Mad Hedge Technology Letter

November 1, 2018

Fiat Lux

Featured Trade:

(LOOK AT ZENDESK FOR YOUR NEXT TEN BAGGER)

(ZEN), (RHT), (AMZN), (MSFT), (CRM), (IBM), (SNAP)

Mad Hedge Technology Letter

November 1, 2018

Fiat Lux

Featured Trade:

(LOOK AT ZENDESK FOR YOUR NEXT TEN BAGGER)

(ZEN), (RHT), (AMZN), (MSFT), (CRM), (IBM), (SNAP)

At the recent Mad Hedge Lake Tahoe Conference, I pinpointed software companies as a robust group of tech stocks that are the perfect late cycle investment in the economic environment we find ourselves in now.

To add some granularity about my thesis, I would like to start elaborating on an up-and-coming software stock that I find compelling and in the middle of a growth sweet spot.

And with the rapacious pullback, the tech sector has experienced as of late, this high-octane growth stock is poised to rev back up, albeit with more than your average volatility attached to its stock symbol.

If you can stomach the volatility, then Zendesk (ZEN) is the company for you to dip your toe in.

Zendesk is a customer service software offering solutions to clients through a flexible platform revolving around customer service tickets.

This $6 billion market cap tech firm thriving in the dodgy San Francisco Tenderloin district only need to be reminded of how fast a tech firm can be disrupted by stepping out of the office and experiencing ground zero of the San Francisco homeless movement in the scruffy Tenderloin.

I usually get lambasted for the lack of time I spend following budding tech firms, but you cannot blame me when the bulk of this year’s stock market gains have been extracted by the biggest and mightiest tech titans.

That does not mean all small tech is dead, but they certainly do have heightened existential risk because of the Amazons (AMZN) and Microsofts (MSFT) of the world, spreading their network effects far and wide.

International Business Machines Corporation’s (IBM) purchase of cloud company Red Hat (RHT) underscores the value of applying M&A to grow the top and bottom line, and the chronic bidders of these smaller minnows are usually the Amazons and Microsofts themselves who have the cash to dole out.

Salesforce (CRM) is always adding to its arsenal of integrated software companies that can scale up in the cloud, and Marc Benioff’s M&A strategy has thrived to devastating effect boosting the bottom and top line.

I must admit, tech does get the rub of the green over other industries because of the scaling effect afforded to profit poor tech companies.

The ample time to prove to investors they can snatch a growing user base, enhance product offerings, and develop an eco-system intertwined with recurring subscription products is not fair to other industries who are judged on different metrics mainly profits and profits now.

Well, life isn’t fair.

The addressable market is usually massive causing investors to stick with these burgeoning tech firms through thick and thin.

Zendesk is another company burning money, but let me tell you, they are no Snapchat (SNAP).

Operating margins are marching towards positive territory, meaning this outfit is well-run.

It was only at the beginning of 2015 when Zendesk’s operating margin registered -53%, and since then, they have dramatically reduced it to -36% at the end of 2016 and now -24% in 2018.

Gross margins next quarter will be hit a bit with its acquisition of Base CRM, headquartered in Mountain View, California and R&D offices in Krakow, Poland, offering a web-based all-in-one sales platform featuring tools for email, phone dialing, pipeline management, and forecasting.

Improving service offerings in the tech world usually means nabbing niche cloud companies that can easily be integrated into the larger eco-system and Base CRM, even though it has lower margins than Zendesk, is a nice pickup for the company boosting the top line while expanding cross-selling activities.

Then there is the sales revenue growth demonstrating all the hallmarks powerful software companies live up to with its 39% quarterly revenue growth.

Zendesk’s management has remarked that they fully expect to hit $1 billion in total sales by 2020 which is more than double the 2017 annual revenue of $430 million.

This year, Zendesk is forecasted to post just shy of $600 million in sales.

Large clients keep piling in hoping to modernize their customer service operations and wean themselves off the siloed legacy systems.

Disruption by some fresh newcomer in a disruptive industry that they operate in is usually the trigger forcing companies to spruce up their customer service software.

This path of migration will healthily continue for Zendesk reaffirming management’s thesis of $1 billion in sales by 2020.

Zendesk, flaunting off their innovation skills, identified the universal popularity of messenger app WhatsApp as an effective platform for its services and rolled out a product that integrates Zendesk services with WhatsApp.

