Mad Hedge Technology Letter

February 13, 2023

Fiat Lux

Featured Trade:

(ECOMMERCE TAKES A BACK SEAT)

(CPNG), (AMZN)

Mad Hedge Technology Letter

February 13, 2023

Fiat Lux

Featured Trade:

(ECOMMERCE TAKES A BACK SEAT)

(CPNG), (AMZN)

American ecommerce companies are certainly feeling the pinch of high inflation as many US consumers tighten up their purse strings.

Ecommerce was one of the few growth engines for tech before 2020, now it’s harder to move the needle for many subsectors.

Just take a look at the giant ecommerce company Amazon (AMZN) whose stock price was higher in August 2018 compared to today.

Between now and 2018, Amazon experienced a pulsating melt-up due to a business boom, low interest rates, and positive global growth.

On the way down, the reverse has taken place.

We, as investors, just cannot assume tech will go from the bottom left to the top right anymore.

So if ecommerce companies of Amazon’s ilk are struggling to navigate tighter conditions, imagine how bad it is for ecommerce flagship companies in an Asian third-world backwater like South Korea.

The ecommerce company I am talking about is Coupang (CPNG), which I’ve been highly negative of since public inception, and rightly so.

CPNG's share price has done nothing but drop since its IPO from its $50 peak and now stands at $15 after bottoming out at $9.

What next for CPNG?

CPNG the South Korean e-commerce pioneer has lost billions of dollars since its inception but is rolling out an army of robots at fulfillment centers in the hope of achieving profitability.

They burned cash by building distribution centers throughout South Korea that could help it push the boundaries of speedy delivery with a broad selection.

Now the company is almost breaking even, with analysts projecting it will turn a profit for the second straight quarter and then report its first annual operating profit in 2023.

Coupang has used private venture capital to fund this expansion combined with a 2021 initial public offering to build logistics domestically.

Coupang is also pushing to expand new markets in Taiwan and Japan. I see that as a hard endeavor because legacy ecommerce like Rakuten is quite entrenched there.

I think they will be unable to outmaneuver local competition.

Strategies like cash burning to seize market share don’t work anymore because of the high cost of capital.

CPNG needs to optimize what it can in South Korea even if the country presides over one of the worst demographics in the world, with the average age of customers approaching the age of nursing home residents.

CPNG has more than 100 fulfillment and logistics centers in South Korea, but no footprint overseas.

Barreling into mature markets is a marginal strategy for CPNG today because they are 10 years too late.

Yet, I do really like what they are doing on the automation front domestically integrating automated robots into their operation.

The lack of workers and consumers in South Korea is another headwind due to poor demographics.

Externally, they also face various headwinds from the global backdrop souring.

I do believe in the short term as tech equities benefit from the disinflation narrative, there is a narrow path to a higher market share for CPNG to around $25 per share in 2023.

Anything higher I would avoid because it’s not worth paying a premium for this ecommerce company.

Relying on a “tide lift all boats” strategy is not ideal in today’s tech world, because that isn’t for sure anymore.

Long term, my assessment of CPNG is less rosy. This could be a good buyout ticket for a bigger fish because, at some point, they will realize that they were late to the party and might as well sell it off for whatever it's worth.

Mad Hedge Technology Letter

March 16, 2022

Fiat Lux

Featured Trade:

(THE GENIUS AT SOFTBANK GETS EXPOSED)

(SFTBY), (ARKK), (DIDI), (BABA), (CPNG)

Mad Hedge Technology Letter

June 21, 2021

Fiat Lux

Featured Trade:

(SOFTBANK’S EPIC COMEBACK)

(SOFTBANK), (CS), (CPNG), (GRAB), (AAPL), (GOOGL), (BABA)

I haven’t touched on the Softbank Vision Fund since pre-pandemic times, but it is time to take a barometer of the state of their fund because they also represent a snapshot of the state of emerging technology.

The Fund reported a massive loss of $18 billion during the nadir of the tech correction in 2020, and its clout in the tech world fell by epic proportions to almost pariah status.

