Mad Hedge Technology Letter

April 25, 2018

Fiat Lux

Featured Trade:

(FANGS DELIVER ON EARNINGS, BUT FAIL ON PRICE ACTION),

(GOOGL), (AMZN), (MSFT), (AAPL), (FB),

(DBX), (NFLX), (BOX), (WDC)

Mad Hedge Technology Letter

April 25, 2018

Fiat Lux

Featured Trade:

(FANGS DELIVER ON EARNINGS, BUT FAIL ON PRICE ACTION),

(GOOGL), (AMZN), (MSFT), (AAPL), (FB),

(DBX), (NFLX), (BOX), (WDC)

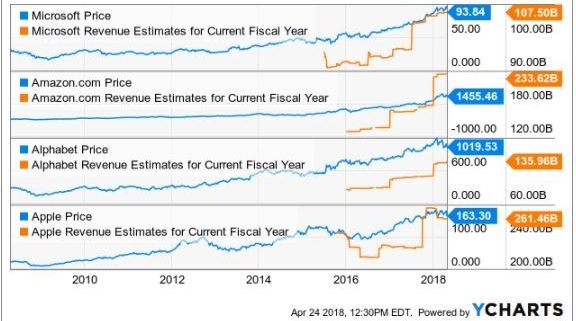

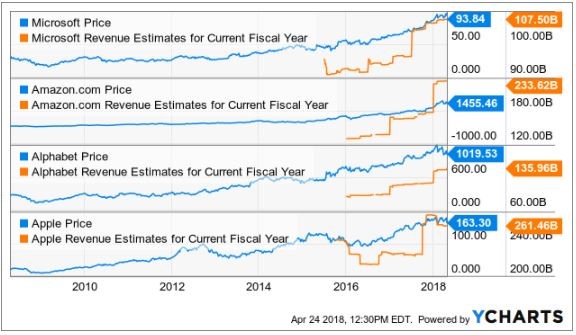

Alphabet (GOOGL) did a great job alleviating fears that large-cap tech would be dragged through the mud and fading earnings would dishearten investors.

The major takeaways from the recent deluge of tech earnings are large-cap tech is getting better at what they do best, and the biggest are getting decisively bigger.

Of the 26% rise to $31.1 billion in Alphabet's quarterly revenue, more than $26 billion was concentrated around its mammoth digital ad revenue business.

Alphabet, even though rebranded to express a diverse portfolio of assets, is still very much reliant on its ad revenue to carry the load made possible by Google search.

Its "other bets" category failed to impact the bottom line with loss-making speculative projects such as Nest Labs in charge of mounting a battle against Amazon's (AMZN) Alexa.

The quandary in this battle is the margins Alphabet will surrender to seize a portion of the future smart home market.

What we are seeing is a case of strength fueling further strength.

Alphabet did a lot to smooth over fears that government regulation would put a dent in its business model, asserting that it has been preparing for the new EU privacy rules for "18 months" and its search ad business will not be materially affected by these new standards.

CFO Ruth Porat emphasized the shift to mobile, as mobile growth is leading the charge due to Internet users' migration to mobile platforms.

Google search remains an unrivaled product that transcends culture, language, and society at optimal levels.

Sure, there are other online search engines out there, but the accuracy of results pale in comparison to the preeminent first-class operation at Google search.

Alphabet does not divulge revenue details about its cloud unit. However, the cloud unit is dropped into the "other revenues" category, which also includes hardware sales and posted close to $4.4 billion, up 36% YOY.

Although the cloud segment will never dwarf its premier digital ad segment, if Alphabet can ameliorate its cloud engine into a $10 billion per quarter segment, investors would dance in the streets with delight.

Another problem with the FANGs is that they are one-trick ponies. And if those ponies ever got locked up in the barn, it would spell imminent disaster.

Apple (AAPL) is trying its best to diversify away from the iconic product with which consumers identify.

The iPhone company is ramping up its services and subscription business to combat waning iPhone demand.

Alphabet is charging hard into the autonomous ride-sharing business seizing a leadership position.

Netflix (NFLX) is doubling down on what it already does great - create top-level original content.

This was after it shed its DVD business in the early stages after CEO Reed Hastings identified its imminent implosion.

Tech companies habitually display flexibility and nimbleness of which big corporations dream.

One of the few negatives in an otherwise solid earnings report was the TAC (traffic acquisition costs) reported at $6.28 billion, which make up 24% of total revenue.