This will allow businesses to manage customer service interactions and engage with customers directly on WhatsApp.

The customized integration links conversations between businesses and their customers on WhatsApp within Zendesk.

This move will allow Zendesk to stretch their tentacles further and wider while being able to provide faster support for customer service tickets which are incredibly time-sensitive.

Since management highlighted that WhatsApp is the go-to messenger in Asia Pacific and Latin America, there was no reason not to extend their offerings in a way that captures this vital userbase.

The WhatsApp pivot has been a nice addition with Zendesk’s management remarking that they “handle over 20% of our order status inquiries daily with WhatsApp and Zendesk, which is much faster than traditional methods.”

Omnichannel support within Zendesk’s platform will be key to securing the growth it needs to reach its $1 billion of sales milestone.

Innovation is the crucial ingredient in constructing the perfect products that can maximize customer service performance.

Its overseas exploits are not just a flash in the pan with its services supported in 30 languages and offices in 15 different countries. It all makes sense considering half their revenue is outside of America.

With IBM’s recent acquisition of Red Hat, buyers are still hunting for the right pieces to add to their portfolio.

The Red Hat purchase proved that demand still eclipses supply by a far margin.

Zendesk is one of those in the queue for a big buyer to swoop in with a mega offer.

It’s no guarantee that a company will pay a 63% premium like IBM did, but some sort of premium will be definitely warranted.

Zendesk offers the type of robust growth and premium cloud services that could easily fit into a bigger cloud player looking to improve their assortment of cloud tools.

This type of tailwind itself will naturally boost the stock by 5-10% alone if the macro picture can somehow manage to gain footing for the rest of the year.

As with the rest of tech, Zendesk dipped about 20% in the last 30 days but by no means does that mean this is a bad company with a weak future.

I would very much argue the opposite.

The weakness in sales offers a prime entry point in a fast-growing company that is part of the software and cloud movement that I have incessantly harped about.

If this company can show continued operating margins growth, maintain sales growth of above 30% YOY, and demonstrate product innovation, this stock will break out to higher levels.

As of now, that is exactly the road they are headed down.

Business abroad is doing so well that Zendesk recently splurged on a Europe, Middle East and Africa (EMEA) headquarters in Dublin, Ireland coined as the “the tech capital of Europe.”

Zendesk started with two employees in Dublin in 2012 and now boast over 300 employees occupying 58,000 square feet in a new office costing $10 million.

By 2020, Zendesk expects to build their Dublin branch to over 500 employees implying that the overseas pipeline is ripe for the taking.

I am highly bullish Zendesk and recommend that readers check out this attractive growth story.

![]()

Mad Hedge Technology Letter

October 23, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Global Market Comments

October 22, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or HEADING FOR LAKE TAHOE),

