Mad Hedge Technology Letter

May 22, 2023

Fiat Lux

Featured Trade:

(BUY EMERGING CHIP COMPANIES ON BIG DIPS)

(SWKS), (CRUS), (QRVO)

Mad Hedge Technology Letter

May 22, 2023

Fiat Lux

Featured Trade:

(BUY EMERGING CHIP COMPANIES ON BIG DIPS)

(SWKS), (CRUS), (QRVO)

So what about these small chip companies that attach themselves to Apple’s future?

The ones like Qorvo (QRVO), Skyworks Solutions (SWKS), and Cirrus Logic (CRUS).

Many refuse to invest in them because they are too reliant on Apple.

I would argue the exact opposite.

It’s exactly because they have strong relationships with Apple that readers need to invest in these stocks.

The issue is that they are highly volatile and missing the optimal entry point can mean the difference between a profit and a loss.

Apple can’t develop everything internally.

It’s just too much to do.

I don’t believe the tech giant could gradually replace most of its third-party components with first-party ones.

Furthermore, I do not see Apple abruptly swapping suppliers or canceling an existing supplier's orders with its competitors to secure lower prices.

As a result, most of Apple's suppliers can negotiate favorable terms.

For 2023, iPhone shipments appear stable as the market continues to recover from weak demand and ongoing macroeconomic challenges, but I believe this is just a short-term blip.

Cirrus Logic mainly sells audio converters and chips, but it also develops other mixed-signal processing chips for wireless headsets, wearables, augmented reality/virtual reality (AR/VR) headsets, notebook computers, and mobile devices. Apple installs Cirrus' audio chips and IC controllers in its iPhones, iPads, and Macs.

Skyworks produces a wide range of wireless chips for the mobile, automotive, home automation, wireless infrastructure, and industrial markets. Apple installs Skyworks' wireless chips in its iPhones, iPads, Macs, Apple Watches, and other devices.

Lumentum is a diversified supplier of optical chips for service providers, 3D-sensing chips which are used in mobile devices, cars, 3D printers, and other industrial machines, as well as commercial lasers for manufacturing various products. Apple uses Lumentum's 3D-sensing chips and lasers to power its Face ID features.

These companies bask in the glory of being connected to Apple when many other chip companies wish they were in the same position.

Cirrus relied on Apple for 79% of its revenue in 2022 and the gains from this contract are precisely why it is great to hold this company's stock.

Skyworks generated 58% of its revenue from Apple in fiscal 2022, while Lumentum generated 29% of its revenue from Apple in 2022.

The semiconductor industry has been prone to cycles. Periods of soaring demand are followed by periods of drought, causing some wild swings in many chip stocks. But some news reports predict that because of the demand for chips throughout the economy, these boom-bust cycles might be over.

Semiconductors are now going into various devices between 5G, cloud datacenters, phones, PCs, laptops, cars are using more and more semiconductors that the demand is becoming so diversified and that supply is becoming so expensive to bring on. It's going to be much more of a steadier business going forward, more like a steady growth business rather than a cyclical business with booms and busts.

Don’t believe the naysayers who urge investors to stay out of chip stocks because of overreliance. That is like saying Warren Buffet is too reliant on Apple which is false.

Wait for a big dip of 15% or 20% to invest in these small chip stocks.

Global Market Comments

September 10, 2019

Fiat Lux

SPECIAL ARTIFICIAL INTELLIGENCE ISSUE

Featured Trade:

(NEW PLAYS IN ARTIFICIAL INTELLIGENCE),

(NVDA), (AMD), (ADI), (AMAT), (AVGO), (CRUS),

(CY), (INTC), (LRCX), (MU), (TSM)

