Mad Hedge Biotech and Healthcare Letter

May 20, 2025

Fiat Lux

Featured Trade:

(HEALTHCARE’S FALLING KNIFE)

(UNH), (CI), (CVS), (LLY), (VRTX), (SGRY), (AAPL), (AMZN)

Mad Hedge Biotech and Healthcare Letter

May 20, 2025

Fiat Lux

Featured Trade:

(HEALTHCARE’S FALLING KNIFE)

(UNH), (CI), (CVS), (LLY), (VRTX), (SGRY), (AAPL), (AMZN)

Mad Hedge Biotech and Healthcare Letter

December 24, 2024

Fiat Lux

Featured Trade:

(THE LAB RESULTS ARE IN)

(GILD), (TSLA), (WVE), (EDIT), (CRSP), (LLY), (NVO), (WMT), (CVS), (CCCC), (RHHBY)

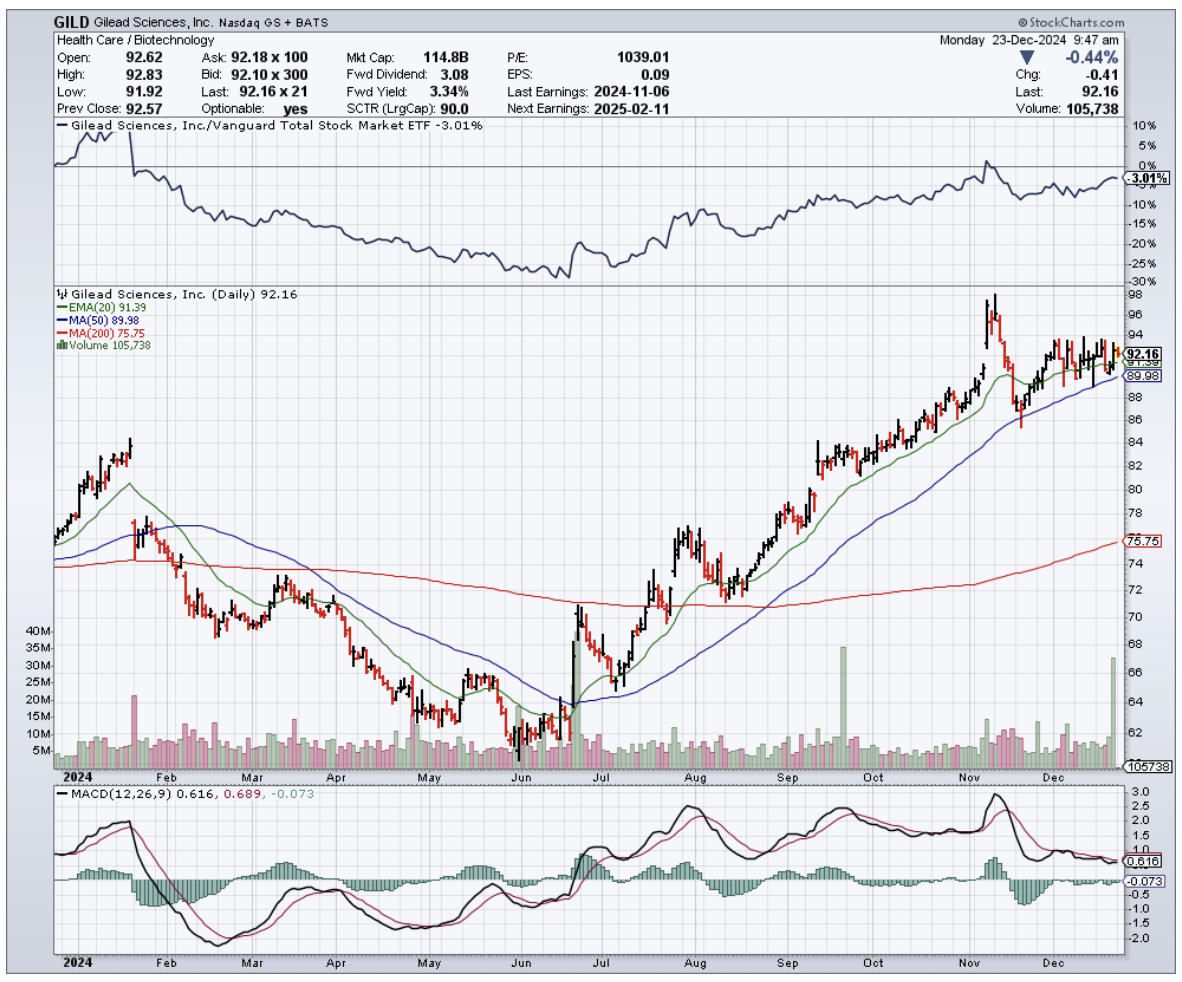

I found myself gridlocked in Bay Area traffic a few days ago, inching past Gilead's (GILD) sprawling Foster City headquarters, when my phone lit up with a call from an old friend at Goldman.

“Alright, tell me—what’s the real story with biotech this year?” she asked, her tone hovering somewhere between curiosity and exasperation. “Half my portfolio feels like a masterstroke, the other half... well, let’s just say it’s testing my patience.”

As I watched a Tesla (TSLA) weave through traffic like it was auditioning for a Fast & Furious reboot, I smiled.

Biotech has always been a bit of a high-stakes chess game—brilliance in one corner, chaos in another, and always a few surprises lurking behind the next move.

“Let me break it down for you,” I said, steering the conversation as carefully as I did my car through the bumper-to-bumper maze.

First, the winners are crushing it, and I mean crushing it. Gilead (GILD) finally cracked the code on HIV treatment, developing what's essentially a vaccine that doesn't require popping pills like they're Tic Tacs.

My contacts in clinical development tell me the Phase 3 data in cisgender women is nothing short of spectacular. With a $6 billion annual market potential by 2028, this isn't just another incremental advance - it's the kind of breakthrough that makes everyone in biotech salivate.

Then there's Wave Life Sciences (WVE) and their RNA editing technology. Remember when we thought CRISPR was the only game in town? Well, Wave just showed us there's more than one way to edit a gene.

Their liver-targeting therapy is the first successful RNA editing in humans - think of it as spell-check for your DNA, but reversible. The market's currently at $1.1 billion, but with 35% CAGR through 2030, this train is just leaving the station.

