Mad Hedge Technology Letter

February 19, 2019

Fiat Lux

Featured Trade:

(THE SAFE PLACE TO HIDE IN TECH),

(CSCO), (ORCL), (WDAY), (ZEN), (HUBS), (NOW), (PYPL), (VEEV), (TWLO)

Mad Hedge Technology Letter

February 19, 2019

Fiat Lux

Featured Trade:

(THE SAFE PLACE TO HIDE IN TECH),

(CSCO), (ORCL), (WDAY), (ZEN), (HUBS), (NOW), (PYPL), (VEEV), (TWLO)

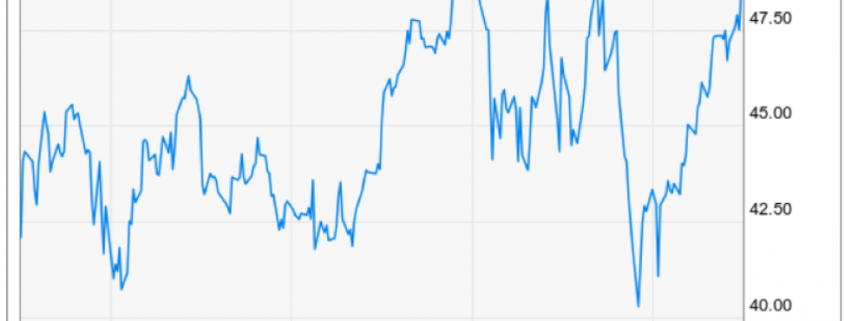

Great quarter by Cisco (CSCO).

That was the first thought in my head when perusing their quarterly earnings.

It’s been hit or miss for tech companies lately and at the end of 2018, I stood up and told readers to double down on software companies and specifically enterprise software companies.

Well, Cisco has skin in this software game because corporations cultivating software need the best type of network infrastructure money can buy.

Cisco is the foundational hardware on what current high-end software is built on.

It is all rosy to have a spectacular roof design, but without a solid foundation, we have nothing more than a house of cards.

The great part about Cisco is that they are immune to the software battle taking place inside of industries because they do not build the enterprise software that is built on top of the Cisco infrastructure.

We have seen our fair share of software companies go sideways such as Oracle (ORCL) who have presided over a stale patchwork of database system software created last gen.

However, on the other side of the coin, my prediction of enterprise software companies leading tech has been spot on.

Zendesk (ZEN), HubSpot (HUBS), ServiceNow (NOW), Workday (WDAY), PayPal (PYPL), Salesforce (CRM), Veeva Systems (VEEV), and Twilio (TWLO) are software companies that I was incredibly bullish on as we turned the calendar year and they have not disappointed with nearly all of these names flirting with all-time highs.

All these software companies need Cisco.

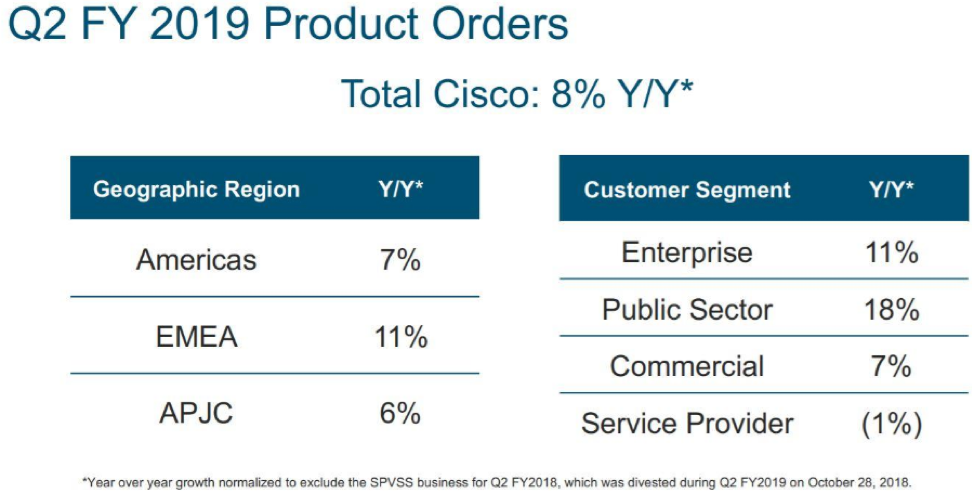

What stood out for me was that public sector orders grew 18% last quarter signaling that not only are the private corporations snapping up Cisco products, but governments are embedding their offices with Cisco’s Internet Protocol-based networking and other products related to the communications and information technology industry.

