Mad Hedge Technology Letter

March 6, 2024

Fiat Lux

Featured Trade:

(CYBER SECURITY IS STILL GROWTH)

(CRWD), (PANW)

Mad Hedge Technology Letter

March 6, 2024

Fiat Lux

Featured Trade:

(CYBER SECURITY IS STILL GROWTH)

(CRWD), (PANW)

Since starting the company, CrowdStrike (CRWD) has brought cybersecurity to the cloud.

They have pioneered AI for cybersecurity, and quickly become the de-facto security platform that disrupts, displaces, and consolidates other vendors.

This stock has been really good to Mad Hedge Tech Letter followers, and we recently took profits in a successful in-the-money bull call spread in CRWD.

Money will flow into enterprise protection as the stakes get higher with hackers looking to strike gold.

When talking about the threat landscape, CrowdStrike pioneered commercial threat intelligence that governments and companies of all sizes depend on.

It's CrowdStrike that delivers billions of new threat detections every month to stop breaches.

It's CrowdStrike that is the search bar of security, where security analysts complete millions of queries daily.

What took hackers hours, has shrunk to minutes and seconds. Attack speeds will only accelerate.

The cloud is increasingly under attack and CRWD exists to protect businesses against these attacks.

CRWD tracked a 75% year-over-year increase in cloud intrusion attempts.

The cloud is today's battleground for cyberattacks.

Generative AI is an adversary force multiplier and the last few years have seen the onboarding of this new force multiplier.

Gen AI puts advanced cybercrime tradecraft in the hands of attackers of all skill levels. Gen AI will dramatically grow the adversary population.

CRWD collects trillions of threat signals daily, creating one of the world's largest and fastest-growing cyberthreat datasets.

From day one, CRWD has been an AI company, training the industry's most effective and accurate AI models to prevent attacks based on data mode.

Embedded in the Falcon platform is a virtuous data cycle where CRWD collects cybersecurity's very best threat intelligence data, builds, and trains robust preventative and generative models, and protects CRWD customers with community immunity.

In today's environment of heightened cyberattacks, the latest SEC breach disclosure regulation only increases the pressure on companies and their boards.

One of the best of breeds and its superior performance are a critical reason to why the share price has moved up in the last few years.

Let’s look at the numbers behind the business model.

Moving to the P&L, total revenue grew 33% year over year to reach $845.3 million.

Subscription revenue grew 33% over Q4 of last year to reach $795.9 million. Professional services revenue was $49.4 million, representing 26% year-over-year growth.

Subscription customers were five or more, six or more, and seven or more modules growing to 64%, 43%, and 27% of subscription customers, respectively.

CRWD is landing bigger with new customers on average adopting 4.9 modules out of the gate, an increase over last year. CRWD’s gross retention rate remained high at 98%.

CRWD is knocking it out of the park.

It’s hard to maintain growth company status in the head of major macro headwinds.

Many enterprise businesses are pulling back spend, but cybersecurity hasn’t been curtailed as of yet.

Tech companies are becoming more efficient and cybercrime hasn’t felt the pain of leaner software budgets.

This bodes well for the future of cyber security and the main players in the industry.

Mad Hedge Technology Letter

January 17, 2024

Fiat Lux

Featured Trade:

(GROW WITH CROWDSTRIKE)

(CRWD), (NVDA)

CrowdStrike (CRWD) is expensive by any metric, but so are other tech stocks like Nvidia (NVDA).

The trajectory of the stock still looks bright.

The cybersecurity company truly dishes out impressive growth numbers.

They are expected to grow sales by 39% over the next year and growth remains voluminous with no headwinds appear in the short term.

I’d be foolish not to mention one of the largest tailwinds in the tech sector in the form of defending and deterring digital malicious actors.

It’s real and capital is being allocated towards it.

The global cost of cybercrime is expected to double by 2028.

Sporting a market capitalization of $68 billion, CrowdStrike would need annualized returns of 18% to reach the $1 trillion club by 2040.

What do they mainly do?

Sifting through trillions of data points every week, CrowdStrike's single-agent, cloud-based cybersecurity platform grows more robust for each additional customer that joins its platform.

Quickly expanding its solutions from focusing primarily on endpoint protection (think laptops, printers, and servers) to becoming a complete security platform, CrowdStrike has grown from three security modules in 2016 to 27 today.

Each module provides a unique security solution and can be added by customers to fit their specific needs - all by relying upon just one agent, CrowdStrike's Falcon platform. The average number of agents on an endpoint today is 13 or more, so CrowdStrike's platform offers much-needed vendor consolidation for businesses looking to simplify their operations.