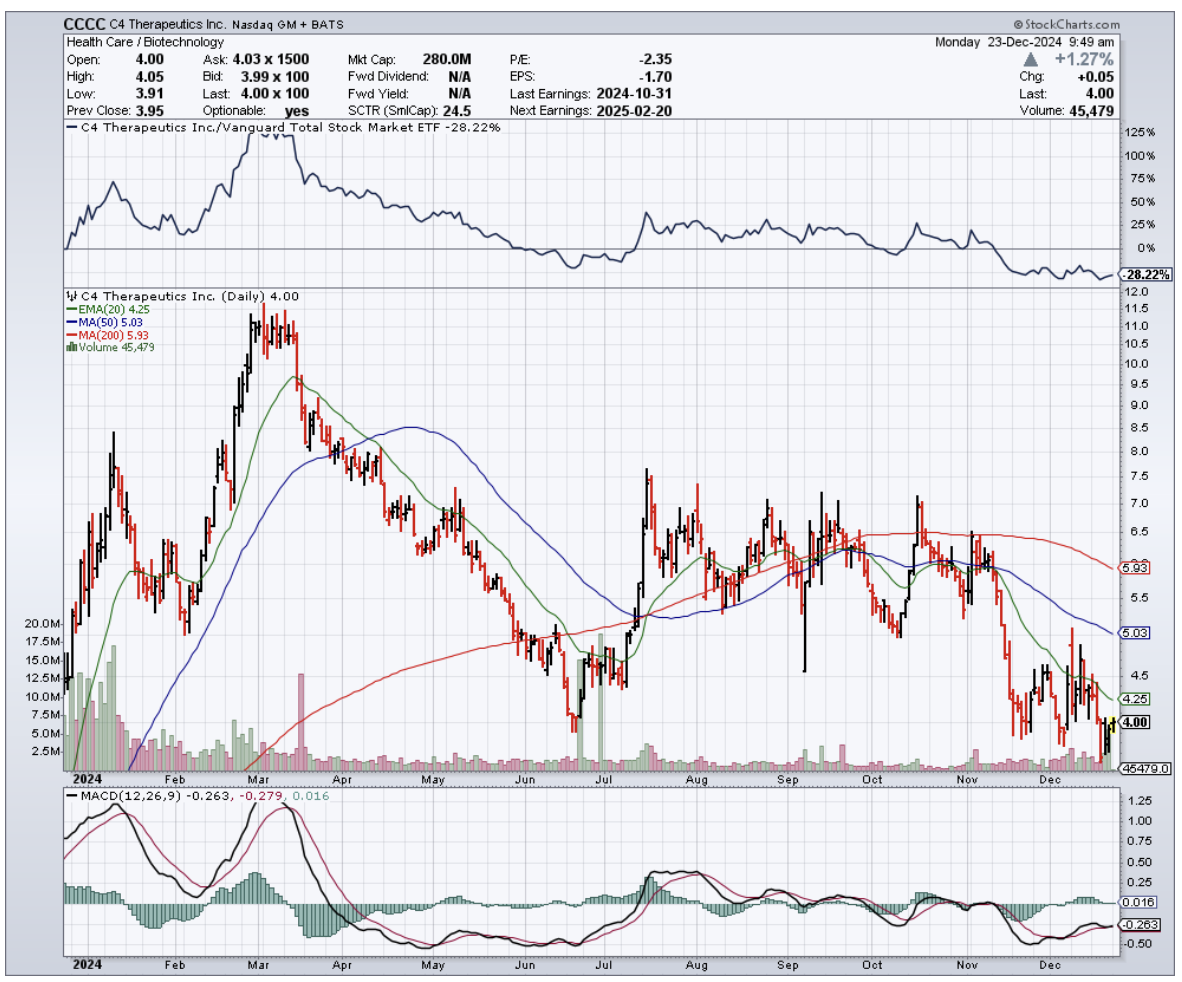

Speaking of trains leaving stations, molecular glue developers like C4 Therapeutics (CCCC) are watching Big Pharma back up the Brink's truck.

We're talking $8 billion in licensing deals this year alone. After all, when Roche (RHHBY) drops $300 million upfront - not milestone payments, mind you, but cold hard cash - you know they've seen something special in the data room.

But here's where it gets interesting, and I had to pull over at this point in the conversation because my friend wasn't going to like what came next.

CRISPR stocks? Down 20%. Editas (EDIT) and CRISPR Therapeutics (CRSP) are learning that revolutionary science doesn't always translate to revolutionary returns.

My friend Janet at the Fed might be talking about higher rates, but these companies are bleeding cash faster than a Silicon Valley startup's WeWork budget.

The obesity market? Unless your name is Eli Lilly (LLY) or Novo Nordisk (NVO), you're probably not having a great time.

Only three startups cleared $100 million in funding this year. In biotech terms, that's like trying to build a house with pocket change.

The global market's sitting at $4.1 billion, but it's more crowded than a San Francisco coffee shop during a tech conference.

And don't get me started on Walmart (WMT) and CVS (CVS) trying to play doctor. They thought they could disrupt traditional healthcare with their “get your physical next to the garden tools” model.

The result? A combined loss of $250 million and a wave of clinic closures.

The lesson here is clear: just because you can sell lightbulbs and Band-Aids in the same aisle doesn’t mean you should try to diagnose strep throat next to the automotive department.

A kid in a modded Subaru WRX cut me off as I wrapped up the call, but I left my friend with this: In biotech, timing is everything.

