Global Market Comments

June 13, 2019

Fiat Lux

Featured Trade:

(TUESDAY, JUNE 25 SYDNEY, AUSTRALIA STRATEGY LUNCHEON)

(CYBERSECURITY IS ONLY JUST GETTING STARTED),

(PANW), (HACK), (FEYE), (CSCO), (FTNT), (JNPR), (CIBR)

Global Market Comments

June 13, 2019

Fiat Lux

Featured Trade:

(TUESDAY, JUNE 25 SYDNEY, AUSTRALIA STRATEGY LUNCHEON)

(CYBERSECURITY IS ONLY JUST GETTING STARTED),

(PANW), (HACK), (FEYE), (CSCO), (FTNT), (JNPR), (CIBR)

Global Market Comments

June 6, 2019

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 28 PERTH, AUSTRALIA STRATEGY LUNCHEON)

(THE IRS LETTER YOU SHOULD DREAD),

(PANW), (CSCO), (FEYE),

(CYBR), (CHKP), (HACK), (SNE)

(CHINA’S COMING DEMOGRAPHIC NIGHTMARE)

Mad Hedge Technology Letter

May 23, 2019

Fiat Lux

Featured Trade:

(ANOTHER 5G PLAY TO LOOK AT)

(EQIX), (CSCO), (GOOGL), (MSFT), (ORCL)

One of the seismic outcomes from the upcoming rollout of 5G is the plethora of generated data and data storage that will be needed from it.

If you are a cloud purist and want to bet the ranch on data being the new oil, then look no further than Equinix (EQIX) who connects the world's leading businesses to their customers, employees, and partners inside the most-interconnected data centers.

On this global platform for digital business, companies come together worldwide on five continents to reach everywhere, interconnect everyone and integrate everything they need to reap a digital windfall.

And whether we like it or not, the future will be more interconnected than ever because of the explosion of data and the 5G that harnesses the data will allow business to reach across the globe and expand their addressable audience.

The stock has reacted like you would have thought with a victorious swing up after a tumultuous last winter.

The cherry on top was the positive earnings report earlier this month.

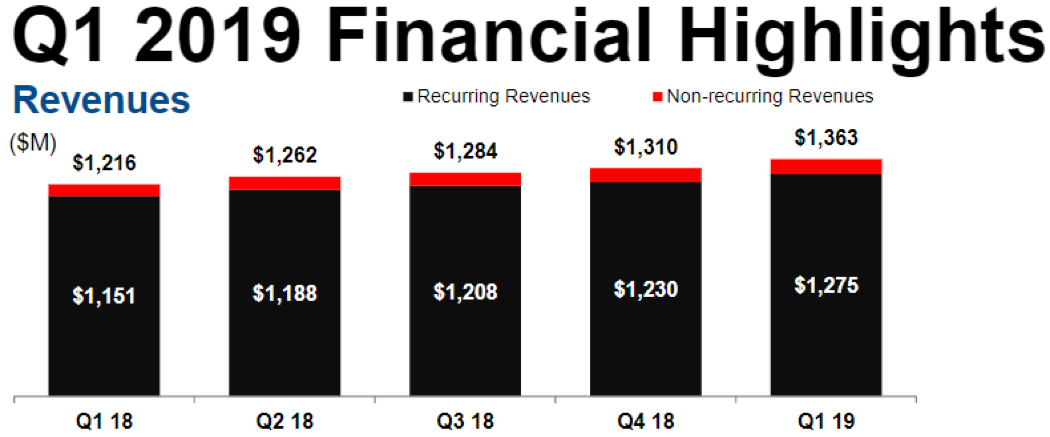

The highlights were impressive and plentiful with revenues for Q1 coming in at $1.36 billion, up 11% year-over-year meaningfully ahead of management expectations.

Equinix’s market-leading interconnection franchise is performing well, with revenues continuing to outpace colocation, growing 12% year-over-year, as the cloud ecosystem continues to scale.

Penetration in “lighthouse accounts” or early adopters increased nearly 50% from the Fortune 500 and 35% from the Global 2,000 demonstrating the expanding opportunity as Equinix unearths more value from the enterprise industry.