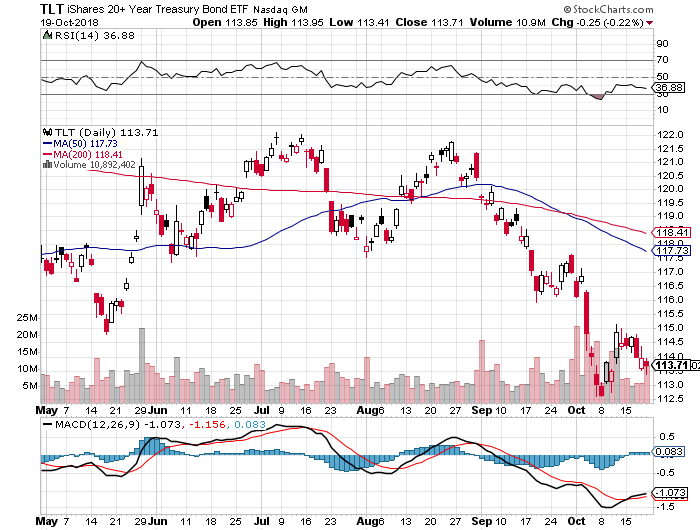

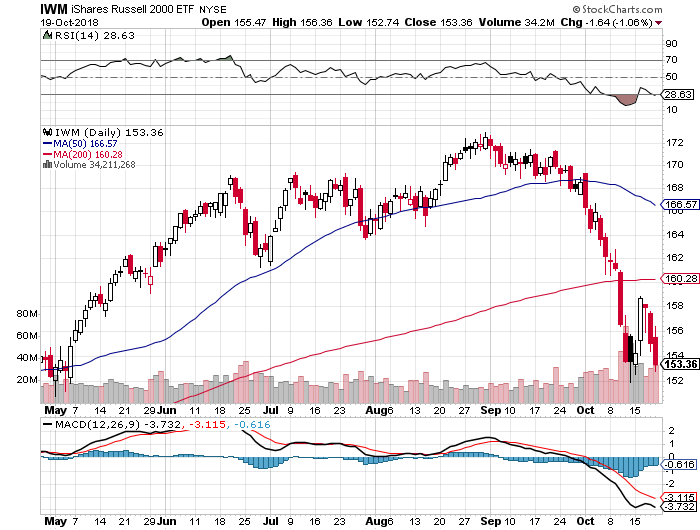

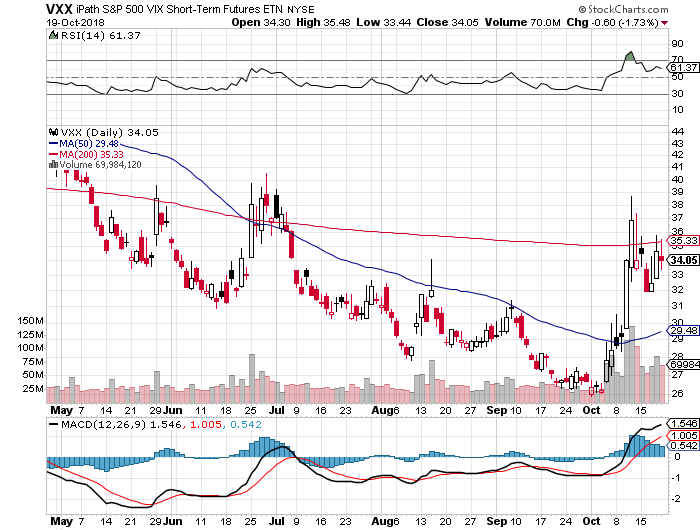

(SPY), (TLT), (VIX), (MSFT), (AMZN), (CRM), (ROKU),

(BRING BACK THE UPTICK RULE!)

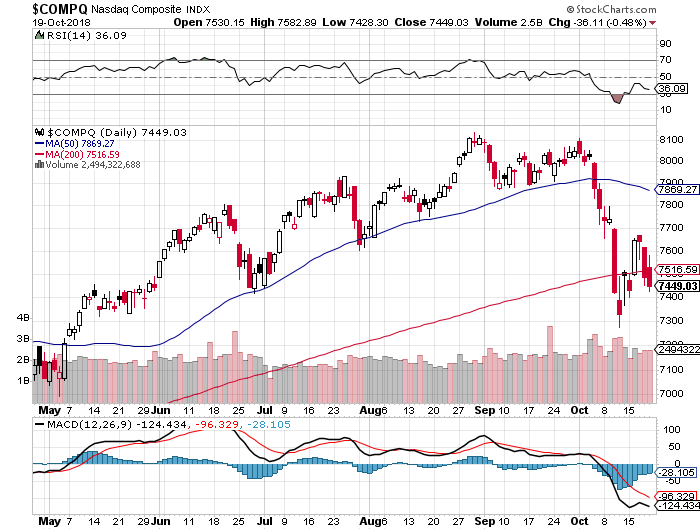

There’s nothing like a quickie five-day tour of the Southeast to give one an instant snapshot of the US economy. The economy is definitely overheating and could blow up sometime in 2019 or 2020.

Traffic everywhere is horrendous as drivers struggle to cope with a road system built to handle half the current US population. Service has gotten terrible as workers vacate the lower paid sectors of the economy. Everyone you talk to tells you business is great, from the CEOs down to the Uber drivers.

I managed to miss Hurricane Michael by two days. Hartsfield Jackson Atlanta International Airport was busy with exhausted transiting Red Cross workers. The Interstate from Savanna to Atlanta, Georgia was lined with thousands of downed trees. In Houston mountains of debris were evident everywhere, the rotting, soggy remnants of last year’s Hurricane Harvey.

I managed to score all day parking in downtown Atlanta for only $8. I kept the receipt to show my disbelieving friends at home.