Gilead and Wave are showing us that patience pays off when the science is solid. Meanwhile, CRISPR stocks remind us that even the most promising technology needs good timing and deep pockets.

So, watch those clinical trial results like a hawk, and keep an eye on where the venture money's flowing.

But most importantly, remember what my old mentor used to say: "In biotech, you're not just betting on the science - you're betting on the scientist, the CFO, and sometimes, just sometimes, on whether people are ready to get their flu shot next to the garden center."

Now, where's that highway patrol when you need them?

Mad Hedge Biotech and Healthcare Letter

December 10, 2024

Fiat Lux

Featured Trade:

(THE INSURANCE COMPANY ALWAYS RINGS TWICE)

(UNH), (CI), (CVS), (HUM), (AMGN), (BIIB), (GILD)

Got an interesting call yesterday from an old college buddy - let's call him Bob. We go way back to our UCLA days, before I headed to Tokyo and he went into tech.

He was fuming because UnitedHealth (UNH) just denied his family's third claim this year, something about an "experimental treatment" for his daughter's rare condition.

Coming from a guy who just cashed out of his third startup, hearing him rant about insurance bureaucracy was pretty rich.

Still, his situation got me thinking. After hanging up, I dug into what's really happening with insurance stocks, and the picture isn't pretty.

UnitedHealth Group, our nation's biggest health insurer, just had its worst week in years - dropping 9.5% after one of their executives was tragically murdered, which sparked an unexpected spotlight on their claims practices.

Cigna (CI) and CVS Health (CVS) caught the same downdraft, falling 4.5% and 5% respectively.

But here's what really caught my attention: UnitedHealthcare's denial rate for Medicare Advantage claims has more than doubled since 2020, hitting 22.7% last year.

Interestingly, this spike happened right as they rolled out new automation processes. Funny how that works, isn't it?

Experian Health's latest report shows this isn't isolated - 73% of healthcare providers are reporting more denials than ever, with processing times stretching longer and longer.

The cost of this trend? The Council for Affordable Quality Healthcare estimates $31 billion annually in administrative expenses alone.

Meanwhile, biotech companies find themselves in an awkward position. They're developing treatments that cost more than a house in the Hamptons and then need these very same insurers to make them accessible.

Amgen's (AMGN) been crushing it with their human therapeutics portfolio, pulling in $28.2 billion in revenue last year.

Biogen's (BIIB) making serious moves in neurological treatments, though their path has been rockier - just ask anyone who followed the Aduhelm saga.

Gilead Sciences (GILD), our antiviral champions, have managed to stay above the fray, partly because their HIV and hepatitis treatments have become standard of care.

But even these giants must wonder:: as insurers tighten their prior authorization screws, what happens to patient access?

These biotechs spend billions developing breakthrough treatments - Amgen alone dropped $4.4 billion on R&D last year - only to face the insurance industry's equivalent of "computer says no."

The irony isn't lost on anyone: insurers need innovative treatments to justify their premiums, while biotech needs insurance coverage to justify their R&D spending.

It's a delicate dance that's worked reasonably well so far, but these rising denial rates have everyone on edge. Just last quarter, we saw several biotech earnings calls dominated by questions about insurance coverage rather than clinical trials.

So what should we do? Well, I say UnitedHealth and Cigna are "holds" right now - the current turbulence needs time to settle.

