Global Market Comments

January 16, 2019

Fiat Lux

Featured Trade:

(WHAT THE HECK IS ESG INVESTING?),

(TSLA), (MO)

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

Global Market Comments

January 16, 2019

Fiat Lux

Featured Trade:

(WHAT THE HECK IS ESG INVESTING?),

(TSLA), (MO)

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

I am always watching for market-topping indicators and I have found a whopper. The number of new IPOs from technology mega unicorns is about to explode. And not by a little bit but a large multiple, possibly tenfold.

Some 220 San Francisco Bay Area private tech companies valued by investors at more than $700 billion are likely to thunder into the public market next year, raising buckets of cash for themselves and minting new wealth for their investors, executives, and employees on a once-unimaginable scale.

Will it kill the goose that laid the golden egg?

Newly minted hoody-wearing millionaires are about to stampede through my neighborhood once again, buying up everything in sight.

That will make 2020 the biggest year for tech debuts since Facebook’s gargantuan $104 billion initial public offering in 2012. The difference this time: It’s not just one company but hundreds that are based in San Francisco, which could see a concentrated injection of wealth as the nouveaux riches buy homes, cars and other big-ticket items.

If this is not ringing a bell with you, remember back to 2000. This is exactly the sort of new issuance tidal wave that popped the notorious Dotcom Bubble.

And here is the big problem for you. If too much money gets sucked up into the new issue market, there is nothing left for the secondary market, and the major indexes can fall by a lot. Granted, probably only $100 billion worth of stock will be actually sold, but that is still a big nut to cover.

The onslaught of IPOs includes home-sharing company Airbnb at $31 billion, data analytics firm Palantir at $20 billion, and FinTech company Stripe at $20 billion.

The fear of an imminent recession starting sometime in 2020 or 2021 is the principal factor causing the unicorn stampede. Once the economy slows and the markets fall, the new issue market slams shut, sometimes for years as they did after 2000. That starves rapidly growing companies of capital and can drive them under.

For many of these companies, it is now or never. They have to go public and raise new money or go under. The initial venture capital firms that have had their money tied up here for a decade or more want to cash out now and roll the proceeds into the “next big thing,” such as blockchain, healthcare, or artificial intelligence. The founders may also want to raise some pocket money to buy that mansion or mega yacht.

Or, perhaps they just want to start another company after a well-earned rest. Serial entrepreneurs like Tesla’s Elon Musk (TSLA) and Netflix’s Reed Hastings (NFLX) are already on their second, third, or fourth startups.

And while a sudden increase in new issues is often terrible for the market, getting multiple IPOs from within the same industry, as is the case with ride-sharing Uber and Lyft, is even worse. Remember the five pet companies that went public in 1999? None survived.

Some 80% of all IPOs lost money last year. This was definitely NOT the year to be a golfing partner or fraternity brother with a broker.

What is so unusual in this cycle is that so many firms have left going public to the last possible minute. The desire has been to milk the firms for all they are worth during their high growth phase and then unload them just as they go ex-growth.

Also holding back some firms from launching IPOs is the fear that public markets will assign a lower valuation than the last private valuation. That’s an unwelcome circumstance that can trigger protective clauses that reward early investors and punish employees and founders. That happened to Square (SQ) in its 2015 IPO.

That’s happening less and less frequently: In 2019, one-third of IPOs cut companies’ valuations as they went from private to public. In 2019, that ratio has dropped to one in six.

Also unusual this time around is an effort to bring in more of the “little people” in the IPO. Gig economy companies like Uber and Lyft have lobbied the SEC for changes in new issue rules that enabled their drivers to participate even though they may be financially unqualified. They were all hit with losses of a third once the companies went public.

As a result, when the end comes, this could come as the cruelest bubble top of all.

Global Market Comments

March 6, 2018

Fiat Lux

Featured Trade:

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

(A NOTE ON OPTIONS CALLED AWAY), (TLT)

Global Market Comments

October 23, 2018

Fiat Lux

Featured Trade:

(WATCH OUT FOR THE UNICORN STAMPEDE IN 2019),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

(A NOTE ON OPTIONS CALLED AWAY), (MSFT)

I am always watching for market topping indicators and I have found a whopper. The number of new IPOs from technology mega unicorns is about to explode. And not by a little bit but a large multiple, possibly tenfold.

Six San Francisco Bay Area private tech companies valued by investors at more than $10 billion each are likely to thunder into the public market next year, raising buckets of cash for themselves and minting new wealth for their investors, executives, and employees on a once-unimaginable scale.

Will it kill the goose that laid the golden egg?

Newly minted hoody-wearing millionaires are about to stampede through my neighborhood once again, buying up everything in sight.