CrowdStrike is gradually becoming a one-stop shop for businesses' cybersecurity needs. Its growth potential and optionality seem almost boundless as it releases new modules tailor-made for its customers' desires. Look no further than two of its recent module advancements, each highlighting the company's ongoing shift toward becoming a complete security platform:

Falcon ID: CrowdStrike's identity protection and detection modules could become the company's next massive growth outlet. With 80% of global attacks stemming from exploited IDs, sales for these solutions grew from $7 million in annual recurring revenue (ARR) in Q3 of 2021 to over $200 million in Q2 of 2024.

Falcon Cloud: Bolstered by its recent acquisition of Bionic, which focuses on identifying and protecting items in the cloud, CrowdStrike now offers a complete cloud security solution. Growing its ARR from $106 million in Q4 of 2022 to nearly $300 million today, this cloud unit operates in a market expected to be worth over $32 billion by 2028.

Crowdstrike also landed an eight-figure deal from the federal government in its latest quarter. It counts less than 1% of the public sector as customers, so deals like this ignite a juicy channel of new revenue.

Thanks partly to its land-and-expand business model, CrowdStrike sees increasing profit margins for each additional module it sells to existing clients and each new customer it adds.

Who doesn’t like accelerating revenue and hypergrowth?

That’s what you get from CRWD.

The stock has been in overdrive pushing to new heights so I wouldn’t chase it right here.

It was only 365 days ago that the stock was at $101 and just touched $283.

That extraordinary rise is not the norm but is common with hyper-growth stocks.

It’s time to take the foot off the pedal and wait for a large dip which I do believe we will get.

That will be the next buying opportunity around $240 per share for CRWD.

Mad Hedge Technology Letter

November 30, 2022

Fiat Lux

Featured Trade:

(WEAK SALES FOR 2023)

(CRWD), (APPL), (SNAP), (DASH)

Tech growth needs a timeout.

The recent earnings report from cyber security software firm CrowdStrike (CRWD) illustrates the difficulty for firms to project strength in forward guidance.

2023 isn’t looking so rosy for selling security software.

CRWD management offered us weak guidance citing a weakening macroeconomic picture and specifically telling us that small businesses are reluctant to sign new contracts for 2023.

The macroeconomic picture at best isn’t getting better, therefore, some of the forward guidance is coming in tepid.

The natural reaction is for tech stocks to sell off.

In 2022, it’s never been more difficult being a tech CEO and some of the best tech growth companies are getting haircuts that we used to never see before.

Even more worrisome is that tech companies like Apple and Twitter are starting to cannibalize each other because tech is now perceived as a zero sum game more than at any other time I can remember it.

Firms simply don’t think the pie is big enough to share.

This is why ecosystems like Apple and others are executing policies that directly hinder competition.

Unfortunately, cyber security is another add-on that is being sacrificed as tech companies become leaner and meaner.

Many tech companies can still function by skimping on the security defenses.

Shaving the fat to the bone is what we are currently seeing and that doesn’t bode well in the short term for tech stocks that are used to thriving in the excesses.

Another example is Snapchat (SNAP), which ordered back staff to a 4-day in-office work week starting February.

And it’s not just Snapchat or CrowdStrike.

The belt tightening has been broad-based in technology with DoorDash cutting another 1,250 jobs today.

Many of these growth companies over-hired during the government-mandated lockdowns and now are regressing back to the mean.

Since there are no more lockdowns in non-Chinese countries, there is no need for the giant number of DoorDash food deliverers.

Yet the US consumer is still spending even if they get less for each incremental $1 spent.

CrowdStrike reported annual recurring revenue (ARR) of $2.34 billion, up 54% year over year. The company also added 1,460 net new subscription customers for the quarter.

In high times, CrowdStrike and the tech growth with superior business models are unique and stand out.

However, in overwhelming macroeconomic weakness, CRWD gets lumped in with the rest.

I don’t recommend buying CRWD on the dip even if it feels cheap.

The peak CRWD share price almost reached $300 meaning the current stock price is only around 35% of what it once was.

Tech growth will overshoot to the upside when it finds it mojo again, which won’t come back until sometime in 2023.

The lockdowns brought forward a tsunami of demand, revenue, and momentum.

Now we are experiencing the reversing of those tailwinds which is why the stock price has suffered.

Avoid tech growth for now, they will have their time in the sun once again once the headwinds have been digested and CRWD should be on your list for a tech growth stock to purchase on the way up.

Mad Hedge Technology Letter

October 18, 2021

Fiat Lux

Featured Trade:

(THE BEST CLOUD SECURITY GROWTH STOCK TODAY)

(CRWD)

Today’s sophisticated hackers are going “beyond malware” to breach organizations.

These hackers are increasingly relying on hard-to-detect methods such as credential theft and tools that are already part of the victim’s environment.