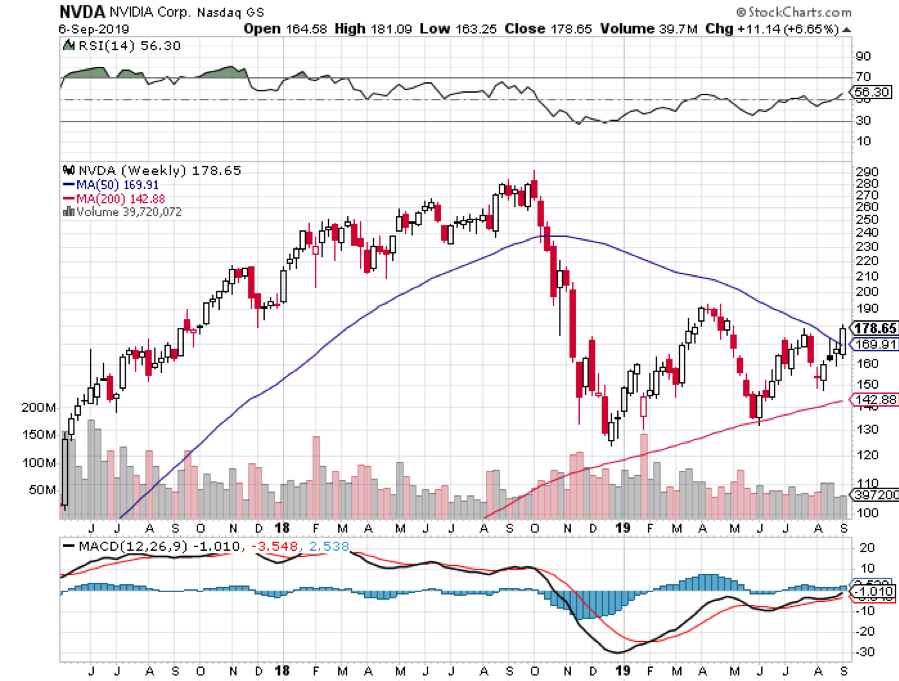

It’s been three years since I published my first Special Report on artificial intelligence and urged readers to buy the processor maker NVIDIA (NVDA) at $68.80.

The stock quadrupled, readers are understandably asking me for my next act in the sector.

The good news is that I have one.

For a start, you could go out and buy NVIDIA again.

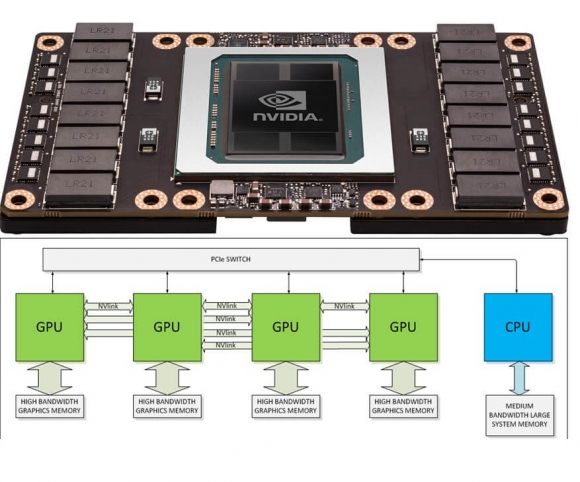

With an explosive 50% annual earnings growth, a near-monopoly in super fast processors, and a huge lead over the competition, I think there is another double in the shares that could take the price up to a stratospheric $300. Its newest super-fast graphics card, the Turing, promises to be a real barn burner and dominate the industry yet again.

But I can do better than that.

The good news if you are new to this sector is that the entire AI space has started to broaden out to offer a host of investment opportunities beyond the tiny handful I first mentioned in 2016.

These include legacy chipmakers, survivors of the great Dotcom bust, whose shares have barely moved in years.

Yes, there is such a thing as a cheap AI stock. To find out who they are, read on.

The reason for the expansion of the AI sector is that practically overnight these ultra-sophisticated algorithms have become essential to any company that wants to survive in online commerce or stay in business….period.

Those of us who have been in this business for more than 15 minutes have seen this pattern before, and the resulting impact on share prices: the Boeing 707, the personal computer, Windows, the Internet, and the smart cell phone.

AI is everywhere.

In the old days, visiting a website and window-shopping their products was easy. You just clicked around a few times and then moved on to the next site.

Now if you click on a product once, that site will follow you around relentlessly for months, appearing in the margins of your emails, offering you endless discounts and special deals.

I bought a Dell computer six months ago, and it is still pounding away at me with better offers. I feel like such a dummy buying a machine at the first price asked.

That is all AI.

The auto industry is now a major growth industry for AI. Even a simple garden-variety vehicle needs 100 chips just to operate.

The gull-wing doors on my new Tesla Model X each has its own learning program. They never open the same way twice.

In fact, when I first picked up the car last year, the salesman warned by saying it would be “stupid” for the first 3,000 miles.

