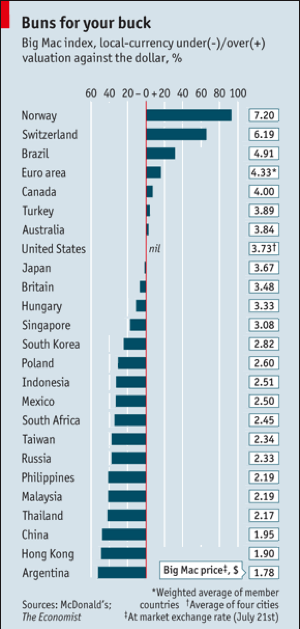

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its "Big Mac" index of international currency valuations.

Although initially launched as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald's (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai baht are cheap.

I couldn't agree more with many of these conclusions. It's as if the august weekly publication was tapping The Diary of a Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool than a speedy lunch.

The Big Mac in Yen is Definitely Not a Buy

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-07-05 02:04:412019-08-05 17:45:40Where The Economist "Big Mac" Index Finds Currency Value

Whatever the market is drinking right now, I’ll take some of that stuff. If you could bottle it and sell it, you’d be rich. Certainly, the Viagra business would go broke.

To see the Dow average only give up 7% in response to the worst trade war in a century is nothing less than stunning. To see it then make half of that back in the next four days is even more amazing. But then, that is the world we live in now.

When the stock market shrugs off the causes of the last great depression like it’s nothing, you have to reexamine the root causes of the bull market. It’s all about the Fed, the Fed, the Fed.

Our August central bank’s decision to cancel all interest rate rises for a year provided a major tailwind for share prices at the end of 2018. The ending of quantitative tightening six months early injected the steroids, some $50 billion in new cash for the economy per month.

We now have a free Fed put option on share prices. Even if we did enter another 4,500-point swan dive, most now believe that the Fed will counter with more interest rate cuts, thanks to extreme pressure from Washington. A high stock market is seen as crucial to winning the 2020 presidential election.

Furthermore, permabulls are poo-pooing the threat to the US economy the China (FXI) trade war presents. Some $500 billion in Chinese exports barely dent the $21.3 trillion US GDP. It’s not even a lot for China, amounting to 3.7% of their $13.4 trillion GDP, or so the argument goes.

Here’s the problem with that logic. The lack of a $5 part from China can ground the manufacture of $30 million aircraft when there are no domestic alternatives. Similarly, millions of small online businesses, mostly based in the Midwest, couldn’t survive a 25% price increase in the cost of their inventory.

As for the Chinese, while trade with us is only 3.7% of their economy, it most likely accounts for 90% of their profits. That’s why the Chinese yuan (CYB) has recently been in free fall in a desperate attempt to offset punitive tariffs with a substantially cheaper currency.

The market will figure out all of this eventually on a delayed basis and probably in a few months when slowing economic growth becomes undeniable. However, the answer for now is NOT YET!

Markets can be dumb, poor sighted, and mostly deaf animals. It takes them a while to see the obvious. One of the problems with seeing things before the rest of the world does, I can be early on trades, and that can translate into losing money. So, I have to be cautious here.

When that happens, I revert to an approach I call “Trading devoid of the thought process.” When prices are high, I sell. When they are low, I buy. All other information is noise. And I keep my size small and stop out of losers lightning fast. That’s how I managed to eke out a modest 0.63% profit so far this month, despite horrendous trading conditions.

You have to trade the market you have, not what it should be, or what you wish you had. It goes without saying that the Mad Hedge Market Timing Index become an incredibly valuable tool in such conditions.

It was a volatile week, to say the least.

China retaliated, raising tariffs on US goods, ratcheting up the trade war. US markets were crushed with the Dow average down 720 intraday and Chinese plays like Apple (AAPL) and Boeing (BA) especially hard hit.

China tariffs are to cost US households $500 each in rising import costs. Don’t point at me! I buy all American with my Tesla (TSLA).

The China tariffs delivered the largest tax increases in history, some $72 billion according to US Treasury figures. With Walmart (WMT) already issuing warnings on coming price hikes, we should sit up and take notice. It is a highly regressive tax hike, with the poorest hardest hit.