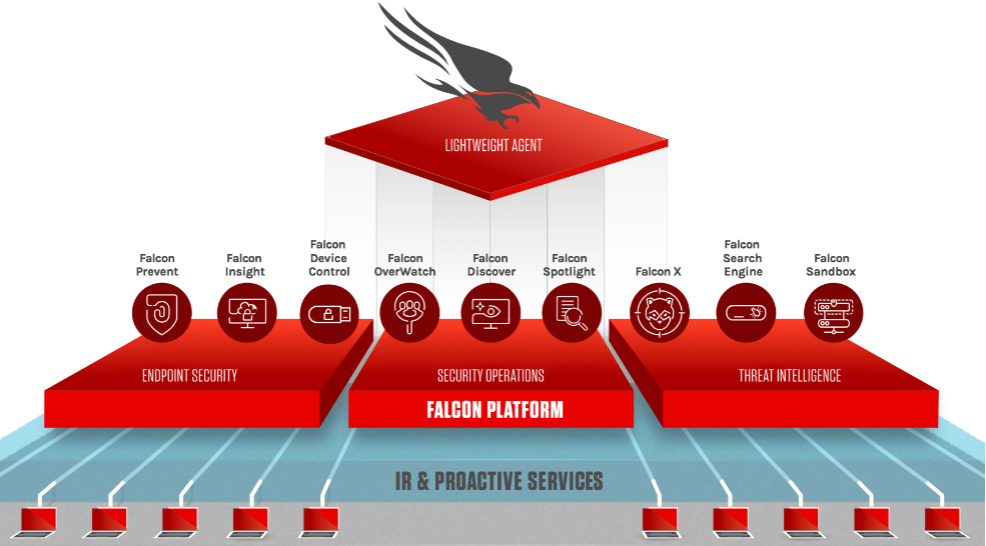

Falcon is the preeminent security platform built by CrowdStrike (CRWD) to stop breaches via a unified set of cloud-delivered technologies that prevent all types of attacks.

Falcon is the major reason why this tech stock is growing so rapidly and why many investors are jumping on the bandwagon.

The stock is up over 400% in the past 5 years, and this is just the beginning of its growth.

CrowdStrike Falcon responds to malicious challenges with a powerful yet lightweight solution.

It unifies next-generation antivirus, endpoint detection and response, cyber threat intelligence, and managed threat hunting capabilities.

Management’s approach to stopping breaches with the Falcon platform is foundational to CrowdStrike's leadership position and maintaining the overperformance which many investors have been impressed with.

Using AI, machine learning, and an intelligent lightweight agent, the Falcon platform defends against today's most sophisticated threats with unmatched speed and simplicity.

Simply put, companies need to employ a holistic breach prevention strategy rather than overly relying on malware prevention.

Nearly every breach you have ever heard of had two things in common, the victims had both a firewall and an antivirus solution, which is why management decided to build the Falcon platform from the ground up to stop breaches and not just prevent malware.

Meanwhile, competitors have fallen further behind as they continue to blindly promote a strategy that relies on malware prevention versus a comprehensive solution, focused on people, process, and technology that stops breaches.

Today, more than half of the detections analyzed were not malware-based.

Attackers are increasingly attempting to accomplish objectives without using malware.

They are exploiting the proliferation of vulnerabilities and abusing systemic weaknesses in identity architecture to get on the system and then move laterally.

This makes it more difficult for legacy and next-gen malware-focused products to be effective because they are not focused on breach prevention.

To further demonstrate my point, I'd like to share a situation with a certain unnamed company using Microsoft's legacy security products that failed to rise to the challenges of today's adversaries and ended up unnecessarily costing them.

This company experienced a long and difficult deployment process, particularly in low bandwidth environments where endpoint performance was critical.

Notably frustrated, this company began to evaluate alternatives when it was unfortunately hit by ransomware that encrypted their primary and backup data, causing weeks of business disruption and a financial impact estimated to be in the tens to hundreds of millions of dollars.

This is a typical story that is told to CrowdStrike and more will follow as the volume of companies ill-prepared is voluminous.

Many of these damaging experiences by companies are then followed by their in-house IT teams connecting with CrowdStrike’s incident response team to remediate and stabilize their IT operations — followed up with deploying Falcon Complete across their environment.

The Falcon platform processes approximately 1 trillion events per day from millions of agents, delivering unprecedented security insights.

This empowers Falcon to benefit from crowdsourcing and economies of scale unlike any other solution on the market today, which I believe enables AI algorithms to be uniquely effective.

CrowdStrike’s success hinges on growing leadership as the trusted security partner of choice and especially growing the Falcon platform.

Several outside reports have praised Falcon Complete and recognized its strength in its breach prevention warranty, fully remote automated remediation, breadth of threat hunting capabilities, and strong machine learning and artificial intelligence capabilities for detection and response.

The net result of focusing on the Falcon platform to increase revenue upside is the subscription revenue growing 71% over Q2 to reach $315.8 million.

While it’s understandable that subscription gross margin fluctuates quarter to quarter, management expects it to remain solidly within an increased target model range of 77% to 82%.