Those were perilous times for Softbank Founder and CEO Masayoshi Son who held the distinction of losing the most wealth in the world before making it all back.

The ensuing flood of liquidity, accessible at the tech lows, catapulted most of Softbank’s investments in the U.S. tech market and they recently reported the highest-ever profit for a Japanese company.

Softbank Group reported profits of $48 billion for the fourth quarter, while Softbank Vision Fund, which invests in startups, reported a profit of $37 billion.

After massive weakness in assets including Airbnb, Oyo, and WeWork, we saw the value in these startups dip to an all-time low, then they were essentially bailed out by the Fed.

During that recapitalization process, Softbank Vision Fund fired 10% of its employees to cut costs.

When you combine that with big up moves from South Korean e-commerce company Coupang (CPNG) and ride-hailing firm Grab planning to go public via an SPAC, betting all his chips in emerging tech was the right thing to do and Son was handsomely rewarded for this outsized risk.

Son is quite famous for some of his speculative energy that he has channeled towards China’s Alibaba (BABA) before Alibaba became famous.

More than a decade later, that investment is worth $130 billion, becoming one of the most successful startup bets in history. He then aggressively invested in several startups around the world, including Snapdeal, Oyo, Ola, and Paytm in India.

For as many lemons in his basket, he’s had his fair share of 10-baggers and 433-baggers like Alibaba that validated his aggressive tech strategy.

Son got into many investments before venture capitalists in tech started being copied around the world and before the Arab sovereign funds and Chinese could get their house in order to partake as well.

He wasn’t the first, but the first group mover advantage made these deals possible, and by borrowing heavily against his Softbank equity, he was able to bet the ranch on many emerging techs by acquiring the proper financing and leverage.

However, the Softbank Vision Fund is a harbinger for what’s to come in tech and Son laughing all the way to the bank could also be loosely translated as the low hanging fruit in tech and its harvest has been plucked dry.

Venture capitalists are having a harder time in 2021 finding those 433-baggers or even 3-baggers.

An ominous sign that bodes ill for emerging tech is the financing hawks that have started to highlight the extreme risks involved in investing big in little-known business models with the propensity to fail.

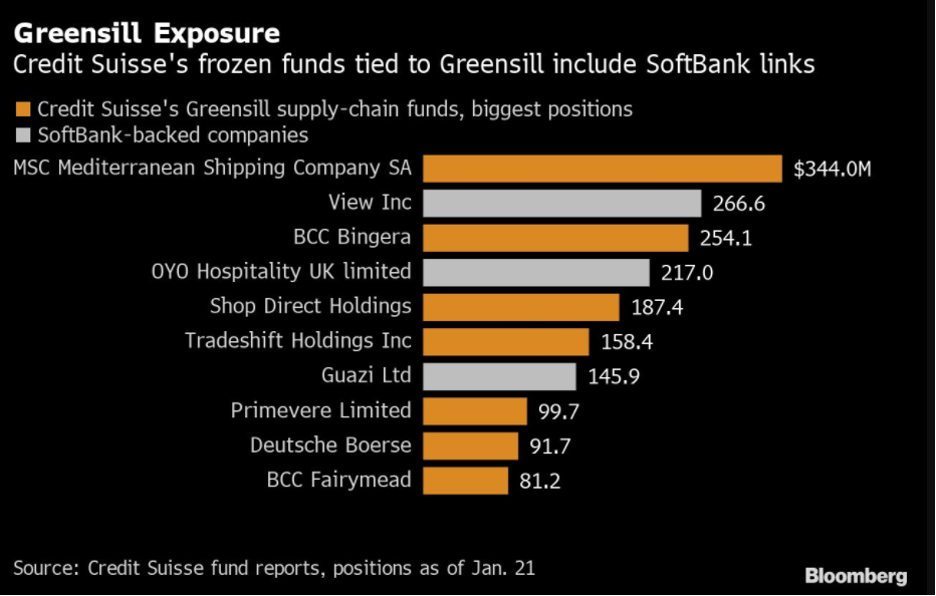

Credit Suisse (CS) has put Son recently on notice by dissolving a longstanding personal lending relationship as the bank clamps down on transactions with his company, according to regulatory filings and people familiar with the situation.