The Atlanta Fed already axed growth prospects for Q2, from 3.2% to 1.1%. This trade war is getting expensive. No wonder stocks have been in a swan dive.

US Retail Sales cratered in March while Industrial Production was off 0.5%. Why is the data suddenly turning recessionary? It isn’t even reflecting the escalated trade war yet.

European auto tariff delay boosted markets in one of the administration’s daily attempts to manipulate the stock market and guarantee support of Michigan, Wisconsin, and Pennsylvania during the next presidential election. All government decisions are now political all the time.

Weekly Jobless Claims plunged by 16,000 to 212,000. Have you noticed how dumb support staff have recently become? I have started asking workers how long they have been at their jobs and the average so far is three months. No one knows anything. This is what a full employment economy gets you.

Four oil tankers were attacked at the Saudi port of Fujairah, sending oil soaring. America’s “two war” strategy may be put to the test, with the US attacking Iran and North Korea simultaneously.

Bitcoin topped 8,000, on a massive “RISK OFF” trade, now double its December low. The cryptocurrency is clearly replacing gold as the fear trade.

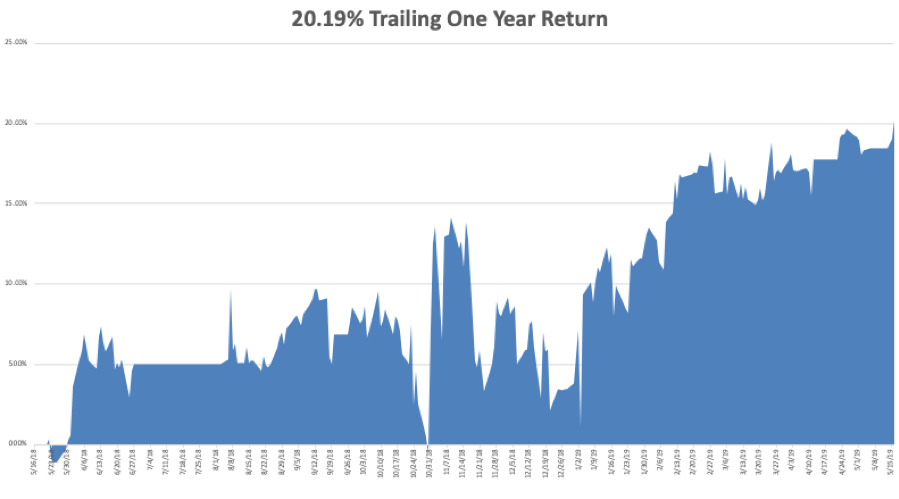

The Mad Hedge Fund Trader managed to blast through to a new all-time high last week.

Global Trading Dispatch closed the week up 16.35% year to date and is up 0.63% so far in May. My trailing one-year rose to +20.19%. We jumped in and out of short positions in bonds (TLT) for a small profit, and our tech positions appreciated.

The Mad Hedge Technology Letter did OK, making some good money with a long position in Intuit (INTU) but stopping out for a small loss in Alphabet (GOOGL).

Some 10 out of 13 Mad Hedge Technology Letter round trips have been profitable this year.