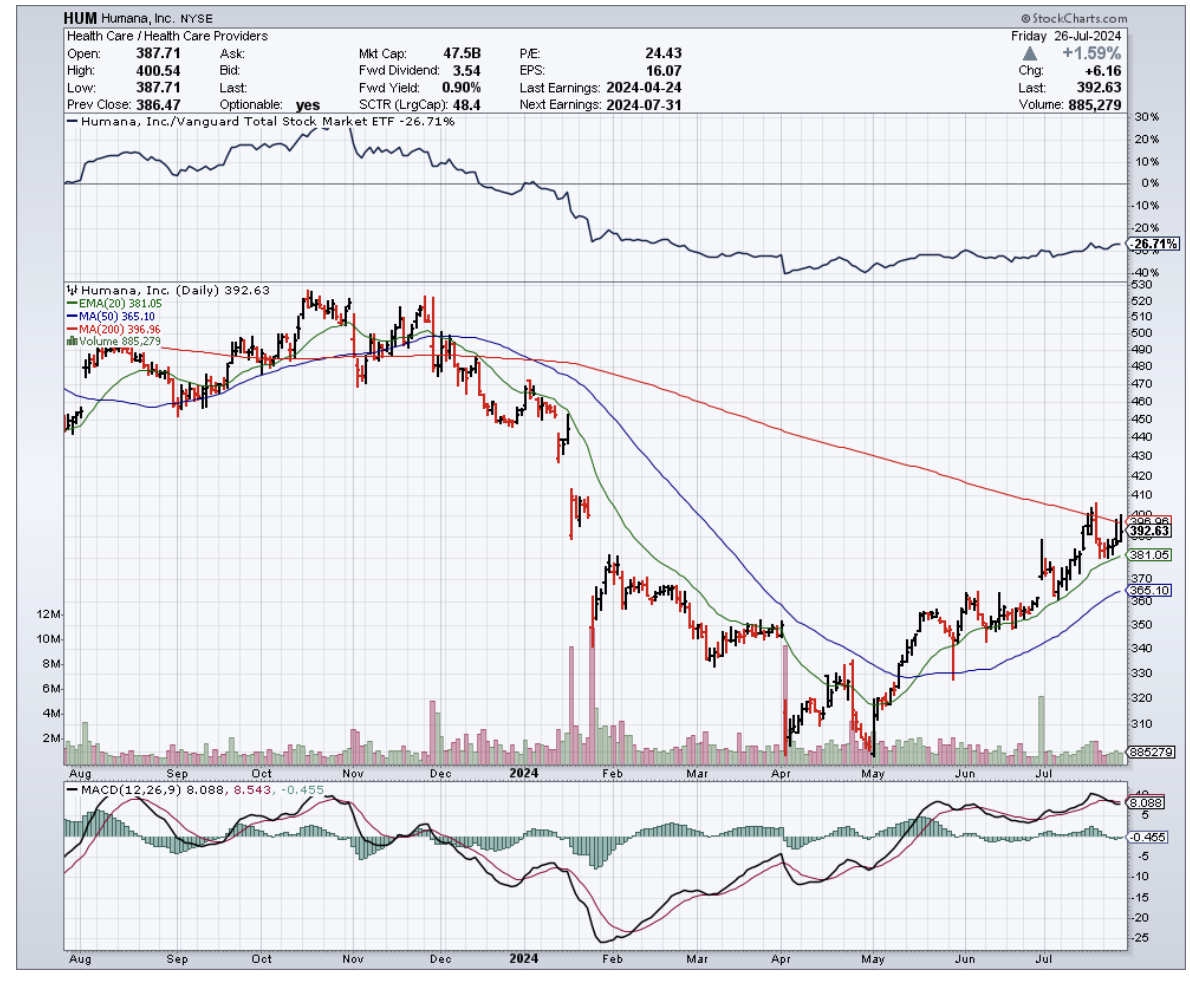

CVS Health is showing broader operational challenges that suggest it might be wise to consider selling. But Humana (HUM), with their strong Medicare Advantage presence, looks promising.

On the biotech side, Gilead looks like an excellent stock to buy on the dip. Its leadership in antivirals and solid pipeline make it compelling.

Amgen and Biogen? Keep them on your watch list while they try to find their footing in this situation.

Bob texted me again this morning - turns out he's filing an appeal with help from one of Silicon Valley's top healthcare attorneys. Typical Bob, bringing a cannon to a knife fight.

But maybe that's exactly what this sector needs right now - some heavy artillery to shake up the status quo.

For those willing to dodge the crossfire, there might just be some spoils of war worth picking up. After all, fortune favors the bold—and sometimes, the heavily armed.