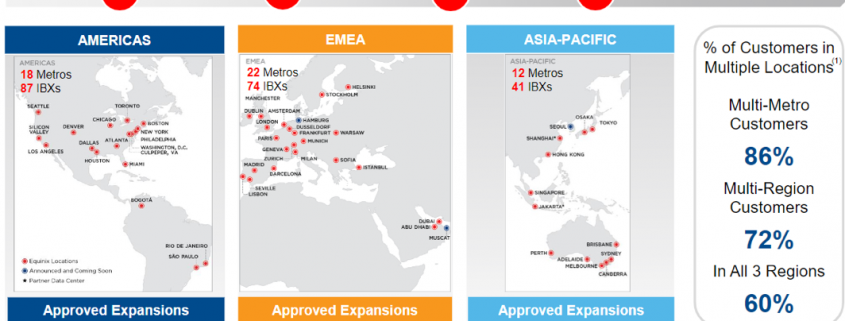

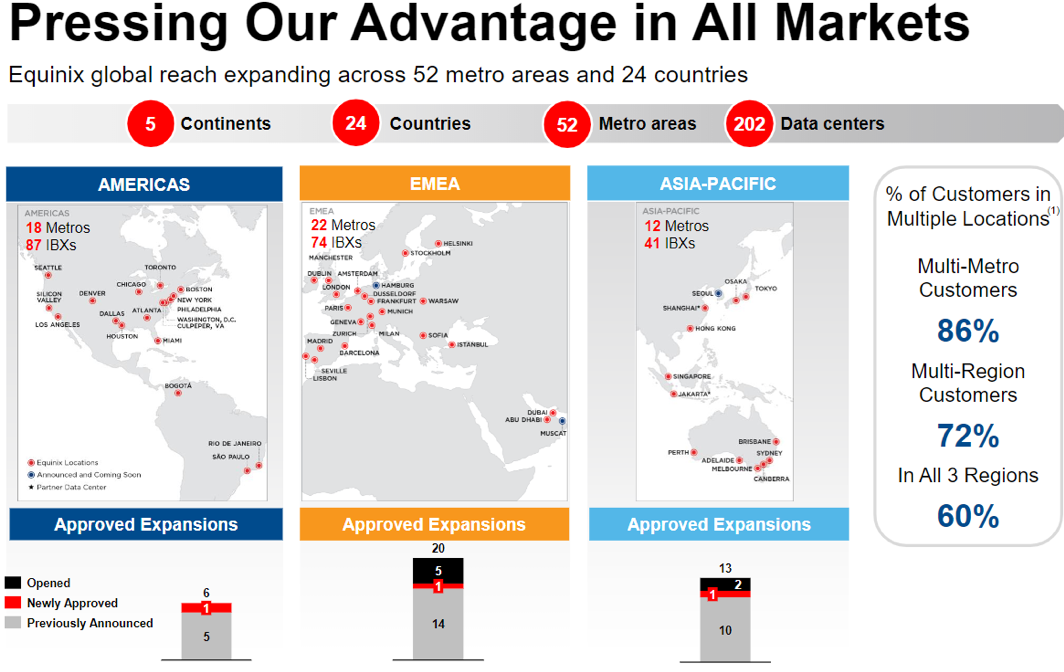

Equinix is now the market leader in 16 out of the 24 countries in which they operate, and they’re expanding its platform with 32 projects announced across 27 markets, with Q1 openings in Frankfurt, Hong Kong, London, Paris, and Shanghai.

Equinix’s network vertical experienced solid bookings led by strength in Access Point (AP), which is a hardware device or a computer's software that acts as a communication hub for users of a wireless device to connect to a wired LAN.

APs are important for providing heightened wireless security and for extending the physical range of service a wireless user has access to and driven by major telecommunication companies, mobile operators, and NSP resale.

Expansions this quarter include Hutchison, a leading British mobile network operator upgrading their infrastructure to support 5G and cloud services, as well as a leading Asian communication provider, migrating subsea cable notes and connecting to ECX Fabric for low latency.

Equinix’s financial services vertical experienced record bookings led by Europe, the Middle East and Africa (EMEA) and rapid growth in insurance and banking.

New contracts include a fortune 500 Global insurer transforming IT delivery with a cloud-first strategy, a top three auto insurer transforming network topology while securely connecting to multiple clouds, and one of the largest global payment and technology companies optimizing their corporate and commercial networks.