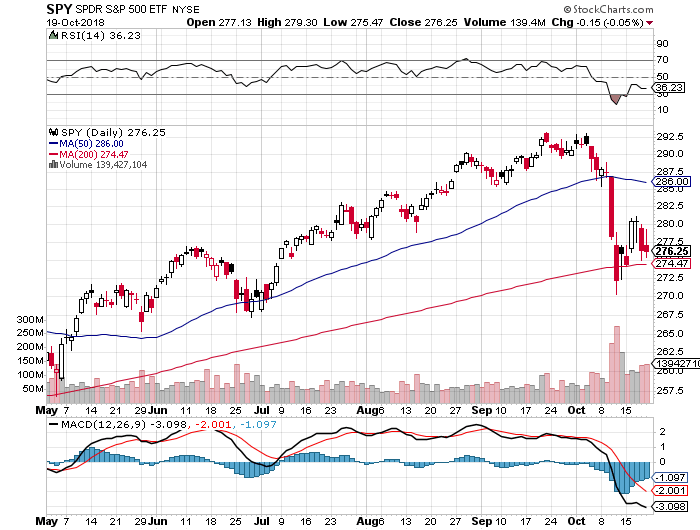

Bull markets climb a wall of worry and this one has been no exception. However, the higher we get the greater the demands on the faithful.

Last week saw my Mad Hedge Market Timing Index plunge to an all-time low reading of 4. I back-tested the data and was stunned to discover that October saw the steepest selloff since the 1987 crash, which saw the average crater 21% in one day.

And while evidence of a coming bear market is everywhere, the reality is that stocks can keep rising for another year. Market bottoms are easy to quantify based on traditional valuation measure, but tops are notoriously difficult to call. Look for one more high volume melt up like we saw in January and that should be it.

Real interest rates are still zero (3.2% bond yields – 3.2% inflation), so there is no way this is any more than a short-term correction in a bull market.

The world is still awash in liquidity

The Fed says they’re still raising rates four times in a year no matter what the president says. Look for a 3.25% overnight rate in a year, and 4% for three months funds. If inflation rises to 4% at the same time, real rates will still be at zero.

There certainly has not been a shortage of things to worry about on the geopolitical front. After Saudi Arabia was caught red-handed with video and audio proof of torturing and killing a Washington Post reporter, it threatened to cut off our oil supply and dump their substantial holding of technology stocks.

Tesla made another move towards the mass market by accelerating its release of the $35,000 Tesla 3. Production is now well over 6,000 units a month.

If you had any doubts that housing was now in recession, look no further than the September Existing Home Sales which were down a disastrous 3.5%. In the meantime, the auto industry continues to plumb new depths. In some industries, the recession has already started.

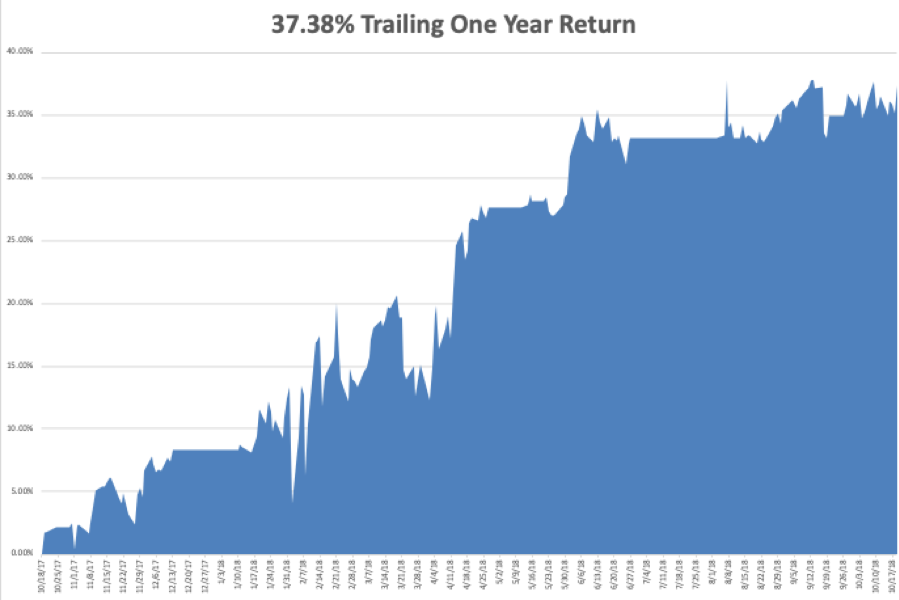

We have been killing it on the trading front. My 2018 year-to-date performance has bounced back to a robust 29.07%, and my trailing one-year return stands at 35.37%. October is up +0.68%, despite a gut-punching, nearly instant NASDAQ swoon of 10.50%. Most people will take that in these horrific conditions.