An escalation of TAC as a percentage of revenue is certainly a risk factor for the digital ad business. But nibbling away at margins is not the end of the world, and the digital ad business will remain highly profitable moving forward.

TAC comprised 22% of revenue in Q1 2017, and the rise in costs reflects that mobile ads are priced at a premium.

Google noted that TAC will experience further pricing pressure because of the great leap toward mobile devices, but the pace of price increases will recede.

The increased cost of luring new eyeballs will not diminish FANGs' earnings report buttressed by secular trends that pervade Silicon Valley's platforms.

The year of the cloud has positive implications for Alphabet. It ranks No. 3 in the cloud industry behind Microsoft (MSFT) and Amazon.

Amazon and Microsoft announce earnings later this week. The robust cloud segments should easily reaffirm the bullish sentiment in tech stocks.

Amazon's earnings call could provide clarity on the bizarre backbiting emanating from the White House, even though Jeff Bezos rarely frequents the earnings call.

A thinly veiled or bold response would comfort investors because rumors of tech peaking would add immediate downside pressure to equities.

The wider-reaching short-term problem is the macro headwinds that could knock over tech's position on top of the equity pedestal and bring it back down to reality in a war of diplomatic rhetoric and international tariffs.

Google, Facebook, and Netflix are the least affected FANGs because they have been locked out of the Chinese market for years.

The Amazon Web Services (AWS) cloud arm of Amazon blew past cloud revenue estimates of 42% last quarter by registering a 45% jump in revenue.

Microsoft reiterated that immense cloud growth permeating through the industry, expanding 99% QOQ.

I expect repeat performances from the best cloud plays in the industry.

Any cloud firm growing under 20% is not even worth a look since the bull case for cloud revenue revolves around a minimum of 20% growth QOQ.

Amazon still boasts around 30% market share in the cloud space with Microsoft staking 15% but gaining each quarter.

AWS growth has been stunted for the past nine quarters as competition and cybersecurity costs related to patches erode margins.

Above all else, the one company that investors can pinpoint with margin problems is Amazon, which abandoned margin strength for market share years ago and that investors approved in droves.

AWS is the key driver of profits that allows Amazon to fund its e-commerce business.

Cloud adoption is still in the early stages.

Microsoft Azure and Google have a chance to catch up to AWS. There will be ample opportunity for these players to leverage existing infrastructure and expertise to rival AWS's strength.

As the recent IPO performance suggests, there is nothing hotter than this narrow sliver of tech, and this is all happening with numerous companies losing vast amounts of money such as Dropbox (DBX) and Box (BOX).

Microsoft has been inching toward gross profits of $8 billion per quarter and has been profitable for years.

And now it has a hyper-expanding cloud division to boot.

Any macro sell-off that pulls down Microsoft to around the $90 level or if Alphabet dips below $1,000, these would be great entry points into the core pillars of the equity market.

If tech goes, so will everything else.

If it plays its cards right, Microsoft Azure has the tools in place to overtake AWS.

Shorting cloud companies is a difficult proposition because the leg ups are legendary.

If traders are looking for any tech shorts to pile into, then focus on the legacy companies that lack a cloud growth driver.

Another cue would be a company that has not completed the resuscitation process yet, such as Western Digital (WDC) whose shares have traded sideways for the past year.

But for now, as the 10-year interest rate shoots past 3%, investors should bide their time as cheaper entry points will shortly appear.

_________________________________________________________________________________________________

Quote of the Day

"Technology is a word that describes something that doesn't work yet." - said British author Douglas Adams.

Mad Hedge Technology Letter

April 17, 2018

Fiat Lux

Featured Trade:

(WHY THE CLOUD IS WHERE TRADING DREAMS COME TRUE),

(ZS), (ZUO), (SPOT), (DBX), (AMZN), (CSCO), (CRM)

Dreams don't often come true - but they do frequently these days.

Highly disruptive transformative companies on the verge of redefining the status quo give investors a golden chance to get in before the stock goes parabolic.

Traditional business models are all ripe for reinvention.

The first phase of reformulation in big data was inventing the cloud as a business.

Amazon (AMZN) and its Amazon Web Services (AWS) division pioneered this foundational model, and its share price is the obvious ballistic winner.

The second phase of cloud ingenuity is trickling in as we speak in the form of companies that focus on functionality, performance, and maintenance on the cloud platform.

This is a big break away from the pure accumulation side of stashing raw data in servers.

However, derivations of this type of application are limitless.