For the next quarter, CrowdStrike expects total revenue to be in the range of $358 million to $365.3 million, reflecting a year-over-year growth rate of 54% to 57%.

Management has reaffirmed that demand for their Falcon platform is still hot, but I am not thrilled that the total revenue growth is expected to drop to the mid-50% from 70%.

Even though this drop is a seasonal adjustment, it was only just in 2018 when the company was doing $100 million in total revenue, and we are talking now about reaching $2 billion per year after almost surpassing $1 billion per year in 2020.

The stock has substantially more upside and any significant drop should be bought.

We are hovering near all-time high’s so any 5-10% drops should be bought into.

I am still highly bullish on this cloud security company and believe its best days are ahead of them.

Mad Hedge Technology Letter

June 28, 2021

Fiat Lux

Featured Trade:

(HOW TO STOP RANSOMWARE-AS-A-SERVICE)

(CRWD)

The world has changed, and protecting one’s network has been thrusted to the top of every CEO's checklist and the CFO is there to make it happen smoothly as well.

Just how to protect the most critical computer networks is still a work in progress; many firms still haven’t got a clue.

Just recently, oil pipeline operator Colonial Pipeline revealed that it had opted to pay hackers a $4.4 million ransom to regain control of its infrastructure.

Another headline rattler, major meat company JBS learned they, too, had been hacked.

The ultimate cost of all this hacking?

Cybersecurity Ventures currently pegs the annual figure at around $6 trillion, though further estimates that the ransomware "business" will be worth $10.5 trillion by 2025.

Threat actors are well resourced and becoming more sophisticated as we speak.

Crazily enough, ransomware-as-a-service sites are making it simpler for even novice e-criminals to run successful and lucrative campaigns, which is contributing to the proliferation of ransomware activity.

This is highly illegal yet actors from abroad feel almost immune wielding their power from offshore authoritarian strongholds where dictators usually chuckle on the news that western companies have been hacked again.

The 2020 CrowdStrike Global Security Attitude Survey revealed that more than half of organizations surveyed worldwide had suffered a ransomware attack within the previous 12 months.

A scary fact is that many of these ransomware attacks, failures and successes, are not publicly reported because companies don’t want the negative publicity and the accompanying stock sell-off with it.

Some hacks are just too big to hide under the carpet.

At the same time, organizations need to transform their businesses in order to keep up with evolving business needs such as work from anywhere and moving their critical applications and workloads to the cloud.

Naturally, this is the perfect time for hackers, new and old, to pounce on the transitory nature of deploying networks into a work-from-home set-up.

CrowdStrike’s Falcon platform is at the epicenter of restoring trust to the security apparatus of companies worldwide.

The integration of threat intelligence and threat hunting into the Falcon platform provides deep insight into the adversaries and how they operate.

Extensive capabilities of the Falcon platform significantly set CrowdStrike apart from both legacy and next-gen vendors.

This includes their acquisition of Preempt and Humio, which could not have been timelier as companies are discovering new ways to shore up protection of their active directories, stop lateral movement and have even greater real-time visibility and search into their endpoints, identities, applications, network edge and cloud from a single data layer.

CRWD was also recognized as the best cloud computing security solution and best managed security service at the 2021 SC Awards where Shawn Henry, president of services and chief security officer, received a Security Executive of the Year award as well.

This growth company has the accelerating metrics to back up its hubris.

In the first quarter, they reached a new milestone as subscription customers surpassed the 10,000 mark.

They added 1,524 net new subscription customers including the customers CRWD acquired from Humio. On an organic basis, the net new subscription customers added in the quarter grew 69% year over year. In total, they now service 11,420 subscription customers worldwide.

To sum up the positivity, the outperformance is attributed to CRWD’s Falcon platform's ability to fully utilize the power of the cloud and AI to stop breaches and provide community immunity.

Also helpful, is the ability to easily and rapidly deploy lightweight agent at scale across both endpoints and workloads without requiring a reboot, while other next-gen vendors fail to scale and require reboots.

The platform is easy to use and easy to manage all from a single user interface; and their ability to leverage the power of the cloud to collect data once and solve many real-world business problems that deliver better outcomes and immediate ROI for customers.

It is entirely possible that with the rate of ransomware accelerating, CRWD will be able to grow the service base from over 11,000 now to 100,000 in less than 2.5 years.

They should be able to achieve this while accelerating their subscription gross-margin target to 85% which would represent an acceleration of the current gross rate margin of 77%.

This company is growing faster and becoming more profitable, what’s there not to like?

In light of the strength I just mentioned, a pullback to $230 would be a great entry point to ride to over $400.

If the firm can at least deliver 70,000 customers in the next few years, the stock is easily at least $400 which would make it around a $100 billion company.

That is entirely doable for CRWD.