Demand in the social media sub-segment as providers are hellbent on improving user experience and expanding the scope of their business models.

Equinix’s gaming and e-commerce sub-segment grew the fastest year-over-year led by customers, including Tencent, neighbor, and roadblocks.

Cloud and IT verticals also captured strong bookings led by SaaS as the cloud diversifies towards a hybrid multi-cloud architecture.

A robust pipeline can be rejoiced around as cloud service providers continue to push to new frontiers and roll out additional services.

Developments include a leading SaaS provider expanding to support growth in new markets and with the Federal Government as well as an AI-powered commerce platform upgrading to enhance user experience support a rapidly growing customer base.

As digital transformation accelerates, the enterprise vertical continues to be Equinix’s sweet spot led by healthcare, legal and travel sub-segments this quarter and main catalysts to why I keep recommending reader into enterprise software companies.

The chips are being counted with new contracts from Air Canada, a top five North American airline deploying a hybrid multi-cloud strategy, Space X deploying infrastructure to interconnect dense network and partner ecosystems and one of the big four audit firms regenerating networks and interconnecting to multi-cloud to improve the user experience for both employees and clients.

Channel bookings also registered continued strength delivering over 20% of bookings with accelerated growth rates selling to Equinix’s key cloud players and technology alliance partners, including Cisco (CSCO), Google (GOOGL), Microsoft (MSFT), and Oracle (ORCL).

New channel wins this quarter includes a win with Anixter for a leading French transportation and freight logistics company deploying mobility platform, as well as a win with AT&T for a top-five U.S. Bank accessing our network and cloud provider.

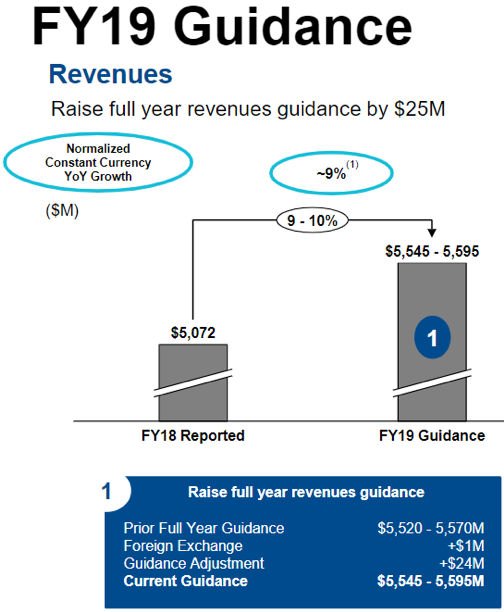

Management signaled to investors they are expecting a great year with full-year revenue guidance of $5.6B, a 9-10% year-over-year boost and a $25M revision from the previous guidance.

Equinix can boast 65 consecutive quarters of increasing revenues, which eclipses every other company in the S&P 500, and it anticipates 8%-10% in annual revenue growth through 2022.

This is an incredibly stable yet growing business and the 2.17% dividend yield, although not the highest, is another sign of a healthy balance sheet for a profitable company.

If you had any concerns about this stock, then just take a look at its 3-year EPS growth rate of 73% which should tell you that the massive operational scale of Equinix is starting to allow efficiencies to take hold dropping revenue straight down to the bottom line.

If you are searching for a company that cuts across every nook and cranny of the tech sector by taking advantage of the unifying demand and storage requirements of big data, then this is the perfect company for you.

This company will only become more vital once 5G goes online and being the global wizards of the data center will mean the stock goes higher in the long-term.

Mad Hedge Technology Letter

May 20, 2019

Fiat Lux

Featured Trade:

(THE BIG PLAY IN CISCO)

(CSCO), (JNPR), (ANET), (INTC), (GOOGL), (AMZN)

You can’t steal the mojo from the company that sells network software and infrastructure equipment.

Cisco (CSCO) is effectively an indirect bet on people using the internet because companies need the network infrastructure to offer all the cool and useful services that tech provides.

Technology and the services that result from it continues to be at the heart of customer strategy and now more than ever, Cisco’s market-leading portfolio and differentiated innovation are resonating with them as they transform their IT infrastructure.