Swiftly identifying these applied cloud companies is crucial for investors to stay ahead of the game and participate in the next gap up of tech growth.

The markets' reaction to Spotify's (SPOT) and Dropbox's (DBX) hugely successful IPOs was head-turning.

Both companies finished the first day of trading firmly well above their respective, original opening prices -- or for Spotify, the opening reference price.

The pent-up momentum for anything "Cloud" has its merits, and these two shining stars will give other ambitious cloud firms the impetus to go public.

If Spotify and Dropbox laid an egg, momentum would have screeched to a juddering halt, and companies such as Pivotal Software would reanalyze the idea of soon going public.

Now it's a no-brainer proposition.

There are more than 40 more public cloud companies that are valued at more than a $1 billion, and more are in the pipeline.

To understand the full magnitude of the situation, evaluating recent IPO performance is a useful barometer of health in the tech industry.

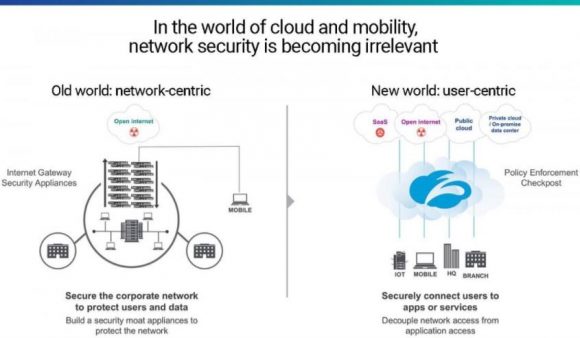

The first company Zscaler (ZS) is an enterprise company focused on cloud security that closed 106% above its opening price when it went public this past March 16.

It opened up at $16 a share and finished the day at $33.

Zscaler CEO, Jay Chaudhry, audaciously rebuffed two offers leading up to the March 16 IPO. Both offers were more than $2 billion, and both were looking to acquire Zscaler at a discount.

The decision to forego these offers was a prudent move considering (ZS)s current market cap is around $3.3 billion and rising.

One of the companies vying for (ZS) was Cisco Systems (CSCO), which is also in the cloud security business. Cisco is looking to add another appendage to its offerings with the cash hoard it just repatriated from abroad.

Cisco has been willing to dip into its cash hoard by buying San Francisco-based AppDynamics for $3.7 billion in 2017, which specializes in managing the performance of apps across the cloud platform and inside the data center.

Cloud security is critical for outside companies to feel comfortable implementing universal cloud technology.

Storing sensitive data online in a storage server is also a risk and difficult to migrate back once on the cloud.

Without solid security to protect data, data-heavy companies will hesitate to vault up their data in a public place and could remain old-school with external data locations storing all of a firm's secrets.

However, this traditional approach is not sustainable. There is just too much generated data in 2018.

Cybersecurity has expeditiously evolved because hackers have become greatly sophisticated. Plus, they are getting a lot of free PR.

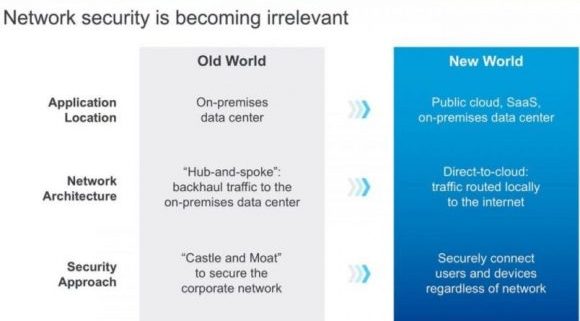

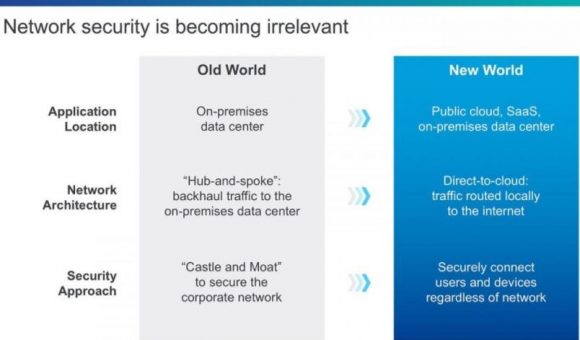

Data center and in-house applications secured operations by managing access and using an industrial strength firewall.

This was the old security model.

Security became ineffective as companies started using cloud platforms, meaning many users accessed applications outside of corporate networks and on various devices.