Mad Hedge Biotech and Healthcare Letter

October 24, 2024

Fiat Lux

Featured Trade:

(A HEALTHCARE STOCK THAT OWNS TOMORROW)

(UNH), (HUM), (ELV), (CVS)

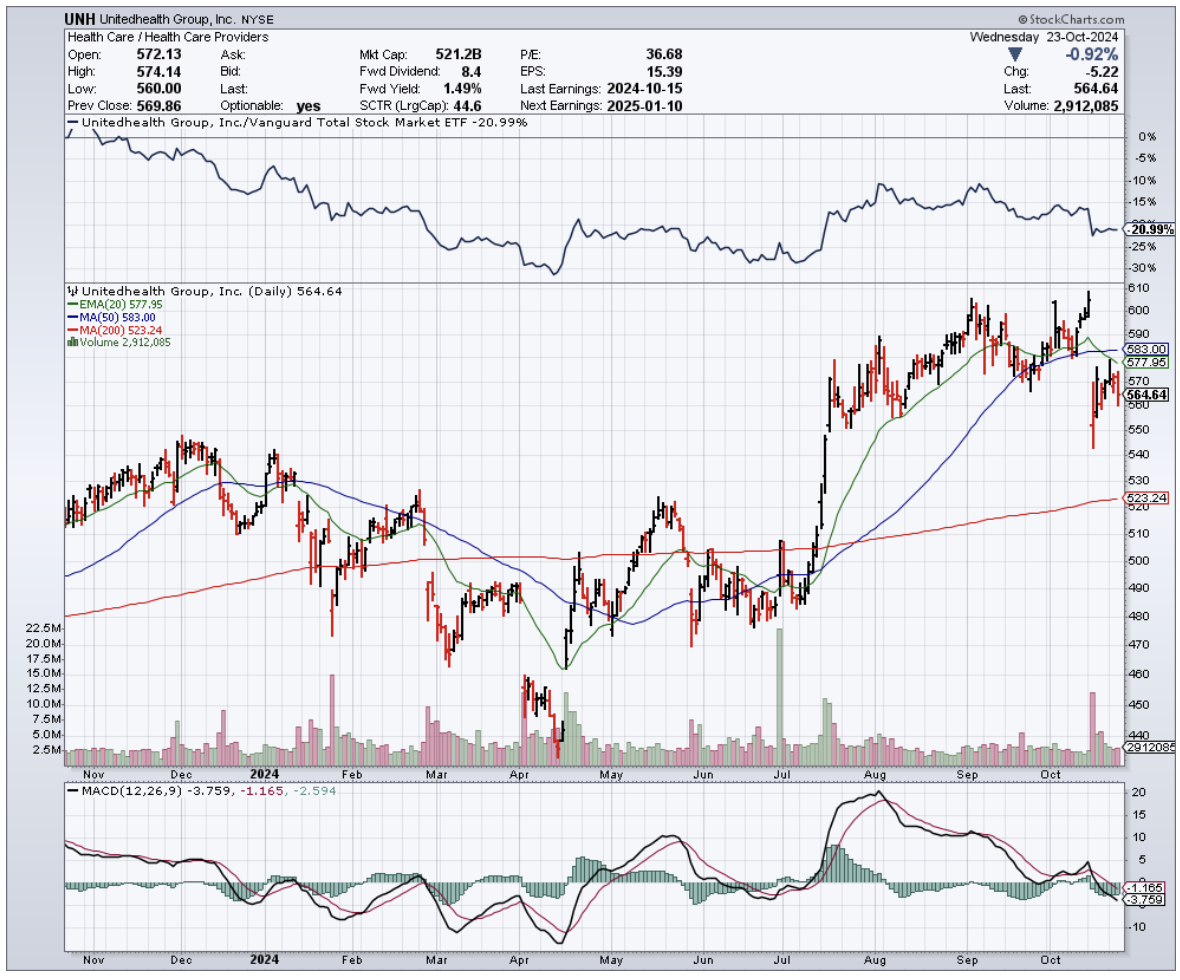

After decades of watching healthcare stocks, I've learned one immutable truth - demographics always win. And right now, demographics are handing UnitedHealth Group (UNH) the keys to the kingdom.