That will make 2019 the biggest year for tech debuts since Facebook’s gargantuan $104 billion initial public offering in 2012. The difference this time: It’s not just one company, and five of them are based in San Francisco, which could see a concentrated injection of wealth as the nouveaux riches buy homes, cars and other big-ticket items.

If this is not ringing a bell with you, remember back to 2000. This is exactly the sort of new issuance tidal wave that popped the notorious Dotcom Bubble.

And here is the big problem for you. If too much money gets sucked up into the new issue market, there is nothing left for the secondary market, and the major indexes can fall, buy a lot.

The onslaught of IPOs includes ride-sharing firm Uber at $120 billion, home-sharing company Airbnb at $31 billion, data analytics firm Palantir at $20 billion, FinTech company Stripe at $20 billion, another ride-sharing firm Lyft at $15 billion, and social networking firm Pinterest at $12 billion.

Just these six names alone look to absorb an eye-popping $218 billion, and that does not include hundreds of other smaller firms waiting on the sidelines looking to tap the public market soon.

The fear of an imminent recession starting sometime in 2019 or 2020 is the principal factor causing the unicorn stampede. Once the economy slows and the markets fall, the new issue market slams shut, sometimes for years as they did after 2000. That starves rapidly growing companies of capital and can drive them under.

For many of these companies, it is now or never. The initial venture capital firms that have had their money tied up here for a decade or more want to cash out now and roll the proceeds into the “next big thing,” such as blockchain, health care, or artificial in intelligence. The founders may also want to raise some pocket money to buy that mansion or mega yacht.

Or, perhaps they just want to start another company after a well-earned rest. Serial entrepreneurs like Tesla’s Elon Musk (TSLA) and Netflix’s Reed Hastings (NFLX) are already on their second, third, or fourth startups.

And while a sudden increase in new issues is often terrible for the market, getting multiple IPOs from within the same industry, as is the case with ride-sharing Uber and Lyft, is even worse. Remember the five pet companies that went public in 1999? None survived.

