When I toured Australia a couple of years ago, I couldn’t help but notice a surprising number of fresh-faced young people driving luxury Ferraris, Lamborghinis, and Porsches.

I remarked to my Aussie friend that there must be a lot of indulgent parents in The Lucky Country these days. “It’s not the parents who are buying these cars,” he remarked, “It’s the kids.”

He went on to explain that the mining boom had driven wages for skilled labor to spectacular levels. Workers in their early twenties could earn as much as $200,000 a year, with generous benefits.

The big resource companies flew them by private jet a thousand miles to remote locations where they toiled at four-week on, four-week off schedules.

This was creating social problems, as it is tough for parents to manage offspring who make far more than they do.

The Next Great Commodity Boom has started and, in fact, we are already years into a prolonged supercycle that could stretch into the 2030s.

China, the world’s largest consumer of commodities, is currently stimulating its economy on multiple fronts, to break the back of a Covid hangover.

Those include generous corporate tax breaks, relaxed reserve requirements, government bailouts of financial institutions, and interest rate cuts. Get triggers like the impending moderation of its trade war with the US and it will be off to the races once more for the entire sector.

The last bear market in commodities was certainly punishing. From the 2011 peaks, copper (COPX) shed 65%, gold (GLD) gave back 47%, and iron ore was cut by 78%. One research house estimated that some $150 billion in resource projects in Australia were suspended or cancelled.

Budgeted capital spending during 2012-2015 was slashed by a blood-curdling 30%. Contract negotiations for price breaks demanded by end consumers broke out like a bad case of chicken pox.

The shellacking was reflected in the major producer shares, like BHP Billiton (BHP), Freeport McMoRan (FCX), and Rio Tinto (RIO), with prices down by half or more. Write-downs of asset values became epidemic at many of these firms.

The selloff was especially punishing for the gold miners, with lead firm Barrack Gold (GOLD) seeing its stock down by nearly 80% at one point, lower than the darkest days of the 2008-9 stock market crash.

You also saw the bloodshed in the currencies of commodity-producing countries. The Australian dollar led the retreat, falling 30%. The South African Rand has also taken it on the nose, off 30%. In Canada, the Loonie got cooked.

The impact of China cannot be underestimated. In 2012, it consumed 11.7% of the planet’s oil, 40% of its copper, 46% of its iron ore, 46% of its aluminum, and 50% of its coal. It is much smaller than that today, with its annual growth rate dropping by more than half, from 13.7% to 3.50% today.

What happens to commodity prices when China recovers even a fraction of the heady growth rates of yore? It boggles the mind.

The rise of emerging market standards of living will also provide a boost to hard asset prices. As China goes, so does its satellite trading partners, who rely on the Middle Kingdom as their largest customer. Many are also major commodity exporters themselves, like Chile (ECH), Brazil (EWZ), and Indonesia (IDX), who are looking to come back big time.