The moves came after the collapse of SoftBank-backed Greensill Capital that caused turmoil for Credit Suisse forcing them to book a massive loss.

That was on the heels of Credit Suisse’s $5.5 billion loss originating from trading by family office Archegos Capital Management.

The bank is now avoiding business with big tech investors who are likely to reach further up the risk barometer and inflict heavy damage.

Does this mean the era of subsidized tech business models is over?

No, but it will become more difficult to originate financing from traditional methods like European banks to invest in these types of exotic tech projects.

Mr. Son had long used Credit Suisse and other banks to borrow money against the value of his substantial holdings in SoftBank.

As recently as February, Mr. Son had around $3 billion of his shares in the company pledged as collateral with Credit Suisse, one of the biggest amounts of any bank, according to Japanese securities filings.

The share pledge loan relationship stretched back almost 20 years. By May, that lending had gone to zero.

Bloomberg News reported in May that Credit Suisse refuses to do any new business with SoftBank, but the silver lining is that Softbank has $48 billion in new profits to theoretically spin into some new projects it likes.

Of course, it’s always easier when you use other people’s money, but these are then new rules of the game.

Its bounty from the liquidity surge will help them advance into this new post-pandemic tech ecosystem with substantial gunpowder.

So I can’t say it’s been all bad for everyone at the individual level because this pandemic divided the masses into tech winners and losers.

Notice that many Bay Area tech investors were taking profits from the tech pandemic stock surge and rolled the capital into $3-5 million Lake Tahoe Mountain chalets as a summer house or dinner party house.

And if they didn’t do that, they were rolling these profits into Hawaiian beachfront properties with views of Diamond Head in Oahu or even dabbling in villas on the Kauai Island.

This could partially explain why Apple (AAPL) has gone sideways for the past 11 months.

This year has instigated a tech reset and in the short term, the Nasdaq has been overwhelmed by external headlines like of perceived inflation fears, chip shortage, and a built-in assumption that earnings will be perfect.

These sky-high earnings expectations have created a “buy the rumor and sell the news” type of price action with only a handful of companies able to top these insane expectations like Google (GOOGL).

Mad Hedge Technology Letter

March 26, 2021

Fiat Lux

Featured Trade:

(AVOID THIS KOREAN ECOMMERCE COMPANY)

(CPNG), (AMZN), (GRUB), (UBER), (JD), (SHOP), (MELI)

I might characterize Coupang (CPNG) as something akin to China’s JD.com.

It's an e-commerce company that has fulfillment solutions, not dissimilar to Amazon (AMZN) Fulfillment. They also have storefronts that they provide for businesses, which isn't dissimilar to say, a Shopify (SHOP).

Even combining aspects of Amazon and Shopify are there but they don’t have the powerful AWS cloud business.

Similar to JD.com (JD), which is a Chinese e-commerce platform, Coupang has differentiated itself by owning its entire logistics and delivery system.

What is different about Coupang versus the other players in Korean e-commerce is that they own their own inventory for the most part.

That means that they have inventory sitting on their balance sheets.

They have responsibility for pushing that through. But it also means, since they directly negotiate with the manufacturers of these items, they're able, for the most part, to get lower prices.

Total Korean e-commerce spend was $128 billion in 2019, which is expected to grow to $206 billion by 2024, implying a CAGR of approximately 10%.

This is where Coupang has a chance but in a rising interest rate environment and with competition on the New York exchanges from Amazon (AMZN), Shopify (SHOP), even MercadoLibre (MELI), I don’t believe Coupang is more attractive than these 3 in its current form as it relates to American investors pouring money into their stock.

Is it an advantage if 70% of Koreans live within seven miles of the Coupang logistic centers?

Certainly, there is that train of thought.

The massive investments into fulfillment centers mean they can surpass the delivery speed of many of its competitors because South Korea is essentially one capital city with millions upon millions hovering on top of each other like many other parts of Asia.