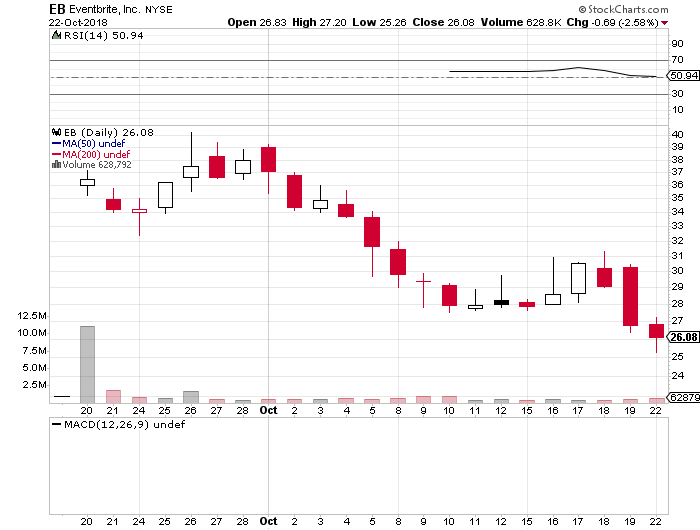

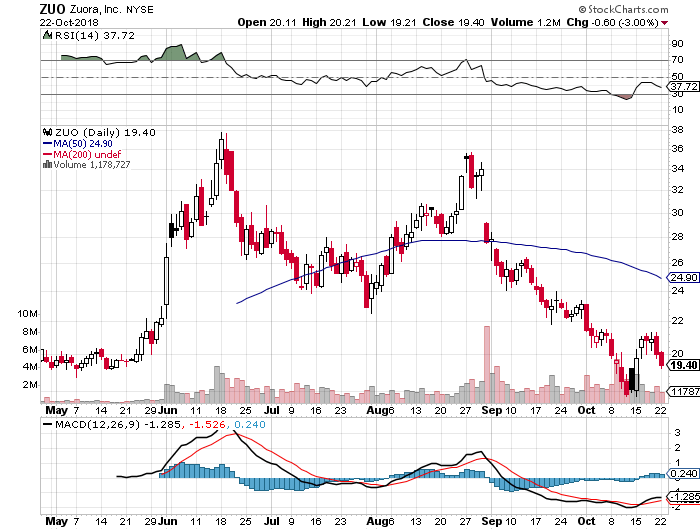

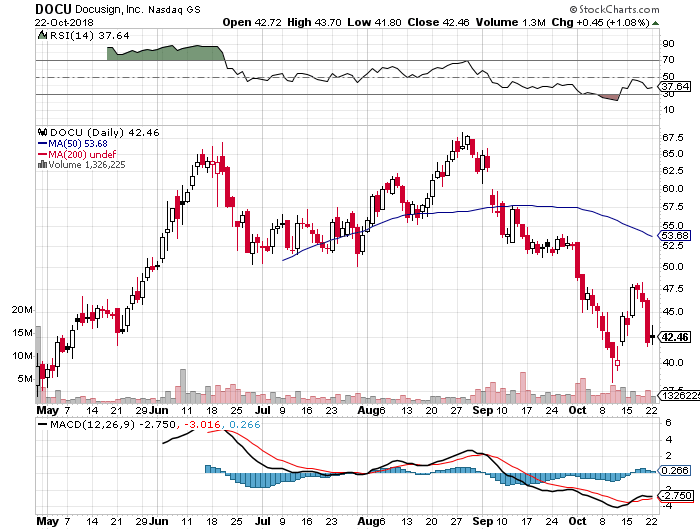

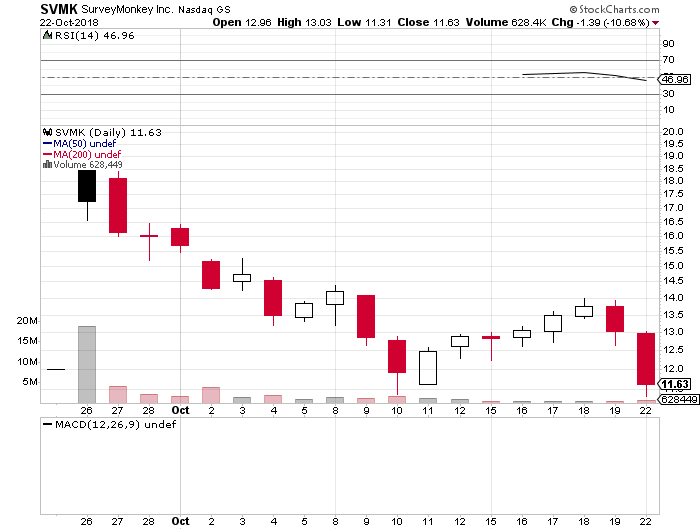

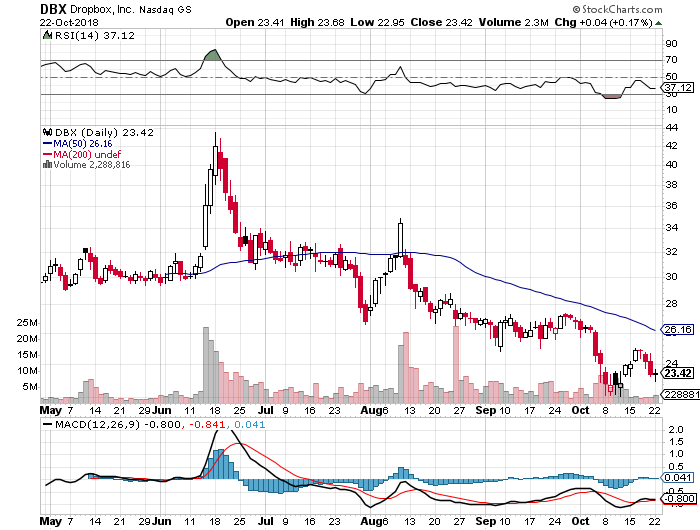

The move comes on the heels of an IPO market in 2018 that was a huge disappointment. While blockbuster issues like Dropbox (DB) and DocuSign (DOCU) initially did well, Eventbrite (EB), SurveyMonkey (SVMK), and Zuora (ZUO) have all been disasters.

Some 80% of all IPOs lost money this year. This was definitely NOT the year to be a golfing partner or fraternity brother with a broker.

What is so unusual in this cycle is that so many firms have left going public to the last possible minute. The desire has been to milk the firms for all they are worth during their high growth phase and then unload them just as they go ex-growth.

The ramp has been obvious for all to see. In the first nine months of 2018, 44 tech IPOs brought in $17 billion, according to Dealogic. That’s more than tech IPOs reaped for all of 2016 and 2017 combined.

Also holding back some firms from launching IPOs is the fear that public markets will assign a lower valuation than the last private valuation. That’s an unwelcome circumstance that can trigger protective clauses that reward early investors and punish employees and founders. That happened to Square (SQ) in its 2015 IPO.

That’s happening less and less frequently: In 2017, one-third of IPOs cut companies’ valuations as they went from private to public. In 2018, that ratio has dropped to one in six.

Also unusual this time around is an effort to bring in more of the “little people” in the IPO. Gig economy companies like Uber and Lyft are lobbying the SEC for changes in new issue rules that will enable their drivers to participate even though they may be financially unqualified.

As a result, when the end comes, this could come as the cruelest bubble top of all.