My single stock positions have been money makers, but my short volatility position (VXX), which I put on early, refuses to go down, eating up much of my profits.

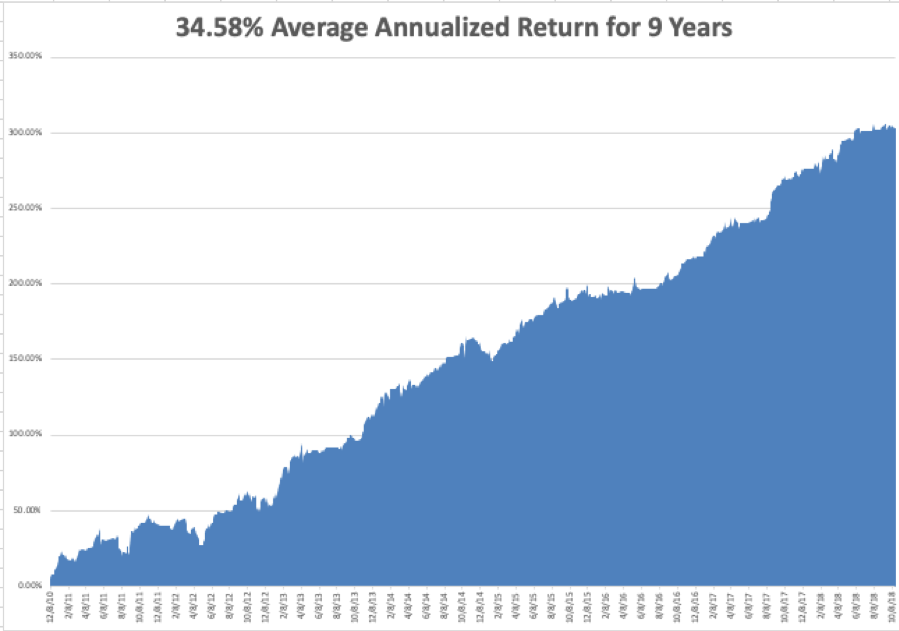

My nine-year return appreciated to 305.54%. The average annualized return stands at 34.58%. Global Trading Dispatch is now only 44 basis points from an all-time high.

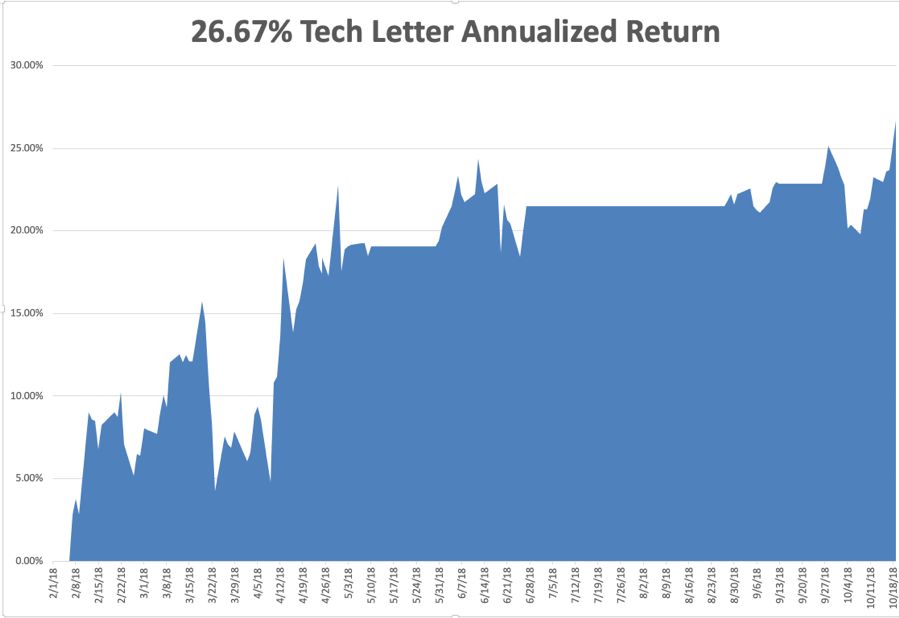

The Mad Hedge Technology Letter has done even better, blasting through to a new all-time high at an annualized 26.67%. It almost completely missed the tech meltdown and then went aggressively long our favorite names right at the market bottom.