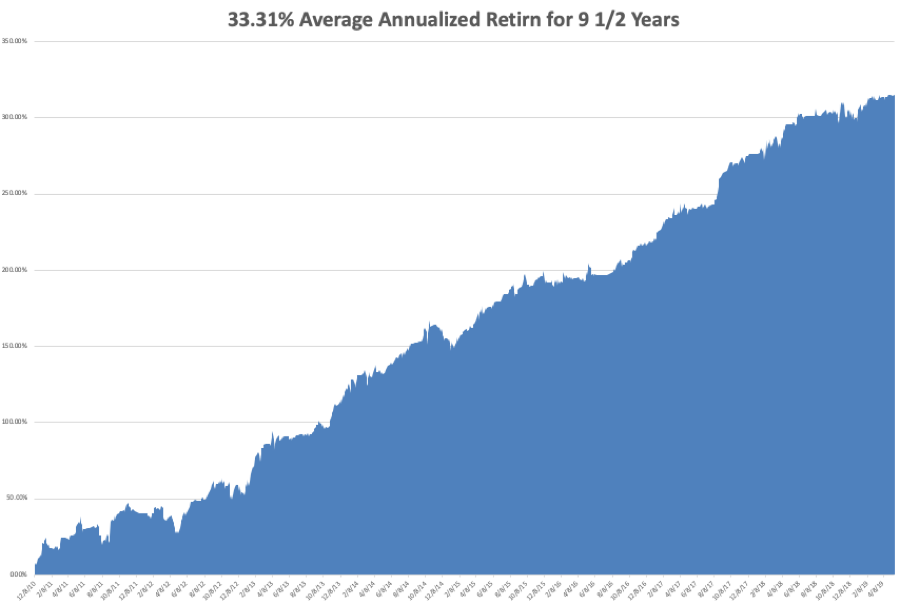

My nine and a half year profit jumped to +316.49%.The average annualized return popped to +33.21%. With the markets incredibly and dangerously volatile, I am now 80% in cash with Global Trading Dispatch and 80% cash in the Mad Hedge Tech Letter.

I’ll wait until the markets retest the bottom end of the recent range before considering another long position.

The coming week will see only one report of any real importance, the Fed Minutes on Wednesday afternoon. Q1 earnings are almost done.

On Monday, May 20 at 8:30 AM, the April Chicago Fed National Activity Index is out.

On Tuesday, May 21, 10:00 AM EST, the April Existing Home Sales is released. Home Depot (HD) announces earnings.

On Wednesday, May 22 at 2:00 PM, the minutes of the last FOMC Meeting are published. Lowes (LOW) announces earnings.

On Thursday, May 16 at 23 AM, Weekly Jobless Claims are published. Intuit (INTU) announces earnings.

On Friday, May 24 at 8:30 AM, April Durable Goods is announced.

As for me, I’ll be taking a carload of Boy Scouts to volunteer at the Oakland Food Bank to help distribute food to the poor and the homeless. Despite living in the richest and highest paid urban area in the world, some 20% of the population now lives on handouts, including many public employees and members of the military. It truly is a have, or have-not economy.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/05/john-thomas-3.png816612Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-20 02:02:272019-07-09 03:43:34The Market Outlook for the Week Ahead, or I’ll Take Some of That!

Featured Trade:

(DON'T MISS THE MAY 9 GLOBAL STRATEGY WEBINAR),

(A DAY IN THE LIFE OF THE MAD HEDGE FUND TRADER),

(SPY), (TLT), (TBT), (FXE),(GLD), (GDX), (USO),

(AMLP), (STBX), (NFLX), (DIS), (AAPL), (GM)

Everyone who has been reading this letter for the past decade (yes, there are quite a few of you), know that I am a fundamentalist first and a technician second.

Of course, you need to use both, as those who mistakenly leave one tool in the bag reliably underperform indexes.

The one-liner here is that I use fundamentals to identify broad, long-term, even epochal trends, and technicals for the short-term timing of my Trade Alerts.

Do both well, and you will prosper mightily.

Strategists often like to cloak themselves in the fundamental or technical mantels alone. But parse their words carefully, and the best fundamentalists talk about support and resistance levels, while the ace technicians refer to the latest economic data points.

The reality is that the best of the best are using both all the time. The differential titles have more to do with marketing purposes than anything else.

Having said all that, you better take a good, hard look at the chart below for the Shanghai Stock Exchange Composite Index ($SSEC). The 2016 low has held and the long-term uptrend lives.

My bet is that it resolves to the upside. All it would be doing then is coming in line with the rest of the global equity markets, including those of many emerging markets.

Since the last top, the earnings multiple of Chinese companies has plunged, from 35 times to a mere 15 times. This means that the 6.5% a year growing economy (China) is trading at a lower multiple than the 2.3% a year growing one (the U.S.). The big question among strategists since 2009 has been how far these valuations would diverge.

If I am right, then you can expect a rally of at least 25% in the Shanghai market soon, and more in peripheral markets, such as Hong Kong (EWH) and in single Chinese names. My bet is that it starts in August, when the current correction ends and we resume the year-end ramp-up.