Global Market Comments

April 4, 2018

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE FRIDAY, APRIL 6, INCLINE VILLAGE, NEVADA, GLOBAL STRATEGY LUNCHEON),

(WHY YOU SHOULD CARE ABOUT THE LIBOR CRISIS), (DB),

(ARE YOU A FINANCIAL ADVISOR LOOKING FOR NEW CLIENTS?)

You know those bond shorts you're carrying on my recommendation? They are about to pay off big time.

We are only one more capitulation sell-off day in the stock market from bonds starting to fall like a rock.

There is a financial crisis taking place overseas, which you probably don't know, or care about.

Here is my one-liner on this: You should care.

The London Interbank Offered Rate (LIBOR) is a measure of the cost of short-term borrowing in Europe. It is essentially their version of our own Fed funds rate. And here's the problem. It has been rising almost every day for two months.

If you read the financial press, you probably already know about LIBOR as the subject of a bid rigging scandal that prompted billion-dollar fines and jail terms for the parties involved.

You can take this as the opening salvo in the coming credit crisis. It probably won't start to seriously bite here in the US for two years. But it is already hurting the profitability of European banks now.

A staggering $350 trillion in loans in the US and abroad are tied to LIBOR-based loans, including $1.2 trillion in mortgages for high-end homeowners. Rising interest rates for this debt bring immediate pain.

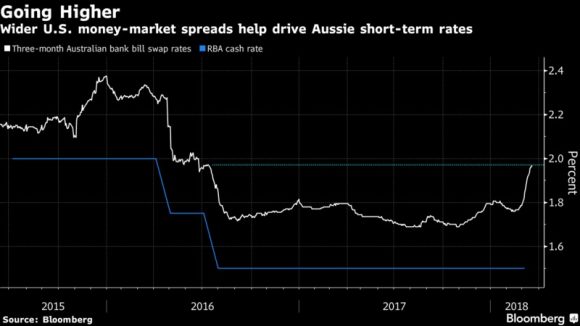

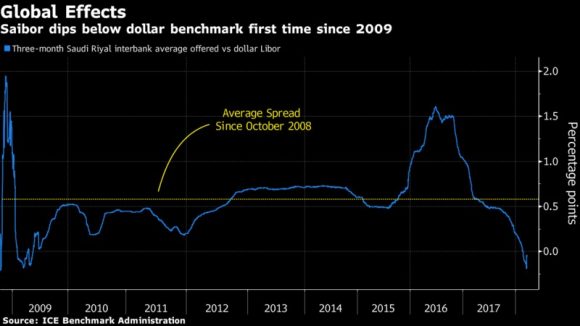

You can see this clearly is the cost of funds around the world, as outlined by the charts below.

Saudi Arabia's cost of funds, or SAIBOR, historically a net supplier of funds to the continent thanks to its perennial oil surplus, has just been raised 60 basis points, the first such move in a decade.

It is causing cash squeeze in Hong Kong, as seen through escalating HIBOR rates. Even Australian banks, normally seen as the bedrock of the global financial system, have seen the sharpest rise in interest rates in eight years.

Of course, the reasons for the global credit squeeze here at home are screamingly obvious. The US government is in the process of tripling its annual borrowing needs, as the budgets deficit soars from $400 billion to $1.2 trillion.

Exacerbating the influence on the markets is the US Treasury's new preference for short-term borrowing instead of the long-term kind, thus boosting the cost of shorter-term money.

This is to reduce the immediate up-front cost of borrowing. Like so many administration policies, it is reaping a short-term paper advantage for a very much higher long-term real cost.

As we are just entering a 20-year bear market for bonds, the Feds should be borrowing as much long-term money as they possibly can.

This is what private corporations are doing, such as Apple (AAPL) and Goldman Sachs (GS), issuing 30- to 100-year bonds, even though they don't need the money.

The tax bill passed at the end of 2017 also has had the unintended side effect of raising European rates. US companies now are mobilizing some $2.5 trillion to bring home at minimal tax rates.

That has brought them to unload longer term investments and shift the funds into overnight commercial paper, further boosting rates.

You normally don't see this kind of divergence in domestic and foreign costs of money without some kind of credit crisis.

Nervous eyes are cast toward Germany's Deutsche Bank (DB), holder of the world's largest derivatives book, and whose share price has plunged a stunning 30% in two months. Clearly, the insider money is getting out. Expect to hear a lot more about Deutsche Bank in the coming months.

I have said all along that the true cost of the tax bill won't be in the immediate up-front price tag, but the long-range unintended consequences.

You don't turn America's $20.5 trillion economy on a dime without creating a lot of disruption. And now they want to pass a second tax bill!

Spiking Rates are Becoming a Real Headache