It had to “learn” how to drive before I let it attempt any sophisticated self-driving maneuvers, like backing into a parking space on a crowded street.

I let it park itself in my garage now. I have only had a heart attack once.

With US annual auto production at 16.7 million units annualized, and global car and commercial vehicle production at a record 94.64 million, that is a lot of processors.

I have been covering Silicon Valley since it was a verdant, sun-kissed peach orchard in Northern California.

I have to say that in the half-century that I have followed the technology industry, I have never seen the principals, gurus, and visionaries so excited about a major new trend like AI.

Asking if AI is relevant now is like pondering the future of Thomas Edison’s new electricity invention in 1890.

If you think that AI still belongs in the realm of science fiction, you obviously didn’t get the memo. It is all around us all the time, 24/7. You just don’t know it yet.

And here’s the rub.

It is impossible to invest purely in AI.

All-new AI startups comprise small teams of experts from private labs and universities financed by big venture capital firms like Sequoia Capital, Kleiner Perkins, and Andreeson Horowitz.

After developing software for a year or two, they are sold on to major technology firms at huge premiums. They never see the light of day in the form of a public listing.

Alphabet (GOOGL) acquired Britain-based Deep Mind in 2014. Later that year, Google’s AlphaGo program defeated the world’s top-ranked Go player.

In 2016, Microsoft (MSFT) purchased Equivio, a small firm that applies AI to advanced document searches on the Internet.

Amazon (AMZN) recently bought out Orbeus, a startup known for machine learning tools for image recognition.

Amazon’s Jeff Bezos now says that his Amazon Fresh home food delivery service is using AI to grade strawberries.

Really!

We’re not talking small potatoes here.

The global artificial intelligence market is expected to grow at an annual rate of 44.3% a year to $23.5 billion by 2025.

Nearly half of all applications now use some form of AI that by 2020 will earn businesses an extra $60 billion a year in profits.

And from what I have learned from speaking to the major players over the last few weeks, I am convinced that these are low numbers by an order of magnitude.

I have been following developments in artificial intelligence since the 1960s.

There were those feeble computer dating attempts in the early seventies where we all had to prepare IBM punch cards.

I was matched with an annoyingly aggressive bleach blonde real estate agent. (Really?). Her only real qualification was that she was female.

It took decades and tens of thousands of programming man-hours before IBM’s Deep Blue could become a chess grandmaster in 1996, defeating Gary Kasparov.

Big Blue’s latest effort came to us with Watson in 2007, an 85,000-watt behemoth with 90 servers and 15 terabytes of data, or three quarters of the content of the entire Library of Congress.

The machine can read a staggering 1 million books a second. IBM has so far poured $15 billion into the project.

In 2011, Watson defeated the top-rated Jeopardy game show contestant by answering the question “What city’s national museum lost the “Lion of Nimrod.” The answer was “What is Baghdad” (I knew that!).

Today, Watson is on loan to the University of North Carolina at Chapel Hill where it has been deployed to cure cancer.

It took scientists a week to teach Watson how to read medical literature. In the second week, it read every paper published on cancer, some 25 million.

By the third week, it was proposing customized cures for advanced cancer patients, which achieved a 33% success rate.

After all, it can read all of the 8,000 cancer papers that are published every day from around the world IN SECONDS!

Scientists say that Watson has so far reached only 1% of its true potential.

It gets better than that.

A clinic can now biopsy your tumor, sequence its DNA, design a custom protein that will target and destroy your personal tumor, mass-produce it, inject it in your tumor, and cure you of cancer in a month.

This is being done with human volunteers in clinical trials NOW.

Expect this procedure to go retail and be made available to you in about five years. And by that, I mean cheap, locally available, and covered by your health insurance policy.

I believe that Watson and its future offspring will cure the major human maladies within a decade. My generation will probably be the last to suffer serious disease.

It isn’t just Watson that will take us the great leap forward in computing. By 2020, you will be able to buy a low-end laptop for $500 that can hold ALL KNOWLEDGE ACCUMULATED IN HUMAN HISTORY!

They better hurry. That body of knowledge is doubling every 18 months!

It is a key part of my argument that the US will enjoy a Golden Age and see a return of the “Roaring Twenties” during the 2020s.

If you have in any way been involved in the stock market for the past five years, AI has invaded your life.

High frequency trading and hedge funds now account for 70% of the daily trading volume on the major stock exchanges, and almost all of this is AI-driven.