And if you wanted a general tech stock to capture the migration from analog commerce to digital and stay out of the high stakes online media segment, this would be the stable name that would check all the boxes.

And if you thought this was just a domestic story, once again, the scope is wider with Europe, the Middle East and Africa (EMEA) sales expanding by 11% which eclipsed America sales by 4%.

The only blip on the radar was service revenue slipping by 1% to $3.17 billion, but I do not view that as a pattern of sequential deceleration and pricing mechanisms can be altered to relaunch growth.

If you thought that Cisco doesn’t sell any software – you are wrong.

The software they do sell applies to operating the proprietary hardware that they produce.

Cisco’s wide competitive advantage stems from the industries toweringly high barriers of entry and that they make great products relative to other players.

The infrastructure software that liaises brilliantly with its hardware is succinctly named Cisco ONE Software.

This software suite is molded to face the most relevant use cases in the data center, WAN, and access edge.

CEO of Cisco Chuck Robbins characterized the current geopolitical and overall economic landscape as “complex” but experienced “zero difference” in Chinese revenue giving the company a quarterly victory in the Middle Kingdom.

China’s economy is decelerating faster than we can understand. The latest details of ride-hailing leader Didi sacking 2,000 employees is a warning flare to the rest that open wounds are appearing in the economy and are becoming harder to conceal.

And for Cisco to do a quarter with no significant Chinese downdraft is a good sign that the company can handle the upcoming recession in 2020.

As a sign of further strength, Cisco raised its dividend and boosted stock buybacks which are all the trappings of what great companies do.

Cisco already made $5 billion of repurchases last quarter which was on top of the $6 billion they bought in October 2018.

This method of financial engineering helps put a solid floor under the stock delighting investors and ignites the share price.

And the capital allocation encore means that Cisco will pile $15 billion into its buyback program with this fresh authorization, and the company is forecasted to produce at least $15 billion in free cash flow over the next year.

Cisco’s balance sheet is glistening and even has options to adventure into meaningful M&A if they see something that catches their eye without any real hit to the balance sheet.

These multiple tailwinds in a precarious economic point in the cycle have investors aware that there are worse options out there to invest capital than tech thoroughbred Cisco.

And if you thought the one variable that could turn this earnings report from good to bad was expenses and margins, well, Cisco covered their bases on that one too.

Margins came within the forecasted guidance with gross margins slightly trending down by 1% to 64.1%.

Expenses were reigned in and management saw a small nudge up of 3% causing investors to take a deep sigh of relief.

Cisco is in a superior strategic spot to most tech companies and is a staunch participant of the migration to digital.

Buy shares on the dip.

Global Market Comments

December 31, 2018

Fiat Lux

Featured Trade:

(WILL SYNBIO SAVE OR DESTROY THE WORLD?),

(XLV), (XPH), (XBI), (IMB), (GOOG), (AAPL), (CSCO), (BIIB)

Mad Hedge Technology Letter

September 12, 2018

Fiat Lux

Featured Trade:

(HOW TO PLAY “SOFTWARE AS A SERVICE”),

(AMZN), (IBM), (ADBE), (CRM), (BABA), (CSCO), (SAP), (ORCL), (GOOGL)

If you have read any of our content in the first year of the Mad Hedge Technology Letter, the content is distinctly bullish technology stocks.

A fundamental driver propelling this cogent argument is the dominant Software-as-a-Service (SaaS) industry booming inside the confines of Silicon Valley.

If you want to boil down your tech investment thesis to one indispensable rule – only invest in tech companies that carve out prominent SaaS businesses.

If you stick with this nostrum, you will be delivered profits in spades.

We have recently taken in a swarm of new tech letter subscribers and understanding the panacea that is SaaS will entrench your portfolio in a glorious position to reap untold profits.

What is SaaS?

SaaS is a distribution method in which software is diffused to paid subscribers, usually on an annual, reoccurring payment plan, and the software is remotely stored on a centralized cloud platform awaiting use.