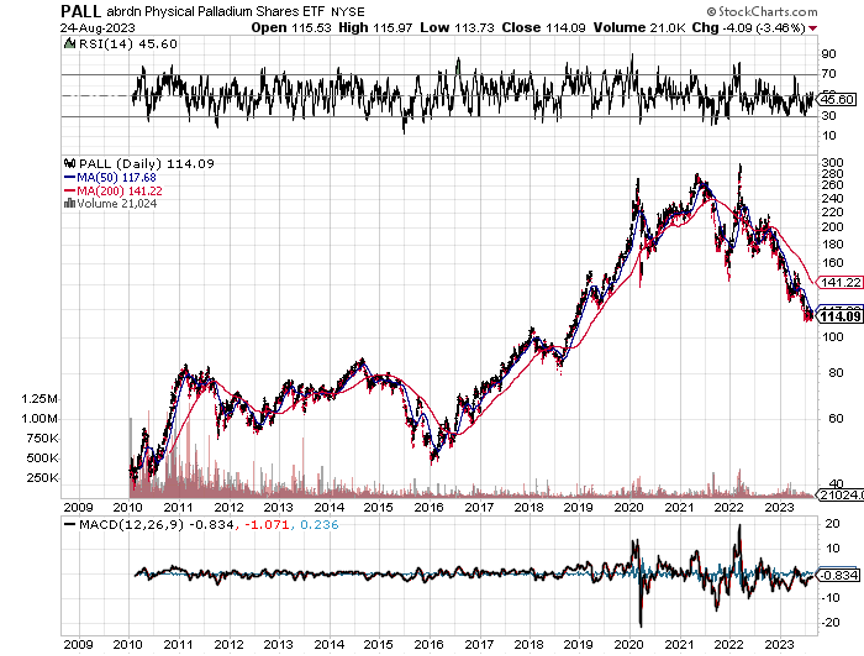

As a result, Western hedge funds will soon be moving money out of paper assets, like stocks and bonds, into hard ones, such as gold, silver (SIL), palladium (PALL), platinum (PPLT), and copper.

A massive US stock market rally has sent managers in search of any investment that can’t be created with a printing press. Look at the best-performing sectors this year and they are dominated by the commodity space.

The bulls may be right for as long as a decade thanks to the cruel arithmetic of the commodities cycle. These are your classic textbook inelastic markets.

Mines often take 10-15 years to progress from conception to production. Deposits need to be mapped, plans drafted, permits obtained, infrastructure built, capital raised, and bribes paid in certain countries. By the time they come online, prices have peaked, drowning investors in red ink.

So a 1% rise in demand can trigger a price rise of 50% or more. There are not a lot of substitutes for iron ore. Hedge funds then throw gasoline on the fire with excess leverage and high-frequency trading. That gives us higher highs, to be followed by lower lows.

I am old enough to have lived through a couple of these cycles now, so it is all old news for me. The previous bull legs of supercycles ran from 1870-1913 and 1945-1973. The current one started for the whole range of commodities in 2016. Before that, it was down from seven years.

While the present one is short in terms of years, no one can deny how business cycles will be greatly accelerated by the end of the pandemic.

Some new factors are weighing on miners that didn’t plague them in the past. Reregulation of the US banking system is forced several large players, like JP Morgan (JPM) and Goldman Sachs (GS) to pull out of the industry completely. That impairs trading liquidity and widens spreads— developments that can only accelerate upside price moves.

The prospect of falling US interest rates is also attracting capital. That reduces the opportunity cost of staying in raw metals, which pay neither interest nor dividends.

The future is bright for the resource industry. While the gains in Chinese demand are smaller than they have been in the past, they are off of a much larger base. In 20 years, Chinese GDP has soared from $1 trillion to $14.5 trillion.

Some 20 million people a year are still moving from the countryside to the coastal cities in search of a better standard of living and improved prospects for their children.

That is the good news. The bad news is that it looks like the headaches of Australian parents of juvenile high earners may persist for a lot longer than they wish.

Buy all commodities on dips for the next several years.

Global Market Comments

June 9, 2023

Fiat Lux

Featured Trades:

(JUNE 7 BIWEEKLY STRATEGY WEBINAR Q&A),

($VIX), (TSLA), (TLT), (FCX), (RUT), (COIN), (AAPL),

(ROM), (AMZN), (PYPL), (NVDA), (COPX), (FXI)

CLICK HERE to download today's position sheet.

Below please find subscribers’ Q&A for the June 7 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, NV.

Q: Do you ever trade the CBOE Volatility Index ($VIX)?

A: No, I used to, but I got hit a few times. That’s because 95% of the year is spent seeing the ($VIX) go down, and then the other 5% basically doubles overnight. It’s a short play only. With a long ($VIX), the time decay is enormous, and it’s just not worth owning. The only way to make money in ($VIX) is to buy it right before a giant VIX spike. And the floor traders in Chicago have a huge inside advantage in that market. So, I finally gave up and decided there's better things to do.

Q: Buy the price dip for Tesla (TSLA)?

A: I’d have to look at the charts, but if it gets back down to $200, I would start hoovering it up again. The fundamentals are really arriving for Tesla big time, as is the long-term bull case.