Having spent my entire life trading stocks, I can confirm that in recent years the market’s character has dramatically changed, and not for the better. Call it trading untouched by human hands.

Algorithms are trading against algorithms, and whoever wins the nuclear arms race brings home the big bucks.

You used to need degrees in Finance and Economics, or perhaps an MBA, to become a professional fund manager. Now it’s a Ph.D. in Computer Science.

Remember the May 2010 flash crash when the Dow Average plunged 1,100 points in minutes wiping out $4.1 billion in equity value? AI’s fingerprints were all over that.

In 2016, the British pound lost 6% of its value in a mere two minutes, a move unprecedented in the history of foreign exchange markets. The culprit was AI.

Don’t expect the path forward to AI to be an easy one.

Indeed, the machines already have the power of life and death over all of us.

No less figures than Nobel Prize winner Dr. Stephen Hawking and Tesla’s Elon Musk have warned that computers and the Internet may have the power to pose a threat to human existence within a decade.

They are especially concerned about the militarization of powerful robots, something I know the US Defense Department is hell-bent on developing.

As I write this, the only thing preventing a drone attacking a village in Afghanistan is an Army corporal hitting a red button on a console in Nevada.

In the future, antivirus software won’t be needed to protect your computer. It will be essential to protect you FROM your computer.

You know that massive denial of service attack that hit the United States on October 21, 2016?

I asked one of my friends at security giant Palo Alto Networks (PANW) if it was the Russians again. He replied, “You better hope it’s the Russians.”

The implication is that the Internet may have launched the attack itself.

Now, about that stock recommendation.

Since we aren’t venture capitalists, we can’t buy into pure AI firms in their early stages. And I’m too old to get a Ph.D. in computer science.

We, therefore, have to be sneaky and get in through the back door via an indirect play which still has plenty of upside leverage.

My current favorite among the AI alternative stocks is Advanced Micro Devices (AMD).

If Intel only piques your appetite for AI stocks and you feel you need another serving, I have listed below ten names that will benefit mightily from this once-a-century opportunity.

AI Stock to BUY

Advanced Micro Devices (AMD)

Analogue Devices Communication (ADI)

Applied Materials (AMAT)

Broadcom (AVGO)

Cirrus Logic (CRUS)

Cypress Semiconductor (CY)

Intel (INTC)

Lam Research (LRCX)

Micron Technology (MU)

Taiwan Semiconductor (TSM)

If you’re really lazy, you can just buy a basket of semiconductor stocks through an industry-specific ETF.

The largest is the VanEck Vectors Semiconductor ETF (SMH), with $1.3 billion in assets under management. For a prospectus on the fund, please click here.

Or you could just stick with NVIDIA.

No matter how you want to slice and dice it, AI should be a dominant factor in your IRA, 401k, or benefit plan.

And you are a trader by nature, this will be a great sector to trade around.

As for your computer, you better start leaving it unplugged at night.

You never know.

![]()

Mad Hedge Technology Letter

December 20, 2018

Fiat Lux

Featured Trade:

(MICRON TECHNOLOGY BOMBS AGAIN)

(MU), (FDX), (UPS), (AAPL), (QRVO), (SWKS), (NXPI), (CRUS), (LITE),

If there was ever a canary in the coal mine, we got one with chipmaker Micron (MU) delivering weak earnings results missing on the top line but squeaking through a one-cent beat on the bottom line.

Love them or hate them, chip companies are susceptible to the boom-bust cycle that is a hallmark of the chip industry.

The beginning of the bust stage of the cycle is upon us with management detailing an “inventory adjustment” that put a damper on revenue.

Micron followed that up by reducing capex for next year and it will take 2-3 quarters to work off this bloated inventory channel.

The perpetrator to the inventory backlog is the smartphone industry.

President and CEO of Micron Sanjay Mehrotra particularly noted “high-end smartphones” as the malefactor tugging down the demand.

This is another damming testament to the prospects of Apple’s (AAPL) suppliers Quorvo (QRVO), Skyworks Solutions (SWKS), NXP Semiconductors (NXPI), Cirrus Logic (CRUS), and Lumentum Holdings (LITE) who can’t catch a break.

The last six months have fired a barrage of poison-tipped arrows at their core business and these stocks are squarely in the no-fly zone until Apple and the trade war can conjure up some good news.