The archaic "moat" method to security has died a quick death, as organizations have toiled to ziplock end points that offer hackers premium entry points into the system.

Zscaler combats the danger with a new breed of security. The platform works to control network traffic without crashing or stalling applications.

As cloud migration accelerates, the demand for cloud security will be robust.

Another point of cloud monetization falls within payments.

Tech billing has evolved past the linear models that credit and debit in simplistic fashion.

SaaS (Software as a Service), the hot payment model, has gone ballistic in every segment of the cloud and even has been adopted by legacy companies for legacy products.

Instead of billing once for full ownership, companies offer an annual subscription fee to annually lease the product.

However, reoccurring payments blew up the analog accounting models that couldn't adjust and cannot record this type of revenue stream 10 to 20 years out.

Zuora (ZUO) CEO Tien Tzuo understood the obstacles years ago when he worked for Marc Benioff, CEO of Salesforce (CRM), during the early stages in the 90s.

Cherry-picked after graduating from Stanford's MBA program, he made a great impression at Salesforce and parlayed it into CMO (Chief Marketing Officer) where he built the product management and marketing organization from scratch.

More importantly, Tzuo built Salesforce's original billing system and pioneered the underlying system for SaaS.

It was in his nine years at Salesforce that Tzuo diagnosed what Salesforce and the general industry were lacking in the billing system.

His response was creating a company to seal up these technical deficits.

Other second derivative cloud plays are popping up, focusing on just one smidgeon of the business such as analytics or Red Hat's container management cloud service.

SaaS payment model has become the standard, and legacy accounting programs are too far behind to capture the benefits.

Zuora allows tech companies to seamlessly integrate and automate SaaS billing into their businesses.

Tzuo's last official job at Salesforce was Chief Strategy Officer before handing in his two-week notice. Benioff, his former boss, was impressed by Tzuo's vision, and is one of the seed investors for Zuora.

These smaller niche cloud plays are mouthwateringly attractive to the bigger firms that desire additional optionality and functionality such as MuleSoft, integration software connecting applications, data and devices.

MuleSoft was bought by Salesforce for $6.5 billion to fill a gap in the business. Cloud security is another area in which it is looking to acquire more talent and products.

If you believe SaaS is a payment model here to stay, which it is, then Zuora is a must-buy stock, even after the 42% melt up on the first day of trading.

The stock opened at $14 and finished at $20.

One of the next cloud IPOs of 2018 is DocuSign, a company that provides electronic signature technology on the cloud and is used by 90% of Fortune 500 companies.

The company was worth more than $3 billion in a round of 2015 funding and is worth substantially more today.

These smaller cloud plays valued around $2 billion to $3 billion are a great entry point into the cloud story because of the growth trajectory. They will be worth double or triple their valuation in years to come.

It's a safe bet that Microsoft and Amazon will continue to push the envelope as the No. 1 and No. 2 leaders of the industry. However, these big cloud platforms always are improving by diverting large sums of money for reinvestment.

The easiest way to improve is by buying companies such as Zuora and Zscaler.

In short, cloud companies are in demand although there is a shortage of quality cloud companies.

__________________________________________________________________________________________________

Quote of the Day

"The great thing about fact-based decisions is that they overrule the hierarchy." - said Amazon founder and CEO, Jeff Bezos

Mad Hedge Technology Letter

April 4, 2018

Fiat Lux

Featured Trade:

(SPOTIFY KILLS IT ON LISTING DAY),

(SPOT), (DBX), (GOOGL), (AAPL), (AMZN), (CRM), (NFLX), (FB)

The banner year for the cloud continues as Dropbox's (DBX) blowout IPO passed with flying colors.

Investors' voracity for anything connecting to big data continues unabated.

Big data shares are now fetching a big premium, and recent negative news has highlighted how important big data is to every business.

Let's face it, Spotify (SPOT) needs capital to reinvest into its platform to achieve the type of scale that deems margins healthy enough to profit, even though it says it doesn't.

Big data architecture takes time to cultivate, but more importantly it costs a huge chunk of money to construct a platform worthy enough to satisfy consumers.

The daunting proposition of competing with the FANGs for users only makes sense if there is a reservoir of funds to accompany the fight.

Spotify CEO Daniel Ek has milked the private market for funding, making himself a multibillionaire in the process. And as another avenue of capital raising, he might as well go to the public to fund the venture in the future.

Cloud and big data companies have identified the insatiable investor appetite for their services. Crystalizing this sentiment is Salesforce's (CRM) recent purchase of MuleSoft - integration software that connects apps, data, and devices - for 18% more than its original offer for $6.5 billion.