I’d like to think my 50 years of trading experience is finally paying off, or maybe I’m just lucky. Who knows?

This coming week will be pretty sedentary on the data front, with the Friday Q3 GDP print the big kahuna. Individual company earnings reports will be the main market driver.

Monday, October 22 at 8:30 AM, the Chicago Fed National Activity Index is out. 3M (MMM), and Logitech (LOGI) report.

On Tuesday, October 23 at 10:00 AM, the Richmond Fed Manufacturing Index is published. Juniper Networks (JNPR), Lockheed Martin (LMT), and United Technologies report.

On Wednesday, October 24 at 10:00 AM, September New Home Sales will give another read on entry-level housing. At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report. Advanced Micro Devices (AMD), Ford Motor (F), and Microsoft (MSFT) report.

Thursday, October 25 at 8:30, we get Weekly Jobless Claims. Alphabet (GOOGL) and Intel (INTC) report.

On Friday, October 26, at 8:30 AM, a new read on Q3 GDP is announced.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I am headed up to Lake Tahoe this week to host the Mad Hedge Lake Tahoe Conference. The weather will be perfect, the evening temperatures in the mid-twenties, and there is already a dusting of snow on the high peaks. The Mount Rose Ski Resort is honoring the event by opening this weekend.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

October 10, 2018

Fiat Lux

Featured Trade:

(DON’T BUY SURVEYMONKEY ON THE DIP),

(SVMK), (GOOGL), (CRM)

If a company takes almost 20 years and still isn’t profitable - it probably never will.

Granted, tech firms are given a Rapunzel-length leash to collect users, scale out the product, refine algorithms to industry standard, and build up the engineering team.

I know this takes time – it doesn’t happen in one day.

After whipping up a frenzy of momentum and venture capitalists claiming stakes, tech stocks usually go public.

This is the common process of what it takes to construct a Silicon Valley tech firm, and there are no shortcuts to this long hard slog.

And if after almost 20 years, amid a nine-year bull market, a tech firm in the most dominating sector in the world cannot figure how to be in the black, investors should stay away from this company in droves.

SurveyMonkey (SVMK), who recently achieved a blockbuster IPO, were the rock stars of the tech world for one day and one day only.

The stock peaking after the first trading day is a ghastly signal and ominous sign.

Their fifteen minutes of fame is all they will get because this practically ex-growth company has no indicators of a rosier future.

The company went public at $12 per share and even that was too generous.

The stock took off like a banshee, on the verge of overshooting the $20 level before falling back to grace.

The stock is now trolling around $13, and on the verge of heading to the purgatory of single digits.

What caused such a swan dive after such a promising start?

On the surface, everything looks like peaches and daffodils – a growing Silicon Valley cloud company even with Facebook spin doctor Sheryl Sandberg on the board.

The optics pass all the marks.

But wait a second, looking at the nuts and bolts, it’s crystal clear why this stock has been throttled back.

The first half of 2018, SurveyMonkey presided over a tepid 3% of paid user growth.

Yes, SurveyMonkey is growing, but not by much.

In this same period, the company lost $27.2 million and this was after an annual 2017 loss of $24 million.

Profitability isn’t exactly their forte.

The 14% of revenue growth the company secured was done after taking a machete and gutting margins to appear pretty for the IPO.

And it’s painfully obvious that SurveyMonkey is failing at converting the freemium users into paid converts.

The online survey doesn’t exactly have the highest barriers of entry.

Google (GOOGL) Forms is the competitor in this space offering straightforward free surveys with basic analysis.

The tool is highly functional.

The pricing structure to SurveyMonkey’s individual membership is presented as a luxury service like the US postal service.

The individual service costs $384 per year and rises all the way up to the bloated price of $1,188 per year.

Any individual paying $1,188 per year for this needs to check themselves into a mental hospital.

Google Forms could easily undercut this pricing model by offering survey tool packages for a fraction of this amount.

The “team plan” is also laughable by charging $75 per month for up to three users, and this type of plan is capped at an exorbitant $225 per month.