Unsurprisingly, SaaS remains the most lucrative segment of the cloud market.

In 2017, the tech industry did $60.2 billion in annual SaaS sales, that number is poised to explode to $117.1 billion in 2021.

The near doubling of sales underscores the robust nature of these tech firms setting up businesses of this ilk, and the positive effects dripping down to the bottom line.

Simply put, no SaaS business, no reason to invest.

SaaS isn’t the only cloud revenue companies can carve out. Tech firms also offer platform-as-a-service (PaaS) and infrastructure-as-a-service (IaaS).

However, SaaS is by far the prominent growth lever in the high-margin cloud industry.

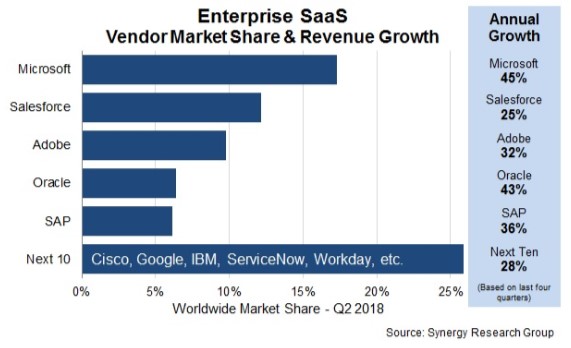

The indomitable presence inside the SaaS industry is Bill Gates’ creation Microsoft (MSFT).

Microsoft leads all companies with a 17% global share of the SaaS market.

The Redmond, Washington, outfit blew past stalwart Salesforce (CRM) nine quarters ago.

Microsoft’s sizzling SaaS business is an oversized contributor to its 45% revenue growth rate, which is head-and-shoulders above the industry average.

Salesforce (CRM), Adobe (ADBE), Oracle (ORCL) and SAP (SAP) fill out the top five largest global SaaS businesses, but it is really a tale of two stories.

Oracle and SAP, which are competing in the same market, are grappling with legacy database businesses and legacy tech, which are punished by investors.

John Dinsdale, a chief analyst at Synergy Research Group, mentioned two outliers of “Cisco (CSCO) and Google too who are making ever-bigger inroads into the SaaS market” leveraging Cisco’s multitude of software assets and Google’s G Suite.

The thing that makes SaaS the x-factor for tech companies is that inevitably every company from every walk of life will adopt this mode of software, giving legs to this distribution model.

Vendors are scrambling to put together some resemblance of a SaaS product together, and this trend is a vital contributor to an industry that is growing 32% YOY worldwide.

Kevin Cochrane, chief marketing officer of SAP Customer Experience lay bare his thoughts about this type of service describing it as the “Golden Age of SaaS.”

Companies are becoming digital first from end to end, explaining the sharp rise in IT professional salaries and rise in quality software products.

As we look around the corner to the IaaS part of the cloud industry, which is growing at around 30% YOY, there is one dominant player, and everybody knows its name.

Amazon (AMZN) is the No. 1 vendor with Microsoft, Alibaba (BABA), Google, and International Business Machines Corporation (IBM) trailing behind.

The top four IaaS players have carved out a total of 73% of the global market ravaging any resemblance of competition.

Amazon is the industry standard with the best record of customer success.

If Amazon branched off into the SaaS industry, it could unlock an additional $100 billion in annual revenue.

A shift into this direction could pad Amazon’s margin’s even more after successfully boosting North American e-commerce margins from 2.4% to 4.7%.

It’s not entirely inconceivable that Amazon could break the $2 trillion valuation in three to five years, as its revved up digital ad business registered growth of 129% YOY last quarter.

Microsoft seized the runner-up position in the IaaS market to Amazon by growing 98% YOY with sales eclipsing $3.1 billion in 2017.

Wherever you turn, whether toward the cloud business or gaming, investors can find Microsoft making sales.

Microsoft has been a favorite of the Mad Hedge Technology Letter and it’s hard pressed to find a better public tech company in operation now.

The SaaS industry is not a one-size-fits-all proposition.

Thus, there is abundant room for niche offerings that quench companies’ demand for specific services.

This is the reason why cloud companies have participated in a non-stop buying binge of smaller companies that fit their needs.