The price was so exorbitant, analysts speculated that a price war broke out, but Salesforce paid such a high price because it is convinced that MuleSoft will triple in size by 2021. That is another great trading opportunity missed by you and me.

An 18% premium to the original price will seem like peanuts in five years. The year 2018 is unequivocally a sellers' market from the chips up to the end product and everything in between on the supply chain.

Spotify cannot make money if it's not scaled to 150 million users, compared to its current 76 million. And 200 million and 300 million would give CEO Daniel Ek peace of mind, but it's a hard slog.

Pouring gas on the fire, Spotify is going public at the worst possible time as tech stocks have been the recipient of a regulatory witch hunt pounding the NASDAQ, sending it firmly into correction territory.

Next up was Spotify's day to shine in the sun directly listing its stock.

Existing investors and Spotify employees are free to unload shares all they want, or load up on the first day. In addition, no new shares are being issued. This is unprecedented in the history of new NYSE listings.

Spotify is betting on its brand recognition and massive desire for big data accumulation. It worked big time, with a first day's closing price of $149, verses initial low ball estimates of $49.

Cloud companies are the cream of the big data crop, but Spotify's data hoard will contain every miniscule music preference and detail a human can possibly exhibit for potentially 100 million-plus people.

Spotify's data will become the most valuable music data in the world and for that it is worth paying.

But at what price?

Spotify has no investment bankers, and circumnavigating the hair-raising fees a bank would earn is a bold statement for the entire tech industry.

Sidestepping the traditional process has ruffled some feathers in the financial industry.

The mere fact that Spotify has the gall to execute a direct listing is just the precursor to big banks being phased out of the profitable investment banking sector.

Goldman Sachs (GS) was the lead advisor on Dropbox's (DBX) traditional IPO, and it was a resounding success rocketing 40% a few days after going public.

IPOs are not cheap.

The numbers are a tad misleading because Spotify paid about $40 million in advisory to the big investment banks leading up to the big day.

This is about a $28 million less than when Snapchat (SNAP) went public last year.

Uber and Lyft almost certainly would consider this option if Spotify nails its IPO day.

Banks are being squeezed from all sides as nimble, unregulated tech firms have proved better adaptable in this quickly changing environment.

Spotify's business model is based on spectacular future growth, which may occur.

It is a loss-making company that produces no proprietary solutions but is overlooked for its valuable data.

The company is the market leader in paid subscribers at 76 million, far outpacing Apple Music at 39 million and Pandora at 5.5 million.

Total MAUs (Monthly Active Users) expect to reach more than 200 million users, and paid subscribers could hit the 96 million mark by the end of 2018.

Spotify's business model bets on transforming the free subscribers who use Spotify with ad-supported interfaces into paid subscribers that are ad-free. Converting a small amount would be highly positive.

Gross margin is a number that sheds light on the real efficiencies of the company, and Spotify hopes to hit the 25% gross margin point by the end of 2018.

I am highly skeptical that gross margins can rise that high unless they solve the music royalty problem.

Royalty costs are killer, forcing Spotify to shell out a massive $9.75 billion in music royalties since its inception in 2006.

Spotify is paying too much for its content, but that is the cruel nature of the music industry.

The ideal solution would eventually amount to producing high quality original entertainment content on its proprietary platform akin to Netflix's (NFLX) business model with video content.

Spotify's capital is being drained by royalty fees amounting to 79% of its revenue.

This needs to be stopped. It's a losing strategy.

Considering Google (GOOGL) and Facebook (FB) do not pay for their own content, it frees up capital to pile into the pure technical side of the operations, enhancing their ad platforms luring in new users.

This is why the Mad Hedge Technology Letter sent you an urgent Trade Alert to buy Google yesterday when it was trading at $1,000.

All told, Spotify has managed to lose $2.9 billion since it was created 12 years ago - enough capital to create a new FANG in its own right.

Dropbox was an outstanding success and attaching itself to the parabolic cloud industry is ingenious.

However, potential insane volatility should temper investors' expectations for the first day of trading.

The lack of a road show, no lockup period, and no underwriting or book building will sacrifice stability in the short term.

There is incontestably a place for Spotify, and the expected 30% to 36% growth in 2018 looks attractive.

But then again, I would rather jump into sturdier names such as Lam Research (LRCX), Nvidia (NVDA), and Amazon (AMZN) once markets quiet down.