Cisco is also a fabulous bet on 5G as the most recent technologies like cloud, AI, IoT, and WiFi 6 among others are developing together to revolutionize the way business operates and delivers new experiences for customers and teams.

Cisco is fundamentally changing the way customers approach their technology infrastructure to address the rising complexity in their IT environments.

They have constructed the only integrated multi-domain intent-based architecture with security at the foundation.

This is designed to allow customers to securely connect their users and devices over any network to any application.

Enterprise networks today must be optimized for agility and heightened security, leveraging cloud and wireless capabilities with the ability to extract insights from the data and security integrated throughout.

Cisco is in pole position to deliver this to customers.

Last quarter saw the launch of new platforms expanding the enterprise networking assets with the launch of subscription-based WiFi 6 access points and Catalyst 9600 campus core switches purpose-built for cloud-scale networking.

By combining automation and analytics software with a broad portfolio of switches, access points, and controllers, Cisco is creating a seamless end-to-end wireless first architecture.

With the newest Catalyst 9000 additions, Cisco has completed the most comprehensive enterprise networking portfolio upgrade in their history.

Cisco rebuilt their entire access portfolio with intent-based networking across wired and wireless.

Cisco also now have one unified operating system and policy management platform to drive simplicity and consistency across networks all enabled by a software subscription model.

In the data center, their strategy is to deliver multi-cloud architectures that bring policy and operational consistency no matter where applications or data resides by extending Application Centric Infrastructure (ACI) and offering HyperFlex to the cloud.

According to Cisco’s official website, its HyperFlex product is “a converged infrastructure system that integrates computing, networking and storage resources to increase efficiency and enable centralized management.”

Cisco’s partnerships with Amazon Web Services (AWS), Google Cloud, and Microsoft Azure are great examples of how they continue to work with web-scale providers to deliver new innovation.

Some new additions are Cisco’s cloud ACI for AWS, a service that allows customers to manage and secure applications running in a private data center or in Amazon Web Services cloud environments.

They also expanded agreements with Alphabet (GOOGL) by announcing support for their multi-cloud platform Anthos to help customers build secure applications everywhere from private data centers to public clouds with greater simplicity.

Going forward, Cisco will integrate this platform with its broad data center portfolio, including HyperFlex, ACI, SD-WAN, and Stealthwatch cloud to deliver the best multi-cloud experience.

Organic growth has surpassed 4% for five straight quarters and expanded margins and positive guidance for the current quarter will reaccelerate PE multiples, increasing as more investors buy into the strong narrative.

CEO of Cisco CEO Chuck Robbins boasted on the call that “we see very minimal impact at this point based on all the great work the teams have done, and it is absolutely baked into our guide going forward” when referring to the headwinds of the global trade war.

It’s been quite the new normal for chip firms to guide down for the rest of 2019, and Intel’s (INTC) worries are emblematic of the growing challenges facing the tech industry.

Cisco bucked the trend by issuing strong forward guidance of 4.5% to 6.5% revenue growth in its fiscal fourth quarter, and earnings of 80 cents to 82 cents per share.

In an in-house survey, Cisco found that 11% of respondents have upgraded networking infrastructure and 16% expect to do so in the next 12 months.

The “minimal impact” of the trade war indicates to investors that even with negative tech sentiment brooding around the world, Cisco’s best in class tech infrastructure still cannot be sacrificed and the migration of companies to digital directly benefits Cisco who provides the building blocks for software and hardware tech companies to develop around.

Cisco even felt bold enough to hike prices giving consternation to current customers.

Both Juniper (JNPR) and Arista (ANET), lower quality network infrastructure companies, have indicated their enterprise businesses are growing faster than the overall market and Cisco’s price hike was probably a bad time to up margins in the current frosty climate.

Even more worrying is data that suggests a general Enterprise pause in spending at a minimum and could entrap the broader tech market as many capital expenditures could be put on hold in the late economic cycle.

Keep in mind that Cisco’s Catalyst 9000 line had an abnormally strong last fourth quarter due to brisk adoption accelerating meaning comps will be hard to beat in the next earnings report.

However, these are minor bumps on the road at a time when the major narrative is running smoothly and shows no signs of stopping.

Cisco shares will continue to rise if they continue to upgrade their products and back it up with their best of breed reputation that could spur more price hikes.