Q: With the debt crisis over, how low will the iShares 20 Plus Year Treasury Bond ETF (TLT) go in the short term?

A: Well, we know they have to issue a trillion dollars of 90-day T-bills in the next few weeks. The debt ceiling crisis stopped Treasury bill issuance for several months and now they have a lot of catch-up to do. So, best case scenario, the (TLT) drops to $95, then you load the boat for the rest of your life in (TLT) LEAPS, like a $95-$100 2024 LEAPS. And that should double about every year.

Q: Are you concerned about commodities given the weakness in the Chinese economy?

A: Yes, it’s definitely slowing the commodities recovery, but is also giving you a fantastic opportunity to get into things like Freeport McMoRan (FCX) at a cheaper price, where it was just a couple of weeks ago. All of the commodities look like they’re bottoming now, it’s time to buy them.

Q: It seems like you really love the Russell 2000 (RUT).

A: I hate the Russell. You only want to own big money stocks because that's where the big money goes first. Big money doesn’t go into the Russell, and as long as there's any doubt of a recession coming, they’ll perform poorly.

Q: Coinbase (COIN) is getting sued by the SEC, should I buy on the dip?

A: No, the whole crypto infrastructure is getting sued out of existence and disappearing. They went after Binance also. It seems like the SEC just doesn’t like crypto very much. That kind of shrinks the whole industry back down to hot wallets, where you slowly have direct control of your bitcoin on the network and you don't use any outside brokers to buy and sell it because there may not be any left shortly.

Q: Should we still hold the Apple (AAPL) bull call spread?

A: Yes, I think we have enough room on our call spread in the next 7 trading days to take max profit. However, if you have any doubts, no one ever gets fired for taking a profit.

Q: Is the ProShares Ultra Technology ETF (ROM) a buy at this time?

A: No, if anything, ROM is a sell. It almost had a near-double move. So no, wait for a 20% or 30% correction this summer in ROM and then go in. It has actually led most tech because it's a 2X long ETF. Sometimes I just want to shoot myself. You buy before stocks double, not afterwards.

Q: What will trigger a correction this summer?

A: The risk of a further rise in interest rates, which we may get. Other than that, the market is running out of negatives.

Q: What is the risk of US currency not being the world reserve?

A: Zero. I have been asked this question every day for the last 50 years and so far, I have been right. What would you rather keep your savings in Chinese Yuan, Russian rubles, or Euros? I would say none of those. And US currency will remain the reserve currency for this century, easily, until a digital US dollar comes out.

Q: Do you want to buy the cellphone companies?

A: No, not really. They weren’t very interesting before—it's a low margin, highly competitive cutthroat business—and now you have one of the world's largest companies, Amazon (AMZN), potentially offering phones for free? I think I'll pass on that one.

Q: Do you have any interest in pairs trading?

A: No, they blow up too often.

Q: Did you say you sent out a one-year LEAPS on Freeport McMoRan (FCX), the $35-$38?

A: Yes, if you didn’t get it, email customer support.

Q: Are investing in 90-day Treasury bills until the next one or two Fed meetings are over a good idea?

A: Yes, that is a good idea. Cash has a high-value night now. Remember, a dollar at a market top is worth $10 at a market bottom, and we now have a rare opportunity to get paid 5.2% or 5.3% while we wait. That hasn’t happened in almost 20 years.

Q: Will the new Apple VR headset be a boon to the stock price?

A: Yes, adding 10% to your earnings is always good, but it won’t happen immediately. You need a few thousand third-party app developers to come through with services before the earnings really get going. That's what happened with iTunes when the iPhone came out. Growth was slow when Apple only allowed its in-house apps to be sold—when they opened to the public, the business went up 100 times. That's maybe what will happen with the virtual headset.

Q: PayPal (PYPL) has dropped a lot, should I buy it here?

A: No, cutthroat competition in the sector is destroying the share price. There are too many other better things to buy.

Q: Why do so many professional analysts say the market will go down this year, but it goes up every day?