Microsoft purchased developer favorite GitHub for $7.5 billion earlier this year, and similar examples are scattered all over the tech ecosphere.

Artificial Intelligence (AI) will be the kicker that powers SaaS performance to new heights because incorporating this groundbreaking technology will enhance functionality and, in return, raise profits for all involved.

The scalability of SaaS products has allowed companies to offer software for affordable prices allowing the smallest of firms to adopt a digital-first strategy.

This software connects with other software seamlessly integrating an array of productive apps that help teams overperform and overdeliver.

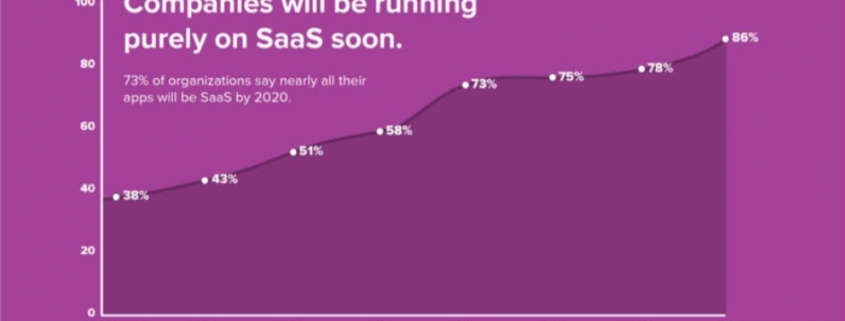

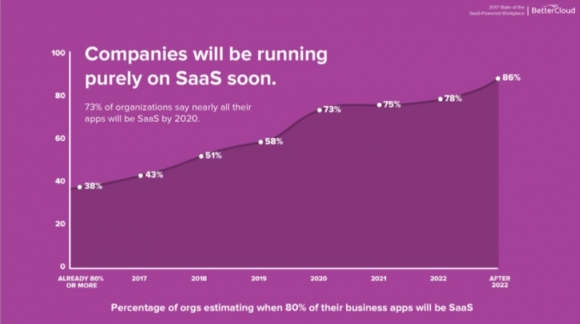

In the American workplace, 73% of companies will be exclusively using SaaS to function by 2020.

American companies are using 16 apps on average per day, a 33% jump in the number of apps they were using just two years ago.

The migration to mobile has swallowed up SaaS products as well with more mobile-specific software rolling out to mobile devices.

The meteoric rise of SaaS offerings has cut IT security budgets substantially as security has been delegated to the cloud instead of in expensive in-house security teams.

No longer do tech firms need to beef up guarding their own gates.

Protection is provided on a centralized cloud with a third-party company ensuring safety.

This development has helped a new industry rise – cloud security.

Whether people realize it or not, the SaaS industry is here to stay and will become more prevalent in every industry going forward.

This is incredibly bullish for companies that sell SaaS products as revenue will continue to rise.

________________________________________________________________________________________________

Quote of the Day

“Growth and comfort do not coexist,” – said CEO of IBM Ginni Rometty.

Mad Hedge Technology Letter

July 20, 2018

Fiat Lux

Featured Trade:

(A SELLERS' MARKET)

(CSCO), (MSCC), (GOOGL), (MCHP), (SWKS), (JNPR), (AMAT),

(PANW), (UBER), (AMZN), (AVGO), (QCOM), (CA), (CRM)

I bet you are wondering where all that money from the tax cuts is going.

Believe it or not, the No. 1 destination of this new windfall is technology companies, not just the stocks, but entire companies.

In fact, the takeover boom in Silicon Valley has already started, and it is rapidly accelerating.

The only logical conclusion in 2018 is that tech firms are about to get a lot more expensive. I'll explain exactly why.

The corporate cash glut is pushing up prices for unrealized M&A activity in 2018. U.S. firms accumulated an overseas treasure trove of around $2.6 trillion and the capital is spilling back into the States with a herd-type mentality.

I have chewed the fat with many CEOs about their cash pile road map. All mirrored each other to a T: strategic acquisition and share buybacks, period. The acquisition effect will be felt through all channels of the tech arterial system in 2018.

As the global race to acquire the best next generation technology heats up, domestic mergers could pierce the 400-deal threshold after a lukewarm 2017.

Spend or die.