The numbers tell an impressive story. UnitedHealth just reported Q3 2024 revenue of $100.82 billion, up 9.2% year-over-year. That's a billion dollars above what Wall Street expected, even after weathering a nasty cyberattack on their Change Healthcare unit in February.

Let's put this in perspective. By 2031, America's national health expenditure will hit $7.17 trillion - more than the GDP of Japan and Germany combined. This isn't just another growth story.

Besides, having managed hedge fund money through multiple market cycles, I’d like to think that I know the difference between lucky timing and structural advantage. From the looks of how things are going, UnitedHealth has engineered themselves the latter.

The company's UnitedHealthcare segment tells only part of the story, bringing in $74.85 billion in Q3, up 7.2% from last year.

Their Medicare Advantage enrollment grew from 7.65 million to 7.81 million people, while their U.S. commercial health plans expanded from 27.25 million to 29.73 million members.

Yes, they took a hit on their global numbers after selling their Brazilian business - dropping from 5.48 million to 1.34 million customers. But sometimes the best deals are the ones you don't do.

The real story here is Optum and its aggressive push into value-based care.

While competitors are still figuring out how to merge technology with healthcare delivery, UnitedHealth has already built a fortress. Their $13 billion acquisition of Change Healthcare wasn't just about processing claims - it was about owning the healthcare data highway.

Optum's revenue jumped 12.5% to $63.79 billion, with their pharmacy division surging 18.5% to $34.21 billion. They processed 410 million prescriptions in Q3 alone - that's 30 million more than last year.

What Wall Street is missing is UnitedHealth's positioning for the post-COVID healthcare landscape. They're not just riding the telehealth wave - they're reshaping it.

Their OptumRx digital platform now handles 80% of all prescription transactions, while their virtual care visits have grown tenfold since 2019.

In fact, the regulatory environment plays into their hands.

While smaller players struggle with Medicare Advantage rate adjustments and value-based care requirements, UnitedHealth's scale and technology infrastructure turn these challenges into opportunities.

Their compliance systems and data analytics capabilities give them a moat that gets wider every quarter.

Wall Street expects Q4 revenue between $100.48 billion and $104.14 billion. Their P/S ratio of 1.41x looks rich compared to Humana (HUM) at 0.29x and Elevance Health (ELV) at 0.57x. But in this market, scale and execution command a premium.

Looking ahead, I see UnitedHealth hitting $552 billion in revenue by 2028. The catalysts are clear: aging demographics, rising chronic disease management post-COVID, and the unstoppable march toward value-based care.

Their Q3 non-GAAP EPS of $7.15 beat estimates by 12 cents. By 2028, I expect EPS to reach $44, with their P/E ratio dropping from 22.75x to 12.99x.

Their balance sheet remains rock solid - net debt/EBITDA ratio below 1.5x, with investment-grade ratings from S&P Global (SPGI), Fitch, and Moody's (MCO).

UnitedHealth also keeps growing its dividend by double digits, maintains a predictable business model, and outperforms competitors like CVS Health (CVS) and Humana on ROE.

Admittedly, they slightly lowered their 2024 adjusted EPS guidance, spooking some traders. But in my experience, Wall Street's short-term panic creates long-term opportunities.

So, what’s the play here? I suggest you build a position in UnitedHealth now while the stock has pulled back. Scale in gradually if you're concerned about timing, but don't miss this opportunity.

Remember, in the end, this isn't just about healthcare - it's about owning a piece of America's unstoppable demographic destiny. And that's a trend even a skeptic like me can believe in.