The problem I can have with this scenario is that margins could suffer because a busy Korean lifestyle doesn't lend itself to things like in-store shopping as readily as it does in the United States, and it could manifest itself with Koreans tapping into higher frequency in which they buy online which will push up total spend, but margins will decrease because you are buying stuff that won’t move the needle higher because you've paid for the service.

I can easily see someone just buying one item for delivery in the morning and doing that seven days per week.

Now I need a set of tweezers, I'm going to order that. Tomorrow, I need cotton pads, I’m going to order that.

Over time, operating margin will get butchered with a business like this.

And what do you know? I’m right, they have been losing billions upon billions the past few years with no end in sight.

How long will the external investors subsidize their losses?

At a broader level, mobile phone penetration is already at 96% of Koreans and 40% of Koreans order groceries online, so it’s hard for me to digest where the addressable market can expand from here because they have already collected so much of the available harvest.

This IPO does feel a little bit like an ex-growth dump on the retail investor and that’s not saying shares can’t appreciate at all, but investors believing this is the next Amazon are sorely mistaken.

They are not Amazon, not even close, and they are also confined to one small market where the population has peaked and will start decreasing in numbers.

The population is only 15% of the U.S. and incomes in the U.S. are vastly higher, so how does Coupang become an Amazon without the AWS business?