A: Professional analysts are just that—they're analysts, not traders. And often these days, to save money, your professional analyst is 26 years old, so they don’t have much market experience. I like to think that 50 years of trading experience backed with algorithms helps.

Q: Do you think oil could hit $100 a barrel next year?

A: Yes, definitely. Especially if we get a decent economic recovery and Saudi Arabia doesn’t immediately bring back 3 million barrels a day that they’ve cut.

Q: Should I chase NVIDIA (NVDA) here?

A: No, better to own cash here than Nvidia. Buy Nvidia on the next dip, or another Nvidia wannabe company, which will almost certainly arrive shortly.

Q: When will we get peace in Ukraine?

A: Within a year, I would say. Russia has literally run out of ammunition, and Ukraine is getting more. Ukraine is also getting F16s, our older fighter planes, and many other advanced weapons and parts—those are a big help. They can beat anything the Russians throw up.

Q: Is Global X Copper Miners ETF (COPX) a good copper play?

A: Yes it is, but you don’t get the leverage that you do with an FCX LEAP. I don’t know how far the top will go, but that would be a great trade one to two years out.

Q: Can you explain why there is a short squeeze in copper?

A: There are 200 pounds of copper needed for each EV, and EV production is exploding both here and in China. Tesla is expected to make 2 million EVs this year, especially with the $33,000 price point. China manufactures this many EVs as well. Four million EVS and 200 pounds of copper per EV equals the entire annual production of copper right now. At some point, people will notice that and they’ll take copper as much as they took lithium up last year.

Q: What do you mean when you say LEAPS one or two years?

A: It really depends on your risk. When you buy a two-year LEAPS, you usually get the extra year for free or almost nothing, and if you get a rapid increase in the underlying share price, the two-year LEAP will go up almost as much as the one year. So for most people who don’t want to watch the market every day, the two-year LEAPS is probably a better choice.

Q: Why did you buy only one LEAPS contracts?

A: All of my LEAPS recommendations are only for one contract. It is up to you to decide what your risk tolerance and experience level is, whether you buy 1, 100, or 1,000 contracts, so I leave the size up to you because it can vary tremendously depending on the person. Also, one contract makes the math really easy for people to understand.

Q: At what point do you sell your LEAPS?

A: Well, if you get a rapid 500% profit, which happened with many of the LEAPS that we did in October as well as the ones we did in March, I would take it. However, the goal on these is to go for the 10 baggers, or the 100% return in a year, and you usually need to hold it for the full year to get that. But, if the stock takes off like a rocket, I would take the profit. How many times in your life do you get a 500% profit in a month or two? I would say none. So, when you get that with these LEAPS recommendations, take it and run like a madman, move to a different country, and change your name.

Q: With the ($VIX) this low and many great companies for the second half down, would you buy single LEAPS instead of spreads?

A: I would; the problem with the call spread strategy is that it’s not the best thing to do at big market bottoms, down 20%, 30%, and 40%. The better thing to do is the LEAPS, but the LEAPS is a one- or two-year position, and I have to be sending out trade alerts every day. At market bottoms, you definitely want to get the most market leverage possible on the upside, and LEAPS does that for you in spades. They essentially turn your stock into a synthetic futures contract with a 10x leverage.

Q: When do we expect China (FXI) to take over Taiwan?

A: Never, because if they invade Taiwan, China loses its food supply from the US, which cannot be replaced anywhere. They also lose their international trade, so they won’t have the profits with which to buy food elsewhere. I’ve been in China when millions died during a famine and let me tell you, there is NO substitute for food. Not all the money in the world can buy it when it just plain isn’t available. But China will keep threatening and bluffing as they have done for 74 years.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Sometimes the Market Can be Tough to Figure Out

Global Market Comments

September 13, 2022

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPERCYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

December 10, 2021

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPERCYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

April 30, 2021

Fiat Lux

Featured Trade:

(APRIL 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(PFE), (MRNA), (USO), (DAL), (TSLA), (CRSP), (ROM), (QQQ), (T), (NTLA),

(EDIT), (FARO), (PYPL), (COPX), (FCX), (IWM), (GOOG), (MSFT), (AMZN)