The private deals that took place before the IPO changed hands were in the range of $99 to $150. Considering the reference point will be set at $132, nabbing Spotify under $100 would be a great deal.

The market will determine the opening price by analyzing the buy and sell orders for the day with the help of Citadel Securities.

It's a risky proposition that 91% of shares are tradable upon the open. Theoretically, all these shares could be sold immediately after the open.

Legging into limit orders below $140 is the only prudent strategy for this gutsy IPO, but better to sit and observe.

__________________________________________________________________________________________________

Quote of the Day

"One of the only ways to get out of a tight box is to invent your way out." - Amazon CEO Jeff Bezos

Mad Hedge Technology Letter

April 2, 2018

Fiat Lux

Featured Trade:

(WHY THERE WILL NEVER BE AN ANTITRUST CASE AGAINST AMAZON)

(AMZN), (WMT), (MSFT), (FB), (DBX), (NFLX)

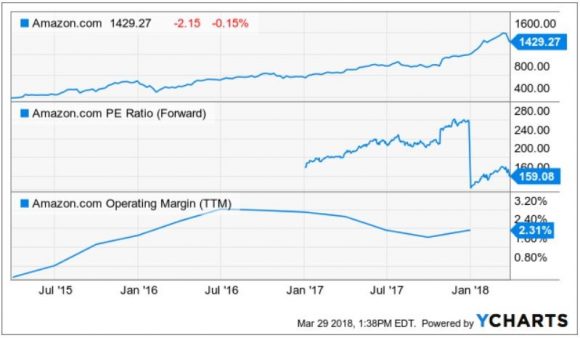

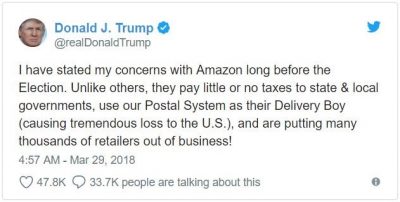

POTUS's Amazon tweet of March 29 has given investors the best entry point into Amazon (AMZN) since the January 2016 sell-off. Since then, the stock has essentially gone up every day.

Entry points have been few and far between as every small pullback has been followed by aggressive buying by big institutional money.

The 200-point nosedive was a function of the White House's dissatisfaction of leaked stories that would find their way into the Washington Post owned by Amazon CEO Jeff Bezos, my former colleague and good friend.

Although there are concerns about Amazon's business model, notably its lack of actual profits, there is no impending regulatory action. And, if there is one company that's in hotter water now, it's Facebook (FB), which inadvertently sells every little detail about your personal life to third-party Eastern European hackers.

Amazon's e-commerce business does not violate the Federal Trade Commission Act of 1914 of "deceptive" or "unfair practices."

The American economy has rapidly evolved thanks to hyper-accelerating technology, and the jobs required to support the modern economy have changed beyond all recognition.

The Clayton Antitrust Act of 1914 addressing harmful mergers that destroy competition hasn't been breached either since Amazon has grown organically.

Analyzing the most comprehensive law, the Sherman Antitrust Act of 1890, which was originally passed to control unions, espouses economic freedom aimed at "preserving free and unfettered competition as the rule of trade."

And, in a way, Amazon could be susceptible, but it would be awfully difficult to persuade the U.S. Department of Justice (DOJ) Antitrust Division and would take a decade.

Amazon's business model will change many times over by the time any antitrust decision can be delivered, or even entertained.

Helping Amazon's case even more is the DOJ interpretation of the three antitrust rules. It is the company's duty to first and foremost protect the consumer and ensure business is operating efficiently, which keeps prices low and quality high. Antitrust laws are, in effect, consumer protection laws.

Amazon's e-commerce segment epitomizes the DOJ's perception of these 100-year-old laws.

The controversial part of Amazon's business model is funneling profits from its Amazon Web Services (AWS) division as a way to offer the lowest prices in America for its e-commerce products.

This strategy has the same effect as dumping since it is selling products for a loss, but it is not officially dumping.

POTUS has usually delivered more bark than bite. The steel and aluminum tariffs went from no exceptions to exceptions galore in less than a week. Policies and employees change in a blink of an eye in the White House.

The backlash is a case of the White House not being a huge admirer of Amazon, but individual government workers probably have Amazon boxes stacked to the heavens on their doorsteps.

It is true that Amazon has negatively affected retail business. It is doing even more damage to traditional shopping malls, which it turns out are owned by close friends of the president. The mom-and-pop stores have disappeared long ago. But Amazon could argue this trend is occurring with or without Amazon.