Mad Hedge Biotech and Healthcare Letter

July 30, 2024

Fiat Lux

Featured Trade:

(RETAIL THERAPY, MEET RETAIL RX)

(HUM), (WMT), (WBA), (UNH), (CVS), (TDOC)

In my years of covering the markets, from the trading floors of Tokyo to the halls of power in Washington, I've seen my fair share of unexpected partnerships.

But the recent tie-up between Walmart (WMT) and Humana (HUM) has me sitting up and paying attention.

That’s right. Walmart, the king of rollbacks and home of the $1 hot dog, has found a new tenant for the vacant spaces that used to house its healthcare business: Humana's CenterWell health clinics.

Humana, as you know, is one of the biggest players in the Medicare Advantage game, and is setting up shop in 23 Walmart Supercenters across Florida, Georgia, Missouri, and Texas.

And they're not just dipping their toes in the water – they're diving in headfirst, with plans to have these clinics up and running by the first half of 2025.

Now, I know what you're thinking. "John, why should I care about some dusty old retail giant like Walmart getting into bed with a health insurance company?"

Let me tell you why.

Humana's Q1 2024 earnings were nothing to sneeze at, with revenues growing 11% year-over-year to a whopping $29.6 billion.

And while the company did revise its full-year EPS guidance downward, it maintained its outlook for adjusted EPS and even revised its membership growth in MA plans upward.

This is a big deal, folks. Medicare Advantage plans have been the bread and butter of Humana's business model, underpinning the company's phenomenal share price gains from $25 per share in 2010 to over $550 in late 2022.

With the population aging faster than fine wine, the demand for senior-focused healthcare services will only grow.

But Humana isn't the only one benefiting from this partnership.

For Walmart, renting out these spaces to CenterWell allows them to recoup some of the infrastructure investments they made in building out their 51 Walmart Health clinics, which they recently shut down due to profitability challenges.

It's like finding a roommate to help pay the rent after your startup goes belly up.

But the healthcare industry is like a giant game of Jenga, with players constantly pulling out blocks and hoping the whole thing doesn't come crashing down.

Just look at Walgreens Boots Alliance (WBA), another retail giant that recently announced the closure of 150 of its in-store clinics due to profitability challenges. It's a stark reminder of how difficult it can be to make a buck in this business.

That's why Walmart's pivot to a partnership model with Humana is so intriguing.

By leasing out pre-equipped facilities to CenterWell, Walmart is essentially letting Humana handle the nitty-gritty of patient care while still maintaining a presence in the rapidly growing primary care industry.

It's like having your cake and eating it too, without having to worry about the pesky details of actually baking the cake.

As expected, Walmart and Humana aren't the only ones making moves in the healthcare space.

CVS Health (CVS) and UnitedHealth Group (UNH) are also betting big on primary care, with CVS acquiring Oak Street Health for $10.6 billion and UnitedHealth's Optum division going on an acquisition spree to expand its network of physicians and healthcare providers.

Then, there’s the meteoric rise of telehealth during the pandemic. Companies like Teladoc Health (TDOC) saw their revenues skyrocket as patients turned to virtual care in droves.

While growth has slowed down since the height of the pandemic, telehealth is still a force to be reckoned with and could potentially disrupt traditional brick-and-mortar clinics.

So, what does all this mean for us?

Well, if you're an investor looking to get in on the action, you've got plenty of options. From established players like Humana and UnitedHealth to up-and-comers like Oak Street Health and Teladoc, there's no shortage of companies vying for a piece of the healthcare pie.

With an aging population, rising healthcare costs, and a growing focus on preventative care and chronic disease management, the demand for innovative healthcare solutions is only going to increase in the coming years.

And who knows, maybe one day we'll all be getting our annual check-ups at the local Walmart, with a side of low-priced toilet paper and a jumbo bag of Cheetos.

Stranger things have happened in the wild world of healthcare.

Mad Hedge Biotech and Healthcare Letter

February 13, 2024

Fiat Lux

Featured Trade:

(PILL PUSHERS IN PERIL)

(CVS), (WBA), (RADCQ), (SBUX)