Let’s remember that Microsoft offers Microsoft Office 365 Personal for an annual total of $59.99 and is million times more useful.

This annual subscription comes with premium versions of Word, Excel, PowerPoint, OneDrive, OneNote, Outlook, Publisher, and Access.

The OneDrive cloud service includes 1 terabyte (TB) of cloud storage.

Just by this simple comparison, it is easy to see which service is of value and which service is building castles in the sky.

With the explosion of service-as-a-software (SaaS) apps flooding desktops, I imagine the paid version of SurveyMonkey would be first on the chopping block due to its overly ambitious pricing.

In this strategy, the company is more concerned about milking as much as they can from each existing paid user instead of juicing up the core user base.

Effectively, this is a poor management decision, and the company is harming the growth of the potential paid usership base by robbing all incentive to convert to the paid version.

As Netflix masterfully proved, draw in the eyeballs at a lower price, build up the service to an optimum quality level, and subscribers never leave.

The opposite strategy is an indirect way of management believing the product is not good enough or the niche is too small to perpetualize a solid relationship.

And since growth numbers aren’t accelerating, there is infinitesimal reason to even consider investing in this fading company.

SurveyMoney has also racked up the debt - $317 million of it to be precise putting its debt $100 million over total revenue in 2017.

They were burning cash quickly and only had $43 million left in the coffers.

Part of the rationale for going public was a way to pay down debt.

Another chunk of proceeds from the IPO will be used to pay taxes.

The company has no innovative roadmap going forward and using the cash to pay down existing obligations shows the anemic level of intent from this company.

The silver lining in this company is that the losses of $76.4 million in 2016 were pared back in 2017.

In the IPO prospectus, SurveyMonkey noted that most unpaid customers do not become paid customers.

Even though the product is useful and it’s a long-time favorite of mine, the stock is a different animal.

There was not much meat in the prospectus and most of it were dry bones.

The IPO day was buoyed by the $40 million in stock venture-capital arm of Salesforce (CRM) pocketed, but that short-term boost has faded quickly as investors have dissected this company in every which way.

Use their free survey tools but avoid paying for the paid version and don’t buy the stock.

There are many other fishes in the sea.

Mad Hedge Technology Letter

October 3, 2018

Fiat Lux

Featured Trade:

(OUR HOME RUN ON SQUARE),

(SQ), (V), (AMZN), (GRUB), (SPOT), (MSFT), (CRM), (AAPL)

Pat yourself on the back if you pulled the trigger on Square (SQ) when I told you so because the stock has just lurched over an intra-day level of $100.

It was me aggressively pushing readers into buying this gem of a fin-tech company at $49. To read that story, please click here (you must be logged in to www.madhedgefundtrader.com).

Since then, the price action has defied gravity levitating higher each passing day immune to any ill-effects.

The Teflon-like momentum boils down to the company being at the cross-section of an American fin-tech renaissance and spewing out supremely innovative products.

At first, Square nurtured the business by targeting the low hanging fruit– small and medium size enterprises in dire need of a strong injection of fin-tech infrastructure.

It largely stayed away from the big corporations that adorn billboards across the Manhattan skyline.

That was then, and this is now.

Square is going after the Goliath’s fueling a violent rise in gross payment volume (GPV).

Modifying themselves for larger institutions is the next leg up for Square.

They recently inaugurated Square for Restaurants for larger full-service restaurants.

Business owners do not need technical backgrounds to operate the software and integrating Caviar into this program emphasizes the feed through all of Square’s software.

Dorsey has built an ecosystem that has morphed into a one-stop shop for comprehensively running a business.

Migrating into business with the premium corporations offers an opportunity to augment higher margin business.

This is the lucrative path ahead for Square and why investors are festively lining up at the door to get a piece of the action.

The downside with an uber-growth company like Square are lean profits, but they have managed to eke out three straight quarters of marginal spoils.

However, the absence of profits can be stomached considering the total addressable market is up to $350 billion.

Grabbing a chunk of that would mean profits galore for this too hot to handle company.

Expenses are always a head spinner for Silicon Valley firms and attracting a dazzling array of engineers to spin out breathtaking profits can’t be done on the cheap.

The Cash app download figures are sizzling and is one of the most popular apps in the app store.

Square’s marketing strategy is also turning a corner getting out their name leading to sale conversions.

These are just several irons in the fire.