To say these shares are oversold is an understatement, but we are in an extreme trading environment with volatility shooting up the wazoo.

Further reducing the glimmer, Chinese tariffs took up a worrying amount of the conference call dialogue. Investors found out that tariffs pinged half a percent of gross margins.

I have been outright bearish the chip industry from the middle part of the year and Micron is heavily reliant on China for about half of its revenues which is a death sentence in December 2018.

As the China risks have spiked after each head fake détente, so have the execution risks to chip companies with an overly reliant manufacturing process in China.

Not only has the execution risk ratcheted up, but the regulatory risk through costly tariffs is now eroding Micron’s margins.

If you thought that was a downer, then FedEx (FDX) made sure the nail was in the coffin by its ghastly earnings report.

The stock sold off hard confirming fears that global growth is decelerating.

Management did not mince their words about the state of the world and investors usually listen because FedEx is a reliable yardstick of the bigger global economy.

CEO of FedEx Fred Smith offered an olive branch painting a picture of a “solid” US economy, but the conundrum is that the US economy and any other country don't exist in a vacuum and that has been highly evident in Britain who is engaging in economic suicide by disengaging from the globalized world.

Smith cited Europe as a stumbling block and blamed the bulk of weak guidance on “bad political choices”, a thinly veiled dig at the poor level of governance carried out around the world lately.

I might chime in that it is quite strange when political parties and sovereign nations adopt the game of chicken as the leading political strategy applying it to everything and anything.

The side effects to business have been startling with management unable to assuage investor sentiment and business plans shredded apart because of impulsive policy moves.

Politicians aren’t grasping fully that stock market moves are inherently tied to the news cycle and the overwhelming volume of bad news that shouldn’t be as bad as it should be, has a multiplier effect on the stock market algos that go haywire.

It truly is the world of the algos and humans are living in their world and not the other way around.

The most important takeaway from FedEx is what they didn’t say.

Early development of the de-facto Amazon Airlines has already cost FedEx up to 3% of total volume growth.

And this is just the beginning.

Amazon is still feeling around for the rocks at the bottom while it tries to cross the river.

Once it masters logistics, expect a radical swivel towards the integration of their own airline into the bulk of Amazon.com’s package deliveries.

And when FedEx’s management claims that the market has gotten it wrong about the Amazon threat, that means the market is completely correct.

The market is always right.

Amazon’s master plan is to vertically integrate every last process down to the last mile, the doorbell, and now the microwave as Amazon has rolled out a myriad of smart home products.

FedEx management has to be blind to understand this won’t damage future sales.

It is materially false if FedEx thinks Amazon is not competing with them, and the sad part of this is there is not much FedEx can do about it.

The shipping giant cut its 2019 earnings forecast between $15.50 and $16.60 per share — from $17.20 to $17.80 a share.

FedEx’s goal of eclipsing $1.5 billion in operating income by fiscal 2020 has been shelved disappointing investors. FedEx cratered 12% on a day that saw the Fed do its best body slam imitation on the market.

The first phase of the logistics swivel is taking delivery of 40 planes and constructing a hub that will be able to operate 100 planes, then it will do as Amazon does with everything – scale it to the hills.

FedEx and UPS have a few years to figure out how to counteract this existential crisis and not decades.

Technology moves that fast now in this interconnected world.

Domestic volume comprises 17% of revenues at UPS and 19% at FedEx, management won’t be able to hide this problem under the carpet as the drag becomes highly visible like a sore thumb.

Analysts expect Amazon Air to offer more than slim savings to its business model saving between $2 to $4 per package next year.

The annual savings add up from $1 billion to $2 billion or 3% to 6% of its global shipping costs.

It is spot-on to admit that over the last few years, the explosion of packages during the holiday shopping season has put higher levels of stress on the U.S. Postal Service, UPS (UPS), and FedEx.

Even though overloaded with business, all three carriers have posted record levels of on-time deliveries and they appear to be handling the surge in volume.

But there will come a moment in time when an inflection point will give Amazon the keys to the car.

They will suddenly stop offering their e-commerce packages to these three carriers and business will drop off a cliff for them.

That is the future these three are confronted with and there is nothing they can do unless they build their own Amazon.com which is a pie in the sky dream at this point.

Amazon is out to prove they can execute the logistic part of their business cheaper and faster than anyone else because of the superior management and mountain of data they can act on.

I believe it will happen.