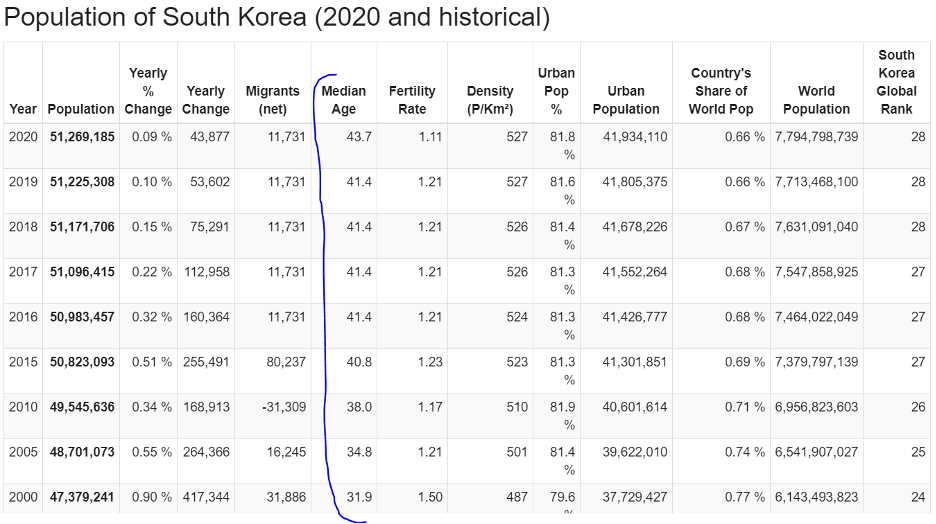

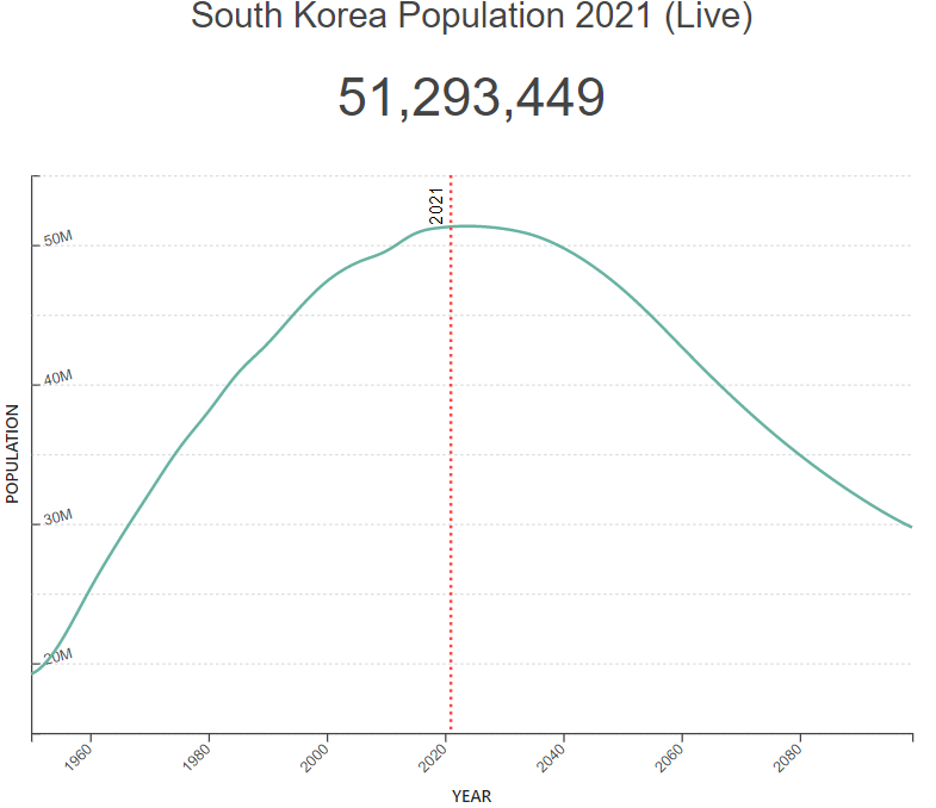

Just as disturbing, the median age in Korea has ballooned from 31.9 in 2000 to 43.7 in 2020 and this cohort doesn’t strike me as the group in the glory years of family formation, peak spend, or technological know-how.

As the Korean population starts to decline in 2025 and the median age creeps up from 43.7 to 50, then aside from adult diapers, where does the incremental growth come from in Korea?

I just don’t see it.

Personal incomes are going to rise at an annualized rate of about 3% every year and I believe much of the total spend will be fought out attempting to woo the big buyers which offer a point of attack for competition that should come around in the next 2 to 3 years.

They also have Coupang Eats, not dissimilar to Grubhub (GRUB) or Uber (UBER) Eats. They have grocery delivery, and even an integrated payment processor. All of these things that took Amazon much longer to build out, admittedly, were a little before their time there, Coupang has already integrated that into the platform.

For this, I give them credit, but they are still nothing like Amazon in terms of potency and scale.

In 2019, active customers rose 34% and that’s what a prototypical growth company should do.

It’s not shocking.

Then an analyst would think that with covid and all that public chaos pinning consumers at home, surely, Coupang would grow active customers by 50% of even 60% in 2020, right?

But active customers only grew 18% in 2020, and they provided zero insight about why active customer growth slowed nearly in half year-over-year, and that for me shows, Coupang is severely limited by what Korea can offer in terms of growth and total spend.

If readers want to get into the Korean economy then I would advise to wait on other Korean homegrown entrepreneur-led startups with IPOs in the pipeline by Krafton Inc., the creator of hit game PUBG, and the country’s biggest mobile-only bank Kakao Bank. Unlike Coupang, those firms are profitable.

Ultimately, total e-commerce spend for all Internet buyers in Korea is expected to grow from approximately $2,600 in 2019 to approximately $4,300 in 2024 on a per buyer basis and Coupang will take advantage of that but I don’t foresee the 30% annual rise in underlying shares that others do.

I can definitely visualize a grind up with periodical substantial selloffs because of missed targets and disappointing forecasts.

That’s not the type of price action I want to see.

The signs point to Coupang maturing immediately and the executive management creating a special clause to allow them to dump shares right after the IPO illustrates that this tech company will stall out moving forward.

Normally, management must wait 6 months after going public before the lock-up period ends.

Highly unusual and can you believe it? They even gave stock shares to their courier drivers at the IPO, making me pause, then come to the conclusion that I rather invest in a tech company returning incremental value to the shareholders and not the manual labor that is paid by an hourly wage. How bizarre!

Avoid Coupang like the plague.