In addition, Walmart (WMT) was the original retail killer, and it currently is morphing into another Amazon by investing aggressively into its e-commerce division. Does the White House go after (WMT) next?

Unlikely.

Amazon didn't create e-commerce.

Amazon also didn't create the Internet.

Amazon also does pay state and local taxes, some $970 million worth last year.

Technology has been a growth play for years.

Investors and venture capitalists are willing to fork over their hard-earned cash for the chance to own the next Google (GOOGL) or Apple (AAPL).

Many investors do lose money searching for the next unicorn. A good portion of these unicorns lose boatloads of money, too.

Spotify, slated to go public soon, is a huge loss-maker and investors will pay up anyway.

Investors went gaga for Dropbox (DBX), already up 40% from its IPO, and it lost $112 million in 2017.

The risk-appetite is hearty for these burgeoning tech companies if they can scale appropriately.

Should investors be prosecuted for gambling on these cash-losing businesses?

Definitely not. Caveat emptor. Buyer beware.

It is true that Amazon pumps an extraordinary percentage of revenues back into product development and enhancement.

But that is exactly what makes Amazon great. It not only is focused on making money but also on making a terrific product.

The bulk of its enhancement is allocated in warehouse and data center expansion. Splurging on more original entertainment content is another segment warranting heavy investment, too, a la Netflix (NFLX). Did you spot Jeff Bezos at the last Oscar ceremony?

Contrary to popular belief, Amazon is in the black.

It has posted gains for 11 straight quarters and expects a 12th straight profitable quarter for Q1 2018.

The one highly negative aspect is profit margins. It is absolutely slaughtered under the current existing model.

However, investors continually ignore the damage-to-profit margins and have a laser-like focus on the AWS cloud revenue.

Amazon's AWS segment could be a company in itself. Cloud revenue last quarter was $5.11 billion, which handily beat estimates at $4.97 billion.

Amazon's cloud revenue is five times bigger than Dropbox's.

The biggest threat to Amazon is not the administration, but Microsoft (MSFT), which announced amazing cloud revenue numbers up 98% QOQ, and has grown into the second-largest cloud player.

(MSFT) is equipped with its array of mainstay software programs and other hybrid cloud solutions that lure in new enterprise business.

(MSFT) has the chance to break Amazon's stranglehold if it can outmuscle its cloud segment. However, any degradation to Amazon's business model will not kill off AWS, considering Amazon also is heavily investing in its cloud segment, too.

Lost in the tweet frenzy is this behemoth cloud war fighting for storage of data that is somewhat lost in all the political noise.

This is truly the year of the cloud, and dismantling Amazon is only possible by blowing up its AWS segment. The more likely scenario is that AWS and MSFT Azure continue their nonstop growth trajectory for the benefit of shareholders.

Antitrust won't affect Amazon, and after every dip investors should pile into the best two cloud plays - Amazon and Microsoft.

__________________________________________________________________________________________________

Quote of the Day

Mad Hedge Technology Letter

March 29, 2018

Fiat Lux

Featured Trade:

(TECHNOLOGY'S UPSIDE IN THE TRADE WAR)

(RHT), (DBX), (SPOTIFY)

After watching the performance of technology stocks over the past two weeks, you may be on the verge of slitting your wrist, overdosing on drugs, and then jumping off the Golden Gate Bridge.

However, the results reported by tech companies this week say you should be doing otherwise.

As tech companies confront upcoming regulation and an overseas trade war, it has felt like a death by a thousand cuts.

It almost is starting to feel as if being a technology company is akin to drinking from a poisoned chalice.

I beg to differ.

I will tell you why the destiny of tech is quite positive.

The long-term secular growth drivers will prevail of accelerated earnings amid a backdrop of global economic synchronized expansion.

Assiduous capital reallocation programs will attract investors instead of detract from them.

The ironic angle to the precarious diplomatic tumult is that regulation will ultimately benefit the current pacesetters and culprits of technology because the barriers of entry become insurmountable.

The trade war has the same effect as the data regulation because it is ultimately for the betterment and protection of domestic, made-in-USA technology.

Washington knows the FANGs all too well, and the bull market will cease to exist if Beijing buys out our technological expertise.

Short-term pain for long-term gain. That's it in a nutshell.

The White House further understands that it's better to start a trade war now when it holds a stronger hand. No doubt after 20 more years of an ascending China, the Middle Kingdom will leverage its economic clout for diplomatic power dictating the outcome more ruthlessly.