You should place a laser-like focus on the Chinese Internet sector, so you won't go wrong picking up some Baidu (BIDU) around $180, if you can get it (click here for my original recommendation to buy the stock at $12 nine years ago).

If you are looking for further confirmation of the coming bull move in China across asset classes, please peruse the chart below for copper. The red metal has one of the closest correlations out there with the fate of the Middle Kingdom's economy and stock markets. It appears to be breaking out of a major five-year downtrend as well.

The other nice thing about this scenario is that it provides more fodder for my expectation of another global bull market move in the fall, when you can expect major indexes to tack on another 10% by year-end.

Jim Chanos, watch your back!

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Man-in-China-story-2-image-6.jpg225336MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-03 01:06:152018-05-03 01:06:15Don't Be Short China Here

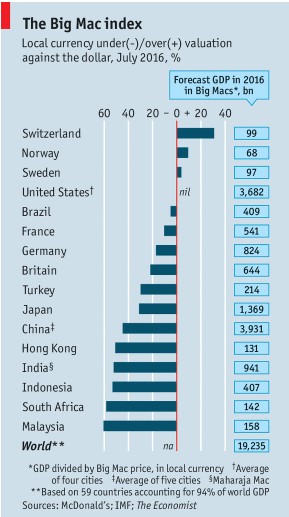

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its "Big Mac" index of international currency valuations.

Although initially launched as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald's (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai baht are cheap.

I couldn't agree more with many of these conclusions. It's as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool than a speedy lunch.

The World's Most Expensive Big Mac

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/Worlds-most-expensive-big-mac-story-2-image-2-e1523918262313.jpg225300MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-04-17 01:06:412018-04-17 01:06:41Where The Economist "Big Mac" Index Finds Currency Value

Don?t waste your time trying to analyze financial markets right now.

There is only one ticker symbol you need to know about, that for the Shanghai Stock Exchange Composite Index, the ($SSEC).

When Shanghai goes up, the rest of the world?s risk assets happily join the party. When it drops, ?RISK OFF? fever goes pandemic.

China upped the ante this week when it allowed its currency, the Yuan, or the renminbi as it is known locally (the people?s currency), to float freely for the first time in 25 years. That produced a two-day devaluation of 3.6%.

In the very long history of currency debasements, this one was barely a whimper.

Ancient Sumerians used to shave the edges off of gold and silver coins 5,000 years ago.

When President Nixon took the US off of the gold standard in 1973, the dollar eventually fell 75% against the European currencies.

More recently, the Euro has given up 37% against the greenback, moving from a position of grotesque over valuation to dealing with the Greek credit crisis.

So Beijing?s move this week barely tips the needle in the official history of devaluations.

What it does do is create a giant psychological effect, and therein lies the problem.

Since June, the Mandarins in China have been pulling out all the stops to halt a free fall in the country?s share prices.

It has cut interest rates and relaxed reserve requirements. It banned high frequency trading, blaming the collapse on foreign short sellers (sound familiar?). It has even made stock selling illegal in roughly 94% of the country?s free float.

Still, the bears remain emboldened by their recent success.

By cutting the value of the Yuan, the government is providing a modest boost to the economy. A cheaper currency means less expensive exports and more of them, thus, making local businesses more profitable and creating jobs.

But not by much.

There are not a lot of products that live or die on a 3.6% margin. America has not just lost a chunk of its own exports from the additional competition, contrary to the claims of the TV networks and bogus newsletters with which I compete.

But by taking the first such move to undercut the Yuan in 25 years, it is showing the world how serious a problem is the stock crash.

Will the stock collapse feed into the main economy? Is 10% of the world?s GDP going into a Great Recession? Yikes!

SELL, SELL!

There are a few other problems with the Chinese firecracker.

It violates a secret agreement with the US government, made a decade ago, to allow a steady 3-4% a year appreciation of the Yuan against the dollar.

This was designed to slowly eliminate the artificial under valuation of the Yuan that gave the Middle Kingdom an unfair export advantage. The arrangement was responsible for the 20% rise of the Yuan since 2009.