The last two years has seen this stock double each year, could we be in for another double next year?

If measured by growth, then I see why not.

Growth is the ultimate acid test deciding whether this stock will be dragged down into the quick sand or let loose to run riot.

Other second-tier tech firms in the middle of a sweet growth spot pack a potent punch like Spotify (SPOT) and Grubhub (GRUB) which are growing annual sales around 50-60%.

Material profits are also irrelevant for the aforementioned tech juggernauts.

Square is expanding at the same fervent pace too, and the hyper-growth only makes payment processors like Visa (V) quasi-jealous of such staggering numbers.

And when Square trots out numbers to the public like that with (GPV) shooting out the roof, the stock does nothing but go gangbusters.

Either way, Square has popularized making credit card payments through smartphones and that in itself was a tough nut to crack amongst tough nuts.

Square also has a line-up of impressive point-of-sales products such as Caviar.

In fact, merchant sellers are adopting an average of 3.4 Square software apps with invoices, loans, marketing, and payroll software being the most beloved.

Square also offers other software that can handle back office tasks and manage inventory.

The software and services business is on pace to register over $1 billion in sales in 2019.

The breadth of functions that can boost a company’s execution highlights the quality of software Dorsey has produced.

I always revert back to one key ingredient that all tech companies must wildly indulge in to fire up the stock price – innovation.

Innovation in bucket loads is something all the brilliant tech firms crave such as Microsoft (MSFT), Amazon, and Salesforce (CRM).

Overperformance starts from the top and trickles down to the people they hand pick to manage and run the businesses.

Jack Dorsey is right up there with the best of them and his influence cannot be denied or ignored.

His stewardship over his other company Twitter (TWTR) is sometimes worrisome because of a pure scheduling conflict, but it’s obvious which company is having a better year.

Square steers clear of the privacy and regulatory minefields handcuffing Twitter.

And it could be safely assumed that Dorsey enjoys his afternoons more at Square than his mornings across the street at Twitter where he is bombarded by heinous problems up the wazoo.

When you conjure up an up-and-coming company that could rattle the establishment, Square is one of the first companies that comes to mind.

Some analysts even argue this company deserves to be lifted into the vaunted Fang group.

I would say they are on their merry way but they just aren’t big enough to command a spot on the Fang roster.

I have immense conviction this stock will be a deep influencer of our time, and its diversified software offerings add limitless dimensions underpinning massive revenue streams.

In Q2, the subscription revenue grew 127% YOY underscoring the success the software team is having, crafting productive apps applicable to business owners.

Business owners can even take out a loan through Square Capital which issues micro-loans to small business owners.

In need of financing? Ring up Dorsey’s company for a few quid.

Starkly contrasting Square in the payment processors space is Visa (V).

Visa is not a hyper-growth company going ballistic, but a stoic behemoth unperturbed.

The 3.283 billion visa cards that adorn its insignia represents scintillating brand awareness and efficiency.

When Tim Cook was asked if Apple (AAPL) plans to disrupt Visa, he smirked and said, “People love their credit cards.”

This is a prototypical steady as she goes-type of company.

They do not offer micro-loans to small businesses or dabble with any of the murky sort of products that can be found on the edge of the risk curve.

They are a safe and steady pure payment processor.

Its network can digest 65,000 transactions per second and is universally cherished as a brand around the world.

All of this led to an operating margin of 66% in 2017.

Square has identified other parts of the payment process to snatch and do not directly compete with Visa.

They partner with Visa and pay them a processing fee.

Subsequently, Square is paid a merchant fee after the payment is approved.

Visa has a monopoly and a moat around their business as wide as can be.

Square is a different type of beast – growing uncontrollably and hell-bent on spawning a revolutionary fin-tech paradigm shift.

The question is can Square eventually turn payment heavyweights like Visa on its head?

The path is fraught with booby traps and as Square generates the projected sales and bolsters its revenue, it could start to encroach on these legacy processors too.

Yet, it’s too early to delve into that threat yet.

Enjoy the ride with Square and better to lay off this potent stock until a better entry point presents itself.

This stock will go higher. Giddy-up!

Mad Hedge Technology Letter

September 18, 2018

Fiat Lux

Featured Trade:

(THE DANGERS OF PLAYING TECH SMALL FRY),

(FIT), (AAPL), (CRM), (FTNT), (SQ), (SNAP), (BBY)