Apple alone boomeranged back more than $250 billion with hopes of selective mergers and share buybacks. Cisco (CSCO), Microsoft (MSFT), and Google (GOOGL) were also in the running for most cash repatriated.

The tech behemoths are eager to make transformative injections into security, big data, semiconductor chips, and SaaS (service as a software) among others.

Hint: You want to own stocks in all of these areas.

Even non-traditional tech companies are getting in on the act with Walmart concentrating the heart of its strategic future on the pivot to technology.

Walk into your nearest Walmart every few months.

You'll notice major changes and not for decorative measures.

U-turns from legacy technology firms hawking desktop computers and HDD's (Hard Disk Drive) suddenly realize they are behind the eight ball.

M&A activity will naturally tilt toward firms dabbling in earlier-stage software and 5G supported technology. This flourishing trend will reshape autonomous vehicles and IoT (Internet of Things) products.

The dilemma in waiting to splash on a potential new expansion initiative is that the premium grows with the passage of time. Time is money.

It's a sellers' market and the sellers know this wholeheartedly.

Unleashing the M&A beast comes amid a seismic shift of rapid consolidation in the semiconductor sector. Cut costs to compete now or get crushed under the weight of other rivals that do. Ruthless rules of the game cause ruthless executive decisions.

The best way to cut costs is with immense scale to offer nice shortcuts in the cost structure. Buying another company and using each other's dynamism to find a cheaper way to operate is what Microchip Technology's (MCHP) culling of Microsemi Corporation (MSCC) in a deal worth $10bn was about.

Microsemi, based in Aliso Viejo, California, focuses on manufacturing chips for aerospace, military, and communications equipment.

Microchip's focal point is industrial, automobile and IoT products.

Included in the party bag is a built-in $1.8 billion annual revenue stream and more than $300 million of dynamic synergies set to take effect within three years. The bonus from this package is the ability to cross-sell chips into unique end markets opposed to selling from scratch.

Each business hyper-targets different segments of the chip industry and is highly complementary.

Benefits of a relatively robust credit market create an environment ripe for mergers. Some 57% of tech management questioned intend to go on the prowl for marquee pieces to add to their arsenal.

Then we have chip company Broadcom (AVGO) led by CEO Hock Tan, whose entire strategy is based on M&A and minimal capital spending.

His low-quality strategy of buying market share will ultimately fritter out. His lack of capital spending was also a salient reason for blocking Broadcom's purchase of Qualcomm (QCOM), which if stripped of its capital spending budget would have fallen behind China's Huawei to develop critical 5G infrastructure.

Tan's strategy flies in the face of the most powerful tech companies that are using M&A to enhance their products expanding their halo effect around the world.

Gutting innovation and skimming profits off the top is an entirely self-serving, myopic strategy to the detriment of long-term shareholders.

Investors punished Broadcom for it's latest investment of CA Technologies (CA) for $18.9 billion, even though this pickup signals a different tack.

CA Technologies is a leading provider of information technology (IT) management software, which suggests a belated move into the enterprise software market dominated by incumbents such as Salesforce (CRM).

Better late than never.

No need to mince words here as 2018 won't see any discounts of any sort. Nimble buyers should prepare for price wars as the new normal.

Not only are the plain vanilla big cap tech firms dicing up ways to enter new markets, alternative funds are looking to splash the cash, too.

Sovereign wealth funds and private equity firms are ambitiously circling around like vultures above waiting for the prey to show itself.

Private equity firms dove head first into the M&A circus already tripling output for tech firms.

Highlighting the synchronized show of force is none other than Travis Kalanick, the infamous founder of Uber. He christened his own venture capital fund that hopes to invest in e-commerce, real estate, and companies located in China and India.

The new fund is called 10100 and is backed by his own money. All this is possible because of SoftBank CEO Masayoshi Son's investment in Uber, which netted Kalanick a cool $1.4 billion representing Kalanick's 30% stake in Uber.

It is undeniable that valuations are exorbitant, but all data and chip related companies are selling for huge premiums. The premium will only increase as the applications of 5G, A.I., autonomous cars start to pervade deeper into the mainstream economy.

Adding fuel to the fire is the corporate tax cut. The lower tax rate will rotate more cash into M&A instead of Washington's tax coffers enhancing the ability for companies to stump up for a higher bill. Sellers know firms are bloated with cash and position themselves accordingly.