(Sorry Donald, but you?re holding the chart upside down. Yes, I know, stock charts can be pesky things).

Reneging on the deal is ruffling feathers at the US Treasury in Washington. But it won?t amount to more than that, as long as it is temporary.

Which it will be.

China still has a massive trade surplus with the United States. In 2014, it totaled a staggering $343 billion. It maintained that heady pace, totaling $171 billion during the first half of 2015.

There are an awful lot of Chinese clothes, electronics, and toys sitting on the shelves of American retailers.

Its imports are falling, thanks to the collapse of the price of oil and other bulk commodities.

The natural state of the currency of any country running such huge surpluses is for it to rise in value. That will continue in China?s case for the foreseeable future.

Once the waters settle in the stock market, you can count on the Yuan to regain its upward path.

However, this isn?t going to happen in a day. It could be weeks or months until order returns to Chinese equity markets. Until then, expect some scary days there and here as well.

Compound these problems with the uncertainty over the Federal Reserve?s decision on interest rates in September and slower than expected US growth.

It certainly leaves traders and investors alike, with a full plate of issues to consider.

As if we didn?t have enough to worry about.

For some background on my 45 year coverage of the Middle Kingdom, please click here for my 2011 SPECIAL CHINA ISSUE.

Surprise!

https://www.madhedgefundtrader.com/wp-content/uploads/2015/08/China-Firecracker-e1439470828256.jpg272400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-08-13 01:05:262015-08-13 01:05:26China?s Firecracker Surprise

One of the oldest games in the foreign exchange market is to always buy the currencies of strong countries that are growing and to sell short the currencies of the weak countries that are shrinking.

Any doubts that China?s Yuan is a huge screaming buy should have been dispelled when news came out that exports have once again started to surge, thanks to the recovery of its largest customer, Europe.

China?s surging exports of electrical machinery, power generation equipment, clothes and steel were a major contributor.

Interest rate rises for the Yuan and a constant snugging of bank reserve requirements by the People?s Bank of China, have stiffened the backbone of the Middle Kingdom?s currency even further.

That is the price of allowing the Federal Reserve to set China?s monetary policy via a semi fixed Yuan exchange rate.

The last really big currency realignment was a series of devaluations that took the Yuan down from a high of 1.50 to the dollar in 1980. By the mid-nineties, it had depreciated by 84%. The goal was to make exports more competitive. The Chinese succeeded beyond their wildest dreams.

There is absolutely no way that the fixed rate regime can continue and there are only two possible outcomes. An artificially low Yuan has to eventually cause the country?s inflation rate to explode. Or a future global economic recovery causes Chinese exports to balloon to politically intolerable levels. Either case forces a revaluation.

Of course timing is everything. It?s tough to know how many sticks it takes to break a camel?s back. Talk to senior officials at the People?s Bank of China and they?ll tell you they still need a weak currency to develop their impoverished economy. Per capita income is still at only $6,000, less than a tenth of that of the US. But that is up a lot from a mere $100 in 1978.

Talk to senior US Treasury officials and they?ll tell you they are amazed that the Chinese peg has lasted this long. How many exports will it take to break it? $1.5 trillion, $2 trillion, $2.5 trillion? It?s anyone?s guess.

One thing is certain. A free floating Yuan would be at least 50% higher than it is today, and possibly 100%. In fact, the desire to prevent foreign hedge funds from making a killing in the market is not a small element in Beijing?s thinking.

The Chinese government says it won?t entertain a revaluation for the foreseeable future. The Americans say they need it tomorrow. To me that means it?s coming.

Buy the Yuan ETF, the (CYB). Just think of it as an ETF with an attached lottery ticket. If the Chinese continue to stonewall, you will get the token 3%-4% annual revaluation they are thought to tolerate. Double that with margin, and your yield rises to 6%-10%, not bad in this low yielding world. Since the chance of the Chinese devaluing is nil, that beats the hell out of the zero interest rates you now get with T-bills.

If they cave, then you could be in for a home run.

Ready for a Long Term Relationship with China?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/09/Girl-Chinese.jpg376284Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-07-09 01:03:512015-07-09 01:03:51Play China?s Yuan from the Long Side

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.