Effectively, Trump's trade fracas is a one step back and two steps forward policy. During the one step back phase simply seems as if the economy is taking a nosedive into the ocean floor.

Love it or hate it, technology is becoming more (and not less) ubiquitous. However, it's gone too far too fast, and society and public officials require time to absorb the new environment or you risk the current backlash.

Simultaneously, America is in the one step back phase of data regulation, trade laws, and society's backlash of encroaching tech.

Bad timing.

The teething problems will gradually subside, the stock market will re-ignite, and tech will advance further into regular life.

The market even has seen some green shoots with the blockbuster Dropbox (DBX) IPO up over 40% intraday on the first day of trading.

In the S-1 filing required for IPOs, (DBX) stated that it may "not be able to achieve or maintain profitability" because of increasing expenses. The disclosure also prefaced its "history of net losses" to justify the business direction.

(DBX) lost $111.7 million in 2017, on revenues of just over $1 billion.

Technology must be doing something right if loss-making firms are treated with a 40% gain on IPO day; and, Spotify, an even bigger money loser, will go public next week.

If investors are smitten with loss-making tech companies, I imagine they feel quite comfortable with the ones earning billions in quarterly profits and growing at a pace where analysts cannot hike their price targets quick enough, making them look foolish.

The outstanding gains by (DBX) was for one reason and one reason only.

It's a pure cloud play, and pure cloud plays have been rewarded in spades.

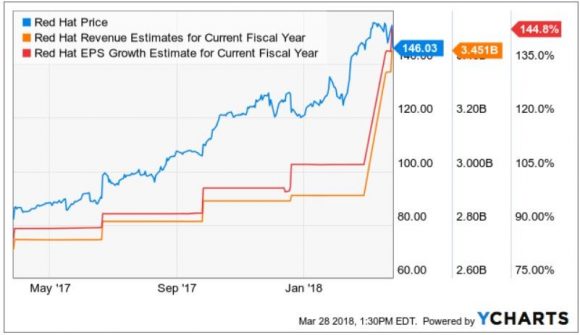

Red Hat's (RHT) stellar earnings were on the heels of the (DBX) IPO success.

Red Hat is a medium-size unadulterated cloud play that lacks the financial resources of the FANGs but is still turning a profit.

It is the poster boy for enterprise cloud companies flourishing in an unrelenting fierce environment.

If the world is going to hell in a handbasket, then how did Red Hat achieve aggregate billings growth of 25%?

Everyone and their uncle expect tech companies to start floundering, but the opposite is true. They overpromise then over deliver to the upside every quarter.

Red Hat booked the most deals over $1 million in Q4 2017 in its history.

Cross-selling cloud applications was especially strong with 81% of deals over $1 million spending on multiple software services.

The critical subscription revenue comprised 88% of Q4 revenue and is up 15% YOY. Application development-related subscriptions were up 42% YOY, higher than the infrastructure-related subscription revenue growing 17% YOY.

Companies are churning out innovation on top of their existing platforms using various software solutions. And every company in the world is migrating toward cloud software and infrastructure. There has never been a better time to be a pure cloud company.

The most poignant telltale sign was that Red Hat renewed 99 out of 100 of its top deals and disclosed that multiyear deals were healthy.

Ansible, its software for automating data center operations, OpenShift, its software for container-based deployment and management, and OpenStack, an infrastructure-as-a-service (IaaS) for cloud computing are the underpinnings to Red Hat's supreme business.

The reoccurring revenue salted away is legion.

The FY 2018 guidance was even more impressive than the quarterly earnings report. Red Hat expects a revenue range between $800 million and $810 million, up from the $748 million last quarter and expects quarterly EPS at $0.81, up from $0.70 last quarter.

Toward the end of the earnings call, Red Hat CEO Jim Whitehurst described the cloud growth environment as "very, very, very fast growth."

Market conditions and heightened volatility could stay irrational for longer than expected but leadership stocks are always the last to fall.

If (DBX) can catch a bid, and headway is made on political issues, then jump back into the cloud names that perform like Red Hat and about which I have been beating the drum.

And don't forget that these regulatory and political hindrances all point toward giving big cap tech cozier conditions and an elevated runway from which to operate.

__________________________________________________________________________________________________

Quote of the Day

"We know where you are. We know where you've been. We can more or less know what you're thinking about." - said Eric Schmidt in 2010, the former executive chairman of Google from 2001-2017