Investors should wait for dips to buy in this name until there are any signs of product quality erosion which I believe will not happen in 2019.

Mad Hedge Technology Letter

March 13, 2019

Fiat Lux

Featured Trade:

(NVIDIA STEPS UP ITS GAME),

(NVDA), (INTC), (MSFT), (ANET), (CSCO), (MCHP), (XLNX)

Nvidia (NVDA) was right to pull the trigger – that was my first reaction when I first learned that they had aggressively acquired Israeli chip company Mellanox for $6.9 billion.

The fight to seize these assets were fierce triggering a bidding war -American heavyweights Intel and Microsoft were also in the mix but lost out.

CEO of Nvidia Jensen Huang touted the importance of the deal by explaining that “the emergence of AI and data science as well as billions of simultaneous computer users, is fueling skyrocketing demand on the world's data centers."

Therefore, satisfying this demand will require holistic architectures that connect massive numbers of fast computing nodes over intelligent networking fabrics to form a giant datacenter-scale compute engine.

Mellanox and its capabilities cover all the bases for Nvidia and will nicely slot into its portfolio offering, an added bonus of cross-selling and upselling opportunities to existing clients.

The strategic motives behind the deal are plentiful with increased importance of connectivity and bandwidth enhancing Nvidia's ability to provide datacenter-scale computing across the full stack for next-generation high-performance computing and AI workloads.

The agreement is the result of the company's shift toward next-gen technology as adoption of cloud, AI, and robotics ramps up and Nvidia will be at the forefront of this massive migration.

As the fourth industrial revolution advances, Nvidia is best of breed of semiconductor companies and the imminent adoption of 5G will aid the likes of Microchip Technology (MCHP) and Xilinx (XLNX).

Technology is rapidly changing, and the data center is the segment that is accelerating at a faster clip than in previous years translating into de-emphasizing current revenues of gaming and autonomous on a relative growth basis.

These segments will be secondary to the addressable opportunity in data center and signing up Mellanox is a key strategic initiative to exploit this growth opportunity.

Missing the boat on this compelling opportunity could have dragged Nvidia into an existential crisis down the road as the missed opportunity costs of lucrative data center revenues would begin to bite, and with no quick fix on the horizon, Nvidia’s growth drivers would be potentially disarmed.

Investors need to remember that Nvidia derives half of its revenue from China and up until this point, gaming had been a huge tailwind to its total revenue, however, the Chinese communist party has identified gaming addiction in young adults as a national crisis and have been refusing to deliver new gaming licenses to gaming creators.

As the data center via the cloud begins its next ramp-up of insatiable demand, Nvidia was acutely aware they could not miss the boat and to grab a foot hole against larger player Intel.

Almost overpaying to have more skin in the game does not do justice to what the ramifications would have been if Intel or even Microsoft were able to hijack this deal.

The two-fold victory will in turn boost sales of Nvidia's data center products long term while depriving Intel of extending the lead in data center.

And after the lack of recent underperformance in the prior quarter, Nvidia needed a gamechanger to cauterize the blood flow.

Nvidia's total revenue plunged more than 24% YOY in Q4 of 2018, and shareholders have been looking for remedies, especially after the once mythical cryptocurrency business blew up and the company was stuck with a glut of inventory.

The purchase of Mellanox will help Nvidia start competing with other dominant players like Cisco Systems (CSCO) and Arista Networks (ANET).

Mellanox is one of a handful of firms selling hardware that connects devices in the data center through network cards, switches, and cables.

The deal still needs regulatory approval and could be a stumbling block if Chinese authorities drag this into the orbit of the trade war and make it a bullet point in negotiations.

The net result is positive to the overall business model, and this move will breathe oxygen into Nvidia’s long-term narrative with a flow of revenue set to come online once the 5,000 Mellanox employees are integrated into Nvidia’s levers of operation.

Shares should be the recipient of short-term strength and after getting smushed by a poor last quarter, there is substantial room to the upside.

A dip back to $150 would serve as a good entry point to strap on a short-term bullish trade in Nvidia shares.

Mad Hedge Technology Letter

February 25, 2019

Fiat Lux

Featured Trade:

(THE CLEANEST INTERNET PLAY OUT THERE),

(GDDY), (WIX), (CSCO),

Check out GoDaddy (GDDY).