Part of stretching themselves with a new army of minions in Washington D.C., New York, and Nashville is partly about fulfilling the job of comprehensively and vertically integrating their e-commerce platform.

It will take a horde of workers to make this happen.

If the prophecy from FedEx management comes true and the global economy indeed softens next year, the stock will bear the brunt of the downside momentum and UPS too.

Stay away from the trio of deliverers. There are healthier fishes in the sea.

And as for the chip sector and Apple, wait on the sidelines for some good news.

Global Market Comments

August 16, 2018

Fiat Lux

SPECIAL ARTIFICIAL INTELLIGENCE ISSUE

Featured Trade:

(NEW PLAYS IN ARTIFICIAL INTELLIGENCE),

(NVDA), (AMD), (ADI), (AMAT), (AVGO), (CRUS),

(CY), (INTC), (LRCX), (MU), (TSM)

Global Market Comments

July 27, 2018

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE FRIDAY, AUGUST 3, 2018,

AMSTERDAM, THE NETHERLANDS GLOBAL STRATEGY DINNER),

(STOCKS TO BUY ON THE OUTBREAK OF TRADE PEACE),

(QQQ), (SPY), (SOYB), (CORN), (WEAT), (CAT),

(DE), (BA), (QCOM), (MU), (LRCX), (CRUS),

(ORIENT EXPRESS PART II, or REPORT FROM VENICE)

So, how will the trade war end? It could be the crucial trading call of 2018.

"That which can't continue, won't," I paraphrase the noted economist Herbert Stein. I think that logic neatly applies to our global trade wars today.

In 1970, some 25% of world GDP was accounted for by international trade. Today it is 52%. Germany has been the powerhouse, with trade growing from 25% to 80%, largely through exploding auto exports. Trade growth in the U.K. has been pitiful as the old colonial ties loosened, improving only from 40% of GDP to 52%.

In the U.S., trade has grown from 10% to 25% of GDP during this time. It is far lower than the rest of the G7 nations because of the massive size of its domestic economy.

Still, placing restraints on 25% of U.S. GDP, or about $5 trillion, is quite a big hit. Think an imminent recession, quite possible a severe one. The $13 billion in subsidies offered the agriculture sector is but a drop in the bucket. It would be like killing off the goose that laid the golden egg.

Trump has a weak hand, which is growing weaker by the day. It is just a matter of time before he folds. Not to do so would entirely wipe out the benefits of the December tax package, yet still leave the U.S. government with $2 trillion in new debt. It is a perfect money destruction machine.

My bet is that Trump will claim victory at some point soon, regardless of what transpires on the negotiation front. Take the trade war away, and stocks will immediately jump 10%. That's what the stock market thinks, with NASDAQ (QQQ) at an all-time high, and the S&P 500 (SPY) just short of one. Stocks are trading over the medium term as if Donald Trump doesn't exist.

Which stocks should you buy when trade peace breaks out? Buy those that have suffered the most. The ags have to be at the top of your list, such as Soybeans (SOYB), Corn (CORN), and Wheat (WEAT), the worst hit. The old industrials such as Caterpillar (CAT), John Deere (DE), and Boeing (BA) also have to be a priority.

In the technology area you have to rotate out of the FANGs and into chip stocks, the worst performers of the sector this year. Perhaps this is what the market is shouting at us with the horrific one-day decline in Facebook (FB) yesterday. China relies on the U.S. for 80% of its chips and all of its high-end graphics cards.

China's canceling of the QUALCOM (QCOM) takeover of its NXP Semiconductors shows to what extent it is willing to retaliate in the tech area. Chip stocks to buy for the rebound should include Micron Technology (MU), Cirrus Logic (CRUS), and Lam Research (LRCX).

Even if the trade war ends tomorrow, business conditions will never be the same. Confidence in American reliability will never completely recover. Sure, Trump will be gone in 2 1/2 years. But what if he is replaced by someone worse? Trading with the United States now incurs a level of political risk not seen since the War of 1812, when Washington burned.

But no trade war is certainly better than a trade war if you are a trader or investor.

Telling the Captain How to Steer the Ship

Mad Hedge Technology Letter

July 26, 2018

Fiat Lux

Featured Trade:

(THE TRADE WAR'S COLLATERAL DAMAGE),

(SWKS), (ACIA), (CRUS), (XLNX), (ROKU), (SQ)