Highlighting the challenges buyers face in a sellers' market is Microsemi Corp.'s (MSCC) purchase of PMC-Sierra Inc. Even though PMC-Sierra had been looking to get in bed with Skyworks Solutions Inc. (SWKS) just before the MSCC merger, PMC-Sierra reneged on the acquisition after (SWKS) refused to bump up its original offer.

(SWKS) manufactures radio frequency semiconductors facilitating communication among smartphones, tablets and wireless networks found in iPhones and iPads.

(SWKS) is a prime takeover target for Apple. (SWKS) estimates to have the highest EPS growth over the next three to five years for companies not already participating in M&A. Apple (AAPL) could briskly mold this piece into its supply chain. Directly manufacturing chips would be a huge boon for Apple in a chip market in short supply.

In 2013, Japan's Tokyo Electron and Applied Materials (AMAT) angled to become one company called Eteris. This maneuver would have created the world's largest supplier of semiconductor processing equipment.

After two years of regulatory review, the merger was in violation of anti-trust concerns according to the United States. (AMAT), headquartered in Santa Clara, California, is a premium target as equipment is critical to manufacturing semiconductor chips. (AMAT) competes directly with Lam Research (LRCX), which is an absolute gem of a company.

Juniper Networks (JNPR) sells the third-most routers and switches used by ISP's (Internet Service Providers). It is also No. 2 in core routers with a 25% market share. Additionally, (JNPR) has a 24.8% market share of the firewall market.

In 2014, Palo Alto Networks (PANW), another takeover target focusing on cybersecurity, paid a $175 million settlement fee for allegedly infringing (JNPR)'s application firewall patents.

In data center security applications, (JNPR) routinely plays second fiddle to Cisco Systems (CSCO). Cisco, the best of breed in this space would benefit by snapping up (JNPR) and integrating its expertise into an expanding network.

Unsurprisingly, health care is the other sector experiencing a tidal wave of M&A, and it's not shocking that health care firms accumulated cash hoards abroad too. The dots are all starting to connect.

Firms want to partner with innovative companies. Companies hope to focus on customer demands and build a great user experience that will lead the economy. Health care costs are outrageous in America, and Jeff Bezos could flip this industry on its head.

Amazon (AMZN) pursuing lower health costs ultimately will bind these two industries together at the hip and is net positive for the American consumer.

Ride-sharing company Uber embarked on a new digital application called Uber Health that book patients who are medically unfit for regular Uber and shuttle them around to hospital facilities.

Health care providers can hail a ride for sick people immediately and are able to make an appointment 30 days in advance. It is a little difficult to move around in a wheel chair, and tech solves problems that stir up zero appetite for most business ventures. Apple is another large cap tech titan keeping close tabs on the health care space.

It's a two-way street with health care companies looking to snap up exceptional tech and vice versa.

It's practically a game of musical chairs.

Ultimately, Tech M&A is the catch of the day, and boosting earnings requires cutting-edge technology no matter how expensive it is. Investors will be kicking themselves for waiting too long. Buy now while you can.

Yes, It's All Going Into Tech Stocks

________________________________________________________________________________________________

Quote of the Day

"Companies in every industry need to assume that a software revolution is coming," - said American venture capitalist Marc Andreessen.

Mad Hedge Technology Letter

June 8, 2018

Fiat Lux

Featured Trade:

(WILL SYNBIO SAVE OR DESTROY THE WORLD?),

(XLV), (XPH), (XBI), (MON), (IBM), (GOOG), (AAPL), (CSCO)

Global Market Comments

May 4, 2018

Fiat Lux

Featured Trade:

(DON'T MISS THE MAY 9 GLOBAL STRATEGY WEBINAR),

(A DAY IN THE LIFE OF THE MAD HEDGE FUND TRADER),

(SPY), (TLT), (TBT), (FXE),(GLD), (GDX), (USO),

(AMLP), (STBX), (NFLX), (DIS), (AAPL), (GM)

Global Market Comments

May 3, 2018

Fiat Lux

Featured Trade:

(STORAGE WARS),

(MSFT), (IBM), (CSCO), (SWCH),

(DON'T BE SHORT CHINA HERE),

($SSEC), (FXI), (CYB), (CHL), (BIDU),