It’s a general bet on more people using the internet.

This trade dovetails nicely with my broader thesis of the dramatic migration to digital.

Brick and mortar stores will have no choice but to create a unique website and one of the most prominent web hosting services is GoDaddy.

The Mad Hedge Technology Letter is even powered by its services.

Lately, I’ve been all about this digital migration mantra and we are in the early innings of this seminal trend.

I gave you Cisco (CSCO) as a hot pick which is a bet on an increase in enterprise software business.

This is more of a question of how fast than if or when.

Are you ready for 5G?

The technology is on the verge of rolling-out to select cities around the US, and it will juice of web usage simply because users can navigate around more in a smaller time window.

GoDaddy was established by fellow Marine Bob Parsons in Baltimore 22 years ago and before GoDaddy, Parsons sold off his financial software services company, Parsons Technology to Intuit for $65 million.

He then launched Jomax Technologies which later morphed into GoDaddy in 1999 when employees were collaborating to change the company name and someone jokingly shouted out, "How about Big Daddy?"

Sadly, when the company found out that domain name had already been registered, Parsons replied, "How about Go Daddy?" and that was that.

What do I like about GoDaddy’s financials?

Better than expected profitability.

EPS forecasts were beaten handily with the company posting 24 cents, almost a double of the forecasted 13 cents.

Estimates of $693.5 million for the top line were marginally beaten by $2.3 million.

The company gave positive all-important guidance indicating robust momentum.

The firm is expecting $3 billion in 2019 sales and that is after doing $2.23 billion of sales in 2017.

Management has kept sales growth strong with a 3-year sales growth rate of 19%.

Customer renewal strength and higher average revenue per user (ARPU) growth is resonating with investors, and fused with higher operating margin could propel this firm’s shares higher.

ARPU mushroomed to $148.00 up 7% YOY while total customers rose 7% bringing the total customer base to over 18.5 million.

In 2018, over 1 million new customers were lured into the ecosystem.

The reason for this successful rise in domestic ARPU is enhanced site and product experiences, interactions focused on details and conversational marketing.

In a tech climate where a good portion of company outlooks are tepid at best, GoDaddy didn’t mince its words offering a better than expected positive outlook.

The financials look solid but allow me to explain a little more about its core products.

Almost 35% of websites on the internet is already constructed using WordPress’s platform and GoDaddy is the biggest host of paid WordPress at the end of last year.

GoDaddy’s supported WordPress offering automates the entire process of operating a secure WordPress website making it easy to use and highly popular to its customer base.

The role GoCentral's, GoDaddy’s flagship DIY website building product, plays is expanding as its numerous features increase and efficient performance is a consistent highlight for the firm.

The journey started in 2017 when GoDaddy established this service as a simple website building tool.

Concrete foundations were set and this service was integrated across a myriad of relevant third-party platforms while boosting product functions that are seeing outsized growth.

Daily entrepreneurs can now produce robust websites and carry out syndicate marketing across the e-commerce landscape.

The tandem of WordPress and GoCentral are growing subscriptions more than 40% YOY.

North America and Canada are the main revenue drivers, but international business is a wide-open opportunity waiting for management to pick off whether that's Latin America, Asia, or even in the Middle East.

The strategy for Europe is extracting the capability and product portfolio of North America, whether it be conversational marketing or features like security, backup, malware scans, plug-ins, and proactively migrate it to Europe because the model in America is obviously working and using that model will be a great development point.

Mexico and Brazil possess great growth potential and Asia continues to be about customer adds because the willingness to pay is different.

Competitor Wix (WIX) lately announced a shift in strategy, removing Domain Connect, and some of the low-end products and saying that they're going to come after WordPress.

But Chief Executive Officer of GoDaddy Scott Wagner is not worried about this nascent threat and is sure that this is the case of GoDaddy is in control of its own destiny than Wix being a viable threat.

As long as the company reinvests in its offerings and maximizes the user experience, Wix has a long way to go to compete with WordPress and are substantially smaller than GoDaddy.

And as GoDaddy keeps working on offering great value propositions and expanding the ecosphere with integrated and high-quality software, the stock is bound to jump further.

The momentum is palpable with this website hosting service a top player in its industry.

Wait for a pullback to buy some shares.